Attached files

| file | filename |

|---|---|

| EX-32.01 - EXHIBIT 32.01 - STEVEN MADDEN, LTD. | ex32_01.htm |

| EX-10.10 - EXHIBIT 10.10 - STEVEN MADDEN, LTD. | ex10_10.htm |

| EX-21.01 - EXHIBIT 21.01 - STEVEN MADDEN, LTD. | ex21_01.htm |

| EX-10.29 - EXHIBIT 10.29 - STEVEN MADDEN, LTD. | ex10_29.htm |

| EX-31.01 - EXHIBIT 31.01 - STEVEN MADDEN, LTD. | ex31_01.htm |

| EX-23.01 - EXHIBIT 23.01 - STEVEN MADDEN, LTD. | ex23_01.htm |

| EX-32.02 - EXHIBIT 32.02 - STEVEN MADDEN, LTD. | ex32_02.htm |

| EX-31.02 - EXHIBIT 31.02 - STEVEN MADDEN, LTD. | ex31_02.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

FORM

10-K

(Mark

One)

x ANNUAL REPORT PURSUANT TO

SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For

the fiscal year ended December 31, 2009

or

o TRANSITION REPORT PURSUANT

TO SECTION 13 OR 15(d) OF THE SECURITIES AND EXCHANGE ACT OF

1934

For the

transition period from to

Commission

File Number 0-23702

|

STEVEN

MADDEN, LTD.

|

||

|

(Exact

name of registrant as specified in its charter)

|

||

|

Delaware

|

13-3588231

|

|

|

(State

or other jurisdiction of

incorporation

or organization)

|

(I.R.S.

employer identification no.)

|

|

52-16

Barnett Avenue, Long Island City, New York 11104

(Address

of principal executive offices) (Zip Code)

(718)

446-1800

(Registrant’s

Telephone Number, Including Area Code)

Securities

Registered Pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange on Which

Registered

|

|

|

Common

Stock, par value $.0001 per share

|

The

NASDAQ Stock Market LLC

|

|

|

Preferred

Stock Purchase Rights

|

The

NASDAQ Stock Market LLC

|

Securities

Registered Pursuant to Section 12(g) of the Act: None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act.

Yes

o No

x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or 15(d) of the Securities Act.

Yes o No

x

Indicate

by check mark whether the registrant: (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and

posted on its corporate website, if any, every Interactive Data File required to

be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of

this chapter) during the preceding 12 months (or for such shorter period that

the registrant was required to submit and post such files).

Yes o No o

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained, to the best

of registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment to this

Form 10-K. o

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer or a smaller reporting company. See

the definitions of “large accelerated filer”, “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer x | Non-accelerated filer o | Smaller reporting company o |

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act).

Yes o No x

The

aggregate market value of the common equity held by non-affiliates of the

registrant (assuming for these purposes, but without conceding, that all

executive officers and directors are “affiliates” of the registrant) as of June

30, 2009, the last business day of the registrant’s most recently completed

second fiscal quarter, was approximately $385,532,000 (based on the closing sale

price of the registrant’s common stock on that date as reported on The NASDAQ

Global Select Market).

The

number of outstanding shares of the registrant’s common stock as of March 9,

2010 was 18,348,786 shares.

DOCUMENTS

INCORPORATED BY REFERENCE:

PART III

INCORPORATES CERTAIN INFORMATION BY REFERENCE FROM THE REGISTRANT’S DEFINITIVE

PROXY STATEMENT FOR THE REGISTRANT’S 2010 ANNUAL MEETING OF

STOCKHOLDERS.

| 1 | ||||

| 1 | ||||

| 9 | ||||

| 12 | ||||

| 12 | ||||

| 13 | ||||

| 14 | ||||

| 14 | ||||

| 17 | ||||

| 18 | ||||

| 27 | ||||

| 28 | ||||

| 28 | ||||

| 28 | ||||

| 30 | ||||

| 30 | ||||

| 30 | ||||

| 30 | ||||

| 30 | ||||

| 30 | ||||

| 31 | ||||

This

Annual Report on Form 10-K contains forward-looking statements as that term is

defined in the federal securities laws that are made pursuant to the safe harbor

provisions of the Private Securities Litigation Reform Act of 1995, which

include statements with regard to future revenue, projected 2010 results,

earnings, spending, margins, cash flow, orders, expected timing of shipment of

products, inventory levels, future growth or success in specific countries,

categories or market sectors, continued or expected distribution to specific

retailers, liquidity, capital resources and market risk, strategies and

objectives and other future events. Forward-looking statements include, without

limitation, any statement that may predict, forecast, indicate or simply state

future results, performance or achievements, and can be identified by the use of

forward looking language such as “believe,” “anticipate,”

“expect,” “estimate,” “intend,” “plan,” “project,” “will be,” “will continue,”

“will result,” “could,” “may,” “might,” or any variations of such words with

similar meanings. Factors that may affect our results include, but are not

limited to, the risks and uncertainties discussed in Item 1A of this Annual

Report on Form 10-K.

Any such

statements are subject to risks and uncertainties, many of which are beyond our

control, that may influence the accuracy of the statements and the projections

upon which the statements are based that could cause actual results to differ

materially from those projected in forward-looking statements. As such, we

caution you that these statements are not guarantees of future performance or

events. Our actual results, performance and achievements could differ materially

from those expressed or implied in these forward-looking statements. We

undertake no obligation to publicly update or revise any forward-looking

statements, whether from new information, future events or

otherwise.

| ITEM 1 | BUSINESS |

Steven

Madden, Ltd. and its subsidiaries (collectively, the “Company”) design, source,

market and sell fashion-forward footwear for women, men and children. In

addition, we design, source, market and sell name brand and private label

fashion handbags and accessories through our Accessories Division. We distribute

products through our retail stores, our e-commerce website, department and

specialty stores throughout the United States and through special distribution

arrangements in Asia, Canada, Europe, Central and South America, Australia and

Africa. Our product line includes a broad range of updated styles designed to

establish or capitalize on market trends, complemented by core products. We have

established a reputation for our creative designs, popular styles and quality

products at affordable price points.

Fiscal

year 2009 was a record year for Steven Madden, Ltd. Consolidated net sales for

2009 increased to a record $503.6 million from $457.0 million during 2008. Our

gross margin increased in fiscal year 2009 to 42.9%, 200 basis points greater

than the 40.9% achieved in 2008. Net income increased 79% in 2009 to a record

$50.1 million from $28.0 million in 2008. Diluted earnings per share for the

year ended December 31, 2009 increased 81% to a record $2.73 per share on

18,323,000 diluted weighted average shares outstanding compared to $1.51 per

share on 18,519,000 diluted weighted average shares outstanding in 2008. Net

cash provided by operating activities increased to a record $64.3 million in

2009 compared to $41.8 million in 2008.

We have expanded our accessories

portfolio through two recent acquisitions. In July, 2009, we acquired certain

assets constituting the Zone 88 and Shakedown Street (together “Zone 88”) lines

of SML Brands, LLC, a subsidiary of Aimee Lynn, Inc, which designs and markets

primarily private label accessories, principally handbags, for mass merchants

and mid-tier retailers. The acquisition was completed for $1.3 million in cash.

We believe this acquisition will enable us to expand our accessories business in

the private label arena with value priced customers.

Most recently, subsequent to our year

end, on February 10, 2010, the Company acquired all of the outstanding shares of

stock of Big Buddha, Inc. (“Big Buddha”) from its sole stockholder, Jeremy

Bassan. Founded in 2003, Big Buddha designs and markets fashion-forward handbags

to specialty retailers and better department stores. The acquisition was

completed for $11.0 million in cash plus potential earn out payments based on

annual financial performance of Big Buddha through March 31, 2013.

1

On

September 2, 2009, the Company expanded its brand portfolio by entering into an

additional license agreement with Dualstar Entertainment Group, LLC, under which

the Company has the right to use the Olsenboye® trademark in connection with the

sale and marketing of footwear and accessories exclusively to J.C. Penney. The

agreement requires the Company to make royalty and advertising payments equal to

a percentage of net sales and a minimum royalty and advertising payment in the

event that specified net sales targets are not achieved. The agreement expires

on December 31, 2011, but is renewable, at our option, for one three-year term,

if certain conditions are met.

In addition, we made progress on our

stated goal to evolve Steve Madden® into a global lifestyle brand by entering

into two new license agreements. On October 20, 2009, we signed a license

agreement to license our Steve Madden® trademark for the design, manufacture and

worldwide distribution of women’s fashion apparel. On January 7, 2010, we signed

a license agreement to license our Steve Madden® and Steven by Steve Madden®

trademarks for the design, manufacture and worldwide distribution of women’s

fashion jewelry. The new fashion apparel and jewelry lines, which will initially

ship in the spring and fall of 2010, respectively, join our existing licenses

for cold weather accessories, sunglasses, eyewear, outerwear, bedding and

hosiery offerings. Management is pleased to be expanding the Company’s presence

beyond footwear and accessories and believes the new apparel and jewelry lines

mark very logical extensions of the Company’s brands.

Steven

Madden, Ltd. was incorporated as a New York corporation on July 9, 1990 and

reincorporated under the same name in Delaware in November 1998. We completed

our initial public offering in December 1993 and our shares of common stock,

$.0001 par value per share, currently trade on the NASDAQ Global Select Market

under the symbol “SHOO”.

We

maintain our principal executive offices at 52-16 Barnett Avenue, Long Island

City, NY 11104 and our telephone number is (718) 446-1800.

Our

website is http://www.stevemadden.com. We file Annual Reports on Form 10-K,

Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other reports

and information with the Securities and Exchange Commission (the “SEC”) pursuant

to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended,

(the “Exchange Act”). We make these reports, any amendments to such reports, and

our proxy statements for our stockholders’ meetings available free of charge, on

our website as soon as reasonably practicable after such material is

electronically filed with, or furnished to, the SEC. We will provide paper

copies of such filings free of charge upon request. The public may read and copy

any materials filed by us with the SEC at the SEC’s Public Reference Room at 100

R Street, NE, Washington, D.C. 20549. The public may also obtain information on

the operation of the SEC’s Public Reference Room by calling the SEC at

1-800-SEC-0330. In addition, the SEC maintains an Internet site that contains

reports, proxy and information statements and other information regarding us,

which is available at http://www.sec.gov.

Product

Distribution Segments

Our business is comprised of five

distinct segments (Wholesale Footwear, Wholesale Accessories, Retail, First Cost

and Licensing). Our Wholesale Footwear segment includes seven core divisions:

Steve Madden Women’s, Steve Madden Men’s, Madden Girl, Steven, Stevies,

Elizabeth and James and our international business. Our Wholesale Accessories

segment, through license agreements, includes Betsey Johnson®, Daisy Fuentes®

and Olsenboye® accessories brands. Steven Madden Retail, Inc., our wholly owned

retail subsidiary, operates Steve Madden and Steven retail stores as well as our

e-commerce website. There are also three stores licensed to a third party. The

First Cost segment represents activities of a subsidiary which earns commissions

for serving as a buying agent for footwear products under private labels and

licensed brands (such as l.e.i.®, Candie’s® and Olsenboye®) for many of the

country’s large mass-market merchandisers, shoe chains and other off-price

retailers. In the Licensing segment, the Company licenses its Steve Madden® and

Steven by Steve Madden® trademarks for use in connection with the manufacturing,

marketing and sale of cold weather accessories, sunglasses, eyewear, outerwear,

bedding, hosiery, women’s fashion apparel and jewelry.

2

Wholesale

Footwear Segment

Steve Madden Women’s Division.

The Steve Madden Women’s Division (“Madden Women’s”) designs, sources and

markets our Steve Madden brand to major department stores, mid-tier department

stores, better specialty stores and independently owned boutiques throughout the

United States. The Steve Madden brand has become a leading life-style brand in

the fashion conscious marketplace. To serve our customers (primarily women ages

16 to 35), Madden Women’s creates and markets fashion forward footwear designed

to appeal to customers seeking exciting, new footwear designs at affordable

prices.

As our

largest division, Madden Women’s generated net sales of $148.0

million for the year ended December 31, 2009, or approximately 29% of

our total net sales. New products for Madden Women’s are test marketed at our

retail stores. Typically, within a few days, we can determine if the test

product appeals to our customers. This enables us to use our flexible sourcing

model to rapidly respond to changing trends, which we believe is essential for

success in the fashion arena.

Madden Girl Division. The

Madden Girl Division (“Madden Girl”) designs, sources and markets a full

collection of directional young women’s shoes. Madden Girl is geared for young

women ages 13 to 20 and is an “opening price point” brand that is currently sold

at major department stores, mid-tier retailers and specialty stores. Madden Girl

generated net sales of $62.5 million for the year ended December 31, 2009, or

approximately 12% of our total net sales.

Steve Madden Men’s Division.

The Steve Madden Men’s Division (“Madden Men’s”) designs, sources and markets a

full collection of directional men’s shoes and fashion forward athletic shoes to

major department stores, mid-tier department stores, better specialty stores and

independent shoe stores throughout the United States. Price points range from

$70 to $100 at retail, targeted at men ages 20 to 40 years old. Madden Men’s

generated net sales of $40.0 million for the year ended December 31,

2009, or approximately 8% of our total net sales. Madden Men’s maintains

open stock inventory positions in select patterns to serve the replenishment

programs of its wholesale customers.

Steven Division. The Steven

Division designs, sources and markets women’s fashion footwear under the Steven®

trademark through major department and better footwear specialty stores

throughout the United States. Priced a tier above the Steve Madden brand, Steven

products are designed to appeal principally to fashion conscious women, ages 25

to 45, who shop at department stores and footwear boutiques. The Steven

Division generated

net sales of $23.6 million for the year ended December 31, 2009, or

approximately 5% of our total net sales.

International Division. Prior

to 2009, our international business (the “International Division”) operated

under the “first cost” model and, thus, the revenues derived from our

international business were included in Commissions and Licensing Fees in the

Consolidated Statements of Income of our Financial Statements. In order to

improve operating efficiencies, and to give our international partners better

visibility in the process, as of January 2009, we have changed the operating

model for our international business to the “wholesale” model. Our International

Division ships products to China, Canada, Mexico, the United Kingdom, Israel,

UAE, Turkey, Australia, Korea, Morocco, and several countries in southeast Asia,

Europe and Central and South America. Our International Division generated net

sales of $22.1 million for the year ended December 31, 2009 or 4% of our total

net sales.

Elizabeth and James Division.

On September 10, 2008, we entered into a license agreement with Dualstar

Entertainment Group, LLC, under which we have the right to use the Elizabeth and

James trademark in connection with the sale and marketing of footwear. The

Elizabeth and James brand, which was created by Mary-Kate and Ashley Olsen, is

distributed through luxury retailers to women ages 25 to 36 years with average

retail price points from $200 to $350 for shoes and from $350 to $500 for boots.

Our Elizabeth and James Division, which began shipping in April 2009, generated

net sales of $4.3 million for the year ended December 31, 2009 or 1% of our

total net sales.

Steve Madden Kids Division.

Our Steve Madden Kids Division (“Madden Kids”) designs, sources and markets

footwear for young girls to department stores, specialty stores and independent

boutiques throughout the United States. Madden Kids generated net sales

of $7.3 million for the year ended December 31, 2009, or

approximately 1% of our total net sales.

3

Wholesale

Accessories Segment

Our

Wholesale Accessories segment designs, sources and markets name brand (including

Betsey Johnson®, Daisy Fuentes® and Olsenboye® in addition to our Steve Madden®

and Steven by Steve Madden® brands) and private label fashion handbags and

accessories to major department stores, mid-tier department stores, value price

retailers and independent stores throughout the United States. The Wholesale

Accessories segment generated net sales of $70.4 million for the year

ended December 31, 2009, or approximately 14% of our total net

sales.

Retail

Segment

Steven Madden Retail, Inc. As

of December 31, 2009, the Company, through our wholly owned subsidiary Steven

Madden Retail, Inc., owned and operated 89 retail stores including 84

stores under the Steve Madden name, four under the Steven name and our

e-commerce website (at www.stevemadden.com). In 2009, we opened two new stores,

closed seven underperforming stores and licensed out three stores. Steve

Madden stores are located in major shopping malls and in urban street locations

across the United States, primarily focused in New York, California and Florida.

In 2009, our retail stores generated annual sales in excess of $640 per square

foot. Comparative store sales (sales of those stores, including the

e-commerce website, that were open for all of 2009 and 2008) increased 1%

in fiscal year 2009 compared to fiscal year 2008. The Retail segment generated

net sales of $123.7 million for the year ended December 31, 2009, or

approximately 25% of our total net sales.

We

believe that the Retail segment will continue to enhance overall sales and

profitability while increasing recognition for the Steve Madden brand. We plan

to open one to three new retail stores and close six to nine

underperforming stores during 2010. Our retail stores enable us to test and

react to new products and classifications which, in turn, strengthens the

product development efforts of the Steve Madden Wholesale segments.

First

Cost Segment

The First

Cost segment represents activities of a subsidiary which earns commissions for

serving as a buying agent for footwear products under private labels and

licensed brands (such as l.e.i.®, Candie’s® and Olsenboye®) for many of the

country’s large mass-market merchandisers, shoe chains and other mid-tier

retailers. As a buying agent, we utilize our expertise and our relationships

with shoe manufacturers to facilitate the production of private label shoes to

our customers’ specifications. We believe that by operating in the private

label, mass merchandising market, we are able to maximize additional non-branded

sales opportunities. This leverages our overall sourcing and design

capabilities. Currently, this segment serves as a buying agent for the

procurement of women’s, men’s and children’s footwear for large retailers,

including Target, Wal-Mart, Kohl’s, J.C. Penney and Sears. The First Cost

segment receives buying agent’s commissions from its customers. In addition, we

have leveraged the strength of our Steve Madden brands and product designs

resulting in a partial recovery of our design, product and development costs

from our suppliers. The First Cost segment generated operating income of

$16.8 million for the year ended December 31, 2009.

Licensing

Segment

We

license our Steve Madden® and Steven by Steve Madden® trademarks for use in

connection with the manufacturing, marketing and sale of cold weather

accessories, sunglasses, eyewear, outerwear, bedding, hosiery, women’s fashion

apparel and jewelry. Most of our license agreements require the licensee to pay

us a royalty based on actual net sales, a minimum royalty in the event that

specified net sales targets are not achieved and a percentage of sales for

advertising the brand. Licensing income for the year ended December 31, 2009

was $3.1 million.

See Note

N to our Consolidated Financial Statements for additional information relating

to our five operating segments.

4

Product

Design and Development

We have

established a reputation for our creative designs, marketing and trendy products

at affordable price points. We believe that our future success will

substantially depend on our ability to continue to anticipate and react to

changing consumer demands in a timely manner. To meet this objective, we have

developed an unparalleled design process that allows us to recognize and act

quickly to changing consumer demands. Our design team strives to create designs

which it believes fit our image, reflect current or future trends and can be

manufactured in a timely and cost-effective manner. Once the initial design is

complete, a prototype is developed, primarily in our Long Island City facility,

which is reviewed and refined prior to the commencement of initial production.

Most new products are then tested in selected Steve Madden retail stores. Based

on these tests, among other things, management selects the products that are

then offered for wholesale and retail distribution nationwide. We believe that

our design and testing process and flexible sourcing model is a significant

competitive advantage allowing us to mitigate the risk of production costs and

the distribution of less desirable designs.

Product

Sourcing and Distribution

We source

each of our product lines separately based on the individual design, style and

quality specifications of the products in such product lines. We do not own or

operate manufacturing facilities; rather, we source our products through agents

and our own sourcing office with independently owned manufacturers in China,

Mexico, Brazil, Italy, Spain and India. We have established relationships with a

number of manufacturers and agents in each of these countries. Although we have

not entered into any long-term manufacturing or supply contracts, we believe

that a sufficient number of alternative sources exist for the manufacture of our

products. We continually monitor the availability of the principal materials

used in our footwear, which are available from a number of sources in various

parts of the world. We track inventory flow on a regular basis, monitor

sell-through data and incorporate input on product demand from wholesale

customers. We use retailers’ feedback to adjust the production or manufacture of

new products on a timely basis, which helps reduce the close out of slow-moving

products.

We

distribute our products from three third-party distribution warehouse centers

located in California and New Jersey. By utilizing distribution facilities that

specialize in distributing products to certain wholesale accounts, Steve Madden

retail stores and Internet fulfillment, we believe that our customers are better

served.

Customers

Our

wholesale customers consist principally of department stores and specialty

stores, including independent boutiques. Approximately 69% of our wholesale

revenue is generated from department and specialty stores, including Macy’s,

DSW, Nordstrom, Famous Footwear, Dillard’s and Lord & Taylor as well as

mid-tier department stores and catalog retailers, including Victoria’s Secret.

For the year ended December 31, 2009, DSW accounted for approximately $52.9

million, or 14% of our wholesale net sales and 11% of our total net sales.

Macy’s accounted for approximately $39.0 million, or 10% of our wholesale net

sales and 8% of our total net sales in 2009.

Distribution

Channels

United

States

We sell

our products principally through department stores, specialty stores and

discount stores and through our company-owned retail stores. For the year ended

December 31, 2009, our Retail segment and our Wholesale segment generated net

sales of approximately $123.7 million and $379.8 million, or 25% and 75% of our

total net sales, respectively. Each of these distribution channels are described

below.

5

Steve Madden and Steven Retail

Stores. As of December 31, 2009, we operated 84 company-owned retail

stores under the Steve Madden name and four under the Steven name and our

e-commerce website (at www.stevemadden.com). We believe that our retail stores

will continue to enhance overall sales, profitability, and our ability to react

to changing consumer trends. The stores are also a marketing tool that allows us

to strengthen brand recognition and to showcase selected items from our full

line of branded and licensed products. Furthermore, the retail stores provide us

with a venue to test and introduce new products and merchandising strategies.

Specifically, we often test new designs at our Steve Madden retail stores before

scheduling them for mass production and wholesale distribution. In addition to

these test marketing benefits, we have been able to leverage sales information

gathered at Steve Madden retail stores to assist our wholesale customers in

order placement and inventory management.

A typical

Steve Madden store is approximately 1,400 to 1,600 square feet and is located in

a mall or street location that we expect will attract the highest concentration

of our core demographic, style-conscious customer base. The Steven stores, which

are generally the same size as our Steve Madden stores, have a more

sophisticated design and format styled to appeal to their more mature target

audience. In addition to carefully analyzing mall demographics and locations, we

set profitability guidelines for each potential store site. Specifically, we

target well trafficked sites at which the demographics fit our consumer profile

and seek new locations where the projected fixed annual rent expense stays

within our guidelines. By setting these guidelines, we seek to identify stores

that will contribute to our overall profitability both in the near and longer

terms.

Department Stores. We

currently sell to over 1,900 doors of 17 department stores throughout the United

States. Our major accounts include Macy’s, Nordstrom, Dillard’s and Lord &

Taylor.

We

provide merchandising support to our department store customers which includes

in-store fixtures and signage, supervision of displays and merchandising of our

various product lines. Our wholesale merchandising effort includes the creation

of in-store concept shops, where a broader collection of our branded products

are showcased. These in-store concept shops create an environment that is

consistent with our image and are designed to enable the retailer to display and

sell a greater volume of our products per square foot of retail space. In

addition, these in-store concept shops encourage longer term commitment by the

retailer to our products and enhance consumer brand awareness.

In

addition to merchandising support, our key account executives maintain weekly

communications with their respective accounts to guide them in placing orders

and to assist them in managing inventory, assortment and retail sales. We

leverage our sell-through data gathered at our retail stores to assist

department stores in allocating their open-to-buy dollars to the most popular

styles in the product line and to phase out styles with weaker sell-throughs,

which reduces markdown exposure at season’s end.

Specialty Stores/Catalog

Sales. We currently sell to specialty store locations throughout the

United States. Our major specialty store accounts include DSW, Famous Footwear

and Journeys. We offer our specialty store accounts the same merchandising,

sell-through and inventory tracking support offered to our department store

accounts. Sales of our products are also made through various catalogs,

such as Victoria’s Secret.

Internet Sales. We operate an

Internet website, www.stevemadden.com, where customers can purchase numerous

styles of our Madden Women’s, Steven and Madden Men’s as well as selected styles

of Madden Girl, footwear and accessory products.

International

Our

products are available in many countries and territories worldwide via several

retail selling and distribution agreements. Under the terms of the various

agreements, the distributors and retailers are generally required to open a

minimum number of stores each year and to pay us a fee for each pair of footwear

purchased, and in many cases, an additional sales royalty as a percentage of

sales or a predetermined amount per unit of sale. Distributors are required to

purchase a specified minimum number of products within specified periods. The

agreements we have in place expire at various times through December 31, 2014

and include renewal options. These agreements are exclusive in their specific

territories, which include China, Canada, Mexico, the United Kingdom,

Israel, UAE, Turkey, Australia, Korea, Morocco, and several countries in

Southeast Asia, Europe and Central and South America.

6

Competition

The

fashion industry is highly competitive. We compete with specialty shoe and

accessory companies as well as companies with diversified footwear product

lines, such as Nine West, Skechers, Kenneth Cole, Nike, Guess and Jessica

Simpson. Our competitors may have greater financial and other resources than us.

We believe effective advertising and marketing, fashionable styling, high

quality, value and fast manufacturing turnaround are the most important

competitive factors and intend to continue to employ these elements as we

develop our products. However, we cannot be certain that we will be able to

compete successfully against our current and future competitors, or that

competitive pressures will not have a material adverse effect on our business,

financial condition and results of operations.

Marketing

and Sales

We have

focused on creating an integrated brand building program to establish Steve

Madden as a leading designer of fashion footwear for style-conscious young women

and men. Principal marketing activities include product placements in lifestyle

and fashion magazines, personal appearances by our founder and Creative and

Design Chief, Steve Madden, and in-store promotions. In addition, we continue to

promote our e-commerce website (www.stevemadden.com) where customers can

purchase products under the brands Steve Madden, Steven, Steve Madden Men’s and

selected styles from Madden Girl footwear, as well as view exclusive content,

participate in contests and “live chat” with customer service

representatives.

Management

Information Systems (MIS) Operations

Sophisticated

information systems are essential to our ability to maintain our competitive

position and to support continued growth. We operate on a dual AS/400 system

which provides system support for all aspects of our business, including

manufacturing purchase orders, customer purchase orders, order allocations,

invoicing, accounts receivable management, quick response replenishment,

point-of-sale support and financial and management reporting functions. We have

a PKMS bar coded warehousing system that is integrated with the wholesale system

in order to provide accurate inventory positions and quick response size

replenishment for our customers. In addition, we have installed an EDI system

which provides a computer link between us and certain wholesale customers that

enables both the customer and us to monitor purchases, shipments and invoicing.

The EDI system also improves our ability to respond to customer inventory

requirements on a weekly basis.

Intellectual

Property

Trademarks

We own

numerous trademarks including Steve Madden®, Steve Madden plus Design®, Steven

by Steve Madden® and various PEACE LOVE SHOES designs. As of December 31, 2009,

we have 216 U.S. and internationally registered trademarks or trademark

applications pending in the trademark offices of 67 countries around the

world including the U.S. From time to time we adopt new trademarks in connection

with the marketing of new product lines. We believe that our trademarks have

significant value and are important to the marketing of our products,

identifying the Company and distinguishing our products from the products of

others. We consider our Steve Madden®, Steve

Madden plus Design®, Steven by Steve Madden® and the various PEACE LOVE SHOES

design marks to be among our most valuable assets and have registered these

marks in numerous countries and in numerous International Classes. We act

aggressively to register and vigorously to protect our trademarks against

infringement. There can be no assurance, however, that we will be able to

effectively obtain rights to our marks throughout all of the countries of the

world. Moreover, no assurance can be given that others will not assert rights in

or ownership of, our marks and other proprietary rights or that we will be able

to resolve any such conflicts successfully. Our failure to protect such rights

from unlawful and improper appropriation may have a material adverse effect on

our business, financial condition, results of operations and

liquidity.

7

Trademark

Licensing

We

believe that expanding the Company’s presence beyond footwear and accessories is

a logical extension of the Company’s brands. Therefore, on October 20, 2009, we

licensed our Steve Madden® mark for the design, manufacture and worldwide

distribution of women’s fashion apparel and, on January 7, 2010, we licensed our

Steve Madden® and Steven by Steve Madden® marks for the design, manufacture and

worldwide distribution of women’s fashion jewelry. The new fashion apparel and

jewelry lines, which will initially ship in the spring and fall of 2010,

respectively, join our existing licenses for cold weather accessories,

sunglasses, eyewear, outerwear, bedding and hosiery offerings. Our licensees pay

us a royalty and, in substantially all of our license agreements, an advertising

fee equal to a percentage of net sales and a minimum royalty and advertising fee

in the event that specified net sales targets are not achieved. See Note A[13]

to our Consolidated Financial Statements included in this Annual Report on Form

10-K for additional disclosure regarding these licensing

arrangements.

In addition to out-licenses of our

trademarks, we also license from third parties certain marks used in connection

with certain of our product lines. We have a license from Betsey Johnson LLC

providing the right to use the Betsey Johnson® and Betseyville® trademarks in

connection with the sale and marketing of handbags, small leather goods, belts

and umbrellas. In addition, we have licenses from Dualstar Entertainment Group,

LLC under which the Company has the right to use the Olsenboye® trademark in

connection with the sale and marketing of footwear and accessories and the

Elizabeth and James® trademark in connection with the sale and marketing of

footwear. We also hold a license from Phat Fashions LLC to design, manufacture

and distribute women’s footwear, handbags and belts and related accessories

under the Fabulosity® brand and a license from Jones Investment Co. Inc. to use

the l.e.i.® trademark in connection with the marketing and sale of women’s

footwear exclusively to Wal-Mart. We also hold a license from Dafu Licensing,

Inc. to design, manufacture and distribute handbags and belts and related

accessories under the DF Daisy Fuentes® and the Daisy Fuentes® brands. We also

hold a license from IP Holdings LLC to sell Candie’s® banded footwear to Kohl’s.

Substantially all of these licensing agreements require us to make royalty and

advertising payments to the licensor equal to a percentage of our net sales and

a minimum royalty and advertising payment in the event that specified net sales

targets are not achieved.

See Item

7, “Management’s Discussion and Analysis of Financial Condition and Results of

Operations” and Note L[4] to our Consolidated Financial Statements included in

this Annual Report on Form 10-K for additional information relating to each of

the above referenced licensing arrangements.

Employees

On

February 5, 2010, we employed approximately 1,370 employees, of whom

approximately 700 work on a full-time basis and approximately 670 work on a

part-time basis, most of whom work in the Retail segment. All of our employees

are located in the United States with the exception of approximately 30

employees located in Hong Kong and China who perform quality control and

administrative duties. None of our employees are represented by a union. Our

management considers relations with our employees to be good. The Company has

never experienced a material interruption of its operations due to a labor

dispute.

Seasonality

Historically,

our merchandising businesses have experienced holiday retail seasonality. In

addition to seasonal fluctuations, our operating results fluctuate quarter to

quarter as a result of the timing of holidays, weather, the timing of larger

shipments of footwear, market acceptance of our products, product mix, pricing

and presentation of the products offered and sold, the hiring and training of

additional personnel, inventory write downs for obsolescence, the cost of

materials, the product mix between wholesale, retail and licensing businesses,

the incurrence of other operating costs and factors beyond our control, such as

general economic conditions and actions of competitors.

Backlog

We had

unfilled wholesale customer orders of $151.7 million and $90.5 million, as of

February 21, 2010 and 2009, respectively. Our backlog at a particular time

is affected by a number of factors, including seasonality, timing of market

weeks and wholesale customer purchases of our core basic products through our

open stock program. Accordingly, a comparison of backlog from period to period

may not be indicative of eventual shipments.

8

| ITEM 1A | RISK FACTORS |

You

should carefully consider the risks and uncertainties we describe below and the

other information in this Annual Report on Form 10-K before deciding to invest

in, sell or retain shares of our common stock. These are not the only risks and

uncertainties that we face. Additional risks and uncertainties that we do not

currently know about or that we currently believe are immaterial, or that we

have not predicted, may also harm our business operations or adversely affect

us. If any of these risks or uncertainties actually occurs, our business,

financial condition, results of operations and liquidity could be materially

harmed.

Fashion Industry

Risks. Our

success depends in significant part upon our ability to anticipate and respond

to product and fashion trends as well as to anticipate, gauge and react to

changing consumer demands in a timely manner. There can be no assurance that our

products will correspond to the changes in taste and demand or that we will be

able to successfully market products that respond to such trends. If we misjudge

the market for our products, we may be faced with significant excess inventories

for some products and missed opportunities for others. In addition, misjudgments

in merchandise selection could adversely affect our image with our customers

resulting in lower sales and increased markdown allowances for customers which

could have a material adverse effect on our business, financial condition,

results of operations and liquidity.

The

industry in which we operate is cyclical, with purchases tending to decline

during recessionary periods when disposable income is low. Purchases of

contemporary shoes and accessories tend to decline during recessionary periods

and also may decline at other times. There can be no assurance that we will be

able to grow or even maintain our current level of revenues and earnings, or

remain profitable in the future. A recession in the national or regional

economies or uncertainties regarding future economic prospects, among other

things, could affect consumer spending habits. The recent volatility and

disruption of global economic and financial market conditions has led to

declines in consumer confidence and spending in the United States and

internationally. Further deterioration or a continued weakness of economic and

financial market conditions for an extended period of time could have a material

adverse effect on our business, financial condition, results of operations and

liquidity.

In recent

years, the retail industry has experienced consolidation and other ownership

changes. In the future, retailers in the United States and in foreign markets

may further consolidate, undergo restructurings or reorganizations, or realign

their affiliations, any of which could decrease the number of stores that carry

our products or increase the ownership concentration within the retail industry.

While such changes in the retail industry to date have not had a material

adverse effect on our business or financial condition, results of operations and

liquidity, there can be no assurance as to the future effect of any such

changes.

Economic

Uncertainty and Political Risks. Our opportunities for long-term growth

and profitability are accompanied by significant challenges and risks,

particularly in the near term. Specifically, our business is dependent on

consumer demand for our products. We believe that declining consumer confidence

accompanied with changes in credit availability, interest rates, energy prices,

unemployment rates and consumers’ disposable income negatively impacted the

level of consumer spending for discretionary items during the years ended

December 31, 2008 and 2009. Despite the worsening retail environment, in 2009 we

achieved a substantial revenue growth in the Wholesale segment that was

partially offset by a small decrease in revenues in the Retail segment. A

continued weak economic environment could have a negative effect on the

Company’s sales and results of operations during the year ending December 31,

2010 and thereafter. In addition, unstable political conditions in some parts of

the world, including potential or actual international conflicts, or the

continuation or escalation of terrorism, could have a material adverse effect on

our business, financial condition, results of operations and

liquidity.

Inventory

Management. The

fashion-oriented nature of our products and the rapid changes in customer

preferences leave us vulnerable to an increased risk of inventory obsolescence.

Thus, our ability to manage our inventories properly is an important factor in

our operations. Inventory shortages can adversely affect the timing of shipments

to customers and diminish sales and brand loyalty. Conversely, excess

inventories can result in lower gross margins due to the excessive discounts and

markdowns that might be necessary to reduce inventory levels. Our inability to

effectively manage our inventory could have a material adverse effect on our

business, financial condition, results of operations and liquidity.

9

Dependence upon

Customers and Risks Related to Extending Credit to Customers. Our customers consist

principally of major department stores, mid-tier department stores, better

specialty stores and independently-owned boutiques. Certain of our department

store customers, including some under common ownership, account for significant

portions of our wholesale business.

We

generally enter into a number of purchase order commitments with our customers

for each of our lines every season and do not enter into long-term agreements

with any of our customers. Therefore, a decision by a significant customer,

whether motivated by competitive conditions, financial difficulties or

otherwise, to decrease the amount of merchandise purchased from us or to change

its manner of doing business could have a material adverse effect on our

business, financial condition, results of operations and liquidity.

We sell

our products primarily to retail stores across the United States and extend

credit based on an evaluation of each customer’s financial condition, usually

without collateral. While various retailers, including some of our customers,

have experienced financial difficulties in the past few years which increased

the risk of extending credit to such retailers, our losses due to bad debts have

been limited. Pursuant to the terms of our factoring agreement, our factor,

Rosenthal & Rosenthal, Inc., currently assumes the credit risk related to

approximately 83% of our accounts receivable. However, financial

difficulties of a customer could cause us to curtail business with such customer

or require us to assume more credit risk relating to such customer’s accounts

receivable.

Impact of Foreign

Manufacturers; Custom Duties. Virtually all of our products are

purchased through arrangements with a number of foreign manufacturers, primarily

from China, Mexico, Brazil, Italy, Spain and India.

Risks

inherent in foreign operations include work stoppages, transportation delays and

interruptions, changes in social, political and economic conditions which could

result in the disruption of trade from the countries in which our manufacturers

or suppliers are located, the imposition of additional regulations relating to

imports, the imposition of additional duties, taxes and other charges on

imports, significant fluctuations of the value of the dollar against foreign

currencies, or restrictions on the transfer of funds, any of which could have a

material adverse effect on our business, financial condition, results of

operations and liquidity. We do not believe that any such economic or political

condition will materially affect our ability to purchase products, since a

variety of materials and alternative sources are available. However, we cannot

be certain that we will be able to identify such alternative sources without

delay, if at all, or without greater cost to us. Our inability to identify and

secure alternative sources of supply in this situation could have a material

adverse effect on our business, financial condition, results of operations and

liquidity.

Our

imported products are also subject to United States custom duties. The United

States and the countries in which our products are produced or sold, from time

to time, impose new quotas, duties, tariffs, or other restrictions, or may

adversely adjust prevailing quota, duty or tariff levels, any of which could

have a material adverse effect on our business, financial condition, results of

operations and liquidity.

Possible Adverse

Impact of Manufacturers’ Inability to Manufacture in a Timely Manner, Meet

Quality Standards or to Use Acceptable Labor Practices. As is common in

the footwear industry, we contract for the manufacture of virtually all of

our products to our specifications through foreign manufacturers. We do not own

or operate any manufacturing facilities and, therefore, we are dependent upon

third parties for the manufacture of all of our products. The inability of a

manufacturer to ship orders of our products in a timely manner or to meet our

quality standards could cause us to miss the delivery date requirements of our

customers for those items, which could result in cancellation of orders, refusal

to accept deliveries or a reduction in purchase prices, any of which could have

a material adverse effect on our business, financial condition, results of

operations and liquidity.

Although

we enter into a number of purchase order commitments each season specifying a

time frame for delivery, method of payment, design and quality specifications

and other standard industry provisions, we do not have long-term contracts with

any manufacturer. As a consequence, any of these manufacturing relationships may

be terminated, by either party, at any time. Although we believe that other

facilities are available for the manufacture of our products, there can be no

assurance that such facilities would be available to us on an immediate basis,

if at all, or that the costs charged to us by such manufacturers would not be

greater than those presently paid.

10

We do not

control our licensing partners or independent manufacturers or their labor

practices. The violation of labor or other laws by an independent manufacturer

of ours or by one of our licensing partners, or the divergence of a

manufacturer’s or a licensing partner’s labor practices from those generally

accepted as ethical in the United States, could have a material adverse effect

on our business, financial condition, results of operations and

liquidity.

Intense Industry

Competition. The

fashion footwear industry is highly competitive and barriers to entry are low.

Our competitors include specialty companies as well as companies with

diversified product lines. The recent market growth in the sales of fashion

footwear has encouraged the entry of many new competitors and increased

competition from established companies. Most of these competitors, including

Nine West, Skechers, Kenneth Cole, Nike, Guess and Jessica Simpson may have

significantly greater financial and other resources than we do and there can be

no assurance that we will be able to compete successfully with other fashion

footwear companies. Increased competition could result in pricing pressures,

increased marketing expenditures and loss of market share, and could have a

material adverse effect on our business, financial condition, results of

operations and liquidity. We believe effective advertising and marketing,

branding of the Steve Madden® trademark, fashionable styling, high quality and

value are the most important competitive factors and we plan to continue to

employ these elements as we develop our products. Our inability to effectively

advertise and market our products could have a material adverse effect on our

business, financial condition, results of operations and liquidity.

Expansion of

Retail Business.

Our continued growth depends to a significant degree on further developing the

Steve Madden, Stevies, Steven, Madden Girl, Steve Madden Men’s, Steve Madden

Fix, Candies, Elizabeth and James, Olsenboye and l.e.i. brands, creating new

product categories and businesses and operating company-owned Steve Madden and

Steven stores on a profitable basis. During the year ended December 31, 2009, we

opened two, closed seven and licensed out three Steve Madden retail stores and

have plans to open one to three and close six to nine stores in the year ending

December 31, 2010. We also remodeled seven existing stores. Our future

expansion plan includes the opening of stores in new geographic markets as well

as strengthening existing markets. New markets have in the past presented, and

will continue to present, competitive and merchandising challenges that are

different from those faced by us in our existing markets. There can be no

assurance that we will be able to open new stores, and if opened, that such new

stores will be able to achieve sales and profitability levels consistent with

management’s expectations. Our retail expansion is dependent on a number of

factors, including our ability to locate and obtain favorable store sites, the

performance of our wholesale and retail operations, and our ability to manage

such expansion and hire and train personnel. Past comparable store sales results

may not be indicative of future results, and there can be no assurance that our

comparable store sales results can be maintained or will increase in the future.

In addition, there can be no assurance that our strategies to increase other

sources of revenue, which may include expansion of our licensing activities,

will be successful or that our overall sales or profitability will increase or

not be adversely affected as a result of the implementation of such retail

strategies.

Management of

Growth. Our

operations have increased and will continue to increase demand on our

managerial, operational and administrative resources. We have recently invested

significant resources in, among other things, our management information systems

and hiring and training new personnel. However, in order to manage currently

anticipated levels of future demand, we may be required to, among other things,

expand our distribution facilities, establish relationships with new

manufacturers to produce our product, and continue to expand and improve our

financial, management and operating systems. There can be no assurance that we

will be able to manage future growth effectively and a failure to do so could

have a material adverse effect on our business, financial condition, results of

operations and liquidity.

Seasonal and

Quarterly Fluctuations.

Our results may fluctuate quarter to quarter as a result of the timing of

holidays, weather, the timing of larger shipments of footwear, market acceptance

of our products, the mix, pricing and presentation of the products offered and

sold, the hiring and training of additional personnel, inventory write downs for

obsolescence, the cost of materials, the product mix between wholesale, retail

and licensing businesses, the incurrence of other operating costs and factors

beyond our control, such as general economic conditions and actions of

competitors. In addition, we expect that our sales and operating results may be

significantly impacted by the opening of new retail stores and the introduction

of new products. Accordingly, the results of operations in any quarter will not

necessarily be indicative of the results that may be achieved for a full fiscal

year or any future quarter.

11

Trademark

Protection. We

believe that our trademarks and other proprietary rights are important to our

success and our competitive position. Accordingly, we devote substantial

resources to the establishment and protection of our marks on a worldwide basis.

Nevertheless, there can be no assurance that the actions taken by us to

establish and protect our marks and other proprietary rights will be adequate to

prevent imitation of our products by others or to prevent others from seeking to

block sales of our products on the basis that our products violate the

trademarks and proprietary rights of others. Moreover, no assurance can be given

that others will not assert rights in, or ownership of, trademarks and other

proprietary rights of ours or that we will be able to successfully resolve such

conflicts. In addition, the laws of certain foreign countries may not protect

proprietary rights to the same extent as do the laws of the United States. Our

failure to establish and then protect such proprietary rights from unlawful and

improper utilization could have a material adverse effect on our business,

financial condition, results of operations and liquidity.

Foreign Currency

Fluctuations. We

make approximately 99% of our purchases in U.S. dollars. However, we source

substantially all of our products overseas and, as such, the cost of these

products may be affected by changes in the value of the relevant currencies.

Changes in currency exchange rates may also affect the relative prices at which

we and our foreign competitors sell products in the same market. There can be no

assurance that foreign currency fluctuations will not have a material adverse

effect on our business, financial condition, results of operations and

liquidity.

Dependence on Key

Personnel. The future of our

business depends to a significant degree on the skills and efforts of our

Creative and Design Chief, Steven Madden, and our senior executives. If we lose

the services of our Creative and Design Chief or any of our senior executives,

and especially if any of our executives joins a competitor or forms a competing

company, our business and financial performance could be seriously harmed. A

loss of our Creative and Design Chief’s or any of our executive officers’

skills, knowledge of the industry, contacts and expertise could cause a setback

to our operating plan and strategy.

Outstanding

Options. As of

March 9, 2010, there were outstanding options to purchase an aggregate of

approximately 1,076,000 shares of our common stock. Holders of such

options are likely to exercise them when the market price of our stock is

significantly higher than the exercise price of the options. Further, while

options are outstanding, they may adversely affect the terms on which we could

obtain additional capital, if required.

| ITEM 1B | UNRESOLVED STAFF COMMENTS |

None.

| ITEM 2 | PROPERTIES |

We lease

approximately 41,900 square feet for our corporate headquarters and sample

production facilities at 52-16 Barnett Avenue, Long Island City, NY 11104

pursuant to a lease which expires on June 30, 2013. The Steve Madden showroom is

located at 1370 Avenue of the Americas, New York, NY. All of our brands are

displayed for sale from this 9,917 square foot space. The lease for our showroom

expires on February 28, 2013.

We lease

approximately 20,000 square feet for our Accessories Division’s offices and

showroom space at 10 West 33rd Street, New York, NY. The lease expires on

December 31, 2014.

We lease

approximately 6,500 square feet for our Madden Zone Division’s office space at

17-19 West 34th Street, New York, NY. The initial term of the lease expires on

April 30, 2010 with an option, at our election, to extend it on a month-to-month

basis that can be terminated by either party with 30 days’ prior written

notice.

We

maintain approximately 7,200 square feet as a storage facility at 25-15 Borough

Place, Woodside, NY. The lease for this space expires on October 31,

2013.

We own a

building that is approximately 2,200 square feet that is located across the

street from our executive offices at 38-35 Woodside Avenue, Long Island City, NY

11104.

12

We lease

approximately 3,600 square feet for office space in Kwai Chung, Hong Kong. This

lease will expire on March 4, 2011.

In

addition, we lease approximately 4,825 square feet for office space in Kuangdong

Province, China. This lease will expire on January 31, 2013.

All of

our retail stores are leased pursuant to leases that, under their original

terms, extend for an average of ten years. A majority of the leases include

clauses that provide for contingent rental payments if gross sales exceed

certain targets and, as such, a majority of the leases enable us and/or the

landlord to terminate the lease in the event that our gross sales do not achieve

certain minimum levels during a prescribed period. Many of the leases contain

rent escalation clauses to compensate for increases in operating costs and real

estate taxes. The current terms of our retail store leases, including our three

licensed stores and two unoccupied locations, expire as follows:

|

Years

Lease Terms Expire

|

Number

of Stores

|

|

|

2010

|

12

|

|

|

2011

|

14

|

|

|

2012

|

8

|

|

|

2013

|

13

|

|

|

2014

|

5

|

|

|

2015

|

5

|

|

|

2016

|

6

|

|

|

2017

|

14

|

|

|

2018

|

10

|

|

|

2019

|

6

|

|

|

2020

|

1

|

| ITEM 3 | LEGAL PROCEEDINGS |

On June

24, 2009, The Center For Environmental Health filed a lawsuit, Center for Environmental Health v.

Lulu NYC, LLC, Steve Madden, Ltd., Steve Madden Retail, Inc., et al.,

Case No. RG09459448, in California Superior Court, Alameda County, against the

Company and dozens of other California retailers and vendors of leather, vinyl,

and/or imitation leather handbags, belts, and shoes alleging that the retailers

and vendors failed to warn that certain of such products may expose California

citizens to lead and lead compounds. The parties have been in negotiations to

resolve the matters informally and have finalized the substance of a consent

judgment, the terms of which are not material to the Company’s Consolidated

Financial Statements.

On June

24, 2009, a class action lawsuit Shahrzad Tahvilian, et al. v. Steve

Madden Retail, Inc. and Steve Madden, Ltd., Case No. BC 414217, was filed

in the Superior Court of California, Los Angeles County, against the Company and

its wholly-owned subsidiary, Steven Madden Retail, Inc.. The complaint, which

seeks unspecified damages, alleges violations of California labor laws,

including, among other things, that the Company failed to provide mandated meal

breaks to its employees and failed to provide overtime pay as required. The

Company filed an answer in the litigation denying all allegations stated in the

complaint. The parties have agreed to submit the claim to private mediation,

which is scheduled for March 29, 2010. The Company, with the advice of legal

counsel, has evaluated the liability in this case and believes that it is not

likely to exceed $1 million. Accordingly, the Company accrued $1 million in the

fiscal year 2009. The accrual is subject to change to reflect the status of this

matter.

13

On August

10, 2005, following the conclusion of an audit of the Company conducted by

auditors of U.S. Customs and Border Protection (“U.S. Customs”) during 2004 and

2005, U.S. Customs issued a report that asserts that certain commissions that

the Company treated as “buying agents’ commissions” (which are non-dutiable)

should be treated as “selling agents’ commissions” and hence are dutiable. In

September of 2007, U.S. Customs notified the Company that it had finalized its

assessment of the underpaid duties to be $1.4 million. On October 20, 2005, U.S.

Immigration and Customs Enforcement notified the Company’s legal counsel that a

formal investigation of the Company’s importing practices had been commenced as

a result of the audit. The Company has contested the conclusions of the U.S.

Customs audit and filed a request for review and issuance of rulings thereon by

U.S. Customs Headquarters, Office of Regulations and Rulings, under internal

advice procedures. On November 28, 2007, U.S. Customs Headquarters informed the

Company that its request for internal advice had been accepted and was under

review. All efforts by U.S. Customs to collect additional duties, fees, interest

or penalties have been stayed pending final decision of U.S. Customs

Headquarters. In the event that the U.S. Customs auditors’ position is

ultimately upheld, the Company may be subject to monetary penalties. A final

determination of the matter may not occur for several months or even years. The

Company, with the advice of legal counsel, has evaluated the Company’s potential

liability in this matter, including additional duties, interest and penalties,

and believes that it is not likely to exceed $2.7 million. Therefore, as of

December 31, 2007, the Company had recorded a total reserve of $2.7 million that

was increased by $256 thousand in 2008 and $89 thousand in 2009 to reflect

anticipated additional interest costs, bringing the reserve to $3 million as of

December 31, 2009. Such reserve is subject to change to reflect the status of

this matter.

We have

been named as a defendant in certain other lawsuits in the normal course of

business. In the opinion of management, after consulting with legal counsel, the

liabilities, if any, resulting from these matters should not have a material

effect on our financial position or results of operations.

| ITEM 4 | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

No

matters were submitted to a vote of the holders of our common stock during the

last quarter of our fiscal year ended December 31, 2009.

| ITEM 5 | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information. Our

shares of common stock have traded on the NASDAQ Global Select Market since

August 1, 2007 and were traded on the NASDAQ National Market prior to that date.

The following table sets forth the range of high and low closing sales prices

for our common stock during each fiscal quarter during the two-year period ended

December 31, 2009 as reported by the NASDAQ Global Select. The trading volume of

our securities fluctuates and may be limited during certain periods. As a

result, the liquidity of an investment in our securities may be adversely

affected.

Common

Stock

|

High

|

Low

|

High

|

Low

|

||||||||||||||

|

2009

|

2008

|

||||||||||||||||

|

Quarter

ended March 31, 2009

|

$ | 22.80 | $ | 13.57 |

Quarter

ended March 31, 2008

|

$ | 19.52 | $ | 14.98 | ||||||||

|

Quarter

ended June 30, 2009

|

$ | 30.15 | $ | 19.04 |

Quarter

ended June 30, 2008

|

$ | 22.74 | $ | 16.05 | ||||||||

|

Quarter

ended September 30, 2009

|

$ | 37.25 | $ | 23.87 |

Quarter

ended September 30, 2008

|

$ | 28.36 | $ | 18.13 | ||||||||

|

Quarter

ended December 31, 2009

|

$ | 42.91 | $ | 35.68 |

Quarter

ended December 31, 2008

|

$ | 24.60 | $ | 14.20 | ||||||||

Holders. As of March 9, 2010,

there were 18,348,786 shares of common stock outstanding and 76 holders of

record.

14

Dividends. With the exception

of a special cash dividend paid in November 2005 and in November 2006, we have

not declared or paid any cash dividends in the past to the holders of our common

stock and do not currently anticipate declaring or paying any cash dividends in

the foreseeable future. We intend to retain earnings, if any, to finance the

development and expansion of our business. Future dividend policy will be

subject to the discretion of our Board of Directors and will be contingent upon

future earnings, if any, our financial condition, capital requirements, general

business conditions, and other factors. Therefore, we can give no assurance that

any cash dividends of any kind will be paid to holders of our common stock in

the future.

Equity Compensation Plans.

Information regarding our equity compensation plans as of December 31, 2009 is

disclosed in Item 12,

“Security Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters.”

Issuer Repurchases of Equity

Securities. We did not repurchase any shares of our common stock during

the fourth quarter of fiscal 2009. In February and August of 2007, our Board of

Directors authorized increases of our previously announced share repurchase

program of $30 million and $37 million, respectively. At December 31, 2009, an

aggregate of $2 million remained authorized to repurchase our common stock. The

program has no set

expiration date.

15

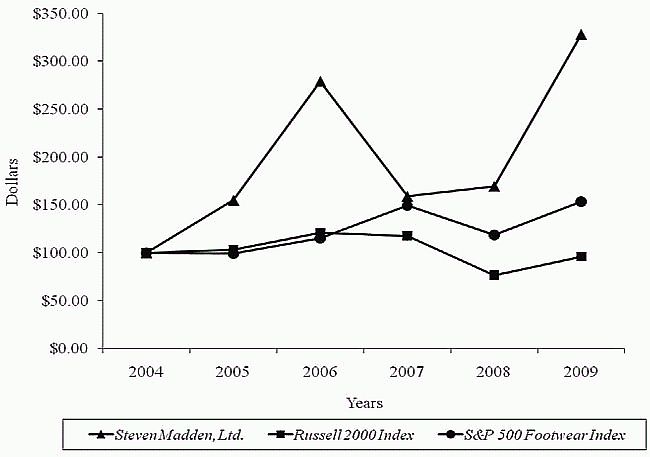

Performance Graph. The

following graph compares the yearly percentage change in the cumulative total

stockholder return on our common stock during the period beginning on December

31, 2004, and ending on December 31, 2009, with the cumulative total return on

the Russell 2000 Index and the S&P 500 Footwear Index. The comparison

assumes that $100 was invested on December 31, 2004 in our common stock and in

the foregoing indices and assumes the reinvestment of dividends.

|

12/31/2004

|

12/31/2005

|

12/31/2006

|

12/31/2007

|

12/31/2008

|

12/31/2009

|

|||||||||||||||||||

|

Steven

Madden, Ltd.

|

$ | 100.00 | $ | 154.98 | $ | 279.08 | $ | 159.07 | $ | 169.57 | $ | 328.00 | ||||||||||||

|

Russell

2000 Index

|

$ | 100.00 | $ | 103.32 | $ | 120.89 | $ | 117.57 | $ | 76.65 | $ | 95.98 | ||||||||||||

|

S&P

500 Footwear Index

|

$ | 100.00 | $ | 99.42 | $ | 114.97 | $ | 149.17 | $ | 118.42 | $ | 153.42 | ||||||||||||

16

|

SELECTED

FINANCIAL DATA

|

The following selected financial data has been derived from our audited

Consolidated Financial Statements. The Income Statement Data relating to 2009,

2008 and 2007, and the Balance Sheet data as of December 31, 2009 and 2008

should be read in conjunction with the information provided in Item 7,

“Management’s Discussion and Analysis of Financial Condition and Results of

Operations” and the notes to our Consolidated Financial Statements appearing

elsewhere in this Annual Report on Form 10-K.

|

INCOME

STATEMENT DATA

Year

Ended December 31,

(in

thousands, except per share data)

|

||||||||||||||||||||

|

2009

|

2008

|

2007

|

2006

|

2005

|

||||||||||||||||

|

Net

sales

|

$ | 503,550 | $ | 457,046 | $ | 431,050 | $ | 475,163 | $ | 375,786 | ||||||||||

|

Cost

of sales

|

287,361 | 270,222 | 257,646 | 276,734 | 236,631 | |||||||||||||||

|

Gross

profit

|

216,189 | 186,824 | 173,404 | 198,429 | 139,155 | |||||||||||||||

|

Commissions

and licensing fee income - net

|

19,928 | 14,294 | 18,351 | 14,246 | 7,119 | |||||||||||||||

|

Operating

expenses

|

(157,149 | ) | (156,212 | ) | (138,841 | ) | (134,377 | ) | (114,185 | ) | ||||||||||

|

Impairment

of goodwill

|

— | — | — | — | (519 | ) | ||||||||||||||

|

Income

from operations

|

78,968 | 44,906 | 52,914 | 78,298 | 31,570 | |||||||||||||||

|

Interest

income

|

2,096 | 2,620 | 3,876 | 3,703 | 2,554 | |||||||||||||||

|

Interest

expense

|

(93 | ) | (207 | ) | (65 | ) | (100 | ) | (164 | ) | ||||||||||

|

Loss

on sale of marketable securities

|

(182 | ) | (1,013 | ) | (589 | ) | (967 | ) | (500 | ) | ||||||||||

|

Income

before provision for income taxes

|

80,789 | 46,306 | 56,136 | 80,934 | 33,460 | |||||||||||||||

|

Provision

for income taxes

|

30,682 | 18,330 | 20,446 | 34,684 | 14,260 | |||||||||||||||

|

Net

Income

|

$ | 50,107 | $ | 27,976 | $ | 35,690 | $ | 46,250 | $ | 19,200 | ||||||||||

|

Basic

income per share

|

$ | 2.78 | $ | 1.53 | $ | 1.73 | $ | 2.21 | $ | 0.95 | ||||||||||

|

Diluted

income per share

|