Attached files

| file | filename |

|---|---|

| 10-K - FORM 10-K - WINTRUST FINANCIAL CORP | c55863e10vk.htm |

| EX-10.09 - EX-10.09 - WINTRUST FINANCIAL CORP | c55863exv10w09.htm |

| EX-12.2 - EX-12.2 - WINTRUST FINANCIAL CORP | c55863exv12w2.htm |

| EX-12.1 - EX-12.1 - WINTRUST FINANCIAL CORP | c55863exv12w1.htm |

| EX-31.2 - EX-31.2 - WINTRUST FINANCIAL CORP | c55863exv31w2.htm |

| EX-32.1 - EX-32.1 - WINTRUST FINANCIAL CORP | c55863exv32w1.htm |

| EX-31.1 - EX-31.1 - WINTRUST FINANCIAL CORP | c55863exv31w1.htm |

| EX-99.1 - EX-99.1 - WINTRUST FINANCIAL CORP | c55863exv99w1.htm |

| EX-99.2 - EX-99.2 - WINTRUST FINANCIAL CORP | c55863exv99w2.htm |

| EX-21.1 - EX-21.1 - WINTRUST FINANCIAL CORP | c55863exv21w1.htm |

| EX-23.1 - EX-23.1 - WINTRUST FINANCIAL CORP | c55863exv23w1.htm |

2009—Writing Another Chapter

What Can Wintrust Do for You?

Wintrust Allows You to HAVE IT ALL.

Wintrust Allows You to HAVE IT ALL.

At Wintrust, we offer the products and technology of the big banks but pair it with exceptional

service, understanding and proper focus. It means you can Have It AllTM — a full slate of powerful

and sophisticated financial products and the local decision making and personal service that only a

group of community banks and specialty financial companies can offer.

service, understanding and proper focus. It means you can Have It AllTM — a full slate of powerful

and sophisticated financial products and the local decision making and personal service that only a

group of community banks and specialty financial companies can offer.

Retail Banking

| • | Footprint of 15 chartered banks and 78 facilities | ||

| • | Deposit Products | ||

| • | Home Equity & Installment Loans | ||

| • | Residential Mortgages |

Wealth Management

| • | Asset Management (Individual & Institutional) | ||

| • | Financial Planning | ||

| • | Brokerage | ||

| • | Retirement Plans (Business) | ||

| • | Trust & Estate Services (Corporate & Personal) | ||

| • | Life Insurance Premium Financing |

Commercial Lending

| • | Commercial & Industrial (Asset Based) Lending | ||

| • | Commercial Real Estate, Mortgages & Construction | ||

| • | Lines of Credit | ||

| • | Letters of Credit | ||

| • | Property & Casualty Insurance Premium Financing |

Treasury Management

| • | Retail & Wholesale Lockbox | ||

| • | On-Line Lockbox (iBusinessPay) | ||

| • | On-Line Banking & Reporting (iBusinessBanking) | ||

| • | Remote Deposit Capture (iBusinessCapture) | ||

| • | Merchant Card Program | ||

| • | Payroll Services (CheckMate) | ||

| • | ACH & Wire Transfer Services | ||

| • | International Banking Services |

Specialized Financial Services for:

| • | Building Management Companies | ||

| • | Condominium & Homeowner Associations | ||

| • | Insurance Agents & Brokers | ||

| • | Municipalities & School Districts | ||

| • | Physicians, Dentists & Other Medical Personnel | ||

| • | Temporary Staffing & Security Companies |

Contents

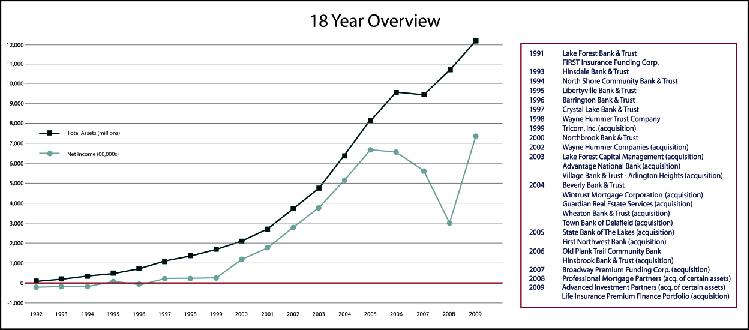

| Selected Financial Trends | ||

| Selected Financial Highlights | ||

| To Our Fellow Shareholders | ||

| Our Locations | ||

| Key Initiatives for 2010 | ||

| Form 10-K | ||

| Corporate Locations | ||

| Corporate Information |

We have always had a policy of presenting our goals, objectives, and financial results in an up

front manner to our shareholders. In this annual report, we are confirming our policy of

reporting thoroughly the financial results, accounting policies, and objectives of Wintrust

Financial Corporation and our operating subsidiaries.

Selected

Financial Highlights

| Years Ended December 31, | ||||||||||||||||||||

| 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

| (dollars in thousands, except per share data) | ||||||||||||||||||||

Selected Financial Condition Data (at end of year): |

||||||||||||||||||||

Total assets |

$ | 12,215,620 | $ | 10,658,326 | $ | 9,368,859 | $ | 9,571,852 | $ | 8,177,042 | ||||||||||

Total loans |

8,411,771 | 7,621,069 | 6,801,602 | 6,496,480 | 5,213,871 | |||||||||||||||

Total deposits |

9,917,074 | 8,376,750 | 7,471,441 | 7,869,240 | 6,729,434 | |||||||||||||||

Junior subordinated debentures |

249,493 | 249,515 | 249,662 | 249,828 | 230,458 | |||||||||||||||

Total shareholders’ equity |

1,138,639 | 1,066,572 | 739,555 | 773,346 | 627,911 | |||||||||||||||

Selected Statements of Operations Data: |

||||||||||||||||||||

Net interest income |

$ | 311,876 | $ | 244,567 | $ | 261,550 | $ | 248,886 | $ | 216,759 | ||||||||||

Net revenue(1) |

629,523 | 344,245 | 341,493 | 339,926 | 310,318 | |||||||||||||||

Net income |

73,069 | 20,488 | 55,653 | 66,493 | 67,016 | |||||||||||||||

Net income per common share — Basic |

2.23 | 0.78 | 2.31 | 2.66 | 2.89 | |||||||||||||||

Net income per common share — Diluted |

2.18 | 0.76 | 2.24 | 2.56 | 2.75 | |||||||||||||||

Selected Financial Ratios and Other Data: |

||||||||||||||||||||

Performance Ratios: |

||||||||||||||||||||

Net interest margin(2) |

3.01 | % | 2.81 | % | 3.11 | % | 3.10 | % | 3.16 | % | ||||||||||

Non-interest income to average assets |

2.78 | 1.02 | 0.85 | 1.02 | 1.23 | |||||||||||||||

Non-interest expense to average assets |

3.01 | 2.63 | 2.57 | 2.56 | 2.62 | |||||||||||||||

Net overhead ratio(3) |

0.23 | 1.60 | 1.72 | 1.54 | 1.39 | |||||||||||||||

Efficiency ratio (2)(4) |

54.44 | 73.00 | 71.05 | 66.94 | 63.97 | |||||||||||||||

Return on average assets |

0.64 | 0.21 | 0.59 | 0.74 | 0.88 | |||||||||||||||

Return on average common equity |

6.70 | 2.44 | 7.64 | 9.47 | 11.00 | |||||||||||||||

Average total assets |

$ | 11,415,322 | $ | 9,753,220 | $ | 9,442,277 | $ | 8,925,557 | $ | 7,587,602 | ||||||||||

Average total shareholders’ equity |

1,081,792 | 779,437 | 727,972 | 701,794 | 609,167 | |||||||||||||||

Average loans to average deposits ratio |

90.5 | % | 94.3 | % | 90.1 | % | 82.2 | % | 83.4 | % | ||||||||||

Common Share Data (at end of year): |

||||||||||||||||||||

Market price per common share |

$ | 30.79 | $ | 20.57 | $ | 33.13 | $ | 48.02 | $ | 54.90 | ||||||||||

Book value per common share |

$ | 35.27 | $ | 33.03 | $ | 31.56 | $ | 30.38 | $ | 26.23 | ||||||||||

Common shares outstanding |

24,206,819 | 23,756,674 | 23,430,490 | 25,457,935 | 23,940,744 | |||||||||||||||

Other Data (at end of year): |

||||||||||||||||||||

Leverage ratio |

9.3 | % | 10.6 | % | 7.7 | % | 8.2 | % | 8.3 | % | ||||||||||

Tier 1 capital to risk-weighted assets |

11.0 | 11.6 | 8.7 | 9.8 | 10.3 | |||||||||||||||

Total capital to risk-weighted assets |

12.4 | 13.1 | 10.2 | 11.3 | 11.9 | |||||||||||||||

Allowance for credit losses(5) |

$ | 101,831 | $ | 71,353 | $ | 50,882 | $ | 46,512 | $ | 40,774 | ||||||||||

Credit discounts on purchased loans(6) |

37,323 | — | — | — | — | |||||||||||||||

Total credit-related reserves |

139,154 | 71,353 | 50,882 | 46,512 | 40,774 | |||||||||||||||

Non-performing loans |

131,804 | 136,094 | 71,854 | 36,874 | 26,189 | |||||||||||||||

Allowance for credit losses to total loans(5) |

1.21 | % | 0.94 | % | 0.75 | % | 0.72 | % | 0.78 | % | ||||||||||

Total credit-related reserves to total loans (7) |

1.65 | 0.94 | 0.75 | 0.72 | 0.78 | |||||||||||||||

Non-performing loans to total loans |

1.57 | 1.79 | 1.06 | 0.57 | 0.50 | |||||||||||||||

Number of: |

||||||||||||||||||||

Bank subsidiaries |

15 | 15 | 15 | 15 | 13 | |||||||||||||||

Non-bank subsidiaries |

8 | 7 | 8 | 8 | 10 | |||||||||||||||

Banking offices |

78 | 79 | 77 | 73 | 62 | |||||||||||||||

| (1) | Net revenue is net interest income plus non-interest income. | |

| (2) | See Item 7, “Managements Discussion and Analysis of Financial Condition and Results of Operations — Non-GAAP Financial Measures/Ratios,” of the Company’s 2009 Form 10-K for a reconciliation of this performance measure/ratio to GAAP. | |

| (3) | The net overhead ratio is calculated by netting total non-interest expense and total non-interest income, annualizing this amount, and dividing by that period’s average total assets. A lower ratio indicates a higher degree of efficiency. | |

| (4) | The efficiency ratio is calculated by dividing total non-interest expense by tax-equivalent net revenues (less securities gains or losses). A lower ratio indicates more efficient revenue generation. | |

| (5) | The allowance for credit losses includes both the allowance for loan losses and the allowance for lending-related commitments. | |

| (6) | Represents the credit discounts on purchased life insurance premium finance loans. | |

| (7) | The sum of allowance for credit losses and credit discounts on purchased life insurance premium finance loans divided by total loans outstanding plus the credit discounts on purchased life insurance premium finance loans. |

| 2009 Annual Report | 3 | |

To Our Fellow Shareholders

Welcome to Wintrust Financial Corporation’s 2009 annual report. We thank you for being a

shareholder.

First, a Comment on Our Cover

Those of you who have been shareholders for a while have undoubtedly noticed that we cycle through

a stable of four cover colors – blue, green, maroon and black. We always go in that order.

For 2009, the color is black. From the view of our industry, this color appears to be a bit

ironic. If it was possible for an entire industry to be awash in red ink, it seemed as if the

banking and finance industries were during 2009.

Wintrust, on the other hand, ended the year profitably. In fact, while

some of our peers posted a second straight year of annual losses, Wintrust earned

net income of $73.1 million ($2.18 per diluted share), achieving 13 years of

consecutive profitability. So, while black may be inappropriate for our industry, it is more than

appropriate for your company.

Now, a Little Background

As we approached the writing of this year’s Shareholders’ Letter, it became apparent that each

year’s Annual Report is another chapter in an ongoing novel. Like a novel of any size, the

chapters of our story are divided into a few distinct parts. This is the fourth chapter of a part that

began in 2006, when we planned for the expected banking industry correction.

We believe the banking industry runs in cycles. In 2006, events unfolded to lead us to think a down

cycle was beginning. We knew property values couldn’t keep going up and bankers could not keep

making increasingly risky, low priced and poorly underwritten loans. At the same time, interest

rates dominated by inverted yield curves were an indicator of a down cycle. As good students of

history and custodians of your company, we stepped back, slowed our growth and waited.

The downturn was far worse than anyone could have predicted. Now, with 2009 behind us, we can

reflect on many of the problems that faced our economy and our industry.

Consider:

| • | The FDIC closed 140 banks nationwide in 2009, costing the FDIC’s deposit insurance fund $37 billion. Twenty-one of those banks were in Illinois. One was in Wisconsin. | ||

| • | Non-performing assets at banks nationwide increased more than 63% in 2009, totaling $330 billion, or 2.78% of all bank assets. | ||

| • | Among our peers, Chicago-based regional banks, we are unique in our level of profitability and measured, organic growth. | ||

| • | The housing market continued to trouble homeowners and lenders in the Midwest. Chicago area home values declined further in 2009. | ||

| • | The long rumored “other shoe,” commercial real estate, showed additional stress in 2009 with commercial occupancy rates declining and a corresponding drop in commercial real estate values. |

The Numbers

| In 2009, Wintrust was able to grow assets, deposits, and loans by double digit percentage increases. Management believes that given the tough banking environment of the past few years, and the performance of many other local banks, the Company is performing well, on a relative basis. |

| An overview summarizing our financial performance during the year follows: |

| • | Wintrust generated net income of $73.1 million in 2009 compared to $20.5 million in 2008, an increase of 257%. Once again, this is 13 consecutive years of profitability. | ||

| • | Earnings per diluted common share increased from $0.76 in 2008 to $2.18 in 2009. | ||

| • | Total assets grew to $12.2 billion as of December 31, 2009, an increase of $1.6 billion, or 15%, compared to a year ago. | ||

| • | Total deposits rose to $9.9 billion as of year-end 2009, an increase of $1.5 billion and total loans reached $8.4 billion, an increase of $790.7 million, compared to December 31, 2008. | ||

| • | Net revenue, which is net interest income and non-interest income, increased to $629.5 million in 2009 from $344.2 million in 2008. |

| 4 | Wintrust Financial Corporation | |

| • | Net interest margin for 2009 improved to 3.01%, compared to 2.81% in 2008. |

Although 2009 showed improvement in some

areas over 2008, we are not resting on our

laurels, and our results are not at the

level that the Company and shareholders

have come to expect.

Executing Our Plan in 2009

As stated earlier, we came into this part

of our story with a plan. The first few

chapters were about maintaining asset

quality, preserving customers and capital,

and protecting shareholders.

We maintained that if we did that properly,

we would be in the best position to start a

new chapter – a return to our true

character. But before we fully could do

that, we had to do four things in 2009:

| 1. | Increase core earnings. | |

| 2. | Reduce problem assets. | |

| 3. | Moderately grow both sides of the balance sheet (loans and deposits). | |

| 4. | Take advantage of market dislocations. |

By focusing on getting our credit house in order and increasing

core earnings to be able to take on future credit stress, we contended that we would end 2009

profitable, strong and well positioned to return

to our historic growth and acquisition patterns.

Increase Core Earnings

We believe that one of the keys to building long term value is to increase core earnings. Very

few things are as simple as they sound, and core earnings is no exception.

Core pre-tax earnings, or earnings before taxes, provision for credit losses, other real-estate

owned expenses and the bargain purchase gains, were $148 million for the full year of 2009 compared

to $90 million in 2008.

This increase was partially driven by the fact that our average cost of funds for 2009 was 102

basis points lower than 2008 as a result of a record low interest

rate environment and benefit we received from re-pricing maturing

certificates of deposit throughout 2009. A committed strategy of targeted relationship growth helped as well by allowing

us to grow customer relationships without necessarily offering an above market interest rate.

This is apparent in the significant growth of our transactional accounts (non-interest bearing

DDA and NOW) and our reduced reliance on Certificates of Deposit.

At the same time, our yield on earning assets, year over year, dropped only 81 basis points. So,

our net interest margin for the year increased by 20 basis points to 3.01% for 2009.

Increasing our core earnings makes it possible for us continue to pay dividends to our

shareholders. In January 2009 and July 2009, Wintrust’s Board of Directors approved semiannual cash

dividends of $0.18 and $0.09, respectively, per share of outstanding common stock. Reducing the

dividend in July 2009 resulted in the preservation of capital to continue to support the growth of

our business and weather the credit crisis. And on January 28, 2010, Wintrust announced that the

Company’s Board of Directors again approved a semi-annual cash dividend of $0.09 per share of

outstanding common stock which was paid on February 25, 2010.

A Peer Comparison of Chicago Commercial Banks

| Wintrust | Peer Group | |||||||

| Financial | Average | |||||||

Assets, in billions

|

$12.22 | $8.76 | ||||||

Deposits, in billions

|

$9.92 | $6.87 | ||||||

Loans, in billions

|

$8.43 | $6.07 | ||||||

Equity, in billions

|

$1.14 | $0.92 | ||||||

Net Income (Loss) – applicable to common shares, in millions

|

$53.51 | $(39.38) | ||||||

EPS

|

$2.18 | $(1.08) | ||||||

Loans to Deposits Ratio

|

85.00% | 88.40% | ||||||

Leverage Ratio

|

9.28% | 9.72% | ||||||

Tier 1 Capital to Risk Weighed Assets

|

11.00% | 12.28% | ||||||

Total Capital to Risk Weighed Assets

|

12.44% | 14.53% | ||||||

Non-performing Loans to Total Loans

|

1.57% | 4.47% | ||||||

Book Value per Common Share

|

$35.27 | $15.64 | ||||||

Peer Group includes local public companies with the following ticker symbols: FMBI, MBFI, PVTB,

and TAYC.

| 2009 Annual Report | 5 | |

Reduce Problem Assets

As bankers, this part is, by far, the least enjoyable. Because we pulled back in 2006 and

2007, we believe that we now have fewer problems than our peers. But we have had our share of credit

stress, as no one is “bigger than the market.”

We ended 2008 with $25.4 million in loans 90 days or more past due and $110.7 million in

non-accruing loans, giving us $136.1 million in non-performing loans, 1.79% of our loan portfolio.

By mid 2009, we had $24.3 million in loans 90 days or more past due and $213.9 million in

non-accruing loans, resulting in $238.2 million in non-performing loans, 3.14% of our loan

portfolio. By the end of 2009, thanks to the efforts of our commercial lenders and our Managed

Asset Division, we reduced our total non-performing loans more than $100 million, ending 2009 at

$131.8 million.

Although the balance of non-performing loans

improved, we are very cognizant of the volatility in and the fragile nature of the national and local

economies. As a result, some of our borrowers can experience severe difficulties and default suddenly

even if they have never been delinquent in loan payments. We believe that the current economic conditions

will continue to apply stress to the quality of our loan portfolio and cannot assure that we will be able to

continue to reduce our non-performing loans. The Company will continue to keep a close eye on our loan portfolio

and quickly identify and address any problems as they appear.

Moderately Grow Both Sides of the Balance Sheet

This goal is actually more complex than the eight words indicate. Anyone can grow loans and

deposits. As we’ve seen over the years, banks can aggressively grow one or the other by playing

with pricing. But that strategy does not bring in sustainable, long term relationships. The key is

to grow loans, deposits and relationships intelligently. Our goal is about controlled growth that

builds franchise value.

On the deposit side, it’s not about growing high rate CD and savings accounts. Instead we want to grow

customer households. In 2009, our community banks increased deposit households and accounts,

growing deposits by 18.4% ($1.54 billion) to more than $9.9 billion.

This includes substantial growth in our MaxSafe® Retail, MaxSafe® Treasury Management and Wayne

Hummer Insured Bank Deposits programs. As customers became more

and more concerned about protecting their savings, they became attracted to our accounts which

provide 15 times the typical FDIC protection (currently $3.75 million per titled account).

On the asset side, we saw similar, measured growth. Total loans grew $790.7 million (10%), to $8.4

billion, while assets grew $1.6 billion (15%) to $12.2 billion. These numbers, while very good,

do not illuminate the fact that our mortgage operations originated more than $4.7 billion in mortgages that

were sold to end investors and our premium finance company maintained approximately $600 million

in an off-balance sheet securitization facility.

Taking into account all loan originations, our community banks and specialty companies made more

than $10.3 billion in new and renewed loans in 2009. For a more detailed overview of Wintrust’s

loan mix, including a breakdown of Commercial Real Estate and Commercial Loans, please see the “Loan Portfolio and Asset Quality” discussion within the body of our Annual Report on Form 10-K.

Take Advantage of Market Dislocations

As expected, this part of the story is often the most fun. However, this vignette will not be

as interesting as some would like, as we decided that it was far more important to get the first

three points right. So, instead of going out and buying failed banks like some other banks did, we

first wanted to ensure our own house was in order.

With that said, we did still manage to take advantage of some extreme market dislocations. Our

acquisition of certain assets of

Professional Mortgage Partners (PMP) in December of 2008 was one of the first and proved to come

at a great time. The refinance boom in 2009 brought large volume increases and made Wintrust

Mortgage (along with our bank mortgage operations) one of the largest mortgage originators in

Greater Chicago.

| 6 | Wintrust Financial Corporation | |

Another of our successes came with personnel. Our community banks hired a number of commercial

bankers from competitors in 2009. Some came from large national banks that reorganized and alienated many of their top producers and others came from our

local peers. All came with the expertise and talent of our current commercial banking teams, as

well as solid customer followings and books of business. Wintrust is quickly becoming known as a

top place to work if you’re a commercial banker in Illinois or Wisconsin.

We’ve seen a similar migration with our wealth management units, with the hiring of additional

financial advisors, asset managers and trust officers in 2009. In some cases, we’ve even hired

entire teams from competitors, allowing us to quickly grow our wealth management business in

several local markets.

Our wealth management group also purchased certain liabilities and assets of Advanced Investment

Partners (AIP) in March. Rolled into Wayne Hummer Asset Management, AIP brought a talented team of

professionals with an impressive track record and a focus on tax-aware and socially responsible

investing.

Our largest success of 2009, of course, was our purchase of a life insurance premium finance

portfolio. In addition to

the $1 billion loan portfolio, increasing the diversity of the Company’s loan mix, at approximately a 30%

discount, this purchase added an experienced, fully staffed loan office in New Jersey. This staff

joined our previously established life insurance premium finance division within FIRST Insurance

Funding Corp. and made FIRST, we believe, the largest life insurance finance company in the nation.

What we did not do, however, was buy other banks. As we stated earlier, it was very important that

we put our own house in order first, before taking on someone else’s problems. This is not to say

that we didn’t look at a few FDIC-assisted transactions in the latter part of 2009. We will

continue to review these opportunities in 2010 and will bid on failed banks if it makes strategic

sense for the Company.

Starting a New Chapter in 2010

Like 2009, 2010 will be the next chapter in the part of a story that started in 2006.

Now, it is likely that this chapter could very well be the climax of this section, as we hope to

see Wintrust returning to is true character — growth and expansion. But, we are “not out of the

woods yet”. As stewards of your Company, we intend to maintain our vigilance in executing the plan

we have laid out.

| 2009 Annual Report | 7 | |

On the surface, our goals for 2010 look a lot like our goals for 2009:

| 1. | Calculated growth on both sides of the balance sheet (loans and deposits). | ||

| 2. | Continue to lower our cost of funds and raise our net interest margin. | ||

| 3. | Clean out problems as they arise. | ||

| 4. | Seek out market dislocations. |

But that’s the great thing about a good novel, the more you read, the more time you spend with the

characters and the plot, the more insight you get into them and the more complex they become.

Restarting the Growth Engine

For those of you who have been long-term shareholders, you can remember Wintrust’s true

personality — solid growth through de novo expansion and acquisition, with organic growth from

existing locations leading the way.

We expect 2010 to be a very opportunistic year for Wintrust. There are a number of areas around

Chicago and southern Wisconsin where we do not have locations. We will be looking to work with the

FDIC on some potential transactions and may even look at non-FDIC assisted deals where they make

sense. (Please see sidebar: “A Quick Note on FDIC Assisted Transactions.”)

Our mortgage, wealth management and specialty finance companies will also be on the look out for

acquisition partners to help them grow market share, move into new territory or enter new lines of

business. Any deal we look at will always have to be priced correctly and be financially prudent

for the Company.

Of course real growth from our existing infrastructure is vital to our overall success. Some of

that growth will be driven by our recently hired commercial loan officers and current commercial

banking teams, as well as our new loan office in downtown Chicago. Populated by some recent

“refugees” from other banks and some existing Wintrust commercial bankers, this office will allow

us to better target downtown companies and centers of influence.

Getting the Word Out

Those of you who live in the greater Chicago area, have probably heard the Wintrust brand

slowly enter the market. We started with our commercial marketing in 2007, pushing our combined

resources, highlighting the “Power of Wintrust” and labeling, for our commercial clients, each of

our banks as “a Wintrust Community Bank.”

In 2008, we started marketing MaxSafe®, “brought to you by your Wintrust Community Banks.” In late

2008 and 2009, we rebranded our mortgage operations into Wintrust Mortgage and marketed the company

throughout the area.

| 8 | Wintrust Financial Corporation | |

In 2010, we will do the same to our wealth management companies. Using the umbrella “a

Wintrust Wealth Management Company,” we will continue to market Wayne Hummer Investments, a

trusted 80 year-old brand. In order to better appeal to institutional customers, we will rename

our asset management unit to Wintrust Capital Management. Our trust company will also take on a

new name that best reflects its strength and heritage.

We also want to make sure that those hit hardest by these economic times know that they can

continue to count on their Wintrust Community Banks for fair and flexible banking solutions. We

will be increasing our outreach efforts by rolling out a number of reasonably priced loan products

for low and moderate income borrowers to turn to rather than the high priced alternatives, as well

as customized checking and savings products that allow the unbanked and under-banked to become part

of the financial system and reach their goals. Being community bankers means providing solutions

for everyone in our communities and we haven’t forgotten that.

Although we are starting to get the word out about Wintrust, our community bank branding has always

been unique. They are true community banks with local leadership, local staff, local boards of

directors and local decision making. Our structure has always given them more strength, flexibility

and resources than a typical community bank.

Eleven of the thirteen members of Wintrust’s Board of Directors, please see legend in the Corporate Information

section at the end of this report.

A Quick Note on FDIC Assisted Transactions

One of the most obvious (and publicly disturbing) symptoms of the current economic cycle is a

dramatic increase in the number of bank failures. The last time we saw an economic cycle like this

(the late 1980s — early 1990s) more than 2,000 banks failed nationally. 140 banks failed in 2009.

Banks fail for any number of reasons, though the most common reason usually centers on a

unmanageable amount of bad loans. As the FDIC seizes and closes these banks, they look for

partners to take over responsibility for the assets and deposits of the failed banks.

Purchasing a failed bank from the FDIC can be attractive to the purchasing bank. In many cases:

| • | The acquiring bank does not pay cash for the failed bank’s assets. It assumes the deposits and some other liabilities, and acquires loans and certain other assets, under terms negotiated with the FDIC. | ||

| • | FDIC transactions may be advantageous from a risk-based capital perspective. Depending on the loss sharing arrangement with the FDIC, loans in the acquired portfolio could have risk-based regulatory capital requirements significantly less than the requirement for similar originated loans. | ||

| • | The transactions, many times, are immediately accretive to the acquirer’s net income. |

However, these purchases can also carry risks to the acquiring bank.

| • | After a competitive bidding process, the FDIC usually picks the acquiring bank based on the bank’s willingness to accept risk on the failed bank’s loan portfolio. The bidder willing to take on the most risk frequently wins. | ||

| • | The acquiring bank carries the failed bank’s loans on its balance sheet and reports the failed bank’s (often substantial) non-performing loans with their own loan portfolio. | ||

| • | The acquiring bank does have to work and attempt to collect on any of the acquired non-performing loan portfolio. This usually requires substantial resources. | ||

| • | Based on the structure of the individual purchase, the acquiring bank may be required to make equity related payments to the FDIC, or make payments to the FDIC up to 10 years after the transaction, based on the performance of the acquired asset portfolio. |

As opportunities arise, please know that we have, and will review each carefully, making sure to

only choose those that are the best fit for our organization and offer the best overall value for

our shareholders.

| 2009 Annual Report | 9 | |

This approach will allow our banks to continue to operate as they always have, as true

community banks, while giving us the ability to tell businesses and wealth management prospects

what it means to work with a Wintrust company.

Returning to What We Do Best

In our 2008 report, we stated that we saw the mission of our Banks coming full circle. Our

mission has always been to offer our customers and neighbors a real alternative to the big banks

who believe their market dominance gives them the ability to charge excessive fees while skimping on

service.

We appear to be in an era when the only choices in some parts of the country are banks that are

“too big to fail” and too big to care or small banks with limited resources, limited capital and,

in 140 cases in 2009, limited lifespans.

Families and businesses in the Midwest have an alternative. Wintrust Community Banks give them the

best of both worlds — the products, technology and resources of the big banks paired with the

service and community focus of community banks. Our customers truly get to “Have It All.”

This starts with all of our outstanding employees, as they allow us to provide our core, key

differentiator: Service, Service, Service. Without them, our model would not work.

In addition, our structure and the talented leadership at each of the Wintrust companies has

positioned us to be one of the first ones to exit the current cycle, while allowing us to take

advantage of opportunities that arise.

However, it is important that we remember that we do not operate in a vacuum. The current economic

storm will continue for a while longer. High unemployment, declining real estate values and a

volatile stock market continue to trouble our customers and shake up the marketplace. But it’s just

this type of storm that reveals opportunities for those that have prepared for the storm and allows

customers to see where real strength resides. We believe that 2010 will be another opportunistic

year for Wintrust.

Thank you for being a shareholder. We hope to see you at our Annual Meeting on May 27, 2010 at

10:00 a.m. at the Deer Path Inn, located in downtown Lake Forest.

Sincerely,  Peter D. Crist Chairman |

Edward J. Wehmer President & Chief Executive Officer |

David A. Dykstra Senior Executive Vice President & Chief Operating Officer |

| 10 | Wintrust Financial Corporation | |

Key Initiatives for 2010

While we covered a number of our larger 2010 strategic initiatives in the Shareholders

Letter, there are a couple key areas that deserve further explanation.

Enhancing the Customer Experience

The success of all parts of our franchise relies on satisfied and engaged customers.

It is important that all of our banks and

subsidiaries understand that it’s not just the individual transactions that build the customer

experience but every interaction the customer has with us, whether in the bank, on the phone,

on-line or at an event.

Our focus remains on initiatives which bring more people into our locations and

position ourselves as the local financial experts. This year will see a significant

expansion of these efforts, including finance-specific events and seminars,

presentations for home-buyers, small business owners, families and

retirees, and covering a variety

of topics such as fraud prevention, identity protection, Roth IRA conversions, finance for

teenagers, and fixed income investing. “We’ll also use these events to continue our outreach to

the unbanked and underbanked with events and seminars focusing on understanding your credit score,

first time home buyers, financial literacy and credit repair.

Other events focus less on finance and more on customer engagement and loyalty. Our Junior Savers

and Platinum Adventures clubs are perfect examples. While primarily designed to teach children the

importance of saving, our Junior Saver families can count on a number of games, cookouts and other

family events throughout the course of the year to keep them coming to the bank. Our Junior Savers

club will be expanded in 2010 to include teenage customers, focusing on budgeting,

saving and investing with rewards centered around electronics and music.

Our Platinum Adventures customers rely on us for both financial knowledge and fun. One day,

they’ll attend a seminar on reverse mortgages or IRA distributions, the next they could be

attending a Broadway show downtown or practicing Brain Aerobics. Our Platinum Adventures clubs saw

good growth in 2009 and we expect to see further expansion in 2010.

Enhancing the customer experience should also lead to a big expansion of our on-line services. In early months of

2010, we will be rolling out mobile account alerts for all customers, as well as personal finance

management software (PFM). Available free of charge to our customers who use on-line banking, PFM

allows these customers to aggregate all their financial information in one place and make it easier to track

spending, set budgets and financial goals, and gain a clearer understanding of their complete

financial picture.

This year will also see an expansion of our banks’ on-line initiatives, including active use of

social media to engage customers and new web sites that will have tailored content for our retail

customers based on their current stage in life, as well as industry-specific portals for our

commercial and small business customers. We are also providing our small business customers with

their own on-line community, where they can look for opportunities and partnerships and get

advice.

Finally, we want to ensure that our customers are receiving the experience they want. While we have

always welcomed and asked for feedback from our customers, we are putting a more formal program in

place. Our customer feedback program for 2010 will include an on-line component at a “My Bank Idea”

section of our bank web sites, where customers can ask questions, present an idea, give praise or

pose a problem. This will be complemented by more traditional methods including response cards

within the banks and customer surveys.

Going Where the Business Is

The middle market business in our service area has seen a number of banks pull back from lending and reduce the

services they provide. Typically comprised of privately owned businesses, in a variety of

industries, with $10 million to $50 million in annual revenue, the middle market poses a tremendous

opportunity for the Company.

For about two years, we’ve touted to local businesses that they can “Have It All — Big Bank

Resources and Community Bank Service.” The commercial lenders across all our banks took this

message to heart as they pursued small and mid-market businesses across the Chicago suburbs and

southern

| 12 | Wintrust Financial Corporation | |

Wisconsin. Customers and prospects realized that Wintrust Community Banks offered businesses something unique — a best in class suite

of robust and flexible Treasury Management solutions, an experienced and

dedicated commercial, industrial and real estate lending team, and the customer

focus that only comes from working with a community bank.

In 2010, we’re expanding to downtown Chicago via a new loan office with commercial lenders coming

from a number of different national, regional and local banks, joined by some of our current

lenders. The downtown Wintrust Commercial Banking team, operating as a loan processing office of

North Shore Community Bank & Trust, will focus on middle market businesses and the firms that

influence them. We want to truly be Chicago’s business bank.

Expanding Our Niches

While we will always count on core loans and deposits to keep our franchise growing, we’ve

developed a number of specialties that help drive growth.

Due to the current economic conditions, commercial real estate can be a volatile and unpredictable

segment. Two of our niches are well positioned to take advantage of solid opportunities. Our

Community Advantage group, out of Barrington Bank & Trust, continues to

see opportunities with condominium, townhome and homeowner associations and

increased activity from management companies. Also, Wintrust Commercial Realty

Advisors has found new life as a lender to opportunistic commercial real estate

investors. These are smaller loans (generally less than $5 million) maintaining

low leverage and with appropriate rates and fees built into the deals.

Another opportunity has become apparent in the franchise area. Wintrust Franchise

Services, operating out of

Highland Park Bank & Trust, is a national lender to McDonald’s owner/ operators

and is seeing solid growth.

Now believed to be the largest life insurance premium finance lender in the

nation and one of the top property & casualty premium finance

companies, FIRST Insurance Funding Corp. continues to see growth opportunities thanks to industry

consolidation and FIRST’s superior products and service. The recent sale in 2010 of one of the

largest property & casualty premium finance companies in the nation will put even more volume into

play.

Not all of our niches are lending focused. To balance out some of this loan demand, our Treasury

Management and other units are always finding new deposit partnerships. Our wholesale MaxSafe®

product was successful for us in 2009 and can be tapped, as needed for additional liquidity, in

2010. Thanks to MaxSafe® and our local bank and personnel reputations,

Wintrust Government Funds is now one of the top providers of treasury management

and financial services to municipalities in our market areas.

Finally, Wintrust Association Services, operating out of St. Charles Bank &

Trust, has found another underserved market among Chicago’s trade associations

and other not-for-profit organizations. Offering full treasury management and

finance solutions to this market is a promising business opportunity and we count

the Illinois Restaurant Association and its Chicago Gourmet event among our

clients.

| 2009 Annual Report | 13 | |

| 14 | Wintrust Financial Corporation | |

Corporate Locations

Corporate Headquarters |

Wintrust Financial Corporation |

727 North Bank Lane |

Lake Forest, IL 60045 |

847-615-4096 |

Illinois Banking &

Wealth Management

Locations |

ALGONQUIN |

Algonquin Bank & Trust |

Wayne Hummer Wealth Management |

4049 W. Algonquin Rd. |

Algonquin, IL 60102 |

847-669-7500 |

ANTIOCH |

State Bank of The Lakes |

Wayne Hummer Wealth Management |

440 Lake St. |

Antioch, IL 60002 |

847-395-2700 |

ARLINGTON HEIGHTS |

Village Bank & Trust |

234 W. Northwest Hwy. |

Arlington Heights, IL 60004 |

847-670-1000 |

Village Bank & Trust |

150 E. Rand Rd. |

Arlington Heights, IL 60004 |

847-870-5000 |

Village Bank & Trust |

Wayne Hummer Wealth Management |

311 S. Arlington Heights Rd. |

Arlington Heights, IL 60005 |

847-483-6000 |

Village Bank & Trust |

1845 E. Rand Rd. |

Arlington Heights, IL 60004 |

847-483-6000 |

BARRINGTON |

Barrington Bank & Trust Company |

Wayne Hummer Wealth Management |

201 S. Hough St. |

Barrington, IL 60010 |

847-842-4500 |

Barrington Bank & Trust Company |

233 W. Northwest Hwy. |

Barrington, IL 60010 |

847-381-1715 |

BLOOMINGDALE |

Old Town Bank & Trust of Bloomingdale |

Wayne Hummer Wealth Management |

165 W. Lake St. |

Bloomingdale, IL 60108 |

630-295-9111 |

BUFFALO GROVE |

Buffalo Grove Bank & Trust |

200 N. Buffalo Grove Rd. |

Buffalo Grove, IL 60089 |

847-634-8400 |

CARY |

Cary Bank & Trust |

60 E. Main St. |

Cary, IL 60013 |

847-462-8881 |

CHICAGO |

Wayne Hummer Wealth Management -

HEADQUARTERS |

222 South Riverside Plaza |

28th Floor |

Chicago, IL 60606 |

312-431-1700 |

Beverly Bank & Trust Company |

Wayne Hummer Wealth Management |

10258 S. Western Ave. |

Chicago, IL 60643 |

773-239-2265 |

Beverly Bank & Trust Company |

1908 W. 103rd St. |

Chicago, IL 60643 |

773-239-2265 |

North Shore Community Bank & Trust Co. |

Wayne Hummer Wealth Management |

4343 W. Peterson Ave. |

Chicago, IL 60646 |

773-545-5700 |

CLARENDON HILLS |

Clarendon Hills Bank |

200 W. Burlington Ave. |

Clarendon Hills, IL 60514 |

630-323-1240 |

CRYSTAL LAKE |

Crystal Lake Bank & Trust Company |

70 N. Williams St. |

Crystal Lake, IL 60014 |

815-479-5200 |

Crystal Lake Bank & Trust Company |

27 N. Main St. |

Crystal Lake, IL 60014 |

Crystal Lake Bank & Trust Company |

1000 McHenry Ave. |

Crystal Lake, IL 60014 |

815-479-5715 |

DEERFIELD |

Deerfield Bank & Trust |

660 Deerfield Rd. |

Deerfield, IL 60015 |

847-945-8660 |

DOWNERS GROVE |

Community Bank of Downers Grove |

Wayne Hummer Wealth Management |

1111 Warren Ave. |

Downers Grove, IL 60515 |

630-968-4700 |

Community Bank of Downers Grove |

718 Ogden Ave. |

Downers Grove, IL 60515 |

630-435-3600 |

ELK GROVE VILLAGE |

Elk Grove Village Bank & Trust |

75 E. Turner Ave. |

Elk Grove Village, IL 60007 |

847-364-0100 |

FRANKFORT |

Old Plank Trail Community Bank |

20901 S. LaGrange Road |

Frankfort, IL 60423 |

815-464-6888 |

GENEVA |

St. Charles Bank & Trust Company |

2401 Kaneville Rd. |

Geneva, IL 60134 |

630-845-4800 |

GLEN ELLYN |

Glen Ellyn Bank & Trust |

Wayne Hummer Wealth Management |

500 Roosevelt Rd. |

Glen Ellyn, IL 60137 |

630-469-3000 |

GLENCOE |

North Shore Community Bank & Trust Co. |

362 Park Ave. |

Glencoe, IL 60022 |

847-835-1700 |

North Shore Community Bank & Trust Co. |

633 Vernon Ave. |

Glencoe, IL 60022 |

GRAYSLAKE |

State Bank of The Lakes |

Wayne Hummer Wealth Management |

50 Commerce Dr. |

Grayslake, IL 60030 |

847-548-2700 |

2009

Annual Report

|

||

GURNEE |

Gurnee Community Bank |

Wayne Hummer Wealth Management |

675 N. O’Plaine Rd. |

Gurnee, IL 60031 |

847-625-3800 |

HIGHLAND PARK |

Highland Park Bank & Trust |

1949 St. Johns Ave. |

Highland Park, IL 60035 |

847-432-9988 |

Highland Park Bank & Trust |

643 Roger Williams Ave. |

Highland Park, IL 60035 |

847-266-0300 |

HIGHWOOD |

Bank of Highwood – Fort Sheridan |

507 Sheridan Rd. |

Highwood, IL 60040 |

847-266-7600 |

HINSDALE |

Hinsdale Bank & Trust Company |

Wayne Hummer Wealth Management |

25 E. First St. |

Hinsdale, IL 60521 |

630-323-4404 |

Hinsdale Bank & Trust Company |

130 W. Chestnut |

Hinsdale, IL 60521 |

630-655-8025 |

HOFFMAN ESTATES |

Hoffman Estates Community Bank |

1375 Palatine Rd. |

Hoffman Estates, IL 60192 |

847-963-9500 |

Hoffman Estates Community Bank |

2497 W. Golf Rd. |

Hoffman Estates, IL 60169 |

847-884-0500 |

ISLAND LAKE |

Wauconda Community Bank |

229 E. State Rd. |

Island Lake, IL 60042 |

847-487-3777 |

LAKE BLUFF |

Lake Forest Bank & Trust Company |

103 E. Scranton Ave. |

Lake Bluff , IL 60044 |

847-615-4060 |

LAKE FOREST |

Lake Forest Bank & Trust Company |

Wayne Hummer Wealth Management |

727 N. Bank Ln. |

Lake Forest, IL 60045 |

847-234-2882 |

Lake Forest Bank & Trust Company |

780 N. Bank Ln. |

Lake Forest, IL 60045 |

847-615-4022 |

Lake Forest Bank & Trust Company |

911 S. Telegraph Rd. |

Lake Forest, IL 60045 |

847-615-4098 |

Lake Forest Bank & Trust Company |

Wayne Hummer Wealth Management |

810 S. Waukegan Rd. |

Lake Forest, IL 60045 |

847-615-4080 |

LAKE VILLA |

State Bank of The Lakes |

345 S. Milwaukee Ave. |

Lake Villa, IL 60046 |

847-265-0300 |

LIBERTYVILLE |

Libertyville Bank & Trust Company |

507 N. Milwaukee Ave. |

Libertyville, IL 60048 |

847-367-6800 |

Libertyville Bank & Trust Company |

201 E. Hurlburt Court |

Libertyville, IL 60048 |

847-247-4045 |

Libertyville Bank & Trust Company |

Wayne Hummer Wealth Management |

1200 S. Milwaukee Ave. |

Libertyville, IL 60048 |

847-367-6800 |

LINDENHURST |

State Bank of The Lakes |

2031 Grand Ave. |

Lindenhurst, IL 60046 |

847-356-5700 |

McHENRY |

McHenry Bank & Trust |

2205 N. Richmond Rd. |

McHenry, IL 60050 |

815-344-6600 |

McHenry Bank & Trust |

2730 W. Route 120 |

McHenry, IL 60050 |

815-344-5100 |

MOKENA |

Old Plank Trail Community Bank |

Wayne Hummer Wealth Management |

20012 Wolf Rd. |

Mokena, IL 60448 |

708-478-4447 |

MUNDELEIN |

Mundelein Community Bank |

1110 W. Maple Ave. |

Mundelein, IL 60060 |

847-837-1110 |

NEW LENOX |

Old Plank Trail Community Bank |

Wayne Hummer Wealth Management |

280 Veterans Pkwy. |

New Lenox, IL 60451 |

815-485-0001 |

NORTH CHICAGO |

North Chicago Community Bank |

1801 Sheridan Rd. |

North Chicago, IL 60064 |

847-473-3006 |

NORTHBROOK |

Northbrook Bank & Trust Company |

1100 Waukegan Rd. |

Northbrook, IL 60062 |

847-418-2800 |

Northbrook Bank & Trust Company |

875 Sanders Rd. |

Northbrook, IL 60062 |

847-418-2850 |

NORTHFIELD |

Northview Bank & Trust |

Wayne Hummer Wealth Management |

245 Waukegan Rd. |

Northfield, IL 60093 |

847-446-0245 |

Northview Bank & Trust |

1751 Orchard Ln. |

Northfield, IL 60093 |

847-441-1751 |

PALATINE |

Palatine Bank & Trust |

Wayne Hummer Wealth Management |

110 W. Palatine Rd. |

Palatine, IL 60067 |

847-963-0047 |

RIVERSIDE |

Riverside Bank |

17 E. Burlington |

Riverside, IL 60546 |

708-447-3222 |

| Wintrust Financial Corporation | ||

ROSELLE |

Advantage National Bank |

1350 W. Lake St. |

Roselle, IL 60172 |

630-529-0100 |

SKOKIE |

North Shore Community Bank & Trust Co. |

7800 Lincoln Ave. |

Skokie, IL 60077 |

847-933-1900 |

SPRING GROVE |

State Bank of The Lakes |

1906 Holian Dr. |

Spring Grove, IL 60081 |

815-675-3700 |

ST. CHARLES |

St. Charles Bank & Trust Company |

411 West Main St. |

St. Charles, IL 60174 |

630-377-9500 |

VERNON HILLS |

Vernon Hills Bank & Trust |

Wayne Hummer Wealth Management |

1101 Lakeview Parkway |

Vernon Hills, IL 60061 |

847-247-1300 |

WAUCONDA |

Wauconda Community Bank |

495 W. Liberty St. |

Wauconda, IL 60084 |

847-487-2500 |

WESTERN SPRINGS |

The Community Bank of Western Springs |

Wayne Hummer Wealth Management |

1000 Hillgrove Ave. |

Western Springs, IL 60558 |

708-246-7100 |

WHEATON |

Wheaton Bank & Trust Company |

211 S. Wheaton Ave. |

Wheaton, IL 60187 |

630-690-1800 |

WILLOWBROOK |

Community Bank of Willowbrook |

6262 S. Route 83 |

Willowbrook, IL 60527 |

630-920-2700 |

WILMETTE |

North Shore Community Bank & Trust Co. |

Wayne Hummer Wealth Management |

1145 Wilmette Ave. |

Wilmette, IL 60091 |

847-853-1145 |

North Shore Community Bank & Trust Co. |

Wayne Hummer Wealth Management |

720 12th St. |

Wilmette, IL 60091 |

North Shore Community Bank & Trust Co. |

351 Linden Ave |

Wilmette, IL 60091 |

WINNETKA |

North Shore Community Bank & Trust Co. |

576 Lincoln Ave. |

Winnetka, IL 60093 |

847-441-2265 |

Wisconsin Banking &

Wealth Management

Locations |

APPLETON |

Wayne Hummer Wealth Management |

200 East Washington Street |

Appleton, WI 54911 |

920-734-1474 |

DELAFIELD |

Town Bank of Delafield |

400 Genesee St. |

Delafield, WI 53018 |

262-646-6888 |

ELM GROVE |

Town Bank of Elm Grove |

13150 Watertown Plank Rd. |

Elm Grove, WI 53122 |

262-789-8696 |

HARTLAND |

Town Bank |

Wayne Hummer Wealth Management |

850 W. North Shore Dr. |

Hartland, WI 53029 |

262-367-1900 |

MADISON |

Town Bank of Madison |

10 W. Mifflin St. |

Madison, WI 53703 |

608-282-4840 |

WALES |

Town Bank of Wales |

200 W. Summit Ave. |

Wales, WI 53183 |

262-968-1740 |

FIRST Insurance

Funding Corp. |

450 Skokie Blvd., Suite 1000 |

Northbrook, IL 60062 |

847-374-3000 |

FIRST Life Funding |

101 Hudson Street, 35th Floor |

Jersey City, NJ 07302 |

201-332-7349 |

Broadway Premium

Funding Corporation |

1747 Veterans Memorial Highway |

Suite 22 |

Islandia, NY 11749 |

212-791-7099 |

Tricom, Inc. of

Milwaukee |

N48 W16866 Lisbon Road |

Menomonee Falls, WI 53051 |

262-509-6200 |

Wintrust Mortgage

Corporation |

Headquarters |

1 South 660 Midwest Rd., Suite 100 |

Oakbrook Terrace, Illinois 60181 |

630-916-9299 |

Branch Offices |

Phoenix, AZ |

Denver, CO |

Madison, GA |

Barrington, IL |

Champaign, IL |

Chicago, IL |

Downers Grove, IL |

Elmhurst, IL |

Frankfort, IL |

Geneva, IL |

Glen Ellyn, IL |

Mokena, IL |

Naperville, IL |

Northbrook, IL |

Northfield, IL |

Oakbrook Terrace, IL |

Schaumburg, IL |

Tinley Park, IL |

Willowbrook, IL |

Crown Point, IN |

Overland Park, KS |

Louisville, KY |

Hanover, MD |

Pataskala, OH |

Madison, WI |

2009 Annual Report

|

||

Corporate Information

Directors

Peter D. Crist (Chairman)

Bruce K. Crowther

Joseph F. Damico

Bert A. Getz, Jr.

H. Patrick Hackett, Jr.

Scott K. Heitmann

Charles H. James, III

Albin F. Moschner

Thomas J. Neis

Christopher J. Perry

Hollis W. Rademacher

Ingrid S. Stafford

Edward J. Wehmer

Peter D. Crist (Chairman)

Bruce K. Crowther

Joseph F. Damico

Bert A. Getz, Jr.

H. Patrick Hackett, Jr.

Scott K. Heitmann

Charles H. James, III

Albin F. Moschner

Thomas J. Neis

Christopher J. Perry

Hollis W. Rademacher

Ingrid S. Stafford

Edward J. Wehmer

Public Listing and Market Symbol

The

Company’s Common Stock is traded on The NASDAQ Global Select Market® under the symbol WTFC.

Website Location

The

Company maintains a financial relations internet website at the following location: www.wintrust.com

Annual Meeting of Shareholders

May 27, 2010

10:00 a.m.

Deer Path Inn

255 E. Illinois Road

Lake Forest, Illinois 60045

10:00 a.m.

Deer Path Inn

255 E. Illinois Road

Lake Forest, Illinois 60045

Form 10-K

The Annual Report on Form 10-K to the Securities and

Exchange Commission is contained herein this document.

The information is also available on the Internet at the Securities and Exchange Commission’s website. The address for the

web site is: http://www.sec.gov.

Transfer Agent

Illinois Stock Transfer Company

209 West Jackson Boulevard

Suite 903

Chicago, Illinois 60606

Telephone: 312-427-2953

Facsimile: 312-427-2879

209 West Jackson Boulevard

Suite 903

Chicago, Illinois 60606

Telephone: 312-427-2953

Facsimile: 312-427-2879

Wintrust Board of Directors Legend

Page 8, (pictured from left to right): Charles H. James, III, Bert A. Getz, Jr., Joseph F. Damico,

Christopher J. Perry, Ingrid S. Stafford, Bruce K. Crowther, and Scott K. Heitmann. Page 9: H.

Patrick Hackett, Jr., Thomas J. Neis, Hollis W. Rademacher, and

Albin F. Moschner. Page 10: Peter D. Crist and Edward J. Wehmer.

| Wintrust Financial Corporation | ||