Attached files

| file | filename |

|---|---|

| 8-K - ANR 8K 03-01-2010 - Alpha Natural Resources, Inc. | anr8k03012010.htm |

EXHIBIT

99.1

1

Investor

Presentation

February/March,

2010

2

Forward

Looking Statements

Statements in this

presentation which are not statements of historical fact are

“forward-looking

statements” within the Safe Harbor provision of the Private Securities Litigation Reform Act of 1995.

Such statements are not guarantees of future performance. Many factors could cause our actual

results, performance or achievements, or industry results, to be materially different from any future

results, performance or achievements expressed or implied by such forward looking-statements.

These factors are discussed in detail in our Annual Report on Form 10-K, Quarterly Reports on

Form 10-Q and in our other filings with the SEC. We make forward-looking statements based on

currently available information, and we assume no obligation to update the statements made today

or contained in our Annual Report or other filings due to changes in underlying factors, new

information, future developments, or otherwise, except as required by law.

statements” within the Safe Harbor provision of the Private Securities Litigation Reform Act of 1995.

Such statements are not guarantees of future performance. Many factors could cause our actual

results, performance or achievements, or industry results, to be materially different from any future

results, performance or achievements expressed or implied by such forward looking-statements.

These factors are discussed in detail in our Annual Report on Form 10-K, Quarterly Reports on

Form 10-Q and in our other filings with the SEC. We make forward-looking statements based on

currently available information, and we assume no obligation to update the statements made today

or contained in our Annual Report or other filings due to changes in underlying factors, new

information, future developments, or otherwise, except as required by law.

3

Coal

Industry Themes - 2010

v Strong met coal

pricing driven by growing

Asian demand

Asian demand

v Met coal tightness

increasing in the Atlantic

basin as economic recovery continues

basin as economic recovery continues

v Significant recent

utility inventory draw - U.S.

thermal market positioned to strengthen

thermal market positioned to strengthen

v Future worldwide

demand for thermal coal

anticipated to strain seaborne supply

anticipated to strain seaborne supply

4

4

Strong

Market Outlook

5

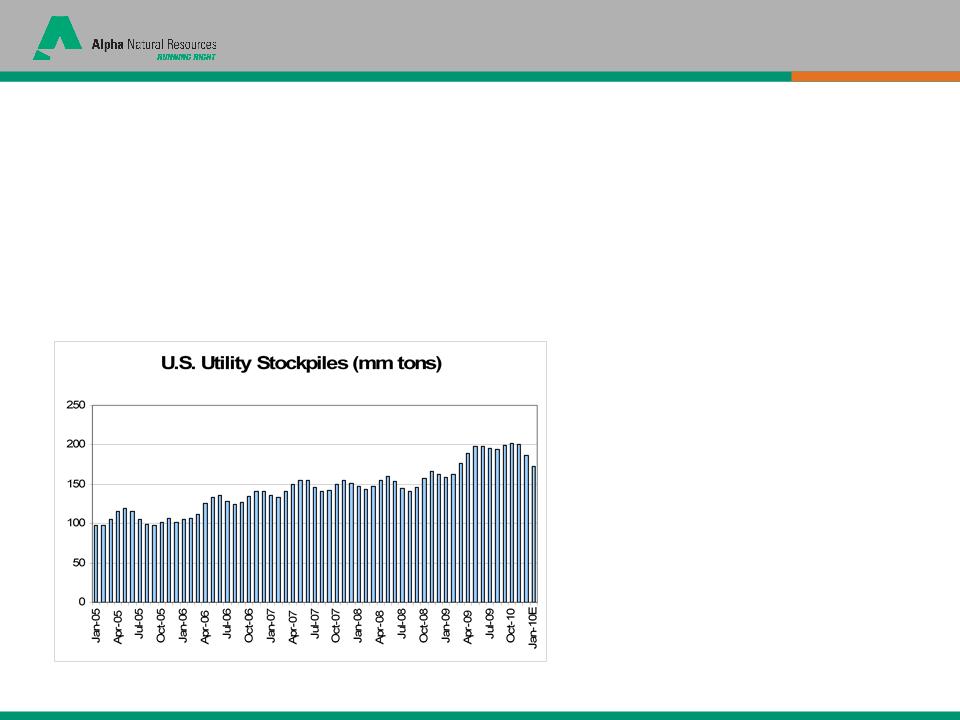

U.S.

Thermal Coal Market Recovering

— Severe

winter weather caused utility inventories to fall by an estimated 30+MTs

since

Nov.

Nov.

— U.S.

thermal coal production unlikely to expand in 2010 and may decline

further

— Economic

recovery likely to drive increased industrial electricity demand

— Forward

natural gas prices indicate that some fuel switching should reverse in

2010

— Global

recovery and weak dollar should drive increasing net exports from the

U.S.

— Crossover

met coal may further reduce available supply in the U.S.

— New

coal-fired generation will increase demand

SOURCE:

DOE NETL, Internal Analysis, Genscape

Given

the rapid drawdown in utility

inventories in the opening weeks of

2010, forecasts of normal inventories

by late 2010 may prove conservative

inventories in the opening weeks of

2010, forecasts of normal inventories

by late 2010 may prove conservative

6

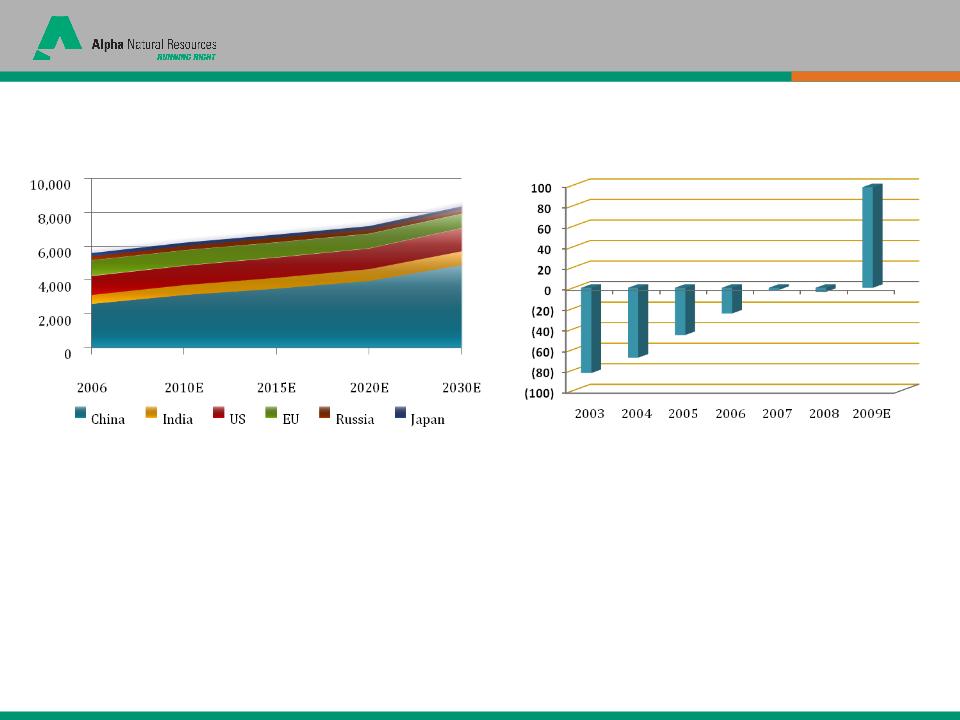

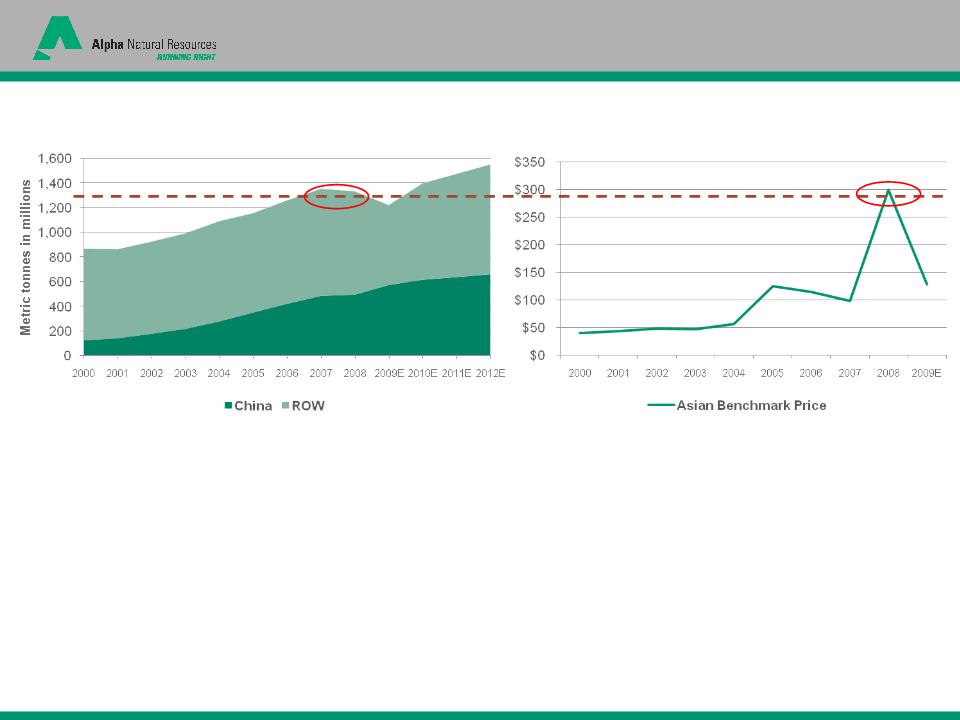

Robust Global Coal Market: Asia Is Key

Global

demand growth, driven primarily by China, is staggering

Global

Coal Consumption (mm tons)

Chinese

Net Imports (mm tonnes)

SOURCE:

Energy Information Administration, International Energy Outlook; International

Energy Agency, World Energy Outlook; Internal Analysis

— Among the countries

representing most of the world’s coal use, coal consumption is forecast to

increase

35% in 20 years (2010 - 2030)

35% in 20 years (2010 - 2030)

— China is forecast to

account for over 80% of this growth of more than 2BTs in annual demand,

increasing

its annual coal consumption by nearly 60% between 2010 and 2030

its annual coal consumption by nearly 60% between 2010 and 2030

— China’s rapid move

to net importer is a well-documented game changer

— India’s coal

consumption is forecast to rise nearly 40% between 2010 and 2030

— Considering that the

U.S. produces ~1BTs per

year…where will the coal come from to satisfy this

incremental increase in demand?

incremental increase in demand?

7

China & India Rely on Coal-fired Electricity

2010E:

80% coal-fired

2030E:

77% coal-fired

2010E:

66% coal-fired

2030E:

69% coal-fired

(Indian

thermal coal imports have grown at 13% CAGR from 1990 - 2008)

Source: IEA;

Booz & Company analysis

8

Source: Wood

Mackenzie; Booz & Company analysis

China

= 14.8% CAGR

ROW

= 1.5% CAGR

Scarcity of

Metallurgical Coal

Global

Steel Production

Metallurgical Coal

Pricing (US$)

— As global steel

production has grown, metallurgical coal has come to be viewed as a

scarce

and differentiated product

and differentiated product

— When worldwide

production of steel exceeds 1.3 billion tons, the supply of met coal

becomes

strained and incremental pricing can rise sharply as was seen in 2008

strained and incremental pricing can rise sharply as was seen in 2008

— While new projects

are planned in places like Mozambique, Mongolia and Siberia, and

additional projects are planned in Australia, all must overcome various infrastructure

limitations or political challenges

additional projects are planned in Australia, all must overcome various infrastructure

limitations or political challenges

— Supply constraints

are likely to persist for several years

9

China

Driving Worldwide Met Demand

Chinese

Growth is Permanently Changing Global Seaborne Met Coal Trading

Dynamics

— Chinese crude steel

production increased an estimated 14% in 2009, and China now produces nearly

half

of the world’s steel

of the world’s steel

— China imported 34M

tonnes of Met coal in 2009, or ~15% of the World’s seaborne supply

— Chinese demand will

be satisfied primarily by Australia, which is near its current export

capacity

— Availability of

seaborne coking coal, which totaled an estimated 240M tonnes in 2008, will be

constrained

by the growth of Chinese imports

by the growth of Chinese imports

— Worldwide steel

production is estimated to be on an annual pace of greater than1.3B tonnes, with

over

600M tonnes expected from China alone in 2010

600M tonnes expected from China alone in 2010

SOURCE:

China’s National Bureau of Statistics, Chinese Customs, Macquarie, Internal

Analysis

10

Met Demand Accelerating in Atlantic Basin

Met

Coal Demand in the Atlantic Basin Should Increase As Developed

Economies Recover and Steel Production Ramps Up

Economies Recover and Steel Production Ramps Up

*

ANR is the leading U.S. supplier & exporter of metallurgical coal with

13-14MTPA export capacity*

— Domestic producers’

rapid response to the recession in 2009 drove U.S. service center inventories to

26-

yr. lows, despite anemic demand for steel—restocking is now occurring

yr. lows, despite anemic demand for steel—restocking is now occurring

— U.S. steel

production capacity utilization has increased to the mid-60% range, up from ‘09

lows in the 30s

— The combination of

strong Chinese demand and increasing steel capacity utilization in the U.S. and

the

rest of the world should drive accelerating Atlantic basin met coal demand in 2010 and beyond

rest of the world should drive accelerating Atlantic basin met coal demand in 2010 and beyond

SOURCE:

Metals Service Center Institute, American Iron and Steel Institute, Macquarie,

Internal Analysis

11

Trends

in Seaborne Trading Patterns

Decreasing

trend

Increasing

trend

Spare

capacity provides opportunity to ramp exports to meet global demand

As

Asian Demand Absorbs Seaborne Supply, The Atlantic Basin Will Increasingly Rely

on U.S. Coals

12

12

Investment

Highlights

13

2009

Year-end Reserves = 2.3 BTs

2009

Revenue Mix by Coal Type

Following

our merger on July 31, 2009, Alpha has delivered consistent

execution

demonstrating the benefit of the company’s enhanced scale and diversification.

demonstrating the benefit of the company’s enhanced scale and diversification.

*ANR

is arguably the most regionally diversified producer in the U.S.

today*

(1) Third

quarter 2009 amounts previously reported have been adjusted by $3.2 million,

$0.03 per share, due to reduced expense.

14

High

Margin Longwall Mining in NAPP

— Alpha operates two

low-cost, high-margin longwall mines in the Pittsburgh #8 seam:

Cumberland and Emerald

Cumberland and Emerald

— In 4Q09, the

longwalls accounted for 3M tons, or 45% of Eastern steam coal shipments, and

on

a pro forma basis these mines shipped 12.1M tons in 2009

a pro forma basis these mines shipped 12.1M tons in 2009

— Cost of coal sales

were the low to mid-$30s per ton for 4Q09 and pro forma full year 2009,

while

average realizations were in the mid-$50s

average realizations were in the mid-$50s

— Even in the

relatively weak thermal coal market of 2009, these mines contributed

approximately

$20/ton of gross coal margins, contributing pro forma total margin of $230 to $240 million

$20/ton of gross coal margins, contributing pro forma total margin of $230 to $240 million

— Due to higher

average realizations in the committed and priced book of business, per ton

coal

margins in 2010 are expected to increase despite higher anticipated per ton costs

margins in 2010 are expected to increase despite higher anticipated per ton costs

*

Longwall mines are highly profitable compared to other Eastern steam

operations*

15

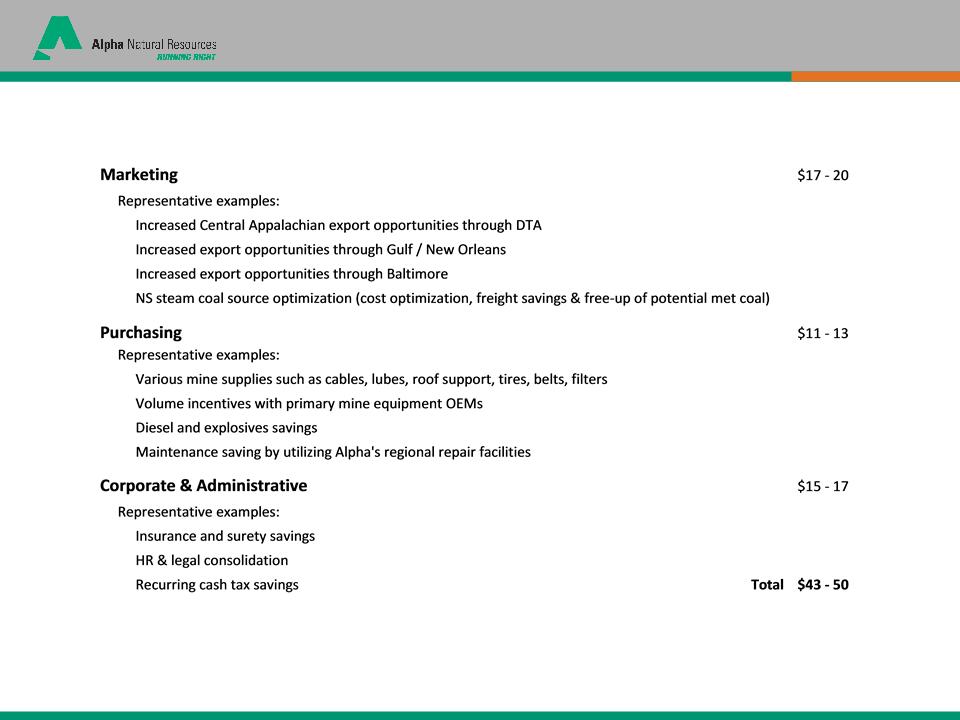

Pacing to Meet or Exceed Synergy Target

Additional

upside possible, primarily driven by additional blending and

optimization opportunities depending on future market conditions

optimization opportunities depending on future market conditions

Annual

net synergies conservatively estimated at $45 million at full

run-rate anticipated to be achieved by mid-year 2010

run-rate anticipated to be achieved by mid-year 2010

16

Consistent History of Positive Cash Flow

Note: Pro

forma capex for 2008 and 2009 includes Lease-By-Application (LBA) bonus bid

payments of $36.1 million each year.

FCF =

Operating cash flow less capex

17

Excellent Liquidity

and Low Leverage

Note: LTM data

as of 12/31/09

(1) LTM combined pro forma Adjusted EBITDA for the fiscal year ended December 31, 2009

(1) LTM combined pro forma Adjusted EBITDA for the fiscal year ended December 31, 2009

Leverage

of approximately 1.2x debt/Adjusted EBITDA and liquidity of approximately $1.1

billion

|

($

millions)

|

Maturity

|

|

As

of

12/31/09 |

|

|

|

|

|

|

|

|

$650mm

Revolving Credit Facility

|

July,

2011

|

|

$0

|

|

|

Term Loan

A

|

July,

2011

|

|

285

|

|

|

2.375%

Convertible Notes

|

April,

2015

|

|

288

|

|

|

7.25% Senior

Unsecured Bonds

|

August,

2014

|

|

298

|

|

|

|

Total

Debt

|

|

|

$871

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Liquidity

and Credit Statistics

|

|

|

|

|

|

Cash &

Equivalents and marketable

securities |

|

|

$584

|

|

|

Revolver

|

|

|

650

|

|

|

Accounts

Receivable Securitization Facility

|

|

|

150

|

|

|

Less: Letters

of Credit Outstanding

|

|

|

(258)

|

|

|

|

Total

Potential Liquidity

|

|

|

$1,126

|

|

|

|

|

|

|

|

Total Debt /

LTM EBITDA

|

|

|

1.2x

|

|

|

|

|

|

|

|

|

LTM Adjusted

EBITDA1

|

|

|

$709

|

|

18

A Leader in the Domestic Coal Industry

Eastern

Coal Operations

Illinois

Basin

Western

Coal Operations

|

Production capacity

|

55.0

|

|

2009

Shipments

|

50.1

|

|

Reserves

|

709

|

|

Reserves

|

26

|

|

Production

Capacity

|

42.0

|

|

2009

Shipments

|

36.0

|

|

Reserves

|

1579

|

Note: Figures

pro forma as of 12/31/09

Strength,

Scale, Diversification

19

(2)CLD revenue, tons

sold and EBITDA as reported for the 12 months ended 12/31/08

(3)JRCC revenue, tons

sold and EBITDA as reported for the twelve

months ended 09/30/09

Market

Capitalization1

($

in billions)

LTM

12/31/09 Tons Sold 2

3 (in

millions)

Peer

Group Comparisons

20

|

Powder

River Basin

|

||

|

Wyoming

Operations

|

Expansion

(MM tons/yr)

|

Capacity

|

|

Truck/shovel

expansion

|

10

|

65

MTPY

|

|

Belle

Ayr LBA

|

200

Million Tons

|

2011

|

|

Central

Appalachia

|

||

|

Mine

|

Resource

Description

|

Production

|

|

Deep

Mine #41

|

~

70 MM Ton Reserve

|

1.0

- 1.2 MTPY (metallurgical)

|

|

Harts

Creek/Atenville

|

~

120 MM Ton Reserve

|

2

- 3 MTPY (metallurgical potential)

|

|

Northern

Appalachia

|

||

|

Mine

|

Resource

Description

|

Production

|

|

Foundation

- longwall

|

~

420 MM Ton Reserve

|

7

- 14 MTPY Pitt #8 (+ Sewickley)

|

|

Freeport

- CM

|

~

68 MM Ton Reserve

|

2

- 3 MTPY (metallurgical)

|

|

Coal

Gas Recovery

|

||

|

Location

|

Resource

Description

|

Production

|

|

CBM

|

~

100-200 Bcf Resource

|

~

5,000 Salable Mcf/Day (current)

|

|

Marcellus

acreage

|

~

18,000 Acres

|

Entered

into JV with Rice Energy 2010

|

Organic

Growth Opportunities

21

• 50/50 Joint Venture

with Rice Energy, LP

• Alpha controls

~18,000 acres of Marcellus in

Greene and Washington Counties of Pennsylvania

Greene and Washington Counties of Pennsylvania

• Initial phase

underway, currently drilling the first of

four wells planned for 2010

four wells planned for 2010

• Each partner

committing acreage and cash

• Total phase 1

capital anticipated to be less than

$20 million

$20 million

• JV potential to

develop ~100 wells in the Marcellus

• Separately, Alpha’s

CBM gas processing plant

expanding from capacity of 5,000 MCF/day to

10,000 MCF/day

expanding from capacity of 5,000 MCF/day to

10,000 MCF/day

Unconventional Gas

Development

22

Summary

of Recent Guidance

NOTES:

1. Based on

committed and priced coal shipments as of February 8, 2010.

2. Eastern

shipments in 2010 and 2011 include an estimated 2.0 to 3.0 million tons of

brokered coal per year.

3. As of

February 8, 2010, compared to the midpoint of shipment guidance

range.

4. In 2010,

committed and un-priced Eastern tons include approximately 1.8 million tons of

met coal subject to market pricing, approximately 0.2 million tons of steam coal

subject to market

pricing, and 0.5 million tons of steam coal subject to collared pricing with an average pricing range of $65.00 to $76.00 per ton. In 2011, committed and unpriced Eastern tons include

approximately 5.9 million tons of met coal subject to market pricing, approximately 3.3 million of steam coal subject to market pricing, approximately 2.9 million tons of steam coal subject to

collared pricing with an average pricing range of $50.00 to $62.00 per ton, and legacy contracts covering approximately 0.4 million tons of steam coal subject to average indexed pricing

estimated at $69.21 per ton.

pricing, and 0.5 million tons of steam coal subject to collared pricing with an average pricing range of $65.00 to $76.00 per ton. In 2011, committed and unpriced Eastern tons include

approximately 5.9 million tons of met coal subject to market pricing, approximately 3.3 million of steam coal subject to market pricing, approximately 2.9 million tons of steam coal subject to

collared pricing with an average pricing range of $50.00 to $62.00 per ton, and legacy contracts covering approximately 0.4 million tons of steam coal subject to average indexed pricing

estimated at $69.21 per ton.

Guidance

(in millions, except

per-ton and percentage amounts)

|

|

2010

|

2011

|

|

Average

per Ton Sales Realization on

Committed and Priced Coal Shipments1 |

|

|

|

West

|

$10.93

|

$11.93

|

|

Eastern

Steam

|

$65.54

|

$67.03

|

|

Eastern

Met

|

$104.63

|

$123.97

|

|

Coal

Shipments2

|

81.0 -

89.0

|

82.0 -

94.0

|

|

West

|

47.0 -

50.0

|

48.0 -

52.0

|

|

Eastern

Steam

|

23.0 -

26.0

|

23.0 -

28.0

|

|

Eastern

Met

|

11.0 -

13.0

|

11.0 -

14.0

|

|

Committed

and Priced (%)3

|

92%

|

59%

|

|

West

|

100%

|

77%

|

|

Eastern

Steam

|

93%

|

44%

|

|

Eastern

Met

|

62%

|

15%

|

|

Committed

and Un-priced (%)4

|

3%

|

14%

|

|

West

|

0%

|

0%

|

|

Eastern

Steam

|

3%

|

26%

|

|

Eastern

Met

|

15%

|

47%

|

|

West

- Cost of Coal Sales per Ton

|

$8.30 -

$8.90

|

|

|

East

- Cost of Coal Sales per Ton

|

$54.00

-

$57.00 |

|

|

Selling,

General & Administrative

Expense |

$150 -

$165

|

|

|

Depletion,

Depreciation &

Amortization |

$370 -

$390

|

|

|

Interest

Expense

|

$70 -

$80

|

|

|

Capital

Expenditures

|

$340 -

$390

|

|

23

Recent

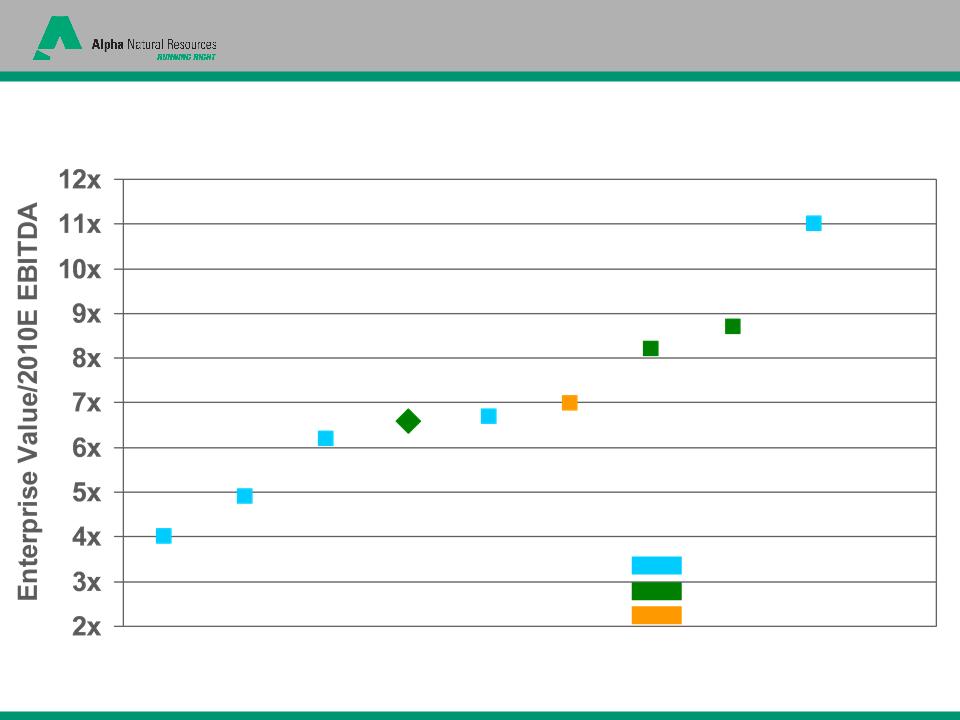

Valuation Comparison 2/19/10

Notes:

Market data and First Call consensus 2010 EBITDA estimates as of

2/19/10

< 50

MM TPY, regional

> 50

MM TPY, diversified

> 50

MM TPY, regional

Compelling Relative

Valuation

ANR

24

Coal

Industry Themes

v Strong met coal

pricing driven by growing

Asian demand

Asian demand

v Met coal tightness

increasing in the Atlantic

basin as economic recovery continues

basin as economic recovery continues

v Significant utility

inventory draw - U.S.

thermal market positioned to strengthen

thermal market positioned to strengthen

v Future worldwide

demand for thermal coal

anticipated to strain seaborne supply

anticipated to strain seaborne supply

ü ANR

is the largest supplier of met coal in the

U.S. and anticipates sales into Asia in 2010

U.S. and anticipates sales into Asia in 2010

ü ANR

is the largest exporter of met coal with 13

-14 MTs of export terminal capacity

-14 MTs of export terminal capacity

ü ANR’s

operations in NAPP, CAPP and PRB

can respond quickly to increased demand

can respond quickly to increased demand

ü Low-cost

production and export capacity

enable ANR to participate in global thermal

demand

enable ANR to participate in global thermal

demand

25

25

Appendices

26

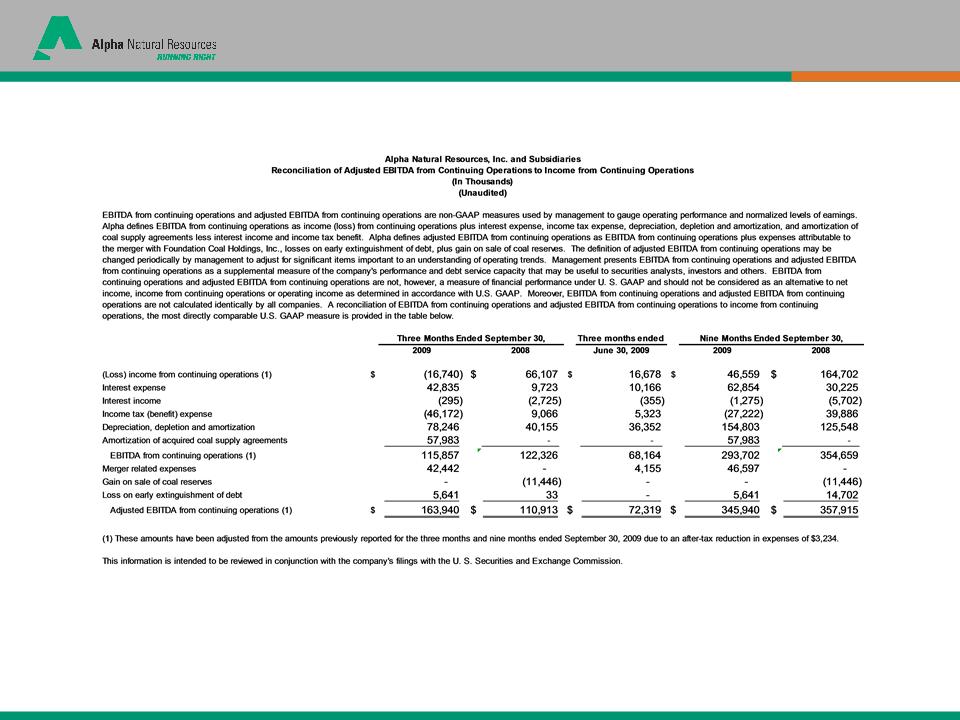

3Q09 Reconciliation of Adjusted EBIDTA

27

3Q09 Reconciliation of Adjusted Income

28

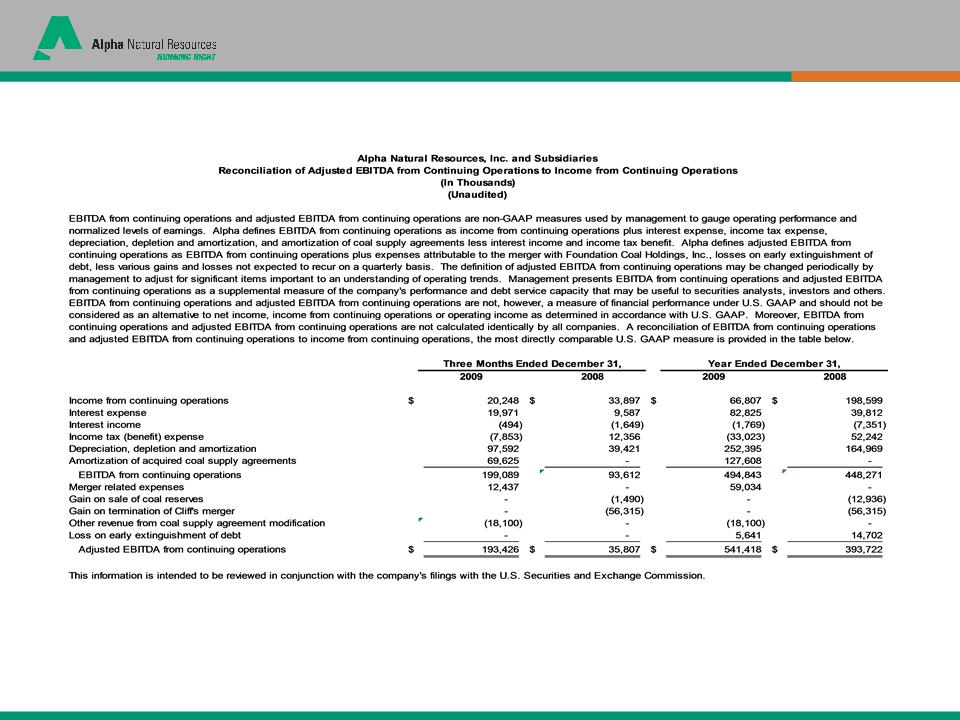

4Q09 Reconciliation of Adjusted EBIDTA

29

4Q09 Reconciliation of Adjusted Income

30

www.alphanr.com