Attached files

| file | filename |

|---|---|

| EX-32 - ACURA PHARMACEUTICALS, INC | v175435_ex32.htm |

| EX-31.1 - ACURA PHARMACEUTICALS, INC | v175435_ex31-1.htm |

| EX-31.2 - ACURA PHARMACEUTICALS, INC | v175435_ex31-2.htm |

| EX-10.30 - ACURA PHARMACEUTICALS, INC | v175435_ex10-30.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

(Mark

One)

|

x

|

ANNUAL REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR

THE FISCAL YEAR ENDED DECEMBER 31,

2009

|

Or

|

¨

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For

the transition period from _____ to _____

Commission

file number 1-10113

ACURA

PHARMACEUTICALS, INC.

(Exact

name of registrant as specified in its charter)

|

New

York

|

11-0853640

|

|

(State

or other jurisdiction of Incorporation or organization)

|

(I.R.S.

Employer Identification No.)

|

|

616

N. North Court, Suite 120, Palatine, Illinois

|

60067

|

|

(Address

of principal executive office)

|

(Zip

code)

|

Registrant's

telephone number, including area code: 847 705 7709

Securities

registered pursuant to section 12(b) of the Act:

Common

Stock, par value $0.01 per share

Securities

registered pursuant to section 12(g) of the Act:

(Title of

Class)

None

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. Yes o No x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. Yes o No x

Indicate

by check mark whether the registrant: (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required

to file such reports), and (2) has been subject to such filing requirements for

the past 90 days. Yes x No o

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files). Yes o No o

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K (§229.405 of this chapter is not contained herein, and will not

be contained, to the best of registrant's knowledge, in definitive proxy or

information statements incorporated by reference in Part III of this Form 10-K

or any amendment to this Form 10-K. x

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company.

o Large Accelerated

Filer, x

Accelerated Filer, ¨ Non-Accelerated Filer,

¨ Smaller Reporting

Company.

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). Yes o No x

Based on

the last sale price on the NASDAQ Capital Market of the Common Stock

on June 30, 2009 ($5.98) (the last

business day of the registrant's most recently completed second fiscal quarter),

the aggregate market value of the voting stock held by non-affiliates of the

registrant was approximately $57,306,507.

As of

February 28, 2010, the registrant had 43,728,626 shares of Common Stock, par

value $0.01, outstanding.

Documents

incorporated by reference: None

Acura

Pharmaceuticals, Inc.

Form

10-K

For

the Fiscal Year Ended December 31, 2009

Tablet

of Contents

|

PAGE

|

||||

|

PART

I

|

||||

|

Item

1.

|

Business

|

3

|

||

|

Item

1A.

|

Risk

Factors

|

21

|

||

|

Item

1B.

|

Unresolved

Staff Comments

|

32

|

||

|

Item

2.

|

Properties

|

32

|

||

|

Item

3.

|

Legal

Proceedings

|

32

|

||

|

Item

4.

|

Reserved

|

33

|

||

|

PART

II

|

33

|

|||

|

Item

5.

|

Market

for Registrant's Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities

|

33

|

||

|

Item

6.

|

Selected

Financial Data

|

34

|

||

|

Item

7.

|

Management's

Discussion and Analysis of Financial Condition and Results of

Operations

|

35

|

||

|

Item

7A.

|

Quantitative

and Qualitative Disclosures About Market Risk

|

43

|

||

|

Item

8.

|

Financial

Statements and Supplementary Data

|

43

|

||

|

Item

9.

|

Changes

in and Disagreement with Accountants on Accounting and Financial

Disclosure

|

43

|

||

|

Item

9A.

|

Controls

and Procedures

|

43

|

||

|

Item

9B.

|

Other

Information

|

46

|

||

|

PART

III

|

||||

|

Item

10.

|

Directors,

Executive Officers and Corporate Governance

|

46

|

||

|

Item

11.

|

Executive

Compensation

|

50

|

||

|

Item

12.

|

Security

Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters

|

70

|

||

|

Item

13.

|

Certain

Relationships and Related Transactions, and Director

Independence

|

72

|

||

|

Item

14.

|

Principal

Accountant Fees and Services

|

74

|

||

|

PART

IV

|

||||

|

Item

15.

|

Exhibits

and Financial Statement Schedules

|

74

|

||

|

Signatures

|

75

|

|||

|

Index

to Financial Statements

|

F-1

|

|||

2

Forward-Looking

Statements

Certain

statements in this Report constitute "forward-looking statements" within the

meaning of the Private Securities Litigation Reform Act of 1995. Such

forward-looking statements involve known and unknown risks, uncertainties and

other factors which may cause our actual results, performance or achievements to

be materially different from any future results, performance, or achievements

expressed or implied by such forward-looking statements. The most significant of

such factors include, but are not limited to, our ability and the ability of

King Pharmaceuticals Research and Development, Inc. (“King”) (to whom we have

licensed our Aversion®

Technology for certain opioid analgesic products in the United States, Canada

and Mexico) and the ability other pharmaceutical companies, if any, to whom we

may license our Aversion®

Technology, to obtain necessary regulatory approvals and commercialize products

utilizing our Aversion® and

Impede™ Technologies, the ability to avoid infringement of patents, trademarks

and other proprietary rights of third parties, and the ability to fulfill the

U.S. Food and Drug Administration’s (“FDA”) requirements for approving our

product candidates for commercial manufacturing and distribution in the United

States, including, without limitation, the adequacy of the results of the

laboratory and clinical studies completed to date and the results of laboratory

and clinical studies we may complete in the future, to support FDA approval of

our product candidates, the adequacy of the development program for our product

candidates, including whether additional clinical studies will be required to

support FDA approval of our product candidates, changes in regulatory

requirements, adverse safety findings relating to our product candidates, the

risk that the FDA may not agree with our analysis of our clinical studies and

may evaluate the results of these studies by different methods or conclude that

the results of the studies are not statistically significant, clinically

meaningful or that there were human errors in the conduct of the studies or the

risk that further studies of our product candidates are not positive or

otherwise do not support FDA approval, whether or when we are able to obtain FDA

approval of labeling for our product candidates for the proposed indications or

for abuse deterrent features, whether our product candidates will ultimately

deter abuse in commercial settings, and the uncertainties inherent in

scientific research, drug development, laboratory and clinical trials and the

regulatory approval process. Other important factors that may also

affect future results include, but are not limited to: our ability to attract

and retain skilled personnel; our ability to secure and protect our patents,

trademarks and other proprietary rights; litigation or regulatory action that

could require us to pay significant damages or change the way we conduct our

business; our ability to compete successfully against current and future

competitors; our dependence on third-party suppliers of raw materials; our

ability to secure U.S. Drug Enforcement Administration ("DEA") quotas and source

the active ingredients for our products in development; difficulties or delays

in conducting clinical trials for our product candidates or in the commercial

manufacture and supply of our products; and other risks and uncertainties

detailed in this Report. When used in this Report, the words "estimate,"

"project," "anticipate," "expect," "intend," "believe," and similar expressions

identify forward-looking statements.

PART

I

ITEM 1. BUSINESS

Overview

We are a

specialty pharmaceutical company engaged in research, development and

manufacture of product candidates intended to provide abuse deterrent features

and benefits utilizing our proprietary Aversion® and Impede™

Technologies. Our Aversion®

Technology opioid analgesic product candidates are intended to effectively

relieve pain while simultaneously discouraging common methods of opioid product

misuse and abuse, including the:

|

|

·

|

intravenous

injection of dissolved tablets or

capsules;

|

|

|

·

|

nasal

snorting of crushed tablets or capsules;

and

|

|

|

·

|

intentional

swallowing of excess quantities of tablets or

capsules.

|

All of

our opioid product candidates utilize Aversion® Technology and are covered by

two issued U.S. patents, which in combination with our anticipated product

labeling and drug product listing strategies are anticipated to provide our

opioid products with protection from generic competition through the expiration

of our patents in 2025.

In addition to Acurox®, our lead

product candidate, we (and/or our licensee, King) are developing Vycavert®

(hydrocodone bitartrate/niacin/APAP), Acuracet®

(oxycodone HCl/niacin/ APAP) and additional undisclosed opioid product

candidates utilizing our Aversion® Technology. Four opioid product

candidates are licensed to King under our License, Development and

Commercialization Agreement dated October 30, 2007. We are also

developing an undisclosed benzodiazepine tablet product candidate utilizing

Aversion® Technology.

3

In addition to our Aversion®

Technology, as part of our continuing research efforts we are investigating and

developing novel mechanisms to incorporate abuse deterrent characteristics into

abused and misused pharmaceutical products. In this regard we are

engaged in initial laboratory testing of a new product candidate developed with

our novel Impede™ Technology. Impede™ Technology is primarily

intended to inhibit the conversion of pseudoephedrine HCl (a legally

available nasal decongestant) into methamphetamine (an illicit and frequently

abused drug).

Acurox® Tablets,

our lead product candidates, is an orally administered immediate release tablet

containing oxycodone HCl as its sole active analgesic ingredient. On

December 30, 2008, we submitted a 505(b)(2) New Drug Application (“NDA”) for

Acurox®

Tablets to the FDA and on June 30, 2009 we received from the FDA a

Complete Response Letter (“CRL”). The CRL raised issues regarding the

potential abuse deterrent benefits of Acurox®. On

September 2, 2009 we and King met with the FDA and agreed that the data and

evidence supporting the Acurox® Tablets

NDA would be presented to an FDA Advisory Committee. The FDA has not yet

scheduled the Advisory Committee meeting to review the NDA for Acurox® Although

the FDA stated that no new Acurox® clinical

trials are required at this time, we and King are conducting an additional

clinical study (see “Acurox® Tablets

Development Program” below) to further support the abuse deterrent features of

Acurox®.

The misuse and abuse of pharmaceutical

products in general, and opioid analgesics in particular, is a significant

societal problem described as epidemic in nature. It is estimated

that 75 million people in the U.S. suffer from pain, and, according to U.S.

government surveys, 34.9 million people, or more than 10% of the U.S.

population, have used prescription opioid analgesics non-medically at some point

in their lifetime. We expect our Aversion®

Technology opioid product candidates to compete primarily in the market for

immediate release opioid products (“IR Opioid Products”) which are commonly

prescribed for relief of pain for durations generally less than 30

days. In 2009, IMS Health reported 252 million prescriptions

dispensed for opioid analgesic tablets and capsules, of which approximately 236

million were for IR Opioid Products and 16 million were for extended release

opioid tablet and capsule products (“ER Opioid Products”) which are commonly

prescribed for relief of chronic pain for durations ranging from several weeks

to several months or longer. We have contracted, through an independent market

research firm, numerous market research studies including two which surveyed 401

and 435 opioid analgesic prescribing U.S. based physicians,

respectively. These studies revealed that physicians are keenly aware

of opioid analgesic abuse and are personally concerned with the potential impact

of drug abuse on their respective medical practices. Our study of 401

physicians indicated that of the prescriptions likely to be written for our

product candidates that utilize the analgesic oxycodone, 59% will be switched

from immediate release products containing either hydrocodone or oxycodone, with

the remaining 41% being

switched from other currently marketed opioid analgesic products such as

codeine, propoxyphene, morphine, and tramadol. Ninety-four percent

(94%) of 401 physicians surveyed indicated they would either prescribe one of

the Aversion®

Technology products profiled in the market research questionnaire for one

of their last five patients receiving an opioid prescription or they are aware

of a patient in their practice for whom Aversion®

Technology opioid analgesic products would be an appropriate

choice.

We have

established and intend to pursue future strategic alliances and licensing

agreements with pharmaceutical companies to enhance our ability to develop and

commercialize our product candidates. In October 2007, we entered into a

License, Development and Commercialization Agreement with King to develop and

commercialize certain opioid analgesic products utilizing our proprietary

Aversion®

Technology, including Acurox®

Tablets. The King Agreement initially provided King with an exclusive

license in the United States, Canada and Mexico (the “King Territory”) to

Acurox® Tablets

and Acuracet®

(oxycodone HCl/niacin/acetaminophen) Tablets, and an option to license future

opioid analgesic product candidates utilizing our Aversion®

Technology in the King Territory. In May and December 2008, King

exercised its option and licensed an undisclosed opioid analgesic tablet product

and Vycavert® (hydrocodone bitartrate/niacin/acetaminophen) Tablets,

respectively. Under the terms of the King Agreement, King made an

upfront cash payment to us of $30 million. As of February 28, 2010,

we had received an additional $26.2 million from King in the form of milestone

payments, option fees and reimbursement for research and development expenses.

In addition, we are eligible for future regulatory and sales milestone payments,

reimbursement for certain research and development expenses and royalties on

combined annual net sales of all products commercialized under the King

Agreement.

4

We

conduct research, development, laboratory, manufacturing, and warehousing

activities at our operations facility in Culver, Indiana and lease an

administrative office in Palatine, Illinois. In addition to internal

capabilities and activities, we engage numerous clinical research organizations

(“CROs”) with expertise in regulatory affairs, clinical trial design and

monitoring, clinical data management, biostatistics, medical writing, laboratory

testing and related services. Such CROs perform, under our direction,

development and regulatory services relating to our Aversion® and

Impede™ Technology product candidates.

Our

Strategy

Our goal

is to become a leading specialty pharmaceutical company focused on addressing

the growing societal problem of pharmaceutical drug abuse by developing

a broad portfolio of products with abuse deterrent features and

benefits. Specifically, we intend to:

|

|

·

|

Capitalize on our Experience

and Expertise in the Research and Development of Pharmaceutical Products

with Abuse Deterrent Features and Benefits. Our strategy

is to facilitate rapid product development and minimize risk by utilizing

active pharmaceutical ingredients with proven safety and efficacy profiles

with known potential for abuse, and develop new products utilizing our

proprietary Aversion®

and Impede™

Technologies using the FDA’s 505(b)(2) and other regulatory

processes.

|

|

|

·

|

Emerge as a Leader in

Developing and Commercializing Products with Abuse Deterrent Features and

Benefits Able to Uniquely Address the Growing Problem of Abuse of

Prescription Drugs. We believe that Acurox®

and our other opioid product candidates in development have

demonstrated that Aversion®

Technology allows products to provide the analgesic benefit they were

intended to deliver, while simultaneously having features that are

intended to deter misuse and abuse. We believe these benefits

will be attractive to physicians, third party payers, and public advocacy

groups sensitive to the problem of prescription drug

abuse.

|

|

|

·

|

Optimize Shareholder Value and

Temper Risk by Licensing our Product Candidates to Strategically Focused

Pharmaceutical Companies in the U.S. and Other Geographic

Territories. On October 30, 2007, we and King entered

into the King Agreement to develop and commercialize in the United States,

Canada and Mexico opioid analgesic products utilizing Aversion®

Technology, including Acurox ®

Tablets and Acuracet®

Tablets. We believe opportunities exist to enter into similar

agreements with other partners for these same opioid products outside the

King Territory, and in the United States and worldwide for developing

additional Aversion®

Technology and Impede™

Technology product candidates for other abusable drugs such as

tranquilizers, stimulants, sedatives and decongestants. By

licensing our product candidates to strategically focused companies with

expertise and infrastructure in commercialization of pharmaceuticals, we

are able to leverage our expertise, intellectual property rights and

Aversion®

and Impede™

Technologies without the need to build costly sales and manufacturing

infrastructure. We anticipate that our future revenue, if any,

will be derived from milestone and royalty payments related to the

commercialization of products utilizing our Aversion®

and Impede™

Technologies.

|

|

|

·

|

Apply our Aversion® and Impede™

Technologies to

Non-Opioid Drugs that are Subject to Abuse. We intend to

first develop a portfolio of opioid analgesic products, and thereafter we

intend to expand to other pharmaceutical product categories containing

potentially abusable active ingredients such as tranquillizers (brand

products such as Valium®,

Xanax®,

Klonopin® and Ativan®),

stimulants (brand products such as Dexedrine®,

Adderall®,

Ritalin®

and Concerta®),

sedatives (brand products such as Nembutal®,

Butisol®,

and Seconal®)

and decongestants (brand products such as Sudafed®, Zyrtec-D®, Allegra-D®,

and Clarinex-D®). These products, like the opioid analgesics on

which we are currently focused, may also be prone to misuse and

abuse.

|

|

|

·

|

Maintain our Efficient

Internal Cost Structure. We maintain a streamlined and

highly efficient cost structure focused on: (i) selection, formulation

development, laboratory evaluation, manufacture, quality assurance and

stability testing of certain finished dosage form product candidates; (ii)

development and prosecution of our patent applications; and (iii)

negotiation and execution of license and development agreements with

strategically focused pharmaceutical companies. By outsourcing

the high cost elements of our product development and commercialization

process, we believe that we substantially reduce required fixed overhead

and capital investment and thereby reduce our business risk. We

currently do not intend to use a physician focused sales force

to commercialize products on our

own.

|

5

Aversion®

Technology Opioid Product Candidates in Development

Aversion®

Technology opioid analgesic product candidates which have demonstrated Proof of

Concept1 are set

forth in the table below.

|

Our Product Candidates

|

Stage of Development

|

|

|

Acurox® (oxycodone

HCl/niacin) Tablets

|

NDA

submitted to FDA on 12/30/08; Complete Response Letter received 6/30/09;

FDA Advisory Committee meeting pending scheduling.

|

|

|

Acuracet®

(oxycodone HCl/niacin/APAP) Tablets

|

Investigational

New Drug Application ("IND") filed with FDA and active beginning

6-1-08. Testing for NDA submission in

progress

|

|

|

Vycavert®

(hydrocodone bitartrate/niacin/APAP) Tablets

|

Proof

of Concept complete. Testing for IND filing in

progress

|

|

|

4th

(undisclosed opioid analgesic) Tablets

|

Proof

of Concept complete.

|

|

|

5th

(undisclosed opioid analgesic) Tablets

|

Proof

of Concept complete

|

|

|

6th

(undisclosed opioid analgesic) Tablets

|

Proof

of Concept complete

|

|

|

7th

(undisclosed opioid analgesic) Tablets

|

Proof

of Concept complete

|

|

|

8th

(undisclosed opioid analgesic) Tablets

|

Proof

of

Concept complete

|

1 Proof of

concept is attained upon demonstration of certain product stability and

bioavailability parameters defined in the King Agreement. Refer to description

of the King Agreement in this Report. With one exception, King has either

licensed or has an option to license all opioid product candidates listed above

in the U.S., Canada and Mexico.

Aversion®

Technology Overview

Aversion®

Technology is a proprietary platform technology providing abuse deterrent

features and benefits to orally administered pharmaceutical drug products

containing potentially abusable active ingredients. Our focus has

been to utilize our Aversion®

Technology with opioid analgesics administered in tablet form. In

addition, we believe Aversion®

Technology is a versatile technology which may be applicable to non-opioid

active ingredients subject to abuse and administered in tablet or capsule form,

including tranquilizers, sedatives and stimulants (See “Aversion® Technology

Non-Opioid Product Candidates in Development” below).

Aversion®

Technology opioid analgesic product candidates include a unique composition of

active and inactive pharmaceutical ingredients. The opioid active

ingredients are intended to provide effective relief from pain while the

proprietary mixture of inactive ingredients provide non-therapeutic

functionality. When dissolved in water or other solvents, the functional

inactive ingredients quickly form a viscous gel, which increases the difficulty

of extracting the opioid active ingredient in a form and volume suitable for

injection. In addition, the combination of functional inactive

ingredients is intended to induce nasal passage discomfort and disliking effects

if the tablets are pulverized and snorted. Aversion®

Technology opioid product candidates may also include niacin, an active

ingredient in vitamins, cholesterol reducers and nutritional supplements, in

amounts determined by us to be well tolerated when our product candidates are

administered at recommended doses but which are intended to induce temporary

disliking effects as increasing numbers of tablets are swallowed in excess of

the recommended analgesic dose. When Aversion®

Technology is utilized, it is intended that the resulting product provides

the same therapeutic benefits as the non Aversion®

Technology product, while simultaneously discouraging the most common methods of

pharmaceutical product misuse and abuse.

Intended

to Deter I.V. Injection of Opioids Extracted from Dissolved Tablets

Prospective

drug abusers may attempt to dissolve currently marketed opioid-containing

tablets or capsules in water, alcohol, or other common solvents, filter the

dissolved solution, and then inject the resulting fluid intravenously to obtain

euphoric effects. In product candidates utilizing Aversion®

Technology, extracting the active ingredient using generally available solvents,

including water or alcohol, into a volume and form suitable for intravenous

(“I.V.”) injection, converts the tablet into a viscous gel mixture and traps the

active ingredient in the gel. Additionally, it is not possible,

without difficulty, to draw this viscous gel through a needle into a syringe for

I.V. injection. We believe that this gel forming feature will inhibit

prospective I.V. drug abusers from extracting and injecting opioid active

ingredients from product candidates developed utilizing Aversion®

Technology.

6

Intended

to Deter Nasal Snorting

Prospective

drug abusers may crush or grind currently marketed pharmaceutical

opioid-containing tablets or capsules and snort the resulting

powder. The abused active ingredient in the powder is absorbed

through the lining of the nasal passages providing the abuser with a rapid onset

of euphoric effects. Aversion®

Technology products are intended to discourage nasal snorting by burning and

irritating the nasal passages of a prospective drug abuser who crushes and

snorts such products. We believe products which utilize Aversion®

Technology will inhibit prospective nasal drug abusers from snorting crushed

tablets.

Intended

to Deter Swallowing Excess Quantities of Tablets

Niacin,

an active ingredient in vitamins, cholesterol reducers and nutritional

supplements, is included in the majority of our opioid analgesic product

candidates utilizing Aversion®

Technology. We believe that should a person swallow excess quantities

of tablets utilizing Aversion®

Technology with niacin they will experience disliking symptoms,

including intense flushing, itching, sweating and/or chills, headache and a

general feeling of discomfort as a result of the increasing dose of

niacin. It is expected that these niacin-induced disliking symptoms

will begin approximately 10 to 15 minutes after the excess dose is swallowed and

will dissipate approximately 75 to 90 minutes later. In addition, we

believe it is generally recognized by physicians, nurses, and other health care

providers that niacin has a well established safety profile in long term

administration at doses far exceeding the amounts in each product candidate

utilizing Aversion®

Technology with niacin. We believe the undesirable niacin effects at

escalating doses will not prevent, but are expected to deter, swallowing excess

quantities of product candidates utilizing Aversion® Technology with

niacin.

U.S.

Market Opportunity for Opioid Analgesic Products Utilizing Aversion® Technology

The

misuse and abuse of prescription drug products in general, and opioid analgesics

in particular, is a significant societal problem that has been described as

epidemic in nature by Joseph A. Califano, Jr., Chairman and President, National

Center for Addiction and Substance Abuse at Columbia University, July

2005. Results from the 2008 National Survey on Drug Use

and Health, estimated that 34.9 million people, or more than 10% of the

population, have used prescription opioid analgesics non-medically at some point

in their lifetime. In addition, it is estimated that more than 75

million people in the U.S. suffer from pain, which is more than the number of

people with diabetes, heart disease and cancer combined. For many

pain sufferers, opioid analgesics provide their only pain relief. As

a result, opioid analgesics are among the largest prescription drug classes in

the U.S. with over 252 million tablet and capsule prescriptions dispensed in

2009 of which approximately 236 million were for IR Opioid Products and 16

million were for ER Opioid Products. However, physicians and

other health care providers at times are reluctant to prescribe opioid

analgesics for fear of misuse, abuse, and diversion of legitimate prescriptions

for illicit use.

We expect

our Aversion® Technology opioid product candidates to compete primarily in the

IR Opioid Product segment of the US opioid analgesic market, a segment which has

grown at a 4% compounded annual rate over the last five years. On average, an IR

Opioid Product prescription contains approximately 57 tablets or

capsules. According to the 2008 National Survey on Drug Use

and Health, prescription drug abusers have supplanted abusers of all

illicit drugs except marijuana. Of these abused prescription

products, IR Opioid Products, which typically provide rapid onset of analgesia

and require dosing every 4 to 6 hours, comprise the vast majority of this abuse

compared with ER Opioid Products, which release their opioids gradually,

generally over a 12 to 24 hour period. Due to fewer identified

competitors and the significantly larger market for dispensed prescriptions for

IR Opioid Products compared to ER Opioid Products, we have initially focused on

developing IR Opioid Products utilizing Aversion® Technology.

According

to IMS Health, in 2009, sales in the IR Opioid Product segment, comprised of 97%

generic products, were $1.9 billion. Assuming the FDA approves

differentiated label claims of the abuse deterrent features and benefits of our

product candidates, of which no assurance can be given, we anticipate that our

Aversion®

Technology IR Opioid Products will be premium priced compared to generic

products resulting in rapid growth of sales in the IR Opioid Product market

segment.

7

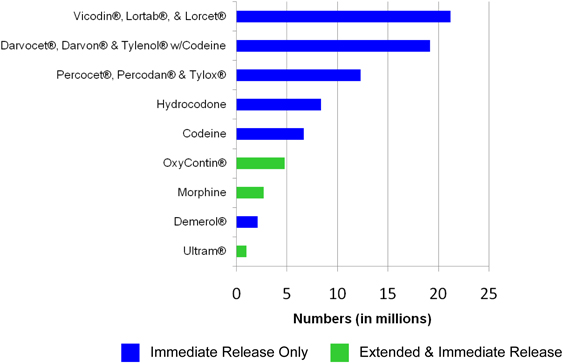

Despite

considerable publicity regarding the abuse of OxyContin® Tablets

and other ER Opioid Products, U.S. government statistics suggest that far more

people have used IR Opioid Products non-medically than ER Opioid

Products. These statistics estimate that nearly 5 times as many

people have misused the IR Opioid Products Vicodin®,

Lortab® and

Lorcet®

(hydrocodone bitartrate/APAP) as have ever abused OxyContin®. We

estimate 60-95% of the 34.9 million lifetime US opioid abusers have

non-medically used the active ingredients in our IR Opioid product

candidates. As indicated in the following chart, the top five abused

opioid products are available only as IR Opioid Products.

Lifetime

Non-Medical Use of Selected Pain Relievers, Age 12 or Older: 2008

Source: SAMHSA,

Office of Applied Studies, 2008 National Survey on Drug Use and

Health.

We have

commissioned, through an independent market research firm, three physician

market research studies with 282, 401 and 435 opioid prescribing U.S. based

physicians, respectively. A sampling of key findings from these

approximately 1,100 physicians includes:

Physicians

are keenly aware of opioid analgesic abuse

|

|

·

|

The

282 physicians surveyed estimated on average that about one out of six

prescriptions for oxycodone and hydrocodone containing products are

abused.

|

|

|

·

|

94%

of the 435 physicians surveyed experienced at least one suspicious

incident regarding opioid abuse in the past month, while nearly 64%

experienced four or more discretely different incidents regarding opioid

abuse in the past month.

|

Physicians

are personally concerned with opioid abusers impact to their respective

practices

|

|

·

|

Following the survey of 282

physicians, the researchers concluded, “abuse [of opioid analgesics] is a

particular problem for physicians because many are not fully sure who is

abusing these opioids, and they view such abuse as a legal threat to their

practice.” “More than half [of the physicians surveyed] believe

their physician colleagues are more concerned about avoiding state review

[of their opioid prescribing habits] than meeting [professional

association] pain guidelines [for their

patients]”.

|

|

|

·

|

After

the survey of 435 physicians the researchers concluded “the primary motive

for prescribing the Aversion®

Technology product[s] is the concern physicians have about opioid abuse

and the threat it represents to their

practice.”

|

8

Physicians

are favorably inclined toward prescribing opioids with abuse deterrent features

and benefits

|

|

·

|

94%

of the 401 physicians surveyed indicated that they would either prescribe

one of the Aversion®

Technology products profiled in the market research questionnaire for one

of their last five patients receiving an opioid prescription or they are

aware of a patient in their practice for whom Aversion®

Technology products would be an appropriate

choice.

|

|

|

·

|

57%

of the 435 physicians indicated that their opioid analgesic prescribing

would increase if they were more certain they were not aiding

abusers.

|

|

|

·

|

Following

the survey of 401 physicians, the researchers concluded “these

[Aversion®

Technology oxycodone products] would disproportionately replace current

immediate release oxycodone [and oxycodone/acetaminophen] prescriptions,

but would also draw substantial volume from hydrocodone/acetaminophen

products.”

|

Overall,

we believe the availability of opioid analgesics with abuse deterrent features,

including products using our Aversion®

Technology, will greatly impact the selection of products used for relief of

pain. Our market research survey of the 401 physicians indicated that

of the prescriptions likely to be written for our product candidates that

utilize oxycodone, 59% will be switched from immediate release products

containing either oxycodone or hydrocodone, with the remaining 41% being

switched from other currently marketed opioid analgesic products such as

codeine, propoxyphene, morphine and tramadol.

A

majority of pharmaceutical products in the U.S. are paid for by third party

payers such as insurers, pharmacy benefit managers, self-insured companies and

the federal and state governments through Medicare, Medicaid and other

programs. We believe our product candidates will have to demonstrate

a clinical benefit to the patient and/or an economic benefit to third party

payers and/or a benefit to health care providers to receive favored

reimbursement status by the payers.

Independent

estimates have been made assessing the potentially significant cost impact of

prescription opioid abuse to insurers. An analysis of health and

pharmacy insurance claims between 1998 and 2002 for almost 2 million Americans

conducted by Analysis Group, Inc. and others indicated that enrollees with a

diagnosis of opioid abuse had average claims of approximately $14,000 per year

higher than an age-gender matched non-opioid abuse sample. A 2007

report by the Coalition Against Insurance Fraud inflated this excess cost per

patient to more than $16,000 for 2007, and by applying the U.S. government’s

estimated 4.4 million annual opioid abusers, concluded that opioid abuse could

costs health insurers up to $72.5 billion a year.

Acurox®

Tablets Development Program

We

submitted a 505(b)(2) NDA for Acurox®

Tablets to the FDA on December 30, 2008 and received a Complete Response Letter

(“CRL”) on June 30, 2009. On September 2, 2009 we and King met with

the FDA and agreed that the data and evidence supporting the Acurox® Tablets

NDA would be presented to an FDA Advisory Committee. The FDA has not yet

scheduled the Advisory Committee meeting to review the NDA for Acurox®.

The NDA

for Acurox® Tablets

includes results from numerous clinical and laboratory studies assessing the

efficacy and safety of Acurox® Tablets

and to demonstrate abuse deterrent features and benefits, including the data and

results from studies set forth in the table below.

9

|

Studies in the Acurox® Tablets 505(b)(2) NDA Submission

|

Summary of Results

|

|||

|

AP-ADF-101

Phase

I

|

Niacin

dose-response (0-75mg)

|

Identified

appropriate niacin dose in each Acurox® Tablet

|

||

|

AP-ADF-104

Phase

I

|

Bioequivalence

to non Aversion® Technology Reference Listed Drug

|

Acurox®

Tablets are bioequivalent to the Reference Listed Drug

|

||

|

AP-ADF-108

Phase

I

|

Single

dose linearity and food effect

|

Acurox®

Tablets demonstrate single dose linearity. Absorption is

delayed by food.

|

||

|

AP-ADF-109

Phase

I

|

Multi-dose

linearity

|

Acurox®

Tablets demonstrate multi-dose linearity

|

||

|

AP-ADF-106

Phase

I

|

Evaluate

effects of nasal snorting in subjects with a history of snorting and nasal

drug abuse

|

Refer

to summary in this Report

|

||

|

AP-ADF-103

Phase

II

|

Repeat

dose safety and tolerability

|

Confirmed

appropriate niacin dose in each Acurox® Tablet

|

||

|

AP-ADF-107

Phase

II

|

Niacin

dose-response (0-600mg)

|

Confirmed

appropriate niacin dose in each Acurox® Tablet

|

||

|

AP-ADF-102

Phase

II

|

Evaluate

relative dislike of oxycodone HCl/niacin versus oxycodone HCl

alone

|

Refer

to summary in this Report

|

||

|

AP-ADF-111

Phase

II

|

Evaluate

abuse liability of oxycodone HCl/niacin versus oxycodone HCl

alone

|

Refer

to summary in this Report

|

||

|

AP-ADF-105

Phase

III

|

Evaluate

safety and efficacy in relief of moderate to severe pain

|

Refer

to summary in this Report

|

||

|

Extraction

Test

|

Laboratory

test quantifying I.V. abuse deterrent properties

|

Refer

to summary in this Report

|

||

|

Syringe

Test

|

Laboratory

test quantifying I.V. abuse deterrent properties

|

Refer

to summary in this

Report

|

||

Although

the FDA stated that no new Acurox® clinical

trials are required at this time, we and King are performing an additional

clinical study (Refer to Study AP-ADF-114 below) to further support the abuse

deterrent features of Acurox®.

Study AP-ADF-114 or Study

114: Study 114 is a randomized, double-blind, placebo- and

active-controlled study designed to assess the relative abuse potential of

Acurox® Tablets. In Study 114, approximately 47 fasted recreational

drug abuse subjects received single oral doses in five test treatments including

(a) two potentially abused excess doses of Acurox® (oxycodone/niacin) Tablets,

(b) two potentially abused excess oral doses of oxycodone HCl alone, and (c)

placebo. Dosing occurred every 48 hours. Prior to the

first test treatment, each subject first demonstrated, through naloxone

challenge, that they were not dependent on opioids. Also, each

subject demonstrated their ability to distinguish, on a 100-point VAS

like/dislike scale, between placebo and oxycodone doses randomly administered on

a blinded basis. Endpoints assessing abuse potential include

subjective assessments on a 100-point VAS of drug liking/disliking, take drug

again, and global overall drug liking/disliking. Study 114 has

completed enrollment and we are awaiting results of the statistical

analysis.

Study AP-ADF-106 or Study

106: Study 106 was a two part, Phase I, single-center,

single-blind, clinical study in non-dependent subjects with a history of

recreational intranasal opioid use to assess the safety, tolerability and

pharmacodynamic effects of intranasally administered crushed Acurox® Tablets,

crushed generic oxycodone HCl tablets and pure oxycodone HCl

powder. The primary objective of Part 1 (15 subjects enrolled, 13

subjects completed, 14 subjects analyzed) was to determine the maximum tolerated

dose of crushed Acurox® Tablets that subjects could snort in a single

administration. Subjects were administered escalating doses of crushed Acurox®

Tablets (7.5/30 mg) starting at one half tablet and increasing in half tablet

increments on successive days. Part 1 also assessed (over 8 hours

after administration) vital signs, subjective ratings of liking and somatic

(bodily) discomfort, and objective assessments of the nasal cavity determined by

endoscopy and intranasal photography. Part 2 (15 subjects

enrolled, 12 subjects completed, 10 subjects analyzed) assessed the relative

abuse liability of intranasally administered crushed Acurox® Tablets (7.5/30

mg), crushed generic oxycodone HCl immediate release tablets and pure oxycodone

HCl powder, all with a quantity of oxycodone HCl equivalent to the group median

highest tolerated dose of Acurox® Tablets determined in Part 1. Part

2 measurements were made over 12 hours and included vital signs, subjective

measures of liking and somatic (bodily) discomfort, objective assessments of the

nasal cavity and the pharmacokinetics of oxycodone after intranasal

administration.

Part 1 of

the study determined the maximum tolerated intranasal dose of crushed Acurox®

Tablets was 15 mg oxycodone HCl/60 mg niacin (i.e. 2 × 7.5/30 mg Acurox®

Tablets).

10

In Part 2

of the study, nasal administration of 2 crushed Acurox® Tablets

(7.5/30 mg ) resulted in disliking and low positive drug effect on the Overall

Drug Experience and Overall Drug Liking scales. In comparison,

crushed generic oxycodone HCl tablets and oxycodone HCl powder resulted in high

drug liking and positive drug effects with the mean difference being

statistically significant at p ≤ 0.0035. Furthermore, subjects were much less

willing to take crushed Acurox® Tablets

again compared to crushed oxycodone tablets and oxycodone powder (p ≤

0.0007). Intranasal administration of crushed Acurox® Tablets

caused significantly greater negative objective effects for nasal congestion and

discharge (p ≤ 0.0223) and negative subjective effects for nasal burning,

congestion and need to blow nose (p ≤ 0.0038). The results were not

statistically significant for the objective assessment of nasal

irritation.

Examination

of endoscopy and external photography revealed visible differences between the

treatments as only the crushed Acurox®

treatment was associated with white foamy

substance in the interior and middle turbinate of the nose and visible facial

flushing. Oxycodone bioavailability was similar between all three

treatments. In both Parts of the study, no serious adverse events were

reported. All adverse events were classified as mild or moderate with

the most prevalent adverse events being nasal symptoms (congestion, discomfort,

discharge), flushing, tearing and euphoria.

The

principal investigator’s overall conclusion was that, based on Study 106

results, intranasal administration of crushed Acurox® Tablets has a

distinctively lower abuse potential than the same oxycodone HCl dose

administered as crushed generic oxycodone HCl tablets or pure oxycodone HCl

powder.

Study AP-ADF-102 or Study

102: Study 102 was a Phase II, single center, randomized,

double blind crossover design clinical trial in 24 subjects with a history of

opioid abuse with a primary endpoint to assess, whether the subjects disliked

the drug effect they were feeling when varying levels of niacin were

administered in combination with 40 mg of oxycodone HCl compared to 40 mg

oxycodone HCl (alone) and a placebo. Each subject was randomized to a

dosing sequence that included doses of niacin (0, 240, 480 , and 600 mg)

administered in combination with 40 mg oxycodone HCl, while the subjects were

fasted and 600 mg niacin in combination with 40 mg oxycodone HCl administered

following a standardized high-fat meal. Each dosing day, vital sign

measures and subjective and behavioral effects were assessed before dosing

(baseline) and at 0.5, 1, 1.5, 2, 3, 4, 5, 6, and 12 hours after

dosing. After completion of the study, subjects responded to a

Treatment Enjoyment Assessment Questionnaire to select which of the treatments

they would take again. The maximum scale response to the question “Do

you dislike the drug effect you are feeling now?” (i.e., the “Disliking Score”),

was designated as the primary efficacy variable. Study results were

as follows:

|

|

·

|

In

the fasting state, all three doses of niacin in combination with oxycodone

HCl 40mg produced significant (p ≤ .05) Disliking Scores compared to

oxycodone HCl 40mg alone. No other subjective measure was

significantly affected by the niacin addition to

oxycodone.

|

|

|

·

|

The

high fat meal eliminated the niacin effect and also delayed the time to

oxycodone peak blood levels.

|

|

|

·

|

The

addition of niacin to oxycodone HCl alters the subjective response to

oxycodone HCl as indicated by the significant responses on the Disliking

Score. This observation in conjunction with the results from the Treatment

Enjoyment Questionnaire indicates that the addition of niacin reduces the

attractiveness of oxycodone to opiate

abusers.

|

|

|

·

|

There

were no serious adverse events. Niacin produced a dose related attenuation

of pupillary constriction, diastolic blood pressure increase and probably

systolic blood pressure increase produced by oxycodone HCl. The

alterations by niacin on the vital sign responses to oxycodone 40 mg were

minimal, were seen primarily with the 600 mg niacin dose and were not

clinically significant.

|

The principal study investigator’s

overall conclusion was that the results of Study 102 supported the hypothesis

that the addition of niacin to oxycodone HCl in a minimal ratio of 30 mg niacin

to 5 mg oxycodone HCl is aversive compared to oxycodone HCl

alone. The addition of niacin did not alter the safety profile of

oxycodone HCl alone.

11

Study AP-ADF-111 or Study

111: Study 111 is entitled "A Phase II, Single-Center,

Randomized, Double-Blind, Assessment of the Abuse Liability of Acurox®

(oxycodone HCl and niacin) Tablets in Subjects with a History of Opioid

Abuse". In Study 111, 30 fasted subjects with a history of opioid

abuse received a single dose of study drugs every 48 hours for 9 days and were

enrolled in two dosing sequences. The first dosing sequence (Sequence

1) included randomized doses of (i) niacin 240mg alone; (ii) a combination of

oxycodone HCl 40mg with niacin 240mg (4 times the expected recommended dose of

Acurox® Tablets

5/30mg); and (iii) placebo tablets. The objective of Sequence 1 was

to assess the effects of oxycodone HCl on the effects of niacin. The

second dosing sequence (Sequence 2) included randomized doses of (i) a

combination of oxycodone HCl 40mg with niacin 240mg (4 times the expected

recommended dose of Acurox® Tablets

5/30mg) and (ii) oxycodone HCl 40mg alone. Sequence 2 was designed to

assess the abuse liability and abuse deterrence potential of Acurox® Tablets

versus oxycodone HCl alone. On each dosing day, vital sign measures

and subjective and behavioral effects were assessed before dosing (baseline) and

at 0.5, 1, 1.5, 2, 3, 4, 5, 6, and 12 hours after dosing. Vital signs

included measurement of pupil size, blood pressure, heart rate, oral temperature

and respiratory rate. For both Sequence 1 and Sequence 2, subjective

changes were measured with a two item Drug Rating Questionnaire-Subject (DRQS)

and a 40 item short form of the Addiction Research Center Inventory

(ARCI). The ARCI was comprised of three scale scores including the

Morphine Benzedrine Group scale (MBG) measuring euphoria, the LSD/dysphoria

scale measuring somatic/bodily discomfort and dysphoria and the Pentobarbital

Chlorpromazine Alcohol Group scale (PCAG) measuring apathetic

sedation. For Sequence 2 only, in addition to the DRQS and ARCI,

subjects also completed a Street Value Assessment Questionnaire and a Treatment

Enjoyment Assessment Questionnaire.

Sequence 1 results demonstrated that

response to niacin 240 mg alone compared to placebo causes significant dislike

scores (p = .03), and significant LSD/dysphoria scores (p < .001) with these

negative niacin induced effects manifesting rapidly, reaching peak at 0.5-1.5

hours and thereafter diminishing. At 0.5 hours after drug

administration, oxycodone HCl 40 mg has limited effect on niacin-induced

disliking and dysphoric effects. At the one hour observation and

afterward, oxycodone may attenuate niacin-induced disliking and dysphoric

effects.

Sequence 2 demonstrated that the

combination of oxycodone HCl 40mg and niacin 240mg (4 times the expected

recommended dose of Acurox® Tablets

5/30mg) had the potential to be aversive when compared to oxycodone HCl 40mg

alone as shown by statistically significant and clinically meaningful results in

the dislike/like scores (p = .033), the Treatment Enjoyment Assessment scores (p

= .005) and the LSD/dysphoria scores (p<.001). The dislike/like

score at 0.5 hours was designated the primary measure of abuse liability and

abuse deterrence potential for Acurox® Tablets

5/30mg and the Treatment Enjoyment Assessment scores and LSD/dysphoria scores at

0.5 hours were additional measures of the abuse deterrence potential of

Acurox®

Tablets. Subjective measures not achieving statistical significance

included the MBG scores measuring euphoria, the PCAG score measuring apathetic

sedation and the Street Value Assessment Questionnaire score, in which subjects

indicated they would pay more for oxycodone HCl alone compared to Acurox® Tablets

(p=.097).

In this study of 30 subjects with a

history of opioid abuse there were no serious adverse events

reported. Alterations by niacin compared to placebo on vital signs

were minimal and not clinically meaningful. The differences in vital

signs between oxycodone HCl/niacin and niacin alone at 4 times the expected

recommended dose of Acurox® Tablets

were minimal and not clinically meaningful.

Study AP-ADF-105 or Study

105: Study 105 is entitled “A Phase III, Randomized,

Double-blind, Placebo-controlled, Multicenter, Repeat-dose Study of the Safety

and Efficacy of Acurox®

(oxycodone HCl and niacin) Tablets versus Placebo for the Treatment of Acute,

Moderate to Severe Postoperative Pain Following Bunionectomy Surgery in Adult

Patients.” A total of 405 patients were randomized to one of three

treatment arms of approximately 135 patients per arm. One treatment

arm received a dose of two Acurox® Tablets

5/30 mg, a second treatment arm received a dose of two Acurox® Tablets

7.5/30 mg, and the third treatment arm received a dose of two placebo

tablets. Study drugs were administered every 6 hours for 48

hours. The primary endpoint was the sum of the difference in pain

intensity, measured on a 100mm visual analog scale (VAS), compared to baseline

over a 48 hour period (“SPID48”). Prior

to initiating Study 105, the study design, endpoints and statistical analysis

plan were submitted to and agreed by the FDA under a Special Protocol Assessment

and the study was conducted accordingly. Results of Study 105

demonstrate that compared to placebo, Acurox® Tablets

5/30 mg and 7.5/30 mg both met the primary pain relief endpoint with p=.0001 and

p<.0001, respectively. Acurox® Tablets

were generally well tolerated with the most prevalent reported adverse events in

patients receiving Acurox® Tablets

being nausea, vomiting, dizziness, pruritus and flushing; side effects known to

be consistent with opioid and niacin therapies. Most adverse events

were mild or moderate and there were no serious adverse events. Six

patients (2.2%) receiving Acurox® Tablets

withdrew from the study due to treatment–emergent adverse events compared with

no withdrawals due to treatment-emergent adverse events for the placebo

group.

12

Extraction Test - In

consultation with experts in the field, a laboratory protocol for evaluating the

relative IV abuse liability of Acurox® Tablets was designed. To

provide unbiased, scientifically derived and documented study results, we

engaged a laboratory CRO specializing in

pharmaceutical product analysis to execute the protocol. The protocol

was intended to mimic the uncontrolled "real world" environment, except that

professional chemists with access to a wide range of laboratory equipment and

supplies would pose as potential IV drug abusers. As would be the

case with a potential IV drug abuser, these chemists were allowed unrestricted

access to information in developing oxycodone extraction methods and

techniques. The CRO was provided with a list of ingredients (active

and inactive) contained in each test product, allotted up to 80 hours total time

to complete the evaluations and allowed to use any methodology and/or solvents

desired to attempt to extract oxycodone HCl from the tablets in a form suitable

for I.V. injection. The test products were: OxyContin® (oxycodone HCl) Tablets 1 x 40

mg (Purdue Pharma), Oxycodone HCl Tabs 8 x 5 mg (Mallinckrodt), Percocet® (oxycodone HCl/APAP) Tablets 8

x 5/325 mg (Endo) and -Acurox®

(oxycodone HCl/niacin) Tablets 8 x 5/30 mg (Acura). The

results of the Extraction Test suggest that currently marketed oxycodone HCl

containing tablets may be easily dissolved in water in as little as 3 - 10

minutes for potential abuse via IV injection. By contrast, the Extraction Test

simulation suggests that preparing an injectable form of Acurox® Tablets is

difficult and not practical due to the time required (almost 6 hours) and the

inability to obtain a sufficient oxycodone yield that would provide any degree

of euphoric effect to the prospective drug abuser.

Syringe Test - The Syringe

Test was developed to simulate the relative difficulty of abusing dissolved

opioid tablets and capsules via IV injection. The test was designed as a

scientifically reproducible method to quantitatively measure the difficulty of

drawing into a syringe a solution made from tablets or capsules dissolved in

varying types and volumes of solvent. The test utilizes seven (7)

solvents available to potential abusers, the largest syringe barrel available

without a prescription and the largest bore needle in the subcutaneous syringe

set family. The needle and barrel are much larger than typically used

by abusers and represent a worst case scenario (e.g. easier to prepare an IV

injection). The Syringe Test results suggest that preparing an

injectable form of Acurox® Tablets using a variety of available solvents is

impractical due to high solvent volume requirements and the viscous/gelatinous

mixture formed when dissolving Acurox® Tablets in lower volumes of the solvents

tested. Even if a "Theoretically Injectable" solution of crushed

Acurox® Tablets is achieved it would require further processing by the

prospective abuser to separate oxycodone from other tablet ingredients

(including niacin and numerous excipients) and a reduction in total volume to

provide a solution in a volume and form that is practically suitable for IV

injection.

Expectations

for Acurox® Tablets

Product Labeling

The FDA has publicly stated that an

explicit indication or claims of abuse deterrence will not be permitted in

product labeling unless such indication or claims are supported by double blind

controlled clinical studies demonstrating an actual reduction in product abuse

by patients or drug abusers. We believe the cost, time and

practicality of designing and implementing clinical studies adequate to support

explicit labeling claims of abuse deterrence are prohibitive. The FDA

has stated that scientifically derived data and information describing the

physical characteristics of a product candidate and/or the results of laboratory

and clinical studies simulating product abuse may be acceptable to include in

the product label. We intend to include in the labels of our

Aversion®

Technology product candidates both a physical description of the abuse deterrent

characteristics and information from our numerous laboratory and clinical

studies designed to simulate the relative difficulty of abusing our product

candidates. The extent to which such information will be included in

the FDA approved product label will be the subject of our discussions with and

agreement by the FDA as part of the NDA review process for each of our product

candidates. Further, because FDA closely regulates promotional

materials, even if FDA initially approves labeling that includes a description

of the abuse deterrent characteristics of the product, the FDA will continue to

review the acceptability of promotional labeling claims and product advertising

campaigns for our product candidates.

King

Agreement

On October 30, 2007, we and King

Pharmaceuticals Research and Development, Inc. (“King”), a wholly-owned

subsidiary of King Pharmaceuticals, Inc., entered into a License, Development

and Commercialization Agreement (the “King Agreement”) to develop and

commercialize in the United States, Canada and Mexico (the "King Territory")

certain opioid analgesic products utilizing our proprietary Aversion®

Technology. The King Agreement initially provided King with an

exclusive license in the King Territory for Acurox®

(oxycodone HCl/niacin) Tablets and Acuracet®

(oxycodone HCl/niacin/APAP) Tablets, utilizing Aversion®

Technology. In addition, the King Agreement provides King with an

option to license in the King Territory all future opioid analgesic products

developed utilizing Aversion®

Technology. At December 31, 2009, King had exercised its option to license two

additional product candidates including an undisclosed opioid analgesic tablet

product and Vycavert®

(hydrocodone bitartrate/niacin/APAP) Tablets, each of which utilize our

Aversion®

Technology. We are responsible for using commercially reasonable

efforts to develop Acurox® Tablets through regulatory approval by the

FDA. The King Agreement provides that we or King may develop

additional opioid analgesic product candidates utilizing our Aversion®

Technology and, if King exercises its option to license such additional product

candidates, they will be subject to the milestone and royalty payments and other

terms of the King Agreement.

13

Pursuant to the King Agreement, we and

King formed a joint steering committee to oversee development and

commercialization strategies for Aversion® opioid analgesic products licensed to

King. We are responsible for all Acurox® Tablet

development activities, the expenses for which we are reimbursed by King,

through FDA approval of a 505(b)(2) NDA. After NDA approval King will be

responsible for commercializing Acurox® Tablets

in the U.S. With respect to all other products licensed by King

pursuant to the Agreement in all King Territories, King will be responsible, at

its own expense, for development, regulatory, and commercialization

activities. All products developed pursuant to the King Agreement

will be manufactured by King or a third party contract manufacturer under the

direction of King. Subject to the King Agreement, King will have final decision

making authority with respect to all development and commercialization

activities for all licensed products. We have reviewed our participation in the

King-Acura joint steering committee in light of the requirements of Emerging

Issues Task Force, Issue No. 00-21, “Revenue Arrangements with Multiple

Deliverables” (“EITF 00-21”) and concluded that this activity has no standalone

value therefore it does not meet the criteria to be considered a separate unit

of accounting.

At December 31, 2009, we had received

aggregate payments of $56.2 million from King, consisting of a $30.0 million

non-refundable upfront cash payment, $15.2 million in reimbursed research and

development expenses relating to Acurox® Tablets, $6.0 million in fees relating

to King’s exercise of its option to license an undisclosed opioid analgesic

tablet product and Vycavert® Tablets,

and a $5.0 million milestone fee relating to our successful achievement of the

primary endpoints for our pivotal Phase III clinical study for Acurox®

Tablets. The King Agreement also provides for King’s payment to us of

a $3.0 million fee upon King’s exercise of its option for each future opioid

product candidate. In the event that King does not exercise its

option for a future opioid product candidate, King may be required to reimburse

us for certain of our expenses relating to such future opioid product

candidate. Further, we may receive up to $23 million in additional

non-refundable milestone payments for each product candidate licensed to King,

including Acurox® Tablets,

which achieve certain regulatory milestones in specific countries in the King

Territory. We can also receive a one-time $50 million sales milestone

payment upon the first attainment of $750 million in net sales of all of our

licensed products across all King Territories. In addition, for sales

occurring following the one year anniversary of the first commercial sale of the

first licensed product sold, King will pay us a royalty at one of 6 rates

ranging from 5% to 25% based on the level of combined annual net sales for all

products licensed by us to King across all King Territories, with the highest

applicable royalty rate applied to such combined annual sales. King’s

royalty payment obligations expire on a product by product and

country-by-country basis upon the later of (i) the expiration of the last valid

patent claim covering such product in such country, or (ii) fifteen (15) years

from the first commercial sale of such product in such country. No

minimum annual fees are payable by either party under the King

Agreement. Reference is made to Item 9 of Note A of the Notes to

Consolidated Financial Statements included as a part of this Report, entitled

“Revenue Recognition and Deferred Program Fee Revenue” for a description of the

revenue recognition method employed by the Company under the King

Agreement.

The King Agreement expires upon the

expiration of King’s royalty payment and other payment obligations under the

King Agreement. King may terminate the King Agreement in its entirety

or with respect to any product at any time after March 31, 2010, upon the

provision of not less than 12 months’ prior written notice, and in its entirety

if regulatory approval of the NDA for Acurox® Tablets

is not received prior to March 31, 2010 and with respect to a particular product

with respect to a country in which regulatory approval for such product is

withdrawn by a regulatory authority in such country. We do not expect to

receive FDA approval of the NDA for Acurox® Tablets

prior to March 31, 2010. As a result, King may terminate the King

Agreement at any time following such date upon written notice to

us. We may terminate the King Agreement with respect to a product in

the United States in the event such product is not commercially launched by King

within 120 days after receipt of regulatory approval of such product or in its

entirety if King commences any interference or opposition proceeding challenging

the validity or enforceability any of our patent rights licensed to King under

the King Agreement. Either party has the right to terminate the King

Agreement on a product by product and country-by-country basis if the other

party is in material breach of its obligations under the King Agreement relating

to such product and such country, and to terminate the Agreement in its entirety

in the event the other party makes an assignment for the benefit of creditors,

files a petition in bankruptcy or otherwise seeks relief under applicable

bankruptcy laws, in each case subject to applicable cure

periods.

14

In the event of termination, no

payments are due except those royalties and milestones that have accrued prior

to termination under the King Agreement and all licenses under the King

Agreement are terminated. For all Acura terminations and termination

by King where we are not in breach, the King Agreement provides for the

transition of development and marketing of the licensed products from King to

us, including the conveyance by King to us of the trademarks and all regulatory

filings and approvals solely used in connection with the commercialization of

such licensed products and, in certain cases, for King’s supply of such licensed

products for a transitional period at King’s cost plus a mark-up.

The foregoing description of the King

Agreement contains forward-looking statements about Acurox® Tablets,

and other product candidates being developed pursuant to the King

Agreement. As with any pharmaceutical products under development or

proposed to be developed, substantial risks and uncertainties exist in

development, regulatory review and commercialization process. There

can be no assurance that the King Agreement will not be terminated by its terms

prior to receipt of regulatory approval for any product developed pursuant to

the King Agreement. Further, there can be no assurance that any

product developed, in whole or in part, pursuant to the King Agreement will

receive regulatory approval or prove to be commercially

successful. Accordingly, investors in the Company should recognize

that there is no assurance that the Company will receive the milestone payments

or royalty revenues described in the King Agreement or even if such milestones

are achieved, that the related products will be successfully commercialized and

that any royalty revenues payable to us by King will materialize. For

further discussion of other risks and uncertainties associated with the Company,

see Item 1A in this Report under the heading “Risks Factors”.

Patents

and Patent Applications

In April 2007, the United States Patent

and Trademark Office (“USPTO”), issued to us a patent titled “Methods and

Compositions for Deterring Abuse of Opioid Containing Dosage Forms” (the “920

Patent”). The 54 allowed claims in the 920 Patent encompass certain

pharmaceutical compositions intended to deter the most common methods of

prescription opioid analgesic product misuse and abuse. These patented

pharmaceutical compositions include specific opioid analgesics such as oxycodone

HCl and hydrocodone bitartrate among others.

In January 2009, the USPTO issued to us

a patent (the “402 Patent”) with 18 allowed claims. The 402 Patent encompasses

certain combinations of kappa and mu opioid receptor agonists

and other ingredients intended to deter opioid analgesic product misuse and

abuse.

In March 2009, the USPTO issued to us a

patent (the “726 Patent”) with 20 allowed claims. The 726 Patent

encompasses a wider range of abuse deterrent compositions than our 920

Patent.

In addition to our issued U.S. patents,

we have filed multiple U.S. patent applications and international patent

applications relating to compositions containing abusable active pharmaceutical

ingredients. Except for those rights conferred in the King Agreement,

we have retained all intellectual property rights to our Aversion® Technology,

Impede™ Technology, and related product candidates.

Reference is made to Item 1A, “Risk

Factors” for a discussion, among other things, of pending patent applications

owned by third parties including claims that may encompass our Acurox® Tablets

and other product candidates. If such third party patent applications

result in valid and enforceable issued patents containing claims in their

current form, we or our licensees could be required to obtain a license to such

patents, should one be available, or alternatively, to alter our product

candidates to avoid infringing such third-party patents.

Competition

in the Opioid Product Market

We

compete to varying degrees with numerous companies in the pharmaceutical

research, development, manufacturing and commercialization fields. Many of our

competitors have substantially greater financial and other resources and are

able to expend more funds and effort than us in research and development of

their competitive technologies and products. Although a larger company with

greater resources than us will not necessarily have a higher likelihood of

receiving regulatory approval for a particular product or technology as compared

to a smaller competitor, the company with a larger research and development

expenditure will be in a position to support more development projects

simultaneously, thereby potentially improving the likelihood of obtaining

regulatory approval of a commercially viable product or technology than its

smaller rivals.

15

We

believe potential competitors may be developing opioid abuse deterrent

technologies and products. Such potential competitors include, but may not be

limited to, Pain Therapeutics of South San Francisco, CA, (in collaboration with

King Pharmaceuticals Inc.), Purdue Pharma of Stamford, CT, Atlantic

Pharmaceuticals, of Atlanta, GA, Egalet a/s, of Verlose, Denmark and Collegium

Pharmaceuticals, Inc., of Cumberland, RI. These companies appear to

be focusing their development efforts on ER Opioid Products while our lead

product candidate, Acurox® Tablets,

and the majority of our other Aversion®

Technology opioid analgesic product candidates under development, are IR Opioid

Products.

Aversion®

Technology Non-Opioid Product Candidates in

Development

We are developing a benzodiazepine

product candidate utilizing our Aversion® Technology intended for the treatment

of anxiety disorders. According to Drugs of Abuse, published by

the US Drug Enforcement Administration, tranquilizers are abused in manners

similar to opioid analgesics. The 2008 National Survey on Drug Use and

Health estimates that 21.5 million people have abused prescription

tranquilizers (including benzodiazepines) at some point in their lifetime and

5.1 million have abused tranquilizers in the past year.

We have completed a 2-way pilot

crossover pharmacokinetic study in 9 healthy adult subjects of a single oral

dose of the Aversion® Technology benzodiazepine product candidate compared to