Attached files

| file | filename |

|---|---|

| EX-31.2 - EXHIBIT 31.2 - IMPAC MORTGAGE HOLDINGS INC | a2196857zex-31_2.htm |

| EX-31.1 - EXHIBIT 31.1 - IMPAC MORTGAGE HOLDINGS INC | a2196857zex-31_1.htm |

| EX-32.1 - EXHIBIT 32.1 - IMPAC MORTGAGE HOLDINGS INC | a2196857zex-32_1.htm |

| EX-23.1 - EXHIBIT 23.1 - IMPAC MORTGAGE HOLDINGS INC | a2196857zex-23_1.htm |

| EX-10.18 - EXHIBIT 10.18 - IMPAC MORTGAGE HOLDINGS INC | a2196857zex-10_18.htm |

| EX-10.17 - EXHIBIT 10.17 - IMPAC MORTGAGE HOLDINGS INC | a2196857zex-10_17.htm |

| EX-10.17(B) - EXHIBIT 10.17(B) - IMPAC MORTGAGE HOLDINGS INC | a2196857zex-10_17b.htm |

| EX-10.17(A) - EXHIBIT 10.17(A) - IMPAC MORTGAGE HOLDINGS INC | a2196857zex-10_17a.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

- ý

- ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF 1934

For the fiscal year ended December 31, 2009 or

- o

- TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to .

Commission File Number: 1-14100

IMPAC MORTGAGE HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| Maryland (State or other jurisdiction of incorporation or organization) |

33-0675505 (I.R.S. Employer Identification No.) |

19500 Jamboree Road, Irvine, California 92612

(Address of principal executive offices)

(949) 475-3600

(Registrant's telephone

number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class

|

Name of each exchange on which registered

|

|

| Common Stock, $0.01 par value | NYSE Amex |

Securities registered pursuant to Section 12(g) of the Act: none

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of the Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company ý |

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2) Yes o No ý

As of June 30, 2009, the aggregate market value of the voting stock held by non-affiliates of the registrant was approximately $7.6 million, based on the closing sales price of common stock on the Pink OTC Markets, Inc. (formerly, Pink Sheets) on that date. For purposes of the calculation only, all directors and executive officers of the registrant have been deemed affiliates. There were 7,698,146 shares of common stock outstanding as of March 16, 2010. The registrant's common stock commenced trading on the NYSE Amex on December 29, 2009. Prior to that, the common stock was quoted on the Pink OTC Markets, Inc.

IMPAC MORTGAGE HOLDINGS, INC.

2009 FORM 10-K ANNUAL REPORT

TABLE OF CONTENTS

IMPAC MORTGAGE HOLDINGS, INC.

2009 FORM 10-K ANNUAL REPORT

TABLE OF CONTENTS

Impac Mortgage Holdings, Inc. (the Company or IMH) is a Maryland corporation incorporated in August 1995 and has the following subsidiaries: Integrated Real Estate Service Corporation (IRES), IMH Assets Corp. (IMH Assets), Impac Warehouse Lending Group, Inc. (IWLG) and Impac Funding Corporation (IFC).

This report on Form 10-K contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements, some of which are based on various assumptions and events that are beyond our control, may be identified by reference to a future period or periods or by the use of forward-looking terminology, such as "may," "will," "believe," "expect," "likely," "should," "could," "seem to," "anticipate," or similar terms or variations on those terms or the negative of those terms. The forward-looking statements are based on current management expectations. Actual results may differ materially as a result of several factors, including, but not limited to the following: the ongoing volatility in the mortgage industry; our ability to successfully manage through the current market environment; our ability to meet liquidity needs from current cash flows or generate new sources of revenue; management's ability to successfully manage and grow the Company's mortgage and real estate fee-based business activities; the ability to make interest payments; increases in default rates or loss severities and mortgage related losses; the ability to satisfy conditions (payment and covenants) in the note payable with a major creditor; our ability to obtain additional financing and the terms of any financing that we do obtain; inability to effectively liquidate properties to mitigate losses; increase in loan repurchase requests and ability to adequately settle repurchase obligations; decreases in value of our residual interests that differ from our assumptions; the ability of our common stock to continue trading in an active market; the outcome of litigation or regulatory actions pending against us or other legal contingencies; our compliance with applicable local, state and federal laws and regulations and other general market and economic conditions.

For a discussion of these and other risks and uncertainties that could cause actual results to differ from those contained in the forward-looking statements, see Item 1A. "Risk Factors" and Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations" in this report. This document speaks only as of its date and we do not undertake, and specifically disclaim any obligation, to publicly release the results of any revisions that may be made to any forward-looking statements to reflect the occurrence of anticipated or unanticipated events or circumstances after the date of such statements.

Our Internet website address is www.impaccompanies.com. We make available our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and proxy statements for our annual stockholders' meetings, as well as any amendments to those reports, free of charge through our website as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission, or "SEC." You can learn more about us by reviewing our SEC filings on our website by clicking on "Stockholder Relations" located on our home page and proceeding to "Financial Reports." We also make available on our website, under "Corporate Governance," charters for the audit, compensation, and governance and nominating committees of our board of directors, our Code of Business Conduct and Ethics, our Corporate Governance Guidelines and other company information, including amendments to such documents and waivers, if any to our

1

Code of Business Conduct and Ethics. These documents will also be furnished, free of charge, upon written request to Impac Mortgage Holdings, Inc., Attention: Stockholder Relations, 19500 Jamboree Road, Irvine, California 92612. The SEC also maintains a website at www.sec.gov that contains reports, proxy statements and other information regarding SEC registrants, including the Company.

During 2009, the Company continued to implement steps to restructure its debt obligations and establish new lines of business in building an integrated mortgage services platform that provides solutions to the mortgage and real estate markets.

The Company continued to improve its liquidity by successfully restructuring its debt obligations in 2009 by both settling and exchanging several significant liabilities, including:

- •

- The Company purchased and canceled $28.5 million in outstanding trust preferred securities for $4.3 million.

Additionally, the Company exchanged an aggregate of $51.3 million in trust preferred securities for junior subordinated notes with an aggregate principal balance of $62.0 million. Under

the terms of the exchange, the interest rate for each note was reduced from the original 8.01 percent to 2.00 percent through 2013 with increases of 1.00 percent per year through

2017, at which point they become variable at 3-month LIBOR plus 375 basis points. Through December 31, 2009, the Company has successfully settled or restructured

$87.8 million of the original $96.3 million in trust preferred securities issued, reducing its annual interest expense obligation from $7.8 million to approximately

$2.0 million.

- •

- The Company completed the purchase of 4,378,880 shares of its preferred stock, representing a liquidation value of

$109.5 million, for $1.3 million plus $7.4 million in accumulated but unpaid dividends. In connection with the purchase, the Company eliminated its $14.9 million annual

preferred dividend obligation.

- •

- The Company entered into a settlement agreement (the Settlement Agreement) with its remaining reverse repurchase facility lender to settle its remaining restructured reverse repurchase line. The agreement retired this facility and removed any further exposure associated with the line or the loans that secured the line. Pursuant to the terms of the settlement agreement, the Company settled the $140.0 million balance of the restructured reverse repurchase line by (i) transferring the loans securing the line to the lender at their approximate carrying values, (ii) making a cash payment of $20.0 million and (iii) entering into a credit agreement (the Credit Agreement) with the lender for a $33.9 million term loan, which is to be paid over 18 months.

The Company also initiated various mortgage and real estate fee-based business activities, including loss mitigation, real estate disposition, monitoring and surveillance services, real estate brokerage and lending services and title and escrow services. The Company has been able to develop and enhance its service offerings in providing services to investors, servicers and individual borrowers primarily by focusing on loss mitigation and performance of our own long-term mortgage portfolio. These services have currently generated fees primarily from the Company's long-term mortgage portfolio and to a lesser extent from the marketplace, but we intend to expand service offerings to the marketplace. The development of these business activities focuses on vertical integration of a centralized platform which we believe we can operate synergistically to maximize their success.

The information contained throughout this document is presented on a continuing basis, unless otherwise stated.

2

The economy continued to contract during 2009 before showing modest signs of improvement toward the end of the year. The current economic environment, considered the worst recession on record since the Great Depression, continues to adversely affect the credit performance of the Company's long-term mortgage portfolio. The economy remains weak, as evidenced by many key economic indicators. Notably, the national unemployment rate increased to 10.1% in October 2009 before declining to 10.0% at the end of the fourth quarter and 9.7% at January 2010. Higher unemployment and weaker overall economic conditions have led to a significant increase in the number of loan defaults, while continued weak housing prices have driven a significant increase in loan loss severities. Activity in the housing sector increased, with new home construction picking up for the first time in three and a half years. Home price appreciation, housing starts and home sales began to exhibit some modest signs of recovery during the second half of the year. Inflation remained low, and the Federal Reserve indicated that the federal funds rate would likely remain low for an "extended period," reiterating its intent to continue to use a wide range of tools to promote economic recovery and maintain price stability.

The Federal Reserve and U.S. government have undertaken certain initiatives during the year to strengthen the capital of financial institutions, promote lending, and inject liquidity into the financial markets. The U.S. government has also developed programs to incent lenders and servicers to provide loan modifications to troubled borrowers in an effort to fight the foreclosure crisis. However, mortgage delinquencies and foreclosures continued to increase in both the prime and subprime loan markets. The level of defaults and the national unemployment rate remain high, which creates some uncertainty about the strength or duration of any recovery. Additional deterioration in the overall economic environment, including continued weakening of the labor market, could cause loan delinquencies to increase beyond the Company's current expectations, resulting in additional increases in losses and reductions in fair value.

Should defaults continue to remain elevated, as the economy and housing market continues to struggle, the credit performance of the Company's long-term mortgage portfolio may continue to be negatively affected by these economic conditions. Delinquencies and nonperforming loans and assets continue to remain at elevated levels, although we have begun to see some stabilization along with significant decreases in REOs. In addition, borrowers with significant negative equity and the ability to pay their mortgage payments are intentionally defaulting, called strategic defaults, because they believe that home prices will not recover in a reasonable amount of time. Additional deterioration in the overall economic environment, including continued deterioration in the labor market, could cause delinquencies to increase beyond the Company's current expectations, resulting in additional increases in losses and reductions in fair value.

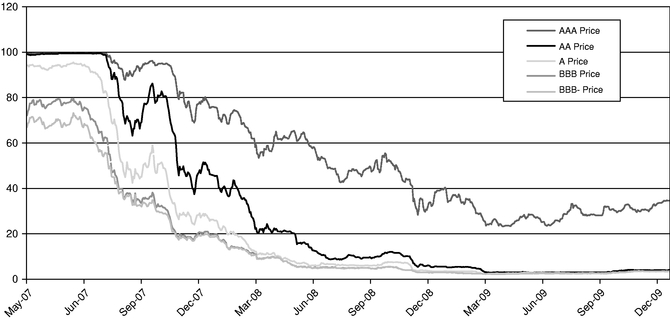

We believe there is currently no index for Alt-A mortgage products, but the general direction and magnitude of price movement in the ABX 2007-1index is reflective of the disruption in the market and general price movement experienced by the Company's securities. The index, which does not include any IMH bonds, is being used for illustrative purposes only because it is a non-conforming single-family mortgage index that has traded consistently in recent years. The ABX 2007-1 Index illustrates market prices for designated groups of subprime securities by credit rating. The index is shown here as an illustration of the price volatility in the general non-conforming subprime mortgage market since the beginning of 2007 and does not reflect actual pricing on IMH bonds, which are backed by Alt-A loans rather than subprime loans. As shown below, the ABX 2007-1 Index displays dramatic declines in the value of such securities.

3

Effects of Recent Market Activity

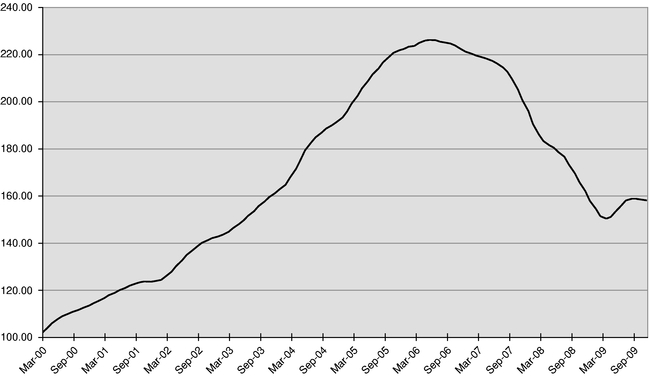

As a result of the Company's inability to sell or securitize non-conforming loans during the second half of 2007, the Company discontinued funding loans and discontinued substantially all of its mortgage (non-conforming single-family loans and commercial loans, which consist primarily of multifamily loans) and warehouse lending operations. Market conditions deteriorated in 2008 and continued to be depressed in 2009. As a result, the Company's investment in securitized non-conforming loans (residual interests) has been affected by the increase in estimated defaults and severities, evidenced by significant home price depreciation. The decline in single-family home prices can be seen in the chart below.

4

As depicted in the chart above, average home prices peaked in June 2006 at 226.29 and continued their dramatic decline through much of the first half of 2009, while increasing slightly over the remaining half of the year. The Standard & Poor's Case-Shiller 10-City Composite Home Price Index (the Index) for December 2009 was 158.18 (with the base of 100.00 for January 2000) and hasn't been this low since October 2003 when the Index was 157.71. Beginning in the third quarter of 2007, the Company began to believe that there was a correlation between the borrowers' perceived equity in their homes and defaults. The original loan-to-value (defined as loan amount as a percentage of collateral value, "LTV") and original combined loan-to-value (defined as first lien plus total subordinate liens to collateral value, "CLTV") ratios of single-family mortgages remaining in the Company's securitized mortgage collateral as of December 31, 2009 was 73 percent and 82 percent, respectively. The current LTV and CLTV ratios likely increased from origination date as a result of the deterioration in the real estate market. We believe that home prices that have declined below the borrower's original purchase price have a higher risk of default within our portfolio. Based on the Index, home prices have declined 30 percent through December 2009 from the 2006 peak. Further, we believe the home prices in general within California and Florida, the states with the highest concentration of our mortgages, have declined even further than the Index. We have considered the deterioration in home prices and its impact on our loss severities, which are a primary assumption used in the valuation of securitized mortgage collateral and borrowings.

In response to the current market environment, during 2009, the Company initiated various fee-based business activities to provide solutions to the mortgage and real estate markets, including loss mitigation services such as loan modifications, real estate disposition and portfolio monitoring and surveillance services.

5

The Company's continuing operations include the mortgage and real estate fee-based business activities conducted by IRES and the long-term mortgage portfolio (residual interests in securitizations reflected as net trust assets and liabilities in the consolidated balance sheets).

Mortgage and real estate services

In 2009, the Company has sought to create an integrated services platform to provide solutions to the mortgage and real estate markets. Pursuant to that, the Company initiated various mortgage and real estate fee-based business activities, including loan modifications, real estate disposition, monitoring and surveillance services, real estate brokerage, mortgage lending, and title and escrow services. The Company has been able to develop and enhance its service offerings in providing services to investors, servicers and individual borrowers primarily by focusing on loss mitigation and performance of our own long-term mortgage portfolio. The development of these business activities focuses on vertical integration of a centralized platform which we believe we can operate synergistically to maximize their success. The Company has established the following business activities:

- •

- Loss Mitigation—The Company has established loss mitigation

operations to provide outsourced services including loan modification and short sale services to investors and institutions with distressed and delinquent residential and multifamily mortgage

portfolios. In addition, we provide modification solutions to individual borrowers by interacting with loan servicers on behalf of the borrowers to assist them in lowering the monthly mortgage

payments to an affordable level allowing them to remain in their homes. The Company receives fees paid by the borrower for loan modification services performed for the borrower.

- •

- Real Estate Solutions—The Company has established real estate

solutions operations to provide real estate owned (REO) surveillance services to servicers and portfolio managers to assist them in maximizing loss mitigation performance in managing distressed

mortgage portfolios and foreclosed real estate assets, along with disposition of such assets. In addition, we perform default surveillance and monitoring services for residential and multifamily

mortgage portfolios for investors and servicers to assist them with overall portfolio performance.

- •

- Real Estate Brokerage—The Company has established real estate

brokerage operations which primarily serves the southern California area. The primary business of the real estate brokerage business is the listing and selling of REO and pre-foreclosure

properties associated with short sales.

- •

- Mortgage Lending Operations—The Company has established

mortgage lending operations as it seeks to re-enter the mortgage lending industry. The mortgage lending activities include earning fees for brokering loans to third-party lenders since

2008 and originating loans through our mortgage banking platform under the "Impac" brand name. Although we originated only a minimal amount of loans in 2009, we expect to increase our loan

originations in 2010 through retail channels, real estate broker channels and captive financing from the Company's portfolio of transactions, focusing on originating only loans that are eligible for

sale to HUD and other government-sponsored enterprises.

- •

- Title and Escrow—During the fourth quarter of 2009, the Company received California Department of Insurance approval for our acquisition of a title insurance agency and escrow operations. Upon the approval, the Company acquired the operations effective December 31, 2009. The title insurance company services California and selected national markets to provide

6

title insurance, escrow and settlement services to residential mortgage lenders, real estate agents, asset managers and REO companies in the residential market sector of the real estate industry. We deliver services through a proprietary integrated technology platform.

For the year ended December 31, 2009, mortgage and real estate services fees were $42.6 million. Although the Company intends to attempt to generate more fees by expanding its services to third parties in the marketplace in the near future, the revenues from these business activities have primarily been generated from the Company's long-term mortgage portfolio. Furthermore, since these business activities are newly established, there remains uncertainty about their future success.

Master Servicing

We have retained master servicing rights on substantially all of our non-conforming single-family residential and commercial mortgage acquisitions and originations that we retained or sold through securitizations. Our function as master servicer includes collecting loan payments from loan servicers and remitting loan payments, less master servicing fees receivable and other fees, to a trustee or other purchaser for each series of mortgage-backed securities or mortgages master serviced. In addition, as master servicer, we monitor compliance with our servicing guidelines and perform, or contract with a third party to perform, all obligations not adequately performed by any loan servicer. We are also required to advance funds or cause our loan servicers to advance funds to cover principal and interest payments not received from borrowers depending on the status of their mortgages. We also earn income or incur expense on principal and interest payments we receive from borrowers until those payments are remitted to the investors of those mortgages. Master servicing fees are generally 0.03 percent per annum on the unpaid principal balance of the mortgages serviced. Cash flows from master servicing has declined significantly due to a decrease in principal balances and a decline in interest rates since the end of 2008, which affects the amount we earn on balances held in custodial accounts. At December 31, 2009, we were the master servicer for approximately 51,700 mortgages with a principal balance of approximately $14.5 billion. At December 31, 2009, the Company's master servicing solely for unconsolidated securitizations included approximately $2.0 billion in servicing of which $0.6 billion of those loans were more than 60 days past due from the previous due date.

Real Estate Advisory Agreement

During 2008, the Company entered into an agreement with a real estate marketing company to generate advisory fees. The real estate marketing company specialized in the marketing of foreclosed properties. During the year, the Company earned $18.4 million in real estate advisory fees plus a $27.0 million fee for agreeing to terminate this relationship in the fourth quarter of 2008.

Long-Term Mortgage Portfolio

The long-term mortgage portfolio consists of the residual interest in securitizations represented on the consolidated balance sheet as the difference between trust assets and trust liabilities.

The long-term mortgage portfolio includes adjustable rate and, to a lesser extent, fixed rate Alt-A single-family residential mortgages and commercial (primarily multifamily) mortgages that were acquired and originated by the Company. Alt-A mortgages are primarily first lien mortgages made to borrowers whose credit is generally within typical Fannie Mae and Freddie Mac guidelines, but have loan characteristics that make them non-conforming under those guidelines.

For instance, Alt-A mortgages frequently may have had loan balances in excess of maximum Fannie Mae and Freddie Mac lending limits and may not have certain documentation or verifications that

7

are required by Fannie Mae and Freddie Mac and, therefore, in making our credit decisions, we were more reliant upon the borrower's credit score and the adequacy of the underlying collateral.

Commercial mortgages (consisting primarily of multifamily residential loans) in the long-term mortgage portfolio are primarily adjustable rate mortgages with initial fixed interest rate periods of two-, three-, five-, seven- and ten-years that subsequently convert to adjustable rate mortgages, or (hybrid ARMs). Commercial mortgages have interest rate floors, which are the initial start rate, in some circumstances, lock out periods and prepayment penalty periods of three-, five- seven- and ten-years. Commercial mortgages have provided greater asset diversification on our balance sheet as borrowers of commercial mortgages typically have higher credit scores and commercial mortgages typically have a lower LTV.

The non-conforming single-family residential and commercial mortgages that we retained were primarily adjustable rate mortgages, or "ARMs," hybrid ARMs and fixed rate mortgages, or "FRMs." The interest rate on ARMs are typically tied to an index, usually the six-month London Interbank Offered Rate, or "LIBOR," plus a spread and adjust periodically (typically semi-annually), subject to lifetime interest rate caps and periodic interest rate and payment caps. The initial interest rates on ARMs are typically lower than average comparable FRMs but may be higher than average comparable FRMs over the life of the mortgage. Hybrid ARMs are mortgages with maturity periods ranging from 15 to 30 years with initial fixed interest rate periods generally ranging from two to ten years, which subsequently adjust to ARMs. The majority of mortgages retained by the long-term investment operations have prepayment penalty features with prepayment penalty periods ranging from six months to seven years. Prepayment penalties may be assessed to the borrower if the borrower refinances or, in some cases, sells the home.

Historically, the Company securitized mortgages in the form of collateralized mortgage obligations (CMOs), which were consolidated and accounted for as secured borrowings for financial statement purposes. Securitized mortgages in the form of real estate mortgage investment conduits (REMICs), were either consolidated or unconsolidated depending on the design of the securitization structure. CMO and certain REMIC securitizations were designed so that the transferee (securitization trust) was not a qualifying special purpose entity (QSPE), and therefore the Company consolidated the variable interest entity (VIE) as it was the primary beneficiary of the sole residual interest in each securitization trust. Generally, this was achieved by including terms in the securitization agreements that gave the Company the ability to unilaterally cause the securitization trust to return specific mortgages, other than through a clean-up call. Amounts consolidated are included in trust assets and liabilities as securitized mortgage collateral, real estate owned, derivative assets, securitized mortgage borrowings and derivative liabilities in the accompanying consolidated balance sheets.

Effective January 1, 2010, former QSPEs are evaluated for consolidation based on the provisions of FASB ASC 810-10-25, which eliminates the concept of a QSPE and changes the approach to determining a securitization trust's primary beneficiary. Refer to Note A-17—Recent Accounting Pronouncements in the notes to the consolidated financial statements for a discussion of the impact these new rules will have on the Company's consolidated balance sheets.

During 2009 and 2008, the Company did not acquire or retain any mortgages in the portfolio.

For additional information regarding the long-term mortgage portfolio refer to Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations," Note C "Securitized Mortgage Collateral" and Note F "Securitized Mortgage Borrowings" in the notes to the consolidated financial statements.

8

Discontinued operations primarily include minimizing or settling repurchase liability exposure and managing the lease liabilities related to our former non-conforming mortgage operations.

In previous years, when our discontinued operations sold loans to investors, we were required to make normal and customary representations and warranties about the loans we had previously sold to investors. Our whole loan sale agreements generally required us to repurchase loans if we breached a representation or warranty given to the loan purchaser. In addition, we also could be required to repurchase loans as a result of borrower fraud or if a payment default occurs on a mortgage loan shortly after its sale. The Company continues to attempt to settle outstanding repurchase requests from third-party investors.

In connection with the discontinuation of our non-conforming mortgage, retail mortgage, warehouse lending and commercial operations, a significant amount of office space that was previously occupied is no longer being used by the Company. Since the discontinuation of these operations, the Company has sought to reduce its liability by subleasing a significant amount of this office space.

Under our mortgage lending and real estate brokerage operations, we have established underwriting guidelines that include provisions for inspections and appraisals, required credit reports on prospective borrowers and determined maximum loan amounts. Our mortgage lending activities are subject to, among other laws, the Equal Credit Opportunity Act, Federal Truth-in-Lending Act, Fair Credit Reporting Act, Fair and Accurate Credit Transaction Act, Fair Housing Act, Gramm-Leach, Bliley Act, Telephone Consumer Protection Act, Can Spam Act, Real Estate Settlement Procedures Act, Home Mortgage Disclosure Act, the Fair Debt Collection Practices Act, the Secure and Fair Enforcement for Mortgage Licensing Act of 2008, and the regulations promulgated thereunder. These laws and regulations, among other things, prohibit discrimination and require the disclosure of certain basic information to mortgagors concerning credit terms and settlement costs, prohibit the payment of kickbacks for the referral of business incident to a real estate settlement service, limit payment for settlement services to the reasonable value of the services rendered and goods furnished, restrict the marketing practices we used to find customers, require us to safeguard non-public information about our customers and require the maintenance, disclosure of information regarding the disposition of mortgage applications based on race, gender, geographical distribution, price and income level and established national minimum standards for mortgage licenses. Our mortgage lending, real estate brokerage and title and escrow activities are also subject to state and local laws and regulations, including state licensing laws, anti-predatory lending laws, and may also be subject to applicable state usury statutes. Our mortgage lending operation is an approved Housing and Urban Development "HUD" lender. As a HUD approved lender and if we become an approved Fannie Mae seller/servicer and Freddie Mac servicer, we are and will be required to submit annually to Fannie Mae, Freddie Mac, and HUD, as applicable, audited financial statements, or the equivalent, according to the financial reporting requirements of each regulatory entity for its sellers/ servicers. Our affairs will also be subject to examination by Fannie Mae and Freddie Mac at any time to assure compliance with applicable regulations, policies and procedures. Also refer to "Regulatory Risks" under Item 1A. Risk Factors for a further discussion of regulations that may affect our Company.

We operate in a highly competitive industry that could become even more competitive as a result of legislative, regulatory, economic, and technological changes, as well as continued consolidation. Our competitors include banks, thrifts, credit unions, real estate brokerage firms, title and escrow

9

companies, and mortgage banking companies. Competition is based on a number of factors including, among others, customer service, quality and range of products and services offered, price, reputation, interest rates, lending limits and customer convenience. To compete effectively, we must have a very high level of operational, technological, and managerial expertise, as well as access to capital at a competitive cost. As a result of reduced access to capital, general housing trends, rising delinquencies and defaults and other factors, many mortgage and real estate services firms have recently experienced severe financial difficulty, with some exiting the business or filing for bankruptcy protection.

Our mortgage and real estate fee-based business activities compete with firms that provide similar services, including loan modification companies, real estate asset management and disposition companies, real estate brokerage firms and title and escrow companies.

Risk factors, as outlined below, provide additional information related to risks associated with competition in the mortgage, real estate services and title and escrow industries.

As of December 31, 2009 and 2008, we had a total of 299 and 127 full-time and part-time employees, respectively. Management believes that relations with its employees are good. We are not a party to any collective bargaining agreements.

Some of the following risk factors relate to a discussion of our assets. For additional information on our asset categories refer to Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations," as well as the accompanying notes to the consolidated financial statements.

Risks Related To Our Businesses

If we fail to generate new sources of revenue successfully, our business, financial condition and results of operations could be materially and adversely affected.

Since 2007, management has been challenged by the unprecedented turmoil in the mortgage market, including significant increases in delinquencies and foreclosures and significant increases in credit-related losses. In response, the Company discontinued its non-conforming mortgage and retail operations, its commercial operations and warehouse lending operations in 2007, and during 2008 and 2009 (i) terminated all of its reverse repurchase financings, except for one, which was restructured, (ii) reduced and restructured its trust preferred payment obligations, (iii) settled a significant portion of its outstanding loan repurchase claims, and (iv) eliminated its preferred stock dividends. Although these actions have decreased our debt obligations, certain others have caused a reduction in our cash and overall liquidity.

In light of the continuing turmoil in the mortgage market, our ability to continue our operations is dependent upon our ability to successfully initiate new sources of revenue, such as our mortgage and real estate fee-based business activities that we established during 2009, and re-enter the mortgage lending industry, which may include acquiring new operations, that contribute sufficient additional cash flow to enable us to generate net revenue to meet our current and future expenses. Our future financial performance and success are dependent in large part upon our ability to implement and maintain our mortgage and real estate fee-based business activities and mortgage lending operations successfully. The mortgage and real estate services market is volatile and highly competitive. The Company's ability to successfully compete in the mortgage and real estate services market is uncertain as these

10

operations are newly established. Our business will be materially affected if we are unable to generate sufficient liquidity to conduct our operations as planned.

Our ability to acquire new businesses is significantly constrained by our limited liquidity and our likely inability to obtain financing or to issue equity securities as a result of our current financial condition and current market conditions, as well as other uncertainties and risks. There can be no assurances that we will be able to initiate or acquire new business operations. We may not be able to implement and maintain our new business operations successfully or achieve the anticipated benefits of their implementation. If we are unable to do so, we may be unable to satisfy our future operating costs and liabilities, including repayment of our note payable and long-term debt.

Our long-term liquidity is dependent on our ability to grow and maintain new businesses.

The ability to meet our long-term liquidity requirements is subject to several factors, such as realizing cash flows from our long-term mortgage portfolio and generating fees from our newly established mortgage and real estate fee-based business activities. Our future financial performance and success are dependent in large part upon our ability to grow our mortgage and real estate fee-based business activities. We believe that current cash balances, short-term investments, cash flows realized from our long-term mortgage portfolio and fees generated from our mortgage and real estate fee-based business activities will be adequate to fund our current operations and liabilities. At December 31, 2009, our debt obligations, consisting of our trust preferred securities, junior subordinated notes, and the note payable related to the Settlement Agreement, was an aggregate of approximately $101.6 million in outstanding principal balance. We cannot provide any assurances that we will be able to operate successfully our new mortgage and real estate fee-based business activities and other business that we may implement in the future. If we are unable to do so, we may be unable to satisfy our future operating costs and liabilities, including repayment of our note payable and long-term debt.

Deteriorating mortgage market conditions have had and may continue to have a material adverse effect on our earnings and financial condition.

Our results of operations are materially affected by conditions in the mortgage and real estate markets, the financial markets and the economy generally. Beginning in 2007, the mortgage industry and the single-family residential housing markets, and to a lesser extent multifamily residential, were adversely affected as home prices declined and delinquencies and defaults significantly increased. Borrowers have found it difficult to refinance due to home price depreciation and lenders tightened their underwriting guidelines, which has led to further increases in defaults and credit losses. During 2009, the Company continued to be significantly and negatively affected by the deteriorating real estate market and the weak economic environment. As a result, non-conforming mortgage loans have not performed up to historical expectations, and the fair value of non-conforming mortgage loans has deteriorated. This, in turn, has resulted in declining revenues and increased expenses, including significant increases in loan losses and impairment charges, losses sustained in the operation of real estate properties acquired in foreclosure proceedings and foreclosure related professional fees. These factors have led to continued deterioration in the quality of the Company's long-term mortgage portfolio, as evidenced by the continued increases in delinquencies, foreclosures and credit losses.

The disruption in the capital markets and secondary mortgage markets has also reduced liquidity and investor demand for mortgage loans and mortgage backed securities, while yield requirements for these products has increased. The increased defaults on residential mortgage loans, increases in the number of ratings downgrades with respect to bonds issued in connection with securitized loans, lack of liquidity in the bond market and the financial condition of many companies that typically participate in this market have negatively affected our ability to operate our business. Continuing concerns about the declining real estate market, as well as inflation, energy costs, geopolitical issues and the availability and

11

cost of credit, have contributed to increased volatility and diminished expectations for the economy and markets going forward. The mortgage market has been severely affected by changes in the lending landscape and there is no assurance that these conditions have stabilized or that they will not worsen. These unprecedented disruptions and deterioration of the mortgage market, have had, and may continue to have, an adverse effect on the Company's earnings and financial condition.

Difficult market conditions have already affected our industry and may continue to adversely affect us.

Reflecting concern about the stability of the financial markets generally and the strength of counterparties, many lenders and institutional investors have reduced or ceased providing funding to borrowers, including other financial institutions. This market turmoil and tightening of credit have led to an increased level of commercial and consumer delinquencies, lack of consumer confidence, increased market volatility and widespread reduction of business activity generally. The resulting economic pressure on consumers and lack of confidence in the financial markets has already adversely affected our industry and may continue to adversely affect our business, financial condition and results of operations. We do not expect that the difficult conditions in the financial markets are likely to improve in the near future. A worsening of these conditions would likely exacerbate the adverse effects of these difficult market conditions on us and others in the financial institutions industry. In particular, we may face the following risks in connection with these events:

- •

- We expect to face increased regulation of our industry. Compliance with such regulation may increase our costs and limit

our ability to pursue business opportunities.

- •

- Our ability to assess the creditworthiness of our customers may be impaired if the models and approaches we use to select,

manage, and underwrite our customers become less predictive of future behaviors.

- •

- The processes we use to estimate losses inherent in our credit exposure requires difficult, subjective, and complex

judgments, including forecast of economic conditions and how these economic conditions might impair the ability of our borrowers to repay their loans, which may no longer be capable of accurate

estimation and which may, in turn, impact the reliability of the processes.

- •

- Our ability to borrow from financial institutions or to engage in sales of mortgage loans to third parties (including

mortgage loan securitization transactions with government-sponsored entities) on favorable terms or at all could be adversely affected by further disruptions in the capital markets or other events,

including deteriorating investor expectations.

- •

- Competition in our industry could intensify as a result of increasing consolidation of financial services companies in

connection with current market conditions.

- •

- Higher credit losses because of federal or state legislation or regulatory action that either (i) reduces the amount that our borrowers are required to pay us, or (ii) limits our ability to foreclose on properties or collateral or makes foreclosures less economically viable. In particular, there is legislation pending in the U.S. Congress that would allow a Chapter 13 bankruptcy plan to "cram down" the value of certain mortgages on a consumer's principal residence to its market value and/or reset debtor interest rate and monthly payments to an amount that permits them to remain in their homes.

12

If defaults on our mortgage loans continue, it will result in continuing declines in revenues and net income.

Loan defaults result in a decrease in interest income and an increase in loan losses. The decrease in interest income resulting from loan defaults may be for a prolonged period of time as we seek to recover, primarily through legal proceedings, the outstanding principal balance and accrued interest due on a defaulted loan, plus the legal costs incurred in pursuing our legal remedies. Legal proceedings, which may include foreclosure actions and bankruptcy proceedings, are expensive and time consuming. The decrease in interest income, the costs incurred from defaulted loans and increases in loan losses will have an adverse impact on our liquidity, net income and shareholders' equity.

The adverse market conditions have negatively affected our mortgage loan delinquencies and real estate owned (REO). At December 31, 2009, the Company's mortgage portfolio had 25.1 percent or $3.1 billion of loans that were 60 days or more delinquent, included in continuing and discontinued operations, compared to 22.7 percent or $3.5 billion at December 31, 2008. REO decreased 76.2 percent to $142.7 million at December 31, 2009 as compared to $599.8 million at December 31, 2008 and we incurred losses from REOs of $218.2 million for the year ended December 31, 2009 compared to $52.0 million for the previous year. During 2009, the Company increased its loss assumptions for its long-term mortgage portfolio due to the increase in expected defaults and loss severities related to the weak economy and housing market. These conditions, which increase the cost and reduce the availability of debt, may continue or worsen in the future.

Without adequate financing, the growth of our business operations will be limited.

We have historically been dependent on warehouse lines, repurchase agreements, credit facilities, securitizations and other structured financings, and equity and debt issuances. The current dislocation and weakness in the capital and credit markets have created difficulties in obtaining financing. We are currently seeking warehouse facilities, and although we have been tentatively approved for an aggregate of $12 million in warehouse financing, as of the date of this report, we have not executed definitive agreements. If we are unable to obtain adequate financing, we will not be able to expand our business operations as planned, which will limit our revenues and operating results.

We may not be able to access financing sources on favorable terms, or at all, which could adversely affect our ability to implement and operate our business as planned.

Future financing sources may include borrowings in the form of bank credit facilities (including term loans and revolving facilities), repurchase agreements, warehouse facilities, structured financing arrangements, public and private equity and debt issuances and derivative instruments, in addition to transaction or asset specific funding arrangements. Our access to sources of financing depend upon a number of factors over which we have little or no control, including general market conditions, our financial performance, and resources and policies or lenders. Under current market conditions, many forms of structured financing arrangements are generally unavailable, which has also limited borrowings under warehouse and repurchase agreements that are intended to be refinanced by such financings. In addition, if regulatory capital requirements imposed on our private lenders change, they may be required to limit, or increase the cost of, financing they provide to us. In general, this could potentially increase our financing costs and reduce our liquidity. Consequently, the implementation of our new mortgage lending operations may be dictated by the cost and availability of financing. Depending on market conditions at the relevant time, we may have to rely more heavily on additional equity issuances, which may be dilutive to our shareholders, or on less efficient forms of debt financing that require a larger portion of our cash flow from operations, thereby reducing funds available for our operations and future business opportunities. We cannot assure you that we will have access to such equity or debt capital on favorable

13

terms (including, without limitation, cost and term) at the desired times, or at all, which could negatively affect our results of operations.

Our current long-term debt obligations, and any future debt financing may, contain restrictive covenants relating to our operations that may inhibit our ability to grow our business and increase revenues.

Our debt obligations consist of trust preferred securities, junior subordinated notes, and the Credit Agreement. The Credit Agreement contains various restrictive covenants, such as the ability to incur additional indebtedness, effect certain asset sales and acquisitions, pay dividends, maintain shareholders equity of not less than zero (based on certain calculations), cash and cash equivalents of not less than $10 million (based on certain calculations), and issue redeemable capital stock. The trust preferred securities and the junior subordinated notes no longer allow the company to defer interest payments and the Company may not repurchase stock, pay dividends or repay debt that is pari passu during an event of default. If or when we obtain additional financing, lenders may impose restrictions on us that would affect our ability to incur additional debt, make certain allocations or acquisitions, reduce liquidity below certain levels, make distributions to our shareholders, redeem debt or equity securities and restrict our flexibility to determine our operating policies and strategies. For example, our loan documents may contain negative covenants that limit, among other things, our ability to repurchase our common shares, employ leverage beyond certain amounts, sell assets, engage in mergers or acquisitions, grant liens, and enter into transactions with affiliates. If we fail to meet or satisfy any of these covenants, we would be in default under these agreements, and our lenders could elect to declare outstanding amounts due and payable, terminate their commitments, require the posting of additional collateral and enforce their interests against existing collateral. We may also be subject to cross-default and acceleration rights and, with respect to collateralized debt, the posting of additional collateral and foreclosure rights upon default. Any new financing could subject us to recourse indebtedness and the risk that debt service on less efficient forms of financing would require a larger portion of our cash flows, thereby reducing cash available for operations. If we are not able to arrange for new financing on terms acceptable to us, or if we default on our covenants causing repayment acceleration and an increase in interest rates, we may not have funds available for operations as well as for future business opportunities, which would have a material adverse effect on our business, financial condition, liquidity and results of operations.

If we are forced to liquidate, we may have few unpledged assets for distribution to unsecured creditors or equity holders.

In the event we are forced to liquidate, the majority of our assets are either collateral for specific borrowings or pledged as collateral for secured liabilities. We may have few remaining assets available for unsecured creditors and equity holders.

A material difference between the assumptions used in the determination of the value of our residual interests and our actual experience would cause us to write down the value of these securities and could harm our liquidity and financial condition.

Investments in residual interests and subordinated securities are much riskier than investments in senior mortgage-backed securities because these subordinated securities bear credit losses prior to the related senior securities. The risk associated with holding residual interests and subordinated securities is greater than holding the underlying mortgage loans directly due to the concentration of losses attributed to the subordinated securities. The value of residual interests represents the present value of future cash flows expected to be received by us from the excess cash flows created in the securitization transaction. In general, future cash flows are estimated by taking the coupon rate of the loans underlying

14

the transaction less the interest rate paid to the bond holders, less contractually specified servicing and trustee fees, and after giving effect to estimated prepayments, credit losses and overcollateralization requirements. We estimate future cash flows from these securities and value them utilizing assumptions based in part on projected interest rates, delinquency, mortgage loan prepayment speeds and credit losses. It is extremely difficult to validate the assumptions we use in valuing our residual interests. Even if the general accuracy of the valuation model is validated, valuations are highly dependent upon the reasonableness of our assumptions and the predictability of the relationships which drive the results of the model. Such assumptions are complex as we must make judgments about the effect of matters that are inherently uncertain. If our actual experience differs from our assumptions, we could be required to reduce the value of these securities. Furthermore, if our actual experience differs materially from these assumptions, our cash flow, financial condition, results of operations and liquidity may be harmed.

The Company's mortgage portfolio contains significant interest rate risks that are not currently hedged by the Company.

Residual interests in certain securitization trusts are expected to generate cash flows to the Company. These cash flows are contingent upon maintaining required overcollateralization levels and can be reduced or eliminated by realized losses from the disposition of loans or REO. Assuming realized losses have not reduced overcollateralization levels below required levels, excess cash flows are distributed to the residual interest holder after the required bond interest and principal payments are made to investors. Interest rates on the loans in the securitization trusts generally adjust bi-annually. Interest rates on the bonds usually adjust monthly with changes partially offset by derivatives instruments (primarily interest rate swap agreements) inside the securitization trusts. Since bond interest rates adjust more frequently than the related loans, increases in LIBOR rates could significantly reduce the future cash flows we receive from these securitization trusts. The amount of the derivatives instruments is not sufficient to fully protect the residual cash flows from increases in LIBOR. The Company does not have the ability to change the derivatives instruments inside the trusts and does not currently hedge this interest rate risk with derivatives instruments outside the securitization trusts. As a result of not fully hedging interest rate risks, the Company's future residual cash flows could be significantly affected by rising LIBOR rates.

We may experience reduced net earnings or losses if our liabilities re-price at different rates than our assets.

A significant source of revenue is net interest income or net interest spread from our long-term mortgage portfolio, which is the difference between the interest we earn on our interest earning assets and the interest we pay on our interest bearing liabilities. The rates we pay on our borrowings are independent of the rates we earn on our assets and may be subject to more frequent periodic rate adjustments. Therefore, we could experience a decrease in net earnings or a loss because the interest rates on our borrowings could increase faster than the interest rates on our assets, if the increased borrowing costs are not offset by reduced cash payments on derivatives recorded in other non-interest income. If our net interest spread becomes negative, we will be paying more interest on our borrowings than we will be earning on our assets and we will be exposed to a risk of loss.

The rates paid on our borrowings and the rates received on our assets may be based upon different indices. Our long-term mortgage portfolio includes mortgages that are one-, three- and six-month LIBOR and one-year LIBOR hybrid ARMs. These are mortgages with fixed interest rates for an initial period of time, after which they begin bearing interest based upon short-term interest rate indices and adjust periodically. We generally funded mortgages with adjustable interest rate borrowings having interest rates that are indexed to short-term interest rates, typically one-month LIBOR, and adjust periodically at various intervals. To the extent that there is an increase in the interest rate index used to

15

determine our adjustable interest rate borrowings and it increases faster than the indices used to determine the rates on our assets (i.e., the increase is not offset by a corresponding increase in the rates at which interest accrues on our assets) or is not offset by various cash payments on interest rate derivatives that we have in place at any given time, our net earnings will decrease or we will have net losses. Additionally, the Company has commenced a policy to modify loans by either reducing the interest rates, waiving accrued and unpaid interest or deferring accrued interest to help minimize delinquencies and maximize recoveries on loans. Although we believe in the long run this is beneficial to the Company, the modification of loans to defer the re-pricing may cause the Company to experience a reduction in expected cash flows.

ARMs typically have interest rate caps, which limit interest rates charged to the borrower during any given period. Our borrowings are not subject to similar restrictions. As a result, in a period of rapidly increasing interest rates, the interest rates we pay on our borrowings could increase without limitation, while the interest rates we earn on our ARMs would be capped. If this occurs, our net interest spread could be significantly reduced or we could suffer a net interest loss if not offset by a decrease in the cash payments on interest rate derivatives that we have in place at any given time.

Second trust deed mortgages in our long term investment portfolio expose us to greater credit risks.

Our security interest in the property securing second mortgages in our portfolio is subordinated to the interest of the first mortgage holder. Typically, the second mortgages have a higher combined loan to value (CLTV) ratio than do our first mortgages. If the borrower experiences difficulties in making senior lien payments or if the value of the property is equal to or less than the amount needed to repay the borrower's obligation to the first mortgage holder upon foreclosure, our second mortgage loan may not be repaid.

Also, our senior security interests may be affected if there are junior liens on the same properties resulting in a higher CLTV which borrowers may perceive have no equity. This could result in our senior liens defaulting at a higher rate than senior liens without a junior lien.

We may be subject to losses on mortgages for which we did not obtain mortgage insurance.

We did not obtain credit enhancements such as mortgage pool or special hazard insurance for all of our mortgages and mortgage investments. Generally, we required mortgage insurance on any first mortgage with an LTV ratio greater than 80 percent. During the time we hold mortgages for investment, we are subject to risks of borrower defaults and bankruptcies and special hazard losses that are not covered by standard hazard insurance. If a borrower defaults on a mortgage that we hold, we bear the risk of loss of principal to the extent there is any deficiency between the value of the related mortgaged property and the amount owing on the mortgage loan and any insurance proceeds available to us through the mortgage insurer. Also, to the extent we have insurance coverage, we bear the risk of the insurance carriers not being able to make the required payments.

Loans to non-conforming borrowers may expose us to a higher risk of delinquencies, foreclosures and losses.

We were an acquirer and originator of non-conforming single family and multifamily mortgage loans. These are mortgages that generally may not qualify for purchase by government-sponsored agencies such as Fannie Mae and Freddie Mac. Our operations have been negatively affected due to our investments in these mortgages. Credit risks associated with these mortgages may be greater than those associated with conforming mortgages. Mortgages made to such borrowers generally entail a higher risk of delinquency and higher losses than mortgages made to borrowers who utilize conventional

16

mortgage sources. Delinquency, foreclosures and losses generally increase during economic slowdowns or recessions. The actual risk of delinquencies, foreclosures and losses on mortgages made to our borrowers are higher under current economic conditions than those in the past. Additionally, the combination of different underwriting criteria and higher rates of interest leads to greater risk, including higher prepayment rates and higher delinquency rates and /or credit losses. We also have loans that are interest only and option-ARM loans that allow a borrower to pay only the stated interest or less than the stated interest, respectively, attributable to their loan for a set period of time. If there is a decline in real estate values borrowers may default on these types of loans since they have not reduced their principal balances, which, therefore, could exceed the value of their property. In addition, a reduction in property values would also cause an increase in the CLTV or LTV ratio for that loan which could have the effect of reducing the value of the property collateralized by that loan, reducing the borrowers' equity in their homes to a level that would increase the risk of default.

Our commercial and multifamily mortgages may expose us to increased lending risks.

Our commercial and multifamily mortgages typically involve larger mortgage balances to single borrowers or groups of related borrowers compared to one- to four-family residential mortgages. These commercial and multifamily mortgages have risks because repayment of the mortgages often depends on the successful operations and the income stream of the borrowers. Additionally, current economic conditions and the resulting tightening of credit markets have limited the opportunities for borrowers seeking to refinance their mortgages prior to scheduled interest rate resets. The inability of commercial and multifamily borrowers to successfully refinance their mortgages prior to scheduled interest rate reset dates could significantly increase delinquencies and losses within our long-term mortgage portfolio.

The geographic concentration of our mortgages increases our exposure to risks in those areas.

We do not set limitations on the percentage of our long-term mortgage portfolio composed of properties located in any one area (whether by state, zip code or other geographic measure). Concentration in any one area increases our exposure to the economic and natural hazard risks associated with that area. A majority of our mortgage acquisitions and originations, long-term mortgage portfolio and finance receivables are secured by properties in California and, to a lesser extent, Florida. California and Florida have experienced, and may experience in the future, an economic downturn and have also suffered the effects of certain natural hazards. As a result of the economic downturn, real estate values in California and Florida have decreased drastically and may continue to decrease in the future, which could have a material adverse effect on our results of operations or financial condition.

Furthermore, if borrowers are not insured for natural disasters, which are typically not covered by standard hazard insurance policies, then they may not be able to repair the property or may stop paying their mortgages if the property is damaged. This would cause increased foreclosures and decrease our ability to recover losses on properties affected by such disasters. This would have a material adverse effect on our results of operations or financial condition.

Representations and warranties made by us in our loan sales and securitizations may subject us to liability.

In connection with our loan sales to third parties and our prior securitizations, we transferred mortgages acquired and originated by us to the third parties or into a trust in exchange for cash and, in the case of a securitized mortgage, residual certificates issued by the trust. The trustee, purchaser, bondholder, or other entities involved in the issuance of the securities (which may include bond insurers) may have recourse to us with respect to the breach of the representations, and warranties made by us at the time such mortgages are transferred or when the securities are sold. While we may have recourse to our customers for any such breaches, there can be no assurance of our customers' abilities to honor

17

their respective obligations. Also, we previously engaged in bulk whole loan sales pursuant to agreements that generally provide for recourse by the purchaser against us in the event of a breach of one of our representations or warranties, any fraud or misrepresentation during the mortgage origination process, or upon early default on such mortgage. We attempted to limit the potential remedies of such purchasers to the potential remedies we received from the customers from whom we acquired or originated the mortgages. However, in some cases, the remedies available to a purchaser of mortgages from us may be broader or extend longer than those available to us against the sellers of the mortgages and should a purchaser enforce its remedies against us, we are not always able to enforce whatever remedies we have against our customers. Furthermore, if we discover, prior to the sale or transfer of a loan, that there is any fraud or misrepresentation with respect to the mortgage and the originator fails to repurchase the mortgage, then we may not be able to sell the mortgage or we may have to sell the mortgage at a discount.

The performance of our long-term mortgage portfolio may be adversely affected by the performance of parties who service or sub-service our mortgage loans.

We sell or contract with third-parties for the servicing of all our mortgage loans, including those in our securitizations. Our operations are subject to risks associated with inadequate or untimely servicing. Poor performance by a servicer may result in greater than expected delinquencies and losses on our mortgage loans. A substantial increase in our delinquency or foreclosure rate could adversely affect our ability to access the capital and secondary markets for our financing needs. Also, with respect to mortgage loans subject to a securitization, greater delinquencies would adversely affect the value of our residual interest, if any, we hold in connection with that securitization.

In a securitization, relevant agreements permit us to be terminated as servicer or master servicer under specific conditions described in these agreements. If, as a result of a servicer or sub-servicer's failure to perform adequately, we were terminated as master servicer of a securitization, the value of any master servicing rights held by us could be adversely affected.

We are a defendant in purported class action lawsuits and may not prevail in these matters.

Class action lawsuits and regulatory actions alleging improper marketing practices, abusive loan terms and fees, disclosure violations, improper yield spread premiums and other matters are risks faced by all mortgage originators, particularly those in the Alt-A and subprime market. We are a defendant in purported class actions pending in different states. Some of the class actions allege generally that the loan originator (not Impac) improperly charged fees in violation of various state lending or consumer protection laws in connection with mortgages that we acquired while others allege that our lending practice was a statutory violation, an unlawful business practice, an unfair business practice or a breach of a contract. Although the suits are not identical, they generally seek unspecified compensatory damages, punitive damages, pre- and post-judgment interest, costs and expenses and rescission of the mortgages, as well as a return of any improperly collected fees. We may incur defense costs and other expenses in connection with the class action lawsuits, and we cannot assure you that the ultimate outcome of these or other actions will not have a material adverse effect on our financial condition or results of operations. In addition to the expense and burden incurred in defending this litigation and any damages that we may suffer, our management's efforts and attention may be diverted from the ordinary business operations in order to address these claims. If the final resolution of this litigation is unfavorable to us, our financial condition, results of operations and cash flows might be materially adversely affected if our existing insurance coverage is unavailable or inadequate to resolve the matters. We believe we have meritorious defenses to the actions and intend to defend against them vigorously; however, an adverse judgment in any of these matters could have a material adverse effect on us.

18

There has been recent litigation in the mortgage industry related to securitizations.

As defaults, delinquencies, foreclosures, and losses in the real estate market continue, there have been recent lawsuits by various investors, insurers, underwriters and others against various participants in securitizations, such as sponsors, depositors, underwriters, and loan sellers. Some lawsuits have alleged that the mortgage loans had origination defects, that there were misrepresentations made about the mortgage loans and the parties failed to properly disclose the quality of the mortgage loans or repurchase defective loans. There have been other claims contending errors or misrepresentations in the securitization documents or process itself. Historically, we both securitized and sold mortgage loans to third parties that may have been deposited or included in pools for securitizations. In connection with these lawsuits, we may be asked to repurchase these mortgage loans, provide indemnification against such claims or we may become subject to litigation related to the securitizations. As a result, we may incur significant legal and other expenses in defending against claims and litigation and we may be required to pay settlement costs, damages, penalties or other charges which could adversely affect our financial results.

We are exposed to environmental liabilities, with respect to properties that we take title to upon foreclosure, that could increase our costs of doing business and harm our results of operations.

In the course of our activities, we may foreclose and take title to residential properties and become subject to environmental or mold liabilities with respect to those properties. The laws and regulations related to mold or environmental contamination often impose liability without regard to responsibility for the contamination. We may be held liable to a governmental entity or to third parties for property damage, personal injury, investigation and clean-up costs incurred by these parties in connection with mold or environmental contamination, or may be required to investigate or clean up hazardous or toxic substances, or chemical releases at a property. The costs associated with investigation or remediation activities could be substantial. Moreover, as the owner or former owner of a contaminated site, we may be subject to common law claims by third parties based upon damages and costs resulting from mold or environmental contamination emanating from the property. If we ever become subject to significant mold or environmental liabilities, our business, financial condition, liquidity and results of operations could be significantly harmed.

We are subject to risks of operational failure that are beyond our control.

Substantially all of our operations are located in Irvine, California. Our systems and operations are vulnerable to damage and interruption from fire, flood, telecommunications failure, break-ins, earthquake and similar events. Our operations may also be interrupted by power disruptions, including rolling black-outs implemented in California due to power shortages. Furthermore, our security mechanisms may be inadequate to prevent security breaches to our computer systems, including from computer viruses, electronic break-ins and similar disruptions. Such security breaches or operational failures could expose us to liability, impair our operations, result in losses, and harm our reputation.

Loss of our current executive officers or other key management could significantly harm our business.

We depend on the diligence, skill and experience of our senior executives, including our chief executive officer and president. We believe that our future results will also depend in part upon our attracting and retaining highly skilled and qualified management. We seek to compensate our executive officers, as well as other employees, through competitive salaries, bonuses and other incentive plans, but there can be no assurance that these programs will allow us to retain key management executives or hire new key employees. The loss of our chief executive officer, president, or other senior executive officers and key management could have a material adverse affect on our operations because other

19

officers may not have the experience and expertise to readily replace these individuals. Competition for such personnel is intense, and we cannot assure you that we will be successful in attracting or retaining such personnel. Furthermore, in light of our present financial condition, no assurance can be given that we will retain these and other executive officers and key management personnel. To the extent that one or more of our top executives or other key management personnel are no longer employed by us, our operations and business prospects may be adversely affected. The loss of, and changes in, key personnel and their responsibilities may be disruptive to our business and could have a material adverse effect on our business, financial condition and results of operations.

If we fail to maintain effective systems of internal control over financial reporting and disclosure controls and procedures, we may not be able to report our financial results accurately or prevent fraud, which could cause current and potential stockholders to lose confidence in our financial reporting, adversely affect the trading price of our securities or harm our operating results.