Attached files

| file | filename |

|---|---|

| EX-23.2 - CONSENT OF CROWE HORWATH LLP - BAYLAKE CORP | baylake101073_ex23-2.htm |

| EX-21.1 - LIST OF SUBSIDIARIES - BAYLAKE CORP | baylake101073_ex21-1.htm |

| EX-23.1 - CONSENT OF BAKER TILLY VIRCHOW KRAUSE - BAYLAKE CORP | baylake101073_ex23-1.htm |

| EX-31.1 - CERTIFICATION OF CEO PURSUANT TO SECTION 302 - BAYLAKE CORP | baylake101073_ex31-1.htm |

| EX-32.2 - CERTIFICAITON OF CFO PURSUANT TO SECTION 906 - BAYLAKE CORP | baylake101073_ex32-2.htm |

| EX-32.1 - CERTIFICATION OF CEO PURSUANT TO SECTION 906 - BAYLAKE CORP | baylake101073_ex32-1.htm |

| EX-31.2 - CERTIFICATION OF CFO PURSUANT TO SECTION 302 - BAYLAKE CORP | baylake101073_ex31-2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

|

|

|

|

|

|

||

|

|

||

|

FORM 10-K |

||

|

|

||

|

|

||

|

|

|

(Mark One) |

|

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE |

||

|

SECURITIES EXCHANGE ACT OF 1934 |

||

|

|

|

|

|

For the fiscal year ended December 31, 2009 |

||

|

or |

||

|

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE |

||

|

SECURITIES EXCHANGE ACT OF 1934 |

||

For the transition period from _________________ to _________________

|

|

|

|

|

Wisconsin |

|

39-1268055 |

|

(State or other jurisdiction of |

|

(I.R.S. Employer |

|

incorporation or organization) |

|

Identification No.) |

|

|

|

|

|

217 North Fourth Avenue, Sturgeon Bay, WI |

|

54235 |

|

(Address of principal executive offices) |

|

(Zip Code) |

|

|

|

|

|

Registrant’s telephone number, including area code: (920)-743-5551 |

||

|

|

|

|

|

Securities registered pursuant to Section 12(b) of the Act: None |

||

Securities registered pursuant to Section 12(g) of the Act: Common Stock $5.00 Par Value Per Share

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such charter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

|

|

|

|

|

Large accelerated filer o |

Accelerated filer o |

Non-accelerated filer o |

Smaller reporting company x |

|

(Do not check if a smaller reporting company) |

|||

1

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) Yes o No x

As of June 30, 2009, (the last business day of the Registrant’s most recently completed second fiscal quarter), the aggregate market value of the Common Stock (based upon the $3.40 reported bid price on that date) held by non-affiliates (excludes a total of 600,043 shares reported as beneficially owned by directors and executive officers-does not constitute an admission as to affiliate status) was approximately $24,859,083. As of March 12, 2010, 7,911,538 shares of Common Stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

|

|

|

|

|

|

|

Part of Form 10-K Into Which |

|

Document |

|

Portions of Documents are Incorporated |

|

|

|

|

|

Definitive Proxy Statement for 2010 Annual Meeting of Shareholders to be filed within 120 days of the fiscal year ended December 31, 2009 |

|

Part III |

2

2009 FORM 10-K

TABLE OF CONTENTS

|

|

|

|

|

|

|

|

DESCRIPTION |

PAGE NO. |

|

|

|

|

|

|

|

|

||

|

|

4 |

||

|

|

8 |

||

|

|

14 |

||

|

|

14 |

||

|

|

14 |

||

|

|

14 |

||

|

|

|

|

|

|

|

|

||

|

|

15 |

||

|

|

17 |

||

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operation |

18 |

|

|

|

43 |

||

|

|

43 |

||

|

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

79 |

|

|

|

79 |

||

|

|

79 |

||

|

|

|

|

|

|

|

|

||

|

|

79 |

||

|

|

79 |

||

|

|

Security Ownership of Certain Beneficial Owners and Management And Related Stockholder Matters |

79 |

|

|

|

Certain Relationships and Related Transactions, and Director independence |

80 |

|

|

|

80 |

||

|

|

|

|

|

|

|

|

||

|

|

81 |

||

|

|

|

|

|

|

|

81 |

3

General

Baylake Corp. is a Wisconsin corporation organized in 1976 and is registered as a bank holding company under the Bank Holding Company Act of 1956, as amended (the “BHCA”). Our primary activities consist of holding the stock of our wholly-owned subsidiary bank, Baylake Bank, and providing a wide range of banking and related business activities through our bank and our other subsidiaries. At December 31, 2009, we had total assets of approximately $1.0 billion. For additional financial information, see our Consolidated Financial Statements and Notes at Part II, Item 8 of this Form 10-K.

Baylake Bank

Baylake Bank is a Wisconsin state bank originally chartered in 1876. Our bank is an independent community bank offering a full range of financial services primarily to small businesses and individuals located in our market area. We conduct our community banking business through 28 full-service financial centers located throughout Northeast Wisconsin, in Brown, Door, Green Lake, Kewaunee, Manitowoc, Outagamie, Waupaca, and Waushara Counties. We have eight financial centers in Door County, which is known for its tourism-related services. We have eight financial centers in Brown County, which includes the city of Green Bay. We serve a broader range of service, manufacturing and retail job segments in the Brown County market. The rest of our financial centers are located in smaller cities and smaller communities. Other principal industries in our market area include industry and manufacturing, agriculture and food related products..

Non-Bank Subsidiaries

In addition to our banking operations, our bank owns three non-bank subsidiaries: Baylake Investments, Inc., located in Las Vegas, Nevada, which holds and manages an investment portfolio; Baylake City Center LLC, which owns 10.9% of a commercial building condominium in Green Bay; and Baylake Insurance Agency, Inc., which offers various types of insurance products to the general public as an independent agent. Our bank also owns a minority interest (49.8% of the outstanding common stock) in United Financial Services, Inc. (“UFS”), a data processing services company located in Grafton, Wisconsin, that provides data processing services to approximately 40 banks (including Baylake Bank) as well as electronic banking processing to four banks.

Corporate Governance Matters

We maintain a website at www.baylake.com. We make available through that website, free of charge, copies of our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports, as soon as reasonably practicable after Baylake electronically files those materials with, or furnishes them to, the Securities and Exchange Commission (“SEC”). Our SEC reports can be accessed through the Baylake Corp. link on our website. The SEC also maintains a website at www.sec.gov that contains reports, proxy statements and other information regarding SEC registrants.

Lending

We offer short-term and long-term loans on a secured and unsecured basis for business and personal purposes. We make real estate, commercial/industrial, agricultural and consumer loans in accordance with the basic lending policies established by our board of directors. We focus lending activities on individuals and small businesses in our market area. Our lending activity has been historically concentrated primarily within the State of Wisconsin. We do not conduct any substantial business with foreign obligors. We serve a wide variety of industries including, on a limited basis, a concentration on businesses directly and indirectly related to the tourism/recreation related industries. Loans to customers in the tourism/recreation industry, including restaurants and lodging businesses, totaled approximately $120.8 million at December 31, 2009, or 18.5% of our aggregate loans outstanding at that date. Although competitive and economic pressures exist in this market segment, business remains relatively steady in the markets we serve. However, any deterioration in the economy of Northeastern Wisconsin (as a result, for example, of a decline in its manufacturing or tourism/recreation industries or otherwise) could have a material adverse effect on our business and operations. In particular, a decline in the Door County tourism business would not only affect our customers in the restaurant and lodging business, and therefore loans to them as described above, but could also affect loans and other business relationships with persons employed in that industry and real estate values (including collateral values) in the area.

4

Our expansion into other market areas has reduced our concentration level in tourism/recreation-related businesses over the last thirty-six months, but these types of businesses still remain an important element of the customer base that we serve.

Our total outstanding loans as of December 31, 2009 were approximately $651.9 million, consisting of 54.2% commercial real estate loans, 19.1% residential real estate loans, 9.6% construction and land development real estate loans, 12.8% commercial and industrial loans, 1.8% consumer and 2.5% tax exempt loans.

Investments

We maintain a portfolio of investments, primarily consisting of U.S. Treasury securities, U.S. Government sponsored agency securities, mortgage-backed securities, obligations of states and their political subdivisions, and private placement and corporate bonds. We attempt to balance our portfolio to manage interest rate risks, maximize tax advantages and meet liquidity needs while endeavoring to maximize investment income.

Deposits

We offer a broad range of depository products, including non-interest bearing demand deposits, interest-bearing demand deposits, various savings and money market accounts and certificates of deposit. Deposits are insured by the Deposit Insurance Fund of the Federal Deposit Insurance Corporation (“FDIC”) up to statutory limits. At December 31, 2009, our total deposits were approximately $831.6 million, including interest-bearing deposits of $750.3 million and non-interest bearing deposits of $81.3 million. Deposits of $41.7 million were covered under the FDIC’s Transaction Account Guarantee Program.

Other Customer Services and Products

Other services and products we offer include transfer agency, safe deposit box services, personal and corporate trust services, conference center facilities, insurance agency and brokerage services, cash management, private banking, financial planning and electronic banking services, including mobile banking, and ebanc, an Internet banking product for our customers.

Seasonality

The tourism/recreation industry, particularly in the Door County market, substantially affects our business with our customers, particularly those customers in the restaurant and lodging businesses. The tourist business of Door County is largely seasonal, with the vast majority of tourists vacationing beginning in early spring and continuing until late fall. Although businesses and customers involved in the delivery of tourism-related services have financial needs throughout the entire year, the seasonal nature of the tourist business tends to result in increased demands for loans shortly before and during the tourist season and causes reduced deposits shortly before and during the early part of the tourist season.

Competition

The financial services industry is highly competitive. We compete with other financial institutions and businesses in both attracting and retaining deposits and making loans in all of our principal markets. The primary factors in competing for deposits are interest rates, personalized services, the quality and range of financial services, convenience of office locations and office hours. Competition for deposit products comes primarily from other commercial banks, savings banks, credit unions and non-bank competitors, including insurance companies, money market and mutual funds, and other investment alternatives. The primary factors in competing for loans are interest rates, loan origination fees, the quality and range of lending services and personalized services. Competition for loans comes primarily from other commercial banks, savings banks, mortgage banking firms, credit unions, finance companies, leasing companies and other financial intermediaries. Some of our competitors are not subject to the same degree of regulation as that imposed on bank holding companies or federally insured state-chartered banks, and may be able to price loans and deposits more aggressively. We also face direct competition from other banks and bank holding companies that have greater assets and resources than ours.

5

Regulation and Supervision

Baylake Corp. As a bank holding company, we are subject to regulation by the Board of Governors of the Federal Reserve (“FRB”) and examination by the Federal Reserve Bank of Chicago (“Reserve Bank”) under the BHCA and are required to file reports of our operations and such additional information as the FRB may require. Under FRB policy, we are expected to act as a source of financial strength to our subsidiary bank and to commit resources to support the bank in circumstances where we might not deem it appropriate to do so, absent such policy.

With certain limited exceptions, the BHCA prohibits bank holding companies from acquiring direct or indirect ownership or control of voting shares or assets of any company other than a bank, unless the company involved is engaged solely in one or more activities which the FRB has determined to be financial in nature or incidental to such financial activity. In 1999, Congress enacted the Gramm-Leach-Bliley Act (“GLB Act”), which eliminated certain barriers to and restrictions on affiliations between banks and securities firms, insurance companies and other financial services organizations. Among other things, the GLB Act amended the BHCA to permit bank holding companies that qualify as “financial holding companies” to engage in a broad list of “financial activities,” and any non-financial activity that the FRB, in consultation with the Secretary of the Treasury, determines is “complementary” to a financial activity and poses no substantial risk to the safety and soundness of depository institutions or the financial system. The GLB Act treats various lending, insurance underwriting, insurance company, portfolio investment, financial advisory, securities underwriting, dealing and market-making, and merchant banking activities as financial in nature for this purpose.

Under the GLB Act, a bank holding company may become certified as a financial holding company by filing a notice with the FRB, together with a certification that the bank holding company meets certain criteria, including capital, management and Community Reinvestment Act requirements. We have not elected to be certified as a financial holding company.

The FRB uses capital adequacy guidelines in its regulation of bank holding companies. If capital falls below minimum guidelines, a bank holding company may, among other things, be denied approval to acquire or establish banks, non-bank businesses or other bank holding companies.

The FRB has issued a policy statement on the payment of cash dividends by bank holding companies, which expresses the FRB’s view that a bank holding company should pay cash dividends only to the extent that its net income for the past year is sufficient to cover both the cash dividend and a rate of retention consistent with its needs. The FRB policy statement also indicates that it would be inappropriate for a bank holding company experiencing serious financial problems to borrow money to pay dividends. In addition, compliance with capital adequacy guidelines at both a bank subsidiary and a bank holding company could affect such entity’s ability to pay dividends, if its capital levels were to decrease.

The Sarbanes-Oxley Act of 2002 (“SOX”) addresses, among other issues, director and officer responsibilities for proper corporate governance of publicly traded companies, including the establishment of audit committees, certification of financial statements, auditor independence and accounting standards, executive compensation, insider loans, whistleblower protection, and enhanced and timely disclosure of corporate information. In general, SOX is intended to allow stockholders to monitor more effectively the performance of publicly traded companies and their management. The SEC has enacted rules to implement various provisions of SOX, which affect us as a publicly-held entity. The federal banking regulators also have adopted generally similar requirements concerning the certification of financial statements. Among these requirements is the adoption of company-wide codes of conduct by banks. SOX also imposes additional corporate governance requirements on publicly-held companies, particularly relating to the functioning of audit committees. We are subject to the requirement of annual attestation and review of our internal control on financial reporting.

6

Baylake Bank. As a FRB member Wisconsin state-chartered bank, we are subject to supervision and regulation by the Wisconsin Department of Financial Institutions, Division of Banking (“WDFI”), the FRB and the FDIC. Federal law and regulations establish supervisory standards applicable to the lending activities of our bank, including internal controls, credit underwriting, loan documentation and loan-to-value ratios for loans secured by real property.

Our bank is subject to federal and state statutory and regulatory restrictions on any extension of credit to us or our subsidiaries, on investments in our stock or other securities of our subsidiaries, on the payment of dividends to us, and on the acceptance of the stock or other securities of our subsidiaries as collateral for loans to any person. Limitations and reporting requirements are also placed on extensions of credit by our bank to our directors and officers, to the directors and officers of our subsidiaries, to our principal shareholders, and to “related interests” of such directors, officers and principal shareholders.

In addition to general requirements that banks retain specified levels of capital and otherwise conduct their business in a safe and sound manner, Wisconsin law requires that dividends of Wisconsin banks be paid out of current earnings or, no more than once within the immediate preceding two years, out of undivided profits. Any other dividends require the prior written consent of the WDFI.

Under the Community Reinvestment Act (“CRA”) and the implementing regulations, our bank has a continuing and affirmative obligation to help meet the credit needs of our local community including low and moderate-income neighborhoods, consistent with the safe and sound operation of the institution. The CRA requires the boards of directors of financial institutions, such as our bank, to adopt a CRA statement for each assessment area that, among other things, describes its efforts to help meet community credit needs and the specific types of credit that the institution is willing to extend. Our bank’s service area is designated and comprises the eight counties within the geographic area of Central and Northeast Wisconsin. Our bank’s board of directors is required to review the appropriateness of this delineation at least annually.

Our bank’s business includes making a variety of types of loans to individuals. In making these loans, we are subject to state usury and regulatory laws and to various federal statutes, such as the Equal Credit Opportunity Act, the Fair Credit Reporting Act, the Truth in Lending Act, the Real Estate Settlement Procedures Act, the Home Mortgage Disclosure Act, and the regulations promulgated thereunder, which prohibit discrimination, specify disclosures to be made to borrowers regarding credit and settlement costs and regulate the mortgage loan servicing activities of our bank, including the maintenance and operation of escrow accounts and the transfer of mortgage loan servicing. In receiving deposits, we are subject to extensive regulation under state and federal law and regulations, including the Truth in Savings Act, the Expedited Funds Availability Act, the Bank Secrecy Act, the Electronic Funds Transfer Act and the Federal Deposit Insurance Act. Violation of these laws could result in the imposition of significant damages and fines upon us, our directors and officers.

Under the GLB Act, all financial institutions are required to adopt privacy policies, restrict the sharing of non public customer data with nonaffiliated parties at the customer’s request and establish procedures and practices to protect customer data from unauthorized access.

Under Title III of the Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act of 2001 (“PATRIOT Act”), also known as the International Money Laundering Abatement and Anti-Terrorism Financing Act of 2001, all financial institutions are required to take certain measures to identify customers, prevent money laundering, monitor certain customer transactions and report suspicious activity to U.S. law enforcement agencies, and to scrutinize or prohibit altogether certain transactions of special concern. Financial institutions are also required to respond to requests for information from federal banking regulatory agencies and law enforcement agencies concerning their customers and their transactions.

Federal law provides that adequately managed bank holding companies from any state may acquire banks and bank holding companies located in any other state, subject to certain conditions.

Financial institution regulatory agencies are given substantial powers to take corrective actions, which may include restrictions on methods of doing business and the prohibition of certain actions.

Employees

At December 31, 2009, we had 306 full-time equivalent employees company-wide. We consider our relationship with our employees to be good.

7

Forward-Looking Statements

This report contains statements that may constitute forward-looking statements within the meaning of the safe-harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995, such as statements other than historical facts contained or incorporated by reference in this report. These forward-looking statements include statements with respect to our financial condition, results of operations, plans, objectives, future performance and business, including statements preceded by, followed by or that include the words “believes,” “expects,” or “anticipates,” references to estimates or similar expressions. Future filings by us with the Securities and Exchange Commission (“SEC”), and future statements other than historical facts contained in written material, press releases and oral statements issued by us, or on our behalf, may also constitute forward-looking statements.

Forward-looking statements are subject to significant risks and uncertainties, and our actual results may differ materially from the results discussed in such forward-looking statements. Factors that might cause actual results to differ from the results discussed above include, but are not limited to, the Risk Factors set forth below and any other risks identified in this report or in other filings we may make with the SEC. All forward-looking statements contained in this report or which may be contained in future statements made for or on our behalf are based upon information available at the time the statement is made and we assume no obligation to update any forward-looking statements.

Risk Factors

Our business may be adversely affected by conditions in the financial markets and economic conditions generally.

The United States economy has been in a downward cycle since the end of 2007, which has been marked by reduced business activity across a wide range of industries and regions. Many businesses are experiencing serious difficulties due to the lack of consumer spending and the lack of liquidity in the credit markets. In addition, unemployment has increased significantly and continues to grow.

The financial services industry and the securities markets generally have been materially and adversely affected by significant declines in the values of nearly all asset classes and by a serious lack of liquidity. This was initially triggered by declines in home prices and the resulting impact on sub-prime mortgages but has since spread to all mortgage and real estate asset classes, as well as equity securities.

The economic downturn has also resulted in the failure of a number of prominent financial institutions, resulting in further losses as a consequence of defaults on securities issued by them and defaults under contracts with such entities as counterparties. In addition, declining asset values, defaults on mortgages and consumer loans, the lack of market and investor confidence and other factors have all combined to cause rating agencies to lower credit ratings and to otherwise increase the cost and decrease the availability of liquidity. Some banks and other lenders have suffered significant losses and have become reluctant to lend, even on a secured basis, due to the increased risk of default, and the impact of declining collateral values and greater regulatory scrutiny. In 2008 and 2009, the U.S. government, the FRB and other regulators took numerous steps to increase liquidity and to restore investor confidence, including investing in the equity of other banking organizations through the Capital Purchase Program under the Troubled Asset Relief Program. In spite of this, asset values have continued to decline, and access to liquidity continues to be very limited. If these measures are unsuccessful or if the economic downturn continues, our earnings and, consequently, our financial condition could be depressed.

Our operations are geographically limited and are more at risk for downturns in those areas.

Our financial performance generally is highly dependent upon the business environment in Northeastern Wisconsin, particularly in Door and Brown Counties. As a result of this geographical concentration, we are more vulnerable to downturns or other factors that affect the local economy or decrease demand for our services than if our operations were conducted over a wider area. Other local factors, such as natural disasters and the local regulatory climate, could also significantly affect our results because of our lack of geographical diversity.

8

In our market area, especially in Door County, a significant percentage of our customer base is in the tourism industry, particularly lodging and restaurants. Many of our customers depend indirectly on the tourism industry. This concentration in a single industry could cause any downturn or other issues affecting local tourism to reduce the demand for our services, increase problem loans and thus disproportionately affect our results of operations.

The overall business environment during 2009 has been adverse for many households and businesses in Northeast Wisconsin. The business environment in the markets in which we operate has been adversely affected and continues to deteriorate, albeit at a moderating pace. It is possible that the business environment in Northeastern Wisconsin will continue to deteriorate for the foreseeable future. Such conditions could have a material adverse effect on the credit quality of our loans, and therefore, our financial condition and results of operations.

Weakness in the markets for residential or commercial real estate, including the secondary residential mortgage loan markets, could reduce our net income and profitability.

Since 2007, softening residential housing markets, increasing delinquency and default rates, and increasingly volatile and constrained secondary credit markets have been negatively impacting the mortgage industry. Our financial results have been adversely affected by changes in real estate values, primarily in Northeastern Wisconsin. Decreases in real estate values have adversely affected the value of property used as collateral for loans and investments in our portfolio. The poor economic condition experienced in 2007 through 2009 resulted in decreased demand for commercial real estate loans, and our net income and profits have suffered as a result.

The declines in home prices in many markets across the U.S., including Northeastern Wisconsin, along with the reduced availability of mortgage credit, also has resulted in increases in delinquencies and losses in our portfolio of loans related to residential real estate. Further declines in home prices within Northeastern Wisconsin coupled with the continued impact of the economic recession and high unemployment levels, could drive losses beyond the levels provided for in our allowance for loan losses. In that event, our future earnings would be adversely affected.

Significant ongoing disruption in the secondary market for residential mortgage loans has limited the market for and liquidity of most mortgage loans other than conforming Fannie Mae, Freddie Mac and Ginnie Mae loans. The effects of ongoing mortgage market challenges, combined with the ongoing correction in residential real estate market prices and reduced levels of home sales has resulted in price reductions in single family home values, adversely impacting the value securing mortgage loans held. Continued declines in real estate values and home sales volumes within Northeastern Wisconsin, and financial stress on borrowers as a result of job losses, or other factors, could have further adverse effects on borrowers that result in higher delinquencies and greater charge-offs in future periods, which would adversely affect our financial condition and results of operations.

We are subject to interest rate risk.

Our earnings and cash flows are largely dependent upon our net interest income, which is the difference between interest income on interest-earning assets such as loans and securities and interest expense paid on interest-bearing liabilities such as deposits and borrowed funds. There are many factors which influence interest rates that are beyond our control, including but not limited to general economic conditions and governmental policy, in particular, the policies of the FRB. Any changes in such policies, including changes in interest rates, could influence the amount of interest we receive on loans and securities and the amount of interest we pay on deposits and borrowings. Such changes could also affect (i) our ability to originate loans and obtain deposits, (ii) the value of our financial assets and liabilities, and (iii) the average maturity of our securities portfolio. In addition, an increase in the general level of interest rates may also adversely affect the ability of certain of our borrowers to repay their obligations. If the interest rates paid on deposits and other borrowings increase at a faster rate than the interest rates received on loans and other investments, our net interest income, and therefore our earnings, would be adversely affected. Earnings would also be adversely affected if the interest rates received on loans and other investments fall more quickly than the interest rates paid on deposits and other borrowings.

Management uses various methods to monitor interest rate risk and believes it has implemented effective asset and liability strategies to reduce the potential effects of changes in interest rates on our results of operations. Management also periodically adjusts our mix of assets and liabilities to manage interest rate risk. However, any substantial, unexpected, prolonged change in market interest rates could have a material adverse effect on our consolidated financial condition and results of operations.

9

We are subject to lending risk.

There are inherent risks associated with our lending activities. These risks include the impact of changes in interest rates and change in the economic conditions in the markets we serve, as well as those across the United States. An increase in interest rates and/or continuing weakening economic conditions could adversely impact the ability of our borrowers to repay outstanding loans, or could substantially weaken the value of the collateral securing those loans. Continuing economic weakness on real estate and related markets could further increase our lending risk as it relates to our commercial real estate loan portfolio and the value of the underlying collateral. Approximately 54.2% of our loans are concentrated in commercial real estate as well as 19.1% in residential real estate lending as of December 31 2009, compared to 52.4% and 19.4% as of December 31, 2008, respectively. Continued downward pressure on real estate values could increase the potential for problem loans and thus have a direct impact on our consolidated results of operations.

We are also subject to various laws and regulations that affect our lending activities. Failure to comply with applicable laws and regulations could subject us to regulatory enforcement action that could result in the assessment of significant civil monetary penalties against us.

Our allowance for loan losses may be insufficient.

To address risks inherent in our loan portfolio, we maintain an allowance for loan losses that represents management’s best estimate of probable losses that may occur within our existing loan portfolio. The level of the allowance reflects management’s continuing evaluation of various factors, including industry concentrations, specific credit risks, loan loss experience, current loan portfolio quality, present economic, political and regulatory conditions, and unidentified losses inherent in the current loan portfolio. Determining the appropriate level of the allowance for loan losses involves a high degree of subjectivity and requires us to make estimates of significant credit risks and future trends, all of which may undergo material changes. In evaluating our impaired loans, we assess repayment expectations and determine collateral values based on all information that is available to us. However, we must often make subjective decisions based on our assumptions about the creditworthiness of the borrowers and the value of the collateral.

Continuing deterioration in economic conditions affecting borrowers, new information regarding existing loans, identification of additional problem loans, and other factors, both within and outside of our control, may require an increase in our allowance for loan losses. In addition, bank regulatory agencies periodically examine our allowance for loan losses and may require an increase in the allowance or the recognition of further loan charge-offs, based on judgments different from those of management.

If charge-offs in future periods exceed our allowance for loan losses, we will need to take additional loan loss provisions to increase our allowance for loan losses. Any additional loan loss provisions will reduce our net income or increase our net loss, which would have a material adverse effect on our financial condition and results of operations.

Uncertainty in the financial markets could result in lower fair values for our investment securities, which fair values may not be realizable if we were to sell those securities today.

The upheaval in the financial markets over the past two years has adversely impacted investor demand for all classes of securities and has resulted in volatility in the fair values of our investment securities. Significant prolonged reduction in investor demand could result in lower fair values for these securities and may result in recognition of an other-than-temporary impairment charge, which would have a direct adverse impact on our consolidated results of operations.

We are subject to environmental liability risk associated with collateral securing our real estate lending.

Because a significant portion of our loan portfolio is secured by real property, from time to time we may find it necessary to foreclose on and take title to properties securing such loans. In doing so, there is a risk that hazardous or toxic substances could be found on those properties. If such substances are found, we may be liable for remediation costs, as well as for personal injury and property damage. We may also be required to incur substantial expenses that could materially reduce the affected property’s value or limit our ability to use or sell the affected property. In addition, future environmental laws or more stringent interpretations or enforcement policies with respect to existing laws may increase our exposure to environmental liability. Although we are careful to perform environmental reviews on properties prior to foreclosure, our reviews may not detect all environmental hazards.

We may be adversely affected by the soundness of other financial institutions.

Financial services institutions are interrelated as a result of trading, clearing, counterparty or other relationships. We routinely execute transactions with counterparties in the financial services industry, including commercial banks, brokers and dealers, investments banks, and other institutional clients. Many of these transactions expose us to credit risk in the event of default by a counterparty. In addition, our credit risk may be heightened when the collateral we hold cannot be realized upon liquidation or is liquidated at prices not sufficient to recover the full amount of the credit or derivative exposure due to us. Any such losses could have a material adverse effect on our consolidated financial condition and results of operations.

10

Competition may affect our results.

We face strong competition in originating loans, in seeking deposits and in offering our other services. We must compete with commercial banks, savings associations, trust companies, mortgage banking firms, credit unions, finance companies, mutual funds, insurance companies and brokerage and investment banking firms. Our market area is also served by several commercial banks and savings associations that are substantially larger than us in terms of deposits and loans and have greater human and financial resources.

This competitive climate can make it more difficult to establish and maintain relationships with new and existing customers and can lower the rate we are able to charge on loans, increase the rates we must offer on deposits, and affect our charges for other services. Those factors can, in turn, adversely affect our results of operations and profitability.

Maintaining or increasing our market share may depend on lowering prices and market acceptance of new products and services.

Our success depends, in part, on our ability to adapt our products and services to evolving industry standards. There is increasing pressure to provide products and services at lower prices. Lower prices can reduce our net interest margin and revenues from our fee-based products and services. In addition, the widespread adoption of new technologies, including internet services, could require us to make substantial expenditures to modify or adapt our existing products and services. Also, these and other capital investments in our business may not produce expected growth in earnings anticipated at the time of the expenditure. We may not be successful in introducing new products and services, achieving market acceptance of our products and services, or developing and maintaining loyal customers.

Acts or threats of terrorism and political or military actions by the United States or other governments could adversely affect general economic industry conditions.

Geopolitical conditions may affect our earnings. Acts or threats of terrorism and political actions taken by the United States or other governments in response to terrorism, or similar activity, could adversely affect general economic or industry conditions and, as a result, our consolidated financial condition and results of operations.

We operate in a highly regulated environment, which could increase our cost structure or have other negative impacts on our operations.

We are highly regulated by both federal and state regulatory authorities. Regulation includes, among other things, capital and reserve requirements, permissible investments and lines of business, dividend limitations, limitations on products and services offered, loan limits, geographical limits, consumer credit regulations, community reinvestment requirements and restrictions on transactions with affiliated parties. The system of supervision and regulation applicable to us establishes a comprehensive framework for our operations and is intended primarily for the protection of the Deposit Insurance Fund, our depositors and the public, rather than our stockholders. We are also subject to regulation by the SEC. Failure to comply with applicable laws, regulations or policies could result in sanction by regulatory agencies, civil monetary penalties, and/or damage to our reputation, which could have a material adverse effect on our business, consolidated financial condition and results of operations. In addition, any change in government regulation could have a material adverse effect on our business.

Recent legislative and regulatory actions taken to stabilize the United States banking system and additional actions being considered may not succeed or may disadvantage us.

In response to the recent financial crisis, the United States government, specifically the Department of Treasury, FRB and FDIC, working in cooperation with foreign governments and other central banks, has taken a variety of extraordinary measures designed to restore confidence in the financial markets and to strengthen financial institutions, including measures available under the Emergency Economic Stabilization Act (“EESA”). The EESA followed, and has been followed by, numerous actions by the FRB, United States Congress, Department of Treasury, FDIC, SEC and others to address the current liquidity and credit crisis. These measures included homeowner relief that encourages loan restructuring and modification; the establishment of significant liquidity and credit facilities for financial institutions and investment banks; the lowering of the federal funds rate; emergency action against short selling practices; a temporary guaranty program for money market funds; the establishment of a commercial paper funding facility to provide back-stop liquidity to commercial paper issuers; and coordinated international efforts to address illiquidity and other weaknesses in the financial sector. The purpose of these legislative and regulatory actions is to stabilize the U.S. banking system. However, there can be no assurance as to the actual impact the EESA will have on the financial markets, including the extreme levels of volatility and limited credit availability currently being experienced by some institutions, and they may not have the desired effects. If the volatility in the markets continues and economic conditions fail to improve or continue to worsen, our business and consolidated financial condition and results of operations could be materially adversely affected.

The Department of Treasury is currently developing additional programs to further alleviate the ongoing financial crisis. There can be no assurance that we will be able to participate in any such future programs. If we are unable to participate or choose not to participate, it may have a material adverse effect on our competitive position and consolidated financial condition and results of operations.

We are subject to increases in FDIC insurance premiums and special assessments by the FDIC.

During 2008 and continuing in 2009, higher levels of bank failures have dramatically increased resolution costs of the FDIC and depleted the deposit insurance fund. In addition, the FDIC instituted two temporary programs to further insure customer deposits at FDIC insured banks: deposit accounts now are insured up to $250,000 per customer (up from $100,000) and noninterest-bearing transactional accounts are currently fully insured (unlimited coverage). These programs have placed additional stress on the Deposit Insurance Fund. In order to maintain a strong funding position and restore reserve ratios of the Deposit Insurance Fund, the FDIC has increased assessment rates of the insured institutions. In addition, on November 12, 2009, the FDIC adopted a rule requiring banks to prepay three years’ worth of estimated deposit insurance premiums by December 31, 2009. We are generally unable to control the amount of premiums that we are required to pay for FDIC insurance. If there are additional bank or financial institution failures, or the cost of resolving prior failures exceeds expectations, we may be required to pay even higher FDIC premiums than the recently increased levels. These announced increases and any future increases or required prepayments of FDIC insurance premiums may adversely impact our earnings and financial condition.

11

Unauthorized disclosure of sensitive or confidential client or customer information, whether through a breach of our computer system or otherwise, could severely harm our business.

As part of our financial and data processing products and services, we collect, process and retain sensitive and confidential client and customer information. Despite the security measures we have in place, our facilities and systems, and those of third party service providers, may be vulnerable to security breaches, acts of vandalism, computer viruses, misplaced or lost data, programming and/or human error, or other similar events. Any security breach involving the misappropriation, loss or other unauthorized disclosure of confidential information, whether by us or our vendors, could severely damage our reputation, expose us to the risks of litigation and liability, disrupt our operations and harm our business.

Customers may decide not to use banks to complete their financial transactions, which could result in a loss of income to us.

Technology and other changes are allowing customers to complete financial transactions that historically have involved banks at one or both ends of the transaction. For example, customers can now pay bills and transfer funds directly without going through a bank. The process of eliminating banks as intermediaries, known as disintermediation, could result in the loss of fee income, as well as the loss of customer deposits.

Our controls and procedures may fail or be circumvented.

Management regularly reviews and updates our internal controls, disclosure controls and procedures, and corporate governance policies and procedures. Any system of controls, however well-designed and operated, is based in part on certain assumptions and can provide only reasonable assurances that the objectives of the system are met. Any failure or circumvention of our controls and procedures or failure to comply with regulations related to controls and procedures could have a material adverse effect on our business, consolidated financial condition and results of operations.

We rely on the accuracy and completeness of information about customers or counterparties, and inaccurate or incomplete information could negatively impact our consolidated financial condition and results of operations.

In deciding whether to extend credit or enter into other transactions with customers and counterparties, we may rely on information provided to us by such customers and counterparties, including financial statements and other financial information. We may also rely on representations of customers and counterparties as to the accuracy and completeness of that information and, with respect to financial statements, on reports of independent auditors. Our financial condition and results of operations could be negatively impacted to the extent we rely on financial statements that do not comply with generally accepted accounting principles or that are inaccurate or misleading.

We are subject to examinations and challenges by taxing authorities.

In the normal course of business, we are routinely subjected to examinations and challenges from federal and state taxing authorities regarding the amount of taxes due in connection with our investments and the businesses in which we engage. Federal and state taxing authorities have recently become increasingly aggressive in challenging tax positions taken by financial institutions. These tax positions may relate to tax compliance, sales and use, franchise, gross receipts, payroll, property or income tax issues, including tax base, apportionment and tax planning. The challenges made by taxing authorities may result in adjustments to the timing or amount of taxable income or deductions or the allocations of income among tax jurisdictions. If any such challenges are not resolved in our favor, they could have a material adverse impact on our consolidated financial condition and results of operations.

We could experience an unexpected inability to obtain needed liquidity.

Liquidity measures the ability to meet current and future cash flow needs as they become due. The liquidity of a financial institution reflects its ability to meet loan requests, to accommodate possible outflows in deposits, and to take advantage of interest rate market opportunities. The ability of a financial institution to meet its current financial obligations is a function of its balance sheet structure, its ability to liquidate assets and its access to alternative sources of funds. We seek to ensure our funding needs are met by maintaining an appropriate level of liquidity through asset/liability management. If we become unable to obtain funds when needed, it could have a material adverse effect on our business and, in turn, our consolidated financial condition and results of operations.

A decline in our stock price could require a write-down of some portion or all of our goodwill.

If our stock price were to decline, or remain below our tangible book value for an extended period of time, we could be required to write off all or a portion of our goodwill, which represents our value in excess of our tangible book value. Such write-off would reduce earnings in the period in which it is recorded. Our stock price is subject to market conditions that can be impacted by forces outside the control of management, such as a perceived weakness in financial institutions in general, and may not be a direct result of our performance. A write-off of goodwill could have a material adverse effect on our consolidated financial condition and results of operations.

12

Future growth or operating results may require us to raise additional capital but that capital may not be available.

We are required by federal and state regulatory authorities to maintain adequate levels of capital to support our operations. To the extent our future operating results erode capital or we elect to expand through loan growth or acquisition, we may be required to raise capital.

Our ability to raise capital will depend on conditions in the capital markets, which are outside of our control, and on our financial performance. Accordingly, we cannot be assured of our ability to raise capital when needed or on favorable terms. If we cannot raise additional capital when needed, we will be subject to increased regulatory supervision and the imposition of restrictions on our growth and business. These could negatively impact our ability to operate or further expand our operations and may result in increases in operating expenses and reductions in revenues that could have a material effect on our consolidated financial condition and results of operations.

The holders of our junior subordinated debentures have rights that are senior to those of our shareholders.

On March 31, 2006, we issued $16.1 million of floating rate junior subordinated debentures in connection with a $16.1 million trust preferred securities issuance by our subsidiary, Baylake Capital Trust II. The 2006 junior subordinated debentures mature in March of 2036. The purpose of the transaction was to raise additional capital in order for us to redeem our trust preferred securities issued by our subsidiary Baylake Capital Trust I.

Payments of the principal and interest on the trust preferred securities are conditionally guaranteed by us. The junior subordinated debentures are senior to our shares of common stock. As a result, we must make payments on the junior subordinated debentures (and the related trust preferred securities) before any dividends can be paid on our common stock and, in the event of our bankruptcy, dissolution or liquidation, the holders of the debentures must be satisfied before any distributions can be made to the holders of our common stock. We have the right to defer distributions on the junior subordinated debentures (and the related trust preferred securities) for up to five years, during which time no dividends may be paid to holders of our common stock.

To the extent that we issue additional junior subordinated debentures in connection with an additional trust preferred securities issuance, the additional junior subordinated debentures will rank pari passu with our existing 2006 junior subordinated debentures and senior to our shares of common stock.

The holders of our convertible notes will have rights that are senior to those of our shareholders.

During the third and fourth quarter of 2009, we issued $5.35 million of our 10% Convertible Notes due June 30, 2017 (the “Convertible Notes”). The Convertible Notes are senior to our junior subordinated debentures issued in connection with trust preferred securities, as well as shares of our common stock. In the event of our bankruptcy, dissolution or liquidation, the holders of our Convertible Notes must be satisfied before any distributions can be made to the holders of our common stock.

Our securities are not an insured deposit.

Securities issued by us are not a bank deposit and are not insured or guaranteed by the FDIC or any other government agency. Your investment in our securities are subject to investment risk, and you must be capable of affording the loss of your entire investment.

The holding company cannot rely on dividends from Baylake Bank.

Our holding company is a separate and distinct legal entity from its subsidiaries. Historically, it has received substantially all of its revenue from dividends from Baylake Bank. Federal and/or state laws and regulations limit the amount of dividends that the Bank may pay to the holding company. Also, a holding company’s right to participate in a distribution of assets upon a subsidiary’s liquidation or reorganization is subject to the prior claims of the subsidiary’s creditors. In the event Baylake Bank is unable to pay dividends to the holding company, when needed, the holding company may not be able to service debt or pay its obligations, including dividends on the Trust Preferred Stock and Convertible Promissory Notes. The inability to receive dividends from Baylake Bank could have a material adverse effect on our business, financial condition and results of operations. Our recent losses have had the consequence of not allowing Baylake Bank to pay dividends to the parent company without prior regulatory approval.

We may not be able to attract and retain skilled people.

Our success depends, in large part, on our ability to attract and retain key people. Competition for the best people in most activities engaged in by us can be intense and we may not be able to hire people or retain them. The unexpected loss of services of one or more of our key personnel could have a material adverse impact on our business because of their skills, knowledge of our local markets, years of industry experience and the difficulty of promptly finding qualified replacement personnel.

We continually encounter technological change.

The financial services industry is continually undergoing rapid technological change with frequent introductions of new technology driven by products and services. The effective use of technology increases efficiency and enables financial institutions to better serve customers and to reduce costs. Our future success depends, in part, upon our ability to address the needs of our customers by using technology to provide products and services that will satisfy customer demands, as well as to create additional efficiencies in our operations. Many of our competitors have substantially greater resources to invest in technological improvements. We may not be able to effectively implement new technology driven products and services or be successful in marketing these products and services to our customers. Failure to successfully keep pace with technological change affecting the financial services industry could have a material adverse impact on our business and, in turn, our financial condition and results of operations.

Possible restrictions on bank overdraft programs could significantly reduce our deposit service charge income.

On November 12, 2009, the Federal Reserve Board announced final rules that prohibit institutions from charging consumers fees for paying overdrafts on automated teller machine (ATM) and one-time debit card transactions. The new rules require consumers to consent, or opt in, to the overdraft service for these two types of transactions before fees can be charged. We anticipate these new rules could significantly impact our nonsufficient funds and overdraft income the last two quarters of 2010 because of the required implementation dates of July 1 for new accounts and August 15 for existing accounts. A team is currently in place ensuring our systems are ready to meet the new rules. In addition, this team is working on a communication plan for existing accounts, which will educate our customers on the various overdraft options. Beyond this regulatory change, a bill has been introduced to the House which could place further restrictions on overdraft charges. If this bill or one similar to it passed, our service charge income could be reduced even further.

13

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

Our bank owns its headquarters and twenty-six branches and leases one branch office from a third party. The main office is located in Sturgeon Bay, Wisconsin and the branches are distributed by county as follows: eight in Brown County, seven in Door County, one in Green Lake County, four in Kewaunee County, one in Manitowoc County, one in Outagamie County, four in Waupaca County and one in Waushara County.

The main office building located in Sturgeon Bay serves as our corporate headquarters and main banking office. The main office also accommodates our expanded business, primarily an insurance agency (Baylake Insurance Agency) and brokerage service. The twenty-seven branches owned or leased by our bank are in good condition and considered adequate for present and near term requirements. In addition, our bank owns other real property that we do not consider in the aggregate to be material to our consolidated financial position. All of such other real property is reserved for future expansion and is located in the following Wisconsin municipalities: Berlin, Appleton, Neenah, and Oshkosh.

We may be involved from time to time in various routine legal proceedings incidental to our business. Neither we nor any of our subsidiaries is currently engaged in any legal proceedings that are expected to have a material adverse effect on our consolidated financial statements.

14

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Historically, trading in shares of our common stock has been limited. Since mid-1993, our common stock has been quoted on the OTC Bulletin Board (Trading symbol: BYLK.OB), an electronic interdealer quotation system providing real-time quotations on eligible securities.

The following table summarizes high and low bid prices and cash dividends declared for our common stock for the periods indicated. Bid prices are as reported from the OTC Bulletin Board. The reported high and low prices represent interdealer bid prices, without retail mark-up, mark-downs or commission, and may not necessarily represent actual transactions.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Calendar period |

|

High |

|

Low |

|

Cash dividends per |

|

|||||

|

2008 |

|

|

1st Quarter |

|

$ |

11.75 |

|

$ |

8.55 |

|

$ |

— |

|

|

|

|

|

|

2nd Quarter |

|

$ |

9.05 |

|

$ |

6.00 |

|

$ |

— |

|

|

|

|

|

|

3rd Quarter |

|

$ |

6.75 |

|

$ |

4.00 |

|

$ |

— |

|

|

|

|

|

|

4th Quarter |

|

$ |

6.75 |

|

$ |

3.50 |

|

$ |

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2009 |

|

|

1st Quarter |

|

$ |

5.05 |

|

$ |

1.55 |

|

$ |

— |

|

|

|

|

|

|

2nd Quarter |

|

$ |

4.95 |

|

$ |

1.85 |

|

$ |

— |

|

|

|

|

|

|

3rd Quarter |

|

$ |

4.20 |

|

$ |

2.99 |

|

$ |

— |

|

|

|

|

|

|

4th Quarter |

|

$ |

3.75 |

|

$ |

2.50 |

|

$ |

— |

|

|

We had approximately 1,746 shareholders of record at March 12, 2010. The number of shareholders does not separately reflect persons or entities that hold their stock in nominee or “street” name through various brokerage firms.

The holders of our common stock are entitled to receive such dividends when and as declared by our Board of Directors and approved by our regulators. In determining the payment of cash dividends, our Board of Directors considers the earnings, capital and debt servicing requirements, financial ratio guidelines issued by the FRB and other banking regulators, our financial condition, and other relevant factors.

Our ability to pay dividends is dependent upon our receipt of dividends from our subsidiary bank, which is subject to regulatory restrictions. Such restrictions, which govern state-chartered banks, generally limit the payment of dividends on bank stock to the bank’s undivided profits after all payments of all necessary expenses, provided that the bank’s surplus equals or exceeds its capital, as discussed further in Item 7, Management Discussion and Analysis of Financial Condition and Results of Operation-Capital Resources. In addition, under the terms of our junior subordinated debentures due 2036, we would be precluded from paying dividends on our common stock if we were in default under the Debentures, if we exercised our right to defer payments of interest on the Debentures, or if certain related defaults occurred.

Through 2007, cash dividends on our common stock had historically been paid on a quarterly basis in March, June, September and January. No cash dividends were declared during 2008 and 2009 versus total cash dividends of $0.64 per share declared during 2007. Beginning in February 2008, our Board of Directors, in consultation with our federal and state bank regulators, elected to forego the payment of cash dividends on our common stock. The payment of dividends in relationship to our financial position continues to be monitored on a quarterly basis and our intentions are to reinstate payment of dividends at the earliest appropriate opportunity. However, there is no assurance if or when we will be able to do so or if we do, in what amounts. In order to pay dividends, we will need to seek approval from the WDFI as well as the FRB.

In the event and at such time as we do resume payment of quarterly dividends, we maintain a dividend reinvestment plan enabling participating shareholders to elect to purchase shares of our common stock in lieu of receiving cash dividends. Such shares may be newly issued or acquired by us in the open market. New shares issued under this plan are limited to 1 million over the life of the plan.

15

On August 14, 2009 and September 30, 2009, we completed closings for a private placement of 10% Convertible Notes due June 30, 2017 (the “Convertible Notes”). Additional closings occurred on November 1, 2009 and December 31, 2009. The Convertible Notes were offered and sold primarily to “accredited investors” as defined in Securities Act of 1933 and up to 35 non-accredited investors in reliance on the exemption from registration under Section 4(2) of the Securities Act of 1933, as amended and Rule 506 promulgated thereunder. At the closings, we issued in aggregate $5.4 million of Convertible Notes. The proceeds of this financing will be contributed, in part, as additional capital to Baylake Bank and otherwise used for general corporate purposes.

The Convertible Notes accrue interest at a fixed rate of 10% per annum upon issuance and until maturity or earlier conversion or redemption. Interest is payable quarterly, in arrears, on January 1, April 1, July 1, and October 1, of each year, commencing October 1, 2009. The Convertible Notes are convertible into shares of our common stock at a conversion ratio of one share of common stock for each $5.00 in aggregate principal amount held on the record date of the conversion subject to certain adjustments as described in the Convertible Notes. Prior to October 1, 2014, each holder of the Convertible Notes may convert up to 100% (at the discretion of the holder) of the original principal amount into shares of our common stock at the conversion ratio. On October 1, 2014, one-half of the original principal amounts are mandatorily convertible at the conversion ratio if conversion has not occurred. The principal amount of any Convertible Note that has not been converted or redeemed will be payable at maturity on June 30, 2017. We are not obligated to register the common stock related to the conversion of the Convertible Notes.

We sold $1.15 million of the Convertible Notes without registration during the fourth quarter of 2009.

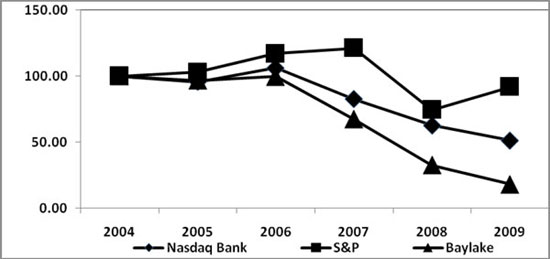

Performance Graph

The following graph shows the cumulative stockholder return on our common stock over the last five fiscal years compared to the returns of Standard & Poors 500 Stock Index and the NASDAQ Bank Index, prepared for NASDAQ by the Center for Research in Securities Prices at the University of Chicago.

Cumulative Total Return(1)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

At December 31, |

|

||||||||||||||||

|

|

|

2004 |

|

2005 |

|

2006 |

|

2007 |

|

2008 |

|

2009 |

|

||||||

|

Baylake Corp. |

|

|

100.00 |

|

|

96.90 |

|

|

99.87 |

|

|

67.41 |

|

|

32.57 |

|

|

18.24 |

|

|

NASDAQ Bank Index |

|

|

100.00 |

|

|

95.67 |

|

|

106.20 |

|

|

82.76 |

|

|

62.96 |

|

|

51.31 |

|

|

S&P 500 |

|

|

100.00 |

|

|

103.00 |

|

|

117.03 |

|

|

121.16 |

|

|

74.53 |

|

|

92.01 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(1) |

Assumes $100 invested on December 31, 2004 in each of Baylake Corp. common stock, the Standard & Poors 500 Stock Index and the NASDAQ Bank Index. Dividends are assumed to be reinvested. |

16

ITEM 6. SELECTED FINANCIAL DATA

BAYLAKE CORP.

FIVE YEAR SELECTED CONSOLIDATED FINANCIAL DATA

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year Ended December 31, |

|

|

|

|

|

|

|

|||||||

|

|

|

2009 |

|

2008 |

|

2007 |

|

2006 |

|

2005 |

|

|||||

|

|

|

(dollars in thousands, except per share data) |

|

|||||||||||||

|

|

||||||||||||||||

|

Results of operations: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest and dividend income |

|

$ |

47,468 |

|

$ |

57,276 |

|

$ |

69,668 |

|

$ |

70,014 |

|

$ |

61,538 |

|

|

Interest expense |

|

|

18,259 |

|

|

28,227 |

|

|

38,753 |

|

|

36,378 |

|

|

26,660 |

|

|

Net interest income |

|

|

29,209 |

|

|

29,049 |

|

|

30,915 |

|

|

33,636 |

|

|

34,878 |

|

|

Provision for loan losses |

|

|

6,500 |

|

|

17,961 |

|

|

9,761 |

|

|

903 |

|

|

3,217 |

|

|

Net interest income after provision for loan losses |

|

|

22,709 |

|

|

11,088 |

|

|

21,154 |

|

|

32,733 |

|

|

31,661 |

|

|

Non-interest income |

|

|

12,485 |

|

|

9,257 |

|

|

9,174 |

|

|

9,737 |

|

|

11,597 |

|

|

Non-interest expense: |

|

|

29,978 |

|

|

38,022 |

|

|

32,578 |

|

|

32,329 |

|

|

30,519 |

|

|

Income (loss) before provision (benefit) for income taxes |

|

|

5,216 |

|

|

(17,677 |

) |

|

(2,250 |

) |

|

10,141 |

|

|

12,739 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Income tax provision (benefit) |

|

|

887 |

|

|

(7,860 |

) |

|

(2,416 |

) |

|

2,765 |

|

|

3,836 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) |

|

$ |

4,329 |

|

$ |

(9,817 |

) |

$ |

166 |

|

$ |

7,376 |

|

$ |

8,903 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Per Share Data: (1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) per share (basic)(1) |

|

$ |

.55 |

|

$ |

(1.24 |

) |

$ |

0.02 |

|

$ |

0.95 |

|

$ |

1.15 |

|

|

Net income (loss) per share (diluted)(1) |

|

|

.55 |

|

|

(1.24 |

) |

|

0.02 |

|

|

0.94 |

|

|

1.14 |

|

|

Cash dividends per common share |

|

|

— |

|

|

— |

|

|

0.64 |

|

|

0.64 |

|

|

0.61 |

|

|

Book value per share at end of period |

|

|

9.43 |

|

|

8.72 |

|

|

10.18 |

|

|

10.50 |

|

|

10.09 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Selected Financial Condition Data (at December 31): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets |

|

$ |

1,044,457 |

|

$ |

1,062,913 |

|

$ |

1,106,616 |

|

$ |

1,111,684 |

|

$ |

1,089,408 |

|

|

Securities |

|

|

204,834 |

|

|

225,417 |

|

|

222,475 |

|

|

188,315 |

|

|

171,638 |

|

|

Gross loans |

|

|

651,894 |

|

|

728,722 |

|

|

760,210 |

|

|

819,568 |

|

|

812,296 |

|

|

Total deposits |

|

|

831,629 |

|

|

849,758 |

|

|

884,185 |

|

|

878,911 |

|

|

856,711 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Short-term borrowings (2) |

|

|

21,122 |

|

|

30,174 |

|

|

27,174 |

|

|

4,480 |

|

|

1,315 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other borrowings (3) |

|

|

85,000 |

|

|

85,095 |

|

|

85,172 |

|

|

115,179 |

|

|

125,185 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Subordinated debentures |

|

|

16,100 |

|

|

16,100 |

|

|

16,100 |

|

|

16,100 |

|

|

16,100 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Convertible promissory notes |

|

|

5,350 |

|

|

— |

|

|

— |

|

|

— |

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total shareholders’ equity |

|