Attached files

| file | filename |

|---|---|

| EX-21 - EXHIBIT 21 - LaSalle Hotel Properties | dex21.htm |

| EX-23 - EXHIBIT 23 - LaSalle Hotel Properties | dex23.htm |

| EX-32.1 - EXHIBIT 32.1 - LaSalle Hotel Properties | dex321.htm |

| EX-31.2 - EXHIBIT 31.2 - LaSalle Hotel Properties | dex312.htm |

| EX-12.1 - EXHIBIT 12.1 - LaSalle Hotel Properties | dex121.htm |

| EX-31.1 - EXHIBIT 31.1 - LaSalle Hotel Properties | dex311.htm |

| EX-10.25 - EXHIBIT 10.25 - LaSalle Hotel Properties | dex1025.htm |

| EX-10.26 - EXHIBIT 10.26 - LaSalle Hotel Properties | dex1026.htm |

| EX-10.24 - EXHIBIT 10.24 - LaSalle Hotel Properties | dex1024.htm |

| EX-10.20 - EXHIBIT 10.20 - LaSalle Hotel Properties | dex1020.htm |

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Fiscal Year Ended December 31, 2009

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission file number 1-14045

LASALLE HOTEL PROPERTIES

(Exact name of registrant as specified in its charter)

| Maryland |

36-4219376 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) | |

| 3 Bethesda Metro Center, Suite 1200 Bethesda, Maryland |

20814 | |

| (Address of principal executive offices) | (Zip Code) |

(301) 941-1500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Shares of Beneficial Interest ($0.01 par value) |

New York Stock Exchange | |

| 8 3/8% Series B Cumulative Redeemable Preferred Shares ($0.01 par value) |

New York Stock Exchange | |

| 7 1/2% Series D Cumulative Redeemable Preferred Shares ($0.01 par value) |

New York Stock Exchange | |

| 8% Series E Cumulative Redeemable Preferred Shares ($0.01 par value) |

New York Stock Exchange | |

| 7 1/4% Series G Cumulative Redeemable Preferred Shares ($0.01 par value) |

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. Check one:

| Large accelerated filer x | Accelerated filer ¨ |

Non-accelerated filer ¨ |

Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the 62,601,655 common shares of beneficial interest held by non-affiliates of the registrant was approximately $772.5 million based on the closing price on the New York Stock Exchange for such common shares of beneficial interest as of June 30, 2009.

Number of the registrant’s common shares of beneficial interest outstanding as of February 12, 2010: 63,651,064.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for its 2010 Annual Meeting of Shareholders to be held on or about April 22, 2010 are incorporated by reference in Part III of this report.

Table of Contents

INDEX

| Item No. |

Form 10-K Report Page | |||

| PART I | ||||

| 1. | 2 | |||

| 1A. | 7 | |||

| 1B. | 13 | |||

| 2. | 14 | |||

| 3. | 15 | |||

| 4. | 15 | |||

| PART II | ||||

| 5. | 16 | |||

| 6. | 19 | |||

| 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

21 | ||

| 7A. | 44 | |||

| 8. | 44 | |||

| 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

44 | ||

| 9A. | 44 | |||

| PART III | ||||

| 9B. | 45 | |||

| 10. | 45 | |||

| 11. | 45 | |||

| 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

45 | ||

| 13. | Certain Relationships and Related Transactions, and Trustee Independence |

45 | ||

| 14. | 45 | |||

| PART IV | ||||

| 15. | 46 | |||

Table of Contents

Forward-Looking Statements

This report, together with other statements and information publicly disseminated by the Company, contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. The Company intends such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995 and includes this statement for purposes of complying with these safe harbor provisions. Forward-looking statements, which are based on certain assumptions and describe the Company’s future plans, strategies and expectations, are generally identifiable by use of the words “believe,” “expect,” “intend,” “anticipate,” “estimate,” “project” or similar expressions. Forward-looking statements in this report include, among others, statements about the Company’s business strategy, including its acquisition and development strategies, industry trends, estimated revenues and expenses, ability to realize deferred tax assets, expected liquidity needs and sources (including capital expenditures and the ability to obtain financing or raise capital). You should not rely on forward-looking statements since they involve known and unknown risks, uncertainties and other factors that are, in some cases, beyond the Company’s control and which could materially affect actual results, performances or achievements. Factors that may cause actual results to differ materially from current expectations include, but are not limited to:

| • | risks associated with the hotel industry, including competition, increases in wages, energy costs and other operating costs, potential unionization, actual or threatened terrorist attacks, any type of flu or disease-related pandemic, downturns in general and local economic conditions; |

| • | the availability and terms of financing and capital and the general volatility of securities markets; |

| • | the Company’s dependence on third-party managers of its hotels, including its inability to implement strategic business decisions directly; |

| • | risks associated with the real estate industry, including environmental contamination and costs of complying with the Americans with Disabilities Act and similar laws; |

| • | interest rate increases; |

| • | the possible failure of the Company to qualify as a REIT and the risk of changes in laws affecting REITs; |

| • | the possibility of uninsured losses; |

| • | risks associated with redevelopment and repositioning projects, including delays and cost overruns; and |

| • | the risk factors discussed under the heading “Risk Factors” in this Annual Report on Form 10-K. |

Accordingly, there is no assurance that the Company’s expectations will be realized. Except as otherwise required by the federal securities laws, the Company disclaims any obligations or undertaking to publicly release any updates or revisions to any forward-looking statement contained herein (or elsewhere) to reflect any change in the Company’s expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based.

The “Company”, “we” or “us” means LaSalle Hotel Properties, a Maryland real estate investment trust, and one or more of its subsidiaries (including LaSalle Hotel Operating Partnership, L.P. (the “Operating Partnership”) and LaSalle Hotel Lessee, Inc. (“LHL”)), or, as the context may require, LaSalle Hotel Properties only, the Operating Partnership only or LHL only.

1

Table of Contents

PART I

| Item 1. | Business |

General

The Company was organized as a Maryland real estate investment trust on January 15, 1998 to buy, own, redevelop and lease primarily upscale and luxury full-service hotels located in convention, resort and major urban business markets. The Company is a self-managed and self-administered real estate investment trust (“REIT”) as defined in the Internal Revenue Code of 1986, as amended (the “Code”). As a REIT, the Company is generally not subject to federal corporate income tax on that portion of its net income that is currently distributed to shareholders. The income of LHL, the Company’s taxable-REIT subsidiary, is subject to taxation at normal corporate rates.

As of December 31, 2009, the Company owned interests in 31 hotels with approximately 8,500 rooms/suites located in 11 states and the District of Columbia. Each hotel is leased under a participating lease that provides for rental payments equal to the greater of (i) base rent or (ii) participating rent based on hotel revenues. All 31 of the hotels are leased to LHL, or a wholly-owned subsidiary of LHL, including one hotel which transitioned from a lease with an unaffiliated lessee to a new lease with LHL as of January 1, 2009. The LHL leases expire between 2010 and 2014. Lease revenue from LHL and its wholly-owned subsidiaries is eliminated in consolidation. A third-party or non-affiliated hotel operator manages each hotel, which is also subject to a hotel management agreement, the terms of which are discussed in more detail under “—Hotel Managers and Hotel Management Agreements”. Additionally, the Company owned a 95.0% joint venture interest in a property under development.

Substantially all of the Company’s assets are held by, and all of its operations are conducted through, the Operating Partnership. The Company is the sole general partner of the Operating Partnership. The Company owned, through a combination of direct and indirect interests, 100% of the common units of the Operating Partnership at December 31, 2009. During 2009, an unaffiliated limited partner redeemed 70,000 common units of limited partnership interest, leaving none held by limited partners other than directly or indirectly by the Company at December 31, 2009. Common units of the Operating Partnership were redeemable for cash or, at the option of the Company, for a like number of common shares of beneficial interest, par value $0.01 per share, of the Company. On February 1, 2009, a limited partner redeemed 2,348,888 Series C Preferred Units of limited interest in the Operating Partnership for 2,348,888 7.25% Series C Cumulative Redeemable Preferred Shares of Beneficial Interest (liquidation preference $25.00 per share), $0.01 par value per share. All of the Series C Preferred Shares were exchanged for Series G Preferred Shares on a one-for-one basis on April 16, 2009. No Series C Preferred Shares were outstanding as of December 31, 2009.

The Company’s principal offices are located at 3 Bethesda Metro Center, Suite 1200, Bethesda, Maryland 20814. The Company’s website is www.lasallehotels.com. The Company makes available on its website free of charge its filings with the Securities and Exchange Commission (“SEC”), including its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports.

Strategies and Objectives

The Company’s primary objectives are to provide income to its shareholders through increases in distributable cash flow and to increase long-term total returns to shareholders through appreciation in the value of its common shares of beneficial interest. To achieve these objectives, the Company seeks to:

| • | enhance the return from, and the value of, the hotels in which it owns interests and any additional hotels the Company may acquire or develop; and |

| • | invest in or acquire additional hotel properties on favorable terms. |

2

Table of Contents

The Company seeks to achieve revenue growth principally through:

| • | renovations, repositionings and/or expansions at selected hotels; |

| • | acquisitions of full-service hotels located in convention, resort and major urban markets in the U.S. and abroad, especially upscale and luxury full-service hotels in such markets where the Company perceives strong demand growth or significant barriers to entry; |

| • | selective development of hotel properties, particularly upscale and luxury full-service hotels in high barrier-to-entry and high demand markets where development economics are favorable; and |

| • | revenue enhancing programs at the hotels. |

The Company intends to acquire (when the economic environment improves) additional hotels in urban, convention and resort markets, consistent with the growth strategies outlined above and which may:

| • | possess unique competitive advantages in the form of location, physical facilities or other attributes; |

| • | be available at significant discounts to replacement cost, including when such discounts result from reduced competition for hotels with long-term management and/or franchise agreements; |

| • | benefit from brand or franchise conversion or removal, new management, renovations or redevelopment or other active and aggressive asset management strategies; or |

| • | have expansion opportunities. |

The Company continues to focus on eight primary urban markets; however, it will acquire assets in other markets if the investment is consistent with the Company’s strategies and return criteria. The primary urban markets are:

| • Boston | • San Diego | |

| • Chicago | • San Francisco | |

| • Los Angeles | • Seattle | |

| • New York | • Washington, DC |

Hotel Managers and Hotel Management Agreements

The Company seeks to grow through strategic relationships with premier, internationally recognized hotel operating companies, including Westin Hotels and Resorts, Sheraton Hotels and Resorts Worldwide, Inc., Hilton Hotels Corporation, Outrigger Lodging Services, Noble House Hotels and Resorts, Hyatt Hotels Corporation, Benchmark Hospitality, White Lodging Services Corporation, Thompson Hotels, Sandcastle Resorts & Hotels, Davidson Hotel Company, Denihan Hospitality Group, Kimpton Hotel & Restaurant Group, L.L.C. and Dolce Hotels and Resorts. The Company believes that having multiple operators creates a network that will generate acquisition opportunities. In addition, the Company believes its acquisition capabilities are enhanced by its considerable experience, resources and relationships in the hotel industry specifically and the real estate industry generally.

As of December 31, 2009, all of our 31 hotels are leased by LHL, and are managed and operated by third parties pursuant to management agreements entered into between LHL and the respective hotel management companies.

Our management agreements for the 31 hotels leased to LHL have the terms described below.

| • | Base Management Fees. Our management agreements generally provide for the payment of base management fees between 1.0% and 3.5% of the applicable hotel’s revenues or a fixed amount, as determined in the agreements. |

| • | Incentive Management and Other Fees. Some of our management agreements provide for the payment of incentive management fees between 10.0% and 20.0% of gross operating profit or as a percentage of, or in excess of, certain thresholds of net operating income or cash flow of the applicable hotel, if certain criteria are met. Certain of the management agreements also provide for the payment by us of sales and marketing, accounting and other fees. |

3

Table of Contents

| • | Terms. The terms of our management agreements range from 1.5 years to 20 years not including renewals, and 1.5 years to 37 years including renewals. |

| • | Ability to Terminate. We have 31 management agreements of which 25 are terminable at will and 2 are terminable upon sale. The remaining 4 management agreements are terminable only with cause. Termination fees range from zero to up to three times annual base management and incentive management fees. |

| • | Operational Services. Each manager has exclusive authority to supervise, direct and control the day-to-day operation and management of the respective hotel including establishing all room rates, processing reservations, procuring inventories, supplies and services, and preparing public relations, publicity and marketing plans for the hotel. |

| • | Executive Supervision and Management Services. Each manager supervises all managerial and other employees for the respective hotel, reviews the operation and maintenance of the respective hotel, prepares reports, budgets and projections, and provides other administrative and accounting support services to the respective hotel. |

| • | Chain Services. Our management agreements with major brands require the managers to furnish chain services that are generally made available to other hotels managed by such operators. Such services may, for example, include: (1) the development and operation of computer systems and reservation services; (2) management and administrative services; (3) marketing and sales services; (4) human resources training services and (5) such additional services as may from time to time be more efficiently performed on a national, regional or group level. |

| • | Working Capital. Our management agreements typically require us to maintain working capital for a hotel and to fund the cost of supplies such as linen and other similar items. We are also responsible for providing funds to meet the cash needs for the hotel operations if at any time the funds available from the hotel operations are insufficient to meet the financial requirements of the hotel. |

| • | Furniture, Fixtures and Equipment Replacements. We are required to provide to the managers all the necessary furniture, fixtures and equipment for the operation of the hotels (including funding any required furniture, fixture and equipment replacements). Our management agreements generally provide that once each year the managers will prepare a list of furniture, fixtures and equipment to be acquired and certain routine repairs to be performed in the next year and an estimate of funds that are necessary therefore, subject to our review and approval. For purposes of funding the furniture, fixtures and equipment replacements, a specified percentage of the gross revenues of each hotel is either deposited by the manager in an escrow account (typically 3.0% to 5.0%) or held by the owner. |

| • | Building Alterations, Improvements and Renewals. Our management agreements generally require the managers to prepare an annual estimate of the expenditures necessary for major repairs, alterations, improvements, renewals and replacements to the structural, mechanical, electrical, heating, ventilating, air conditioning, plumbing and vertical transportation elements of the hotels. In addition to the foregoing, the management agreements generally provide that the managers may propose such changes, alterations and improvements to the hotels as required by reason of laws or regulations or, in each manager’s reasonable judgment, to keep each respective hotel in a safe, competitive and efficient operating condition. |

| • | Sale of a Hotel. Three of our management agreements limit our ability to sell, lease or otherwise transfer a hotel, unless the transferee assumes the related management agreement and meets specified other conditions and/or unless the transferee is not a competitor of the manager. |

| • | Service Marks. During the term of our management agreements, the service mark, symbols and logos currently used by the managers may be used in the operation of the hotels. Any right to use the service marks, logo and symbols and related trademarks at a hotel will terminate with respect to that hotel upon termination of the management agreement with respect to such hotel. |

4

Table of Contents

Recent Developments

On February 1, 2010, the Company repaid the Le Montrose Suite Hotel mortgage loan in the amount of $12.8 million plus accrued interest with cash and additional borrowings on its senior unsecured credit facility. The loan was due to mature in July 2010.

On February 2, 2010, the Company and LaSalle Investment Management (“LIM”) mutually agreed to dissolve their joint venture arrangement. The joint venture was formed to seek domestic hotel investments in high barrier-to-entry urban and resort markets in the U.S. See “—Joint Ventures.”

Hotel Renovations

The Company believes that its regular program of capital improvements at the hotels, including replacement and refurbishment of furniture, fixtures and equipment helps maintain and enhance its competitiveness and maximizes revenue growth.

The Donovan House was closed for renovations on February 21, 2006 and re-opened on March 28, 2008 as a luxury high-style, independent hotel. A new restaurant was completed and opened on June 8, 2009. The Company invested $36.0 million from 2006 through 2009, excluding capitalized interest, to complete the renovation and repositioning.

The Chaminade Resort and Conference Center (excluding the spa and fitness center) was closed for renovations relating to an ongoing repositioning project on November 18, 2007 and re-opened as scheduled on January 31, 2008. The spa was renovated and re-opened on February 1, 2009. The Company invested $9.3 million from 2006 through 2009, excluding capitalized interest, to complete the project.

Joint Ventures

On March 18, 2008, the Company, through Modern Magic Hotel LLC, a joint venture in which the Company holds a 95.0% controlling interest, acquired floors 2 through 13 and a portion of the first floor of the existing 52-story IBM Building located at 330 N. Wabash Avenue in downtown Chicago, IL for $46.0 million plus acquisition costs. The joint venture has developed plans to convert the existing vacant floors to a super luxury hotel. Redevelopment activity has been temporarily suspended, but is expected to resume when economic conditions and lodging industry fundamentals demonstrate sustained improvement. As a result of the suspension of redevelopment activity, the Company has temporarily ceased the capitalization of interest, real estate taxes and insurance costs incurred by the development. Since the Company holds a controlling interest, the accounts of the joint venture have been included in the consolidated financial statements. Initial acquisition and subsequent costs, including capitalized interest, totaling $62.2 million and $60.1 million are included in property under development in the Company’s consolidated balance sheets as of December 31, 2009 and 2008, respectively. The 5.0% interest of the outside partner is included in redeemable noncontrolling interest in consolidated entity in the Company’s consolidated balance sheets.

On February 2, 2010, the Company’s joint venture arrangement with LIM, entered into on April 17, 2008, was mutually dissolved. The joint venture arrangement with LIM, a leading global real estate investment manager, was to seek domestic hotel investments in high barrier-to-entry urban and resort markets in the U.S. The two companies planned to invest up to $250.0 million of equity in the joint venture. The Company, through the Operating Partnership, owned a 15.0% equity interest in the joint venture. The Company accounted for its investment in this joint venture under the equity method of accounting. As of December 31, 2009, there were no acquisitions through the joint venture.

Tax Status

The Company has elected to be taxed as a REIT under Sections 856 through 860 of the Code. As a result, the Company generally is not subject to corporate income tax on that portion of its net income that is currently

5

Table of Contents

distributed to shareholders. A REIT is subject to a number of highly technical and complex organizational and operational requirements, including requirements with respect to the nature of its gross income and assets and a requirement that it currently distribute at least 90% of its taxable income. The Company may, however, be subject to certain state and local taxes on its income and property.

Effective January 1, 2001, the Company elected to operate its wholly-owned subsidiary, LHL, as provided for under the REIT Modernization Act as a taxable-REIT subsidiary. Accordingly, LHL is required to pay corporate income taxes at the applicable rates.

Seasonality

The Company’s hotels’ operations historically have been seasonal. Taken together, the hotels maintain higher occupancy rates during the second and third quarters. These seasonality patterns can be expected to cause fluctuations in the hotel operating revenues of LHL and the Company’s quarterly lease revenues from LHL.

Competition

The hotel industry is highly competitive. Each of the hotels is located in a developed area that includes other hotel properties. The number of competitive hotel properties in a particular area could have a material adverse effect on occupancy, average daily rate and room revenue per available room at the Company’s current hotels or at hotels acquired in the future. The Company may be competing for investment opportunities with entities that have substantially greater financial resources than the Company. These entities may generally be able to accept more risk than the Company can prudently manage, including risks with respect to the amount of leverage utilized, creditworthiness of a hotel operator or the geographic proximity of its investments. Competition may generally reduce the number of suitable investment opportunities offered to the Company and increase the bargaining power of property owners seeking to sell.

Environmental Matters

In connection with the ownership of hotels, the Company is subject to various federal, state and local laws, ordinances and regulations relating to environmental protection. Under these laws, a current or previous owner or operator of real estate may be liable for the costs of removal or remediation of certain hazardous or toxic substances on, under or in such property. Such laws often impose liability without regard to whether the owner or operator knew of, or was responsible for, the presence of hazardous or toxic substances. In addition, the presence of contamination from hazardous or toxic substances, or the failure to remediate such contaminated property properly, may adversely affect the owner’s ability to borrow using such property as collateral. Furthermore, a person who arranges for the disposal or treatment of a hazardous or toxic substance at a property owned by another, or who transports such substance to or from such property, may be liable for the costs of removal or remediation of such substance released into the environment at the disposal or treatment facility. The costs of remediation or removal of such substances may be substantial, and the presence of such substances may adversely affect the owner’s ability to sell such real estate or to borrow using such real estate as collateral. In connection with the ownership of hotels, the Company may be potentially liable for such costs.

The Company believes that its hotels are in compliance, in all material respects, with all federal, state and local environmental ordinances and regulations regarding hazardous or toxic substances and other environmental matters, the violation of which could have a material adverse effect on the Company. The Company has not received written notice from any governmental authority of any material noncompliance, liability or claim relating to hazardous or toxic substances or other environmental matters in connection with any of its present properties.

Employees

The Company had 26 employees as of February 12, 2010. All persons employed in the day-to-day operations of the hotels are employees of the management companies engaged by the lessees to operate such hotels.

6

Table of Contents

Additional Information

All reports filed with the SEC may also be read and copied at the SEC’s public reference room at 100 F Street, NE, Washington, DC 20549. Further information regarding the operation of the public reference room may be obtained by calling 1-800-SEC-0330. In addition, all of our filed reports can be obtained at the SEC’s website at www.sec.gov or through our website at www.lasallehotels.com.

| Item 1A. | Risk Factors |

The following risk factors and other information included in this Annual Report on Form 10-K should be carefully considered. The risks and uncertainties described below are not the only ones the Company faces. Additional risks and uncertainties not presently known to the Company or that it may currently deem immaterial also may impair its business operations. If any of the following risks occur, the Company’s business, financial condition, operating results and cash flows could be materially adversely affected.

In the past, events beyond our control, including an economic slowdown or downturn and terrorism, harmed the operating performance of the hotel industry generally and the performance of our hotels. If these or similar events occur or continue to occur, such as the continued general economic downturn, our operating and financial results may be harmed by declines in occupancy, average daily room rates and/or other operating revenues.

The performance of the lodging industry has traditionally been closely linked with the performance of the general economy and, specifically, growth in the U.S. gross domestic product. For example, revenue per available room, or RevPAR, in the lodging industry declined 6.9% in 2001 and 2.6% in 2002. All of our hotels are classified as upper upscale. In an economic downturn, these types of hotels may be more susceptible to a decrease in revenue, as compared to hotels in other categories that have lower room rates. This characteristic may result from the fact that upper upscale hotels generally target business and high-end leisure travelers. In periods of economic difficulties, business and leisure travelers may seek to reduce travel costs by limiting travel or seeking to reduce costs on their trips. In addition, the terrorist attacks of September 11, 2001 had a dramatic adverse effect on business and leisure travel, and on the occupancy and average daily rate of our hotels. Future terrorist activities could have a harmful effect on both the industry and us. Likewise, the volatility in the credit and equity markets and the economic recession will continue to have an adverse effect on our business. Even after an economic recovery begins, a significant period of time may elapse before RevPar, operating margins and other key lodging fundamentals improve.

The return on our hotels depends upon the ability of the hotel operators to operate and manage the hotels.

To maintain our status as a REIT, we are not permitted to operate any of our hotels. As a result, we are unable to directly implement strategic business decisions with respect to the operation and marketing of our hotels, such as decisions with respect to the setting of room rates, repositioning of a hotel, food and beverage pricing and certain similar matters. Although LHL consults with the hotel operators with respect to strategic business plans, the hotel operators are under no obligation to implement any of our recommendations with respect to such matters. Thus, even if we believe our hotels are being operated inefficiently or in a manner that does not result in satisfactory occupancy rates, revenue per available room, average daily rates or operating profits, we may not have sufficient rights under our hotel operating agreements to enable us to force the hotel operator to change its method of operation. We generally can only seek redress if a hotel operator violates the terms of the applicable operating agreement, and then only to the extent of the remedies provided for under the terms of the agreement. Some of the operating agreements have lengthy terms and may not be terminable by us before the agreement’s expiration. In the event that we are able to and do replace any of our hotel operators, we may experience significant disruptions at the affected hotels, which may adversely affect our ability to make distributions to our shareholders.

7

Table of Contents

We currently own only upper upscale hotels. The upper upscale segment of the lodging market is highly competitive and generally subject to greater volatility than most other market segments, which could negatively affect our profitability.

The upper upscale segment of the hotel business is highly competitive. Our hotels compete on the basis of location, room rates, quality, service levels, reputation and reservations systems, among many factors. There are many competitors in the upper upscale segment, and many of these competitors may have substantially greater marketing and financial resources than we have. This competition could reduce occupancy levels and room revenue at our hotels, which would harm our operations. Over-building in the hotel industry may increase the number of rooms available and may decrease occupancy and room rates. In addition, in periods of weak demand, as may occur during a general economic recession, profitability is negatively affected by the relatively high fixed costs of operating upper upscale hotels.

Our performance and our ability to make distributions on our shares are subject to risks associated with the hotel industry.

Competition for guests, increases in operating costs, dependence on travel and economic conditions could adversely affect our cash flow. Our hotels are subject to all operating risks common to the hotel industry. These risks include:

| • | adverse effects of weak national, regional and local economic conditions; |

| • | tightening credit standards; |

| • | competition for guests and meetings from other hotels including competition and pricing pressure from internet wholesalers and distributors; |

| • | increases in operating costs, including wages, benefits, insurance, property taxes and energy, due to inflation and other factors, which may not be offset in the future by increased room rates; |

| • | labor strikes, disruptions or lockouts that may impact operating performance; |

| • | dependence on demand from business and leisure travelers, which may fluctuate and be seasonal; |

| • | increases in energy costs, airline fares and other expenses related to travel, which may negatively affect traveling; and |

| • | terrorism, terrorism alerts and warnings, military actions such as the engagements in Iraq and Afghanistan, pandemics or other medical events which may cause decreases in business and leisure travel. |

These factors could adversely affect the ability of the lessees (including our taxable-REIT subsidiary lessees) to generate revenues and to make rental payments to us.

Unexpected capital expenditures could adversely affect our cash flow. Hotels require ongoing renovations and other capital improvements, including periodic replacement or refurbishment of furniture, fixtures and equipment. Under the terms of our leases, we are obligated to pay the cost of certain capital expenditures at the hotels, including new brand standards, and to pay for periodic replacement or refurbishment of furniture, fixtures and equipment. If capital expenditures exceed expectations, there can be no assurance that sufficient sources of financing will be available to fund such expenditures.

In addition, we have acquired hotels that have undergone significant renovation and may acquire additional hotels in the future that require significant renovation. Renovations of hotels involve numerous risks, including the possibility of environmental problems, construction cost overruns and delays, the effect on current demand, uncertainties as to market demand or deterioration in market demand after commencement of renovation and the emergence of unanticipated competition from other hotels.

8

Table of Contents

Our lenders may have suffered losses related to the weakening economy and may not be able to fund our borrowings.

Our lenders, including the lenders participating in our $450.0 million senior unsecured credit facility, may have suffered losses related to their lending and other financial relationships, especially because of the general weakening of the national economy and increased financial instability of many borrowers. As a result, lenders may become insolvent or tighten their lending standards, which could make it more difficult for us to borrow under our credit facility or to obtain other financing on favorable terms or at all. Our financial condition and results of operations would be adversely affected if we were unable to draw funds under our credit facility because of a lender default or to obtain other cost-effective financing.

Our obligation to comply with financial covenants in our unsecured credit facilities and mortgages on some of our hotel properties could restrict our range of operating activities, may require us to liquidate our properties and could adversely affect our ability to make distributions to our shareholders.

Our unsecured credit facilities. We have a senior unsecured credit facility with a syndicate of banks, which provides for a maximum borrowing of up to $450.0 million. The senior unsecured credit facility matures on April 13, 2011 and has a one-year extension option. The senior unsecured credit facility contains certain financial covenants relating to interest coverage, debt service coverage, fixed charge coverage and ratios related to net worth and total funded indebtedness. The senior unsecured credit facility also contains a cross-default provision that allows the lenders under the credit facility to stop future extensions of credit and/or accelerate the maturity of any outstanding principal balances under the credit facility if we are in default under another debt obligation, including our non-recourse secured mortgage indebtedness.

LHL has an unsecured revolving credit facility with U.S. Bank National Association, which provides for a maximum borrowing of up to $25.0 million. The unsecured credit facility matures on April 13, 2011 and, at our option, has a one-year extension option. The unsecured credit facility contains certain financial covenants relating to interest coverage, debt service coverage, fixed charge coverage and ratios related to net worth and total funded indebtedness.

If we violate the financial covenants contained in either credit facility described above, we may attempt to negotiate a waiver of the violation or amend the terms of the credit facility with the lenders thereunder; however, we can make no assurance that we would be successful in any such negotiations or that, if successful in obtaining a waiver or amendment, that such amendment or waiver would be on terms attractive to us. Accordingly, if we violate the financial covenants in our facilities, we could be required to repay all or a portion of our indebtedness with respect to such credit facility before maturity at a time when we might be unable to arrange financing for such repayment on attractive terms, or at all. Moreover, if we are unable to refinance our debt on acceptable terms, including at maturity of our credit facilities, we may be forced to dispose of hotel properties on disadvantageous terms, potentially resulting in losses that reduce cash flow from operating activities. Failure to comply with our financial covenants contained in our credit facilities, or our non-recourse secured mortgages described below, could result from, among other things, changes in our results of operations, the incurrence of additional debt or changes in general economic conditions.

Our non-recourse secured mortgages. In addition to our senior unsecured credit facility and the LHL unsecured revolving credit facility, we have from time to time entered into non-recourse mortgages secured by specific hotel properties. Under the terms of these debt obligations, a lender’s only remedy in the event of default is against the real property securing the mortgage, except where a borrower has, among other customary exceptions, engaged in an action constituting fraud or an intentional misrepresentation. In those cases, a lender may seek a remedy for a breach directly against the borrower, including its other assets. The Le Montrose Suite Hotel, Indianapolis Marriott Downtown, Hilton San Diego Gaslamp Quarter, Westin Copley Place, Hotel Deca, Westin Michigan Avenue and Hotel Solamar are each mortgaged to secure payment of indebtedness aggregating $595.0 million (excluding loan premiums) as of December 31, 2009. The Harborside Hyatt Conference Center & Hotel is mortgaged to secure payment of principal and interest on bonds with an aggregate par value of $42.5

9

Table of Contents

million. These mortgages contain debt service coverage tests related to the mortgaged property. If our debt service coverage ratio fails, for that specific property, to exceed a threshold level specified in a mortgage, cash flows from that hotel will automatically be directed to the lender to satisfy required payments, and to fund certain reserves required by the mortgage and to fund additional cash reserves for future required payments, including final payment, until such time as we again become compliant with the specified debt service coverage ratio or the mortgage is paid off.

If we are unable to meet mortgage payment obligations, including the payment obligation upon maturity of the mortgage borrowing, the mortgage securing the specific property could be foreclosed upon by, or the property could be otherwise transferred to, the mortgagee with a consequent loss of income and asset value to us. We may also elect to sell the property, if we are able to sell the property, for a loss in advance of a foreclosure or other transfer. An event of default under our non-recourse secured mortgage may also constitute an event of default under our senior unsecured credit facility.

As of December 31, 2009, the Company is in compliance with all debt covenants, current on all loan payments and not otherwise in default under the credit facilities or mortgages.

Our liquidity may be reduced and our cost of debt financing may be increased because we may be unable to, or elect not to, remarket debt securities related to our Harborside Hyatt Conference Center & Hotel for which we may be liable.

We are the obligor with respect to a $37.1 million tax-exempt special project revenue bond and a $5.4 million taxable special project revenue bond, both issued by the Massachusetts Port Authority (collectively, the “Massport Bonds”). The Massport Bonds, which mature on March 1, 2018, bear interest based on weekly floating rates and have no principal reductions prior to their scheduled maturities. The Massport Bonds may be redeemed at any time, at our option, without penalty. The Royal Bank of Scotland provides the supporting letters of credit on the Massport Bonds. The letters of credit expire on February 14, 2011 unless extended per the agreements. If the Royal Bank of Scotland fails to renew its letters of credit at expiration and an acceptable replacement provider cannot be found, we may be required to pay off the bonds. If we are unable to, or elect not to, issue or remarket the Massport Bonds, we would expect to rely primarily on our available cash and revolving credit facility to pay off the Massport Bonds. At certain times, we may hold some of the Massport Bonds that have not been successfully remarketed. Our borrowing costs under our revolving credit facility may be higher than tax-exempt bond financing costs. Borrowings under the revolving credit facility to pay off the Massport Bonds would also reduce our liquidity to meet other obligations.

Our performance is subject to real estate industry conditions, the terms of our leases and management agreements.

Because real estate investments are illiquid, we may not be able to sell hotels when desired. Real estate investments generally cannot be sold quickly. We may not be able to vary our portfolio promptly in response to economic or other conditions. In addition, provisions of the Code limit a REIT’s ability to sell properties in some situations when it may be economically advantageous to do so.

Liability for environmental matters could adversely affect our financial condition. As an owner of real property, we are subject to various federal, state and local laws and regulations relating to the protection of the environment that may require a current or previous owner of real estate to investigate and clean-up hazardous or toxic substances at a property. These laws often impose such liability without regard to whether the owner knew of or caused the presence of the contaminants, and liability is not limited under the enactments and could exceed the value of the property and/or the aggregate assets of the owner. Persons who arrange for the disposal or treatment facility, whether or not such facility is owned or operated by the person may be liable for the costs of removal or remediation of such substance released into the environment at the disposal or treatment facility. Even if more than one person were responsible for the contamination, each person covered by the environmental laws may be held responsible for the entire amount of clean-up costs incurred.

10

Table of Contents

Environmental laws also govern the presence, maintenance and removal of asbestos-containing materials. These laws impose liability for release of asbestos-containing materials into the air and third parties may seek recovery from owners or operators of real properties for personal injury associated with asbestos-containing materials. In connection with ownership (direct or indirect) of our hotels, we may be considered an owner or operator of properties with asbestos-containing materials. Having arranged for the disposal or treatment of contaminants, we may be potentially liable for removal, remediation and other costs, including governmental fines and injuries to persons and property.

The costs of compliance with the Americans with Disabilities Act and other government regulations could adversely affect our cash flow. Under the Americans with Disabilities Act of 1990, or ADA, all public accommodations are required to meet certain federal requirements related to access and use by disabled persons. A determination that we are not in compliance with the ADA could result in imposition of fines or an award of damages to private litigants. If we are required to make substantial modifications to our hotels, whether to comply with ADA or other government regulation such as building codes or fire safety regulations, our financial condition, results of operations and ability to make shareholder distributions could be adversely affected.

Certain leases and management agreements may constrain us from acting in the best interest of shareholders or require us to make certain payments. The Harborside Hyatt Conference Center & Hotel, San Diego Paradise Point Resort and Spa and The Hilton San Diego Resort and Spa are each subject to a ground lease with a third-party lessor which requires us to obtain the consent of the relevant third party lessor in order to sell any of these hotels or to assign our leasehold interest in any of the ground leases. Part of a parking lot at the Sheraton Bloomington Hotel Minneapolis South is also subject to a ground lease with a third-party lessor; third-party lessor consent is required to assign the leasehold interest unless the assignment is in conjunction with the sale of the hotel. Accordingly, if we determine that the sale of any of these hotels or the assignment of our leasehold interest in any of these ground leases is in the best interest of our shareholders, we may be prevented from completing such a transaction if we are unable to obtain the required consent from the relevant lessor. The Indianapolis Marriott Downtown, Westin Copley Place, Hotel Solamar, and one of two golf courses, the Pines, at Seaview Resort are each subject to a ground or air rights lease and do not require approval from the relevant third-party lessor.

In some instances, we may be required to obtain the consent of the hotel operator or franchisor prior to selling the hotel. Typically, such consent is only required in connection with certain proposed sales, such as if the proposed purchaser is engaged in the operation of a competing hotel or does not meet certain minimum financial requirements. The operators of Harborside Hyatt Conference Center & Hotel and Alexis Hotel require approval of certain sales.

Some of our hotels are subject to rights of first refusal which may adversely affect our ability to sell those properties on favorable terms or at all.

The Westin City Center Dallas is a unit of a commercial condominium complex and is subject to a right of first refusal in favor of the owner of the remaining condominium units. We are also subject to a franchisor’s right of first offer with respect to the Hilton Alexandria Old Town, Hilton San Diego Gaslamp Quarter and The Hilton San Diego Resort and Spa. These third-party rights may adversely affect our ability to timely dispose of these properties on favorable terms, or at all.

Increases in interest rates may increase our interest expense.

As of December 31, 2009, $48.8 million of aggregate indebtedness (7.6% of total indebtedness) was subject to variable interest rates. An increase in interest rates could increase our interest expense and reduce our cash flow and may affect our ability to make distributions to shareholders and to service our indebtedness.

11

Table of Contents

Failure to qualify as a REIT would be costly.

We have operated (and intend to so operate in the future) so as to qualify as a REIT under the Code beginning with our taxable year ended December 31, 1998. Although management believes that we are organized and operated in a manner to so qualify, no assurance can be given that we will qualify or remain qualified as a REIT.

If we fail to qualify as a REIT in any taxable year, we will be subject to federal income tax (including any applicable alternative minimum tax) on our taxable income at regular corporate rates. Moreover, unless entitled to relief under certain statutory provisions, we also will be disqualified from treatment as a REIT for the four taxable years following the year during which qualification was lost. This treatment would cause us to incur additional tax liabilities and would significantly impair our ability to service indebtedness, and reduce the amount of cash available to make new investments or to make distributions on our common shares of beneficial interest and preferred shares.

Current laws include provisions that could provide relief in the event we violate certain provisions of the Code that otherwise would result in our failure to qualify as a REIT. We cannot assure that these relief provisions would apply if we failed to comply with the REIT qualification laws. Even if the relief provisions do apply, we would be subject to a penalty tax of at least $50,000 for each disqualifying event in most cases.

Property ownership through partnerships and joint ventures could limit our control of those investments.

Partnership or joint venture investments may involve risks not otherwise present for investments made solely by us, including among others, the possibility that our co-investors might become bankrupt, might at any time have goals or interests that are different from ours because of disparate tax consequences or otherwise, and may take action contrary to our instructions, requests, policies or objectives, including our policy with respect to maintaining our qualification as a REIT. Other risks of joint venture investments include an impasse on decisions, such as a sale, because neither our co-investors nor we would have full control over the partnership or joint venture. There is no limitation under our organizational documents as to the amount of funds that may be invested in partnerships or joint ventures.

We may not have enough insurance.

We carry comprehensive liability, fire, flood, earthquake, extended coverage and business interruption policies that insure us against losses with policy specifications and insurance limits that we believe are reasonable. There are certain types of losses, such as losses from environmental problems or terrorism, that management may not be able to insure against or may decide not to insure against since the cost of insuring is not economical. We may suffer losses that exceed our insurance coverage. Further, market conditions, changes in building codes and ordinances or other factors such as environmental laws may make it too expensive to repair or replace a property that has been damaged or destroyed, even if covered by insurance.

Our organizational documents and agreements with our executives and applicable Maryland law contain provisions that may delay, defer or prevent change of control transactions and may prevent shareholders from realizing a premium for their shares.

Our trustees serve staggered three-year terms, the trustees may only be removed for cause and remaining trustees may fill board vacancies. Our Board of Trustees is divided into three classes of trustees, each serving staggered three-year terms. In addition, a trustee may only be removed for cause by the affirmative vote of the holders of a majority of our outstanding common shares. Our declaration of trust and bylaws also provide that a majority of the remaining trustees may fill any vacancy on the Board of Trustees and further effectively provide that only the Board of Trustees may increase or decrease the number of persons serving on the Board of Trustees. These provisions preclude shareholders from removing incumbent trustees, except for cause after a majority affirmative vote, and filling the vacancies created by such removal with their own nominees.

12

Table of Contents

Our Board of Trustees may approve the issuance of shares with terms that may discourage a third party from acquiring the Company. The Board of Trustees has the power under the declaration of trust to classify any of our unissued preferred shares, and to reclassify any of our previously classified but unissued preferred shares of any series from time to time, in one or more series of preferred shares, without shareholder approval. The issuance of preferred shares could adversely affect the voting power, dividend and other rights of holders of common shares and the value of the common shares.

Our declaration of trust prohibits ownership of more than 9.8% of the common shares or 9.8% of any series of preferred shares. To qualify as a REIT under the Code, no more than 50% of the value of our outstanding shares may be owned, directly or under applicable attribution rules, by five or fewer individuals (as defined to include certain entities) during the last half of each taxable year. Our declaration of trust generally prohibits direct or indirect ownership by any person of (i) more than 9.8% of the number or value (whichever is more restrictive) of the outstanding common shares or (ii) more than 9.8% of the number or value (whichever is more restrictive) of the outstanding shares of any class or series of preferred shares. Generally, shares owned by affiliated owners will be aggregated for purposes of the ownership limitation. Any transfer of shares that would violate the ownership limitation will result in the shares that would otherwise be held in violation of the ownership limit being designated as “shares-in-trust” and transferred automatically to a charitable trust effective on the day before the purported transfer or other event giving rise to such excess ownership. The intended transferee will acquire no rights in such shares.

The Maryland Business Combination Statute applies to us. A Maryland “business combination” statute contains provisions that, subject to limitations, prohibit certain business combinations between us and an “interested stockholder” (defined generally as any person who beneficially owns 10% or more of the voting power of our shares or an affiliate thereof) for five years after the most recent date on which the shareholder becomes an interested stockholder, and thereafter impose special shareholder voting requirements on these combinations.

The Board of Trustees may choose to subject us to the Maryland Control Share Act. A Maryland law known as the “Maryland Control Share Act” provides that “control shares” of a company (defined as shares which, when aggregated with other shares controlled by the acquiring shareholder, entitle the shareholder to exercise one of three increasing ranges of voting power in electing trustees) acquired in a “control share acquisition” (defined as the direct or indirect acquisition of ownership or control of “control shares”) have no voting rights except to the extent approved by the company’s shareholders by the affirmative vote of at least two-thirds of all the votes entitled to be cast on the matter, excluding all interested shares. Our bylaws currently provide that we are not subject to these provisions. However, the Board of Trustees, without shareholder approval, may repeal this bylaw and cause us to become subject to the Maryland Control Share Act.

Other provisions of our organization documents may delay or prevent a change of control of the Company. Among other provisions, our organizational documents provide that the number of trustees constituting the full Board of Trustees may be fixed only by the trustees and that a special meeting of shareholders may not be called by holders of common shares holding less than a majority of the outstanding common shares entitled to vote at such meeting.

Our executive officers have agreements that provide them with benefits in the event of a change in control of the Company. We entered into agreements with our executive officers that provide them with severance benefits if their employment ends under certain circumstances within one year following a “change in control” of the Company (as defined in the agreements) or if the executive officer resigns for “good reason” (as defined in the agreements). These benefits could increase the cost to a potential acquirer of the Company and thereby prevent or deter a change in control of the Company that might involve a premium price for the common shares or otherwise be in our shareholders’ best interests.

| Item 1B. | Unresolved Staff Comments |

None.

13

Table of Contents

| Item 2. | Properties |

Hotel Properties

At December 31, 2009, the Company owned interests in the following 31 hotel properties and additionally, through a joint venture, holds a 95.0% controlling interest of floors 2 through 13 and a portion of the first floor of an existing 52-story building located at 330 N. Wabash Avenue in Chicago, IL:

| Hotel Properties |

Number of Rooms/Suite |

Location | ||

| 1. Sheraton Bloomington Hotel Minneapolis South(1) |

564 | Bloomington, MN | ||

| 2. Westin City Center Dallas |

407 | Dallas, TX | ||

| 3. Seaview Resort(2) |

297 | Galloway, NJ (Atlantic City) | ||

| 4. Le Montrose Suite Hotel |

133 | West Hollywood, CA | ||

| 5. San Diego Paradise Point Resort and Spa(3) |

462 | San Diego, CA | ||

| 6. Harborside Hyatt Conference Center & Hotel(4)(3) |

270 | Boston, MA | ||

| 7. Hotel Viking |

209 | Newport, RI | ||

| 8. Topaz Hotel |

99 | Washington, D.C. | ||

| 9. Hotel Rouge |

137 | Washington, D.C. | ||

| 10. Hotel Madera |

82 | Washington, D.C. | ||

| 11. Hotel Helix |

178 | Washington, D.C. | ||

| 12. The Liaison Capitol Hill |

343 | Washington, D.C. | ||

| 13. Lansdowne Resort |

296 | Lansdowne, VA | ||

| 14. Hotel George |

139 | Washington, D.C. | ||

| 15. Indianapolis Marriott Downtown(4)(3) |

622 | Indianapolis, IN | ||

| 16. Hilton Alexandria Old Town |

246 | Alexandria, VA | ||

| 17. Chaminade Resort and Conference Center |

156 | Santa Cruz, CA | ||

| 18. Hilton San Diego Gaslamp Quarter(4) |

283 | San Diego, CA | ||

| 19. The Grafton on Sunset |

108 | West Hollywood, CA | ||

| 20. Onyx Hotel |

112 | Boston, MA | ||

| 21. Westin Copley Place(4)(5) |

803 | Boston, MA | ||

| 22. Hotel Deca(4) |

158 | Seattle, WA | ||

| 23. The Hilton San Diego Resort and Spa(3) |

357 | San Diego, CA | ||

| 24. Donovan House |

193 | Washington, D.C. | ||

| 25. Le Parc Suite Hotel |

154 | West Hollywood, CA | ||

| 26. Hotel Sax Chicago |

353 | Chicago, IL | ||

| 27. Westin Michigan Avenue(4) |

752 | Chicago, IL | ||

| 28. Alexis Hotel |

121 | Seattle, WA | ||

| 29. Hotel Solamar(4)(3) |

235 | San Diego, CA | ||

| 30. Gild Hall |

126 | New York, NY | ||

| 31. Hotel Amarano Burbank |

99 | Burbank, CA | ||

| Total number of rooms/suites |

8,494 | |||

| (1) | Part of the parking lot of this property is subject to a long-term ground lease. |

| (2) | One of the golf courses at this property is subject to a ground lease. |

| (3) | Properties subject to long-term ground leases. |

| (4) | Properties subject to a mortgage/debt. As of February 1, 2010, Le Montrose Suite Hotel is no longer subject to a mortgage. |

| (5) | Property subject to long-term air rights lease. |

Each of our hotels is full service, with 30 classified as “upper upscale” and one classified as “upscale”, as defined by Smith Travel Research, a provider of hotel industry data.

14

Table of Contents

For each of calendar years 2004 through 2008, the Company notified Marriott International (“Marriott”) that it was terminating the management agreement at the Seaview Resort and Spa due to Marriott’s failure to meet certain hotel operating performance thresholds as defined in the management agreement. Pursuant to the management agreement, Marriott had the right to avoid termination by making cure payments within 60 days of notification. Through May 8, 2009, Marriott made cure payments totaling $12.3 million for the calendar years 2004 through 2007 to avoid termination. Marriott could have recouped these amounts in the event certain future operating performance thresholds were attained. Through May 8, 2009, Marriott had recouped a total of $2.8 million for the calendar years 2004 through 2008. The Company recorded a deferred liability of $9.5 million as of December 31, 2008, which was included in accounts payable and accrued expenses on the consolidated balance sheet. Marriott failed to make the required cure payment due in 2009 for the calendar year 2008, and therefore the Company recognized $9.5 million as pre-tax income in other income in the consolidated statement of operations in May 2009. The management agreement with Marriott was terminated on May 8, 2009. The hotel now operates as an independent hotel, Seaview Resort; the hotel facilities are operated by Dolce Hotels and Resorts, and the golf facilities are operated by Troon Golf. The deferred liability is zero as of December 31, 2009.

The following is a reconciliation of the cure payments and deferred liability as of and for the years ended December 31, 2009, 2008, 2007, 2006 and 2005 (dollars in thousands):

| Year Ended |

Notification Date | Cure Payment | Recoup Amount |

Pre-Tax Income |

Deferred Liability Balance | |||||||||||||||

| Performance Year |

Date | Amount | ||||||||||||||||||

| 2005 |

March 11, 2005 | 2004 | April 28, 2005 | $ | 2,394 | $ | (1,540 | ) | $ | — | $ | 854 | ||||||||

| 2006 |

March 9, 2006 | 2005 | May 2, 2006 | 3,715 | (280 | ) | — | $ | 4,289 | |||||||||||

| 2007 |

February 22, 2007 | 2006 | April 5, 2007 | 3,083 | (1,001 | ) | — | $ | 6,371 | |||||||||||

| 2008 |

February 26, 2008 | 2007 | April 10, 2008 | 3,123 | — | — | $ | 9,494 | ||||||||||||

| 2009* |

February 27, 2009 | 2008 | N/A | — | — | — | $ | 9,494 | ||||||||||||

| May 9, 2009 | — | — | (9,494 | ) | $ | — | ||||||||||||||

| As of December 31, 2009 | $ | 12,315 | $ | (2,821 | ) | $ | (9,494 | ) | ||||||||||||

| * | Period through Marriott management agreement termination date, May 8, 2009. |

| Item 3. | Legal Proceedings |

In connection with the 2002 termination of the Meridien Hotels Inc. (“Meridien”) affiliates at the New Orleans and Dallas hotels, the Company was engaged in litigation with Meridien and related affiliates. On September 11, 2008, the Company entered into a Settlement Agreement with Meridien that resolved and released each of the parties’ respective claims, in consideration for a one-time payment by the Company in the amount of $5.5 million. The Company had previously accrued $1.2 million as a contingent liability, and as a result, the Company recognized an additional expense of $4.3 million for the year ended December 31, 2008, which is included in lease termination expense in the consolidated statement of operations.

The nature of operations of the hotels exposes the hotels, the Company and the Operating Partnership to the risk of claims and litigation in the normal course of their business. The Company is not presently subject to any material litigation nor, to the Company’s knowledge, is any litigation threatened against the Company, other than routine actions for negligence or other claims and administrative proceedings arising in the ordinary course of business, some of which are expected to be covered by liability insurance and all of which collectively are not expected to have a material adverse effect of the liquidity, results of operations or business or financial condition of the Company.

| Item 4. | Submission of Matters to a Vote of Security Holders |

There were no matters submitted to a vote of the Company’s shareholders during the fourth quarter of the year covered by this Annual Report on Form 10-K.

15

Table of Contents

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market Information

The common shares of the Company began trading on the New York Stock Exchange (“NYSE”) on April 24, 1998 under the symbol “LHO.” The following table sets forth, for the periods indicated, the high and low sale prices per common share and the cash distributions declared per share:

| Calendar Year 2009 | Calendar Year 2008 | |||||||||||||||||

| High | Low | Distribution | High | Low | Distribution | |||||||||||||

| First Quarter |

$ | 12.75 | $ | 3.57 | $ | 0.01 | $ | 33.29 | $ | 26.05 | $ | 0.51 | ||||||

| Second Quarter |

$ | 17.24 | $ | 5.31 | $ | 0.01 | $ | 34.45 | $ | 24.96 | $ | 0.51 | ||||||

| Third Quarter |

$ | 20.47 | $ | 10.34 | $ | 0.01 | $ | 30.24 | $ | 18.55 | $ | 0.525 | ||||||

| Fourth Quarter |

$ | 22.79 | $ | 16.28 | $ | 0.01 | $ | 24.00 | $ | 6.58 | $ | 0.255 | ||||||

The closing price for the Company’s common shares, as reported by the NYSE on December 31, 2009, was $21.23 per share.

16

Table of Contents

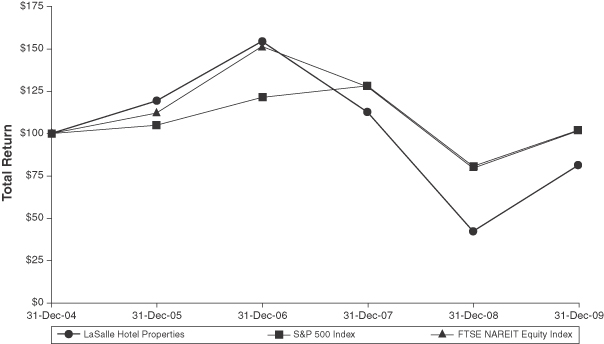

SHARE PERFORMANCE GRAPH

The following graph provides a comparison of the cumulative total return on the common shares of the Company from December 31, 2004 to the NYSE closing price per share on December 31, 2009 with the cumulative total return on the Standard & Poor’s 500 Composite Stock Price Index (the “S&P 500 Index”) and the FTSE National Association of Real Estate Investment Trusts Equity REITs Index (“FTSE NAREIT Equity Index”). Total return values were calculated assuming a $100 investment on December 31, 2004 with reinvestment of all dividends in (i) the common shares of the Company, (ii) the S&P 500 Index and (iii) the FTSE NAREIT Equity Index.

The actual returns on the graph above are as follows:

| Name |

Initial Investment at December 31, 2004 |

Value of Initial Investment at December 31, 2005 |

Value of Initial Investment at December 31, 2006 |

Value of Initial Investment at December 31, 2007 |

Value of Initial Investment at December 31, 2008 |

Value of Initial Investment at December 31, 2009 | ||||||||||||

| LaSalle Hotel Properties |

$ | 100.00 | $ | 119.27 | $ | 154.48 | $ | 112.64 | $ | 42.29 | $ | 81.54 | ||||||

| S&P 500 Index |

$ | 100.00 | $ | 104.91 | $ | 121.48 | $ | 128.15 | $ | 80.74 | $ | 102.11 | ||||||

| FTSE NAREIT Equity Index |

$ | 100.00 | $ | 112.16 | $ | 151.49 | $ | 127.72 | $ | 79.53 | $ | 101.79 | ||||||

Shareholder Information

As of February 12, 2010, there were 125 record holders of the Company’s common shares of beneficial interest, including shares held in “street name” by nominees who are record holders, and approximately 50,500 beneficial holders.

Distribution Information

For 2009, the Company paid $0.04 per common share in distributions, of which $0.04 was recognized as 2009 distributions for tax purposes. Additionally, distributions of $0.085 per common share for 2008 were

17

Table of Contents

recognized as 2009 distributions for tax purposes, bringing total 2009 distributions for tax purposes to $0.125 per common share. Of the $0.125, 100% represented ordinary income. Distributions for 2009 were paid quarterly to the Company’s common shareholders and common unitholders at a level of $0.01 per common share and limited partnership common unit.

For 2008, the Company paid $1.80 per common share in distributions, of which $1.715 was recognized as 2008 distributions for tax purposes. Additionally, distributions of $0.17 per common share for 2007 were recognized as 2008 distributions for tax purposes, bringing total 2008 distributions for tax purposes to $1.885 per common share. Of the $1.885, 64.9% represented ordinary income and 35.1% represented return of capital for tax purposes. These distributions were paid monthly to the Company’s common shareholders and common unitholders at a level of $0.17, $0.175 and $0.085 per common share and limited partnership common unit for the months of January 2008 through June 2008, July 2008 through September 2008 and October 2008 through December 2008, respectively.

The declaration of distributions by the Company is in the sole discretion of the Company’s Board of Trustees, and depends on the actual cash flow of the Company, its financial condition, capital expenditure requirements for the Company’s hotels, the annual distribution requirements under the REIT provisions of the Code and such other factors as the Board of Trustees deems relevant.

Operating Partnership Units and Recent Sales of Unregistered Securities

The Operating Partnership issued 3,181,723 common units of limited partnership interest to third parties on April 24, 1998 (inception), in conjunction with the initial public offering. The following is a summary of common unit activity since inception:

| Common units issued at initial public offering |

3,181,723 | ||

| Common units redeemed: |

|||

| 1999-2006 |

(3,164,860 | ) | |

| 2007 |

— | ||

| 2008 |

(33,530 | ) | |

| 2009 |

(70,000 | ) | |

| Common units issued: |

|||

| 2000-2006 |

86,667 | ||

| Common units outstanding at December 31, 2009 |

— | ||

Holders of common units of limited partnership interest receive distributions per unit in the same manner as distributions on a per common share basis to the common shareholders of beneficial interest.

Common shares issued upon redemption of common units of limited partnership interest were issued in reliance on an exemption from registration under Section 4(2) of the Securities Act of 1933. The Company relied on the exemption based on representations given by the limited partners that redeemed the units.

On November 17, 2006, in connection with the Company’s acquisition of Gild Hall and as part of the consideration for the hotel acquisition, the Operating Partnership issued 70,000 common units of limited partnership interest and 1,098,348 Series F Preferred Units (liquidation preference $25.00 per unit) of limited partnership interest. During 2008, all 1,098,348 of the Series F Preferred Units were redeemed for 568,786 common shares of beneficial interest and $14.5 million. During 2009, all 70,000 common units were redeemed for 69,500 common shares of beneficial interest and an insignificant amount of cash. The issuance of the common units and the Series F Preferred Units and the subsequent issuance of common shares upon the redemption of the common units and the Series F Preferred Units were each effected in reliance upon an exemption from registration provided by Section 4(2) under the Securities Act of 1933. The Company relied on the exemption based on representations given by the holder of the common units and the Series F Preferred Units.

18

Table of Contents

In August 2005, the Company acquired the Westin Copley Place in Boston, Massachusetts. As part of the consideration to acquire the hotel, the Operating Partnership issued 2,348,888 7.25% Series C Cumulative Redeemable Preferred Units (liquidation preference $25.00 per unit) of the Operating Partnership. The Series C Preferred Units were redeemable for 7.25% Series C Cumulative Redeemable Preferred Shares of Beneficial Interest (liquidation preference $25.00 per share), $0.01 par value per share, of the Company on a one-for-one basis. On February 1, 2009, each of the Series C Preferred Units was redeemed and the Company issued 2,348,888 7.25% Series C Cumulative Redeemable Preferred Shares of Beneficial Interest (the “Series C Preferred Shares”). Prior to the exchange described below, the Series C Preferred Shares were held by SCG Hotel DLP, L.P. (“SCG”). On April 16, 2009, SCG exchanged its Series C Preferred Shares for an equal number of 7.25% Series G Cumulative Redeemable Preferred Shares of Beneficial Interest (liquidation preference $25.00 per share), $0.01 par value per share (the “Series G Preferred Shares”), of the Company in a private transaction. Each of the issuance of the Series C Preferred Shares and the exchange of the Series C Preferred Shares for Series G Preferred Shares was exempt from registration pursuant to Section 4(2) of the Securities Exchange Act of 1933, as amended. On April 17, 2009, the Company filed a registration statement with the SEC to register the resale of the Series G Preferred Shares. On May 13, 2009, in connection with the exchange, SCG paid the Company a fee of $1.0 million, which the Company recognized as income.

| Item 6. | Selected Financial Data |

The following tables set forth selected historical operating and financial data for the Company. The selected historical operating and financial data for the Company for the years ended December 31, 2009, 2008, 2007, 2006 and 2005 have been derived from the historical financial statements of the Company. The following selected financial information should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and all of the financial statements and notes thereto included elsewhere in this Annual Report on Form 10-K.

19

Table of Contents

LASALLE HOTEL PROPERTIES

Selected Historical Operating and Financial Data

(Unaudited, dollars in thousands, except share data)

| For the year ended December 31, | ||||||||||||||||||||

| 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

| Operating Data: |

||||||||||||||||||||

| Revenues: |

||||||||||||||||||||

| Hotel operating revenues |

$ | 590,746 | $ | 663,006 | $ | 628,880 | $ | 562,380 | $ | 340,578 | ||||||||||

| Participating lease revenue |

— | 12,799 | 27,193 | 25,401 | 21,527 | |||||||||||||||

| Other income |

16,253 | 7,572 | 5,637 | 6,050 | 862 | |||||||||||||||

| Total revenues |

606,999 | 683,377 | 661,710 | 593,831 | 362,967 | |||||||||||||||

| Expenses: |

||||||||||||||||||||

| Hotel operating expenses |

390,300 | 424,357 | 399,764 | 365,125 | 232,042 | |||||||||||||||

| Depreciation and amortization |

109,896 | 106,748 | 92,338 | 77,019 | 46,790 | |||||||||||||||

| Real estate taxes, personal property taxes and insurance |

32,167 | 34,606 | 32,562 | 27,212 | 13,828 | |||||||||||||||

| Ground rent |

5,828 | 7,213 | 6,964 | 6,433 | 3,986 | |||||||||||||||

| General and administrative |

15,239 | 17,549 | 13,574 | 12,403 | 10,216 | |||||||||||||||

| Lease termination expense |