Attached files

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

———————

FORM

10-K

———————

þ ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the

fiscal year ended December 31, 2009

Commission

file number: 000-51354

| AE BIOFUELS, INC. |

| (Exact name of registrant as specified in its charter) |

|

Nevada

|

26-1407544

|

|

|

(State

or other jurisdiction of

incorporation

or organization)

|

(I.R.S.

Employer

Identification

Number)

|

20400

Stevens Creek Blvd., Suite 700

Cupertino,

California 95014

(Address

of principal executive offices)

Registrant’s

telephone number (including area code): (408) 213-0940

Securities

registered under Section 12(g) of the Exchange Act:

Common

Stock, Par Value $.001

(Title of

class)

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. Yes o No

þ

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or Section 15(d) of the Securities Exchange Act of 1934

during the preceding 12 months (or for such shorter period that the registrant

was required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days. Yes þ No

o

Indicate by check mark whether the registrant has submitted

electronically and posted on its corporate Web site, if any, every Interactive

Data File required to be submitted and posted pursuant to Rule 405 of Regulation

S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such

shorter period that the registrant was required to submit and post such files).

Yes þ

No o

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K (§229.405 of this chapter) is not contained herein, and will not

be contained, to the best of registrant’s knowledge, in definitive proxy or

information statements incorporated by reference in Part III of this Form 10-K

or any amendment to this Form 10-K. o

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting company. See

the definitions of “large accelerated filer,” “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large

accelerated filer

|

o

|

Accelerated

filer

o

|

|

Non-accelerated

filer

(Do

not check if a smaller reporting company)

|

o

|

Smaller

reporting company

þ

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). Yes o

No þ

The

aggregate market value of the voting and non-voting common equity held by

non-affiliates of the registrant was approximately $9,265,234 as of June 30,

2009, the registrant’s most recently completed second fiscal quarter, based on

the average bid and asked price on the Over-The-Counter Bulletin Board reported

for such date. This calculation does not reflect a determination that certain

persons are affiliates of the registrant for any other purpose.

The

number of shares outstanding of the registrant’s Common Stock on March 3, 2010

was 86,181,532 shares.

DOCUMENTS

INCORPORATED BY REFERENCE

None

TABLE OF CONTENTS

|

Page

|

||||

|

PART

I

|

||||

|

Special

Note Regarding Forward-Looking Statements

|

1

|

|||

|

Item

1. Business

|

1

|

|||

|

Item

1A. Risk Factors

|

12

|

|||

|

Item

2. Properties

|

23

|

|||

|

Item

3. Legal Proceedings

|

23

|

|||

|

PART

II

|

||||

|

Item

5. Market for Registrant's Common Equity, Related Stockholder Matters

and Issuer Purchases of Equity Securities

|

24

|

|||

|

Item

7. Management’s Discussion and Analysis of Financial Condition and Results

of Operations

|

25

|

|||

|

Item

8. Financial Statements and Supplementary Data

|

35

|

|||

|

Item

9. Changes in and Disagreements with Accountants on Accounting and

Financial Disclosure

|

35

|

|||

|

Item

9A(T). Controls and Procedures

|

35

|

|||

|

Item

9B. Other Information

|

37

|

|||

|

PART

III

|

||||

|

Item

10. Directors, Executive Officers and Corporate Governance

|

38

|

|||

|

Item

11. Executive Compensation

|

43

|

|||

|

Item

12. Security Ownership of Certain Beneficial Owners and Management and

Related Stockholder Matters

|

47

|

|||

|

Item

13. Certain Relationships and Related Transactions, and Director

Independence

|

48

|

|||

|

Item

14. Principal Accounting Fees and Services

|

49

|

|||

|

PART

IV

|

||||

|

Item

15. Exhibits and Financial Statement Schedules

|

50

|

|||

|

Index

to Financial Statements

|

52

|

|||

|

SIGNATURES

|

80

|

|||

PART

I

|

SPECIAL

NOTE REGARDING FORWARD—LOOKING

STATEMENTS

|

On one or

more occasions, we may make forward-looking statements in this Annual Report on

Form 10-K regarding our assumptions, projections, expectations, targets,

intentions or beliefs about future events. Words or phrases such as

“anticipates,” “may,” “will,” “should,” “believes,” “estimates,” “expects,”

“intends,” “plans,” “predicts,” “projects,” “targets,” “will likely result,”

“will continue” or similar expressions identify forward-looking statements.

These forward-looking statements are only our predictions and involve numerous

assumptions, risks and uncertainties, including, but not limited to those

business risks and factors described in Part I, Item 1A-Risk Factors and

elsewhere in this report and our other Securities and Exchange Commission

filings.

We

undertake no obligation to publicly update or revise any forward-looking

statements, whether as a result of new information, future events or otherwise.

However, your attention is directed to any further disclosures made on related

subjects in our subsequent annual and periodic reports filed with the Securities

and Exchange Commission on Forms 10-K, 10-Q and 8-K and Proxy Statements on

Schedule 14A.

We

obtained the market data used in this report from internal company reports and

industry publications. Industry publications generally state that the

information contained in those publications has been obtained from sources

believed to be reliable but their accuracy and completeness are not guaranteed

and their reliability cannot be assured. Although we believe market data used in

this 10-K is reliable, it has not been independently verified. Similarly, while

we believe internal company reports are reliable, we have not had the content of

these reports independently verified.

Unless

the context requires otherwise, references to “we,” “us,” “our,” and “the

Company” refer specifically to AE Biofuels, Inc. and its subsidiaries.

ITEM 1.

BUSINESS

General

We are an

international biofuels company focused on the development, acquisition,

construction and operation of next-generation fuel grade ethanol and biodiesel

facilities, and the distribution, storage, and marketing of biofuels. We

currently operate a biodiesel manufacturing facility with a nameplate capacity

of 55 million gallons per year (MGY) in Kakinada, India and have a

next-generation integrated cellulose and starch ethanol demonstration facility

in Butte, Montana. On

December 1, 2009, the Company and two of our wholly owned subsidiaries, AE

Advanced Fuels, Inc. and AE Advanced Fuels Keyes, Inc. entered into a Project

Agreement and Lease Agreement with Cilion, Inc. the owner of a 55 million gallon

per year (MGY) ethanol plant in Keyes, California. Under the Project Agreement,

the Company agreed to provide $1.6 million and Cilion, Inc. agreed to provide

$1.0 million to retrofit the Plant. Under the terms of the Lease

Agreement, AE Advanced Fuels Keyes, Inc. will lease the Plant for a term of up

to thirty-six (36) months commencing upon substantial completion of the retrofit

activities. The Company raised the $1.6 million in January 2010 and on March 15,

2010, received one-half of Cilion’s funds and took possession of the Keyes

plant. After we bring the Keyes plant back into production using traditional

feedstocks, we intend to utilize the plant to commercialize our proprietary,

patent pending enzyme technology. Our plan includes designing,

constructing and operating a next-generation integrated cellulose and starch

ethanol production facility at the Keyes plant to utilize available agricultural

waste feedstocks from the surrounding central valley region of California.

Our implementation of the enzyme technology is subject to approval by the

owners of the plant and will need to be financed through either cash flows from

the plant or from a debt or equity raise. There can be no assurances

that we will obtain the necessary approval by the owners of the plant or that we

will be successful in raising sufficient funds needed to finance the

implementation of the enzyme technology.

The

Company has 56 full-time equivalent employees in offices or plant sites in

Cupertino, California; Keyes, California; Butte, Montana; Kakinada, India and

Hyderabad, India.

Our

mailing address and executive offices are located at 20400 Stevens Creek Blvd.,

Suite 700, Cupertino, California 95014. Our telephone number is (408) 213-0940.

Our corporate website is www.aebiofuels.com. Our Annual Reports on Form 10-K,

Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to

those reports filed or furnished pursuant to Section 13(a) or 15(d) of the

Securities Exchange Act of 1934, as amended, are available free of charge on our

website when such reports are available on the U.S. Securities and Exchange

Commission (“SEC”) website. The public may read and copy any materials we file

with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington,

D.C. 20549. The public may obtain information on the operation of the Public

Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains a website

at www.sec.gov that contains reports, proxy and information statements, and

other information regarding issuers that file electronically with the SEC. The

content of any website referred to in this Form 10-K is not incorporated by

reference into this filing. Further, our references to the URLs for these

websites are intended to be inactive textual references only.

1

Products

and Segments

We review

separate financial information for each geographic region of our business. We

currently have two regions that are operating: India and North America. The two

operating reporting segments and our Other segment are defined as

follows:

|

|

●

|

The

“India” operating segment encompasses our 50 MGY nameplate capacity

biodiesel manufacturing plant in Kakinada, the administrative offices in

Hyderabad, and holding companies in Nevada and Mauritius. We currently

market and sell our biodiesel to customers in India and to Europe. We

employ our own sales force to sell biodiesel directly to end users and

through independent brokers. For the year ended December 31, 2009 and

2008, revenues from our Indian operations were 100% of total net revenues.

Indian revenues consist of domestic sales within India of biodiesel and

glycerin (a byproduct of biodiesel production) to industrial users,

brokers and local retailers. Export revenues consist of sales of biodiesel

to fuel blenders in Europe. The majority of our consolidated assets as of

December 31, 2009 were attributable to our Indian

operations.

|

|

|

●

|

The

“North America” operating segment encompasses the commercialization of our

proprietary, patent-pending enzyme technology at our integrated cellulose

and starch ethanol demonstration facility in Butte, Montana, land held for

next-generation ethanol plant development in Sutton, Nebraska and our

operations at the ethanol plant in Keyes,

California.

|

|

|

●

|

The

“Other” segment encompasses our costs associated with new market

development, company-wide fund raising, executive compensation and other

corporate expenses.

|

For

revenue and other information regarding the aforementioned segments and for

additional geographic information on our revenues and long-lived assets, see

Note 14 — “Segment Information,” of the Notes to Consolidated Financial

Statements, which is incorporated herein by reference. Also, for a discussion of

the risks attendant to our Indian operations, see “Part I, Item 1A-Risk

Factors,” which is incorporated herein by reference.

Biofuels

Market

Ethanol

Market in the United States

In the

United States ethanol is primarily used as a clean air additive, an octane

enhancer and a renewable fuel extender. Ethanol is blended with gasoline (i) as

an oxygenate to help meet fuel emission standards, (ii) to improve gasoline

performance by increasing octane levels and (iii) to extend fuel supplies. A

growing amount of ethanol is also sold as E85, a renewable fuels-driven blend

comprised of up to 85% ethanol, with the remainder being

gasoline. E85 fuel is sold for use in flexible fuel

vehicles.

Ethanol

is generally sold through short-term contracts. Today, the majority

of ethanol sold in the United States is priced based upon a spot index price at

the time of shipment. The price of ethanol has historically moved in relation to

the price of wholesale crude oil and refined gasoline and the value of the

Volumetric Ethanol Excise Tax Credit (“VEETC”). The price of ethanol

over the last two years has been largely driven by wholesale crude oil, refined

gasoline, and the price of corn.

The fuel

ethanol industry in the United States experienced rapid growth over the past

decade, increasing from 1.4 billion gallons produced in 1998 to approximately

10.6 billion gallons produced in 2009, reaching a record 761,000 barrels per day

in November 2009. In January 2010, operating ethanol production

capacity stood at 11.8 billion gallons annually, with an additional 1.4 billion

gallons of annual capacity under construction for a total of 14.4 billion

gallons. Ethanol blends accounted for approximately 6.3% of the U.S. gasoline

supply in 2008. U.S. ethanol industry supports nearly 400,000 jobs and

added $53.3 billion to the nation’s gross domestic product (GDP). The

combination of increased GDP and higher household income contributed $8.4

billion in tax revenue for the federal government and nearly $7.5 billion in tax

revenue for state and local governments'.

Factors Driving Increase in

Ethanol Usage

Renewable Fuel Standard

(RFS): The growth in the United States ethanol industry during the last

decade and the expected continued growth in the ethanol industry over future

decades is largely driven by laws mandating the use of renewable fuels,

including ethanol. For example, The Energy Independence and Security

Act of 2007, signed into law on December 19, 2007, mandated the use of 11.1

billion gallons of renewable fuels in 2009 increasing to 12.95 billion gallons

in 2010 and 36 billion gallons by 2022. The upper range mandate for corn based

ethanol is 15 billion gallons by 2022. In addition, the RFS mandate

for cellulosic biofuels in 2022 is 16 billion gallons per year.

The U.S.

Environmental Protection Agency (EPA) released its final rule for the expanded

Renewable Fuels Standard (RFS2) on February 3, 2010. Based on additional

internal analysis, public comments from stakeholders, and comments from peer

reviewers, the EPA made numerous modifications to the proposed regulations. Most

of the changes are minor in nature and the general complexion of the rule

remains unchanged (e.g., indirect land use change, renewable biomass

requirements, and other controversial elements remain largely intact), but

several modifications have notable implications for the ethanol industry.1

2

The

Renewable Fuel Standard's revised statutory requirements establish new specific

annual volume standards for cellulosic biofuel, biomass-based diesel, advanced

biofuel, and total renewable fuel that must be used in transportation fuel. The

revised statutory requirements also include new definitions and criteria for

both renewable fuels and the feedstocks used to produce them, including new

greenhouse gas (GHG) emission thresholds as determined by lifecycle analysis

(LCA). Central provision requires that all biofuels produced under the program

meet certain greenhouse gas performance thresholds in order to qualify for

generating Renewable Identification Numbers (RINs). In order to

qualify for the volume categories, fuels must demonstrate that their 'fuel

pathways' meet or exceed the respective required minimum lifecycle GHG

thresholds as compared to the baseline for gasoline and diesel. These

thresholds are: 20% for 'renewable fuel,' 50% for 'advanced biofuel,' 50% for

'Biomass-based diesel,' and 60% for 'cellulosic biofuel.' Compliance

with each threshold requires comprehensive evaluation of the renewable fuels

produced, on the basis of lifecycle emissions, including direct emissions and

indirect emissions such as emissions from indirect land use changes

(ILUC). The Final Rule contains improved GHG performance calculations

for corn ethanol, which include updated models, expanded satellite data, and

available land types, yielding an aggregate improvement effect of reducing by

half the emissions from ILUC as compared to earlier versions of the rule.2

Economics of ethanol

blending: As crude oil prices experienced extreme fluctuations in the

commodities marketplace from 2007 - 2009, the price of gasoline also experienced

volatility. The price per gallon of ethanol during this same time period,

although increasing, did not keep pace with the increase in the price of

gasoline. This phenomenon created an opportunity for refiners and blenders to

increase the profitability of the gasoline they sold by blending ethanol in

amounts in excess of mandated levels (although not in excess of 10%). This

discretionary blending was a driving force behind the rapid growth in the

consumption of ethanol in 2007 and the first half of 2008. The profitability of

blending ethanol was further enhanced by the VEETC, which was then $0.51 for

each gallon of ethanol blended. However, as the price of oil began to fall

rapidly in the second half of 2008 through the first half of 2009, discretionary

blending above mandated levels was no longer profitable and diminished

significantly. In the second half of 2009 and in early 2010, crude

oil prices increased, creating a more favorable discretionary blending

market for ethanol producers, again.

Renewable Identification

Number credits (“RINS”): Refiners, importers and blenders (other than

oxygen blenders) of gasoline are obligated parties under the Renewable Fuels

Standard (RFS). These obligated parties are allowed to meet their requirement to

consume renewable fuels through the accumulation or purchase of excess RINS,

instead of from the actual physical purchase of renewable fuels. As of February

2010, the U.S. EPA is still finalizing revisions to the National Renewable Fuel

Standard program (commonly known as the RFS program). This rule makes changes to

the Renewable Fuel Standard program as required by the Energy Independence and

Security Act of 2007 (EISA). The revised statutory requirements establish new

specific annual volume standards for cellulosic biofuel, biomass-based diesel,

advanced biofuel, and total renewable fuel that must be used in transportation

fuel. The revised statutory requirements also include new definitions and

criteria for both renewable fuels and the feedstocks used to produce them,

including new greenhouse gas emission (GHG) thresholds as determined by

lifecycle analysis. The regulatory requirements for RFS will apply to domestic

and foreign producers and importers of renewable fuel used in the

U.S.

Emission reduction:

Ethanol is an oxygenate which, when blended with gasoline, reduces

vehicle emissions. Ethanol’s high oxygen content burns more completely, emitting

fewer pollutants into the air. Ethanol demand increased substantially beginning

in 1990 when federal law began requiring the use of oxygenates (such as ethanol

or methyl tertiary butyl ether (“MTBE”)) in reformulated gasoline in cities with

unhealthy levels of air pollution on a seasonal or year round basis. Although

the federal oxygenate requirement was eliminated in May 2006 as part of the

Energy Policy Act of 2005, oxygenated gasoline continues to be used in order to

help meet separate federal and state air emission standards. Due to significant

environmental concerns involving groundwater contamination, the refining

industry has all but abandoned the use of MTBE, a competing product to ethanol,

making ethanol the primary clean air oxygenate currently used.

Octane Enhancer:

Ethanol, with an octane rating of 113, is used to increase the octane

value of gasoline with which it is blended. It is used as an octane enhancer

both for producing regular grade gasoline from lower octane blending stocks

(including both reformulated gasoline blendstock for oxygenate blending (“RBOB”)

and conventional gasoline blendstock for oxygenate blending (“CBOB”)), and for

upgrading regular gasoline to premium grades.

2 Source: EPA RFS2 summary.

3

Fuel stock extender:

According to the Energy Information Administration (EIA), while domestic

petroleum refinery output has increased by approximately 29% from 1980 to 2008,

domestic gasoline consumption has increased 36% over the same period. By

blending ethanol with gasoline, refiners are able to meet increased demand and

expand the overall volume and sale of gasoline.

Biodiesel

Market in India and

Europe

Indian Biodiesel

Market

India is

the world’s fifth largest consumer of energy, according to the Brookings

Institute, and by 2030 it is expected to become the third largest, overtaking

Japan and Russia. While global oil demand is expected to increase at an annual

average rate of 1.6%, India’s demand for oil is expected to increase at an

average rate of 2.9% annually over the next quarter century.

In India,

oil and its products are used in the transport, commercial, industrial, and

domestic sectors. As India’s power grids fail to provide a reliable and

consistent source of electricity, diesel is also being used in captive power

generation, as well as to power irrigation for agriculture. The gap between

India’s consumption and production of oil is widening. India imports

over 70% of its oil. India has only 0.4% of the world’s proven reserves and the

International Energy Agency (IEA) estimates that India’s oil production will

continue to decline. As a result, India’s dependence on foreign oil is projected

to grow to 90% over the next 15 or 20 years.

The

Indian government is becoming increasingly concerned about the country’s

consumption of fossil fuel and petroleum products because of (i) the huge export

of funds to pay for these oil imports, (ii) increasing pollution and

environmental hazards, and (iii) concerns over the declining state of the

country’s environment and the health of its citizens. The Indian government

views biofuels as good substitutes for oil in the transportation sector. As a

result, mandates have been instituted as a solution to the country’s

environmental problems, energy security, desire to reduce imports and increase

rural employment, and desire to improve the country’s agricultural

economy.

On

September 11, 2008, the Indian government approved a National Policy on

Biofuels. The National Policy on Biofuels in part:

|

|

●

|

Establishes

a National Biofuel Coordination Committee, headed by the Prime Minister of

India and a Biofuel Steering Committee headed by a Cabinet

Secretary;

|

|

|

●

|

Establishes

a biofuel blending target of 20% by 2017, including ethanol and

biodiesel;

|

|

|

●

|

Encourages

biodiesel production from non-edible

sources;

|

|

|

●

|

Recommends

establishing a minimum purchase price for biodiesel linked to the

prevailing retail diesel

price;

|

|

|

●

|

Recommends

that biofuels be brought under the ambit of “Declared Goods” to ensure

unrestricted movement within and outside India;

and

|

|

|

●

|

Recommends

that no taxes and duties should be levied on

biodiesel.

|

India's

Minister of State for Petroleum & Natural Gas has informed the Council of

States in a written reply that under the terms of the Motor Spirit and High

Speed Diesel Order, 2005, all the State Governments/Union Territories have been

advised to take suitable action immediately in order to curb unauthorized

marketing of bio-diesel for use as transportation fuel, Indian Government News

reports.

The

Minister stated that his Ministry has formulated the Bio-diesel Purchase Policy

to lend support to the activities for blending of bio-diesel in diesel and

marketing of such blended fuel. As per Bio-diesel Purchase Policy, the Public

Sector Oil Marketing Companies (OMCs) shall purchase bio-diesel (B100), through

its selected twenty purchase centers, which meet the fuel quality standard

prescribed in the Bureau of Indian Standards specification at a price declared

by OMCs periodically. He also said that the present orders and policies do not

allow the manufactures of bio-diesel to resort to direct retail marketing of

B-100 product to automobile vehicles fitted with spark ignition engines or

compression ignition engines.3

European

Biodiesel Market

Europe is

the world’s largest producer and consumer of biodiesel, yet it consumes much

more that is able to produce and therefore imports biodiesel. Higher

blending obligations in some European countries (Bulgaria, Finland, France,

Germany, Hungary, Poland, Portugal, the Netherlands, Slovakia, Spain, Sweden,

United Kingdom) are expected to boost biodiesel consumption in 2010

and beyond. Industry experts forecast a double digit increase in consumption of

biodiesel in 2010 in Europe. Imports of biodiesel into Europe were expected to

reach over 50,000,000 gallons in 2009.

4

Imports

of Asian based biodiesel are expected to increase significantly in 2010 due

to the projected increase in biodiesel usage in Europe, combined with the

reduction of the amount of biodiesel imported from the United States. Imports

from the U.S. dropped significantly in early 2009 as a result

of antidumping duties implemented by place in March

2009. The duties are in place for five years.

Benefit

of Biodiesel

Biodiesel

is a biodegradable fuel produced from renewable sources such as vegetable oils

or animal fats. In the U.S., Europe and India, biodiesel is generally blended

with petroleum diesel, though it is also used in its pure form as a diesel

substitute. Biodiesel is gaining popularity as an alternative fuel in India

because it:

|

|

●

|

is

more environmentally friendly than petroleum-based diesel fuel, as

biodiesel has been shown to reduce greenhouse gas, carbon monoxide,

particulate matter and hydrocarbon

emissions;·

|

|

|

●

|

reduces

dependence on imported oil and extends diesel fuel supplies. The U.S.,

Europe and India are currently net importers of crude oil and other fuel

supplies;

|

|

|

●

|

has

excellent engine lubrication characteristics, even when blended with

diesel fuel at low blend rates such as 1% or

2%;

|

|

|

●

|

can

be used in existing diesel engines generally with no or minor engine

modifications;

|

|

|

●

|

is

compatible with the existing diesel fuel distribution infrastructure;

and

|

|

|

●

|

can

be produced from a wide variety of renewable feedstocks including

vegetable oils, such as soybean and palm, or animal

fats.

|

Strategy

Our goal

is to be a leader in the production of next-generation fuels to meet the

increasing demand for renewable, high-octane transportation fuels, and to reduce

dependence on petroleum-based energy sources in an environmentally responsible

manner.

India

The

Company owns and operates a biodiesel production facility in Kakinada with a

nameplate capacity of 50 MGY. This facility is one of the largest biodiesel

production facilities in India on a nameplate capacity basis. Our objective is

to build on our leading market position in India and to continue to capitalize

on the substantial growth potential of the industry. Key elements of our

strategy include the following:

|

|

●

|

Expand market demand for

biodiesel and its byproducts. We plan to create additional demand

for biodiesel by continuing to produce and market high quality biodiesel

and expand the awareness and acceptance of our product. We intend to

expand our sales channels into neighboring states and large population

centers within India. We also expect to increase sales by selling our

biodiesel into the international market during the summer months when

diesel and biodiesel use in Europe and the United States increases with

the onset of warmer weather.

|

|

|

●

|

Diversify our

feedstocks. We designed our Kakinada plant with the capability of

producing biodiesel from multiple-feedstocks. In 2008 we produced

biodiesel from refined palm oil and in 2009 we began to produce biodiesel

from palm stearin. Being able to reliably produce, on a continuous-flow

basis, biodiesel from multiple feedstocks that meets our customers’

specifications will mitigate the effect of commodity price

volatility.

|

|

|

●

|

Pursue strategic investment

opportunities. We believe that there will be opportunities to

expand our business as the biodiesel industry in India continues to grow,

either by acquisitions of other plants or additional capital investment.

We will continue to evaluate opportunities to acquire or invest in

additional biodiesel production and distribution facilities or biodiesel

or other renewable energy production and design technologies in India and

internationally.

|

5

North

America

In 2007,

we acquired patent-pending enzyme technology that allows us to produce ethanol

from a combination of starch and cellulose, or from cellulose alone (“AE

Technology”). Our objective is to build on our position as a developer of

cellulosic ethanol technology and to expand the production of cellulosic ethanol

in the U.S. Key elements of our strategy is to deploy our proprietary,

patent-pending enzyme technology at existing corn ethanol plants or in

stand-alone, cellulose-only, ethanol plants in the U.S. Our unique

approach is to integrate our patent-pending enzyme technology with existing corn

ethanol plants to create integrated cellulose and starch ethanol facilities. We

believe this approach will enable existing producers to immediately reduce

operating expenses by lowering energy costs and water consumption, as well as

lowering feedstock costs by replacing up to 25% of the total feedstock with

cellulosic sources which may include wheat straw or corn stover. By employing

this flexible approach, the Company can address different segments of the same

market (legacy businesses and new businesses), therefore minimizing the risk of

becoming captive to a single approach or technology.

We

anticipate our first deployment of our technology will be at the 55 MGY ethanol

plant in Keyes, California. On December 1, 2009, the Company and two

of our wholly owned subsidiaries, AE Advanced Fuels, Inc. and AE Advanced Fuels

Keyes, Inc. entered into a Project Agreement and Lease Agreement with Cilion,

Inc. Under the terms of the Lease Agreement AE Advanced Fuels Keyes, Inc. will

lease the Plant for a term of up to thirty-six (36) months. The Lease

term and rental payments begin upon substantial completion of certain repair and

retrofit activities, determined by mutual agreement of the parties. Our project

company that will be operating the Keyes Plant during the lease term will have a

royalty-free, site specific license to the AE Technology that runs coterminous

with the term of the lease. We plan to use the AE Technology to design, engineer

and construct modifications to the Keyes plant to use our integrated cellulosic

ethanol enzyme technology to produce ethanol from both corn and cellulosic

feedstocks such as wheat straw or corn stover. Any modifications to the Keyes

plant are subject to Cilion’s approval. On March 15 2010, Cilion

delivered possession of the Keyes plant to the project company and we began the

repair and retrofit activities.

We also

own two potential ethanol or cellulosic ethanol plant sites in Danville,

Illinois and Sutton, Nebraska. The Company does not have any immediate plans to

construct stand alone corn ethanol or cellulosic ethanol plants at these

sites.

Current

Biodiesel Projects

Our

biodiesel production facility in Kakinada started commercial sales in November

2008 and is capable of producing biodiesel from multiple feedstocks. We

currently produce biodiesel from palm stearin, a non-edible feedstock, which we

source from suppliers in India. Our plant was originally established as an

export only unit to produce biodiesel for sale outside of India, which would

have allowed us to save on import duties. However, that original designation did

not permit us to buy feedstock and sell biodiesel into the India domestic

market. In 2008, during our construction and commissioning of the

plant, we found a market for our biodiesel product in India in addition to the

export market. In 2009, we obtained the necessary permits and

approvals to sell our biodiesel into the Indian domestic market on an ongoing

basis by receiving advance licenses for duty free import of feedstock. We can

also sell biodiesel into the export market.

The plant

was constructed by De Smet Chemfood Engineering Private Limited, a part of De

Smet Ballestra Groups, a leading biodiesel technology provider based in Belgium.

In addition to the equipment in the plant, De Smet Chemfood provided on-site

assistance during the construction and commissioning phase. De Smet Chemfood

provided us a non-exclusive perpetual royalty free license for the related

process technology.

Although

we primarily use palm stearin as feedstock, our plant has been designed to

permit us to use different types of feedstock for manufacturing biodiesel. We

believe this feature of our plant gives us flexibility, reduces our exposure to

commodity price fluctuations, and is in line with our strategy to shift to

non-edible feedstock for a portion of our biodiesel production when it becomes

available. In addition, we have plans to complete construction of a

pre-treatment facility and a glycerin refinery at our Kakinada plant. The

pre-treatment facility will enable us to use cheaper unrefined feedstock such as

crude palm oil and the glycerin refinery will enable us to refine the crude

glycerin produced as a byproduct of the biodiesel production process for sale to

end users including pharmaceutical and cosmetic companies.

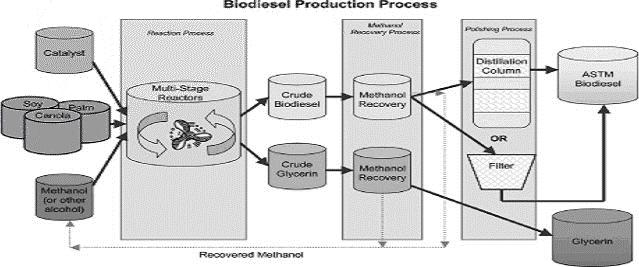

Biodiesel

Production Process

Biodiesel

is produced by a process known as transesterification. Vegetable oil or animal

fat feedstock is reacted with methanol, in the presence of a catalyst, such as

sodium methoxide, and this chemical reaction produces biodiesel and crude

glycerin, which is then separated from the biodiesel. We intend to further

refine this crude glycerin for sale to end users such as pharmaceutical or

cosmetic companies.

The

multi-feedstock technology that we employ in our biodiesel production process

enables us to reduce our costs by utilizing different feedstocks based on

availability and price. Our Kakinada production facility has been designed, and

our additional planned production facilities will be designed, as

multi-feedstock facilities that can produce biodiesel from many kinds of animal

and vegetable oils.

6

Our

production process is set forth below:

Procurement

of raw material

The main

raw materials used in the production of biodiesel are palm oil or palm stearin

and methanol. Operating at 100% of our capacity, our feedstock requirement is

approximately 150,000 metric tons per year. We source palm oil from Indonesia,

which is one of the major producers of palm oil in the world and palm stearin

from the local Kakinada area. Methanol is readily available locally and can also

be imported and transported through port facilities next to our plant in

Kakinada.

Product

quality

Our

primary market for biodiesel is India. Our biodiesel complies with all European

(EN) standards other than the cold filter plugging point. Upon request, we

provide third-party testing analysis to ensure our biodiesel meets our

customers’ product quality standards.

Safety

and Controls

We have

an advanced fire prevention system to ensure the safety of the plant and our

employees. We have a system of water pumps that can deliver water up to 30

meters high to help extinguish a fire at the plant. In addition, we can disperse

foam and CO

2 . Fire extinguishers are also available throughout the facility. We

also conduct regular safety inspections.

The plant

is fully automated and operations can be controlled via our control room. The

control room monitors, among other things, temperatures, pressure, flow, vacuum

of the various liquids used during the processing of feedstock, as well as the

performance of all our equipment. From the control room, we can shut down any

piece of equipment or all the operations in the plant. We have an additional set

of controls in a different area of the facility that can shut down the plant in

the event of an emergency.

Infrastructure,

transportation and logistics

Power is

supplied to our plant by the Andhra Pradesh Electrical Board and by our own

diesel generators. We procure water from underground wells on the site.

Additionally, we recycle water and steam captured from the biodiesel production

process.

The plant

is approximately 7.5 kilometers from the Kakinada port from which raw materials

can be received and biodiesel can be shipped. The plant is connected to the port

via non-corrosive, mild steel pipes owned and operated by third-parties. When

palm oil is brought to the port at Kakinada, it is also transported through

third party pipes directly to our storage tanks. Similarly, refined biodiesel

can be transported from our storage tanks through the pipe network to the

port.

We have

separate storage tanks for crude palm oil, refined biodiesel and glycerin. Each

of these is connected with separate pipes to the plant. We have smaller storage

tanks for testing samples of biodiesel and glycerin. Once the samples are tested

and are found to be of acceptable quality, we transport the biodiesel and the

glycerin, as the case may be, to separate (larger) tanks for storage, where they

remain until sold.

We burn

rice husks to fire our boilers, which is available. Rice is a major crop grown

in Andhra Pradesh and there are several reliable low cost suppliers of rice husk

in and around Kakinada, although we have not entered into any long-term

contracts with suppliers of these products.

Current

Ethanol Projects

Ethanol

is produced by the fermentation of carbohydrates found in grains and other

biomass. Although ethanol can be produced from a number of different sources,

including grains such as corn, sorghum and wheat, sugar by-products, rice hulls,

cheese whey, potato waste, brewery waste, beverage waste, forestry by-products

and paper wastes, approximately 90% of ethanol in the U.S. today is produced

from corn. Corn is the primary source for ethanol because corn produces large

quantities of relatively cheap carbohydrates, which convert into glucose more

efficiently than other kinds of biomass. However, biomass inputs such as wheat

grass, switch grass, corn stover, and other non-food inputs are

increasingly being adopted, through various technologies, as alternatives to

corn.

7

On

December 1, 2009, the Company and two of our wholly owned subsidiaries, AE

Advanced Fuels, Inc. and AE Advanced Fuels Keyes, Inc. entered into a Project

Agreement and Lease Agreement with Cilion, Inc. the owner of a 55 MGY ethanol

plant in Keyes, California. Under the terms of the Lease Agreement

the Project Company will lease the Keyes plant for a term of up to thirty-six

(36) months at a monthly rental amount of $250,000. The Lease term and rental

payments begin upon substantial completion of certain repair and retrofit

activities, determined by mutual agreement of the parties. We took possession of

the Keyes plant, per the terms of the Project Agreement, on March 15, 2010 and

began the repair and retrofit activities. We expect to restart the

Keyes plant within 120 days of possession. At full production, the plant is

expected to produce 55 million gallons of ethanol annually. We

expect the plant will restart within 120 days of possession. The

plant is expected to produce 55 million gallons of ethanol annually.

In

February 2007, the Company acquired a majority interest in Energy Enzymes, Inc.,

a cellulosic technology company. Energy Enzymes has developed patent-pending

ambient temperature enzymes that can produce ethanol from traditional feedstock

such as corn, as well as other biomass which may include wheat straw, corn

stover and sugar cane bagasse. The technology can be immediately deployed at

existing corn ethanol plants to reduce the amount of natural gas and water used

in the process. The net result is lower operating costs and improved margins. In

addition, existing corn ethanol plants that use our technology can replace up to

25% of their traditional corn feedstock with cellulosic material, thereby

reducing costs.

In 2008,

the Company built and commissioned a 9,000 square foot integrated cellulose and

starch ethanol commercial demonstration facility located in Butte. At the Butte

plant we are able to evaluate various types of biomass, including wheat straw,

corn stover, and sugar cane bagasse, to optimize our proprietary, patent-pending

enzyme technology for the commercial production of next-generation

ethanol.

We

anticipate the first deployment of our technology will be at the ethanol plant

in Keyes, California, in the first half of 2011. We also expect to deploy our

proprietary, patent-pending enzyme technology at other corn ethanol plants

through acquisition, joint venture, or licensing agreements.

Ethanol

Byproducts

Distiller

Grains with Solubles (DGS) are a high protein, high-energy livestock and animal

feed supplement produced as a by-product of ethanol production. DGS are an

important source of revenue to ethanol producers. According to the Renewable

Fuels Association, the estimated market value of feed co-products from ethanol

production in 2009 was $3.5 billion (approximately 30.5 million metric

tons).

At the

Keyes, California ethanol plant, we anticipate selling non-dried or “wet”

distillers grains to the local dairy industry. By removing the drying

step and thus reducing the plant’s overall energy consumption, we expect to sell

the DGS at a slight premium over dried DGS.

Competition

North

America

In 2009,

according to the Renewable Fuels Association, there were over 200 commercial

corn ethanol production facilities in operation in the U.S. with a combined

production of nearly 10.6 billion gallons.

In 2009,

there were only a handful of operating cellulosic ethanol production facilities

in the U.S. with total production capacity well below 500,000 gallons per year

in total. In 2010, additional cellulosic ethanol facilities are

expected to become operational but will only increase capacity to approximately

6.5 million gallons.

India

We currently compete primarily on a

regional basis within the Indian State of Andhra Pradesh where our plant is

located. Our primary competitors (who are also potential customers) in this area

are the three state-controlled oil companies, including Indian Oil Corporation,

Bharat Petroleum and Hindustan Petroleum, and two private oil companies,

Reliance Petroleum and Essar Oil. Indian Oil Corporation together with its

subsidiaries holds 46% of the total petroleum products market in India and 34%

of the total Indian refining capacity. In addition, the Indian Oil Corporation

group of companies owns and operates 10 of India’s 19 refineries with a combined

refining capacity of 60.2 million metric tons per year. Indian Oil also operates

the largest and the widest network of fuel stations in the country, numbering

approximately 18,278.

4

The price

of our biodiesel is generally indexed to the price of petroleum diesel, which is

set by the Indian government. In addition, our competitors have significantly

larger market shares than us, and control a significant share of the

distribution network. If the Indian government were to significantly reduce

diesel prices, or if our oil company competitors were to significantly increase

production of petroleum diesel, our business, operating results and financial

condition could be adversely affected.

4 India

Oil Company presentation, March 4, 2010

8

We also

compete with other biodiesel producers in India, including Naturol Bioenergy

Limited, Cleancities Biodiesel India Limited, BioMax Fuels, Emami Biotech

Limited, Southern Online Bio Technologies Limited, and Coastal Energy Limited.

We believe that our ability to compete successfully in the biodiesel industry

depends on many factors, including the following principal competitive

factors:

|

●

|

price;

and

|

|

●

|

quality,

based on the reliability and consistency of our production

processes.

|

When we

complete our glycerin refinery, we will compete with other glycerin refiners. We

believe the principal competitive factors for sales of refined glycerin are

price, proximity to purchasers and product quality.

Customers

India

Segment

We began

selling biodiesel in November 2008. Our plant is capable of producing

approximately 425 metric tons of biodiesel per day. In 2009, we sold an average

of 37 metric tons per day or 9% of our daily capacity. In 2008, we sold an

average of 48 metric tons per day or 11% of our daily capacity. Our customers

include one European biodiesel distribution company who bought 4,125 metric tons

of biodiesel in August 2009, trucking and other transportation companies, marine

vessels and the Port of Kakinada. In 2009 and 2008 all of our revenues were from

sales to a total of 201 customers. In 2009, one customer, Masefield

AG, accounted for 31% of our consolidated revenues. In

2008, due to our limited sales, three of our customers, V.V.R. Engine Oils, SAF

Shipping Agencies, and SriDevi Manikanta Oil & Chemicals, accounted for

approximately 37%, 20%, and 16%, respectively, of our consolidated

revenue.

North

America Segment

We

currently have no active operations and no customers in North America. On March

15, 2010 we took possession of a 55 MGY ethanol plant in Keyes, California

pursuant to a project agreement with the owner of the plant, Cilion, Inc. When

we restart the Keyes plant, we expect to enter into an agreement with a leading

ethanol marketing company for the sale and distribution of ethanol produced at

the Keyes plant. The marketing company would sell product directly to companies

that blend ethanol with refined gasoline. We may also choose to sell a portion

of the ethanol we product directly to major oil refiners or into the spot

market. We also anticipate selling our distillers grains through a third party

marketer.

Pricing

and Backlog

India

Segment

To date,

we price our biodiesel based on the price of petroleum diesel which is set by

the Indian government or based on spot market prices for biodiesel for delivery

into Europe. We sell our biodiesel primarily to resellers, distributors and

refiners on an as-needed basis. We have no long term sales

contracts.

North

America Segment

When we

restart the Keyes plant we expect to sell the ethanol we produce to large

gasoline refiners and blenders on an as-needed basis at or near spot prices

quoted by either the Chicago Board of Trade (“CBOT”) or Oil Price Information

Service (“OPIS”). We currently have no short or long term sales

contracts.

Raw Materials and Suppliers

India

Segment

We

require three key inputs for our biodiesel production: high quality vegetable

oil, methanol and chemical catalysts. In 2008, we produced all of our biodiesel

from refined palm oil. Refined palm oil can be obtained through numerous sources

as it is an internationally traded commodity. Typical sources for refined palm

oil for our plant are producers from Malaysia and Indonesia. Our plant in

Kakinada is situated on approximately 32,000 square meters of land located 7.5

kilometers from the local seaport having connectivity through a pipe line to the

port jetty. The pipe line facilitates the importing of raw materials and

exporting finished product.

9

In 2009,

due to favorable palm stearin prices, we began to manufacture biodiesel from

palm stearin. Our Kakinada plant is located near multiple palm oil refineries

which produce palm stearin as a by-product of the palm oil refinement process.

Palm stearin is trucked from nearby refiners to our plant, which significantly

reduces transportation costs. Palm stearin is also widely available in other

areas of India and we believe that we have ample access to palm stearin

suppliers. Our plant has ample storage capacity with the ability of rent

additional storage from a commercial tank farm located on adjacent property.

Although palm stearin can be obtained from multiple sources, and while

historically we have not suffered any significant limitations on our ability to

procure palm stearin, any delay or disruption in our suppliers’ ability to

provide us with the necessary palm stearin may significantly affect our business

operations and have a negative effect on our operating results or financial

condition.

In

November 2008, we entered into an agreement with Secunderabad Oils Limited.

Under this agreement Secunderabad agreed to provide us with working capital to

fund the purchase of feedstock and other raw materials for our Kakinada

biodiesel facility, as well as plant operational expertise on an as-needed

basis. In return, we agreed to pay Secunderabad monthly an amount equal to 30%

of the plant’s monthly net operating profit plus interest on working capital

advances at Secunderabad’s actual bank borrowing rate. The agreement can be

terminated by either party at any time without penalty. Secunderabad began

providing us with working capital under this agreement in the first quarter of

2009.

The key

elements of our procurement strategies are the assurance of a stable supply and

the avoidance, where possible, of exposures to price fluctuations. We believe

that our ability to produce biodiesel from multiple feedstock sources and, when

completed, our pretreatment facility helps to reduce our exposure to price

fluctuations.

We do not

have long-term or fixed-price contracts for methanol and chemical catalysts. We

purchase methanol and other chemicals on the open market at prevailing prices

from local suppliers.

North

America Segment

Initially

corn will be the primary feedstock utilized at the Keyes plant. We expect to

enter into a long-term agreement with a major grain supplier located in

California. We may also enter into contracts with suppliers of

denaturant, and various chemicals used in the ethanol production

process.

Sales

and Marketing

India

Segment

We began

selling biodiesel in November 2008. Our biodiesel is sold predominantly to

industrial users, resellers, blenders, distributors and refiners who typically

blend biodiesel with petroleum-based diesel fuel. We sell our biodiesel

both directly and through brokers. We intend to hire additional sales

personnel, initiate additional marketing programs and build additional

relationships with brokers and resellers as demand grows.

We also

market and sell the glycerin by-product from our facility.

North

America Segment

When we

restart the Keyes plant, we expect to enter into an agreement with a leading

ethanol marketing company for the sale and distribution of some or all of the

ethanol we produce. We expect that the marketing company would sell our product

directly to companies that blend ethanol with refined gasoline. We may also sell

ethanol directly to major oil refiners or directly into the spot market. We also

expect to enter into a marketing and distribution agreement with a third party

marketer to sell our distillers grains.

Risk Management Practices

India

& North America Segments

The

markets for feedstock, the largest expense in our India and North America

segments, and biodiesel and ethanol, our largest source of revenues, are

volatile and are generally uncorrelated. We are, therefore, exposed to

substantial commodity price risk in our business. Our risk management policies

are aimed at managing product margins. As noted above, we are focused on

utilizing lower-cost feedstock, as reflected in the multi-feedstock capability

of our production facilities. In addition, we have in the past, and expect in

the future, to use forward contracting and hedging strategies, including

strategies using futures and options contracts. However, the extent to which we

engage in these risk management strategies varies substantially from time to

time, depending on market conditions and other factors. In establishing our risk

management strategies, we draw from our own in-house risk management expertise.

We also use research conducted by outside firms to provide additional market

information and risk management strategies. We believe combining these sources

of knowledge, experience, and expertise gives us a more sophisticated and global

view of the fluctuating commodity markets for raw materials and energies, which

we then can incorporate into risk management strategies.

10

Our

ability to mitigate our risk of falling biodiesel prices is more limited. The

price of our biodiesel is generally indexed to the price of petroleum diesel

which is set by the Indian government. There is no established market for

biodiesel futures. Ethanol and corn are sold on an indexed basis, and futures

contracts exist for both. We expect that our efforts to hedge against

falling biodiesel prices will involve negotiating long-term fixed-price

contracts with our customers and offsetting these contracts with long-term fixed

price contracts for feedstock, although to date we have not entered into any

long-term agreements with our customers or suppliers. For ethanol

sales, we expect to largely sell product through index-based

contracts. For corn acquisition, the company intends to seek

favorable pricing through the use of opportunistic hedging strategies and

long-term contracts when prices are favorable.

Research

and Development

Our

research and development efforts consist of the development of our

next-generation ethanol technology and our integrated cellulosic and starch

ethanol production process and the prosecution of patents around this

technology. Our primary objective of this development activity is to optimize

the production of ethanol using our proprietary, patent-pending enzyme

technology for large scale commercial production. Research and development

expense was approximately $539,000 in 2009 and $1 million in 2008.

Patents

and Trademarks

We have

filed a number of trademark applications within the U.S. We do not consider the

success of our business, as a whole, to be dependent on these trademarks. In

addition, we have three patent applications pending in the United States in

connection with our cellulosic ethanol technology.

It is

possible that the Company will not receive patents for every application it

files. Furthermore, when patents are issued, the issued patents may not

adequately protect our technology from infringement or prevent others from

claiming that our products infringe the patents of third-parties. The Company’s

failure to protect our intellectual property could materially harm our business.

In addition, the Company’s competitors may independently develop similar or

superior technology or design around our patents. It is possible that litigation

may be necessary in the future to enforce the Company’s intellectual property

rights, to protect its trade secrets or to determine the validity and scope of

the proprietary rights of others. Litigation could result in substantial costs

and diversion of resources and could materially harm the Company’s

business.

The

Company may receive in the future, notice of claims of infringement of other

parties’ proprietary rights. Infringement or other claims could be asserted or

prosecuted against the Company in the future and it is possible that future

assertions or prosecutions could harm our business. Any such claims, with or

without merit, could be time-consuming, result in costly litigation and

diversion of technical and management personnel, cause delays in the development

of our products, or require the Company to develop non-infringing technology or

enter into royalty or licensing arrangements. Such royalty or licensing

arrangements, if required, may require the Company to license back its

technology or may not be available on terms acceptable to the Company, or at

all. For these reasons, infringement claims could materially harm the Company’s

business.

Environmental

and Regulatory Matters

India

Segment

We are

subject to federal, state and local environmental laws, regulations and permits,

including with respect to the generation, storage, handling, use, transportation

and disposal of hazardous materials, and the health and safety of our employees.

These laws may require us to make operational changes to limit actual or

potential impacts to the environment. A violation of these laws, regulations or

permits can result in substantial fines, natural resource damages, criminal

sanctions, permit revocations and/or facility shutdowns. In addition,

environmental laws and regulations (and interpretations thereof) change over

time, and any such changes, more vigorous enforcement policies or the discovery

of currently unknown conditions may require substantial additional environmental

expenditures.

North

America Segment

We are

subject to extensive federal, state and local environmental laws, regulations

and permit conditions (and interpretations thereof), including those relating to

the discharge of materials into the air, water and ground, the generation,

storage, handling, use, transportation and disposal of hazardous materials, and

the health and safety of our employees. These laws, regulations, and permits

require us to incur significant capital and other costs, including costs to

obtain and maintain expensive pollution control equipment. They may also require

us to make operational changes to limit actual or potential impacts to the

environment. A violation of these laws, regulations or permit conditions can

result in substantial fines, natural resource damages, criminal sanctions,

permit revocations and/or facility shutdowns. In addition, environmental laws

and regulations (and interpretations thereof) change over time, and any such

changes, more vigorous enforcement policies or the discovery of currently

unknown conditions may require substantial additional environmental

expenditures.

11

We are

also subject to potential liability for the investigation and cleanup of

environmental contamination at each of the properties that we may own or operate

and at off-site locations where we arranged for the disposal of hazardous

wastes. If significant contamination is identified at our properties in the

future, costs to investigate and remediate this contamination as well as any

costs to investigate or remediate associated natural resource damages could be

significant. If any of these sites are subject to investigation and/or

remediation requirements, we may be responsible under the Comprehensive

Environmental Response, Compensation and Liability Act of 1980 (“CERCLA”) or

other environmental laws for all or part of the costs of such investigation

and/or remediation, and for damages to natural resources. We may also be subject

to related claims by private parties alleging property damage or personal injury

due to exposure to hazardous or other materials at or from such properties.

While costs to address contamination or related third-party claims could be

significant, based upon currently available information, we are not aware of any

material contamination or such third party claims. We have not accrued any

amounts for environmental matters as of December 31, 2009. The ultimate costs of

any liabilities that may be identified or the discovery of additional

contaminants could adversely impact our results of operation or financial

condition.

In

addition, the hazards and risks associated with producing and transporting our

products (such as fires, natural disasters, explosions, and abnormal pressures)

may result in spills or releases of hazardous substances, or claims from

governmental authorities or third parties relating to actual or alleged personal

injury, property damage, or damages to natural resources. We maintain insurance

coverage against some, but not all, potential losses caused by our operations.

Our coverage includes, but is not limited to, physical damage to assets,

employer’s liability, comprehensive general liability, automobile liability and

workers’ compensation. We do not carry environmental insurance. We believe that

our insurance is adequate for our industry, but losses could occur for

uninsurable or uninsured risks or in amounts in excess of existing insurance

coverage. The occurrence of events which result in significant personal injury

or damage to our property, natural resources or third parties that is not

covered by insurance could have a material adverse impact on our results of

operations and financial condition.

Our air

emissions are subject to the federal Clean Air Act, and similar State laws which

generally require us to obtain and maintain air emission permits for our ongoing

operations as well as for any expansion of existing facilities or any new

facilities. Obtaining and maintaining those permits requires us to incur costs,

and any future more stringent standards may result in increased costs and may

limit or interfere with our operating flexibility. These costs could have a

material adverse affect on our financial condition and results of operations.

Because other ethanol manufacturers in the U.S. are and will continue to be

subject to similar laws and restrictions, we do not currently believe that our

costs to comply with current or future environmental laws and regulations will

adversely affect our competitive position with other U.S. ethanol producers.

However, because ethanol is produced and traded internationally, these costs

could adversely affect us in our efforts to compete with foreign producers not

subject to such stringent requirements.

New laws

or regulations relating to the production, disposal or emissions of carbon

dioxide and other green house gasses may require us to incur significant

additional costs with respect to ethanol plants that we build or acquire. In

particular, in 2007, Illinois and four other Midwestern States entered into the

Midwestern Greenhouse Gas Reduction Accord, which program directs participating

states to develop a multi-sector cap-and-trade mechanism to help achieve

reductions in greenhouse gases, including carbon dioxide. In addition, it is

possible that other states in which we conduct or plan to conduct business could

join this accord or require other costly carbon dioxide emissions

reductions. Climate Change legislation is being considered in

Washington, D.C. this year which may significantly impact the biofuels

industry's emissions regulations, as will the Renewable Fuel Standard,

California's Low Carbon Fuel Standard, and other potentially significant changes

in existing transportation fuels regulations.

Employees

At

December 31, 2009, we had a total of 56 full-time equivalent employees,

comprised of 12 full-time equivalent employees in the United States and 44

full-time equivalent employees in India. None of our employees are represented

by a union. We believe our relations with our employees are good. Employees are

currently located in the United States headquarters in Cupertino, California; an

integrated starch cellulosic ethanol commercial demonstration facility in Butte,

Montana; an administrative office in Hyderabad, India and a biodiesel plant in

Kakinada, India.

ITEM 1A. RISK FACTORS

Risks

Related to our Overall Business

We

have a limited operating history, which makes it difficult to evaluate our

financial position and our business plan.

We began

generating revenue in November 2008 and have limited business operations.

Accordingly, there is limited prior operating history by which to evaluate the

likelihood of our success or our ability to exist as a going concern. We may

never begin or complete construction of a cellulosic ethanol production facility

in the United States and although we have been producing and selling biodiesel

from our plant in Kakinada, our production and sales have not reached full

capacity and there is no assurance that our production and sales from this

facility will do so in the near future or at all and we may not be able to

generate sufficient revenues to become profitable.

We

are currently in default on our term loan with the State Bank of

India

On

October 7, 2009, UBPL received a demand notice from the State Bank of India

under the Agreement of Loan for Overall Limit dated as of June 26, 2008. The

notice informs UBPL that an event of default has occurred for failure to make an

installment payment on the loan due in June 2009 and demands repayment of the

entire outstanding indebtedness of 19.60 crores (approximately $4 million)

together with all accrued interest thereon and any applicable fees and expenses

by October 10, 2009. Upon the occurrence and during the continuance of an Event

of Default, interest accrues at the default interest rate of 2% above the State

Bank of India Advance Rate pursuant to the Agreement of Loan for Overall Limit.

If the entire principal and interest amount of indebtedness under the loan was

paid in full, we estimate that the amount would be approximately $4.4 million.

Interest continues to accrue at the default rate in the amount of approximately

$48,000 per month during the continuance of default.

12

Our

auditors’ opinion expresses substantial doubt about our ability to continue as a

“going concern.”

Our

independent auditors’ report on our December 31, 2009 and 2008 financial

statements included herein states that the Company has suffered recurring losses

and has a working capital deficit and total stockholders’ deficit and that these

conditions raise substantial doubt about our ability to continue as a going

concern. Should the Company not be able to raise enough equity or debt

financings it may be forced to sell all or a portion of its existing biodiesel

facility or other assets to generate cash to continue the Company’s business

plan or possibly discontinue operations. The Company’s consolidated financial

statements do not include any adjustments that might result from the outcome of

this uncertainty.

We

are a holding company, and there are significant limitations on our ability to

receive distributions from our subsidiaries.

We

conduct substantially all of our operations through subsidiaries and are

dependent on dividends or other intercompany transfers of funds from our

subsidiaries to meet our obligations. Our subsidiaries have not made significant

distributions to the Company and may not have funds legally available for

dividends or distributions in the future. In addition, we may enter into

credit or other agreements that would contractually restrict our subsidiaries

from paying dividends, making distributions or making intercompany loans to our

parent company or to any other subsidiary. In particular, our credit agreement

for the Kakinada refinery requires the prior consent of the lender for dividends

or other intercompany fund transfers. If the amount of capital we are able to

raise from financing activities, together with our revenues from operations that

are available for distribution, are not sufficient to satisfy our ongoing

working capital and corporate overhead requirements needs, even to the extent

that we reduce our operations accordingly, we may be required to cease

operations.

We

are unable to execute on the Company’s business plan which may result in the

need to write down the carrying value of the Company’s long-lived

assets.

We value

our long lived assets based on our ability to execute our business plan,

principally in India, and generate sufficient cash flow to justify the carrying

value of this asset. Should we fall short of our cash flow

projections, we may be required to write down the value of these assets under

the accounting rules and further degrade the value of our

business. We can make no assurances that our future cash flows will

develop and provide us with sufficient cash to maintain the value of these

assets, thus avoiding future impairment to our asset carry values.

Risks

Relating to our U.S. Operations

We took

possession of the Keyes ethanol plant in 2010, we may encounter unanticipated

difficulties in repairing and restarting the plant.

In order to restart and operate the the Keyes plant we intend to implement a repair plan on this 55 million gallon per year nameplate capacity plant. The repair plan may cost significantly more than our estimate to complete. The plant may not operate at nameplate capacity once the repairs are complete. In addition, some of the technology utilized at the Keyes plant is currently not in use at any other corn ethanol plant. We are aware of certain plant design issues that may impede the reliable and continuous operation of the plant. We cannot assure you that the repair plan will fix all the design issues. If we are unable to get the plant repaired and restarted, we will not have revenues derived from the sale of ethanol and distillers grain from the plant in 2010. Therefore we would not be able to recover the costs incurred during the repair and restart of the plant. We may also encounter other factors that could prevent us from conducting operations as expected, resulting in decreased capacity or interruptions in production, including shortages of workers or materials, design issues relating to improvements, construction and equipment cost escalation, transportation constraints, adverse weather, unforeseen difficulties or labor issues, or changes in political administrations at the federal, state or local levels that result in policy change towards ethanol in general or our plants in particular. Furthermore, local water, electricity and gas utilities may not be able to reliably supply the resources that our facilities will need or may not be able to supply them on acceptable terms.

We

expect to start operating and making lease payments on the Keyes ethanol plant

in 2010. If the plant is restarted, we may encounter difficulties in running the

plant and may not be able to make our lease payments.

The Keyes