Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended: December 27, 2009

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 1-9824

The McClatchy Company

(Exact name of registrant as specified in its charter)

| Delaware | 52-2080478 | |

| State or other jurisdiction of incorporation or organization | I.R.S. Employer Identification No. | |

| 2100 “Q” Street, Sacramento, CA | 95816 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: 916-321-1846

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Class A Common Stock, par value $.01 per share | New York Stock Exchange |

Securities registered pursuant to section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ¨ Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer x Non-accelerated filer ¨ (Do not check if a smaller reporting company) Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ¨ Yes x No

Based on the closing price of the Company’s Class A Common Stock on the New York Stock Exchange on June 28, 2009 the last day of the Company’s second fiscal quarter, the aggregate market value of the voting and non-voting common equity held by non-affiliates was approximately $28.1 million. For purposes of the foregoing calculation only, as required by Form 10-K, the Registrant has included in the shares owned by affiliates, the beneficial ownership of Common Stock of officers and directors of the Registrant and members of their families, and such inclusion shall not be construed as an admission that any such person is an affiliate for any purpose.

Shares outstanding as of February 24, 2010:

Class A Common Stock 59,778,534

Class B Common Stock 24,800,962

DOCUMENTS INCORPORATED BY REFERENCE

Definitive Proxy Statement for the Company’s May 19, 2010 Annual Meeting of Shareholders to be filed pursuant to Regulation 14A under the Securities Exchange Act of 1934 (incorporated in Part II and Part III to the extent provided in Items 10, 11, 12, 13 and 14 hereof).

Table of Contents

INDEX TO THE McCLATCHY COMPANY

2009 FORM 10-K

| Item No. |

Page | |||

| PART I | ||||

| 1. |

1 | |||

| 1A. |

7 | |||

| 1B. |

13 | |||

| 2. |

13 | |||

| 3. |

13 | |||

| 4. |

13 | |||

| PART II | ||||

| 5. |

14 | |||

| 6. |

16 | |||

| 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

17 | ||

| 7A. |

37 | |||

| 8. |

38 | |||

| 9. |

Changes In and Disagreements With Accountants on Accounting and Financial Disclosure |

71 | ||

| 9A. |

71 | |||

| 9B. |

71 | |||

| PART III | ||||

| 10. |

72 | |||

| 11. |

72 | |||

| 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

72 | ||

| 13. |

Certain Relationships and Related Transactions, and Director Independence |

73 | ||

| 14. |

73 | |||

| PART IV | ||||

| 15. |

74 | |||

Table of Contents

| ITEM 1. | BUSINESS |

Available Information

The McClatchy Company (McClatchy or the Company) maintains a website which includes an investor relations page available to all interested parties at www.mcclatchy.com. All filings with the United States Securities and Exchange Commission, along with any amendments thereto, are available free of charge on our website at www.mcclatchy.com/investor/. The Company’s corporate governance guidelines; charters for the following committees of the board of directors: audit committee, committee on the board, pension and savings plans committee, compensation and nominating committees; and the Company’s codes of business conduct and ethics and senior officers code of ethics may also be found on this website. In addition, paper copies of any such filings and corporate governance documents are available free of charge by contacting us at the address listed on the cover page of this filing. The contents of this website are not incorporated into this filing. Further, our reference to the URL for this website is intended to be an inactive textual reference only.

Overview

The Company is a hybrid print and online, news and advertising company committed to a three-pronged strategy:

| • | First, to operate high-quality newspapers in growth markets; |

| • | Second, to operate the leading local digital business in each of its daily newspaper markets, including websites, email products, podcasts, mobile services and other electronic media; and |

| • | Third, to extend these franchises by supplementing the mass reach of the newspaper with direct marketing and direct mail products so that advertisers can capture both mass and targeted audiences with one-stop shopping. |

By virtue of its strategy, the Company is the leading local media company in its premium growth markets. The Company has a century and a half of experience in mass and targeted media, with its origins in the California Gold Rush era of 1857. Originally incorporated in California as McClatchy Newspapers, Inc., the Company’s three original California newspapers—The Sacramento Bee, The Fresno Bee and The Modesto Bee—were the core of the Company until 1979 when the Company began to diversify geographically outside of California. At that time, it purchased two newspapers in the Northwest, the Anchorage Daily News and the Tri-City Herald in Southeastern Washington. In 1986, the Company purchased The (Tacoma) News Tribune and in 1987, the Company reincorporated in Delaware. The Company expanded into the Carolinas when it purchased newspapers in South Carolina in 1990 and The News and Observer Publishing Company in North Carolina in 1995. In 1998, the Company expanded into Minnesota with the acquisition of The Star Tribune Company and the combined company became The McClatchy Company.

On June 27, 2006, the Company acquired Knight-Ridder, Inc. (the Acquisition). Of the 32 daily newspapers acquired in the Acquisition, the Company subsequently sold 12 of the daily newspapers, retaining 20 daily papers in strong markets and significant digital assets. On March 5, 2007, the Company sold the (Minneapolis) Star Tribune newspaper and other publications and websites related to the newspaper. Accordingly, the Star Tribune’s results are not included in any of the Company’s discussions of continuing operations in this Report.

The Company is the third largest newspaper publisher by circulation in the United States, with 30 daily newspapers, 43 non-dailies and direct marketing and direct mail operations located in 29 markets across the country. The Company’s newspapers range from large dailies serving metropolitan areas to non-daily newspapers serving small communities. For the fiscal year 2009, the Company had an average paid daily circulation of 2,298,635 and Sunday circulation of 2,946,400. McClatchy also operates local websites in each of

1

Table of Contents

its markets which complement its newspapers and extend its audience reach. Average monthly unique visitors, a measurement of usage of the Company’s websites, totaled 34.5 million. McClatchy-owned newspapers include, among others, The Miami Herald, The Sacramento Bee, the Fort Worth Star-Telegram, The Kansas City Star, The Charlotte Observer, and The (Raleigh) News & Observer.

McClatchy also has a portfolio of premium digital assets. In addition to its local websites, which offer users information, comprehensive news, advertising, e-commerce and other services, McClatchy owns 14.4% of CareerBuilder, the nation’s largest online job site; 25.6% of Classified Ventures, a newspaper industry partnership that offers two of the nation’s premier classified websites: the auto website, cars.com, and the rental site, Apartments.com, and 33.3% of HomeFinder, LLC which operates the real estate website HomeFinder.com.

McClatchy is listed on the New York Stock Exchange under the symbol MNI.

Strategic Emphasis

The Company’s local media businesses are in a period of tremendous structural and cyclical change. The Company’s strategy of being the leading local media company in each of its markets remains sound, but these changes require the Company to focus on five major operational imperatives:

| • | Increasing advertising revenues |

| • | Expanding its digital advertising business; |

| • | Broadening its audience in its local markets; |

| • | Maintaining its commitment to public service journalism; |

| • | Restructuring its operations to reduce its cost structure. |

Increasing Advertising Revenues

Advertising revenues make up the vast majority of the Company’s revenues, making the quality of its sales function of utmost importance. Advertising revenues were approximately 78% of consolidated net revenues in fiscal 2009 and 83% in fiscal 2008. Circulation revenues approximated 19% of consolidated net revenues in fiscal 2009 and 14% in fiscal 2008.

The Company has a local sales force in each of its markets, and believes that these sales forces are generally larger than those of other local media outlets and websites in those markets. The Company’s sales forces are responsible for delivering to advertisers the broad array of its advertising products, including print, digital and direct marketing products. The Company’s advertisers range from large national retail chains to local automobile dealerships and real estate agencies to small businesses and classified advertisers. Increasingly, the Company’s emphasis has been on growing the breadth of products offered to advertisers, particularly its digital products, while expanding its relationships with smaller advertisers. To reach national advertisers, the Company’s newspapers work with national advertising representation firms and the corporate advertising department to develop relationships and make it easier for those large advertisers to place orders.

The Company is enhancing its sales efforts with the following initiatives:

| • | Offering compelling products and services; |

| • | Reallocating sales staff, particularly to online sales; |

| • | Implementing new sales incentive plans focused on online sales; |

| • | Extending sales training aimed at changing the culture and approach to selling; |

| • | Improving sub-zip zoning and other targeting capabilities to address customers’ needs for targeted advertising; and |

2

Table of Contents

| • | Partnering with technology companies and other newspaper companies. |

Expanding McClatchy’s Digital Advertising Business

The Company’s advertising revenues from digital advertising has been growing even as the Company has faced structural and cyclical change. McClatchy continues to be an industry leader in digital advertising revenue from newspaper websites as a percent of total advertising with 16.2% of advertising coming from digital products in fiscal 2009, compared to 11.6% in fiscal 2008. For all of fiscal 2009, 43.7% of the Company’s digital advertising revenues came from advertisements placed only online; that is, they were not tied to a joint print buy. Management believes this independent revenue stream bodes well for the future of the Company’s digital business and is evidence of its importance as a resource for advertisers.

The Company’s websites offer classified advertising products provided by our less than 50%-owned companies, including CareerBuilder for employment, cars.com for autos and Apartments.com in the rental category. These products generate approximately 29.4% of the Company’s digital advertising revenue for fiscal 2009.

In 2007, the Company joined a number of other newspaper companies in forming a broad-based partnership with Yahoo, Inc. (Yahoo). The Company’s local sales force is able to sell Yahoo advertising inventory and share in the revenue from the sales. In addition, the alliance allows the Company to use Yahoo’s behaviorally targeted ad-serving platform (APT platform) to sell advertising on the Company’s websites. While sales of Yahoo inventory and behaviorally targeted sales were conducted on a limited test basis in 2008, the Company began rolling out the APT platform to its newspaper websites in early 2009.

Broadening Newspaper’s Audiences in Their Local Markets

Each of the Company’s daily newspapers has the largest circulation of any newspaper serving its particular community, and coupled with a local website, reaches a broad audience in each market. The Company believes that its broad reach in each market is of primary importance in attracting advertising, the principal source of revenues for the Company.

While daily newspaper paid circulation was down 11.4% and Sunday circulation was down 8.3% in fiscal 2009 compared with fiscal 2008, a portion of the decline in print circulation reflected aggressive price increases at most newspapers and reductions by the Company to eliminate unprofitable circulation that advertisers did not value highly. In addition, the Company’s digital audience continues to show growth, with average monthly unique visitors at McClatchy newspapers’ websites in 2009 up 18.6% from 2008 to 34.5 million average monthly unique visitors.

The Audit Bureau of Circulations (ABC) now certifies audience reach where surveys are available—generally in larger markets. Based on September 2009 ABC data the Company’s newspapers deliver unduplicated reach of print and online readers of nearly 70% in its 21 measured McClatchy markets. Collectively, these 21 measured markets showed audience growth between March and September of 2009.

To remain the leading local media company and a must-buy for advertisers, McClatchy is focused on maintaining broad reach of print and online audiences in each market it serves. McClatchy will continue to refine and strengthen its print platform, but its growth increasingly comes from its digital products and the beneficial impact those products have on the total audience the Company delivers for its advertisers.

Maintaining Commitment to Public Service Journalism

The Company believes that high quality news content is the foundation of the mass reach necessary for the press to play its role in a democratic society. It is also the underpinning of the Company’s success in the marketplace. McClatchy newspapers continually receive national and regional awards among their peers for high-quality journalism.

3

Table of Contents

Today, the Company is able to deliver breaking news, as its websites compete with television and radio broadcasters for news headlines that can subsequently be expanded in its newspapers. The Company’s news organizations can provide both targeted information and in-depth coverage as needed through newspapers, websites, mobile delivery and other developing technologies.

Management believes its newspapers and websites are well equipped to discover, produce and distribute premium quality content in ways that leverage the Company’s size and tap technology to find efficiencies in newsgathering and distribution.

Restructuring McClatchy’s Operations to Reduce its Cost Structure

The ongoing structural and cyclical change in the current economy demands that the Company respond by reengineering and restructuring its operations to achieve an efficient and sustainable cost structure. Compensation expense is the largest component of the Company’s cash operating expenses (total operating expense less depreciation and amortization, noncash impairment charges and severance costs), accounting for 50.2% of cash operating expenses in fiscal 2009 and 52.2% in fiscal 2008. Technology increasingly is giving the Company the ability to operate more efficiently and reduce staff and related compensation expense. The Company looks actively for opportunities to realize efficiencies by outsourcing and/or centralizing certain functions such as production, circulation, finance, information systems, customer call centers, and advertising operations. The Company believes using technology in this way is an important component to the restructuring plans discussed in more detail below.

Cyclical economic pressures are causing the Company to ramp down its costs more quickly to meet new revenue realities. In doing so, the Company’s newspaper operations are emphasizing restructuring moves that are preferred or acceptable to our audiences and advertisers, such as reducing the width of newspapers or reducing unprofitable circulation that reaches areas outside of a newspaper’s core market. The Company is focusing its efforts on quality content production, effective sales efforts and growth in digital operations to position it for an economic recovery.

During 2008 and 2009, in order to make significant progress in achieving an efficient and sustainable cost structure, the Company announced a strategic restructuring programs which resulted in the reduction of staffing by approximately 4,200 positions, and announced the freezing of the Company’s pension plans and other cost saving measures. See further discussion in, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operation”.

Other Operational Information

Each of the Company’s newspapers is largely autonomous in its local advertising and editorial operations in order to meet most effectively the needs of the communities it serves.

The Company has two operating segments. Publishers and editors of each of the newspapers make the day-to-day decisions and report to one of two vice presidents of operations (segment managers). The segment managers are responsible for implementing the operating and financial plans at each of the newspapers within their respective operating segment. The corporate managers, including executive officers, set the basic business, accounting, financial and reporting policies.

Publishers also work together to consolidate functions and share resources regionally and across the Company in operational areas that lend themselves to such efficiencies, such as certain regional or national sales efforts, accounting functions, online publishing systems and products, information technology functions and others. A corporate advertising department was formed in 2008 and is headed by a vice president of advertising who works with the Company’s largest advertisers in placing advertising across the Company in newspapers and online websites. These efforts are often coordinated through the segment managers and corporate personnel.

4

Table of Contents

The Company’s newspaper business is somewhat seasonal, with peak revenues and profits generally occurring in the second and fourth quarters of each year reflecting the spring and Thanksgiving and Christmas holidays, respectively. The first quarter, when holidays are not prevalent, is historically the slowest quarter for revenues and profits.

The following table summarizes the circulation of each of the Company’s daily newspapers. These circulation figures are reported on the Company’s fiscal year basis and are not meant to reflect Audit Bureau of Circulations (ABC) reported figures.

| 2009 |

2008 | |||||||

| Circulation by Newspaper |

Daily |

Sunday |

Daily |

Sunday | ||||

| The Sacramento Bee |

226,329 | 272,738 | 259,223 | 300,510 | ||||

| The Kansas City (Missouri) Star |

222,415 | 316,390 | 243,488 | 332,004 | ||||

| Charlotte Observer |

175,565 | 231,243 | 199,956 | 253,393 | ||||

| (Fort Worth) Star-Telegram |

174,991 | 259,011 | 197,672 | 283,914 | ||||

| The Miami Herald |

167,998 | 245,849 | 221,736 | 285,246 | ||||

| The (Raleigh) News & Observer |

144,356 | 194,924 | 162,224 | 207,080 | ||||

| The Fresno Bee |

129,542 | 153,251 | 142,518 | 167,184 | ||||

| Lexington Herald-Leader |

101,229 | 117,219 | 104,140 | 127,424 | ||||

| The (Tacoma) News Tribune |

91,545 | 104,974 | 106,441 | 120,897 | ||||

| The (Columbia, SC) State |

87,633 | 111,587 | 97,964 | 125,149 | ||||

| The Wichita Eagle |

76,024 | 116,944 | 80,879 | 125,506 | ||||

| The Modesto Bee |

68,102 | 74,903 | 75,390 | 79,430 | ||||

| El Nuevo Herald |

61,261 | 81,634 | 78,255 | 86,733 | ||||

| Idaho Statesman (Boise) |

53,913 | 73,121 | 59,566 | 77,263 | ||||

| Anchorage Daily News |

51,749 | 57,641 | 61,520 | 68,732 | ||||

| Belleville (Illinois) News-Democrat |

50,167 | 57,127 | 50,840 | 59,465 | ||||

| The (Macon, GA) Telegraph |

49,133 | 64,578 | 54,132 | 68,649 | ||||

| The (Myrtle Beach, SC) Sun News |

42,892 | 54,889 | 47,931 | 59,304 | ||||

| (Biloxi) Sun Herald |

39,665 | 45,032 | 42,189 | 47,393 | ||||

| The Bradenton (Florida) Herald |

39,134 | 45,925 | 42,620 | 48,547 | ||||

| Tri-City (Washington) Herald |

37,073 | 39,961 | 39,912 | 42,161 | ||||

| (Columbus, GA) Ledger-Enquirer |

35,483 | 43,933 | 39,749 | 47,738 | ||||

| The (San Luis Obispo, CA) Tribune |

34,579 | 39,717 | 35,891 | 41,290 | ||||

| The Olympian (Washington) |

27,530 | 33,271 | 30,313 | 37,237 | ||||

| The (Rock Hill, SC) Herald |

24,993 | 27,947 | 28,242 | 30,510 | ||||

| (Pennsylvania) Centre Daily Times |

22,024 | 28,352 | 23,274 | 30,291 | ||||

| The Bellingham (Washington) Herald |

19,496 | 24,342 | 21,702 | 27,175 | ||||

| The Island Packet (Hilton Head, SC) |

18,417 | 19,724 | 18,489 | 19,716 | ||||

| Merced (California) Sun-Star |

14,702 | — | 15,618 | — | ||||

| The Beaufort (South Carolina) Gazette |

10,694 | 10,171 | 11,701 | 10,915 | ||||

The Company’s newspapers are generally delivered by independent contractors, and subscription revenues are recorded net of direct delivery costs.

Other Operations

The Company owns 14.4% of Career Builder, the nation’s largest online job site, 25.6% of Classified Ventures, a newspaper industry partnership that offers classified websites such as cars.com and apartments.com. The Company owns one-third of HomeFinder, LLC which operates the real estate website HomeFinder.com. The Company also owns a 15.0% interest in TKG Internet Holdings, which owns 75.0% of Topix.net (Topix), a general interest website focused on local communities, for an effective ownership of 11.3%.

5

Table of Contents

McClatchy Tribune Information Service (MCT), a joint venture of McClatchy and Tribune Company (Tribune), offers stories, graphics, illustrations, photos and paginated pages for print publishers and web-ready content for online publishers. All the Company’s newspapers, Washington D.C. staff and foreign bureaus produce MCT editorial material. Content is also supplied by Tribune newspapers and a number of other newspapers.

The Company owns 49.5% of the voting stock and 70.6% of the nonvoting stock of The Seattle Times Company. The Seattle Times Company owns The Seattle Times newspaper and weekly newspapers in Puget Sound and daily newspapers located in Walla Walla and Yakima, Washington.

In addition, the Company owns a 27.0% interest in Ponderay Newsprint Company (Ponderay), a general partnership, which owns and operates a newsprint mill in the State of Washington. The Company is required to purchase up to 56,800 metric tons of newsprint annually from Ponderay on a “take-if-tendered” basis at prevailing market prices, until Ponderay’s debt is repaid.

The Company and affiliates of Cox Enterprises, Inc. and Media General Inc. each owned a 33.3% interest in SP Newsprint Co. (SP), a newsprint manufacturing company in North America that was sold in 2008. See Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operation” below for an expanded discussion of this transaction. The Company has an annual purchase commitment for up to 149,160 metric tons of newsprint from SP.

The Company uses the equity method of accounting for a majority of its investments in unconsolidated companies.

Raw Materials

During fiscal 2009, the Company consumed approximately 218,000 metric tons of newsprint compared to 314,000 metric tons in fiscal 2008 for its continuing operations. The decrease in tons consumed was primarily due to lower advertising sales and circulation volumes, and to conversion to lighter weight newsprint and reduction of web widths at certain newspapers. The Company currently obtains a majority of its supply of newsprint from Ponderay and SP, as well as a number of other suppliers, and primarily under long term contracts.

The Company’s earnings are sensitive to changes in newsprint prices. Newsprint expense accounted for 10.7% of total operating expenses in fiscal 2009 and 12.7% in fiscal 2008 (excluding masthead impairment from total expenses in 2008). However, because the Company has an ownership interest in Ponderay, an increase in newsprint prices, while negatively affecting the Company’s operating expenses, would increase the earnings from its share of this investment partially offsetting the increase in the Company’s newsprint expense. A decline in newsprint prices would have the opposite effect. Ponderay is also impacted by fluctuations in the cost of energy and fiber used in the papermaking process. The Company estimates that it will use approximately 180,000 metric tons of newsprint in fiscal 2010, depending on the level of print advertising, circulation volumes and other business considerations.

The Company purchased 200,832 metric tons of newsprint from Ponderay and SP in 2009. See the discussion above; Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operation”; and the financial statements and accompanying notes for further discussion of the impact of these investments on the Company’s business.

McClatchy fully supports recycling efforts. In 2009, 99.4% of the newsprint used by McClatchy newspapers was made up of some recycled fiber; the average content was 76.1% recycled fiber. This translates into an overall recycled newsprint average of 75.1%. During 2009, all of McClatchy’s newspapers collected and recycled press waste, newspaper returns and printing plates.

6

Table of Contents

Competition

The Company’s newspapers, direct marketing programs and internet sites compete for advertising revenues and readers’ time with television, radio, other internet sites, direct mail companies, free shoppers, suburban neighborhood and national newspapers and other publications, and billboard companies, among others. In some of its markets, the Company’s newspapers also compete with other newspapers published in nearby cities and towns. Competition for advertising is generally based upon circulation levels, readership demographics, price, internet usage and advertiser results, while competition for circulation and readership is generally based upon the content, journalistic quality, service and the price of the newspaper.

The Company’s major daily newspapers are the primary general circulation newspaper in each of their respective markets and lead their local newspaper competitors in both advertising linage and general circulation and readership. Its newspaper internet sites are generally the leading local sites in each of the Company’s major daily newspaper markets, based upon research conducted by the Company and various independent sources.

Nonetheless, the Company has noted changes in readership trends, including a shift of readers to the internet and mobile devices, and has experienced greater shift of advertising in the classified categories to online advertising. The Company faces greater competition, particularly in the areas of employment, automotive and real estate advertising, by online competitors. To address the structural shift to digital media, the Company’s newspapers provide editorial content on a wide variety of platforms and formats—from its daily newspaper to leading local websites; on social network sites such as Facebook and Twitter; on smart phones and on eReaders; on blogs and in niche publications and websites; in e-mail newsletters and RSS feeds. In addition its websites offer leading digital classified products such as CareerBuilder, cars.com and Apartments.com and the Company continues to expand it partnerships with technology companies such as its affiliation with Yahoo on retail efforts.

Employees—Labor

As of December 27, 2009, the Company had approximately 9,600 full and part-time employees (equating to approximately 8,590 full-time equivalent employees), of whom approximately 5.9% were represented by unions. Most of the Company’s union-represented employees are currently working under labor agreements expiring in various years through 2012. Twenty of the Company’s 30 daily papers have no unions.

While the Company’s newspapers have not had a strike for decades and do not currently anticipate a strike occurring, the Company cannot preclude the possibility that a strike may occur at one or more of its newspapers when future negotiations occur. The Company believes that, in the event of a newspaper strike, it would be able to continue to publish and deliver to subscribers, a capability which is critical to retaining revenues from advertising and circulation, although there can be no assurance of this.

Compliance with Environmental Laws

The Company uses appropriate waste disposal techniques for items such as ink and other toxic fluids. The Company has a $1 million letter of credit shared among various state environmental agencies and the US Environmental Protection Agency to provide collateral related to existing or previously disposed oil drums, but the Company does not have any significant environmental issues and has no significant expenses or capital expenditures related to environmental control facilities.

| ITEM 1A. | RISK FACTORS |

Forward-Looking Information:

This report on Form 10-K contains forward-looking statements regarding the Company’s actual and expected financial performance and operations. These statements are based upon our current expectations and knowledge of factors impacting our business, including, without limitation, statements about our ability to

7

Table of Contents

consummate contemplated sales transactions for our assets or investments which may enable debt reduction on anticipated terms, our customers and the markets in which we operate, advertising revenues, the effect of revenues on the fair value of our reporting units, our impairment analyses and our evaluation of the factors pertinent thereto, the economy, our pension plans, including our assumptions regarding return on pension plan assets and assumed discount rates, newsprint costs, our restructuring plans, including projected costs and savings, amortization expense, stock option expenses, prepayment of debt, capital expenditures, litigation, sufficiency of capital resources, possible acquisitions and investments, and our future financial performance. Such statements are subject to risks, trends and uncertainties. Forward-looking statements are generally preceded by, followed by or are a part of sentences that include the words “believes,” “expects,” “anticipates,” “estimates,” or similar expressions. For all of those statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. You should understand that the following important factors, in addition to those discussed elsewhere in this document, particularly in the section entitled “Risk Factors” and in the documents which we incorporate by reference, could affect the future results of McClatchy and could cause those future results to differ materially from those expressed in our forward-looking statements: the duration and depth of the economic recession; McClatchy might not generate cash from operations, or otherwise, necessary to reduce debt or meet debt covenants as expected; McClatchy might not consummate contemplated transactions to enable debt reduction on anticipated terms or at all; McClatchy might not achieve its expense reduction targets or might do harm to its operations in attempting to achieve such targets; McClatchy’s operations have been, and will likely continue to be, adversely affected by competition, including competition from internet publishing and advertising platforms; increases in the cost of newsprint; bankruptcies or financial strain of its major advertising customers; litigation or any potential litigation; geo-political uncertainties including the risk of war; changes in printing and distribution costs from anticipated levels; changes in interest rates; changes in pension assets and liabilities; increased consolidation among major retailers in our markets or other events depressing the level of advertising; our inability to negotiate and obtain favorable terms under collective bargaining agreements with unions; competitive action by other companies; decreased circulation and diminished revenues from retail, classified and national advertising; and other factors, many of which are beyond our control.

The Company has significant competition in the market for news and advertising, which may reduce its advertising and circulation revenues in the future.

The Company’s primary source of revenues is advertising, followed by circulation. In recent years, the advertising industry generally has experienced a secular shift toward internet advertising and away from other traditional media. In addition, the Company’s circulation has declined over the last two years, reflecting general trends in the newspaper industry including consumer migration toward the internet and other media for news and information. With the continued development of alternative forms of media technologies, the Company faces increasing competition from other online sources for both advertising and circulation revenues. This competition has intensified as a result of the continued developments of digital media technologies. Distribution of news, entertainment and other information over the internet, as well as through mobile phones and other devices, continues to increase in popularity. These technological developments are increasing the number of media choices available to advertisers and audiences. As media audiences fragment, the Company expects advertisers to allocate larger portions of their advertising budgets to digital media. This increased competition has had and is expected to continue to have an adverse effect on the Company’s business and financial results, including negatively impacting revenues and operating income.

Weak general economic and business conditions subject the Company to risks of declines in advertising revenues.

The United States economy is undergoing an extended period of economic uncertainty, which has caused, among other things, a general tightening in the credit markets, limited access to the credit markets, lower levels of liquidity, increases in the rates of default and bankruptcy, lower consumer and business spending, and lower consumer net worth. The resulting pressure on the labor and retail markets and the downturn in consumer

8

Table of Contents

confidence have weakened the economic climate in all of the markets in which the Company does business and have had and are expected to continue to have an adverse effect on the Company’s advertising revenues. Classified advertising revenues have continued to decline since late 2006 and advertising results declined across the board in 2008 and 2009. To the extent these economic conditions continue or worsen, the Company’s business and advertising revenues will be adversely affected, which could negatively impact the Company’s operations and cash flows and the Company’s ability to meet the covenants in its senior secured credit agreement. In addition, seasonal variations in consumer spending cause our quarterly advertising revenues to fluctuate. Second and fourth quarter advertising revenues are typically higher than first and third quarter advertising revenues, reflecting the slower economic activity in the winter and summer and the stronger fourth quarter holiday season. If general economic conditions and other factors cause a decline in revenues, particularly during the second or fourth quarters, we may not be able to grow or maintain our revenues for the year which would have an adverse effect on the Company’s business and financial results.

If management is unable to execute cost-control measures successfully, total operating costs may be greater than expected, which may adversely affect the Company’s profitability.

Given general economic and business conditions and the Company’s recent operating results, the Company has taken steps to lower operating costs by reducing workforce and implementing general cost-control measures. If the Company does not achieve its expected savings from these initiatives, or if operating costs increase as a result of these initiatives, total operating costs may be greater than anticipated. Although management believes that appropriate steps have been taken and are being taken to implement cost-control efforts, such efforts may affect the Company’s business and its ability to generate future revenue. Significant portions of the Company’s expenses are fixed costs that neither increase nor decrease proportionately with revenues. As a result, management is limited in its ability to reduce costs in the short term. If these cost-control efforts do not reduce costs sufficiently, income from continuing operations may continue to decline.

The collectability of accounts receivable under current adverse economic conditions could deteriorate to a greater extent than provided for in the Company’s financial statements.

Recessionary conditions in the U.S have increased the Company’s exposure to losses resulting from the potential bankruptcy of the Company’s advertising customers. The recession could also impair the ability of those with whom the Company does business to satisfy their obligations to the Company even if they do not file for bankruptcy. As a result, the Company’s results of operations may continue to be adversely affected. The Company’s accounts receivables are stated at net estimated realizable value and the Company’s allowance for doubtful accounts has been determined based on several factors, including the aging of accounts receivables and evaluation of significant individual credit risk accounts. If such collectability estimates prove inaccurate, adjustments to future operating results could occur.

The economic downturn and the decline in the price of the Company’s publicly traded stock may result in goodwill and masthead impairment charges.

The Company recorded masthead impairment charges of $59.6 million in 2008 and $3.0 billion of goodwill and masthead impairment charges in 2007 reflecting the economic downturn and the decline in the price of the Company’s publicly traded common stock. Should general economic, market or business conditions continue to decline, and continue to have a negative impact on the Company’s stock price, the Company may be required to record additional impairment charges.

The Company has $1.9 billion in total consolidated debt, which subjects the Company to significant interest rate and credit risk.

As of December 27, 2009, the Company had approximately $1.9 billion in total principal indebtedness outstanding. This level of debt increases the Company’s vulnerability to general adverse economic and industry

9

Table of Contents

conditions. Debt service costs are subject to interest rate changes as well as any changes in the Company’s leverage ratio (ratio of debt to operating cash flow as defined in the Company’s existing senior secured credit agreement with its banks). Higher leverage ratios could increase the level of debt service costs and also affect the Company’s future ability to refinance maturing debt, or the ultimate structure of such refinancing. In addition, the Company’s credit ratings could affect its ability to refinance its debt. On February 11, 2010, Standard & Poor’s upgraded its corporate credit rating on the Company to ‘B-’ from ‘CC’, with a stable rating outlook, and the ratings on the Company’s bonds and senior secured credit facility were upgraded from ‘C’ to ‘B-’ (including the Company’s 11.5% Senior Secured Notes due 2017). On February 11, 2010, Moody’s upgraded its corporate credit rating on the Company to ‘Caa1’ from ‘Caa2’, with a stable rating outlook, and the ratings on the Company’s unsecured bonds were upgraded from ‘Caa3’ to ‘Caa2’ and Moody’s issued a “B1” rating on the Company’s 11.5% Senior Secured Notes due 2017 and senior secured credit facility.

Covenants in the indenture governing the Company’s 11.50% Senior Secured Notes due 2017 (the “2017 Notes”) and its senior secured credit facility will restrict the Company’s operations in many ways.

The indenture governing the 2017 Notes and the senior secured credit facility contain various covenants that limit, subject to certain exceptions, our ability and/or our restricted subsidiaries’ ability to, among other things:

| • | incur liens or additional debt or provide guarantees; |

| • | issue redeemable stock and preferred stock; |

| • | pay dividends or make distributions on capital stock or repurchase capital stock or repurchase outstanding notes or debentures prior to their stated maturity; |

| • | make loans, investments or acquisitions; |

| • | enter into agreements that restrict distributions from its subsidiaries; |

| • | create or permit restrictions on the ability of its subsidiaries to pay dividends or distributions or guarantee debt or create liens; |

| • | sell assets and capital stock of its subsidiaries; |

| • | enter into certain transactions with its affiliates; and dissolve, liquidate, consolidate or merge with or into, or sell substantially all its assets to another person. |

The restrictions contained in the indenture for the 2017 Notes and the senior secured credit facility could adversely affect the Company’s ability to:

| • | finance its operations; |

| • | make needed capital expenditures; |

| • | make strategic acquisitions or investments or enter into alliances; |

| • | withstand a future downturn in its business or the economy in general; |

| • | engage in business activities, including future opportunities, that may be in its interest; and |

| • | plan for or react to market conditions or otherwise execute our business strategies. |

The Company’s ability to comply with covenants contained in the indenture for the 2017 Notes and the senior secured credit facility may be affected by events beyond its control, including prevailing economic, financial and industry conditions. Even if the Company is able to comply with all of the applicable covenants, the restrictions on its ability to manage its business could adversely affect its business by, among other things, limiting its ability to take advantage of financings, mergers, acquisitions and other corporate opportunities that the Company believes would be beneficial to it.

10

Table of Contents

Potential disruptions in the credit markets could adversely affect the availability and cost of short-term funds for liquidity requirements, and could adversely affect the Company’s access to capital or to obtain financing at reasonable rates and its ability to refinance existing debt at reasonable rates or at all.

If internal funds are not available from the Company’s operations, the Company may be required to rely on the banking and credit markets to meet its financial commitments and short-term liquidity needs. Disruptions in the capital and credit markets, as were experienced during 2008 and 2009, could adversely affect the Company’s ability to access additional funds in the capital markets or draw on its senior secured credit facility. Although the Company believes that its operating cash flow and current access to capital and credit markets, including the proceeds from its recent notes offering and funds from its senior secured credit facility, will give it the ability to meet its financial needs for the foreseeable future, there can be no assurance that continued or increased volatility and disruption in the capital and credit markets will not impair the Company’s liquidity. If this should happen, any alternative credit arrangements may not be put in place without a potentially significant increase in the Company’s cost of borrowing.

As of December 27, 2009, on an as adjusted basis after giving effect to the refinancing discussed in Item 7, the Company would have had approximately $2.0 billion in total principal indebtedness, $875 million of which would have consisted of the notes that were issued on February 4, 2010 and $262.0 million of which would have consisted of borrowings under its senior secured credit facility with the remainder in the form of unsecured publicly traded notes maturing in part in 2011, 2014, 2017, 2027 and 2029. While cash flow should permit the Company to lower the amount of this debt before it matures, a significant portion of this debt will probably need to be refinanced in the future. Access to the capital markets for longer-term financing is currently restricted due to the unprecedented and ongoing turmoil in the capital markets.

The Company requires newsprint for operations and, therefore, its operating results may be adversely affected if the price of newsprint increases.

Newsprint is the major component of the Company’s cost of raw materials. Newsprint accounted for 10.7% of McClatchy’s operating expenses for fiscal 2009. Accordingly, earnings are sensitive to changes in newsprint prices. The price of newsprint has historically been volatile and may increase as a result of various factors, including:

| • | declining newsprint supply from mill closures; |

| • | reduction in newsprint suppliers because of consolidation in the newsprint industry; |

| • | paper mills reducing their newsprint supply because of switching their production to other paper grades; and |

| • | a decline in the financial situation of newsprint suppliers. |

The Company has not attempted to hedge fluctuations in the normal purchases of newsprint or enter into contracts with embedded derivatives for the purchase of newsprint. If the price of newsprint increases materially, operating results could be adversely affected. If newsprint suppliers experience labor unrest, transportation difficulties or other supply disruptions, the Company’s ability to produce and deliver newspapers could be impaired and/or the cost of the newsprint could increase, both of which would negatively affect its operating results.

A portion of the Company’s employees are members of unions and if the Company experiences labor unrest, its ability to produce and deliver newspapers could be impaired.

If McClatchy experiences labor unrest, its ability to produce and deliver newspapers could be impaired in some locations. The results of future labor negotiations could harm the Company’s operating results. The Company’s newspapers have not endured a labor strike for decades. However, management cannot ensure that a

11

Table of Contents

strike will not occur at one or more of the Company’s newspapers in the future. As of December 27, 2009, approximately 5.9% of full-time and part-time employees were represented by unions. Most of the Company’s union-represented employees are currently working under labor agreements, which expire at various times through 2012. McClatchy faces collective bargaining upon the expirations of these labor agreements. Even if its newspapers do not suffer a labor strike, the Company’s operating results could be harmed if the results of labor negotiations restrict its ability to maximize the efficiency of its newspaper operations.

Under the Pension Protection Act (PPA), the Company will be required to make greater cash contributions to its defined benefit pension plans in the next several years than previously required, placing greater liquidity needs upon its operations.

The poor capital markets of 2008 that have affected all investments impacted the funds in the Company’s pension plans which had poor returns in 2008. However, strong returns in 2009 helped offset a portion of this impact, but, as a result of the plans’ lower assets, the projected benefit obligations of the Company’s qualified pension plans exceed plan assets by $500.0 million as of December 27, 2009. The excess of benefit obligations over pension assets is expected to give rise to an increase in required pension contributions over the next several years. The PPA funding rules are likely to require the net liability at the end of 2009 to be funded with tax deductible contributions between 2010 and 2015, with approximately $22.0 million coming due in 2010. Contributions in future years, while not yet known, are expected to be substantially higher than the 2010 amounts. While legislation has recently been enacted to give some relief in funding and there may be more related legislation, the contributions will place additional strain on the Company’s liquidity needs.

The Company has invested in certain internet ventures, but such ventures may not be as successful as expected which could adversely affect the results of operations of the Company.

The Company continues to evaluate its business and make strategic investments in digital ventures, either alone or with partners, to further its growth in its online businesses. There can be no assurances that these investments or partnerships will result in growth in advertising or will produce equity income or capital gains in future years.

If the Company is not successful in growing its digital businesses, its business, financial condition and prospects will be adversely affected.

The Company’s future growth depends to a significant degree upon the development of its digital businesses. The growth and success of its digital businesses over the long term depends on various factors, including, among other things the ability to:

| • | continue to increase online audiences; |

| • | attract advertisers to its Web sites; |

| • | maintain or increase the advertising rates on its Web sites; |

| • | exploit new and existing technologies to distinguish its products and services from those of its competitors and developing new content, products and services; and |

| • | invest funds and resources in online opportunities. |

If the Company is not successful in growing its digital businesses, its business, financial condition and prospects will be adversely affected.

12

Table of Contents

Circulation declines could adversely affect the Company’s circulation and advertising revenues.

Advertising and circulation revenues are affected by circulation and readership levels of the Company’s newspapers. In recent years, newspapers have experienced difficulty maintaining or increasing print circulation levels because of a number of factors, including:

| • | increased competition from other publications and other forms of media technologies available in various markets, including the internet and other new media formats that are often free for users; |

| • | continued fragmentation of media audiences; |

| • | a growing preference among some consumers to receive all or a portion of their news other than from a newspaper; |

| • | increases in subscription and newsstand rates; and |

| • | declining discretionary spending by consumers affected by negative economic conditions. |

These factors could also affect the Company’s newspapers’ ability to institute circulation price increases for print products. A prolonged reduction in circulation would have a material adverse effect on advertising revenues. To maintain the Company’s circulation base, it may be required to incur additional costs which it may not be able to recover through circulation and advertising revenues.

Adverse results from litigation or governmental investigations can impact the Company’s business practices and operating results.

From time to time, the Company and its subsidiaries are parties to litigation and regulatory, environmental and other proceedings with governmental authorities and administrative agencies. Adverse outcomes in lawsuits or investigations could result in significant monetary damages or injunctive relief that could adversely affect our operating results or financial condition as well as our ability to conduct our businesses as they are presently being conducted.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

| ITEM 2. | PROPERTIES |

The corporate headquarters of the Company are located at 2100 “Q” Street, Sacramento, California. At December 27, 2009, the Company had newspaper production facilities in 29 markets situated in 15 states. The Company’s facilities vary in size and in total occupy about 7.9 million square feet. Approximately 1.3 million of the total square footage is leased from others, while the remaining square footage is property owned by the Company. The Company owns substantially all of its production equipment, although certain office equipment is leased.

The Company maintains its properties in good condition and believes that its current facilities are adequate to meet the present needs of its newspapers.

| ITEM 3. | LEGAL PROCEEDINGS |

The Company becomes involved from time to time in claims and lawsuits incidental to the ordinary course of its business, including such matters as libel, invasion of privacy, intellectual property infringement, wrongful termination actions, and complaints alleging discrimination. In addition, the Company is involved from time to time in governmental and administrative proceedings concerning employment, labor, environmental and other claims. Historically, such claims and proceedings have not had a material adverse effect upon the Company’s consolidated results of operations or financial condition.

| ITEM 4. | RESERVED |

13

Table of Contents

| ITEM 5. | MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information: The Company’s Class A Common Stock is listed on the New York Stock Exchange (NYSE symbol—MNI). A small amount of Class A Common Stock is also traded on other exchanges. The Company’s Class B Stock is not publicly traded. The following table lists per share dividends paid on both classes of Common Stock and the high and low prices of the Company’s Class A Common Stock as reported by the NYSE for each fiscal quarter of 2009 and 2008:

| HIGH |

LOW |

DIVIDENDS | |||||||

| Year Ended December 27, 2009: |

|||||||||

| First quarter |

$ | 1.87 | $ | 0.35 | $ | 0.09 | |||

| Second quarter |

$ | 1.33 | $ | 0.46 | $ | 0.00 | |||

| Third quarter |

$ | 2.88 | $ | 0.39 | $ | 0.00 | |||

| Fourth quarter |

$ | 4.04 | $ | 2.13 | $ | 0.00 | |||

| Year Ended December 28, 2008: |

|||||||||

| First quarter |

$ | 12.83 | $ | 8.33 | $ | 0.18 | |||

| Second quarter |

$ | 11.21 | $ | 6.86 | $ | 0.18 | |||

| Third quarter |

$ | 7.11 | $ | 2.57 | $ | 0.09 | |||

| Fourth quarter |

$ | 4.85 | $ | 0.62 | $ | 0.09 | |||

Holders:

The number of record holders of Class A and Class B Common Stock at February 24, 2010 was 5,800 and 23, respectively.

Dividends:

The payment and amount of future dividends remain within the discretion of the Board of Directors and will depend upon the Company’s future earnings, financial condition and requirements, and other factors considered relevant by the Board. The Company suspended its dividend after the payment of the first quarter dividend in fiscal 2009. Also, the Company is restricted by its senior secured credit agreement from paying dividends after June 28, 2009 when its leverage is greater than three times its earnings before interest, taxes, depreciation and amortization (EBITDA) as defined in the agreement.

Sales of Unregistered Securities:

None

Purchases of Equity Securities:

None

14

Table of Contents

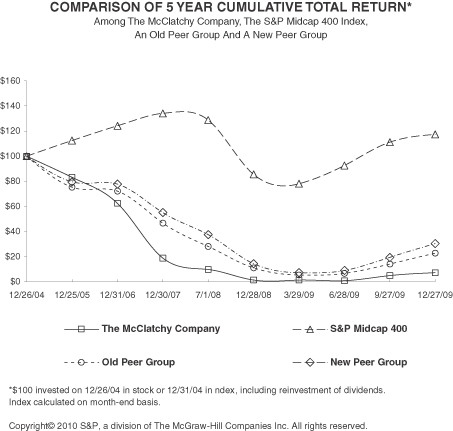

The following graph compares the cumulative 5-year total return attained by shareholders on The McClatchy Company’s common stock versus the cumulative total returns of the S&P Midcap 400 index, and a customized peer group composed of nine companies. The Company selected its peer group based on the fact that McClatchy is a pure-play newspaper publishing and online media company with no other media business beyond its newspaper and online business. The Company added the E W Scripps Company (Scripps) to its peer group in 2009 because Scripps spun off certain non-newspaper operations in mid 2008 and as a result, a majority of its revenues now come from newspaper publishing, making it comparable to the Company. In addition, the Journal Register Company ceased to be publicly traded and accordingly, was deleted from the Company’s peer group in 2009.

| 12/26/04 |

12/25/05 |

12/31/06 |

12/30/07 |

7/1/08 |

12/28/08 |

3/29/09 |

6/28/09 |

9/27/09 |

12/27/09 | |||||||||||

| The McClatchy Company |

100.00 | 83.20 | 62.71 | 18.94 | 9.85 | 1.35 | 1.40 | 0.94 | 5.03 | 7.21 | ||||||||||

| S&P Midcap 400 |

100.00 | 112.55 | 124.17 | 134.08 | 128.84 | 85.50 | 78.10 | 92.74 | 111.27 | 117.46 | ||||||||||

| Old Peer Group |

100.00 | 75.40 | 72.26 | 46.92 | 28.17 | 11.05 | 5.45 | 6.72 | 14.29 | 22.78 | ||||||||||

| New Peer Group |

100.00 | 79.58 | 77.83 | 55.11 | 37.68 | 14.48 | 7.28 | 9.07 | 19.61 | 30.44 |

The stock price performance included in this graph is not necessarily indicative of future stock price performance.

The Company’s current customized peer group includes nine companies which are publicly traded with a majority of their revenues from newspaper publishing. This peer group includes: A H Belo Corp., E W Scripps Company, Gannett Inc., Gatehouse Media Inc., Journal Communications Inc., Lee Enterprises Inc., Media General Inc., New York Times Company and Sun-Times Media Group Inc.

15

Table of Contents

| ITEM 6. | SELECTED FINANCIAL DATA |

The following selected financial data should be read in conjunction with the Consolidated Financial Statements and related notes, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and other financial information appearing elsewhere in this Annual Report on Form 10-K. The information set forth below is not necessarily indicative of the Company’s future financial condition or results of operations.

SELECTED FINANCIAL DATA (1)(2)

(in thousands, except per share amounts)

| December 27, 2009 |

December 28, 2008 |

December 30, 2007 (1) |

December 31, 2006 (2) |

December 25, 2005 | |||||||||||||||

| REVENUES—NET: |

|||||||||||||||||||

| Advertising |

$ | 1,143,129 | $ | 1,568,766 | $ | 1,911,722 | $ | 1,432,913 | $ | 691,790 | |||||||||

| Circulation |

278,256 | 265,584 | 275,658 | 194,940 | 97,205 | ||||||||||||||

| Other |

50,199 | 66,106 | 72,983 | 47,337 | 18,485 | ||||||||||||||

| 1,471,584 | 1,900,456 | 2,260,363 | 1,675,190 | 807,480 | |||||||||||||||

| OPERATING EXPENSES: |

|||||||||||||||||||

| Depreciation and amortization |

142,889 | 142,948 | 148,559 | 98,865 | 39,311 | ||||||||||||||

| Other operating expenses |

1,130,183 | 1,536,343 | 1,685,710 | 1,229,417 | 576,866 | ||||||||||||||

| Goodwill and masthead impairment |

— | 59,563 | 2,992,046 | — | — | ||||||||||||||

| 1,273,072 | 1,738,854 | 4,826,315 | 1,328,282 | 616,177 | |||||||||||||||

| OPERATING INCOME (LOSS) |

198,512 | 161,602 | (2,565,952 | ) | 346,908 | 191,303 | |||||||||||||

| NON-OPERATING (EXPENSES) INCOME: |

|||||||||||||||||||

| Interest expense |

(127,276 | ) | (157,385 | ) | (197,997 | ) | (93,664 | ) | — | ||||||||||

| Interest income |

47 | 1,429 | 243 | 3,562 | 47 | ||||||||||||||

| Equity income (loss) in unconsolidated companies—net |

2,130 | (14,021 | ) | (36,899 | ) | 4,951 | 635 | ||||||||||||

| Write-down of investments and land held for sale |

(28,322 | ) | (26,462 | ) | (84,568 | ) | — | — | |||||||||||

| Gain on non-operating items and other—net |

44,320 | 56,922 | 1,982 | 9,128 | 231 | ||||||||||||||

| (109,101 | ) | (139,517 | ) | (317,239 | ) | (76,023 | ) | 913 | |||||||||||

| INCOME (LOSS) FROM CONTINUING OPERATIONS BEFORE INCOME TAXES |

89,411 | 22,085 | (2,883,191 | ) | 270,885 | 192,216 | |||||||||||||

| INCOME TAX PROVISION (BENEFIT) |

29,147 | 19,278 | (156,582 | ) | 87,390 | 72,701 | |||||||||||||

| INCOME (LOSS) FROM CONTINUING OPERATIONS |

60,264 | 2,807 | (2,726,609 | ) | 183,495 | 119,515 | |||||||||||||

| INCOME (LOSS) FROM DISCONTINUED OPERATIONS, NET OF INCOME TAXES |

(6,174 | ) | (6,758 | ) | (9,404 | ) | (339,072 | ) | 41,004 | ||||||||||

| NET INCOME (LOSS) |

$ | 54,090 | $ | (3,951 | ) | $ | (2,736,013 | ) | $ | (155,577 | ) | $ | 160,519 | ||||||

| NET INCOME (LOSS) PER COMMON SHARE: |

|||||||||||||||||||

| Basic: |

|||||||||||||||||||

| Income (loss) from continuing operations |

$ | 0.72 | $ | 0.03 | $ | (33.26 | ) | $ | 2.85 | $ | 2.56 | ||||||||

| Income (loss) from discontinued operations |

(0.07 | ) | (0.08 | ) | (0.11 | ) | (5.27 | ) | 0.88 | ||||||||||

| Net income (loss) per share |

$ | 0.65 | $ | (0.05 | ) | $ | (33.37 | ) | $ | (2.42 | ) | $ | 3.44 | ||||||

| Diluted: |

|||||||||||||||||||

| Income (loss) from continuing operations |

$ | 0.72 | $ | 0.03 | $ | (33.26 | ) | $ | 2.84 | $ | 2.55 | ||||||||

| Income (loss) from discontinued operations |

(0.07 | ) | (0.08 | ) | (0.11 | ) | (5.25 | ) | 0.87 | ||||||||||

| Net income (loss) per share |

$ | 0.65 | $ | (0.05 | ) | $ | (33.37 | ) | $ | (2.41 | ) | $ | 3.42 | ||||||

| DIVIDENDS PER COMMON SHARE |

$ | 0.09 | $ | 0.54 | $ | 0.72 | $ | 0.72 | $ | 0.67 | |||||||||

| CONSOLIDATED BALANCE SHEET DATA: |

|||||||||||||||||||

| Total assets |

$ | 3,302,899 | $ | 3,522,206 | $ | 4,137,919 | $ | 8,054,710 | $ | 2,087,116 | |||||||||

| Long-term debt (3) |

1,896,436 | 2,037,776 | 2,471,827 | 2,746,669 | 154,200 | ||||||||||||||

| Stockholders’ equity |

170,189 | 52,429 | 425,540 | 3,103,624 | 1,565,591 | ||||||||||||||

| (1) | On March 5, 2007, the Company sold the (Minneapolis) Star Tribune newspaper of Minneapolis, MN. Results of the (Minneapolis) Star Tribune newspaper are included in discontinued operations for all periods presented. |

| (2) | On June 27, 2006 the Company purchased Knight-Ridder, Inc. Information as of and for the year ended December 31, 2006, includes the newspapers and other operations from the acquisition since the beginning of the third quarter of fiscal 2006. |

| (3) | Excludes $530.0 million classified in current liabilities as of December 31, 2006, as such debt was repaid with proceeds from the disposition of the (Minneapolis) Star Tribune newspaper. |

16

Table of Contents

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION |

Overview

The McClatchy Company is the third largest newspaper publisher by circulation in the United States, with 30 daily newspapers, 43 non-dailies, and direct marketing and direct mail operations. McClatchy also operates leading local websites in each of its markets which extend its audience reach. The websites offer users information, comprehensive news, advertising, e-commerce and other services. Together with its newspapers and direct marketing products, these interactive operations make McClatchy the leading local media company in each of its premium high growth markets. McClatchy-owned newspapers include The Miami Herald, The Sacramento Bee, the Fort Worth Star-Telegram, The Kansas City Star, The Charlotte Observer, and The (Raleigh) News & Observer.

McClatchy also owns a portfolio of premium digital assets, including 14.4% of CareerBuilder LLC, the nation’s largest online job site, 25.6% of Classified Ventures LLC, a newspaper industry partnership that offers classified websites such as: the auto website, cars.com, and the rental site, Apartments.com, and 33.3% of HomeFinder, LLC which operates the online real estate website HomeFinder.com.

The Company’s primary source of revenue is print and digital advertising, which accounted for 77.7% of the Company’s revenue for fiscal 2009. Print and digital advertising revenues are derived from retail, national and classified advertising. Print and preprinted insert advertising are sold in the daily newspaper, but are also sold in direct marketing and other advertising products. While percentages vary from year to year and from newspaper to newspaper, classified advertising has steadily decreased as a percentage of total advertising revenues primarily in the employment and real estate categories and to a lesser extent the automotive category. Classified advertising as a percentage of total advertising revenues has declined to 26.9% in fiscal 2009 compared to 31.3% in fiscal 2008 and 36.4% in fiscal 2007, primarily as a result of the economic slowdown affecting classified advertising and the secular shift in advertising demand to online products.

While revenues from retail advertising carried as a part of newspapers (run-of-press or ROP advertising) or in advertising inserts placed in newspapers (preprint advertising) has decreased year over year, retail advertising has steadily increased as a percentage of total advertising up to 53.4% in 2009 compared to 50.1% in fiscal 2008 and 45.7% in fiscal 2007. This is partially a reflection of retail advertising declining at a slower rate than classified advertising, thus increasing as a percent of total advertising.

National advertising as a percentage of total advertising revenue remained relatively similar year over year and contributed 9.3% of total advertising revenue in fiscal 2009. Direct marketing and other advertising made up the remainder of the Company’s advertising revenues in fiscal 2009.

While included in the revenues described above, all categories of digital advertising are performing better than print advertising. In 2007, the Company joined a number of other newspaper companies in forming a broad-based partnership with Yahoo, Inc. (Yahoo). The Company’s local sales force is able to sell Yahoo advertising inventory and share in the revenue from the sales. In addition, the alliance allows the Company to use Yahoo’s behaviorally targeted ad-serving platform (APT platform) to sell advertising on the Company’s websites. While sales of Yahoo inventory and behaviorally targeted sales were conducted on a limited test basis in 2008, the Company began rolling out the APT platform to its newspaper websites in early 2009.

In total, revenues from digital advertising increased 2.3% in fiscal 2009 compared to the fiscal 2008 while print advertising revenues declined 31.0% over the same periods. However, employment advertising revenues, which have been negatively affected by the economic downturn, are down substantially in both print and digital. Excluding employment advertising, digital advertising revenues grew 27.8% in fiscal 2009, compared to fiscal 2008. Also, digital advertising revenues represented 16.2% of total advertising revenues in fiscal 2009, up from 11.6% of total advertising revenues in fiscal 2008 and from 8.6% of total advertising in fiscal 2007.

17

Table of Contents

Circulation revenues increased to 18.9% of the Company’s newspaper revenues in fiscal 2009 from 14.0% in fiscal 2008 and 12.2% in fiscal 2007. Most of the Company’s newspapers are delivered by independent contractors. Circulation revenues are recorded net of direct delivery costs.

See the following “Results of Operations” for a discussion of the Company’s revenue performance and contribution by category for fiscal 2009, 2008 and 2007.

Recent Events and Trends

Advertising Revenues:

Advertising revenues declined across the board in fiscal 2009 and fiscal 2008 and in nearly every category in fiscal 2007. Classified advertising revenues have continued to decline since late 2006. Real estate advertising revenues began to weaken in the fourth fiscal quarter of 2006 and have declined substantially since then. The decline in automotive classified advertising revenues reflected an industry-wide decline that began in 2004, while employment advertising revenues have declined in most markets since the third fiscal quarter of 2006. National advertising also declined in fiscal years 2007 through 2009 reflecting a slowdown in a number of segments including telecommunications, national automotive and financial advertising. In each case, management believes the declines are primarily attributable to the weaknesses in the United States economy, and to a lesser extent, the general shift in advertising to the internet where the Company’s newspapers face increased competition.

Advertising revenues in the fourth quarter of 2009 and in January and February 2010 have declined at a slower rate than the first nine months of 2009, evidence that the recession may be lessening in impact in the markets in which the Company operates.

See the revenue discussions in management’s review of the Company’s “Results of Operations”.

Restructuring Plans and Other Expense Activity:

In 2008, the Company announced plans to reduce its workforce, as the Company streamlined its operations and staff size. The Company’s workforce in 2008 was reduced by approximately 2,550 positions. The workforce reductions resulted in total severance costs of approximately $45 million which was largely paid in 2008.

In March 2009, the Company announced additional restructuring efforts which included reducing the Company’s workforce by 15%, or 1,650 positions, the freezing of the Company’s pension plans and a temporary suspension of the Company matching contribution to the 401(k) plan as of March 31, 2009. The Company’s restructuring plan also involved wage reductions across the Company for additional savings. The Company’s chairman and chief executive officer (CEO) declined his 2008 and 2009 bonuses and other executive officers did not receive bonuses for 2008. In addition, effective March 30, 2009, the CEO’s base salary was reduced by 15%, other executive officers’ salaries were reduced by 10%, and no bonuses were paid to any employee in 2009. The Company also reduced the cash compensation, including retainers and meeting fees, paid to its directors by approximately 13%, and the directors declined any stock awards for 2008 and 2009. Much of the expected expense reductions from this plan, which are largely permanent in nature, began to be realized in the second quarter of 2009. A total of $28.6 million in severance related costs associated with this restructuring plan (which represents substantially all costs associated with this plan) were incurred and largely paid through December 27, 2009.

Newsprint:

Newsprint prices are volatile and are largely dependent on global demand and supply for newsprint. Global demand remains weak resulting in continued low capacity utilization and below average newsprint prices. Newsprint prices peaked in the fourth quarter of 2008 and producers dropped prices in fiscal 2009. Prices began

18

Table of Contents

to increase in the second half of 2009 but announcement of further price increases have been delayed since late 2009. Hence, the Company does not yet know whether the full amount of announced newsprint price increases will be implemented or the timing of such increases.

Significant changes in newsprint prices can increase or decrease the Company’s operating expenses and therefore, directly affect the Company’s operating results. However, because the Company has ownership interests in newsprint producer Ponderay, an increase in newsprint prices, while negatively affecting the Company’s operating expenses, would increase its share of earnings from this investment. A decline in newsprint prices would have the opposite effect. Ponderay is also impacted by the higher cost of energy and fiber used in the papermaking process. The impact of newsprint price increases on the Company’s financial results is discussed under “Results of Operations”.

Equity Investments:

On March 31, 2008, the Company, along with the other general partners of SP Newsprint Co. (SP), completed the sale of SP, of which the Company was a one-third owner. The Company recorded a gain on the transaction of $34.4 million. The Company used the $55.0 million of proceeds it received from the sale to reduce debt and received $5.0 million of proceeds in 2009, which was used to reduce debt.

On June 30, 2008, the Company sold its 15.0% ownership interest in ShopLocal, for $7.9 million and used the proceeds to reduce debt. The Company reduced its carrying value of ShopLocal to match the sales price. In addition, Classified Ventures, identified goodwill impairment at a real estate-related reporting unit and as a result, the Company recognized a charge related to this investment in fiscal 2008. The total non-cash pre-tax charges related to impairments of internet investments, including ShopLocal and Classified Ventures, recorded in fiscal 2008 were $26.5 million.

At the end of 2008, The Seattle Times Company (STC) recorded a comprehensive loss related to its retirement plan liabilities. The Company recorded its share of the comprehensive loss in the Company’s comprehensive income (loss) in stockholders’ equity to the extent that it had a carrying value in its investment in STC. As result the Company’s investment in STC at December 28, 2008 was zero, and no future income or losses from STC will be recorded until the Company’s carrying value is restored through future earnings by STC.

Refinancing and Debt Exchange Offers:

Debt Refinancing—The Company was a party to a credit agreement, dated as of June 27, 2006 (as amended through May 20, 2009, the “original credit agreement”), which provided for a five-year revolving credit facility and term loans. On January 26, 2010, the Company entered into an amendment to the original credit agreement that became effective on February 11, 2010, immediately prior to the closing of an offering of $875 million of senior secured public notes. The original credit agreement was amended and restated in its entirety (the “Amended and Restated Credit Agreement or Credit Agreement”). The Amended and Restated Credit Agreement provides for a $262.0 million term loan and a $249.3 million revolving credit facility, including a $100 million letter of credit sub-facility, and extended the term of certain of the credit commitments to July 1, 2013. In connection with the Amended and Restated Credit Agreement, certain of the lenders did not extend the maturity of their commitments from the original maturity date of June 27, 2011. Non-extended term loans equaling $72.3 million will mature on June 27, 2011 as will revolving loan commitments equal to $42.2 million. The remaining term loans and revolving loan commitments under the Amended and Restated Credit Agreement will mature on July 1, 2013. No revolving loans were outstanding as of February 11, 2010 and the Company had excess proceeds of approximately $83.8 million which were invested in cash equivalents and will be used to prepay Term A debt. Based on the terms of the Credit Agreement, a portion of the excess proceeds will be used to further reduce the available facilities under the Credit Agreement within 30 days of the closing of the transaction.

In connection with the Credit Agreement, the Company issued new 11.5% Senior Secured Notes due 2017 (the “2017 Notes”), totaling $875 million. The 2017 Notes are secured by a first-priority lien on certain of McClatchy’s and the subsidiary guarantors’ assets, and will rank pari passu with liens granted under McClatchy’s