Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the Fiscal Year Ended: January 30, 2010 |

or

| ¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the transition period from to |

Commission File Number: 1-13113

SAKS INCORPORATED

(Exact Name of Registrant as Specified in Its Charter)

| Tennessee | 62-0331040 | |

| (State of Incorporation) | (I.R.S. Employer Identification Number) | |

| 12 East 49th Street New York, New York |

10017 | |

| (Address of Principal Executive Offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (212) 940-5305

Securities Registered Pursuant to Section 12 (b) of the Act:

| Title of each class |

Name of Each Exchange on which registered | |

| Common Shares, par value $0.10 | New York Stock Exchange |

Securities Registered Pursuant to Section 12 (g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark if the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule-405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting stock held by non-affiliates of the registrant as of July 31, 2009 (the last business day of the registrant’s most recently completed second fiscal quarter) was approximately $739,950,295.

As of March 12, 2010, the number of shares of the registrant’s Common Stock outstanding was 160,615,141.

DOCUMENTS INCORPORATED BY REFERENCE

Applicable portions of the Saks Incorporated Proxy Statement for the 2010 Annual Meeting of Shareholders to be held on June 8, 2010 are incorporated by reference into Part III of this Form 10-K.

Table of Contents

| PART I |

||||

| Item 1. |

2 | |||

| Item 1A. |

7 | |||

| Item 1B. |

12 | |||

| 13 | ||||

| Item 2. |

15 | |||

| Item 3. |

17 | |||

| PART II |

||||

| Item 5. |

18 | |||

| Item 6. |

21 | |||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

22 | ||

| Item 7A. |

42 | |||

| Item 8. |

43 | |||

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

43 | ||

| Item 9A. |

43 | |||

| Item 9B. |

44 | |||

| PART III |

||||

| Item 10. |

45 | |||

| Item 11. |

45 | |||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

45 | ||

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

45 | ||

| Item 14. |

45 | |||

| PART IV |

||||

| Item 15. |

46 | |||

| 47 | ||||

| 48 | ||||

| F-1 | ||||

| F-2 | ||||

| F-3 | ||||

| F-4 | ||||

| F-5 | ||||

| F-6 | ||||

| F-7 | ||||

| Financial Statement Schedule |

||||

| F-47 | ||||

1

Table of Contents

PART I

General

The operations of Saks Incorporated, a Tennessee corporation first incorporated in 1919, and its subsidiaries (together the “Company”) consist of Saks Fifth Avenue (“SFA”), Saks Fifth Avenue OFF 5TH (“OFF 5TH”), and SFA’s e-commerce operations.

The Company is primarily a fashion retail organization offering a wide assortment of distinctive luxury fashion apparel, shoes, accessories, jewelry, cosmetics, and gifts. SFA stores are principally free-standing stores in exclusive shopping destinations or anchor stores in upscale regional malls. Customers may also purchase SFA products online at www.saks.com or by catalog. OFF 5TH is intended to be the premier luxury off-price retailer in the United States. OFF 5TH stores are primarily located in upscale mixed-use and off-price centers and offer luxury apparel, shoes, and accessories, targeting the value-conscious customer. As of January 30, 2010, the Company operated 53 SFA stores with a total of approximately 5.9 million square feet and 55 OFF 5TH stores with a total of approximately 1.6 million square feet.

Merchandising, sales promotion, and store operating support functions reside in New York, New York. The back office sales support functions for the Company, such as accounting, credit card administration, store planning, and information technology, are located principally in the Company’s operations center in Jackson, Mississippi or in the SFA corporate offices in New York City.

The Company’s fiscal year ends on the Saturday closest to January 31. Fiscal years 2009, 2008, and 2007 each contained 52 weeks and ended on January 30, 2010, January 31, 2009, and February 2, 2008, respectively.

Merchandising

The Company’s stores and e-commerce operations carry luxury merchandise from both core vendors and new and emerging designers. The Company has key relationships with the leading American and European fashion houses, including Giorgio Armani, Chanel, Gucci, Prada, Louis Vuitton, St. John, Zegna, Theory, Cartier, David Yurman, Hugo Boss, Elie Tahari, Tory Burch, Ralph Lauren, Akris and Burberry, among many others.

The Company has developed a knowledge of each of its trade areas and customer bases for its operations. This knowledge is gained through use of on-line merchandise information, store visits by senior management and merchandising personnel, and frequent communication between merchandising staff and store management. The Company strives to tailor each store’s merchandise assortment to the characteristics of its trade areas and customer bases and to the lifestyle needs of its local customers.

Certain departments in the Company’s SFA stores are leased to independent companies in order to provide high quality service and merchandise where specialization and expertise are critical. The leased departments are designed to complement the Company’s owned merchandising departments. The principal leased departments in the SFA stores are furs and certain designer handbags. The terms of the lease agreements typically are between one and seven years and may require the lessee to pay for a portion of the fixtures and provide its own employees. Management regularly evaluates the performance of the leased departments and requires compliance with established customer service guidelines.

2

Table of Contents

For the year ended January 30, 2010, SFA’s percentages of owned sales (exclusive of sales generated by leased departments) by major merchandise category were as follows:

| Women’s Apparel |

35.2 | % | |

| Accessories |

19.6 | % | |

| Cosmetics |

16.3 | % | |

| Men’s Apparel |

14.0 | % | |

| Women’s Shoes |

10.3 | % | |

| Other |

4.6 | % | |

| Total |

100.0 | % | |

Inventory Purchasing and Distribution

Consistent with practices in the retail industry, the Company purchases merchandise assortments and volumes to coincide with the seasonality of the business and expected customer demand. Retailers typically purchase and receive larger amounts of merchandise in the fall as they prepare for the holiday shopping season (primarily November and December).

The Company purchases merchandise from many vendors. Management monitors profitability and sales history with vendors and believes it has alternative sources available for each category of merchandise it purchases. Management believes it maintains good relationships with its vendors.

The Company has two distribution facilities serving its stores. Refer to “Item 2. Properties” for additional information about these facilities.

The Company’s distribution facilities operate on a modern warehouse management system that leverages electronic data interchange (“EDI”) technology in conjunction with high-speed automated conveyor systems in order to receive and distribute merchandise as economically as possible to the Company’s stores. Many of the Company’s vendors also utilize EDI technology which permits merchandise to be ‘cross docked’ from the receiving department to the shipping department, with very little handling. The distribution centers also use efficient radio frequency hand-held devices to scan barcodes on merchandise that is too large or fragile for the conveyor system. The warehouse management system is interfaced to the Company’s mainframe to execute ‘booking’ of the merchandise to the stores and to pass the appropriate records to accounting for invoice payment and reconciliation.

Return Policy

The Company offers its customers a fair and liberal return policy, consistent with other luxury retailers, at SFA stores, OFF 5TH stores, and online at www.saks.com. Approximately 23% of merchandise sold is later returned, and a large percentage of merchandise returns occur within a matter of days of the selling transaction. The Company uses historical return patterns to estimate expected returns.

Information Technology

Company management believes that technological investments are necessary to support its business operations and strategies, and, as a result, the Company is continually upgrading its information systems to improve efficiency and productivity. Between 2006 and 2009, the Company completed significant upgrades to its merchandising planning and allocation systems and installed new point-of-sale equipment and software with enhanced clienteling capabilities in each of its SFA stores.

3

Table of Contents

The Company’s information systems provide information deemed necessary for management operating decisions, cost management programs, and customer service enhancements. Individual data processing systems include point-of-sale and sales reporting, purchase order management, receiving, merchandise planning and control, payroll, human resources, general ledger, and accounts payable systems. Bar code ticketing is used, and scanning is utilized at point-of-sale terminals. Information is made available on Company systems to merchandising staff and store management on a timely basis.

The use of EDI technology allows the Company to speed the flow of information and merchandise in an attempt to capitalize on emerging sales trends, maximize inventory turnover, and minimize out-of-stock conditions. EDI technology includes an advance shipping notice system (“ASN”). The ASN system identifies discrepancies between merchandise that is ready to be shipped from a supplier’s warehouse and that which was ordered from the supplier. This early identification provides the Company with a window of time to resolve any discrepancies in order to speed merchandise through the distribution facilities and into its stores.

Marketing

The Company’s marketing principally emphasizes the latest fashion trends in luxury merchandise and primarily utilizes direct mail (catalogs) and email advertising, supplemented with national and local marketing efforts. To promote its image as one of the primary sources of luxury goods in its trade areas, the Company sponsors numerous fashion shows and in-store special events highlighting the designers represented in the Company’s stores. The Company also participates in “cause-related” marketing. This includes special in-store events and related advertising designed to drive store traffic, while raising funds for charitable organizations and causes such as women’s cancer research. The Company’s in-house marketing and sales promotion staff works with outside agencies to produce the Company’s marketing materials and campaigns.

The Company utilizes data captured through the use of proprietary credit cards offered by HSBC Bank Nevada, N.A. (“HSBC”) to develop advertising and promotional events targeted at specific customers who have purchasing patterns for certain brands, departments, and store locations.

Proprietary Credit Cards

HSBC offers proprietary credit card accounts to the Company’s customers. In April 2003, the Company entered into a program agreement with HSBC for a term of ten years expiring in 2013 pursuant to which HSBC owns and issues proprietary credit cards to the Company’s customers. Pursuant to a servicing agreement with HSBC with a ten-year term expiring in 2013, the Company continues to provide key customer service functions, including new account openings, transaction authorizations, billing adjustments and customer inquiries, and receives compensation from HSBC for the provision of these services.

Under the terms of the original program agreement, HSBC assumed substantially all risks while sharing with the Company certain revenue generated by interest and fees on the portfolio. Saks and HSBC have entered into several amendments to the program agreement since 2003. In October 2009, the Company and HSBC entered into a fifth amendment to the program agreement in response to macroeconomic conditions and portfolio performance, which provides for certain changes to the allocation of risk and revenue sharing between the parties. The fifth amendment, which became effective February 1, 2010, provides for HSBC to share with the Company certain credit losses of the card portfolio and also provides increased revenue sharing to the Company.

In September of 2006, the Company entered into agreements with HSBC and MasterCard International Incorporated to issue co-branded MasterCard cards to new and existing proprietary credit card customers. Under this program, qualifying customers are issued an SFA and MasterCard co-branded credit card that functions as a

4

Table of Contents

traditional proprietary credit card when used at any SFA or OFF 5TH store and at www.saks.com or as a MasterCard card when used at any unaffiliated location that accepts MasterCard cards. HSBC establishes and owns the co-brand accounts, retains the benefits associated with the ownership of the accounts, receives the finance charge and other income from the accounts, and incurs the bad debts associated with the accounts.

Historically, proprietary credit card holders have shopped more frequently with the Company and purchased more merchandise than customers who pay with cash or third-party credit cards. The Company also makes frequent use of the names and addresses of the proprietary credit card holders in its direct marketing efforts.

The Company seeks to expand the number and use of the proprietary credit cards by, among other things, providing monetary incentives to sales associates to open new credit accounts, which generally can be opened while a customer is visiting one of the Company’s stores. Customers who open accounts are entitled to a discount on the first day’s purchases. Customers using the proprietary credit card are eligible for the SaksFirst loyalty program that rewards customers for spending on their proprietary charge cards. Additionally, co-brand card customers earn SaksFirst points for purchases made at unaffiliated locations. Increased spending on the proprietary cards is intended to result in an increased rate of reward. Rewards come in the form of electronic gift cards that are redeemable on future purchases. In addition, members of the loyalty program are eligible for other rewards and benefits including special shopping events and travel discounts.

As of January 30, 2010, there were approximately 702,000 proprietary credit accounts that were active within the prior twelve months, accounting for 41.9% of the Company’s 2009 sales.

Trademarks and Service Marks

The Company owns many trademarks and service marks including, but not limited to, “Saks Fifth Avenue,” “Saks & Company,” “SFA,” “S5A,” “The 5TH Avenue Club,” “SAKSFIRST,” “Clothes (Real),” “Saks Fifth Avenue Men’s Collection,” and “OFF 5TH.” Management believes its trademarks and service marks are important and that the loss of certain of its trademarks or trade names, particularly the store nameplates, could have a material adverse effect on the Company. Many of the Company’s trademarks and service marks are registered in the United States Patent and Trademark Office. The terms of these registrations are generally ten years, and they are renewable for additional ten-year periods indefinitely so long as the marks are in use at the time of renewal. The Company is not aware of any claims of infringement or other challenges to its right to use its marks that would have a material adverse effect on the Company’s consolidated financial position, results of operations, or liquidity.

Reliance on Fifth Avenue Store

The Company’s Flagship SFA store located on Fifth Avenue in New York City accounted for approximately 19% of total Company sales in 2009 and plays a significant role in creating awareness for the Saks Fifth Avenue brand name.

Customer Service

The Company believes that good customer service contributes to increased store visits and purchases by its customers.

The Company’s goal is to deliver an inviting, customer-focused shopping experience to each customer. At SFA and OFF 5TH, the Company seeks to enable its customers to discover both accessible and high-end fashion in a warm, welcoming environment, guided by knowledgeable sales associates. Compensation for sales

5

Table of Contents

associates is generally a commission-based program. Sales associates undergo extensive service, selling, and product-knowledge training and are encouraged to maintain frequent, personal contact with their customers. Sales associates are encouraged to utilize detailed customer data available through the Company’s point-of-sale equipment and software for their clienteling efforts, send personalized thank-you notes, and routinely communicate with customers to advise them of new merchandise offerings and special promotions. Typical SFA stores also provide comfortable seating areas, and most SFA stores offer a complimentary personal shopping service called “The Fifth Avenue Club.”

Seasonality

The Company’s business, like that of many retailers, is subject to seasonal influences, with a significant portion of its sales and net income realized during the second half of the fiscal year, which includes the holiday selling season. Approximately 30% of the Company’s sales are generated during the fourth quarter, and normally a large portion of its operating income is generated during the fall season.

Competition

The retail business is highly competitive. The Company’s stores primarily compete with several national and regional department stores, specialty apparel stores, designer boutiques, outlet stores, and mail-order and e-commerce retailers. Management believes that its knowledge of its trade areas and customer base, combined with the Company’s high level of customer service, broad selection of quality fashion merchandise at appropriate prices, innovative marketing, and strategic store locations, positions the Company for a competitive advantage.

Associates

As of January 30, 2010, the Company employed approximately 12,400 associates, of which approximately 22% were employed on a part-time basis. The Company hires additional temporary associates and increases the hours of part-time associates during seasonal peak selling periods. Approximately 1.0% of the Company’s associates are covered by collective bargaining agreements. The Company considers its relations with its associates to be good.

Inflation and Deflation

Inflation and deflation affect the costs incurred by the Company in its purchase of merchandise and in certain components of its selling, general and administrative expenses (“SG&A”). The Company attempts to offset the effects of inflation, which has occurred in recent years in SG&A.

Discontinued Operations

As of January 31, 2009, the Company discontinued the operations of its Club Libby Lu (“CLL”) business, the operations of which are presented as discontinued operations in the Consolidated Statements of Income and the Consolidated Statements of Cash Flows for the current and prior year periods. CLL consisted of 98 leased, mall-based specialty stores, targeting girls aged 4-12 years old. CLL generated revenues of approximately $52.2 million for 2008 and was not profitable. The Company incurred nominal charges in 2009 and charges of $44.5 million in 2008 associated with closing the stores.

6

Table of Contents

Website Access to Information

The Company provides access, free of charge to the Company’s annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and all amendments to those reports as soon as reasonably practicable after the reports are electronically filed with or furnished to the Securities and Exchange Commission (“SEC”) through the Company’s website, www.saksincorporated.com.

Certifications

The Company filed the certification of its Chief Executive Officer with the New York Stock Exchange (“NYSE”) in fiscal 2009 as required pursuant to Section 303A.12(a) of the NYSE Listed Company Manual, and the Company has filed the Sarbanes-Oxley Act Section 302 and Section 906 certifications of its principal executive officer and principal financial officer with the SEC, which are attached hereto as Exhibits 31.1, 31.2, 32.1, and 32.2.

The following are certain risk factors that affect the Company’s business, financial condition, results of operations, and cash flows, some of which are beyond the Company’s control. These risk factors should be considered in connection with evaluating the forward-looking statements contained in this Annual Report on Form 10-K. The risks and uncertainties described below are not the only ones facing the Company. If any of the events described below were to actually occur, the Company’s business, financial condition, results of operations or cash flows could be adversely affected and results could differ materially from expected and historical results.

A decline in the demand for luxury goods due to difficult macroeconomic conditions has had and could continue to have an adverse impact on the Company’s results of operations.

The Company is focused on the luxury retail sector. SFA stores, OFF 5TH stores and www.saks.com offer a wide assortment of luxury fashion apparel, shoes, accessories, jewelry, cosmetics, and gift items. All of the goods that the Company sells are discretionary items. Changes in consumer confidence and fluctuations in financial markets can influence cyclical trends, particularly in the luxury sector. Consequently, starting in the fall of 2008, the downturn in the economy resulted and may continue to result in fewer customers shopping in the Company’s stores. In response, and in order to reduce inventory levels, the Company was required to take additional markdowns and to increase promotional events during Fall of 2008 and Spring of 2009. The increased markdowns and promotional activity negatively impacted the Company’s profitability. Any future unexpected significant decrease in demand could have a similar effect on profit. As a result of a decrease in consumer spending, the Company has been forced to reduce costs. Despite these measures and continued efforts to align inventory levels with expected sales in fiscal year 2010, there is no assurance that the Company will be successful in restoring profitability. In addition, in the event that we are unsuccessful in restoring profitability, we may not be able to realize our net deferred tax assets, which would require us to record a valuation allowance that could have a material impact on our results of operations in the period in which it is recorded.

Poor economic conditions have affected and may continue to affect consumer spending which has harmed and may continue to harm the Company’s business.

The retail industry is continuously subject to domestic and international economic trends. The success of the Company’s business depends to a significant extent upon the level of consumer spending. A number of factors affect the level of consumer spending on merchandise that the Company offers, including, among other things:

| • | general economic, industry, and weather conditions; |

7

Table of Contents

| • | the performance of the financial equity, and credit markets; |

| • | current and expected unemployment levels; |

| • | crude oil prices that affect gasoline and heating oil prices; |

| • | the level of consumer debt; |

| • | the level of consumer savings |

| • | interest rates; |

| • | tax rates and policies; |

| • | consumer confidence in future economic conditions; and |

| • | war, terrorism, and other hostilities. |

Reduced consumer confidence and spending has resulted in reduced demand for discretionary items and has forced the Company to take significant markdowns in the past. If consumer demand for the Company’s merchandise remains weak, the Company may be forced to take additional markdowns in future periods.

Additionally, several of the Company’s stores are in tourist markets, including the flagship SFA New York store. A continuation of the downturn in economic conditions or other events such as terrorist activity could further impact travel and thus negatively affect the results of operations for stores located within these tourist markets. Increases in transportation and fuel costs, the financial condition of the airline industry and its impact on air travel, and sustained recessionary periods in the U.S. and internationally could also unfavorably impact results of the stores located within these tourist markets.

The Company’s business and results of operations are also subject to uncertainties arising out of world events. These uncertainties may include a global economic slowdown, changes in consumer spending or travel, an increase in gasoline and commodity prices, epidemics, and the economic consequences of natural disasters, military action or terrorist activity (including threats of terrorist activity). Any future events arising as a result of terrorist activity, natural disasters or other world events may have a material impact on the Company’s business, its ability to source products, results of operations, and financial condition in the future.

The Company’s flagship SFA New York store is especially susceptible to volatility in the financial markets and employment and compensation trends in the financial sector.

The Company is restricted in its ability to incur additional debt which may affect its ability to adequately finance its operations.

Our revolving credit facility, our senior notes, and our 2.0% convertible notes contain restrictions on liens and sale/leaseback transactions, and our revolving credit facility also contains a restriction on additional indebtedness, in each case, subject to certain limited exceptions. These restrictions under the revolving credit agreement and the outstanding notes may affect the Company’s ability to obtain additional debt financing or financing on favorable terms if its cash flow from operations and funds available under its revolving credit facility are insufficient to satisfy its working capital requirements.

We are unable to predict the impact of potential disruptions in the credit markets and the resulting costs or constraints in obtaining financing on our business and financial results.

The Company’s principal sources of cash come from the Company’s operating activities and borrowings under its revolving credit facility. Disruptions in the credit markets have had a significant adverse impact on a

8

Table of Contents

number of financial institutions and have affected the cost of capital available to the Company. The Company cannot predict with any certainty the impact of any further disruption in the credit environment or any resulting material impact on its liquidity, future financing costs or financial results.

The Company is dependent on its relationships with certain designers, vendors, and other sources of merchandise.

The Company’s relationships with established and emerging designers are a key factor in its position as a retailer of luxury merchandise, and a substantial portion of its revenues are attributable to its sales of designer merchandise. Many of the Company’s key vendors limit the number of retail outlets they use to sell their merchandise, and competition among luxury retailers to obtain and sell these goods is intense. The Company’s relationships with its designers have been a significant contributor to its past success. Although the Company has supply arrangements with some of its merchandising sources, there can be no assurance that such sources will continue to meet the Company’s quality, style, and volume requirements. Moreover, nearly all of the top designer brands sold by the Company are also sold by competing retailers, and many of these top designer brands also have their own dedicated retail stores. If one or more of these top designers were to cease providing the Company with adequate supplies of merchandise or, conversely, were to increase sales of merchandise through its own stores or to the stores of other competitors, the Company’s business could be adversely affected. In addition, any decline in the popularity or quality of any of these designer brands could adversely affect the Company’s business.

The Company’s business and results of operations may be adversely affected by weather conditions and natural disasters.

The Company’s business is adversely affected by unseasonable weather conditions. Periods of unseasonably warm weather in the fall or winter or unseasonably cold or wet weather in the spring or summer affect consumer apparel purchases and could have a material adverse effect on the Company’s results of operations and financial condition. Additionally, severe weather conditions such as winter snowstorms or natural disasters such as hurricanes, tornadoes, earthquakes, and floods may adversely affect the Company’s results of operations and financial condition.

The Company’s business is intensely competitive and increased or new competition could have a material adverse effect on the Company.

The retail industry is intensely competitive. As a retailer offering a broad selection of luxury fashion apparel, shoes, accessories, jewelry, cosmetics, and gift items, the Company currently competes with a diverse group of retailers, including e-commerce retailers, which sell, among other products, products similar to those of the Company. The Company also competes in particular markets with a substantial number of retailers that specialize in one or more types of products that the Company sells. A number of different competitive factors could have a material adverse effect on the Company’s business, results of operations and financial condition including:

| • | increased operational efficiencies of competitors; |

| • | competitive pricing strategies, including deep discount pricing by a broad range of retailers during periods of poor consumer confidence or economic instability; |

| • | expansion of product offerings by existing competitors; |

| • | entry by new competitors into markets in which the Company currently operates; and |

9

Table of Contents

| • | adoption by existing competitors of innovative retail sales methods. |

The Company may not be able to continue to compete successfully with its existing or new competitors, and prolonged periods of deep discount pricing by its competitors may have a material adverse effect on the Company’s business.

The Company faces risks associated with consumer preferences, demand, and fashion trends.

Changes in consumer preferences, demand and interest could have a material adverse effect on the Company’s business. In addition, fashion trends could materially impact sales. Success in the retail business depends, in part, on the Company’s ability to anticipate consumer preferences and demand. Early order commitments often are made far in advance of consumer acceptance. If the Company fails to anticipate accurately and respond to consumer preferences and demand, it could experience lower sales, excess inventories, and lower profit margins, any of which could have a material adverse effect on the Company’s results of operations and financial condition.

The Company faces a number of risks in opening new stores.

As part of its growth strategy, the Company could potentially increase the total number of stores, which may include opening new stores in both new and existing markets. The Company may not be able to operate any new stores profitably. The success of any future store openings will depend upon numerous factors, many of which are beyond the Company’s control, including the following:

| • | the ability of management to adequately analyze and identify suitable markets and individual store sites within those markets; |

| • | the ability to attract appropriate vendors; |

| • | the competition for suitable store sites; |

| • | the ability to negotiate favorable lease terms with landlords; |

| • | the availability of employees to staff new stores and the Company’s ability to hire, train, motivate, and retain store personnel; and |

| • | the ability to attract customers and generate sales sufficient to operate new stores profitably. |

In future years, the Company may enter into additional markets. These markets may have different competitive conditions, consumer trends, and discretionary spending patterns than its existing markets, which may cause new stores in these markets to be less successful than stores in existing markets.

The loss of, or disruption in, the Company’s centralized distribution centers would have a material adverse effect on the Company’s business and operations.

The Company depends on the orderly operation of the receiving and distribution process, which relies on adherence to shipping schedules and effective management of distribution centers. Although the Company believes that its receiving and distribution process is efficient, and the Company has appropriate contingency plans, unforeseen disruptions in operations due to fire, severe weather conditions, natural disasters, or other catastrophic events, labor disagreements, or other shipping problems may result in delays in the delivery of merchandise to the Company’s stores.

10

Table of Contents

Additionally, freight cost is impacted by changes in fuel prices. Fuel prices affect freight cost both on inbound freight from vendors to the distribution centers and outbound freight from the distribution centers to the Company’s stores.

Although the Company maintains business interruption and property insurance, management cannot be assured that the Company’s insurance coverage will be sufficient, or that insurance proceeds will be timely paid to the Company, if any of the distribution centers are shut down for any reason.

Loss of the Company’s trademarks and service marks or damage to the Company’s brand could have a material adverse effect on the Company’s results of operations.

The Company owns many trademarks and service marks including, but not limited to, “Saks Fifth Avenue,” “Saks & Company,” “SFA,” “S5A,” “The 5TH Avenue Club,” “SAKSFIRST,” “Clothes (Real),” “Saks Fifth Avenue Men’s Collection,” and “OFF 5TH.” Management believes its trademarks and service marks are important and that the loss of certain of its trademarks or trade names, particularly the store nameplates, could have a material adverse effect on the Company. Many of the Company’s trademarks and service marks are registered with the United States Patent and Trademark Office. In addition, the Company has a well-recognized brand that it believes represents unsurpassed customer service and quality merchandise. Any significant damage to the Company’s brand or reputation may negatively impact same-store sales, lower employee morale and productivity, and diminish customer trust, resulting in a reduction in shareholder value.

Fluctuations in foreign currency could have an adverse impact on the Company’s business.

The Company purchases a substantial portion of its inventory from foreign suppliers whose functional currency is not the U.S. dollar. Although fluctuations in the Euro-U.S. dollar exchange rate have the largest impact on the Company’s business, the Company procures goods from many countries and, consequently, is affected by fluctuations in the U.S. dollar relative to the currencies of the countries from which the Company purchases goods. Accordingly, changes in the value of the dollar relative to foreign currencies may increase the Company’s cost of goods sold. If the Company is unable to pass such cost increases on to its customers or the higher cost of the products results in decreased consumption, gross margins and ultimately earnings would decrease.

If the Company does not successfully upgrade, maintain and secure our information systems to support the needs of the organization, it could have an adverse impact on the Company’s business.

The Company relies heavily on information systems to manage operations, including a full range of retail, financial, sourcing and merchandising systems, and regularly make investments to upgrade, enhance or replace these systems. The reliability and capacity of information systems is critical. Despite our preventative efforts, the Company’s systems are vulnerable from time to time to damage or interruption from, among other things, security breaches, computer viruses, power outages and other technical malfunctions. Any disruptions affecting the Company’s information systems, or any delays or difficulties in transitioning to new systems or in integrating them with current systems, could have a material adverse impact on our business. In addition, the Company’s ability to continue to operate its business without significant interruption in the event of a disaster or other disruption depends in part on the ability of the Company’s information systems to operate in accordance with our disaster recovery and business continuity plans.

A privacy breach could adversely affect the Company’s business.

The protection of customer, employee, and company data is critical to the Company. The regulatory environment and industry standards surrounding information security and privacy continue to evolve in response

11

Table of Contents

to increased threats to information security. In addition, customers have a high expectation that the Company will adequately protect their personal information. A significant breach of customer, employee, or company data could damage the Company’s reputation and result in lost sales, fines, or litigation resulting in a decrease in the Company’s earnings.

Ownership and leasing of significant amounts of real estate exposes the Company to possible liabilities and losses.

A significant percentage of our SFA stores and one of our OFF 5TH stores are owned. The remainder of our SFA and OFF 5TH stores are leased. Accordingly, the Company is subject to all of the risks associated with owning and leasing real estate. In particular, the value of the assets could decrease, and their costs to operate could increase, because of changes in the investment climate for real estate, demographic trends, and supply or demand for the use of the store, which may result from competition from similar stores in the area, as well as liability for environmental conditions.

Store leases generally require the Company to pay a fixed minimum rent and a variable amount based on a percentage of annual sales at that location. The Company generally cannot terminate these leases. If a store is not profitable, and the Company decides to close it, the Company may be committed to perform certain obligations under the applicable lease including, among other things, paying rent for the balance of the applicable lease term. In addition, as each of the leases expires, the Company may be unable to negotiate renewals, either on commercially acceptable terms or at all, which could cause the Company to close stores in desirable locations.

If an existing owned store is not profitable, and the Company decides to close it, the Company may be required to record an impairment charge and/or exit costs associated with the disposal of the store.

In addition, the Company may not be able to close an unprofitable owned or leased store due to an existing operating covenant which may cause the Company to operate the location at a loss which could result in an impairment charge.

Item 1B. Unresolved Staff Comments.

None.

12

Table of Contents

Executive Officers and Directors of the Registrant.

The name, age, and position held with the Company for each of the executive officers of the Company are set forth below.

| Name |

Age | Position | ||

| Stephen I. Sadove |

58 | Chairman of the Board of Directors; Chief Executive Officer; Director | ||

| Ronald L. Frasch |

60 | President and Chief Merchandising Officer | ||

| Michael A. Brizel |

53 | Executive Vice President and General Counsel | ||

| Jennifer S. de Winter |

49 | Executive Vice President of Stores | ||

| Marc J. Metrick |

36 | Group Senior Vice President of Merchandise Planning and Chief Strategy Officer | ||

| Christine A. Morena |

54 | Executive Vice President of Human Resources | ||

| Michael Rodgers |

45 | Executive Vice President of Service Operations and Chief Information Officer | ||

| Robert T. Wallstrom |

44 | President, OFF 5TH and Group Senior Vice President | ||

| Kevin G. Wills |

44 | Executive Vice President of Finance and Chief Financial Officer | ||

Stephen I. Sadove was named Chief Executive Officer of the Company in January 2006 and assumed the additional role of Chairman of the Board of Directors in May 2007. Mr. Sadove joined the Company in January 2002 as Vice Chairman and assumed the additional responsibility of Chief Operating Officer in March 2004. Prior to joining the Company, Mr. Sadove served as Senior Vice President of Bristol-Myers Squibb and President of Bristol-Myers Squibb Worldwide Beauty Care from 1996 until January 2002. From 1991 until 1996, Mr. Sadove held various other executive positions with Bristol-Myers Squibb. From 1975 until 1991, Mr. Sadove held various positions of increasing responsibility with General Foods USA.

Ronald L. Frasch was named President and Chief Merchandising Officer of the Company in February 2007. Mr. Frasch joined SFA in January 2004, served in a non-executive capacity through November 2004, and held the post of Vice Chairman and Chief Merchant of SFA from November 2004 until January 2007. Prior to joining the Company, he served as Chairman and Chief Executive Officer of Neiman Marcus Group’s Bergdorf Goodman from April 2000 until January 2004. Prior to that, he held merchandising and executive posts with other companies including GFT USA, Escada USA, Neiman Marcus, and SFA.

Michael A. Brizel joined the Company in April 2007 and was named to the post of Executive Vice President and General Counsel in May 2007. Mr. Brizel served in a variety of positions of increasing responsibility with The Reader’s Digest Association, Inc. between 1989 and April 2007, including Senior Vice President and General Counsel, a position he assumed in 2002. Prior to Reader’s Digest, Mr. Brizel was a member of the legal department of General Foods Corporation from 1983 to 1989 and an associate with the New York law firm of Summit, Rovins and Feldesman (and its predecessors) from 1980 to 1983.

Jennifer S. de Winter was named Executive Vice President of Stores in June 2008. She joined Saks Fifth Avenue in 1995 and held various merchandising positions of increasing responsibility, including her most recent post of Group Senior Vice President and General Merchandise Manager of Fashion and Fine Jewelry, Watches, Women’s Shoes, Handbags, and Soft Accessories. Ms. de Winter began her retail career in 1983 at Macy’s, where she held various merchandising positions through 1995 including Vice President, Divisional Merchandise Manager.

13

Table of Contents

Marc J. Metrick was named Group Senior Vice President and Chief Strategy Officer of the Company in February 2007. Mr. Metrick joined the Company in June 1995 as an executive trainee. Beginning in June 1997, Mr. Metrick served in various planning roles, including Vice President – Merchandise Planning and Senior Vice President — Strategic Planning.

Christine A. Morena joined the Company in January 2007 as Executive Vice President of Human Resources. Ms. Morena spent her career from 1976 through 2006 with AT&T Inc., where she held various positions of increasing responsibility, including Senior Vice President of Human Resources for AT&T Corporation, a subsidiary of AT&T Inc.

Michael Rodgers was named Executive Vice President of Service Operations and Chief Information Officer for the Company in February 2008. Mr. Rodgers served as Executive Vice President of Information Technology, Operations and Credit for the Company from May 2007 through January 2008. Mr. Rodgers joined McRae’s, Inc. (acquired by the Company in 1994) in 1993 as Director of Credit. He was promoted to Vice President of Credit for the Company in 1996 and to Senior Vice President of Credit in 1997, a position he held until 2002. Mr. Rodgers served as Executive Vice President of Operations from 2002 until April 2007. Prior to joining the Company, he held credit management positions with Boscov’s and Woodward & Lothrop.

Robert T. Wallstrom was named President, OFF 5TH and Group Senior Vice President of the Company in February 2007. Mr. Wallstrom joined the Company in June 1995 and has held various leadership positions since that time, including Senior Vice President and General Manager of the SFA flagship store in New York City. Prior to joining the Company, he was a store manager for Macy’s/Bullocks.

Kevin G. Wills was named Executive Vice President and Chief Financial Officer of the Company in May 2007. Mr. Wills served as Executive Vice President of Finance and Chief Accounting Officer from May 2005 until May 2007. He joined the Company in September 1997 and has served in the following capacities: Vice President of Financial Reporting from September 1997 to August 1998; Senior Vice President of Strategic Planning from September 1998 to August 1999; Senior Vice President of Planning and Administration of Saks Department Store Group from September 1999 to January 2003; and Executive Vice President of Operations for Parisian from February 2003 to May 2005. Prior to joining the Company, Mr. Wills was Vice President and Controller for the Tennessee Valley Authority and before that, he was an audit manager with Coopers and Lybrand (now PricewaterhouseCoopers LLP).

14

Table of Contents

The name, current position held and place of employment for each of the directors of the Company are set forth below.

| Name |

Current Position and Place of Employment | |

| Robert B. Carter |

Executive Vice President, FedEx Information Systems and Chief Information Officer, FedEx Corporation | |

| Ronald de Waal |

Chairman, WE International, B.V. | |

| Michael S. Gross |

Chairman, Chief Executive Officer and Managing Member, Solar Capital LLC | |

| Donald E. Hess |

Chief Executive Officer, Southwood Partners | |

| Marguerite W. Kondracke |

President and Chief Executive Officer, America’s Promise – The Alliance for Youth | |

| Jerry W. Levin |

Chairman, JW Levin Partners LLC and Chairman and Chief Executive Officer, Wilton Brands Inc. | |

| Nora P. McAniff |

Treasurer and Member of the Executive Committee, Social Venture Partners of Santa Barbara and formerly, Chief Operating Officer, Time, Inc. | |

| C. Warren Neel |

Executive Director, Center for Corporate Governance at the University of Tennessee, Knoxville and Interim President, Lincoln Memorial University | |

| Christopher J. Stadler |

Managing Partner, CVC Capital Partners | |

| Stephen I. Sadove |

Chairman of the Board and Chief Executive Officer, Saks Incorporated | |

The Company currently operates two principal distribution facilities as follows:

| Company Stores Served |

Location of Facility | Square Feet | Owned/Leased | |||

| SFA, OFF 5TH and Saks Direct |

Aberdeen, Maryland | 514,000 | Leased | |||

| SFA and OFF 5TH |

Ontario, California | 120,000 | Leased |

The Company’s principal administrative offices are as follows:

| Office |

Location of Facility | Square Feet | Owned/Leased | |||

| Corporate Operations Center |

Jackson, Mississippi | 272,000 | Owned | |||

| Corporate Office Headquarters and SFA Offices |

New York, New York | 298,000 | Leased |

The majority of the SFA stores and one OFF 5TH store are owned or owned buildings on leased land. All other SFA and OFF 5TH stores are leased. Store leases generally require the Company to pay a fixed minimum rent and a variable amount based on a percentage of annual sales at that location. Generally, the Company is responsible under its store leases for a portion of mall promotion and common area maintenance expenses and for certain utility, property tax, and insurance expenses. Generally, store leases have initial terms ranging from 20 to 30 years and include renewal options ranging from 5 to 20 years. OFF 5TH leases typically have shorter terms.

15

Table of Contents

The following tables set forth information about the Company’s stores as of January 30, 2010:

| Owned Locations* | Leased Locations | Total | ||||||||||

| Number Of Units |

Gross Square Feet (in mil.) |

Number Of Units |

Gross Square Feet (in mil.) |

Number Of Units |

Gross Square Feet (in mil.) | |||||||

| SFA |

29 | 3.9 | 24 | 2.0 | 53 | 5.9 | ||||||

| OFF 5TH |

1 | 0.1 | 54 | 1.5 | 55 | 1.6 | ||||||

| Total |

30 | 4.0 | 78 | 3.5 | 108 | 7.5 | ||||||

| * | Owned locations include owned stores and owned buildings on leased land. |

| Number of Stores |

Owned Stores |

Leased Stores |

Owned Building on Leased Land | |||||

| Alabama |

1 | 1 | — | — | ||||

| Arizona |

3 | — | 3 | — | ||||

| California |

16 | 1 | 14 | 1 | ||||

| Colorado |

3 | — | 2 | 1 | ||||

| Connecticut |

3 | — | 2 | 1 | ||||

| Florida |

17 | — | 14 | 3 | ||||

| Georgia |

3 | — | 2 | 1 | ||||

| Hawaii |

1 | — | 1 | — | ||||

| Illinois |

4 | — | 3 | 1 | ||||

| Indiana |

1 | — | 1 | — | ||||

| Louisiana |

1 | — | 1 | — | ||||

| Massachusetts |

2 | — | 2 | — | ||||

| Maryland |

2 | — | 1 | 1 | ||||

| Michigan |

2 | 1 | 1 | — | ||||

| Minnesota |

1 | — | — | 1 | ||||

| Missouri |

1 | — | — | 1 | ||||

| North Carolina |

3 | 1 | 2 | — | ||||

| New Jersey |

4 | — | 3 | 1 | ||||

| New York |

8 | 1 | 6 | 1 | ||||

| Nevada |

3 | — | 2 | 1 | ||||

| Ohio |

5 | 1 | 2 | 2 | ||||

| Oklahoma |

1 | — | — | 1 | ||||

| Oregon |

1 | — | — | 1 | ||||

| Pennsylvania |

3 | — | 3 | — | ||||

| South Carolina |

2 | — | 2 | — | ||||

| Tennessee |

1 | — | 1 | — | ||||

| Texas |

12 | 1 | 8 | 3 | ||||

| Virginia |

4 | 2 | 2 | — | ||||

| Total |

108 | 9 | 78 | 21 | ||||

16

Table of Contents

Store count activity for the year ended January 30, 2010 was as follows:

| SFA | OFF 5TH |

Total | ||||

| Store count as of January 31, 2009 |

53 | 51 | 104 | |||

| New stores opened |

0 | 4 | 4 | |||

| Stores closed |

0 | 0 | 0 | |||

| Store count as of January 30, 2010 |

53 | 55 | 108 | |||

Additionally, two OFF 5TH stores were replaced during the year ended January 30, 2010.

The Company is involved in legal proceedings arising from its normal business activities and has accruals for losses where appropriate. Management believes that none of these legal proceedings will have a material adverse effect on the Company’s consolidated financial position, results of operations, or liquidity.

17

Table of Contents

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. |

Market Information

The Company’s common stock trades on the New York Stock Exchange (“NYSE”) under the symbol SKS. The prices in the table below represent the high and low sales prices for the stock as reported by the NYSE.

| Year Ended January 30, 2010 |

Year Ended January 31, 2009 | |||||||||||

| High | Low | High | Low | |||||||||

| First Quarter |

$ | 5.40 | $ | 1.50 | $ | 18.36 | $ | 11.04 | ||||

| Second Quarter |

$ | 5.54 | $ | 3.25 | $ | 14.58 | $ | 9.15 | ||||

| Third Quarter |

$ | 7.45 | $ | 5.11 | $ | 12.25 | $ | 4.81 | ||||

| Fourth Quarter |

$ | 7.72 | $ | 5.37 | $ | 6.16 | $ | 2.25 | ||||

Holders

As of March 12, 2010, there were approximately 2,325 shareholders of record of the Company’s common stock.

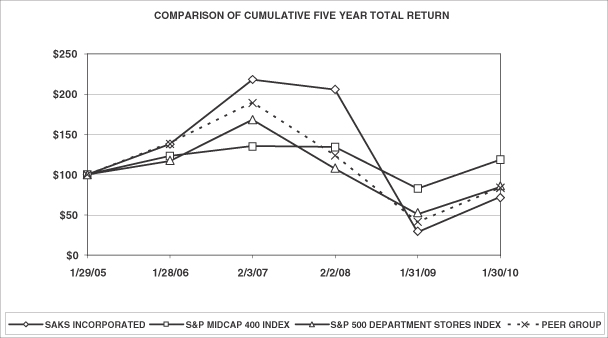

Performance Graph

The following graph and table compare cumulative total shareholder return among the Company, the S&P Midcap 400 Index, the S&P 500 Department Stores Index, and a Retail Peer Group Index (weighted by market capitalization and consisting of Dillard’s, Inc.; Macy’s, Inc.; Nordstrom, Inc.; and J.C. Penney Company, Inc.) assuming an initial investment of $100 and reinvestment of dividends.

18

Table of Contents

| Description |

Starting Basis 1/29/05 |

1/28/06 | 2/3/07 | 2/2/08 | 1/31/09 | 1/30/10 | ||||||||||||

| Saks Incorporated |

$ | 100.00 | $ | 137.75 | $ | 217.71 | $ | 205.39 | $ | 28.22 | $ | 72.12 | ||||||

| S&P Midcap 400 |

$ | 100.00 | $ | 123.18 | $ | 135.57 | $ | 134.06 | $ | 82.57 | $ | 118.37 | ||||||

| S&P 500 Department Stores |

$ | 100.00 | $ | 116.76 | $ | 167.93 | $ | 107.22 | $ | 50.65 | $ | 84.67 | ||||||

| Retail Peer Group |

$ | 100.00 | $ | 139.52 | $ | 189.41 | $ | 123.72 | $ | 41.20 | $ | 83.52 | ||||||

This “Performance Graph” section shall not be deemed to be “soliciting material” or to be “filed” with the SEC or subject to Regulation 14A or 14C or to the liabilities of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

Dividends

During the fiscal years ended January 30, 2010 and January 31, 2009, the Company did not declare any dividends. Future dividends, if any, will be determined by the Company’s Board of Directors in light of circumstances then existing, including earnings, financial requirements, and general business conditions. The Company does not anticipate declaring dividends in the foreseeable future.

Purchases of Equity Securities by the Issuer and Affiliated Purchasers

The Company has a share repurchase program that authorizes it to purchase shares of the Company’s common stock. The Company did not repurchase any shares of common stock during 2009. The Company has remaining availability of approximately 32.7 million shares under its 70 million authorized share repurchase program.

Securities Authorized for Issuance under Equity Compensation Plans

The following table provides equity compensation plan information for all plans approved and not approved by the Company’s shareholders, as of January 30, 2010:

| Plan Category (1) |

Number of securities to be issued upon exercise of outstanding options, warrants and rights (#) (a) |

Weighted-average exercise price of outstanding options, warrants and rights ($) (b) |

Number of securities remaining available for future issuance under equity compensation plans (excluding securities in column (a)) (2) (c) | ||||

| Equity compensation plans approved by security holders |

2,016,731 | $ | 11.37 | 6,027,589 | |||

| Equity compensation plans not approved by security holders (3) |

257,235 | $ | 6.43 | — | |||

| Total |

2,273,966 | $ | 10.81 | 6,027,589 | |||

| (1) | In connection with the acquisition of its former Parisian business, the Company assumed then-outstanding stock options previously granted to employees and directors of the acquired corporation. No additional grants or awards may be made under the plan pursuant to which these stock options were granted. As of January 30, 2010, the total number of shares of Common Stock to be issued upon exercise of these stock options was 34,707 and the weighted-average exercise price of these stock options was $6.54. These stock options are not included in the table. |

| (2) | This amount represents shares of Common Stock available for issuance under the 2009 Incentive Plan. Awards available for grant under the 2009 Incentive Plan include options, stock appreciation rights, restricted stock, performance units, and any combination of the foregoing awards. |

19

Table of Contents

| (3) | On April 9, 1997, the Board approved the Company’s 1997 Stock-Based Incentive Plan (the “1997 Plan”) to assist in attracting, retaining, and motivating employees and directors. The Board amended the 1997 Plan several times. The exercise price for all outstanding options awarded under the 1997 Plan equals the fair market value of the Common Stock on the date of grant. Most options vest in five installments over four years and expire after seven or ten years. Unvested options generally are forfeited if the executive’s employment is terminated. In the event of a change in control or a potential change in control, the Board of Directors may accelerate awards under the 1997 Plan or provide that such awards be cashed out in connection with the transaction. As of January 30, 2010, under the 1997 Plan, there were (i) options outstanding to purchase 257,235 shares, (ii) 14,000 shares of restricted stock outstanding and unvested, and (iii) no shares remaining available for issuance. |

20

Table of Contents

Item 6. Selected Financial Data.

The selected financial data set forth below should be read in conjunction with Management’s Discussion and Analysis of Financial Condition and Results of Operations, the Company’s Consolidated Financial Statements and notes thereto and the other information contained elsewhere in this Form 10-K.

| Year Ended | ||||||||||||||||||||

| (IN THOUSANDS, EXCEPT PER SHARE AMOUNTS) |

January 30, 2010 |

January 31, 2009 (Revised)** |

February 2, 2008 (Revised)** |

February 3, 2007* (Revised)** |

January 28, 2006 (Revised)** |

|||||||||||||||

| CONSOLIDATED INCOME STATEMENT DATA: |

||||||||||||||||||||

| Net sales |

$ | 2,631,532 | $ | 3,043,438 | $ | 3,237,275 | $ | 2,900,383 | $ | 2,741,295 | ||||||||||

| Cost of sales (excluding depreciation and amortization) |

1,668,097 | 2,062,494 | 1,972,251 | 1,780,127 | 1,731,142 | |||||||||||||||

| Gross margin |

963,435 | 980,944 | 1,265,024 | 1,120,256 | 1,010,153 | |||||||||||||||

| Selling, general and administrative expenses |

674,306 | 784,510 | 840,823 | 811,248 | 822,188 | |||||||||||||||

| Other operating expenses |

314,266 | 320,683 | 317,046 | 312,486 | 317,760 | |||||||||||||||

| Impairments and dispositions |

29,348 | 11,139 | 4,279 | 11,775 | (8,349 | ) | ||||||||||||||

| Operating income (loss) |

(54,485 | ) | (135,388 | ) | 102,876 | (15,253 | ) | (121,446 | ) | |||||||||||

| Interest expense |

(49,480 | ) | (45,739 | ) | (48,303 | ) | (55,693 | ) | (82,539 | ) | ||||||||||

| Gain (loss) on extinguishment of debt |

783 | — | (5,634 | ) | 7 | (29,375 | ) | |||||||||||||

| Other income, net |

1,019 | 5,600 | 24,912 | 28,407 | 7,705 | |||||||||||||||

| Income (loss) from continuing operations before income taxes |

(102,163 | ) | (175,527 | ) | 73,851 | (42,532 | ) | (225,655 | ) | |||||||||||

| Provision (benefit) for income taxes |

(44,501 | ) | (48,902 | ) | 26,755 | (34,947 | ) | (92,062 | ) | |||||||||||

| Income (loss) from continuing operations |

(57,662 | ) | (126,625 | ) | 47,096 | (7,585 | ) | (133,593 | ) | |||||||||||

| Discontinued operations: |

||||||||||||||||||||

| Income (loss) from discontinued operations before income taxes |

(395 | ) | (52,727 | ) | (4,860 | ) | 188,227 | 314,943 | ||||||||||||

| Provision (benefit) for income taxes |

(138 | ) | (20,548 | ) | (1,646 | ) | 130,536 | 163,241 | ||||||||||||

| Income (loss) from discontinued operations |

(257 | ) | (32,179 | ) | (3,214 | ) | 57,691 | 151,702 | ||||||||||||

| Net Income (loss) |

$ | (57,919 | ) | $ | (158,804 | ) | $ | 43,882 | $ | 50,106 | $ | 18,109 | ||||||||

| Basic earnings per common share: |

||||||||||||||||||||

| Income (loss) from continuing operations |

$ | (.40 | ) | $ | (.93 | ) | $ | .33 | $ | (.06 | ) | $ | (.97 | ) | ||||||

| Income (loss) from discontinued operations |

$ | — | $ | (.23 | ) | $ | (.02 | ) | $ | .43 | $ | 1.10 | ||||||||

| Net income (loss) |

$ | (.40 | ) | $ | (1.15 | ) | $ | .31 | $ | .37 | $ | .13 | ||||||||

| Diluted earnings per common share: |

||||||||||||||||||||

| Income (loss) from continuing operations |

$ | (.40 | ) | $ | (.92 | ) | $ | .31 | $ | (.06 | ) | $ | (.97 | ) | ||||||

| Income (loss) from discontinued operations |

$ | — | $ | (.23 | ) | $ | (.02 | ) | $ | .43 | $ | 1.10 | ||||||||

| Net income (loss) |

$ | (.40 | ) | $ | (1.15 | ) | $ | .29 | $ | .37 | $ | .13 | ||||||||

| Weighted average common shares: |

||||||||||||||||||||

| Basic |

143,194 | 138,384 | 140,402 | 135,880 | 138,348 | |||||||||||||||

| Diluted |

143,194 | 138,384 | 153,530 | 135,880 | 138,348 | |||||||||||||||

| CONSOLIDATED BALANCE SHEET DATA: |

||||||||||||||||||||

| Working capital |

$ | 546,169 | $ | 503,952 | $ | 345,097 | $ | 388,061 | $ | 799,601 | ||||||||||

| Total assets |

$ | 2,135,701 | $ | 2,147,677 | $ | 2,350,744 | $ | 2,521,211 | $ | 3,825,247 | ||||||||||

| Long-term debt, less current portion |

$ | 493,330 | $ | 593,103 | $ | 204,238 | $ | 394,498 | $ | 661,202 | ||||||||||

| Shareholders' equity |

$ | 1,071,610 | $ | 990,586 | $ | 1,204,434 | $ | 1,128,559 | $ | 2,035,439 | ||||||||||

| Cash dividends (per share) |

$ | — | $ | — | $ | — | $ | 8.00 | $ | — | ||||||||||

| * | The year ended February 3, 2007 includes an extra week, creating a 53-week fiscal year that occurs every six years in the accounting cycle. |

| ** | Prior year amounts have been revised to reflect the retrospective application of adopting a new accounting pronouncement relating to convertible debt. Amounts have also been revised to reflect all shipping and handling revenue in Net Sales. See Note 2 to the consolidated financial statements for further discussion. |

21

Table of Contents

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Management’s Discussion and Analysis (“MD&A”) is intended to provide an analytical view of the business from management’s perspective of operating the business and is considered to have these major components:

| • | Overview |

| • | Results of Operations |

| • | Liquidity and Capital Resources |

| • | Critical Accounting Policies |

MD&A should be read in conjunction with the consolidated financial statements and related notes thereto contained elsewhere in this Form 10-K.

OVERVIEW

GENERAL

The operations of Saks Incorporated, a Tennessee corporation first incorporated in 1919, and its subsidiaries (together the “Company”) consist of Saks Fifth Avenue (“SFA”), Saks Fifth Avenue OFF 5TH (“OFF 5TH”), and SFA’s e-commerce operations. Previously, the Company also operated Club Libby Lu (“CLL”), the operations of which were discontinued in January 2009. The operations of CLL are presented as discontinued operations in the Consolidated Statements of Income and the Consolidated Statements of Cash Flows for the current and prior year periods and are discussed below in “Discontinued Operations.”

The Company is primarily a fashion retail organization offering a wide assortment of distinctive luxury fashion apparel, shoes, accessories, jewelry, cosmetics, and gifts. SFA stores are principally free-standing stores in exclusive shopping destinations or anchor stores in upscale regional malls. Customers may also purchase SFA products by catalog or online at www.saks.com. OFF 5TH is intended to be the premier luxury off-price retailer in the United States. OFF 5TH stores are primarily located in upscale mixed-use and off-price centers and offer luxury apparel, shoes, and accessories, targeting the value-conscious customer. As of January 30, 2010, the Company operated 53 SFA stores with a total of approximately 5.9 million square feet and 55 OFF 5TH stores with a total of approximately 1.6 million square feet.

The Company is primarily focused on the luxury retail sector. All of the goods that the Company sells are discretionary items. Consequently, a downturn in the economy or difficult economic conditions may result in fewer customers shopping in the Company’s stores or online. In response, the Company may have to increase the duration and/or frequency of promotional events and offer larger discounts in order to attract customers, which would reduce gross margin and adversely affect results of operations.

The Company continues to make targeted investments in key areas to improve customer service and enhance merchandise assortment and allocation effectiveness. In addition, strategic investments are being made to remodel existing selling space with a heightened focus on return on investment. The Company believes that its long-term strategic plans can deliver additional operating margin expansion in future years.

The Company seeks to create value for its shareholders by improving returns on its invested capital. The Company attempts to generate improved operating margins by generating sales increases while improving merchandising margins and controlling expenses. The Company uses operating cash flows to reinvest in the business and to repurchase debt or equity. The Company actively manages its real estate portfolio by routinely evaluating opportunities to improve or close underproductive stores and open new stores.

22

Table of Contents

DISCONTINUED OPERATIONS

As of January 31, 2009, the Company discontinued the operations of its CLL business, which consisted of 98 leased, mall-based specialty stores, targeting girls aged 4-12 years old. Charges incurred during 2008 associated with the closing of these stores totaled approximately $44.5 million and included inventory liquidation costs of approximately $7.0 million, asset impairment charges of $17.0 million, lease termination costs of $14.0 million, severance and personnel related costs of $5.1 million, and other closing costs of $1.4 million. These amounts are included in discontinued operations in the Consolidated Statement of Income and the Consolidated Statement of Cash Flows for fiscal year 2008. The remaining amount payable related to the disposition of the CLL business as of January 30, 2010 is $0.7 million and is expected to be paid during the year ending January 29, 2011.

SAKS FIFTH AVENUE NEW ORLEANS STORE

In late August 2005, the SFA store in New Orleans suffered substantial water, fire, and other damage related to Hurricane Katrina. The Company reopened the store in the fourth fiscal quarter of 2006 after necessary repairs and renovations were made to the property.

The SFA New Orleans store was covered by both property damage and business interruption insurance. The property damage coverage paid to repair and/or replace the physical property damage and inventory loss, and the business interruption coverage reimbursed the Company for lost profits as well as continuing expenses related to loss mitigation, recovery, and reconstruction for the full duration of the reconstruction period plus three months. The Company recorded in 2005 both (i) a $14.7 million gain on the excess of the replacement insurance value over the recorded net book value of the lost and damaged assets and (ii) $2.6 million of expenses related to the insurance deductible. In 2006, the Company recorded an adjustment (credit) of $1.6 million related to the insurance deductible. In 2007, the Company recorded a pre-tax gain of $13.5 million associated with the proceeds from the business interruption claims.

FINANCIAL PERFORMANCE SUMMARY

On a consolidated basis, total net sales and comparable store sales for the year ended January 30, 2010 decreased 13.5% and 14.7%, respectively. The Company recorded a loss from continuing operations of $57.7 million, or $0.40 per share compared to a loss from continuing operations of $126.6 million, or $0.92 per share, for the years ended January 30, 2010 and January 31, 2009, respectively. After recognition of the Company’s after-tax loss from discontinued operations of $0.3 million, net loss totaled $57.9 million, or $0.40 per share for the year ended January 30, 2010. After recognition of the Company’s after-tax loss from discontinued operations of $32.2 million, or $0.23 per share, net loss totaled $158.8 million, or $1.15 per share for the year ended January 31, 2009.

The year ended January 30, 2010 included net after tax charges totaling $10.4 million or $0.07 per share, primarily related to $17.3 million or $0.12 per share of asset impairment charges incurred in the normal course of business and a $3.1 million or $0.02 per share non-cash pension charge related to excess lump sum distributions during 2009 primarily resulting from the Company’s 2009 reductions-in-force. The year ended January 30, 2010 also included a net gain of $10.0 million or $0.07 per share, related to federal and state tax adjustments.

The year ended January 31, 2009 included net after-tax charges totaling $26.2 million or $0.19 per share, primarily related to $7.0 million or $0.05 per share of asset impairment charges incurred in the normal course of business and approximately $6.7 million or $0.05 per share of severance costs related to the Company’s 2008 downsizing initiative and the Ft. Lauderdale store closing. The year ended January 31, 2009 also included a write-off and adjustment of $14.6 million or $0.11 per share of certain deferred tax assets primarily associated with federal net operating loss (“NOL”) tax credits that expired at the end of fiscal 2008. These expenses were partially offset by a net gain of $2.1 million or $0.02 per share related to the sale of three unutilized properties.

23

Table of Contents

The year ended February 2, 2008 included net after-tax charges totaling $16.0 million, or $0.10 per share, primarily related to $18.1 million, or $0.12 per share, for retention, severance, and transition costs related to the Company’s downsizing and consolidation following the disposition of its Saks Department Store Group (“SDSG”) businesses. Additionally, legal and investigation costs totaled $3.7 million, or $.02 per share, associated with the previously disclosed investigation by the SEC (which has been concluded) and the investigation by the Office of the United States Attorney for the Southern District of New York as well as the settlement of two related vendor lawsuits. The year ended February 2, 2008 also included a loss on extinguishment of debt totaling $3.4 million or $.02 per share, related to the repurchase of $106.3 million of senior notes, $2.7 million, or $.02 per share, related to asset impairments and dispositions, and $0.8 million expense related to a state tax adjustment. These expenses were partially offset by an insurance adjustment (credit) of $8.1 million, or $0.05 per share, related to the New Orleans Store, as well as a gain of $1.6 million, or $.01 per share, related to an OFF 5TH store closing and the sale of an unused support facility. Lastly, there was a $3.0 million, or $.02 per share, state income tax valuation adjustment (credit).

During the preparation of our condensed consolidated financial statements for the quarterly period ended October 31, 2009, the Company identified a classification error in our Consolidated Statements of Income for the year ended January 31, 2009 and prior periods and the quarterly periods therein. The Company improperly included certain shipping and handling revenue in selling, general and administrative expenses (“SG&A”). The Company corrected this error in the Consolidated Statements of Income by adjusting Net Sales and SG&A to reflect all shipping and handling revenue in Net Sales for all prior periods presented.

Effective February 1, 2009, the Company retrospectively adopted Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 470 related to accounting for convertible debt instruments that may be settled in cash upon conversion (including partial cash settlement) (“ASC 470”), which requires an allocation of convertible debt proceeds between the liability component and the embedded conversion option (i.e., the equity component). The liability component of the debt instrument is accreted to par value using the effective interest method over the remaining life of the debt. The accretion is reported as a component of interest expense. The equity component is not subsequently revalued as long as it continues to qualify for equity treatment.

The Company believes that an understanding of its reported financial condition and results of operations is not complete without considering the effect of all other components of MD&A included herein.

24

Table of Contents

RESULTS OF OPERATIONS

The following table sets forth, for the periods indicated, selected items from the Company’s Consolidated Statements of Income, expressed as percentages of net sales (numbers may not total due to rounding):

| Year Ended | |||||||||

| January 30, 2010 |

January 31, 2009 (Revised) |

February 2, 2008 (Revised) |

|||||||

| Net sales |

100 | % | 100 | % | 100 | % | |||

| Cost of sales (excluding depreciation and amortization) |

63.4 | 67.8 | 60.9 | ||||||

| Gross margin |

36.6 | 32.2 | 39.1 | ||||||

| Selling, general and administrative expenses |

25.6 | 25.8 | 26.0 | ||||||

| Other operating expenses |

12.0 | 10.5 | 9.8 | ||||||

| Impairments and dispositions |

1.1 | 0.4 | 0.1 | ||||||

| Operating income (loss) |

(2.1 | ) | (4.4 | ) | 3.2 | ||||

| Interest expense |

(1.9 | ) | (1.5 | ) | (1.5 | ) | |||

| Gain (loss) on extinguishment of debt |

0.0 | 0.0 | (0.2 | ) | |||||

| Other income, net |

0.0 | 0.2 | 0.8 | ||||||

| Income (loss) from continuing operations before income taxes |

(3.9 | ) | (5.8 | ) | 2.3 | ||||

| Provision (benefit) for income taxes |

(1.7 | ) | (1.6 | ) | 0.8 | ||||

| Income (loss) from continuing operations |

(2.2 | ) | (4.2 | ) | 1.5 | ||||

| Discontinued operations: |

|||||||||

| Loss from discontinued operations |

(0.0 | ) | (1.7 | ) | (0.2 | ) | |||

| Benefit for income taxes |

(0.0 | ) | (0.7 | ) | (0.1 | ) | |||

| Loss from discontinued operations |

(0.0 | ) | (1.1 | ) | (0.1 | ) | |||

| Net income (loss) |

(2.2 | )% | (5.2 | )% | 1.4 | % | |||

FISCAL YEAR ENDED JANUARY 30, 2010 (“2009”) COMPARED TO FISCAL YEAR ENDED JANUARY 31, 2009 (“2008”)

DISCUSSION OF OPERATING LOSS — CONTINUING OPERATIONS

The following table shows the changes in operating loss from 2008 to 2009:

| (In Millions) |

Total Company |

|||

| 2008 Operating Loss—Continuing Operations |

$ | (135.4 | ) | |

| Store sales and margin |

(17.5 | ) | ||

| Operating expenses |

116.6 | |||

| Impairments and dispositions |

(18.2 | ) | ||

| Change |

80.9 | |||

| 2009 Operating Loss—Continuing Operations |

$ | (54.5 | ) | |