Attached files

Table of Contents

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-4858

INTERNATIONAL FLAVORS & FRAGRANCES INC.

(Exact name of registrant as specified in its charter)

| NEW YORK | 13-1432060 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 521 WEST 57TH STREET, NEW YORK, N.Y. | 10019 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code (212) 765-5500

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Stock, par value | New York Stock Exchange | |

| 12 1/2¢ per share |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendments to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

For the purpose of reporting the following market value of registrant’s outstanding common stock, the term “affiliate” refers to persons, entities or groups which directly or indirectly control, are controlled by, or are under common control with the registrant and does not include individual executive officers, directors or less than 10% shareholders. The aggregate market value of registrant’s common stock not held by affiliates as of June 30, 2009 was $2,584,509,708.

As of February 12, 2010, there were 79,235,120 shares of the registrant’s common stock, par value 12 1/2¢ per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s proxy statement for the 2010 Annual Meeting (the “IFF 2010 Proxy Statement”) are incorporated by reference in Part III of this Form 10-K.

Table of Contents

INTERNATIONAL FLAVORS & FRAGRANCES INC.

| PAGE | ||||

| PART I | ||||

| ITEM 1. |

3 | |||

| ITEM 1A. |

7 | |||

| ITEM 1B. |

10 | |||

| ITEM 2. |

10 | |||

| ITEM 3. |

11 | |||

| ITEM 4. |

13 | |||

| PART II | ||||

| ITEM 5. |

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 14 | ||

| ITEM 6. |

17 | |||

| ITEM 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 19 | ||

| ITEM 7A. |

38 | |||

| ITEM 8. |

39 | |||

| ITEM 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 40 | ||

| ITEM 9A. |

Controls and Procedures | 40 | ||

| ITEM 9B. |

41 | |||

| PART III | ||||

| ITEM 10. |

42 | |||

| ITEM 11. |

42 | |||

| ITEM 12. |

Security Ownership of Certain Beneficial Owners and Management, and Related Stockholder Matters | 42 | ||

| ITEM 13. |

Certain Relationships and Related Transactions, and Director Independence | 43 | ||

| ITEM 14. |

43 | |||

| PART IV | ||||

| ITEM 15. |

44 | |||

| 82 | ||||

2

Table of Contents

PART I

| ITEM 1. | BUSINESS. |

International Flavors & Fragrances Inc., incorporated in New York in 1909, and its subsidiaries (the “Registrant”, “IFF”, “we”, “us”, and “our”), is a leading creator and manufacturer of flavor and fragrance products used by other manufacturers to impart or improve flavor or fragrance in a wide variety of consumer products. Fragrance products are sold principally to manufacturers of perfumes, cosmetics, personal care products, hair care products, deodorants, soaps, detergents, fabric care and air care products; our flavor products are sold principally to manufacturers of prepared foods, beverages, pharmaceuticals, dairy and confectionery products as well as the food service industry.

We currently have 31 manufacturing facilities with the major manufacturing facilities located in the United States, Great Britain, Ireland, the Netherlands, Spain, Argentina, Brazil, Mexico, Australia, China, India, Indonesia, Japan and Singapore. The remaining manufacturing facilities are located in 8 other countries. We maintain our own sales and distribution facilities in 32 countries and are represented by sales agents and distributors in other countries. Our principal executive offices are located at 521 West 57th Street, New York, New York 10019 (212-765-5500).

MARKETS

Our flavor products are sold principally to the food and beverage industries for use in consumer products such as soft drinks, non-carbonated drinks, candies, baked goods, desserts, prepared foods, dietary foods, dairy products, drink powders, pharmaceuticals, snack foods and alcoholic beverages. Two of our largest customers for flavor products are major producers of prepared foods and beverages in the United States. In the three years ended December 31, 2009, 2008 and 2007, sales of flavor products accounted for 46%, 46% and 44%, respectively, of our total sales.

Our fragrance products are used by customers in the manufacture of various consumer goods in the home and personal care markets. The home market consists of laundry detergents, fabric care, candles, air fresheners and all-purpose cleaners. The personal care market consists of perfumes, colognes, after-shave lotions, skin care, lipsticks, deodorants and hair preparations. Most of the major global and regional manufacturers in each of these categories are our customers. Five of the largest global companies are among our principal customers. In the three years ended December 31, 2009, 2008 and 2007, sales of fragrance products accounted for 54%, 54% and 56%, respectively, of our total sales.

See Note 12, Segment Information, of the Notes to the Consolidated Financial Statements for information concerning the two business segments, Flavors and Fragrances, and our geographic regions.

PRODUCTS

Our principal fragrance and flavor products consist of compounds of large numbers of ingredients blended in proprietary formulas created by our perfumers and flavorists. Most of these compounds contribute the total fragrance or flavor to the consumer products in which they are used. This fragrance or flavor characteristic is often a major factor in the consumer selection and acceptance of the consumer end product. A smaller number of compounds are sold to manufacturers who further blend them to achieve the finished fragrance or flavor in their products. We produce thousands of compounds, and new compounds are constantly being created in order to meet the many and changing characteristics of our customers’ end products. Most of the fragrance and flavor compounds are created and produced for the exclusive use of particular customers. Our products are sold in powder and liquid forms and in amounts ranging from a few pounds to many tons, depending upon the nature of the product.

The ingredients that we use in our compounds are both synthetic and natural. We manufacture a substantial portion of the synthetic ingredients. While a majority of our synthetic ingredients production is used in our

3

Table of Contents

compounds, a substantial portion is also sold to others. Natural ingredients are derived from flowers, fruits and other botanical products as well as from animal products. They contain varying numbers of organic chemicals, which are responsible for the fragrance or flavor of the natural product. The natural products are purchased in processed or semi-processed form. Some are used in compounds in the state in which they are purchased and others after further processing. Natural products, together with various chemicals, are also used as raw materials for the manufacture of synthetic ingredients by chemical processes. Our flavor products also include extracts and seasonings derived from various fruits, vegetables, nuts, herbs and spices as well as microbiologically-derived ingredients.

MARKET DEVELOPMENTS

The demand for consumer products utilizing flavors and fragrances has been stimulated and broadened by changing social habits resulting from various factors such as increases in personal income, dual-earner households, teenage population, leisure time, urbanization, health and wellness concerns, including increased demand for nature based products and by the continued growth of emerging markets. In the fragrance field, these developments expanded the market for hair care, candles and air care products and deodorant and personal wash products with finer fragrance quality, as well as the market for colognes, toilet waters, men’s toiletries and other products beyond traditional luxury items such as perfumes. In the flavor field, similar market characteristics stimulated the demand for products such as convenience foods, soft drinks and low-fat and organic food products that must conform to expected tastes. New and improved methods of packaging, applying and dispensing have been developed for many consumer products that utilize some of our flavor or fragrance products. These developments called for the creation of new compounds and ingredients compatible with the newly introduced materials and methods of application.

PRODUCT DEVELOPMENT AND RESEARCH

The development of new flavors and fragrances is a complex technical and artistic process calling upon the combined knowledge and skill of our creative perfumers and flavorists, and our scientists. With extensive experience, the perfumers and flavorists continuously advance their skills for creating fragrances or flavors best suited to the market requirements of the customers’ products.

Scientists from various disciplines work in project teams with the perfumers and flavorists to develop flavor and fragrance products with consumer preferred performance characteristics. Scientific expertise includes: natural products research, plant science, organic chemistry, analytical chemistry, biochemistry, microbiology, process engineering, food science, material science and sensory science. Analytical and sensory science is applied to understand the complex interactions of the many ingredients in a consumer product in order to optimize the flavor or fragrance performance at all points of use. Material science technology is applied to create controlled release and delivery systems to enhance flavor and fragrance performance in consumer products. An important contribution to the creation of new flavor and fragrances is the discovery and development of new ingredients having improved fragrance or flavor value. The ingredients research program discovers molecules found in natural substances and creates new molecules that are subsequently tested for their fragrance or flavor value. The new molecules that meet rigorous requirements for commercial development are subsequently transferred to manufacturing operations for production.

Creative and technical product development is conducted in 33 fragrance and flavor laboratories in 26 countries. We maintain a research and development center at Union Beach, New Jersey. We spent $194 million in 2009, $209 million in 2008 and $197 million in 2007 on our research and development activities or about 8% to 9% of our revenues each year. We expect these expenditures to remain at this percentage level for 2010. Of the amount expended in 2009 on such activities, 62% was for fragrances and the balance was for flavors. We employed 1,091 persons in 2009 and 1,146 persons in 2008 in such activities.

Our business is not materially dependent upon any patents, trademarks or licenses.

4

Table of Contents

DISTRIBUTION

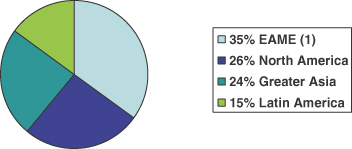

Distribution for both the flavors and fragrances business units is similar in that most of our sales are through our own sales force. The flavors business operates from two sales offices in the United States and 38 sales offices in 30 foreign countries, while the fragrances business operates from two sales offices in the United States and 36 sales offices in 29 foreign countries. Sales in additional countries are made through agents and distributors. For the year ended December 31, 2009, 35% of our sales were to customers in Europe, Africa and Middle East (“EAME”), 26% in North America, 24% in Greater Asia and 15% in Latin America.

During 2009, our 30 largest customers accounted for 57% of our sales. Sales to one customer accounted for 11% of our sales in 2009, 2008 and 2007. These sales were largely in the fragrance business unit.

GOVERNMENTAL REGULATION

The manufacture and sale of our products are subject to regulation in the United States by the Food and Drug Administration, the Department of Agriculture, the Bureau of Alcohol, Tobacco and Firearms, the Environmental Protection Agency, the Occupational Safety and Health Administration, the Drug Enforcement Administration and state authorities. Foreign subsidiaries are subject to similar regulation in a number of countries. In particular, the European Union will require extensive chemical registration and testing over the next 8 years. Compliance with existing governmental requirements regulating the discharge of materials into the environment has not materially affected our operations, earnings or competitive position. In 2010, we expect to spend approximately $6 to $8 million on capital projects and approximately $18 million in operating expenses and governmental charges for the purpose of complying with such requirements.

RAW MATERIAL PURCHASES

We purchase roughly 10,000 different raw materials from many sources all over the world. The principal natural raw materials consist of essential oils, extracts and concentrates which are derived from fruits, vegetables, flowers, woods and other botanicals, animal products and raw fruits. The principal synthetic raw material purchases consist of organic chemicals. We believe that alternate materials or alternate sources of materials are available to enable us to maintain our competitive position in the event of any interruption in the supply of raw materials from present sources.

COMPETITION

We have more than 50 competitors in the world markets. IFF is one of the top four companies, which together represent approximately 70% of the flavors and fragrances industry. While no single factor is responsible, our competitive position is based principally on the creative skills of our perfumers and flavorists, the technological advances resulting from our research and development activities, the quality of our customer service, the support provided by our marketing and application groups, and our understanding of consumers. We believe that we are one of the largest companies producing and marketing, on an international basis, a wide range of fragrance and flavor products for sale to manufacturers of consumer products. In particular countries and localities, we face competition from numerous companies specializing in certain product lines, among which are some companies larger than us and some more important in a particular product line or lines. Most of our customers do not buy all of their fragrance or flavor products from the same supplier, and some customers make their own fragrance or flavor compounds with ingredients supplied by us or others.

EMPLOYEE RELATIONS

At December 31, 2009, we employed approximately 5,400 persons, of whom approximately 1,400 were employed in the United States. We have not experienced a work stoppage or strike and consider our employee relations to be satisfactory.

5

Table of Contents

EXECUTIVE OFFICERS OF REGISTRANT

Effective October 1, 2009, the Company’s Board of Directors appointed Douglas D. Tough, a director of the Company since October 2008, as the Company’s Chairman of the Board. Mr. Tough, age 60, will also assume the role of Chief Executive Officer of the Company on March 1, 2010. Mr. Tough served as Chief Executive Officer and Managing Director of Ansell Limited, a global leader in healthcare barrier protective products, from July 2004 until February 2010.

The current executive officers of the Company, as of February 25, 2010, are listed below.

| Name |

Office and Other Business Experience(1) |

Age | Year First Became Officer | |||

| Kevin C. Berryman |

Member, Temporary Office of the Chief Executive Officer since October 2009 (2); Executive Vice President and Chief Financial Officer since May 2009; Chief Financial Officer, Nestle Professional, Americas, a global foodservice manufacturer, from October 2008 to May 2009; Senior Vice President Group Controller, Nestle S.A., an international food and beverage company, from June 2006 to September 2008; Chief Financial Officer, Nestle Purina Petcare, a manufacturer of pet products, from December 2001 to May 2006. | 51 | 2009 | |||

| Beth E. Ford |

Executive Vice President, Head of Supply Chain since October 2008; Executive Vice President and Chief Operating Officer, Hachette Book Group, a leading US trade publisher, from September 2007 to September 2008; Senior Vice President, Global Operations and Information Technology, Scholastic, Inc., a global publishing, education and media company, prior thereto. | 45 | 2008 | |||

| Nicolas Mirzayantz |

Member, Temporary Office of the Chief Executive Officer since October 2009 (2); Group President, Fragrances since January 2007; Senior Vice President, Fine Fragrance and Beauty Care and Regional Manager, North America Region from April 2005 to December 2006; Senior Vice President, Fine Fragrance and Beauty Care from October 2004 to March 2005; Vice President, Global Business Development, Fine Fragrance and Toiletries, prior thereto. | 47 | 2002 | |||

| Hernan Vaisman |

Member, Temporary Office of the Chief Executive Officer since October 2009 (2); Group President, Flavors since January 2007; Vice President, Latin America Region from October 2004 to December 2006; Regional Finance Director, Latin America Region, prior thereto. | 51 | 2004 | |||

| Angelica T. Cantlon |

Senior Vice President, Human Resources since August 2009; Senior Vice President-International Chief Administrative Officer, MetLife, Inc., an insurance and financial services company, from June 2005 to August 2009 and Senior Vice President-Human Resources Business Leader, prior thereto. | 58 | 2009 | |||

| Dennis M. Meany |

Senior Vice President, General Counsel and Secretary since January 2004. | 62 | 2004 | |||

6

Table of Contents

| Name |

Office and Other Business Experience(1) |

Age | Year First Became Officer | |||

| Richard A. O’Leary |

Vice President and Controller since June 2009; Interim Chief Financial Officer from July 2008 to May 2009; Vice President, Corporate Development from July 2007 to May 2009; Finance Director, International Paper’s, a paper and packaging company, Brazilian affiliate from August 2004 to June 2007; Finance Director, International Paper’s Shorewood Packaging Unit, prior thereto. | 49 | 2007 |

| (1) | Employed by the Company or an affiliated company for the last five years, except as otherwise indicated. |

| (2) | The temporary Office of the Chief Executive Office (CEO) will be in place until Mr. Tough assumes the CEO position. |

We make available free of charge on or through the Investor Relations link on our website, www.iff.com, all materials that we file electronically with the SEC, including our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports, filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after electronically filing such materials with, or furnishing them to, the SEC. During the period covered by this Form 10-K, we made all such materials available through our website as soon as reasonably practicable after filing such materials with the SEC.

You may also read and copy any materials filed by us with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, DC 20549, and you may obtain information on the operation of the Public Reference Room by calling the SEC in the U.S. at 1-800-SEC-0330. In addition, the SEC maintains an Internet website, www.sec.gov, that contains reports, proxy and information statements and other information that we file electronically with the SEC.

A copy of our Corporate Governance Guidelines, Code of Business Conduct and Ethics, and the charters of the Audit Committee, Compensation Committee, and Nominating and Governance Committee of the Board of Directors are posted on the Investor Relations section of our website, www.iff.com.

| ITEM 1A. | RISK FACTORS. |

The following are some important factors that could cause the Company’s actual results to differ materially from those referred to or implied in any forward-looking statement. These are in addition to the risks and uncertainties discussed elsewhere in this Annual Report of Form 10-K and in the Company’s other filings with the Securities and Exchange Commission.

The current volatility in global economic conditions and the financial markets may adversely affect our industry, business and results of operations.

The volatility and disruption to the capital and credit markets since mid-2008 has rapidly impacted global economic conditions, resulting in significant recessionary pressures and declines in consumer confidence and economic growth. These conditions have led to economic contractions in the developed economies and reduced growth rates in the emerging markets. Despite fiscal and monetary intervention, it is possible that further declines in consumer spending and global growth rates may occur in the foreseeable future. Reduced consumer spending may cause changes in customer order patterns including order cancellations, and changes in the level of inventory at our customers, which may adversely affect our industry, business and results of operations. The impact of the credit crisis and economic slowdown will vary by region and country. The diversity of our geographic customer and operating footprint limits our reliance and exposure to any single economy.

7

Table of Contents

These conditions have also resulted in a substantial tightening of the credit markets, including lending by financial institutions and in the commercial paper market, both of which are sources of credit for our borrowing and liquidity. This tightening of the credit markets has increased the cost of capital and reduced the availability of credit. Based on our latest discussions, we believe that the financial institutions syndicated under our revolving credit facility are able to fulfill their commitments as of our filing date. It is difficult to predict how long the current economic and capital and credit market conditions will continue, whether they will continue to deteriorate and which aspects of our products or business could be adversely affected. However, if current levels of economic and capital and credit market disruption and volatility continue or worsen, there can be no assurance that we will not experience an adverse impact, which may be material, on our business, the cost of and access to capital and credit markets, and our results of operations. In addition, we monitor the financial condition of our customers on a regular basis based on public information or data provided directly to us. If the financial condition of one of our major customers was negatively impacted by market conditions or liquidity, we could be adversely impacted in terms of accounts receivable and/or inventory specifically attributable to them.

Failure to maintain the integrity of our raw materials, supply chain and finished goods may adversely impact sales and our results of operations, IFF’s reputation and litigation costs.

The manufacture and sale of our products are subject to various regulatory requirements in each of the countries in which our products are manufactured and sold. In addition, we are subject to product safety and compliance requirements established by the industry or similar oversight bodies. We use a variety of strategies, methodologies and tools to identify current products standards, assess relative risks in our supply chain that can impact product integrity, monitor internal and external performance and test raw materials and finished goods to minimize the likelihood of product non-compliance.

If a non-compliance event went undetected, we could be subject to customer claims, penalties, litigation costs and/or settlements, remediation costs or loss of sales. These consequences would be exacerbated if our customer did not identify the defect and there was a resulting impact at the consumer level. This could lead to potentially large scale adverse publicity and potential consumer litigation.

Competitive factors may negatively impact our sales and marketability.

The market for flavors and fragrances is fragmented and highly competitive. IFF competes with many companies and some of our competitors specialize in one or more of our product segments while others participate in many of the same segments. In addition, some of our competitors may have greater financial and technical resources. The discovery and development of new flavor and fragrance materials, protection of the Company’s intellectual property and development and retention of key employees are important issues in our ability to compete in our businesses. Increased competition by existing or future competitors, including aggressive price competition, could result in the need for us to reduce prices or increase spending and this could have an impact on sales and profitability.

We are subject to economic and social changes which may impact sales.

Demand for consumer products using flavors and fragrances has been stimulated and broadened by changing social habits resulting from factors such as increases in personal income, dual-earner households, teenage population, leisure time, health concerns and urbanization and by the continued growth in world population. Changes in any number of external economic factors, or changes in social or consumer preferences, could adversely impact our results of operations. Nearly 60% of our sales occur in the developed markets of North America, Western Europe and Australasia with the remainder in emerging markets. Accordingly, the impact on our operations will depend upon consumer spending on products for which we supply the flavor or fragrance in these global markets.

Results may be negatively impacted by the price, quality and availability of raw materials.

Raw materials are purchased from many sources from all over the world, including essential oils, extracts and concentrates derived from fruits, vegetables, flowers, woods and other botanicals, animal products, raw fruits

8

Table of Contents

and organic chemicals. Disruptions in the supply or quality of ingredients or rising prices for ingredients purchased could adversely impact our results of operations and profitability. Historically, we have experienced the greatest amount of volatility in natural products that represent approximately 50% of raw material purchases. Availability and pricing of these products can be impacted by crop size and quality, demand balance or alternative land use. To mitigate our sourcing risk, we maintain strategic stock levels covering multiple periods for critical items and/or time purchases to capitalize on favorable market conditions.

Results may be negatively impacted by the inability to implement our business strategy, including the achievement of anticipated cost savings, profitability or growth targets.

We are committed to those particular business strategies and market segments that have been identified as likely to drive profitable future growth and improve operations and customer service. If we are unable to successfully and timely implement these strategies, it would adversely impact our financial condition and results of operations.

Results may be negatively affected by the impact of currency fluctuation or devaluation in principal foreign markets and the effectiveness of hedging and risk management strategies.

Our operations are conducted in many countries, the results of which are reported in the local currency and then translated into U.S. dollars at applicable exchange rates. The exchange rates between these currencies and the U.S. dollar have fluctuated and may continue to do so in the future. We employ a variety of techniques to reduce the impact of exchange rate fluctuations, including sourcing strategies and a limited number of foreign currency hedging activities. However, volatility in currency exchange rates may adversely impact our reported results of operations, financial condition or liquidity.

Results may be negatively impacted by the outcome of uncertainties related to litigation.

We are involved in a number of legal claims. While we believe that related insurance coverage is adequate with respect to such claims, we cannot predict the ultimate outcome of such litigation. In addition, we cannot provide assurance that future events will not result in an increase in the number of claims or require an increase in the amount accrued for any such claims, or require accrual for one or more claims that has not been previously accrued.

Results and cash flows may be negatively impacted by future pension funding and other postretirement obligations.

We establish assumptions concerning discount rates and actuarial assumptions regarding pension funding and other postretirement benefit obligations based on current market conditions, plan participants, asset returns, interest rates and other factors. Changes in pension and other postretirement benefits, plan assets, and associated expenses may occur in the future due to changes in capital markets, employee demographics and actuarial assumptions. These changes may adversely impact our financial condition, results of operations or liquidity.

Results may be negatively impacted by the effect of legal and regulatory requirements, as well as restrictions imposed on operations by foreign and domestic governmental entities.

The manufacture and sale of our products are subject to regulation in the United States by the Food and Drug Administration, the Department of Agriculture, the Bureau of Alcohol, Tobacco and Firearms, the Environmental Protection Agency, the Occupational Safety and Health Administration, the Drug Enforcement Administration and state authorities. In addition, we are subject to product safety and compliance requirements established by the industry or similar oversight bodies. Our foreign operations are subject to similar substantial governmental regulation and oversight standards in a number of countries, including extensive requirements within the European Union. Costs or investments necessary to maintain compliance with existing or future governmental regulations may adversely impact our financial condition, results of operations or liquidity.

9

Table of Contents

We may face risks associated with events which may affect the world economy.

World events such as terrorist attacks, or regional conflicts have and may in the future weaken world economies. Any resulting weaknesses in these economies may adversely affect our business or the businesses of our customers, with a resultant negative impact on our financial condition, results of operations or liquidity.

Our success depends on attracting and retaining talented people within our business. Any shortfall in recruitment or retention could adversely affect our ability to compete and achieve our strategic goals.

Attracting, developing, and retaining talented employees is essential to the successful delivery of our products and success in the marketplace. However, we cannot be certain that we will be able to attract and retain such employees in the future. Any shortfalls in recruitment or retention could adversely affect our ability to operate successfully, grow our business, and effectively compete with our competitors.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS. |

None.

| ITEM 2. | PROPERTIES. |

Our principal properties are as follows:

| Location |

Operation | |

| United States |

||

| Augusta, GA |

Production of fragrance ingredients. | |

| Carrollton, TX(1) |

Production of flavor compounds; flavor laboratories. | |

| Hazlet, NJ(1) |

Production of fragrance compounds; fragrance laboratories. | |

| Jacksonville, FL |

Production of fragrance ingredients. | |

| New York, NY(1) |

Fragrance laboratories. | |

| South Brunswick, NJ(1) |

Production of flavor compounds and ingredients; flavor laboratories. | |

| Union Beach, NJ |

Research and development center. | |

| France |

||

| Neuilly(1) |

Fragrance laboratories. | |

| Grasse |

Production of flavor and fragrance ingredients; fragrance laboratories. | |

| Great Britain |

||

| Haverhill |

Production of flavor compounds and ingredients, and fragrance ingredients; flavor laboratories. | |

| Ireland |

||

| Drogheda |

Production of fragrance compounds. | |

| Netherlands |

||

| Hilversum |

Flavor and fragrance laboratories. | |

| Tilburg |

Production of flavor compounds and ingredients, and fragrance compounds. | |

| Spain |

||

| Benicarlo |

Production of fragrance ingredients. | |

| Argentina |

||

| Garin |

Production of flavor compounds and ingredients, and fragrance compounds; flavor laboratories. | |

10

Table of Contents

| Location |

Operation | |

| Brazil |

||

| Rio de Janeiro |

Production of fragrance compounds. | |

| São Paulo |

Flavor and fragrance laboratories. | |

| Taubate |

Production of flavor compounds and ingredients. | |

| Mexico |

||

| Tlalnepantla |

Production of flavor and fragrance compounds; flavor and fragrance laboratories. | |

| India |

||

| Chennai(2) |

Production of flavor compounds and ingredients, and fragrance compounds; flavor laboratories. | |

| Australia |

||

| Dandenong |

Production of flavor compounds and flavor ingredients. | |

| China |

||

| Guangzhou(4) |

Production of flavor and fragrance compounds. | |

| Shanghai(6) |

Flavor and fragrance laboratories. | |

| Xin’anjiang(5) |

Production of fragrance ingredients. | |

| Zhejiang(4) |

Production of fragrance ingredients. | |

| Indonesia |

||

| Jakarta(3) |

Production of flavor compounds and ingredients, and fragrance compounds and ingredients; flavor and fragrance laboratories. | |

| Japan |

||

| Gotemba |

Production of flavor compounds. | |

| Tokyo |

Flavor and fragrance laboratories. | |

| Singapore |

||

| Jurong(6) |

Production of flavor and fragrance compounds. | |

| Science Park(1) |

Flavor and fragrance laboratories. | |

| (1) | Leased. |

| (2) | We have a 93.4% interest in the subsidiary company that owns this facility. |

| (3) | Land is leased and building is partially leased and partially owned. |

| (4) | Land is leased and building and machinery and equipment are owned. |

| (5) | We have a 90% interest in the subsidiary company that leases the land and owns the buildings and machinery. |

| (6) | Building is leased and machinery and equipment are owned. |

Our principal executive offices and New York laboratory facilities are located at 521 West 57th Street, New York City.

| ITEM 3. | LEGAL PROCEEDINGS. |

We are subject to various claims and legal actions in the ordinary course of our business. For purposes of reporting these actions, Bush Boake Allen, Inc. (“BBA”), a wholly-owned subsidiary of IFF, and/or IFF are referred to as the “Company”.

In September 2001, the Company was named as a defendant in a purported class action brought against it in the Circuit Court of Jasper County, Missouri, on behalf of employees of a plant owned and operated by Gilster-Mary Lee Corp. in Jasper, Missouri (“Benavides case”). The plaintiffs alleged that they sustained respiratory injuries in the workplace due to the use by Gilster-Mary Lee of a BBA and/or IFF flavor.

11

Table of Contents

In January 2004, the Court ruled that class action status was not warranted. As a result of this decision, each of the 47 plaintiff cases was to be tried separately. Subsequently, 8 cases were tried to a verdict, 4 verdicts resulted for the plaintiffs and 4 verdicts resulted for the Company, all of which were appealed by the losing party. Subsequently all plaintiff cases related to the Benavides case, including those on appeal, were settled.

Seventeen actions based on similar claims of alleged respiratory illness due to workplace exposure to flavor ingredients are currently pending against the Company and other flavor suppliers and related companies.

In July 2004, the Company and another flavor supplier were named defendants, and subsequently 10 third and fourth party defendants were added, in a lawsuit by 4 former workers (and 2 spouses for loss of consortium) at a Ridgeway, Illinois factory in an action brought in the Circuit Court for the Second Judicial Circuit, Gallatin County, Illinois (Batteese case). In August 2005, the Company and 22 other companies were named defendants in a lawsuit by 2 former employees of the Gilster-Mary Lee facility in McBride, Missouri in the Missouri Circuit Court, 32nd Judicial Circuit (Fults case). In August 2006, the Company and 3 other flavor and chemical suppliers were named defendants in a lawsuit by 16 current and former employees of the Gilster-Mary Lee facility in Jasper, Missouri in the Missouri Circuit Court of Jasper County (Arles case) and 2 other current and former employees in the same Court (Bowan case).

In January 2007, the Company and another flavor supplier were named defendants in a lawsuit in Hamilton County, Ohio Court of Common Pleas by 83 current and former employees (plus 35 spousal loss of consortium claims) of two separate Marion, Ohio factories (Aldrich case). Three plaintiff cases were settled by confidential agreement in June 2009. In June 2007, the Company and another flavor supplier were named defendants in a lawsuit filed in Hamilton County, Ohio Court of Common Pleas by 18 current and former employees (plus 5 spousal loss of consortium claims) of a Marion, Ohio facility (Arnold case). In July 2007, the Company and another flavor manufacturer were named defendants in a lawsuit filed in Hamilton County, Ohio Court of Common Pleas by 43 current and former workers (plus 15 spousal loss of consortium claims) of two Marion, Ohio facilities (Adamson case). In July 2007, the Company was joined as a defendant in a case filed in June 2005 against 5 companies and a trade association in the 8th Judicial District Court of Montana by the widow of the former owner/operator of a popcorn business in Montana (Yatsko case).

In March 2008, the Company and another flavor supplier were named defendants in two lawsuits in the Hamilton County, Ohio Court of Common Pleas, one by 9 current and former employees and the spouses of two such employees of a popcorn plant in Marion, Ohio (Ferguson case) and the other by 10 current and former employees and 3 spouses of such employees of the same plant (Brown case). In May 2008, the Company and 6 other companies were named defendants in a lawsuit in the District Court of Colorado by a consumer of microwave popcorn and his spouse (Watson case). In August 2008, the Company and 7 other flavor and material suppliers were named defendants in a lawsuit by 9 plaintiffs (plus 8 loss of consortium claims) in the Hamilton County Court of Common Pleas (Auld case). In September 2008, the Company, three other flavor companies and three other companies were named defendants in a lawsuit in the U.S. District Court for the Eastern District of Washington by a consumer of microwave popcorn and his spouse (Newkirk case). The Company was dismissed from this case in October 2009. In September 2008, the Company, another flavor manufacturer and 2 chemical suppliers were named defendants in a lawsuit by 1 plaintiff in the Missouri Circuit Court of Jasper County (Meredith case). The Company was dismissed from this case in October 2009. In October 2008, the Company, 2 other flavor compounders, 2 chemical companies, a microwave popcorn manufacturer and a distributor were named defendants in a lawsuit by a consumer of microwave popcorn and her spouse in the Circuit Court of Jackson County, Missouri (Khouri case). The Company was dismissed from this case in October 2009.

In September 2009, the Company, another flavor supplier and an employer were named as defendants in a lawsuit by the child of a worker at a Ridgeway, Illinois factory in an action brought in the Circuit Court of Cook County, Illinois (Patton case). In September 2009, the Company and another flavor supplier were named as defendants in a lawsuit by two workers and one spouse (Gerfen case) and by another worker (Bradshaw case) at a Marion, Ohio microwave popcorn plant in actions filed in the Court of Common Pleas, Hamilton County, Ohio.

12

Table of Contents

In October 2009, the Company and another flavor supplier were named as defendants in a lawsuit by a worker at a Marion, Ohio microwave popcorn plant in an action filed in the Court of Common Pleas, Hamilton County, Ohio (Criswell case). In December 2009, the Company, 5 other flavor manufacturers and 5 microwave popcorn manufacturers and distributors were named defendants in a lawsuit in the U.S. District Court for the Northern District of Iowa by a consumer of microwave popcorn and her husband (Daughetee case).

The Company believes that all IFF and BBA flavors at issue in these matters meet the requirements of the U.S. Food and Drug Administration and are safe for handling and use by workers in food manufacturing plants when used according to specified safety procedures. These procedures are detailed in instructions that IFF and BBA provided to all their customers for the safe handling and use of their flavors. It is the responsibility of IFF’s customers to ensure that these instructions, which include the use of appropriate engineering controls, such as adequate ventilation, proper handling procedures and respiratory protection for workers, are followed in the workplace.

At each balance sheet date, or more frequently as conditions warrant, the Company reviews the status of each pending claim, as well as its insurance coverage for such claims with due consideration given to potentially applicable deductibles, retentions and reservation of rights under its insurance policies, and the advice of its outside legal counsel and a third party expert in modeling insurance deductible amounts with respect to all of these matters. While the ultimate outcome of any litigation cannot be predicted, management believes that adequate provision has been made with respect to all known claims. Based on information presently available and in light of the merits of its defenses and the availability of insurance, the Company does not expect the outcome of the above cases, singly or in the aggregate, to have a material adverse effect on the Company’s financial condition, results of operation or liquidity. There can be no assurance that future events will not require the Company to increase the amount it has accrued for any matter or accrue for a matter that has not been previously accrued. See Note 16 of the Notes to the Consolidated Financial Statements.

Over the past 20 years, various federal and state authorities and private parties have claimed that the Company is a Potentially Responsible Party (“PRP”) as a generator of waste materials for alleged pollution at a number of waste sites operated by third parties located principally in New Jersey and have sought to recover costs incurred and to be incurred to clean up the sites.

The Company has been identified as a PRP at ten facilities operated by third parties at which investigation and/or remediation activities may be ongoing. The Company analyzes its liability on a regular basis. The Company accrues for environmental liabilities when they are probable and estimable. The Company estimates its share of the total future cost for these sites to be less than $5 million.

While joint and several liability is authorized under federal and state environmental laws, the Company believes the amounts it has paid and anticipates paying in the future for clean-up costs and damages at all sites are not and will not be material to the Company’s financial condition, results of operations or liquidity. This conclusion is based upon, among other things, the involvement of other PRPs at most sites, the status of proceedings, including various settlement agreements and consent decrees, the extended time period over which payments will likely be made and an agreement reached in July 1994 with three of the Company’s liability insurers pursuant to which defense costs and indemnity amounts payable by the Company in respect of the sites will be shared by the insurers up to an agreed amount.

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS. |

None.

13

Table of Contents

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES. |

Market Information.

Our common stock is traded principally on the New York Stock Exchange. The high and low stock prices for each quarter during the last two years were:

| 2009 | 2008 | |||||||||||

| Quarter |

High | Low | High | Low | ||||||||

| First |

$ | 32.35 | $ | 25.30 | $ | 47.20 | $ | 39.48 | ||||

| Second |

33.51 | 29.84 | 46.44 | 39.06 | ||||||||

| Third |

39.15 | 31.21 | 44.47 | 38.27 | ||||||||

| Fourth |

41.85 | 36.85 | 39.33 | 24.90 | ||||||||

Approximate Number of Equity Security Holders.

| (A) Title of Class |

(B) Number of shareholders of record as of February 12, 2010 | |

| Common stock, par value 12 1/2¢ per share | 3,004 |

Dividends.

Cash dividends declared per share for each quarter during the two most recent fiscal years were as follows:

| Quarter |

2009 | 2008 | ||||

| First |

$ | 0.25 | $ | 0.23 | ||

| Second |

0.25 | 0.23 | ||||

| Third |

0.25 | 0.25 | ||||

| Fourth |

0.25 | 0.25 | ||||

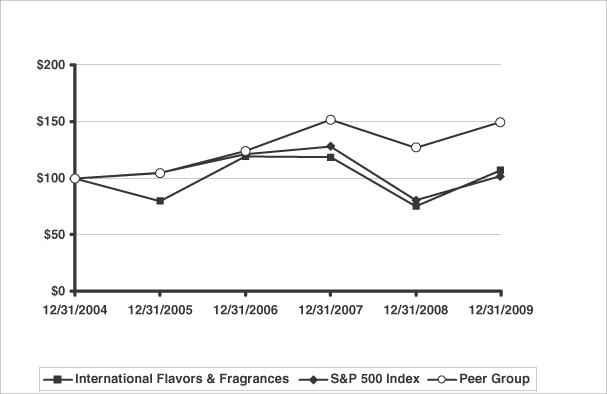

Performance Graph.

Total Return To Shareholders(1)

(Includes reinvestment of dividends)

| Annual Return Percentage Years Ending | ||||||||||

| Company Name / Index |

2005 | 2006 | 2007 | 2008 | 2009 | |||||

| International Flavors & Fragrances |

-20.21 | 49.64 | -0.36 | -36.64 | 42.43 | |||||

| S&P 500 Index |

4.91 | 15.79 | 5.49 | -37.00 | 26.46 | |||||

| Peer Group |

4.58 | 18.66 | 22.37 | -16.32 | 18.05 | |||||

| Indexed Returns Years Ending | ||||||||||||||||||

| Company Name / Index |

Base Period 2004 |

2005 | 2006 | 2007 | 2008 | 2009 | ||||||||||||

| International Flavors & Fragrances |

$ | 100 | $ | 79.79 | $ | 119.40 | $ | 118.97 | $ | 75.38 | $ | 107.36 | ||||||

| S&P 500 Index |

100 | 104.91 | 121.48 | 128.16 | 80.74 | 102.11 | ||||||||||||

| Peer Group |

100 | 104.58 | 124.09 | 151.85 | 127.07 | 150.00 | ||||||||||||

14

Table of Contents

| Peer Group Companies(2) |

||||

| Alberto Culver Company | Hormel Foods Corp. | Unilever NV | ||

| Avon Products | Kellogg Co. | YUM Brands, Inc. | ||

| Campbell Soup Co. | Estee Lauder Companies, Inc. | |||

| Church & Dwight Inc. | McCormick & Company, Inc. | |||

| Clorox Company | McDonald’s Corp. | |||

| Coca-Cola Company | Nestle SA | |||

| Colgate-Palmolive Co. | Pepsico Inc. | |||

| ConAgra Foods, Inc. | Procter & Gamble Co. | |||

| General Mills Inc. | Revlon Inc. | |||

| H.J. Heinz Co. | Sara Lee Corp. | |||

| Hershey Company | Sensient Technologies Corp. |

| (1) | The Cumulative Shareholder Return assumes that the value of an investment in our Common Stock and each index was $100 on December 31, 2004, and that all dividends were reinvested. |

| (2) | Due to the international scope and breadth of our business, we believe that a Peer Group comprised of international public companies, which are representative of the customer group to which we sell our products, is the most appropriate group against which to compare shareholder returns. Wm. Wrigley Jr. Company has been eliminated from the Peer Group for all years presented above due to its acquisition by Mars, Incorporated in October 2008. |

15

Table of Contents

Issuer Purchases of Equity Securities.

The following table presents the total number of shares purchased during the fourth quarter of 2009, the average price paid per share, the number of shares that were purchased as part of a publicly announced repurchase program, and the maximum number of shares that may yet be purchased under the program for the quarter ended December 31, 2009.

| Total Number of Shares Purchased(1) |

Average Price Paid per Share |

Total Number of Shares Purchased as Part of Publicly Announced Program(1) |

Maximum Number of Shares That May Yet Be Purchased Under the Program(1) | |||||

| October 1 – 31, 2009 |

— | — | — | 1,949,065 | ||||

| November 1 – 30, 2009 |

— | — | — | 1,949,065 | ||||

| December 1 – 31, 2009 |

— | — | — | 1,949,065 | ||||

| Total shares purchased |

— | — | — |

| (1) | In July 2007 our Board of Directors authorized a stock repurchase plan (the “2007 Share Repurchase Plan”) to repurchase up to 15% (which represents an aggregate 13,350,000 shares) or $750 million worth of our outstanding common stock, whichever is less. As of December 31, 2009, we are subject to the 15% limitation and as such, we still have the ability to repurchase approximately 2 million shares. There is no stated expiration for the July 2007 share repurchase program. |

16

Table of Contents

| ITEM 6. | SELECTED FINANCIAL DATA. |

INTERNATIONAL FLAVORS & FRAGRANCES INC.

QUARTERLY FINANCIAL DATA (UNAUDITED)

(DOLLARS IN THOUSANDS EXCEPT PER SHARE AMOUNTS)

The following selected consolidated financial data is derived from our Consolidated Financial Statements. This data should be read in conjunction with the Consolidated Financial Statements and Notes thereto, and with Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations.

| Net Income Per Share(b) | ||||||||||||||||||||||||||||||

| Net Sales | Gross Profit | Net Income(a) | Basic | Diluted | ||||||||||||||||||||||||||

| Quarter |

2009 | 2008 | 2009 | 2008 | 2009 | 2008 | 2009 | 2008 | 2009 | 2008 | ||||||||||||||||||||

| First |

$ | 559,630 | $ | 596,605 | $ | 222,200 | $ | 245,482 | $ | 47,197 | $ | 55,948 | $ | 0.60 | $ | 0.69 | $ | 0.60 | $ | 0.69 | ||||||||||

| Second |

568,261 | 636,126 | 228,097 | 263,781 | 48,083 | 67,032 | 0.61 | 0.84 | 0.60 | 0.83 | ||||||||||||||||||||

| Third |

612,634 | 617,538 | 248,969 | 246,739 | 52,800 | 57,684 | 0.67 | 0.73 | 0.66 | 0.73 | ||||||||||||||||||||

| Fourth |

585,633 | 539,103 | 235,860 | 214,632 | 47,446 | 48,964 | 0.60 | 0.62 | 0.59 | 0.62 | ||||||||||||||||||||

| $ | 2,326,158 | $ | 2,389,372 | $ | 935,126 | $ | 970,634 | $ | 195,526 | $ | 229,628 | $ | 2.48 | $ | 2.89 | $ | 2.46 | $ | 2.86 | |||||||||||

| (a) | Net Income Q2-2009 included $2,685 related to restructuring costs driven by weak economic conditions impacting our Fragrance business and $680 pertaining to employee separation costs. Q3-2009 includes $9,186 of restructuring related costs associated with facility rationalizations within our European Fragrance business. Q3-2009 also includes $3,348 of costs associated with the change in our Chief Executive Officer. Q4-2009 includes $2,892 of additional costs associated with the ongoing reorganization of our European businesses and $4 million of expense related to out-of-period tax adjustments. |

Net Income in the 2008 first and fourth quarters included $4,555 and $8,082 of restructuring costs; the first quarter also included a benefit of $1,612 from insurance recovery related to a 2005 product contamination matter; Net Income in the second, third and fourth quarters of 2008 included $2,217, $1,374 and $211, respectively, of employee separation and implementation costs. Net Income in the 2008 first, second and fourth quarters also include tax benefits of $2,106, $3,897 and $17,067.

| (b) | The sum of the 2009 and 2008 quarters’ Net Income per share does not equal the earnings per share for the full year due to changes in average shares outstanding. |

17

Table of Contents

INTERNATIONAL FLAVORS & FRAGRANCES INC.

FIVE-YEAR SUMMARY

(DOLLARS IN THOUSANDS EXCEPT PER SHARE AMOUNTS)

| 2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||||||

| Consolidated Statement of Income Data |

|||||||||||||||||||

| Net sales |

$ | 2,326,158 | $ | 2,389,372 | $ | 2,276,638 | $ | 2,095,390 | $ | 1,993,393 | |||||||||

| Cost of goods sold(b) |

1,391,032 | 1,418,738 | 1,324,424 | 1,211,259 | 1,168,992 | ||||||||||||||

| Research and development expenses(b)(g) |

193,843 | 209,295 | 196,893 | 183,512 | 179,812 | ||||||||||||||

| Selling and administrative expenses(b) |

376,541 | 381,841 | 375,287 | 351,923 | 339,323 | ||||||||||||||

| Amortization of intangibles |

6,153 | 6,153 | 12,878 | 14,843 | 15,071 | ||||||||||||||

| Curtailment loss |

— | — | 5,943 | — | — | ||||||||||||||

| Restructuring and other charges, net(a) |

18,301 | 18,212 | — | 2,680 | 23,319 | ||||||||||||||

| Interest expense |

61,818 | 74,008 | 41,535 | 25,549 | 23,956 | ||||||||||||||

| Other (income) expense, net |

1,921 | (2,797 | ) | (11,136 | ) | (9,838 | ) | (3,268 | ) | ||||||||||

| 2,049,609 | 2,105,450 | 1,945,824 | 1,779,928 | 1,747,205 | |||||||||||||||

| Income before taxes |

276,549 | 283,922 | 330,814 | 315,462 | 246,188 | ||||||||||||||

| Taxes on income(g) |

81,023 | 54,294 | 83,686 | 88,962 | 53,122 | ||||||||||||||

| Net income |

$ | 195,526 | $ | 229,628 | $ | 247,128 | $ | 226,500 | $ | 193,066 | |||||||||

| Percentage of net sales |

8.4 | 9.6 | 10.9 | 10.8 | 9.7 | ||||||||||||||

| Percentage of average shareholders’ equity |

28.9 | 38.0 | 32.0 | 24.6 | 20.9 | ||||||||||||||

| Net income per share — basic |

$ | 2.48 | $ | 2.89 | $ | 2.84 | $ | 2.50 | $ | 2.06 | |||||||||

| Net income per share — diluted |

$ | 2.46 | $ | 2.86 | $ | 2.81 | $ | 2.48 | $ | 2.04 | |||||||||

| Average number of shares (thousands) |

78,403 | 79,032 | 86,541 | 90,443 | 93,584 | ||||||||||||||

| Consolidated Balance Sheet Data |

|||||||||||||||||||

| Cash and cash equivalents |

$ | 80,135 | $ | 178,467 | $ | 151,471 | $ | 114,508 | $ | 272,545 | |||||||||

| Receivables, net |

444,265 | 400,971 | 400,527 | 357,155 | 304,823 | ||||||||||||||

| Inventories |

444,977 | 479,567 | 484,222 | 446,606 | 430,794 | ||||||||||||||

| Property, plant and equipment, net |

501,293 | 496,856 | 508,820 | 495,124 | 499,145 | ||||||||||||||

| Goodwill and intangible assets, net |

720,530 | 726,683 | 732,836 | 745,716 | 772,651 | ||||||||||||||

| Total assets(d) |

2,644,774 | 2,749,913 | 2,726,314 | 2,478,904 | 2,638,196 | ||||||||||||||

| Bank borrowings, overdrafts and current portion of long-term debt |

76,780 | 101,982 | 152,473 | 15,897 | 819,392 | ||||||||||||||

| Long-term debt |

934,749 | 1,153,672 | 1,060,168 | 791,443 | 131,281 | ||||||||||||||

| Total Shareholders’ equity(b) (c) (d) (f) |

771,910 | 580,642 | 626,359 | 916,056 | 925,808 | ||||||||||||||

| Other Data |

|||||||||||||||||||

| Current ratio(e) |

2.3 | 2.6 | 2.1 | 2.4 | 1.0 | ||||||||||||||

| Gross additions to property, plant and equipment |

$ | 66,819 | $ | 85,395 | $ | 65,614 | $ | 58,282 | $ | 93,433 | |||||||||

| Depreciation and amortization expense |

78,525 | 75,986 | 82,788 | 89,733 | 91,928 | ||||||||||||||

| Cash dividends declared |

78,962 | 75,902 | 76,465 | 68,956 | 68,397 | ||||||||||||||

| per share |

$ | 1.00 | $ | 0.96 | $ | 0.88 | $ | 0.765 | $ | 0.73 | |||||||||

| Number of shareholders of record at year-end |

3,004 | 3,167 | 3,248 | 3,393 | 3,207 | ||||||||||||||

| Number of employees at year-end |

5,377 | 5,338 | 5,315 | 5,087 | 5,160 | ||||||||||||||

| (a) | Restructuring and other charges ($14,763 after tax) in 2009, ($12,583 after tax) in 2008, ($1,982 after tax) in 2006, and ($15,857 after tax) in 2005, were the result of various restructuring and reorganization programs of the Company. |

| (b) | 2006 — 2009 amounts include equity compensation expense in accordance with ASC 718 “Compensation — Stock Compensation”. See Note 11 to the Consolidated Financial Statements for additional details. |

| (c) | The 2006 amounts reflect adoption of ASC 715 “Compensation — Retirement Benefits”. See Note 13 to the Consolidated Financial Statements for additional details. |

| (d) | The 2007 amounts reflect adoption of ASC 740 “Income Taxes”. See Note 9 to the Consolidated Financial Statements for additional details. |

| (e) | Current ratio is equal to current assets divided by current liabilities. |

| (f) | Includes noncontrolling interests for all periods presented. See Note 1 to the Consolidated Financial Statements for additional details. |

| (g) | The 2005 — 2008 periods have been revised to properly recognize R&D expense, net of R&D credits. Previously, these credits were reflected as a reduction of tax expense. |

18

Table of Contents

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. |

(UNLESS INDICATED OTHERWISE, DOLLARS IN MILLIONS EXCEPT PER SHARE AMOUNTS)

Organization of Information

Management’s Discussion and Analysis provides a narrative on our operating performance, financial condition and liquidity and should be read in conjunction with the accompanying financial statements. It includes the following sections:

| Ÿ | Executive Overview |

| Ÿ | Sales Commentary |

| Ÿ | Consolidated Operating Results |

| Ÿ | Goodwill and Intangible Assets |

| Ÿ | Restructuring and Other Charges |

| Ÿ | Income Taxes |

| Ÿ | Postretirement Benefits |

| Ÿ | Financial Condition |

| Ÿ | Critical Accounting Policies and Use of Estimates |

| Ÿ | New Accounting Standards |

| Ÿ | Non-GAAP Financial Measures |

| Ÿ | Cautionary Statement Under The Private Securities Litigation Reform Act of 1995 |

Executive Overview

We are a leading creator and manufacturer of flavor and fragrance compounds used to impart or improve the flavor or fragrance in a wide variety of consumer products. The precise size of the global market for flavors and fragrances is difficult to determine because the industry is highly fragmented, both geographically and along product lines; there are a limited number of publicly traded companies in the industry; certain customers maintain in-house capabilities fulfilling a portion of their flavor or fragrance needs; and the quality and depth of market information in developing regions of the world is limited. Analysts generally estimate the global market to be $15 billion of which IFF represents 16%; the largest competitor in the industry has approximately a 25% market share. IFF is one of the top four companies, which together represent approximately 70% of the flavors and fragrances industry.

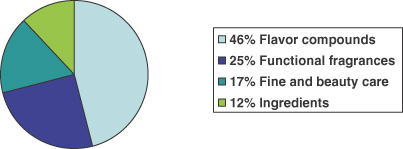

IFF is organized into two units that reflect our flavor and fragrance businesses. Approximately 46% of our 2009 net sales were flavor compounds. Flavor compounds are sold to the food and beverage industries for use in consumer products such as prepared foods, beverages, dairy, food and confectionery products. The remaining 54% of sales, representing the fragrance business unit, were in three fragrance categories: functional fragrances, including fragrance compounds for personal care (e.g., soaps) and household products (e.g., detergents and cleaning agents); fine fragrance and beauty care, including perfumes, colognes and toiletries; and ingredients, consisting of natural and synthetic ingredients that can be combined with other materials to create unique functional and fine fragrance compounds. Major fragrance customers include the cosmetics industry, including perfume and toiletries manufacturers, and the household products industry, including manufacturers of soaps, detergents, fabric care, household cleaners and air fresheners. Approximately 55% of our ingredient production is consumed internally; the balance is sold to third party customers.

The under-pinning of structural growth for the flavor and fragrance industry are population growth, an expanding middle class and technology. Changing social habits resulting from such factors as increases in

19

Table of Contents

personal income, leisure time, health and wellness and urbanization stimulate demand for consumer products utilizing flavors and fragrances. These developments also drive the creation and development of new molecules, technologies and/or solutions that facilitate and improve the end-use consumption of flavors and fragrances in consumer products.

Flavors and fragrances are generally:

| Ÿ | created for the exclusive use by a specific customer; |

| Ÿ | sold in powder or liquid form, in amounts ranging from a few pounds to several tons depending on the nature of the end product in which they are used; |

| Ÿ | a small percentage of the volume and cost of the end product sold to the consumer; and |

| Ÿ | a major factor in consumer selection and acceptance of the product. |

The flavors and fragrances industry is impacted by macroeconomic factors in all product categories and geographic regions. Such factors include the impact of currency on the price of raw materials and operating costs as well as on translation of reported results. In addition, IFF is susceptible to margin pressures due to customers’ cost improvement programs and input cost increases. However, these pressures can often be mitigated through a combination of product reformulation, sourcing strategies and material substitution plus internal cost containment efforts, and the development of innovative and streamlined solutions and processes.

We produce more than 33,000 unique compounds, of which approximately 60% are flavors and 40% fragrances. We continually create new compounds to meet the changing characteristics and needs of our customers’ end products. No single compound represents more than 2% of net sales. Development of flavors and fragrances is a complex artistic and technical process calling upon the combined knowledge and talents of creative perfumers and flavorists, and application and research chemists. An important element of creation is the development of new ingredients. We bear essentially all costs incurred in connection with the creation and development of new flavors and fragrances and such formulae are generally protected under trade secrecy. We are not materially dependent on any patents, trademarks or licenses.

IFF’s success in the flavors and fragrances industry is driven by our ability to create unique sensory experiences that meet evolving consumer needs and expectations. These solutions are delivered in a cost-efficient manner in conjunction with world-class customer service.

STRATEGIC DRIVERS

To increase shareholder value, we pursue and develop a value-creation model that encompasses three main elements: investing in research & development to identify and commercialize new, innovative materials and delivery systems; maintaining a deep understanding of both consumer preferences and consumer product brands; and excellence in our creative capabilities. Our goal is to deliver differentiated solutions that enable our customers’ brands to win in the marketplace.

In order to pursue these strategies, our organization is focused on ensuring that we efficiently create, produce, and sell unique, superior, and economically competitive products through our world class integration of research and development, consumer insight, creativity, via excellence in execution. We believe we are well positioned to achieve success by targeting strategically important global and regional customers in both developed and emerging markets; attracting, developing and retaining top talent; investing in research and development; and fostering a culture of innovation, accountability and continuous improvement.

CHANGE IN MANAGEMENT

Effective September 30, 2009, Robert Amen resigned as Chairman of the Board of Directors (“Chairman”) and Chief Executive Officer (“CEO”) of the Company. Douglas D. Tough, currently a Company Board member,

20

Table of Contents

assumed the position of non-executive Chairman effective October 1, 2009 and will assume the position of executive Chairman and CEO on March 1, 2010. Pending Mr. Tough’s assumption of his title and duties as CEO, beginning October 1, 2009 the Company established a temporary Office of the CEO, which is comprised of three current Company executives, Executive Vice President and Chief Financial Officer, Kevin Berryman; Group President, Fragrances, Nicolas Mirzayantz; and Group President, Flavors, Hernan Vaisman. Each of these executives remains in their current positions while carrying out their Office of the CEO responsibilities. The Office of the CEO reports to the Board of Directors.

Sales Commentary

A breakdown of sales by principal product category is depicted in the graph below.

2009 Sales by Category

Our five largest customers comprise 33% of consolidated sales and our top 30 customers 57%; these percentages have remained fairly constant for several years, although sales to larger customers are trending higher. We have one customer that accounts for 11% of our sales. A key factor for commercial success is inclusion on the strategic customers’ core supplier lists, opening opportunities to win new business. We are on the core supplier lists of a large majority of our strategic customers.

Net sales by business unit for 2009, 2008 and 2007 were as follows:

| Net Sales |

2009 | Percent Change |

2008 | Percent Change |

2007 | ||||||||||

| Flavors |

$ | 1,081 | -1 | % | $ | 1,092 | 9 | % | $ | 1,006 | |||||

| Fragrances |

1,245 | -4 | % | 1,297 | 2 | % | 1,271 | ||||||||

| Total net sales |

$ | 2,326 | -3 | % | $ | 2,389 | 5 | % | $ | 2,277 | |||||

2009 Sales by Destination

We manage our operations by global business units but utilize destination sales as a supplemental performance measure and indicator of underlying market trends. Although reported sales and earnings are affected by the weakening or strengthening of the U.S. dollar, this has not had a long-term effect on the underlying competitiveness of our business.

21

Table of Contents

Net sales by destination for 2009, 2008 and 2007 were as follows:

| Sales by Destination |

2009 | Percent Change |

2008 | Percent Change |

2007 | ||||||||||

| EAME(1) |

$ | 808 | -11 | % | $ | 907 | 6 | % | $ | 858 | |||||

| North America |

600 | 0 | % | 601 | -4 | % | 630 | ||||||||

| Greater Asia |

575 | 5 | % | 547 | 13 | % | 483 | ||||||||

| Latin America |

343 | 3 | % | 334 | 9 | % | 306 | ||||||||

| Total net sales, as reported |

$ | 2,326 | -3 | % | $ | 2,389 | 5 | % | $ | 2,277 | |||||

| (1) | Europe, Africa and Middle East |

2009 in Comparison to 2008

Sales for 2009 totaled $2,326 million, decreasing 3% from the prior year period of $2,389 million, as Flavor sales declined 1% and Fragrance sales decreased 4%. Foreign exchange had a 3% negative impact on reported sales during 2009 as the U.S. dollar was stronger during the first three-quarters of 2009 versus the comparable year-ago period. Market conditions improved during the second half of 2009, as global economic conditions strengthened and customer inventory levels stabilized. Local currency (LC) sales increased over 2% during both the third and fourth quarters compared to a decline of 3% during the first six months of 2009.

Flavors Business Unit

Flavor sales decreased 1% for 2009 compared to 2008 as the effects of a stronger U.S. dollar, soft demand and inventory corrections in Europe and customer specific losses in Latin America more than offset new wins, solid demand and price increases in North America and Greater Asia. Excluding the impact of currencies, sales for the Flavors business increased over 2% during 2009 compared to 2008.

Fragrances Business Unit

Fragrance sales decreased 4% for 2009 compared to 2008 reflecting double-digit LC sales declines for Fine Fragrances, as consumers reduced discretionary spending and the industry significantly reduced inventories across the supply chain. These headwinds were partially offset by solid growth and new wins in beauty care, toiletries and substantially all functional fragrance categories. Excluding the impact of currencies, sales for the Fragrances business declined 1% during 2009 compared to 2008.

Sales by Region and Category

Regional and product category sales performance for 2009 compared to 2008, in reported dollars and local currency, was as follows:

| % Change in Sales — 2009 vs 2008 | ||||||||||||||

| Fine & Beauty Care |

Functional | Ingredients | Total Frag. |

Flavors | Total | |||||||||

| North America |

Reported | -14% | 1% | 5% | -3% | 3% | 0% | |||||||

| EAME |

Reported | -24% | -3% | -11% | -13% | -7% | -11% | |||||||

| Local Currency | -18% | 2% | -6% | -8% | 0% | -5% | ||||||||

| Latin America |

Reported | 8% | 4% | -2% | 5% | 0% | 3% | |||||||

| Local Currency | 9% | 5% | -1% | 5% | 4% | 5% | ||||||||

| Greater Asia |

Reported | 17% | 14% | -1% | 12% | 1% | 5% | |||||||

| Local Currency | 20% | 16% | -3% | 13% | 4% | 7% | ||||||||

| Total |

Reported | -12% | 3% | -4% | -4% | -1% | -3% | |||||||

| Local Currency | -8% | 5% | -2% | -1% | 2% | 0% | ||||||||

22

Table of Contents

Local Currency Sales Drivers

| Ÿ | North America sales were flat as the erosion and volume declines in Fine Fragrance and Flavors compounds offset more than $40 million in new product introductions, plus modest price realization in Flavors and Functional Fragrance. Ingredient sales growth was mainly attributable to cost driven price increases. |

| Ÿ | EAME sales declines in LC were driven by de-stocking and weak underlying demand for Fine Fragrances and Ingredients that more than offset solid win performance in Functional Fragrances. Flavor sales were effectively flat as new wins in Savory and Confectionary plus pricing were offset by customer inventory reductions across most categories. |

| Ÿ | Latin America sales growth was 5% in LC led by near double-digit growth in the Fine Fragrances and Beauty Care and solid performance in the Functional Fragrances and Flavors categories. The growth was primarily driven by new product introductions of approximately $15 million combined with price increases across both businesses. |

| Ÿ | Greater Asia LC sales growth was largely driven by more than $15 million in new product introductions in Fabric and Hair Care, combined with approximately $10 million in new product introductions in Flavors which more than offset the effects of customer inventory reductions in the Ingredients category supply chain. |

2008 in Comparison to 2007

Sales totaled $2,389 million for 2008, up 5% from 2007; Flavor and Fragrance sales increased 9% and 2%, respectively. 2008 sales benefited from the generally weaker U.S. dollar and at comparable exchange rates would have increased 2% over the prior year.

Flavors Business Unit

Flavor sales increased 9% for 2008 based on new wins across all regions, particularly in the beverage category, led by a 21% increase in Latin America. Excluding the impact of currencies, sales growth for the Flavors business was 6%.

Fragrances Business Unit

Fragrance sales increased 2%. Excluding the impact of currencies, Fragrance sales declined 1% as strong growth in emerging markets was offset by weakness in the U.S. market. New product introductions of fragrance compounds were offset by volume declines primarily in the U.S. and EAME. Ingredient sales benefited from price increases, partially offset by volume declines as part of a product rationalization initiative and weaker economies in the U.S. and EAME.

Sales By Region and Category

Regional and product category sales performance for 2008 compared to the prior year, in reported dollars and local currency, was as follows:

| % Change in Sales — 2008 vs 2007 | ||||||||||||||

| Fine & Beauty Care |

Functional | Ingredients | Total Frag. |

Flavors | Total | |||||||||

| North America |

Reported | -14% | -10% | -2% | -10% | 2% | -4% | |||||||

| EAME |

Reported | 2% | 8% | 6% | 5% | 7% | 6% | |||||||

| Local Currency | -4% | 2% | -1% | -1% | 2% | 0% | ||||||||

| Latin America |

Reported | 7% | -2% | 17% | 3% | 21% | 9% | |||||||

| Local Currency | 6% | -2% | 17% | 3% | 18% | 8% | ||||||||

| Greater Asia |

Reported | 19% | 13% | 11% | 14% | 13% | 13% | |||||||

| Local Currency | 17% | 12% | 7% | 12% | 10% | 11% | ||||||||

| Total |

Reported | 0% | 3% | 5% | 2% | 9% | 5% | |||||||

| Local Currency | -4% | 0% | 1% | -1% | 6% | 2% | ||||||||

23

Table of Contents

Local Currency Sales Drivers

| Ÿ | North America flavors new product introductions of $22 million and some benefit from price increases were largely offset by volume declines. Weak economic conditions and significant slowdown in customer order activity led to volume declines in fine and functional fragrance compounds and ingredients. Fine fragrance sales were also negatively impacted by customer inventory corrections in the first half of the year. |

| Ÿ | Flavors sales in EAME were up as new product introductions of $22 million were partially offset by volume declines. Fine and functional fragrance new product introductions of $18 million and $15 million were offset by volume declines. Price increases in ingredients were offset by volume declines. |

| Ÿ | Latin America flavors sales were strong throughout the region, driven mainly by new product introductions of $19 million. Fragrance sales growth was driven by new product introductions of $10 million offset by volume decreases, primarily in functional. Ingredients sales benefited from higher volumes coupled with price increases. |

| Ÿ | Greater Asia sales growth in Flavors was driven by new product introductions of $16 million plus volume and price increases. Fragrance sales benefited from new product introductions of $25 million, partially offset by volume declines. |

Consolidated Operating Results

The percentage relationship of cost of goods sold and other operating expenses to reported sales is detailed as follows:

| 2009 | 2008 | 2007 | ||||

| Cost of goods sold |

59.8% | 59.4% | 58.2% | |||

| Research and development expenses |

8.3% | 8.8% | 8.6% | |||

| Selling and administrative expenses |

16.2% | 16.0% | 16.5% |