Attached files

| file | filename |

|---|---|

| EX-32.2 - EX-32.2 - VITAL IMAGES INC | a09-35845_1ex32d2.htm |

| EX-21.1 - EX-21.1 - VITAL IMAGES INC | a09-35845_1ex21d1.htm |

| EX-23.1 - EX-23.1 - VITAL IMAGES INC | a09-35845_1ex23d1.htm |

| EX-32.1 - EX-32.1 - VITAL IMAGES INC | a09-35845_1ex32d1.htm |

| EX-31.1 - EX-31.1 - VITAL IMAGES INC | a09-35845_1ex31d1.htm |

| EX-31.2 - EX-31.2 - VITAL IMAGES INC | a09-35845_1ex31d2.htm |

| EX-10.22 - EX-10.22 - VITAL IMAGES INC | a09-35845_1ex10d22.htm |

| EX-10.21 - EX-10.21 - VITAL IMAGES INC | a09-35845_1ex10d21.htm |

| EX-10.23 - EX-10.23 - VITAL IMAGES INC | a09-35845_1ex10d23.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

|

x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

OR

|

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 0-22229

Vital Images, Inc.

(Exact name of registrant as specified in its charter)

|

Minnesota |

|

42-1321776 |

|

(State or other jurisdiction of |

|

(I.R.S. Employer Identification No.) |

|

incorporation or organization) |

|

|

|

5850 Opus Parkway, Suite 300 |

|

|

|

Minnetonka, MN 55343-4414 |

|

55343-4414 |

|

(Address of principal executive offices) |

|

(Zip Code) |

(952) 487-9500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

|

Title of Each Class |

|

Name of Each Exchange on Which Registered |

|

|

|

Common Stock, $.01 par value |

|

NASDAQ Global Select Market |

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o |

|

Accelerated filer x |

|

|

|

|

|

Non-accelerated filer o |

|

Smaller reporting company o |

|

(Do not check if a smaller reporting company) |

|

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

As of June 30, 2009, the last day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $161,839,241. The common stock is the registrant’s only class of voting stock.

The number of shares outstanding of the issuer’s class of common stock as of March 9, 2010 was 14,425,889 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of registrant’s definitive Proxy Statement in connection with the Annual Meeting of Stockholders to be held May 11, 2010 (“2010 Proxy Statement”) are incorporated by reference into Part III of this Form 10-K, as indicated in Items 10 through 14 of Part III.

Vital Images, Inc.

Form 10-K

Cautionary Statement Regarding Forward-Looking Information

Vital Images desires to take advantage of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995 (the “Reform Act”) and is filing this cautionary statement in connection with the Reform Act. This Annual Report on Form 10-K and any other written or oral statements made by us or on our behalf may include forward-looking statements that reflect our current views with respect to future events and future financial performance. Certain statements in this Annual Report on Form 10-K are “forward-looking statements” within the meaning of Section 27(a) of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. You can identify these forward-looking statements by our use of the words “believes,” “anticipates,” “forecasts,” “projects,” “could,” “plans,” “expects,” “may,” “will,” “would,” “intends,” “estimates” and similar expressions, whether in the negative or affirmative. We wish to caution you that any forward-looking statements made by us or on our behalf are subject to uncertainties and other factors that could cause such statements to be wrong. We cannot guarantee that we actually will achieve these plans, intentions or expectations. Actual results or events could differ materially from the plans, intentions and expectations disclosed in the forward-looking statements that we make. These statements are only predictions and speak only of our views as of the date the statements were made. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, and/or performance of achievements. We do not assume any obligation to update or revise any forward-looking statements that we make, whether as a result of new information, future events or otherwise.

Factors that may impact forward-looking statements include, among others, our abilities to maintain the technological competitiveness of our current products, develop new products, successfully market our products, respond to competitive developments, develop and maintain partnerships with providers of complementary technologies, manage our costs and the challenges that may come with growth of our business, and attract and retain qualified sales, technical and management employees. We are also affected by the growth and regulation of the medical technology industry, including the acceptance of advanced visualization by hospitals, clinics, and universities, product clearances and approvals by the United States Food and Drug Administration and similar regulatory bodies outside the United States, and reimbursement and regulatory practices by Medicare, Medicaid, and private third-party payer organizations. We are also affected by other factors identified in our filings with the Securities and Exchange Commission, some of which are set forth in the section entitled “Item 1A. Risk Factors” in this Annual Report on Form 10-K (and many of which we have discussed in prior filings). Although we have attempted to list comprehensively these important factors, we also wish to caution investors that other factors may prove to be important in the future in affecting our operating results. New factors emerge from time to time, and it is not possible for us to predict all of these factors, nor can we assess the impact each factor or combination of factors may have on our business.

Our Business

Vital Images, Inc. (“Vital Images,” “we,” “us,” or “our”) is a leading provider of advanced visualization and image analysis solutions for use by medical professionals in clinical analysis and therapy planning for medical conditions. We provide software, customer education, software maintenance and support, professional services and, on occasion, third-party hardware to our customers. Our technology rapidly transforms complex data generated by diagnostic imaging equipment into functional digital images that can be manipulated and analyzed using our specialized applications to better understand internal anatomy and pathology. Our solutions are designed to improve physician workflow and productivity, enhance the ability to make clinical decisions, facilitate less invasive patient care, and complement often significant capital investments in diagnostic imaging equipment made by our customers. Our software is compatible with equipment from all major manufacturers of diagnostic imaging equipment, such as computed tomography (“CT”) scanners, and can be integrated into picture archive and communication systems (“PACS”). Many hospitals use PACS to acquire, distribute and archive medical images and diagnostic reports, reducing the need for film and increasing reliance on advanced visualization solutions such as ours. We also offer a Web-based solution that provides physicians with anywhere, anytime access to medical images and visualization tools through any Internet-enabled computer.

We were founded and incorporated in Iowa in September 1988, and we re-incorporated in Minnesota in March 1997. Our principal executive offices are located at 5850 Opus Parkway, Suite 300, Minnetonka, MN 55343 (telephone (952) 487-9500, facsimile (952) 487-9510, e-mail — info@vitalimages.com ). From May 24, 1994 through May 11, 1997, we were a wholly-owned subsidiary of Bio-Vascular, Inc., which is now known as Synovis Life Technologies, Inc.

Our corporate website address is www.vitalimages.com. To access our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, other reports and documents filed with or furnished to the United States Securities and Exchange Commission (the “SEC”) and amendments to these reports free of charge, go to the “Investors” section of our website, then to the “Financial Information” category, and then to the “SEC Filings” subcategory, where we make such filings available as soon as reasonably practicable after they are filed with or furnished to the SEC. The “Corporate Governance” category of the Investors section of our website also contains free copies of the Charters for the Audit Committee, Compensation Committee, and Governance Committee of our Board of Directors, as well as our Code of Business Conduct and Ethics, which is our written code of ethics under Section 406 of the Sarbanes-Oxley Act of 2002. Each of the above referenced documents can also be obtained free of charge (other than a reasonable charge for copying exhibits to our reports on Forms 10-K, 10-Q or 8-K) in print by any shareowner who requests them from our investor relations department. The investor relations department’s email address is investorrelations@vitalimages.com and its mail address is: Investor Relations, Vital Images, Inc., 5850 Opus Parkway, Suite 300, Minnetonka, MN 55343. Information available on our website is not incorporated by reference into this Annual Report on Form 10-K.

You may also obtain copies of our SEC filings on the SEC’s website at www.sec.gov or at the SEC’s Public Reference Room at 100 F Street N.E., Washington, D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.

Products and Services

Our software solutions are used with medical diagnostic equipment, primarily in clinical analysis and therapy planning. Our software applies proprietary technologies to a variety of data supplied by CT scanners to allow medical clinicians to create 2D, 3D and 4D views of human anatomy and to non-invasively navigate within these images to better visualize and understand internal structures and pathologies. Our main customers are hospitals and clinics, university medical schools and diagnostic imaging centers. We market our products and services to these customers both directly through our own sales force and indirectly through digital imaging equipment manufacturers and PACS companies, who sell our products with other products they either manufacture or acquire from third parties.

Our products initially were used by radiologists on dedicated workstations to interpret data generated by scanning equipment. Our main product for this type of use was and remains Vitrea®. Over time, other medical specialists, primarily cardiologists, began to use advanced visualization software on dedicated workstations. As additional types of specialists began desiring access to the benefits provided by advanced visualization tools, we began to integrate our products onto workstations connected to PACS and to offer a server-based advanced visualization solution called ViTALConnect®.

In 2008, we further expanded access to our advanced visualization products throughout the entirety of the hospital enterprise with our introduction, at that time, of Vital Enterprise. Our enterprise offerings expand the relevance of our advanced visualization options products beyond the radiology department to referring physicians and surgical specialists, particularly in the areas of cardiology, cardiovascular, oncology, neurology and gastroenterology. Our current enterprise offering is called Vitrea Enterprise Suite, which combines all of our proprietary advanced visualization tools into one offering, and may include our proprietary back-end data management software, Vital Image Management System. Vitrea Enterprise Suite can be used by every medical professional that practices with our customer’s enterprise. Both our enterprise and workstation products also serve as an integration platform for applications offered by our visualization technology partners.

Our products work with equipment from all major manufacturers of diagnostic imaging systems, including Toshiba Medical Systems Corporation (“Toshiba”), GE Healthcare (“GE”), Siemens Medical Systems, Inc. (“Siemens”) and Philips Medical Systems (“Philips”). Our products may also be integrated into PACS, such as those marketed by

McKesson Corporation (“McKesson”) and Sectra AB (“Sectra”), and run on off-the-shelf third-party computer hardware.

In addition to software products and installation services, we provide maintenance and support services, as well as certain other services, such as professional consulting services and customer education. We offer maintenance and support services for our software solutions pursuant to which we provide error correction, software enhancements, updates and upgrades, telephone support and other general support services. We provide customer education services for our customers, both in connection with their acquisition of our software and as independent purchases. We conduct customer education programs for our software at our headquarters in Minnetonka, Minnesota, at customers’ locations and at various designated locations through the United States.

We have also signed reseller distribution agreements that allow us to distribute products from certain third parties. These third-party products include MeVis Medical Solutions Inc.’s ImageChecker® CT software applications for the detection of lung nodules; Mirada Solutions Ltd.’s Fusion 7D™ software application for the anatomical alignment of two different image data sets from two different types of diagnostic equipment, such as combining images from CT and PET scanners; Merge Healthcare Incorporated’s CADstream™ breast MRI software; and Medis Inc.’s QMass® MR software.

Marketing and Distribution

We market our products both as standalone software packages and as part of integrated software and hardware systems to radiologists, surgeons, primary care physicians and medical researchers. We market our products directly to end-user customers and through business partners, including diagnostic imaging equipment manufacturers, PACS companies, and software developers, all of whom sell our products with products they either manufacture or acquire from third parties.

Our marketing partners include Toshiba, which markets our software to its customers through its subsidiaries and distributors worldwide. Our agreement with Toshiba commenced in 2001, and it has been extended multiple times, most recently through December 31, 2013. The Marketing and Distribution Agreement, which was entered into by Toshiba and us on November 21, 2008, is a typical reseller or distributor agreement, under which Toshiba resells our imaging products in connection with its sales of its own scanner equipment. Under the Marketing and Distribution Agreement, Toshiba markets and resells our products to its customers. Our sales team may provide assistance to Toshiba in its sales efforts, in a similar manner to how our sales team provides assistance to our other resellers, and we provide back-up technical support for problems that Toshiba cannot resolve. The Marketing and Distribution Agreement ensures a minimum amount of purchases from us by Toshiba. Because purchases by Toshiba have exceeded their commitments, these minimum purchase obligations have not been triggered to date, nor do we have reason to expect these provisions to be triggered in the future. Sales through Toshiba are a material portion of our revenues, comprising approximately 54% of our 2009 revenues, 52% of our 2008 revenues and 47% of our 2007 revenues.

We also have marketing and reseller agreements with several other companies, such as McKesson, Sectra and Cerner Corp., under which these companies may resell our products to their customers as add-on components to their products.

Geographic Information

Our export sales and long-lived assets by significant geographic areas are presented in Note 10 of the Consolidated Financial Statements in our 2009 Annual Report on Form 10-K, listed in Item 15(a)(1) of the Form 10-K.

Research and Development

Our research and development activities are focused on the development of new products and on improvements to existing products. Research and development expense was $16.3 million, $20.3 million and $18.5 million for the years ended December 31, 2009, 2008 and 2007, respectively.

In addition to our Marketing and Distribution Agreement with Toshiba, noted above, we also have entered into a Technology Development Agreement, which became effective on January 8, 2009 and calls for development of

software or clinical applications by us under Product Development Plans, as such term is defined in the Technology Development Agreement. Each Product Development Plan is separately entered into between Toshiba and us and discusses the key features of the project, including the product to be developed, development milestones, and the amount and timing of funding to be provided by Toshiba for the development effort. Upon completion of the project, we can sell the product that is developed both through Toshiba and, after a 180-day exclusivity period, through our direct sales force, although the exclusivity period may be waived for certain projects. We dedicate a specific number of our personnel exclusively to each project that is funded by Toshiba. The Technology Development Agreement currently will terminate six months following the end of all active Product Development Plans, although it may renew upon written agreement by Toshiba and us. If at any time no projects are ongoing during the term of the Technology Development Agreement, Toshiba will continue to provide funding to us at the rates set forth in the Agreement for up to six months for any of our personnel who are assigned to and actively engaged on projects related to errors reported in any project software that was previously released. In addition, Toshiba will also continue to provide funding for the dedicated project personnel for up to six months during the term, if no project is ongoing, or for up to six months after the term, to assist us to cover reallocation and/or termination costs. Funding received by us under the Technology Development Agreement is accounted for as an offset to research and development expense. We recognized a credit to research and development expenses of $1.1 million under the Technology Development Agreement in 2009.

Competition

The advanced visualization market is highly competitive, subject to rapid change and is significantly affected by new product introductions and other market activities of industry participants. Our products compete based on a multitude of factors, including quality, performance, functionality, clinical features, quality of support and service, reputation, brand and price. Our primary competitors are diagnostic imaging system suppliers, which are typically large, multinational companies with far greater financial and technical resources. They also have well-established sales and distribution networks for their products. These companies, including GE, Siemens, and Philips, develop and market medical imaging systems, such as CT and MR equipment, which may be purchased with integrated medical imaging capabilities. Our software works on the products offered by each of these companies. To win business against equipment manufacturers, we must convince customers to buy our solution separately from their purchase of imaging equipment instead of buying integrated systems from our competitors or we must persuade them that introducing our enterprise product throughout their hospitals will provide them with unique benefits not provided by our competitors.

We also face competition from PACS vendors and other suppliers of medical imaging systems and software. PACS companies sometimes provide medical imaging capability in addition to their image archiving and networking products. Some of the diagnostic equipment manufacturers, including GE and Philips, also offer PACS that comprise a large share of the PACS market. Vendors of hospital, clinical and radiology information systems have also diversified into the PACS and medical imaging product lines, either through internal development or business development and partnership channels. These companies, which may be large or small, attempt to offer an integrated system covering a full range of administrative, clinical and radiology information management capabilities to healthcare providers. Other suppliers of medical imaging systems and software, such as TeraRecon, Inc., compete on the basis of volume rendering or other visualization technologies, specific applications or market niches. We are seeing additional competitors enter our market, but have yet to see these competitors attain a meaningful share of the market.

Intellectual Property

We rely primarily on a combination of trade secret and copyright law, employee and third-party nondisclosure agreements and other protective measures to protect intellectual property rights pertaining to our products and technologies. We do not own all of the software and other technologies used in our products, but we believe we have the necessary licenses from third parties to use that technology in our current products. It may be necessary to renegotiate with such third parties for any new versions of current products or any new products. Such third-party licenses may not be available on reasonable terms, or at all.

Governmental Regulation

As medical devices, our software solutions are subject to extensive and rigorous regulation by numerous governmental authorities, principally the U.S. Food and Drug Administration (“FDA”) and corresponding foreign agencies. In the United States, the FDA administers the Federal Food, Drug, and Cosmetic Act, its amendments (the “FD&C Act”) and its related regulations. The FD&C Act and these regulations classify medical devices as Class I, II or III devices, which are subject to general controls, special controls or pre-market approval requirements, respectively. Most Class I and II devices, as well as some Class III devices, can be cleared for marketing pursuant to a 510(k) pre-market notification. The process of obtaining a 510(k) clearance typically can take several months to a year or longer.

Class III devices generally require more stringent clinical investigation and pre-market clearance requirements. In such cases, the FDA will require that the manufacturer submit a pre-market approval (“PMA”) application that must be reviewed and approved by the FDA prior to the sale and marketing of the device in the United States. The process of obtaining a PMA can be expensive, uncertain and lengthy, frequently requiring anywhere from one to several years from the date of FDA submission, if approval is obtained at all. Moreover, a PMA, if granted, may include significant limitations on the indicated uses for which a product may be marketed.

Our software is classified as a Class II medical device and has received marketing clearances from the FDA as the result of 510(k) pre-market notifications. Specifically, our software in general release has been cleared to be marketed for use with CT, MR and PET scanners. Future products, add-on options to existing software, and expanded claims of efficacy will likely require additional 510(k) pre-market notifications.

There can be no assurance that future FDA review processes will not involve delays or that clearances will be granted on a timely basis. In recent years, the FDA has increased its level of scrutiny of medical devices involving software, which requires us to produce additional documentation about the safety and effectiveness of our devices in order to obtain regulatory clearance, and which can lengthen the time required to obtain such clearance. Further, if any of our current or future products become classified as Class III devices, they could be subject to an even more expensive, uncertain and lengthy approval process, and approval, if granted, could include significant limitations on the indicated uses for which a product may be marketed.

We are also subject to regulation in foreign countries in which we sell our products. Many of the regulations applicable to our products in such countries are similar to those of the FDA, but the regulations in several countries, particularly in Asia, may be more particular than those of the FDA, and significantly greater time and resources may be required to obtain approval in those countries. Our ability to successfully market and sell our products in foreign markets depends in large part on our ability to comply with such foreign regulatory requirements. Our products have been Conformité Europeene (“CE”) marked, indicating conformance with applicable sections of the Medical Device Directive 93/42/EEC, as amended by 2007/47/EC, which allows the products to be marketed in the member countries of the European Communities.

We are also subject to periodic inspections by the FDA and similar foreign regulatory agencies, whose primary purpose is to audit our compliance with quality system regulations established by the FDA and other applicable government standards. Regulatory action may be initiated in response to audit deficiencies or product performance problems. We believe that our manufacturing and quality control procedures comply with all applicable requirements of the FDA and foreign regulatory agencies in countries in which we sell our products. We have received and maintain ISO 13485: 2007 Certification.

Medicare and Medicaid laws and regulations may impact the financial arrangements through which we market, sell and distribute our products and services to patients who are Medicare or Medicaid beneficiaries. Violations of these laws and regulations may result in civil and criminal penalties, including substantial fines and imprisonment. In a number of states, the scope of these laws and regulations has been extended to include the provision of services or products to all patients, regardless of the source of payment, although there is variation from state to state as to the exact provisions of such laws or regulations. In other states, and on a national level, several health care reform initiatives have been proposed which would have a similar impact. We believe that our operations and our marketing, sales and distribution practices currently comply with all current applicable fraud and abuse and physician anti-referral laws and regulations.

Employees

As of December 31, 2009, we had 246 full-time employees, with 87 involved in research and development, 70 in sales and marketing, 51 in technical support functions and 38 in administrative functions. We believe our relationship with our employees is good.

Item 1A. Risk Factors

The discussion of our business and operations included in this annual report on Form 10-K should be read together with the risk factors set forth below. They describe various risks and uncertainties to which we are or may become subject. These risks and uncertainties, together with other factors described elsewhere in this report, have the potential to affect our business, financial condition, results of operations, cash flows, strategies or prospects in a material and adverse manner. New risks may emerge at any time, and we cannot predict those risks or estimate the extent to which they may affect financial performance. Each of the risks described below could adversely impact the value of our securities. These statements, like all statements in this report, speak only as of the date of this report (unless another date is indicated), and we undertake no obligation to update or revise the statements in light of future developments.

We offer only one line of products, which is advanced visualization software, related services and hardware, and if our products do not continue to gain market acceptance, our financial results would be adversely affected.

Our current market success depends on our ability to successfully market advanced visualization software for clinical use, and on the ability and willingness of physicians to use enterprise-wide advanced visualization medical imaging software in clinical analysis and therapy planning. Our enterprise-wide advanced visualization software products are alternatives to the conventional methods traditionally used for viewing medical images in the clinical setting. Often, a purchase by a customer of our products means that it has chosen not to utilize software that was provided in connection with the customer’s purchase of a scanner, which means that the customer may pay additional amounts to obtain our products. The acceptance of our products by physicians and other clinicians will depend on our ability to educate those users as to the speed, ease-of-use and other benefits offered by our products and systems, as well as our timely introduction of new features and functions. There can be no assurance that users will prefer advanced visualization and analysis software solutions over less expensive 2D medical imaging software or that we will succeed in our efforts to further develop, commercialize and achieve market acceptance for our products or for any other product in the clinical setting. If our single line of products does not continue to gain market acceptance, our financial results will be adversely affected.

A substantial portion of our revenue is derived from sales of our software in connection with customer purchases of computer tomography, or CT, scanners, and any decline in the purchase of CT scanners or any difficulty we have in growing sales separately from sales of CT scanners could have a material adverse effect on our results of operations and financial condition.

Our business historically was tied to sales of our advanced visualization products on a workstation basis, which were typically purchased concurrently with a customer’s purchase of CT imaging equipment. The market for CT imaging equipment was down significantly in 2009 and is not expected to recover to its past levels within the foreseeable future. In order to improve the marketability of our products separately from sales of CT imaging equipment, during 2008, we evolved our products and business model into sales throughout a customer’s enterprise. We have sold our enterprise-wide advanced visualization products through our direct sales channel since then and began to grow sales of it through our reseller channel during 2009. However, there can be no assurance that sales of our enterprise-wide advanced visualization product through our reseller channel will not remain dependent upon the CT sales cycle, or that such products will be sold by our resellers at the same level as they previously sold our advanced visualization products on a workstation.

We presently depend on Toshiba for a significant portion of our total revenues. A reduction in the business from Toshiba could adversely affect our revenues and could seriously harm our business.

One of our principal distribution channels is to sell our medical imaging software in connection with medical imaging equipment sold by Toshiba. Sales to Toshiba accounted for 54% of our total revenue for the year ended December 31, 2009, 52% of our total revenue for the year ended December 31, 2008 and 47% of our total revenue

for the year ended December 31, 2007. Toshiba’s accounts receivable represented 36% of our accounts receivable at December 31, 2009 and 42% at December 31, 2008. Except for our agreement with Toshiba, we have no significant purchase commitments from any of our customers or business partners, and we generally make sales pursuant to individual transactions. Our joint distribution agreement with Toshiba commenced in 2001 and has been extended multiple times, most recently through December 31, 2013. However, Toshiba does have the ability to conduct in-house development of advanced visualization capabilities for all Toshiba modalities which could lead to a reduction in Toshiba’s need for our products in the future. A reduction, delay, or cancellation of orders from Toshiba, or our inability to collect accounts receivable from Toshiba, likely would have a material adverse effect on our financial condition and operating results.

We operate in a single industry and are therefore dependent upon payer reimbursement rates and market demand for advanced visualization products and services. If reimbursement rates decline or if our market does not grow as we expect, our business, results of operations and financial condition will be adversely affected.

State and federal governmental agencies and private payers are putting pressure on reimbursement rates for advanced visualization examinations, which can negatively affect demand for our products. Many of the major hospitals and medical research centers within the United States have already purchased scanners, PACS and advanced visualization technologies, causing future sales to be upgrades or replacements instead of new installations, potentially lengthening the sales cycles as customers feel less urgency to purchase and implement new systems.

Given the uncertainties associated with the developing stage of many of the geographic and medical specialty markets that we believe represent growth opportunities, there can be no assurance that they will develop in the manner we anticipate or that they will not require a level of investment greater than we expect. Additionally, some of our customers finance their acquisitions through third-party lenders. With the unpredictability of credit availability in the lending market, some customers who would otherwise purchase our products may not be able to obtain sufficient financing and therefore will not complete their purchases. Accordingly, there can be no assurance that the advanced visualization industry will provide growth opportunities for us and our software products or that our business strategies will be successful as the industry continues to evolve. Ultimately, if the advanced visualization industry fails to develop as we expect, our business, results of operations and financial condition will be materially and adversely affected.

Most of our products are used with CT scanning equipment, and are therefore dependent upon the amount of use of CT equipment. If usage of CT equipment is reduced, our business, results of operations and financial condition will be adversely affected.

Most of our products are used with CT scanning equipment, which uses ionizing radiation to generate images of the body. Recently, media and regulatory concern has been directed at the dosage of radiation that may be given to a patient undergoing a CT scan. The optimal radiation dose is “no more or less than what is necessary to produce a high-quality image,” according to a recent FDA white paper. If the current concern results in a reduction in market demand for CT scans, it is likely that the demand for our products could also be reduced. Unless we are successful in developing significant usage for our products other than in connection with CT image data, if the CT equipment manufacturers are unable to develop scanners that produce meaningful data at lower doses of radiation or we are unable to develop software that provides useful images based on the lower dosage levels, our financial results could be adversely affected. Further, recent healthcare regulatory reform seeks to increase the percentage of time of utilization for each scanner that is used in the United States. Utilization reform, while increasing usage of existing scanners, could reduce demand for future scanner purchases, and reduced demand for scanner purchases could materially and adversely affect our business, results of operations and financial condition.

We participate in a highly competitive industry. If we fail to compete effectively, our results of operations and financial condition would be adversely affected.

We face intense competition in the advanced visualization industry. We expect technology to continue to develop rapidly, and our success will depend to a large extent on our ability to maintain a competitive position with our products. Our competitors in the advanced visualization industry include large, established manufacturers of CT and MR imaging equipment. Companies such as GE, Siemens and Philips typically offer their own advanced visualization software and workstations as part of their integrated imaging and scanner systems. Our software works

on the products offered by each of these companies. To win business against equipment manufacturers, we must convince customers to buy our software solutions separately from their purchase of imaging equipment instead of buying integrated systems from our competitors.

In addition to having a competitive advantage in marketing advanced visualization tools as an integrated part of their imaging products, many of our competitors have significantly greater capital and staffing resources for research and development, more recognizable brand names, and more well-established marketing and distribution networks. Although price has been less significant than other factors, increasing competition may result in price reductions and reduced gross margins. Additionally, we face competition from other entities, such as PACS vendors and developers of competitive or ancillary software packages. The advanced visualization market is characterized by rapid innovation and technological change. For example, as scanners become faster and generate increasingly more slices, our software must maintain its capability to handle the increased data volumes generated by such scanners. We may devote time and resources to develop products that do not obtain market acceptance or for which the market is much smaller than we expected when we planned the products. Products developed by our competitors may render our products obsolete or non-competitive. Similarly, our competitors may succeed in developing or marketing products that are viewed as providing superior clinical performance, enterprise access and performance, or are less expensive than our current or future products.

As a result, we may not be able to compete effectively with such manufacturers or competing entities on each or any particular factor, including price, features and service.

As our products are accessed by additional medical professionals throughout an enterprise, the satisfaction of our customers may decrease.

Historically, our products were used by radiologists who received education on the use of imaging products in medical school and continuing education programs and to whom we provided training in connection with their purchases. For radiologists, use of medical imaging products is a relatively routine activity. As our products are used by additional medical professionals throughout an enterprise, they will be used by persons with less training and familiarity with imaging technologies. Occasional and less-trained users of imaging technology may find use of our products to be more difficult than do radiologists, which could increase our time and expenses supporting these users, thus negatively affecting our gross margins for support services. Further, these users may realize less satisfaction than do our historical customers, negatively affecting the adoption of our products elsewhere in the enterprise. Finally, occasional and less-trained users are more likely to use our products incorrectly. Although our products are intended to be secondary analytical devices, their incorrect use could result in errors by medical professionals in their treatment of patients, lowering their satisfaction with our products and potentially exposing us to legal and regulatory liability, which could affect our results of operations and ability to market our products.

We may make future acquisitions, which may be difficult to integrate, divert management resources, result in unanticipated costs or dilute our shareholders.

Part of our continuing business strategy is to evaluate possible acquisitions of, or investments in, companies, products or technologies that complement our current products, enhance our market coverage or technical capabilities, or offer growth opportunities. Future acquisitions could pose numerous risks to our operations, including:

· we may have difficulty integrating the purchased operations, technologies or products;

· we may incur substantial unanticipated integration costs;

· assimilating the acquired businesses may divert significant management attention and financial resources from our other operations and could disrupt our ongoing business;

· acquisitions could result in the loss of key employees, particularly those of the acquired operations;

· we may have difficulty retaining or developing the acquired businesses’ customers;

· acquisitions could adversely affect our existing business relationships with suppliers and customers;

· we may fail to realize the potential cost savings or other financial benefits and/or the strategic benefits of the acquisitions; and

· we may incur liabilities from the acquired businesses for infringement of intellectual property rights or other claims, and we may not be successful in seeking indemnification for such liabilities or claims.

Further, we may not receive the returns from an acquisition that were expected at the time of acquisition. In connection with any acquisition or investment, we could incur debt, be required to amortize expenses related to intangible assets, incur large and immediate write-offs, experience volatility in future earnings resulting from contingent consideration, assume liabilities, or issue stock that would dilute our current shareholders’ percentage of ownership. We may not be able to complete acquisitions or integrate the operations, products or personnel gained through any such acquisition without a material adverse effect on our business, financial condition and results of operations.

We sell our products internationally and are subject to various risks relating to such international activities, which could harm our international sales and profitability.

During the years ended December 31, 2009, 2008 and 2007, 34%, 29% and 19% of our total revenues, respectively, were attributable to international sales. Toshiba has been the primary source of our international sales. We are also developing direct international sales and marketing efforts. By doing business in international markets, we are exposed to risks separate and distinct from those we face in our domestic operations. Our international business may be adversely affected by changing economic conditions in foreign countries. Because most of our sales are currently denominated in U.S. dollars, if the value of the U.S. dollar increases relative to foreign currencies, our products could become more costly to the international consumer and therefore less competitive in international markets, which could adversely affect our profitability. Furthermore, the percentage of sales denominated in non-U.S. currencies may increase in the future, in which case fluctuations in exchange rates could affect demand for our products.

Most of our business in markets outside the United States is provided through third parties with whom we have marketing agreements. There can be no assurance that these third parties will wish to continue our relationships on an indefinite basis or under the same terms as the business is currently conducted. Further, although we have developed direct relationships with customers in markets outside the United States, we may not be successful in doing so at a sufficient level. The loss of or adverse changes in our relationships with our third-party business partners, and our failure to establish sufficient direct relationships with customers outside the United States, would have a material adverse impact on our business, financial condition and results of operations.

Engaging in international business inherently involves a number of other difficulties and risks, including:

· export restrictions and controls relating to technology;

· the availability and level of reimbursement within prevailing foreign healthcare payment systems;

· pricing pressure that we may experience internationally;

· required compliance with existing and new foreign regulatory requirements and laws;

· business customs in other countries that violate U.S. laws, such as the Foreign Corrupt Practices Act;

· laws and business practices favoring local companies;

· longer payment cycles;

· difficulties in enforcing agreements and collecting receivables through foreign legal systems;

· political and economic instability;

· potentially adverse tax consequences, tariffs and other trade barriers;

· international terrorism and anti-American sentiment;

· difficulties and costs of staffing and managing foreign operations;

· changes in currency exchange rates; and

· difficulties in enforcing intellectual property rights.

Our exposure to each of these risks may lower our revenues, increase our costs, lengthen our sales cycle and require significant management attention. We cannot assure you that one or more of these factors will not harm our business.

If our internal control over financial reporting is found to be inadequate, our financial results may not be accurate, raising concerns for investors and potentially adversely affecting our stock price.

Under Section 404 of the Sarbanes-Oxley Act of 2002, we are required to evaluate and determine the effectiveness of our internal controls over financial reporting. We have dedicated a significant amount of time and resources to

ensure compliance with this legislation in recent years and will continue to do so for future periods. We may encounter problems or delays in completing the evaluation, the implementation of improvements, and the receipt of a positive attestation, or any attestation at all, from our independent registered public accounting firm. In addition, our assessment of our internal controls may identify deficiencies that need to be addressed in our internal controls over financial reporting or other matters that may raise concerns for investors as to the accuracy of our reported financial results and adversely affect our stock price.

We may experience fluctuations in operating results, which may result in volatility in the price of our common stock.

We have in the past experienced, and may in the future experience, significant fluctuations in annual and quarterly operating results. If these fluctuations occur, they may result in volatility in the price of our common stock. Quarterly revenue and operating results may fluctuate as a result of a variety of factors that are outside of our control including, but not limited to, the timing of significant orders, the timing of product enhancements and new product introductions by us or our competitors, the pricing of our products, changes in customers’ budgets and competitive conditions. Our quarterly license and services revenue may fluctuate and may be difficult to forecast for a variety of reasons, including the following:

· a significant number of our existing and prospective clients’ decisions regarding whether to enter into license agreements with us are made within the last few weeks or days of each quarter;

· the size and number of license transactions can vary significantly;

· our dependence on Toshiba or any other major customer for a significant portion of our revenues;

· a decrease in license fee revenue which may likely result in a decrease in services revenue in the same or subsequent quarters;

· clients unexpectedly postponing or cancelling projects due to changes in their strategic priorities, project objectives, budget or personnel;

· the uncertainty caused by potential business combinations in the software industry, causing clients and prospective clients to cancel, postpone or reduce capital spending projects on software;

· client evaluations and purchasing processes that vary significantly from company to company, and a client’s internal approval and expenditure authorization process that is difficult and time consuming to complete, even after selection of a vendor;

· the number, timing and significance of software product enhancements and new software product announcements by us or our competitors;

· existing clients declining to renew support for our products, and market pressures that limit our ability to increase support fees or require clients to upgrade from older versions of our products; or

· prospective clients declining or deferring the purchase of new products or releases if we do not have sufficient client references for those products.

We are subject to government regulation of our products, which can result in additional costs or restrict our ability to market our products.

Our products are subject to regulation by the FDA and by comparable agencies in foreign countries. In the United States, the FDA regulates the development, introduction, manufacturing, labeling and record keeping procedures for medical devices, including medical imaging software and systems. Our medical devices require clearance or approval by the FDA before they can be commercially distributed in the United States. Modifications and enhancements to a medical device also require a new FDA clearance or approval if they could significantly affect its safety or effectiveness or would constitute a major change in its intended use, design or manufacture. The FDA requires every manufacturer to make this determination in the first instance, but the FDA may review any manufacturer’s decision and may require a new clearance or approval for the modification if it disagrees with the manufacturer’s decision. If the FDA requires us to seek clearance or approval for the modification of a previously cleared product for which we have concluded that new clearances or approvals are unnecessary, we may be required to cease marketing or to recall the modified product until we obtain clearance or approval, and we may be subject to significant regulatory fines or penalties, which could have a material adverse effect on our financial results and competitive position. The process of obtaining marketing clearance from the FDA for new products and new applications for existing products can be time-consuming and expensive. All of our current products are marketed pursuant to 510(k) pre-market clearance from the FDA. Our products have been cleared to be marketed for use with CT, MR and PET scanners. The FDA may not grant clearance with respect to our future products or enhancements, or future FDA review may involve delays that could adversely affect our ability to market such future products or

enhancements. In addition, the FDA, which is currently under political pressure regarding a handful of products that it cleared over the past few years, including some products that are used for medical imaging, is reviewing the process by which it grants clearance to products. Several of the potential changes could make the process to obtain regulatory clearance more difficult, lengthy and expensive. A more difficult and expensive regulatory clearance process, in addition to potentially causing us to defer or choose not to conduct promising areas of research and development, would by itself slow the time by which products for patient care reach market and could materially and adversely affect our business and results of operations. Further, these changes could affect our products as well as the scanning equipment that produce the data from which our products produce images. If the process becomes more difficult and expensive, medical device manufacturers, including scanning and imaging companies, could increase prices to compensate for the additional risks and costs. Increased prices could further reduce demand for our products, which would materially and adversely affect our business, results of operations and financial condition.

Even if we obtain regulatory clearances and approvals to market a product from the FDA, these approvals may entail limitations on the indicated uses of the product. Product clearances and approvals by the FDA can also be withdrawn due to failure to comply with regulatory standards or the occurrence of unforeseen problems following initial approval. The FDA could also limit or prevent the distribution of our products and has the power to require the recall of such products. FDA regulations depend heavily on administrative interpretation, and future interpretations made by the FDA or other regulatory bodies may adversely affect us. The FDA may inspect our facilities and operations to determine whether we are in compliance with various regulations relating to specification, development, documentation, validation, testing, quality control and product labeling. If the FDA determines that we are in violation of such regulations, it could impose civil penalties, including fines, recall or seize products and, in extreme cases, impose criminal sanctions. If we determine that our facilities, operations or products are not in compliance with FDA requirements, we may voluntarily suspend our operations or recall products.

We market our products both domestically and internationally. International regulatory bodies have established varying regulations governing product standards, packaging requirements, labeling requirements, import restrictions, tariff regulations, duties and tax requirements. Our inability or failure to comply with the varying regulations, or the imposition of new regulations, could restrict our ability to sell our products internationally and could adversely affect our business.

The imposition of requirements under the Health Insurance Portability and Accountability Act of 1996, or HIPAA, could adversely affect our business.

The HIPAA regulations require our customers to observe several requirements for the privacy and security of the protected health information (PHI) of their patients. Although the products and services we provide may technically not be covered under the HIPAA regulations, we may have access to PHI while working with our customers and our customers therefore routinely request that we sign “business associate” agreements with them. A “business associate” is a person or entity that performs certain functions or activities that involve the use or disclosure of protected health information on behalf of, or that provides services to, a covered entity. By law, the HIPAA Privacy Rule applies only to covered entities—health plans, healthcare clearinghouses, and certain healthcare providers. However, most healthcare providers do not carry out all of their healthcare activities and functions by themselves. Instead, they often use the services of a variety of other persons or businesses. The HIPAA Privacy Rule allows covered providers and health plans to disclose protected health information to these “business associates” if the providers or plans obtain satisfactory assurances that the business associate will use the information only for the purposes for which it was engaged by the covered entity, will safeguard the information from misuse, and will help the covered entity comply with some of the covered entity’s duties under the HIPAA Privacy Rule. Covered entities may disclose protected health information to an entity in its role as a business associate only to help the covered entity carry out its healthcare functions—not for the business associate’s independent use or purposes, except as needed for the proper management and administration of the business associate. These agreements are necessary for us in the normal course of servicing and supporting our products and may require us to incur liabilities if we disclose protected health information in a manner not allowed under any respective agreement. Our potential liabilities may include indemnifying our customer against any damages resulting from the disclosure. If we are not willing to or are unable to enter into a business associate agreement with current and potential customers, such customers may not purchase our products or services or discontinue previously-purchased services, which would have a material adverse effect on our business, financial condition, or results of operations.

We are subject to various federal and state “fraud and abuse” laws, and if we are unable to fully comply with such laws, we could face substantial penalties, which may adversely affect our business.

We are subject to various federal and state laws pertaining to health care fraud and abuse, including HIPAA and the following:

· the federal Anti-Kickback Statute, which prohibits persons from knowingly and willfully soliciting, offering, receiving or providing remuneration, directly or indirectly, in cash or in kind, to induce either the referral of an individual, or furnishing or arranging for a good or service, for which payment may be made under federal health care programs (such as Medicare and Medicaid);

· the federal False Claims Act, which prohibits anyone from knowingly presenting or causing to be presented a false or fraudulent claim for payment to the federal government;

· the federal False Statements Statute, which prohibits knowingly and willfully falsifying, concealing or covering up a material fact or making any materially false statement in connection with the delivery of or payment for health care benefits, items or services; and

· state law equivalents to these federal laws, which may not be limited to government reimbursed items, and may not contain identical exceptions.

If our past or present operations are found to be in violation of any of the laws described above or the other similar governmental regulations to which we are subject, we may be subject to the applicable penalty associated with the violation, including civil and criminal penalties, damages, fines, exclusion from federal health care programs and/or the curtailment or restructuring of our operations. Similarly, if the physicians or other providers or entities with which we do business are found to be non-compliant with applicable laws, they may be subject to sanctions, which could also have a negative impact on us. Any penalties, damages, fines, curtailment or restructuring of our operations could adversely affect our ability to operate our business and our financial results. The risk of our being found in violation of these laws is increased by the fact that their provisions are open to a variety of interpretations and are subject to further legal or regulatory change. Any action against us for violation of these laws, even if we successfully defend against it, could cause us to incur significant legal expenses, fines and other penalties, divert our management’s attention from the operation of our business and damage our reputation.

The protection of our intellectual property may be uncertain, and we may face possible claims of others.

Although we have received patents and have filed patent applications with respect to certain aspects of our technology, we generally do not rely principally on patent protection with respect to our products and technologies. Instead, we rely primarily on a combination of trade secret and copyright law, employee and third-party nondisclosure agreements and other protective measures to protect intellectual property rights pertaining to our products and technologies. Such measures may not provide meaningful protection of our trade secrets, know-how or other intellectual property in the event of any unauthorized use, misappropriation or disclosure. Others may independently develop similar technologies or duplicate our technologies. In addition, to the extent that we apply for any patents, such applications may not result in issued patents or, if issued, such patents may not be valid or of value. Third parties could, in the future, assert infringement or misappropriation claims against us with respect to our current or future products and technologies, or we may need to assert claims of infringement against third parties. Any infringement or misappropriation claim by us or against us could place significant strain on our financial resources, divert management’s attention from our business and harm our reputation. The costs of prosecuting or defending an intellectual property claim could be substantial and could adversely affect our business, even if we are ultimately successful in prosecuting or defending any such claims. If our products or technologies are found to infringe the rights of a third party, we could be required to pay significant damages or license fees or cease production, any of which could have a material adverse effect on our business.

We face the risk of product liability claims, and our product liability and errors and omissions insurance coverage may not be adequate to pay products liability claims, which could have a material adverse effect on our financial condition.

Our business exposes us to the risk of product liability claims that is inherent in the manufacturing and marketing of medical devices, including those which may arise from the misuse or malfunction of, or design flaws in, our products. We may be subject to product liability claims if our products cause, or merely appear to have caused, an injury. Claims may be made by patients, healthcare providers or others selling our products. Our product liability

and errors and omissions insurance is subject to deductibles and coverage limitations. Our current product liability insurance may not continue to be available to us on acceptable terms, if at all, and, if available, the coverages may not be adequate to protect us against any future product liability claims. Further, if additional products are approved for marketing, we may seek additional insurance coverage. If we are unable to obtain insurance at an acceptable cost or on acceptable terms with adequate coverages or otherwise protect against potential product liability claims, we will be exposed to significant liabilities, which may harm our business. A product liability claim, recall or other claim with respect to uninsured liabilities or for amounts in excess of insured liabilities could result in significant costs and damage to our reputation and future results, any of which would cause significant harm to our business.

If we fail to attract and retain qualified personnel, our business would be harmed.

Recruiting and retaining talented personnel is critical to our success. There is intense competition from other companies, research and academic institutions, government entities and other organizations for qualified personnel in the areas of our activities. We are located in Minnesota, but compete with companies nationally for employees, particularly those with unique skill sets, and not all potential employees view moving to Minnesota favorably. Further, the pace of change in our industry is rapid, and to keep pace we need to ensure that our existing employees continually upgrade their knowledge and skills. If we fail to identify, attract, retain and motivate these highly skilled personnel, we may be unable to continue our marketing and development activities and may experience interruptions or delays in the execution of our overall business strategy.

We depend on third-party reimbursement. A reduction or other change in reimbursement from third parties could negatively affect our business.

Our products are purchased by hospitals, clinics, imaging centers and other users, which bill various third-party payers, such as government health programs, private health insurance plans, managed care organizations and other similar programs, for the healthcare goods and services provided to their patients. There are currently Current Procedural Terminology, or CPT, reimbursement codes that describe most of the diagnostic procedures that use our products. However, the amount of reimbursement from third-party payers varies by site of service and geographic location and is subject to change. Payers may deny reimbursement if they determine that a product used in a procedure was not used in accordance with established payer protocol regarding cost-effective treatment methods or was used for an unapproved indication. Third-party payers are increasingly challenging the prices charged for medical services and, in some instances, have put pressure on service providers to lower their prices or reduce their services. We are unable to predict what changes will be made in the reimbursement methods used by third-party healthcare payers. Third-party payers may not consider as cost effective the procedures in which our products are used. Reimbursement for such procedures may not be available or, if available, payers’ low reimbursement levels may adversely affect our ability to sell our products on a profitable basis. In addition, there have been and may continue to be changes and proposals by legislators, regulators and third-party payers to curb further these costs in the future. For example, the Deficit Reduction Act of 2005, or the DRA, which was signed into law on February 8, 2006, imposed caps on Medicare payment rates for certain imaging services, including MR and PET, furnished in physicians’ offices and other non-hospital based settings. Under the caps, payments for specified imaging services cannot exceed the hospital outpatient payment rates for these services. Enactment of the DRA appeared to significantly affect one segment of our customer base, the standalone imaging center, and also appeared to reduce demand for imaging products among other segments of our customer base. A failure by hospitals and other users of our products to obtain reimbursement from third-party payers, changes in third-party payers’ policies toward reimbursement for procedures using our products, or legislative action could have a material adverse effect on our business, financial condition and results of operations.

Healthcare reform may negatively impact our business.

The levels of revenue and profitability of medical technology companies may be affected by the efforts of government and third-party payers to contain or reduce the costs of healthcare through various means. In the United States, there has been, and we expect that there will continue to be, a number of federal, state and private proposals to control healthcare costs. These proposals include legislative, regulatory and other initiatives and may contain measures intended to control public and private spending on healthcare as well as to provide universal public access to the healthcare system. If enacted, these proposals may result in a substantial restructuring of the healthcare delivery system. For example, the Congressional Budget Office has issued a report suggesting that radiology benefit managers could require pre-authorization, which could decrease the demand for imaging services. Further, proposals during 2009 included a tax that would be assessed against medical device companies. If such a tax is enacted at

rates discussed at various times, the amount we would owe could be a significant portion of our cash flows from operations. Significant changes in the nation’s healthcare system could have a substantial impact on the manner in which we conduct business and could have a material adverse effect on our business, financial condition and results of operations.

Consolidation in the healthcare industry could lead to demands for price concessions or limit or eliminate our ability to sell to certain of our significant market segments.

The cost of healthcare has risen significantly over the past decade, and numerous initiatives and reforms initiated by legislators, regulators and third-party payers to curb these costs have resulted in a consolidation trend in the medical device industry, as well as among our customers, including healthcare providers. This consolidation has resulted in greater pricing pressures and limitations on our ability to sell to important market segments, as group purchasing organizations, independent delivery networks and large single accounts, such as the Veterans Administration in the United States, continue to consolidate purchasing decisions for some of our healthcare provider customers. We expect that market demand, government regulation, third-party reimbursement policies and societal pressures will continue to change the worldwide healthcare industry, resulting in further business consolidations and alliances which may exert further downward pressure on the prices of our products and adversely impact our business, financial condition and results of operations.

We may incur goodwill impairment charges that adversely affect our operating results.

We review goodwill for impairment annually and more frequently if events and circumstances indicate that the asset may be impaired and that the carrying value may not be recoverable. We operate as one reporting unit and therefore compare our book value to our market value (consisting of market capitalization plus a control premium of 25%). If the market value exceeds the book value, goodwill is generally considered not to be impaired.

Failure of the global economy to recover from the recent downturn, or an extended delay in this recovery, may adversely impact our ability to improve our financial results and grow our business.

We have been affected by the general decline in the global economy, which resulted in contracted capital spending by hospitals and lower interest rates on our cash and investments. Disruptions in the financial markets and the related economic downturn also negatively impacted customer purchasing and payment patterns. Failure of the global economy to recover from this prolonged downturn, or an extended delay in this recovery, may have a material adverse effect on our financial condition and results of operations.

We may issue shares of preferred stock without the consent of our holders of common stock, which could adversely affect the rights of the holders of our common stock.

Our Articles of Incorporation authorize our Board of Directors, without any action by the holders of our common stock, to establish the rights and preferences of up to 5,000,000 shares of currently undesignated preferred stock. These shares of preferred stock could possess voting and conversion rights that could adversely affect the voting power of the holders of the common stock or dilute their ownership rights, and it may have the effect of delaying, deferring or preventing a change in control of Vital Images. No shares of preferred stock or other senior equity securities are currently designated, and currently we have no plan to designate or issue any such securities.

We are subject to certain laws and plans which may discourage takeover attempts that could be beneficial for shareholders.

We are subject to anti-takeover provisions of the Minnesota Business Corporation Act. These provisions may deter or discourage takeover attempts and other changes in control that are not approved by our Board of Directors, and they may have a depressive effect on any market for our stock. As a result, our shareholders may lose opportunities to dispose of their shares at the higher prices typically available in takeover attempts or that may be available under a merger proposal. In addition, these provisions may have the effect of permitting our current directors to retain their positions and place them in a better position to resist changes that our shareholders may wish to make if they are dissatisfied with the conduct of our business.

We have never paid any cash dividends and this practice is expected to continue which means appreciation in our stock price will be our shareholders’ only opportunity to achieve a return on their investment in our common stock.

We have not paid cash dividends on our common stock in the past, and we do not intend to do so in the foreseeable future. Consequently, appreciation in the market price of our common stock and the ability to sell shares at a profit represents our shareholders’ only opportunity to achieve a return on their investment.

Item 1B. Unresolved Staff Comments

None.

Our principal office is located in an office building in Minnetonka, Minnesota, where we currently occupy approximately 72,000 square feet under a lease that expires January 31, 2012. We also lease small offices in Den Haag, the Netherlands, and Beijing, China, for our operations in those countries. We consider our current facilities adequate for our current needs.

We are involved in various claims and legal actions in the normal course of business. We are of the opinion that the outcome of such legal actions will not have a significant adverse effect on our financial position, results of operations or cash flows. Notwithstanding our belief, an unfavorable resolution of some or all of these matters could materially affect our future results of operations or cash flows.

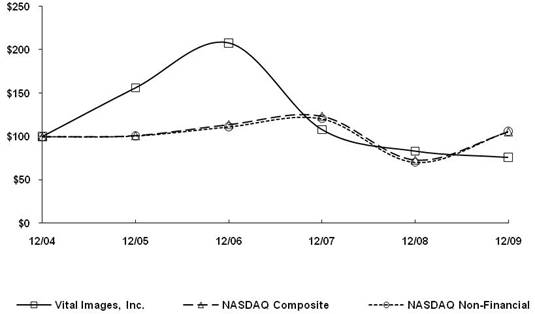

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Vital Images, Inc.’s common stock is quoted on The NASDAQ Global Select Market under the symbol “VTAL.” The table below reflects the high and low per share sale prices of our common stock as reported by The NASDAQ Global Select Market for each of the periods indicated. Such prices reflect inter-dealer prices, do not include adjustments for retail mark-ups, markdowns or commissions, and may not necessarily represent actual transactions.

|

|

|

High |

|

Low |

|

||

|

2009 |

|

|

|

|

|

||

|

Fourth Quarter |

|

$ |

13.18 |

|

$ |

11.35 |

|

|

Third Quarter |

|

$ |

13.75 |

|

$ |

10.19 |

|

|

Second Quarter |

|

$ |

12.25 |

|

$ |

9.64 |

|

|

First Quarter |

|

$ |

14.29 |

|

$ |

8.54 |

|

|

|

|

|

|

|

|

||

|

2008 |

|

|

|

|

|

||

|

Fourth Quarter |

|

$ |

15.24 |

|

$ |

10.23 |

|

|

Third Quarter |

|

$ |

16.95 |

|

$ |

11.86 |

|

|

Second Quarter |

|

$ |

17.13 |

|

$ |

12.43 |

|

|

First Quarter |

|

$ |

18.72 |

|

$ |

13.89 |

|

We have never paid or declared any cash dividends on our common stock and do not intend to pay dividends on our common stock in the foreseeable future. We expect to retain our future anticipated earnings to finance development and expansion of our business. As of February 28, 2010, there were approximately 5,900 beneficial owners and approximately 500 registered holders of record of our common stock.

On May 8, 2008, we announced a share repurchase program of up to $25.0 million of our common stock. On August 7, 2008, we announced additional repurchases of up to $15.0 million of our common stock. On March 3, 2009, we announced additional repurchases of up to 1.0 million shares of our common stock. As of December 31, 2009, we had purchased 3.3 million shares of our common stock for $44.3 million through only open market transactions. The active share repurchase program expires on March 1, 2011.

The following table presents information with respect to purchases of our common stock made during the quarter ended December 31, 2009 by us or our “affiliated purchaser,” as defined in Rule 10b-18(a)(3) under the Securities Exchange Act of 1934.

|

Period |

|

Total Number |

|

Average |

|

Total Number of |

|

Maximum Number of |

|

|

October 1-31, 2009 |

|

— |

|

N/A |

|

— |

|

587,608 |

|

|

November 1-30, 2009 |

|

— |

|

N/A |

|

— |

|

587,608 |

|

|

December 1-31, 2009 |

|

— |

|

N/A |

|

— |

|

587,608 |

|

|

|

|

— |

|

N/A |

|

— |

|

587,608 |

|