Attached files

| file | filename |

|---|---|

| EX-23 - EXHIBIT 23 - FOSTER L B CO | exhibit23.htm |

| EX-31.2 - EXHIBIT 31.2 - FOSTER L B CO | exhibit312.htm |

| EX-32.0 - EXHIBIT 32.0 - FOSTER L B CO | exhibit320.htm |

| EX-31.1 - EXHIBIT 31.1 - FOSTER L B CO | exhibit311.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

[X]

|

Annual Report Pursuant to Section 13 or 15 (d) of the Securities Exchange Act of 1934

|

| For the fiscal year ended December 31, 2009 | |

Or

|

[ ]

|

Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

|

For the transition period from ______ to _____

|

Commission File Number

|

0-10436

|

L. B. FOSTER COMPANY

(Exact name of registrant as specified in its charter)

|

Pennsylvania

|

25-1324733

|

|

(State of Incorporation)

|

(I.R.S. Employer Identification No.)

|

|

415 Holiday Drive, Pittsburgh, Pennsylvania

|

15220

|

|

(Address of principal executive offices)

|

(Zip Code)

|

|

Registrant’s telephone number, including area code:

|

(412) 928-3417

|

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Name of Each Exchange On Which Registered

|

|

Common Stock, Par Value $0.01

|

NASDAQ Global Select Market

|

|

Securities registered pursuant to Section 12(g) of the Act:

|

None

|

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

|

[ ] Yes

|

[X] No

|

|

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act.

|

[ ] Yes

|

[X] No

|

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

|

[X] Yes

|

[ ] No

|

|

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for shorter period that the registrant was required to submit and post such files). *

|

[ ] Yes

|

[ ] No

|

|

* The registrant has not yet been phased into the interactive data requirements.

|

|

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this form 10-K.

|

[ ]

|

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer [ ]

|

Accelerated filer [X]

|

Non-accelerated filer [ ]

|

Smaller reporting company [ ]

|

|

(Do not check if a smaller reporting company)

|

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

|

[ ] Yes

|

[X] No

|

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter was $296,606,330.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

|

Class

|

Outstanding at February 19, 2010

|

|

Common Stock, Par Value $0.01

|

10,163,964 shares

|

Documents Incorporated by Reference:

Portions of the Proxy Statement prepared for the 2010 annual meeting of stockholders are incorporated by reference in Items 10, 11, 12 and 14 of Part III.

|

4

|

||

|

7

|

||

|

10

|

||

|

11

|

||

|

11

|

||

|

12

|

|

14

|

||

|

18

|

||

|

19

|

||

|

43

|

||

|

44

|

||

|

83

|

||

|

83

|

||

|

83

|

|

84

|

||

|

84

|

||

|

84

|

||

|

84

|

||

|

84

|

|

85

|

||

|

85

|

||

|

86

|

||

|

87

|

||

|

91

|

||

|

Certifications

|

|

Summary Description of Businesses

L. B. Foster Company is a leading manufacturer, fabricator and distributor of products and services for the rail, construction, energy and utility markets. As used herein, “Foster” or the “Company” means L. B. Foster Company and its divisions and subsidiaries, unless the context otherwise requires.

For rail markets, Foster provides a full line of new and used rail, trackwork, and accessories to railroads, mines and industry. The Company also designs and produces concrete railroad ties, insulated rail joints, power rail, track fasteners, coverboards and special accessories for mass transit and other rail systems worldwide.

For the construction industry, the Company sells steel sheet piling, H-bearing piling, pipe piling and provides rental sheet piling for foundation requirements. In addition, Foster supplies precast concrete buildings, fabricated structural steel, bridge decking, bridge railing, expansion joints and other products for highway construction and repair.

For tubular markets, the Company supplies pipe coatings for natural gas pipelines and utilities. The Company also produces threaded pipe products for industrial water well and irrigation markets and sells micropiles for construction foundation repair and slope stabilization.

The Company has a joint venture with L B Industries, Inc., L B Pipe & Coupling Products, LLC, in which we have a 45% ownership interest. This venture manufactures, markets and sells various products for the energy, utility and construction markets.

The Company classifies its activities into three business segments: Rail products, Construction products, and Tubular products. Financial information concerning the segments is set forth in Item 8, Note 19. The following table shows for the last three fiscal years the net sales generated by each of the current business segments as a percentage of total net sales.

|

Percentage of Net Sales

|

|||||

|

2009

|

2008

|

2007

|

|||

|

Rail Products

|

47%

|

46%

|

51%

|

||

|

Construction Products

|

48%

|

47%

|

42%

|

||

|

Tubular Products

|

5%

|

7%

|

7%

|

||

|

100%

|

100%

|

100%

|

|||

RAIL PRODUCTS

L. B. Foster Company’s rail products include heavy and light rail, relay rail, concrete ties, insulated rail joints, rail accessories and transit products. The Company is a major rail products supplier to industrial plants, contractors, railroads, mines and mass transit systems.

The Company sells heavy rail mainly to transit authorities, industrial companies, and rail contractors for railroad sidings, plant trackage, and other carrier and material handling applications. Additionally, the Company sells some heavy rail to railroad companies and to foreign buyers. The Company sells light rail for mining and material handling applications.

Rail accessories include trackwork, ties, track spikes, bolts, angle bars and other products required to install or maintain rail lines. These products are sold to railroads, rail contractors, industrial customers, and transit agencies and are manufactured within the Company or purchased from other manufacturers.

The Company’s Allegheny Rail Products (ARP) division engineers and markets insulated rail joints and related accessories for the railroad and mass transit industries. Insulated joints are manufactured at the Company’s facilities in Pueblo, CO and Niles, OH.

The Company’s Transit Products division supplies power rail, direct fixation fasteners, coverboards and special accessories primarily for mass transit systems. Most of these products are manufactured by subcontractors and are usually sold by sealed bid to transit authorities or to rail contractors, worldwide.

The Company’s Trackwork division sells new and relay trackwork for industrial and export markets.

The Company’s CXT subsidiary manufactures engineered concrete railroad ties for the railroad and transit industries at its facilities in Spokane, WA, Grand Island, NE and Tucson, AZ.

CONSTRUCTION PRODUCTS

L. B. Foster Company’s construction products consist of sheet, pipe and bearing piling, fabricated highway products, and precast concrete buildings.

Sheet piling products are interlocking structural steel sections that are generally used to provide lateral support at construction sites. Bearing piling products are steel H-beam sections which, in their principal use, are driven into the ground for support of structures such as bridge piers and high-rise buildings. Sheet piling is sold or rented and bearing piling is sold principally to public projects as well as the private sector.

Other construction products consist of precast concrete buildings, sold principally to national and state parks, and fabricated highway products. Fabricated highway products consist principally of fabricated structural steel, bridge decking, aluminum and steel bridge rail and other bridge products, which are fabricated by the Company. The major purchasers of these products are contractors for state, municipal and other governmental projects.

Sales of the Company’s construction products are partly dependent upon the level of activity in the construction industry. Accordingly, sales of these products have traditionally been somewhat higher during the second and third quarters than during the first and fourth quarters of each year.

TUBULAR PRODUCTS

The Company provides fusion bond and other coatings for corrosion protection on oil, gas and other pipelines. The Company also supplies special pipe products such as water well casing, column pipe, couplings, and related products for agricultural, municipal and industrial water wells. In addition, the Company sells micropiles for construction foundation repair and slope stabilization. Also, the Company owns a facility that will be leased to its corporate joint venture.

JOINT VENTURE

In May 2009, the Company completed the formation of a joint venture with L B Industries, Inc. and another party. The Company has a 45% ownership interest in the new joint venture, L B Pipe & Coupling Products, LLC, and made capital contributions of $1.4 million in 2009.

During the third quarter of 2009, the Company purchased approximately 35 acres of land in Magnolia, TX for approximately $1.1 million and built a facility which will ultimately be leased to the joint venture. This venture will manufacture, market and sell various products, including couplings and micropile, for the energy, utility and construction markets. The joint venture commenced operations during 2010.

MARKETING AND COMPETITION

L. B. Foster Company generally markets its rail, construction and tubular products directly in all major industrial areas of the United States through a national sales force of 55 people, including outside sales, inside sales, and customer service representatives. The Company maintains 14 sales offices and 17 warehouses, plant and yard facilities located throughout the country. During 2009, approximately 4% of the Company’s total sales were for export.

The major markets for the Company’s products are highly competitive. Product availability, quality, service and price are principal factors of competition within each of these markets. No other company provides the same product mix to the various markets the Company serves. There are one or more companies that compete with the Company in each product line. Therefore, the Company faces significant competition from different groups of companies.

RAW MATERIALS AND SUPPLIES

Most of the Company’s inventory is purchased in the form of finished or semi-finished product. With the exception of relay rail which is purchased from railroads or rail take-up contractors, the Company purchases most of its inventory from domestic and foreign steel producers. There are few domestic suppliers of new rail products and the Company could be adversely affected if a domestic supplier ceased making such material available to the Company. Additionally, the Company has an agreement with a steel mill to distribute steel sheet piling and bearing pile in North America. The Company also purchases cement and aggregate used in its concrete railroad tie and precast concrete building businesses from a variety of suppliers.

The Company’s purchases from foreign suppliers are subject to the usual risks associated with changes in international conditions and to United States laws which could impose import restrictions on selected classes of products and anti-dumping duties if products are sold in the United States below certain prices.

BACKLOG

The dollar amount of firm, unfilled customer orders at December 31, 2009 and 2008 by business segment follows:

|

December 31,

|

||||||||

|

2009

|

2008

|

|||||||

|

In thousands

|

||||||||

|

Rail Products

|

$ | 53,350 | $ | 68,438 | ||||

|

Construction Products

|

116,128 | 57,626 | ||||||

|

Tubular Products

|

3,212 | 6,524 | ||||||

|

Total from Continuing Operations

|

$ | 172,690 | $ | 132,588 | ||||

Approximately 6% of the December 31, 2009 backlog is related to projects that will extend beyond 2010.

RESEARCH AND DEVELOPMENT

The Company’s expenditures for research and development are not material.

ENVIRONMENTAL DISCLOSURES

It is not possible to quantify the potential impact of actions regarding environmental matters, particularly for future remediation and other compliance efforts. In the opinion of management, compliance with environmental protection laws will not have a material adverse effect on the financial condition, competitive position, or capital expenditures of the Company. However, the Company’s efforts to comply with stringent environmental regulations may have an adverse effect on the Company’s future earnings.

EMPLOYEES AND EMPLOYEE RELATIONS

As of December 2009, the Company had 593 employees, of whom 347 are hourly production workers and 246 are salaried employees. Of these hourly production workers, 134 are represented by unions. The Company has not suffered any major work stoppages during the past five years and considers its relations with its employees to be satisfactory.

Substantially all of the Company’s hourly paid employees are covered by one of the Company’s noncontributory, defined benefit plans or defined contribution plans. Substantially all of the Company’s salaried employees are covered by a defined contribution plan.

Forward Looking Statements

We make forward looking statements in this report based upon management’s understanding of our business and markets and on information currently available to us. Such statements include information regarding future events and expectations and frequently include words such as “believes,” “expects,” “anticipates,” “intends,” “plans,” “estimates,” or other similar expressions.

Forward looking statements include known and unknown risks and uncertainties. Actual future results may differ greatly from these statements and expectations that we express in this report. We encourage all readers to carefully consider the Risk Factors below and all the information presented in our 2009 Annual Report on Form 10-K and caution you not to rely unduly on any forward looking statements.

The forward looking statements in this report are made as of the date of this report and we assume no obligation to update or revise any forward looking statement, whether as a result of new information, future developments or otherwise.

Risks and Uncertainties

Acquisition Growth Strategy

We continue to evaluate acquisition opportunities that have the potential to support and strengthen our business. We can give no assurances that any opportunity will arise or if they do, that they will be consummated or that potential additional financing will be available. In addition, acquisitions involve inherent risks that the acquired business will not perform in accordance with our expectations. We may not be able to achieve the synergies and other benefits we expect from the integration as successfully or rapidly as projected, if at all. Our failure to integrate newly acquired operations could prevent us from realizing our expected rate of return on an acquired business and could have a material or adverse effect on our results of operations and financial condition.

On February 16, 2010, L.B. Foster Company, a Pennsylvania corporation (“L.B. Foster”), Foster Thomas Company, a West Virginia corporation and a wholly-owned subsidiary of L.B. Foster (“Purchaser”), and Portec Rail Products, Inc., a West Virginia corporation (“Portec” or the “Company”), entered into an Agreement and Plan of Merger (the “Merger Agreement”). Should the merger not be consummated, we would continue with our above acquisition growth strategy. More information regarding the merger can be found in the “Recent Developments” section of Management’s Discussion and Analysis of Financial Condition and Results of Operations. The following two risk factors relate to the proposed merger.

Merger Agreement Consummation

The consummation of the Merger Agreement with Portec is subject to various conditions including the acceptance of the tender offer by at least 65% of the Shareholders of Portec, the absence of legal prohibitions and the receipt of necessary regulatory approvals to the extent they relate to antitrust and competition laws, including the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended. Consummation of the merger is not subject to a financing condition.

Loss of Key Employees or Customers or Otherwise Cause Business Disruption resulting from Merger

Until completion of the Merger Agreement, we and Portec have operated and will continue to operate independently. It is possible that the merger could result in the loss of key employees, result in the disruption of one or more of the companies’ ongoing businesses or identify inconsistencies in standards, controls, procedures and policies that adversely affect one or more of the companies’ ability to maintain relationships with customers, suppliers or creditors. Employee retention before, during or after the combination may be challenging as employees may experience uncertainty about future roles until strategies with regard to the combined company are announced or executed.

General Economic Conditions

We could be adversely impacted by prolonged negative changes in economic conditions affecting either our suppliers or customers as well as the capital markets. No assurances can be given that we will be able to successfully mitigate various prolonged uncertainties including materials cost variability, delayed or reduced customer payments and access to available capital resources outside of operations.

Markets and Competition

We face strong competition in all of the markets in which we participate. Our response to competitor pricing actions and new competitor entries into our product lines, could negatively impact our overall pricing in the marketplace. Efforts to improve pricing could negatively impact our sales volume in all product categories. Significant negative developments in these areas could adversely affect our financial results and condition.

Customer Reliance

Foster could be adversely affected by changes in the business or financial condition of a customer or customers. No assurances can be given that a significant downturn in the business or financial condition of a customer, or customers, would not impact our results of operations and /or financial condition.

A significant decrease in capital spending by our railroad customers could negatively impact our product revenue. The Company’s CXT Rail operation and Allegheny Rail Products division are dependent on the Union Pacific Railroad (UPRR) for a significant portion of their business. The CXT Rail operation was awarded a long-term contract in 2005 from the UPRR for the supply of prestressed concrete railroad ties. CXT Rail expanded and modernized its Grand Island, NE plant in 2005, and completed construction of a new facility in Tucson, AZ in 2006 to accommodate the contract’s requirements. UPRR has agreed to purchase minimum annual quantities from the Grand Island, NE facility through December 2010, and the Tucson, AZ facility through December 2012.

A substantial portion of our operations are heavily dependent on governmental funding of infrastructure projects. Many of these projects have “Buy America” or “Buy American” provisions. Significant changes in the level of government funding of these projects could have a favorable or unfavorable impact on our operating results. Additionally, government actions concerning “Buy America” provisions, taxation, tariffs, the environment, or other matters could impact our operating results.

Supplier Reliance

In our rail and piling distributed products businesses, we rely on one or two suppliers for key products that we sell to our customers. No assurances can be given that a significant downturn in the business of one of these suppliers, a disruption in their manufacturing operations, an unwillingness to continue to sell to us or a disruption in the availability of existing and new piling and rail products would not adversely impact our financial results.

Raw Material Costs and Availability

Most of Foster’s businesses utilize steel as a significant product component. The steel industry is cyclical and prices as well as availability are subject to international market forces. We also use significant amounts of cement and aggregate in our concrete railroad tie and our precast concrete building businesses. Cement and aggregate prices are subject to market conditions but this has not yet had a significant impact on the Company. No assurances can be given that our financial results would not be adversely affected if prices or availability of these materials were to change in a significantly unfavorable manner.

Joint Venture

We have a joint venture with L B Industries, Inc. and another party to manufacture, market and sell various products for the energy, utility and construction markets. In connection with the joint venture agreement, we are required to make initial capital contributions of $1.9 million of which there remains approximately $0.5 million at December 31, 2009. No assurances can be given that additional capital contributions will not be required or that the joint venture will perform in accordance with our expectations.

Union Workforce and Labor Relations

Three of the Company’s manufacturing facilities are staffed by employees represented by labor unions. These 134 employees are currently working under two separate collective bargaining agreements.

In October 2007, we negotiated the renewal of the collective bargaining agreement with our Spokane, WA workforce represented by the United Steelworkers Local Number 338. This agreement, covering approximately 90 employees, expires in September 2011.

In March 2008, we negotiated the renewal of the collective bargaining agreement with our Bedford, PA workforce represented by the Shopman’s Local Union Number 527. This agreement, covering approximately 40 employees, expires in March 2011.

The existing collective bargaining agreements may not prevent a work stoppage at L. B. Foster’s facilities.

Legal Contingencies

Changes in our expectations of the outcome of certain legal actions could vary materially from our current expectations and adversely affect our financial results and/or financial condition.

DM&E Contingent Payments

As part of the 2007 sale of our investment in the Dakota, Minnesota and Eastern Railroad (DM&E) to the Canadian Pacific Railway Limited (CP), we received the right to future contingent payments based on (i) construction commencing on the Powder River Basin Expansion Project (PRB) and (ii) certain PRB tonnage thresholds being surpassed. The CP is obligated to pay the DM&E’s former equity holders an aggregate of $350.0 million, plus interest at 5% per annum, if the CP commences construction of the PRB expansion prior to December 31, 2025. Additionally, CP shall cause the former equity holders to receive certain payments not to exceed $707.0 million if the CP attains milestones, as set forth in the sales agreement, related to PRB coal tonnage thresholds prior to December 31, 2025.

Our share of any of this construction milestone payment or individual future coal milestone payments, if any such payments are made, prior to expenses and any offsets, is approximately 12¼%. No assurances can be given that any of these payments will be made and the CP has stated that it may take several years for it to determine whether to construct the PRB expansion. For more information regarding the sale of our investment in the DM&E, please see our Management’s Discussion and Analysis of Financial Condition and Results of Operations in Form 10-K for the year ended December 31, 2007.

Unexpected Events

Unexpected events including fires or explosions at facilities, natural disasters, war, unplanned outages, equipment failures, failure to meet product specifications, or a disruption in certain of our operations may cause our operating costs to increase or otherwise impact our financial performance.

None.

The location and general description of the principal properties which are owned or leased by L. B. Foster Company, together with the segment of the Company’s business using the properties, are set forth in the following table:

|

Location

|

Function

|

Acres

|

Business Segment

|

Lease Expires

|

|

Bedford, PA

|

Bridge component fabricating plant.

|

10

|

Construction

|

Owned

|

|

Birmingham, AL

|

Pipe coating facility.

|

32

|

Tubular

|

2017

|

|

Columbia City, IN

|

Rail processing facility and yard storage.

|

22

|

Rail

|

Owned

|

|

Georgetown, MA

|

Bridge component fabricating plant.

|

11

|

Construction

|

Owned

|

|

Grand Island, NE

|

CXT concrete tie plant.

|

9

|

Rail

|

2010

|

|

Hillsboro, TX

|

Precast concrete facility.

|

9

|

Construction

|

Owned

|

|

Houston, TX

|

Casing, upset tubing, threading, heat treating and painting. Yard storage.

|

20

|

Tubular, Rail and Construction

|

2018

|

|

Magnolia, TX

|

Joint venture manufacturing facility.

|

35

|

Tubular

|

Owned

|

|

Niles, OH

|

Rail fabrication. Yard storage.

|

35

|

Rail

|

Owned

|

|

Petersburg, VA

|

Piling storage facility.

|

48

|

Construction

|

Owned

|

|

Pueblo, CO

|

Rail joint manufacturing and lubricator assembly.

|

9

|

Rail

|

Owned

|

|

Spokane, WA

|

CXT concrete tie plant.

|

13

|

Rail

|

2010

|

|

Spokane, WA

|

Precast concrete facility.

|

5

|

Construction

|

2012

|

|

Tucson, AZ

|

CXT concrete tie plant.

|

19

|

Rail

|

2012

|

The lease covering the Grand Island, NE CXT concrete tie plant expires in December 2010 and is associated with the concrete tie supply agreement with the UPRR which also expires in December 2010. The Company plans to enter into negotiations with the UPRR in 2010 to extend both the concrete tie supply agreement and the lease for the concrete tie plant.

The lease for the Spokane, WA CXT concrete tie plant expires in July 2010. The Company anticipates that this lease will be extended prior to its expiration.

Including the properties listed above, the Company has 14 sales offices, including its headquarters in Pittsburgh, PA, and 17 warehouses, plant and yard facilities located throughout the country. The Company’s facilities are in good condition.

In the second quarter of 2004, a gas company filed a complaint against the Company in Allegheny County, PA, alleging that in 1989 the Company had applied epoxy coating on 25,000 feet of pipe and that, as a result of inadequate surface preparation of the pipe, the coating had blistered and deteriorated. In January 2010, the Company, while believing it had compelling defenses to these claims, settled the case for $25,000.

In November 2005, the City of Clearfield, Utah, filed suit in the Second District Court, Davis County, Utah, against the Utah Department of Transportation, a general contractor, four design engineers and/or consultants, a bonding company and the Company. The City alleged that the design and engineering of an overpass in 2000 had been faulty and that the Company had provided the mechanical stabilized earth wall system for the project. The City alleged that the embankment to the overpass began, in 2001, to fail and slide away from the stabilized earth wall system, resulting in damage in excess of $3,000,000. The City has agreed to settle its claims against several of the defendants and this settlement has been challenged by other defendants. The Company believes that it has meritorious defenses to these claims, that the Company's products complied with all applicable specifications and that other factors accounted for any alleged failure. The Company has referred this matter to its insurance carrier, which, although it reserved its right to deny coverage, has undertaken the defense of this claim.

Information concerning the executive officers of the Company is set forth below.

|

Name

|

Age

|

Position

|

|

Stan L. Hasselbusch

|

62

|

President and Chief Executive Officer

|

|

Merry L. Brumbaugh

|

52

|

Vice President – Tubular Products

|

|

Samuel K. Fisher

|

57

|

Senior Vice President – Rail Products

|

|

Donald L. Foster

|

54

|

Senior Vice President – Construction Products

|

|

Kevin R. Haugh

|

53

|

Vice President– Concrete Products

|

|

John F. Kasel

|

45

|

Senior Vice President – Operations and Manufacturing

|

|

Brian H. Kelly

|

50

|

Vice President – Human Resources

|

|

Gregory W. Lippard

|

41

|

Vice President – Rail Product Sales

|

|

Linda K. Patterson

|

60

|

Controller

|

|

David J. Russo

|

51

|

Senior Vice President, Chief Financial and Accounting Officer and Treasurer

|

|

David R. Sauder

|

39

|

Vice President – Global Business Development

|

|

David L. Voltz

|

57

|

Vice President, General Counsel and Secretary

|

Mr. Hasselbusch has been Chief Executive Officer and a director of the Company since January 2002, and President of the Company since March 2000. He served as Vice President – Construction and Tubular Products from December 1996 to December 1998 and as Chief Operating Officer from January 1999 until he was named Chief Executive Officer in January 2002.

Ms. Brumbaugh was elected Vice President – Tubular Products in November 2004, having previously served as General Manager, Coated Products since 1996. Ms. Brumbaugh has served in various capacities with the Company since her initial employment in 1980.

Mr. Fisher was elected Senior Vice President – Rail Products in October 2002, having previously served as Senior Vice President – Product Management since June 2000. From October 1997 until June 2000, Mr. Fisher served as Vice President – Rail Procurement. Prior to October 1997, Mr. Fisher served in various other capacities with the Company since his employment in 1977.

Mr. Donald Foster was elected Senior Vice President – Construction Products in February 2005, after having served as Vice President – Piling Products since November 2004 and General Manager of Piling since September 2004. Prior to joining the Company, Mr. Foster was President of Metalsbridge, a financed supply chain logistics entity. He served U.S. Steel Corporation as an officer from 1999 to 2003. During that time, Mr. Foster functioned as Vice President International, President of UEC Technologies and President, United States Steel International, Inc.

Mr. Haugh was elected Vice President – Concrete Products in March 2008 after joining the organization in February 2008. Prior to joining the Company, Mr. Haugh served as Executive Vice President of CANAC, Inc., a subsidiary of Savage Services, and Senior Vice President of Savage Services from 2001 to 2008. His career also included President of Railserve, Inc. prior to 2001.

Mr. Kasel was elected Senior Vice President – Operations and Manufacturing in May 2005 having previously served as Vice President – Operations and Manufacturing since April 2003. Mr. Kasel served as Vice President of Operations for Mammoth, Inc., a Nortek company from 2000 to 2003. His career also included General Manager of Robertshaw Controls and Operations Manager of Shizuki America prior to 2000.

Mr. Kelly was elected Vice President, Human Resources in October 2006 after joining the organization in September 2006. Prior to joining the Company, Mr. Kelly headed Human Resources for 84 Lumber Company from June 2004. Previously, he served as a Director of Human Resources for American Greetings Corp. from June 1994 to June 2004, and he began his career with Nabisco in 1984, serving in progressively responsible generalist human resources positions in both plants and the headquarters.

Mr. Lippard was elected Vice President – Rail Product Sales in June 2000. Prior to re-joining the Company in 2000, Mr. Lippard served as Vice President – International Trading for Tube City, Inc. from June 1998. Mr. Lippard served in various other capacities with the Company since his initial employment in 1991.

Ms. Patterson was elected Controller in February 1999, having previously served as Assistant Controller since May 1997 and Manager of Accounting since March 1988. Prior to March 1988, Ms. Patterson served in various other capacities with the Company since her employment in 1977.

Mr. Russo was elected Senior Vice President, Chief Financial and Accounting Officer and Treasurer in December 2002, having previously served as Vice President and Chief Financial Officer since July 2002. Mr. Russo was Corporate Controller of WESCO International Inc., a distributor of electrical and industrial MRO supplies and integrated supply services, from 1999 until joining the Company in 2002. Mr. Russo also served as Corporate Controller of Life Fitness Inc., an international designer, manufacturer and distributor of aerobic and strength training fitness equipment.

Mr. Sauder was elected Vice President – Global Business Development upon joining the Company in November 2008. Prior to joining the Company, Mr. Sauder was Director, Global Business Development at Joy Mining Machinery where he was responsible for leading mergers and acquisitions and new business initiatives from December 2007. Prior to that, he was Manager, Business Development for Eaton Corporation from April 2006 to December 2007. He previously held various positions of increasing responsibility at Duquesne Light Company from August 1998 to April 2006 and PNC Bank from February 1993 to August 1998.

Mr. Voltz was elected Vice President, General Counsel and Secretary in December 1987. Mr. Voltz joined the Company in 1981.

Officers are elected annually at the organizational meeting of the Board of Directors following the annual meeting of stockholders.

Code of Ethics

L. B. Foster Company has a legal and ethical conduct policy applicable to all directors and employees, including its Chief Executive Officer, Chief Financial Officer and Controller. This policy is posted on the Company’s website, www.lbfoster.com. The Company intends to satisfy the disclosure requirement regarding certain amendments to, or waivers from, provisions of its policy by posting such information on the Company’s website.

Stock Market Information

The Company had 525 common shareholders of record on January 31, 2010. Common stock prices are quoted daily through the NASDAQ Global Select Market quotation service (Symbol FSTR). The quarterly high and low bid price quotations for common shares (which represent prices between broker-dealers and do not include markup, markdown or commission and may not necessarily represent actual transactions) follow:

|

2009

|

2008

|

|||||||||||||||

|

Quarter

|

High

|

Low

|

High

|

Low

|

||||||||||||

|

First

|

$ | 33.14 | $ | 20.56 | $ | 51.57 | $ | 36.43 | ||||||||

|

Second

|

33.15 | 25.40 | 47.96 | 31.02 | ||||||||||||

|

Third

|

35.00 | 28.00 | 39.38 | 29.61 | ||||||||||||

|

Fourth

|

31.37 | 27.29 | 34.85 | 20.46 | ||||||||||||

Dividends

No cash dividends were paid on the Company’s Common stock during 2009 and 2008, and the Company has no plan to pay dividends in the foreseeable future. The Company’s ability to pay cash dividends is limited by its revolving credit agreement.

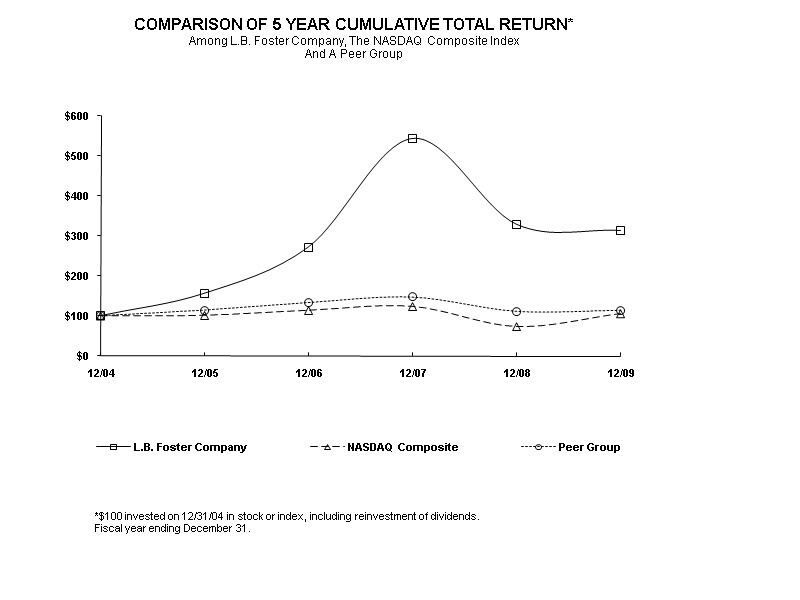

Performance Graph

The following table compares total shareholder returns for the Company over the last five years to the NASDAQ Composite Index and the Company’s Peer Group assuming a $100 investment made on December 31, 2004. Each of the three measures of cumulative total return assumes reinvestment of dividends. The stock performance shown on the graph below is not necessarily indicative of future price performance.

The Company’s Peer Group is composed of Michael Baker Corp., A.M. Castle & Co., Greenbriar Cos., Inc., Northwest Pipe Co, Texas Industries Inc. and Wabtec Corporation. The Company’s peer group was established by selecting similar companies in the rail, construction and steel industries.

|

Cumulative Total Return

|

||||||||||||||||||||||||

| 12/04 | 12/05 | 12/06 | 12/07 | 12/08 | 12/09 | |||||||||||||||||||

|

L.B. Foster Company

|

$ | 100.00 | $ | 156.24 | $ | 272.16 | $ | 543.38 | $ | 328.57 | $ | 313.13 | ||||||||||||

|

NASDAQ Composite

|

100.00 | 101.33 | 114.01 | 123.71 | 73.11 | 105.61 | ||||||||||||||||||

|

Peer Group

|

100.00 | 114.80 | 134.41 | 148.54 | 111.43 | 114.22 | ||||||||||||||||||

Securities Authorized for Issuance Under Equity Compensation Plans

The following table sets forth information as of December 31, 2009 with respect to compensation plans under which equity securities of the Company are authorized for issuance.

|

Number of securities

|

|

Number of securities remaining

|

||||||||||

|

to be issued upon

|

Weighted-average

|

available for future issuance

|

||||||||||

|

exercise of

|

exercise price of

|

under equity compensation

|

||||||||||

|

outstanding options,

|

outstanding options,

|

plans (excluding securities

|

||||||||||

|

warrants and rights

|

warrants and rights |

reflected in column (a))

|

||||||||||

|

Plan Category

|

( a )

|

( b )

|

( c )

|

|||||||||

|

Equity compensation plans approved by shareholders

|

180,950 | $ | 5.60 | 443,566 | ||||||||

|

Equity compensation plans not approved by shareholders

|

- | - | - | |||||||||

|

Total

|

180,950 | $ | 5.60 | 443,566 | ||||||||

The Company awarded shares of its common stock to its outside directors on a biannual basis from June 2000 through January 2003 under an arrangement not approved by the Company’s shareholders. A total of 22,984 shares of common stock were so awarded and this program has been terminated. At the Company’s 2003 Annual Shareholders’ Meeting, a new plan was approved by the Company’s shareholders under which outside directors received 2,500 shares of the Company’s common stock at each annual shareholder meeting at which such outside director was elected or re-elected, commencing with the Company’s 2003 Annual Shareholders’ Meeting. Through 2005 there were 30,000 shares issued under this plan. This plan was discontinued on May 24, 2006 when the Company’s shareholders approved the 2006 Omnibus Incentive Plan. Under the 2006 Omnibus Incentive Plan, non-employee directors automatically are awarded 3,500 shares, or a lesser amount determined by the directors, of the Company’s common stock at each annual shareholder meeting at which such non-employee director is elected or re-elected, commencing May 24, 2006. Through December 31, 2009 there were 56,000 fully vested shares issued under the 2006 Omnibus Incentive Plan to non-employee directors. Additionally, pursuant to the 2006 Omnibus Incentive Plan, during 2008 the Company issued to its officers approximately 11,000 fully-vested shares in lieu of a cash payment earned under the Three Year Incentive Plan.

Issuer Purchases of Equity Securities

The Company had no purchases of its equity securities for the three month period ended December 31, 2009. Purchases under the following plan have not been suspended:

|

Total Number

|

Approximate Dollar

|

|||

|

of Shares

|

Value of Shares

|

|||

|

Average

|

Purchased as

|

that May Yet Be

|

||

|

Total Number

|

Price

|

Part of Publicly

|

Purchased Under

|

|

|

Of Shares

|

Paid per

|

Announced Plans

|

the Plans

|

|

|

Purchased (1)

|

Share

|

or Programs

|

or Programs

|

|

|

Total

|

951,673

|

$29.78

|

951,673

|

$11,654,894

|

(1) On May 12, 2008, the Board of Directors authorized the repurchase of up to $25,000,000 of the Company’s common shares until June 30, 2010. On October 28, 2008, the Board of Directors authorized the repurchase of up to an additional $15,000,000 of the Company’s common shares until December 31, 2010 at which time this authorization will expire.

|

Year Ended December 31,

|

|||||||||||||||||||||||

|

Income Statement Data

|

2009 (1)

|

2008 (2)

|

2007 (3)

|

2006 (4)

|

2005 (5) (6)

|

||||||||||||||||||

|

(All amounts are in thousands, except per share data)

|

|||||||||||||||||||||||

| Net sales | $ | 381,962 | $ | 512,592 | $ | 508,981 | $ | 389,788 | $ | 325,990 | |||||||||||||

| Operating profit | $ | 24,357 | $ | 39,249 | $ | 38,980 | $ | 17,934 | $ | 8,210 | |||||||||||||

| Income from continuing operations | $ | 15,727 | $ | 27,746 | $ | 110,724 | $ | 10,715 | $ | 4,848 | |||||||||||||

| (Loss) income from discontinued | |||||||||||||||||||||||

| operations, net of tax | - | - | (31 | ) | 2,815 | 586 | |||||||||||||||||

| Net income | $ | 15,727 | $ | 27,746 | $ | 110,693 | $ | 13,530 | $ | 5,434 | |||||||||||||

| Basic earnings per common share: | |||||||||||||||||||||||

| Continuing operations | $ | 1.55 | $ | 2.60 | $ | 10.39 | $ | 1.03 | $ | 0.48 | |||||||||||||

| Discontinued operations | - | - | - | 0.27 | 0.06 | ||||||||||||||||||

| Basic earnings per common share | $ | 1.55 | $ | 2.60 | $ | 10.39 | $ | 1.30 | $ | 0.54 | |||||||||||||

| Diluted earnings per common share: | |||||||||||||||||||||||

| Continuing operations | $ | 1.53 | $ | 2.57 | $ | 10.09 | $ | 0.99 | $ | 0.46 | |||||||||||||

| Discontinued operations | - | - | - | 0.26 | 0.06 | ||||||||||||||||||

| Diluted earnings per common share | $ | 1.53 | $ | 2.57 | $ | 10.09 | $ | 1.25 | $ | 0.52 | |||||||||||||

| (1) |

2009 includes a pre-tax gain of $1,194,000 associated with the sale of available-for-sale marketable securities.

|

||||||||||||||||||||||

| (2) |

2008 includes pre-tax gains of $2,022,000 associated with the receipt of escrow proceeds related to the prior year sale of the Company’s DM&E investment and $1,486,000 from the sale and lease-back of our threaded products facility in Houston, TX.

|

||||||||||||||||||||||

| (3) |

2007 includes $8,472,000 in dividend income and a $122,885,000 pre-tax gain due to the announcement and consummation, respectively, of the sale of the Company’s investment in the DM&E.

|

||||||||||||||||||||||

| (4) |

2006 includes a $3,005,000 gain from the sale of the Company’s former Geotechnical Division which was classified as discontinued operations.

|

||||||||||||||||||||||

| (5) |

2005 was restated to reflect the classification of the Company’s former Geotechnical Division as discontinued operations.

|

||||||||||||||||||||||

| (6) |

2005 includes a benefit of $450,000 due to the release of a valuation allowance related to the Company’s ability to utilize state net operating losses and other state tax incentives prior to their expiration.

|

||||||||||||||||||||||

|

December 31,

|

||||||||||||||||||||

|

Balance Sheet Data

|

2009

|

2008

|

2007

|

2006

|

2005

|

|||||||||||||||

|

Total assets

|

$ | 333,168 | $ | 332,120 | $ | 330,772 | $ | 235,833 | $ | 178,868 | ||||||||||

|

Working capital

|

210,332 | 202,264 | 200,645 | 90,844 | 57,009 | |||||||||||||||

|

Long-term debt

|

13,197 | 21,734 | 28,056 | 54,273 | 29,276 | |||||||||||||||

|

Stockholders' equity

|

232,592 | 217,562 | 213,826 | 98,033 | 79,989 | |||||||||||||||

Executive Level Overview

During 2009 we experienced declining product prices and a heightened competitive environment as marketplace demand for many of our products declined. Our results were once again impacted by pricing reductions, and overall, both sales and profits declined from this occurrence. Additionally, the heightened competitive environment and lower market demand negatively impacted our sales volumes in 2009 as compared to 2008. The declining product costs also reduced LIFO reserve requirements by approximately $11.0 million.

During 2009, we purchased 86,141 shares of our common stock for approximately $1.9 million pursuant to two separate Board authorizations totaling $40.0 million. We have approximately $11.7 million remaining on the second authorization that expires on December 31, 2010.

From a cash flow perspective, highlights from 2009 are as follows:

|

|

·

|

We generated $25.7 million of cash from operating activities

|

|

|

·

|

We invested $7.5 million in our plants and facilities as well as a new joint venture

|

|

|

·

|

We repurchased $1.9 million of our common stock

|

|

|

·

|

$8.9 million of debt was repaid

|

While we expect to be challenged in 2010 by reduced sales volumes, reduced production volumes and a recessionary economic environment, we also expect to be profitable and to generate solid positive cash flow.

Recent Developments

On February 16, 2010, L.B. Foster Company, a Pennsylvania corporation (“L.B. Foster”), Foster Thomas Company, a West Virginia corporation and a wholly-owned subsidiary of L.B. Foster (“Purchaser”), and Portec Rail Products, Inc., a West Virginia corporation (“Portec” or the “Company”), entered into an Agreement and Plan of Merger (the “Merger Agreement”).

Pursuant to the terms of the Merger Agreement, Purchaser will commence a tender offer (the “Offer”) for all of the issued and outstanding shares of common stock, $1.00 par value per share (the “Company Common Stock”), of Portec at a price equal to $11.71 per share of Company Common Stock (the “Shares”) net to the seller in cash (the “Per-Share Amount”), without interest (and subject to applicable withholding taxes). Upon the terms and subject to the conditions set forth in the Merger Agreement, following a successful completion of the Offer, Purchaser will be merged with and into Portec with Portec surviving the merger as a wholly-owned subsidiary of L.B. Foster (the “Merger”). In the Merger, each Share (other than Shares owned by L.B. Foster, Purchaser, or shareholders, if any, who have perfected statutory dissenters’ rights under West Virginia law) will be converted into the right to receive the Per-Share Amount, without interest (and subject to applicable withholding taxes). The consummation of the Merger is conditioned upon the receipt of necessary approvals under the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended.

The Offer is conditioned upon, among other things, there being validly tendered and not withdrawn prior to the expiration of the Offer that number of Shares, together with any Shares then owned by L.B. Foster or Purchaser (including Shares subject to the Tender Agreement, discussed below), that, immediately prior to acceptance for payment pursuant to the Offer, represents at least sixty-five percent (65%) of (a) the aggregate number of Shares outstanding immediately prior to acceptance for payment, plus (b) the aggregate number of Shares issuable upon the exercise of any option, warrant, other right to acquire capital stock of the Company or other security exercisable for or convertible into Shares or other capital stock of the Company, any of which is outstanding immediately prior to acceptance for payment of Shares pursuant to the Offer (but excluding any Shares acquired by L.B. Foster or Purchaser pursuant to the Top-Up Option discussed below). Additional conditions to the Offer are set forth in Annex I to the Merger Agreement.

Pursuant to the Merger Agreement, the Company has granted to L.B. Foster and Purchaser an irrevocable option (the “Top-Up Option”) to purchase at the Per-Share Amount that certain number of Shares as is necessary for Purchaser to obtain ownership of at least 90% of the Shares on an as-converted, fully-diluted basis. L.B. Foster and Purchaser’s right to exercise the Top-Up Option expires upon the earlier of (i) the fifth (5th) business day after the later of the expiration date of the Offer and the expiration of any subsequent offering period or (ii) the termination of the Merger Agreement in accordance with its terms.

L.B. Foster, Purchaser and Portec have made customary representations and warranties in the Merger Agreement and agreed to certain customary covenants, including covenants regarding operation of the business of Portec and its subsidiaries prior to the closing and covenants prohibiting Portec from soliciting, or providing information or entering into discussions concerning, or proposals relating to alternative business combination transactions, except in limited circumstances relating to unsolicited proposals that are, or could reasonably be expected to result in, a proposal superior to the transactions contemplated by the Merger Agreement.

Concurrently with the execution of the Merger Agreement, L.B. Foster also entered into a Tender and Voting Agreement, dated as of February 16, 2010 (the “Tender Agreement”), with Purchaser and all of the directors and executive officers of Portec (the “D&O Shareholders”). As of February 16, 2010, the D&O Shareholders collectively owned 2,926,186 Shares, (approximately 30.47% of the Shares) directly or through affiliates. The D&O Shareholders have agreed to tender all of the Shares that each of them owns, including any Shares which such D&O Shareholder acquires ownership of after the date of the Tender Agreement and prior to the termination of the Tender Agreement, to Purchaser in the Offer. Furthermore, each D&O Shareholder has agreed, at any meeting of the shareholders of Portec, to vote all Shares (a) in favor of adopting the Merger Agreement and any transactions contemplated thereby, including the Merger, (b) against any alternative transaction proposal and (c) against any action that would delay, prevent or frustrate the Offer and the Merger and the related transactions contemplated by the Merger Agreement.

On February 24, 2010, a lawsuit related to the Offer and the Merger was filed in the Court of Common Pleas of Allegheny County, Pennsylvania, Everett Harper v. Marshall T. Reynolds, et al. The action is brought by Everett Harper, who claims to be a stockholder of Portec, on his behalf and on behalf of all others similarly situated, and seeks certification as a class action on behalf of all public Portec stockholders, except the defendants and their affiliates. The lawsuit names Portec, each of Portec’s directors, L.B. Foster and Purchaser as defendants. The lawsuit alleges, among other things, that Portec’s directors breached their fiduciary duties and L.B. Foster and Purchaser aided and abetted such alleged breaches of fiduciary duties. Based on these allegations, the lawsuit seeks, among other relief, injunctive relief enjoining the defendants from consummating the Offer and Merger. It also purports to seek recovery of the costs of the action, including reasonable attorney’s fees.

On March 2, 2010, Portec was served with a lawsuit related to the Offer and Merger which was filed on February 19, 2010 in the Circuit Court of Kanawha County, West Virginia, and captioned Barbara Petkus v. Portec Rail Products, Inc. et al., against Portec and each of Portec’s directors, on behalf of a purported class of public stockholders of Portec. The complaint alleges that the director defendants breached their fiduciary duties in connection with the Offer and Merger. Based on these allegations, the plaintiffs seek, among other relief, preliminary and permanent injunctive relief against the Offer and Merger, direction to the director defendants to properly exercise their fiduciary duties with respect to the Offer and Merger or another transaction, and the costs and expenses for the transaction, including reasonable allowance for attorneys’ and experts’ fess and expenses. On February 25, 2010, a request for production of documents relating to the Offer and Merger was filed in the Circuit Court of Kanawha County, West Virginia in connection with the above action.

On March 3, 2010, L.B. Foster and Purchaser were served with a lawsuit related to the Offer and the Merger which was filed on March 2, 2010 in the Court of Common Pleas of Allegheny County, Pennsylvania, and captioned Scott Phillips v. Portec Rail Products, Inc., et al. The action is brought by Scott Phillips, who claims to be a stockholder of Portec, on his own behalf and on behalf of all others similarly situated, and seeks certification as a class action on behalf of all public stockholders of Portec. The lawsuit names Portec, each of Portec’s directors, L.B. Foster and Purchaser as defendants. The lawsuit alleges, among other things, that Portec’s directors breached their fiduciary duties and that L.B. Foster and Purchaser aided and abetted such alleged breaches of fiduciary duties. Based on these allegations, the lawsuit seeks, among other relief, injunctive relief enjoining the defendants from consummating the Offer and the Merger. It also purports to seek recovery of the costs of the action, including reasonable attorney’s fees.

On March 4, 2010, Portec was served with a lawsuit related to the Offer and the Merger which was filed on March 3, 2010 in the Circuit Court of Kanawha County, West Virginia, and captioned Josh Furman v. Marshall Reynolds, et al., against Portec, each of Portec’s directors, L.B. Foster and Purchaser on behalf of a purported class of public stockholders of Portec. L.B. Foster and Purchaser have not yet been served in connection with the lawsuit. The complaint alleges that the director defendants breached their fiduciary duties in connection with the Offer and the Merger and that L.B. Foster and Purchaser aided and abetted such alleged breaches of fiduciary duties. Based on these allegations, the plaintiffs seek, among other relief, certification as a class action on behalf of all public Portec stockholders, preliminary and permanent injunctive relief against the Offer and the Merger, and the costs and expenses of the action, including reasonable allowance for attorneys’ and experts’ fees and expenses.

Also on March 4, 2010, Portec was served with a lawsuit related to the Offer and the Merger which was filed on February 24, 2010 in the Court of Common Pleas of Allegheny County, Pennsylvania, and captioned Richard S. Gesoff v. Marshall T. Reynolds, et al. The action is brought by Richard S. Gesoff, who claims to be a stockholder of Portec, on his own behalf and on behalf of all others similarly situated, and seeks certification as a class action on behalf of all public Portec stockholders, except the defendants and their affiliates. The lawsuit names Portec, each of Portec’s directors, L.B. Foster and Purchaser as defendants. L.B. Foster and Purchaser have not yet been served in connection with the lawsuit. The lawsuit alleges, among other things, that Portec’s directors breached their fiduciary duties and that L.B. Foster and Purchaser aided and abetted such alleged breaches of fiduciary duties. Based on these allegations, the lawsuit seeks, among other relief, injunctive relief enjoining the defendants from consummating the Offer and the Merger. It also purports to seek recovery of the costs of the action, including reasonable attorney’s fees.

2009 Developments

In 2009, we discovered that some of the prestressed concrete railroad ties manufactured between 2004 and 2005 by our CXT Rail operation in Grand Island, NE had failed in track. We believe the cause was related to equipment fatigue on one production line at our Grand Island, NE facility before it was retrofitted with new equipment in the fall of 2005. We recorded a charge of $2.7 million within cost of goods sold for our estimate of cracked concrete ties related to this issue.

While we believe this is a reasonable estimate of this potential warranty claim, this estimate could change due to new information and future events. There can be no assurance at this point that future costs pertaining to this issue will not have a material impact on our results of operations.

Also during the second quarter of 2009, the UPRR notified us that they would not accept certain prestressed concrete railroad ties produced at our Grand Island, NE facility due to questionable quality of certain raw materials. We believe this issue is isolated to below-specification raw material used in the production process received from one supplier. We brought these concrete ties back into inventory and wrote them down to our expected net realizable value. The impact of these rejected prestressed concrete railroad ties was a net unfavorable charge to gross profit of approximately $2.6 million.

During the first quarter of 2009, we purchased 86,141 shares for approximately $1.9 million pursuant to the share repurchase program authorized by the Board of Directors in 2008.

In July 2009, we sold a portion of our investments in available-for-sale marketable securities for approximately $2.1 million in proceeds and recorded a corresponding pre-tax gain of approximately $1.2 million. Our current investments in these securities have a fair value of approximately $2.0 million at December 31, 2009.

General

L.B. Foster Company is a leading manufacturer, fabricator and distributor of products and services for the rail, construction, energy and utility markets. The Company is comprised of three business segments: Rail products, Construction products and Tubular products.

The Company makes certain filings with the Securities and Exchange Commission (SEC), including its annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments and exhibits to those reports, available free of charge through its website, www.lbfoster.com, as soon as reasonably practicable after they are filed with the SEC. These filings are also available through the SEC at the SEC’s Public Reference Room at 100 F Street N.E. Washington, D.C. 20549 or by calling 1-800-SEC-0330. Also, these filings are available on the internet at www.sec.gov. The Company’s press releases are also available on its website.

Rail Products

The Rail products segment is composed of several manufacturing and distribution businesses that provide a variety of products for railroads, transit authorities, industrial companies and mining applications throughout the Americas. Rail products has sales offices throughout the United States and frequently bids on rail projects where it can offer products manufactured by the Company or sourced from numerous suppliers. These products may be provided as a package to rail lines, transit authorities and construction contractors which reduces the customer’s procurement efforts and provides value added, just in time delivery.

The Rail products segment designs and manufactures bonded insulated rail joints, cuts and drills rail and manufactures concrete cross ties and turnout ties. The Company has concrete tie manufacturing facilities in Spokane, WA, Grand Island, NE, and Tucson, AZ. The Company also has two facilities that design, test and fabricate rail products in Atlanta, GA and Niles, OH.

The Rail distribution business provides our customers with access to a variety of products including stick rail, continuous welded rail, specialty trackwork, power rail and various rail accessories. This is a highly competitive business that, once specifications are met, depends heavily on pricing. The Company maintains relationships with several rail manufacturers but procures the majority of the rail it distributes from one supplier. Rail accessories are sourced from a wide variety of suppliers.

Construction Products

The Construction products segment is composed of the following business units: piling, fabricated products, and precast concrete buildings.

The piling division, via a sales force deployed throughout the United States, markets and sells piling internationally. This division offers its customers various types and dimensions of structural beam piling, sheet piling, and pipe piling. These piling products are sourced from various suppliers. The Company is the primary distributor of domestic bearing pile and sheet piling for its primary supplier.

The fabricated products unit manufactures a number of fabricated steel and aluminum products primarily for the highway, bridge and transit industries including grid reinforced concrete deck and open steel grid flooring systems, guardrails, and expansion joints and heavy structural steel fabrications.

The precast concrete buildings unit manufactures concrete buildings for national, state and municipal parks. This unit manufactures restrooms, concession stands and other protective storage buildings available in multiple designs, textures and colors. The Company believes it is the leading high-end supplier in terms of volume, product options and capabilities. The buildings are manufactured in Spokane, WA and Hillsboro, TX.

Tubular Products

The Tubular products segment has two discrete business units: coated pipe and threaded products.

The coated pipe unit, located in Birmingham, AL, coats the outer dimension and, to a lesser extent, the inner dimension of pipe primarily for the gas transmission and, to a much lesser extent, oil transmission industries. Coated pipe partners with its primary customer, a pipe manufacturer, to market fusion bonded epoxy coatings, abrasion resistant coatings and internal linings for a wide variety of pipe dimensions for pipeline projects throughout North America.

The threaded products unit, located in Houston, TX, cuts, threads and paints pipe primarily for water well applications for the agriculture industry and municipal water authorities. Threaded products is also in the micro-pile business and threads pipe used in earth and other structural stabilization. Additionally, the threaded products unit owns a facility in Magnolia, TX that will be leased to our corporate joint venture.

Joint Venture

In May 2009, the Company completed the formation of a joint venture with L B Industries, Inc. and another party. The Company has a 45% ownership interest in the new joint venture, L B Pipe & Coupling Products, LLC, and made capital contributions of $1.4 million in 2009.

During the third quarter of 2009, the Company purchased approximately 35 acres of land in Magnolia, TX for approximately $1.1 million and built a facility that will ultimately be leased to the joint venture. The joint venture will manufacture, market and sell various products, including couplings and micropile, for the energy, utility and construction markets. The joint venture commenced operations during 2010.

Critical Accounting Policies and Estimates

The Company’s significant accounting policies are described in Note 1 to the consolidated financial statements. The accompanying consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States. When more than one accounting principle, or the method of its application, is generally accepted, management selects the principle or method that is appropriate in the Company’s specific circumstance. Application of these accounting principles requires management to make estimates that affect the reported amount of assets, liabilities, revenues, and expenses, and the related disclosure of contingent assets and liabilities. The following critical accounting policies relate to the Company’s more significant judgments and estimates used in the preparation of its consolidated financial statements. There can be no assurance that actual results will not differ from those estimates.

In June 2009, the Financial Accounting Standards Board (FASB) issued Statement of Financial Accounting Standard (SFAS) No. 168, “The FASB Accounting Standards Codification and Hierarchy of Generally Accepted Accounting Principles, a replacement of FASB Statement No. 162.” This statement modifies the Generally Accepted Accounting Principles (GAAP) hierarchy by establishing only two levels of GAAP, authoritative and nonauthoritative accounting literature. Effective July 2009, the FASB Accounting Standards Codification (ASC) is considered the single source of authoritative U.S. accounting and reporting standards, except for additional authoritative rules and interpretive releases issued by the Securities and Exchange Commission (SEC). The codification was developed to organize GAAP pronouncements by topic so that users can more easily access authoritative accounting guidance. This statement applies beginning in the 2009 third quarter. All accounting references have been updated and, therefore, SFAS references have been replaced with ASC references.

Asset impairment – The Company is required to test for asset impairment whenever events or changes in circumstances indicate that the carrying value of an asset might not be recoverable. The Company applies the guidance in FASB ASC 360-10-35, and related guidance, in order to determine whether or not an asset is impaired. This guidance indicates that if the sum of the future expected cash flows associated with an asset, undiscounted and without interest charges, is less than the carrying value, an asset impairment must be recognized in the financial statements. The amount of the impairment is the difference between the fair value of the asset and the carrying value of the asset. The Company believes that the accounting estimate related to asset impairment is a “critical accounting estimate” as it is highly susceptible to change from period to period and because it requires management to make assumptions about the existence of impairment indicators and cash flows over future years. These assumptions impact the amount of an impairment, which would have an impact on the income statement. There were no asset impairments recorded during the three years ended December 31, 2009.

Allowance for Bad Debts – The Company’s operating segments encounter risks associated with the collection of accounts receivable. As such, the Company records a monthly provision for accounts receivable that are deemed uncollectible. In order to calculate the appropriate monthly provision, the Company reviews its accounts receivable aging and calculates an allowance through application of historic reserve factors to overdue receivables. This calculation is supplemented by specific account reviews performed by the Company’s credit department. As necessary, the application of the Company’s allowance rates to specific customers is reviewed and adjusted to more accurately reflect the credit risk inherent within that customer relationship. The reserve is reviewed on a monthly basis. An account receivable is written off against the allowance when management determines it is uncollectible.

The Company believes that the accounting estimate related to the allowance for bad debts is a “critical accounting estimate” because the underlying assumptions used for the allowance can change from period to period and the allowance could potentially cause a material impact to the income statement. Specific customer circumstances and general economic conditions may vary significantly from management’s assumptions and may impact expected earnings. At December 31, 2009 and 2008, the Company maintained an allowance for bad debts of $1.1 million and $2.6 million, respectively.

Product Liability – The Company maintains a current liability for the repair or replacement of defective products. For certain manufactured products, an accrual is made on a monthly basis as a percentage of cost of sales. For long-term construction projects, a liability is established when the claim is known and quantifiable. The product liability accrual is periodically adjusted based on the identification or resolution of known individual product liability claims. The Company believes that this is a “critical accounting estimate” because the underlying assumptions used to calculate the liability can change from period to period. At December 31, 2009 and 2008, the product liability was $3.4 million and $1.6 million, respectively. For additional information regarding the Company’s product liability, refer to Part II, Item 8, Footnote 18 “Commitments and Contingent Liabilities.”

Slow-Moving Inventory – The Company maintains reserves for slow-moving inventory. These reserves, which are reviewed and adjusted routinely, take into account numerous factors such as quantities-on-hand versus turnover, product knowledge, and physical inventory observations. The Company believes this is a “critical accounting estimate” because the underlying assumptions used in calculating the reserve can change from period to period and could have a material impact on the income statement. At December 31, 2009 and 2008, the reserve for slow-moving inventory was $6.8 million and $4.2 million, respectively.

Revenue Recognition on Long-Term Contracts – Revenues from long-term contracts are recognized using the percentage of completion method based upon the proportion of actual costs incurred to estimated total costs. For certain products, the percentage of completion is based upon the ratio of actual direct labor costs to estimated total direct labor costs.

As certain contracts extend over one or more years, revisions to estimates of costs and profits are reflected in the accounting period in which the facts that require the revisions become known. Historically, the Company’s estimates of total costs and costs to complete have reasonably approximated actual costs incurred to complete contracts. At the time a loss on a contract becomes known, the entire amount of the estimated loss is recognized in the financial statements. The Company estimates the extent of progress towards completion, contract revenues and contract costs on its long-term contracts. The Company believes these estimates are “critical accounting estimates” because they require the use of judgments due to uncertainties inherent in the estimation process. As a result, actual revenues and profits could differ materially from estimates.

Pension Plans – The calculation of the Company’s net periodic benefit cost (pension expense) and benefit obligation (pension liability) associated with its defined benefit pension plans (pension plans) requires the use of a number of assumptions that the Company deems to be “critical accounting estimates”. Changes in these assumptions can result in a different pension expense and liability amounts, and future actual experience can differ significantly from the assumptions. The Company believes that the two most critical assumptions are the expected long-term rate of return on plan assets and the assumed discount rate.

The expected long-term rate of return reflects the average rate of earnings expected on funds invested or to be invested in the pension plans to provide for the benefits included in the pension liability. The Company establishes the expected long-term rate of return at the beginning of each fiscal year based upon information available to the Company at that time, including the plan’s investment mix and the forecasted rates of return on these types of securities. Any differences between actual experience and assumed experience are deferred as an unrecognized actuarial gain or loss. The unrecognized actuarial gains or losses are amortized in accordance with applicable guidance, generally FASB ASC 712, “Compensation – Nonretirement postemployment benefits.” The expected long-term rate of return determined by the Company for 2009 and 2008 was 7.75%. Pension expense increases as the expected long-term rate of return decreases.

The assumed discount rate reflects the current rate at which the pension benefits could effectively be settled. In estimating that rate, applicable guidance requires that the Company looks to rates of return on high quality, fixed income investments. The Company’s pension liability increases as the discount rate is reduced. Therefore, the decline in the assumed discount rate has the effect of increasing the Company’s pension obligation and future pension expense. The assumed discount rate used by the Company was 6.00% for 2009 and 2008.

Deferred Tax Assets – The recognition of deferred tax assets requires management to make judgments regarding the future realization of these assets. As prescribed by FASB ASC 740, “Income Taxes,” valuation allowances must be provided for those deferred tax assets for which it is more likely than not (a likelihood more than 50%) that some portion or all of the deferred tax assets will not be realized. This guidance requires management to evaluate positive and negative evidence regarding the recoverability of deferred tax assets. Determination of whether the positive evidence outweighs the negative and quantification of the valuation allowance requires management to make estimates and judgments of future financial results. The Company believes that these estimates and judgments are “critical accounting estimates”.

In July 2006, the Financial Accounting Standards Board (FASB) issued FASB Interpretation No. 48, “Accounting for Uncertainty in Income Taxes - an interpretation of FASB Statement No. 109” (FIN 48). This Interpretation applies to all open tax positions and as been codified by the FASB in ASC 740. This guidance is intended to result in increased relevance and comparability in financial reporting of income taxes and to provide more information about the uncertainty in income tax assets and liabilities.