Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Form 10-K

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Fiscal Year Ended December 31, 2009

Commission file number 1-15967

The Dun & Bradstreet Corporation

(Exact name of registrant as specified in its charter)

| Delaware | 22-3725387 | |

| (State of incorporation) | (I.R.S. Employer Identification No.) | |

| 103 JFK Parkway, Short Hills, NJ | 07078 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (973) 921-5500

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, par value $0.01 per share Preferred Share Purchase Rights |

New York Stock Exchange New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of June 30, 2009, the aggregate market value of all shares of Common Stock of The Dun & Bradstreet Corporation outstanding and held by nonaffiliates* (based upon its closing transaction price on the New York Stock Exchange Composite Tape on June 30, 2009) was approximately $4.256 billion.

As of January 31, 2010, 50,998,069 shares of Common Stock of The Dun & Bradstreet Corporation were outstanding.

Documents Incorporated by Reference

Portions of the registrant’s definitive proxy statement for use in connection with its annual meeting of shareholders scheduled to be held on May 4, 2010, are incorporated into Part III of this Form 10-K.

| * | Calculated by excluding all shares held by executive officers and directors of the registrant. Such exclusions will not be deemed to be an admission that all such persons are “affiliates” of the registrant for purposes of federal securities laws. |

Table of Contents

| Page | ||||

| PART I | ||||

| Item 1. |

3 | |||

| Item 1A. |

11 | |||

| Item 1B. |

18 | |||

| Item 2. |

18 | |||

| Item 3. |

19 | |||

| Item 4. |

19 | |||

| PART II | ||||

| Item 5. |

20 | |||

| Item 6. |

22 | |||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

25 | ||

| Item 7A. |

67 | |||

| Item 8. |

68 | |||

| 71 | ||||

| 72 | ||||

| 73 | ||||

| 74 | ||||

| 75 | ||||

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

137 | ||

| Item 9A. |

137 | |||

| PART III | ||||

| Item 10. |

138 | |||

| Item 11. |

138 | |||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

138 | ||

| Item 13. |

Certain Relationships and Related Transactions and Director Independence |

138 | ||

| Item 14. |

139 | |||

| PART IV | ||||

| Item 15. |

140 | |||

| 141 | ||||

| 142 | ||||

2

Table of Contents

PART I

| Item 1. | Business |

Overview

The Dun & Bradstreet Corporation (“D&B” or “we” or “our” or the “Company”) is the world’s leading source of commercial information and insight on businesses, enabling customers to Decide with Confidence® for over 168 years. Our global commercial database contains more than 150 million business records. The database is enhanced by our proprietary DUNSRight® Quality Process, which provides our customers with quality business information. This quality information is the foundation of our global solutions that customers rely on to make critical business decisions.

D&B provides solution sets that meet a diverse set of customer needs globally. Customers use D&B Risk Management Solutions™ to mitigate credit and supplier risk, increase cash flow and drive increased profitability; D&B Sales & Marketing Solutions™ to increase revenue from new and existing customers; and D&B Internet Solutions™ to convert prospects into clients faster by enabling business professionals to research companies, executives and industries.

Our Aspiration and Our Strategy

Our strategy reflects that D&B is a company that has been and remains committed to delivering Total Shareholder Return (“TSR”). To achieve this objective, we remain focused on three key drivers of TSR over time: revenue growth; margin expansion; and maintaining a disciplined approach to deploying our free cash flow. These have been the central drivers of our success, and they will remain the key areas of focus for us going forward. We continue to execute our strategy in the following ways:

| • | First, we remain focused on the commercial marketplace and continuing to be the world’s largest and best provider of insight about businesses. This is reflected in our aspiration, which is “To be the most trusted source of commercial insight so our customers can Decide with Confidence®.” |

| • | Second, maintaining our fundamental competitive advantage in the market place (i.e. data quality), We will continue to improve our data quality through better coverage and we will provide new value to our customers by leveraging recent advances in technology. |

| • | Third, we will leverage our data assets to better enhance our products and services within our three solution sets: Risk Management Solutions business (“RMS”), Sales & Marketing Solutions business (“S&MS”) and Internet Solutions. To accomplish this, we will invest in a new technology platform that is scalable and far more agile, so we can meet emerging customer demands faster, and at a much lower cost over time. |

3

Table of Contents

Our strategy relies on four core competitive advantages that support our commitment to driving TSR and our aspiration to be the most trusted source of commercial insight so our customers can Decide with Confidence®. These core competitive advantages include our:

| • | Trusted Brand; |

| • | DUNSRight Quality Process; |

| • | Winning Culture; and |

| • | Financial Flexibility. |

For the reasons described below, we believe that these core competitive advantages will continue to drive our growth and profitability going forward.

Trusted Brand

The D&B® brand dates back to the founding of our company in 1841. We believe that the D&B brand is unique in the marketplace, standing for trust and confidence in commercial insight; our customers rely on D&B and the quality of our brand when they make critical business decisions.

DUNSRight Quality Process

DUNSRight is our proprietary quality process that powers all of our customer solution sets and serves as our key strategic differentiator as a commercial insight company.

The foundation of our DUNSRight Quality Process is Quality Assurance, which includes over 2,000 separate automated and manual checks to ensure that data meets our high quality standards.

In addition, our five DUNSRight Quality Drivers work sequentially to enhance the data and make it useful to our customers in making critical business decisions.

The process works as follows:

| • | Global Data Collection brings together data from a variety of sources worldwide; |

| • | We integrate the data into our database through our patented Entity Matching, which produces a single, more accurate picture of each business; |

| • | We apply the D-U-N-S® Number as a unique means of identifying and tracking a business globally throughout every step in the life and activity of the business; |

| • | We use Corporate Linkage to enable our customers to view their total risk or opportunity across related businesses; and |

| • | Finally, our Predictive Indicators use statistical analysis to rate a business’ past performance, to predict how a business is likely to perform in the future. |

Winning Culture

Our culture is focused on developing strong leaders, because we believe that great leadership drives great results, improves customer satisfaction and helps increase TSR. To build such leadership, we have developed and deployed a consistent, principles-based leadership model throughout our Company.

Our leadership development process ensures that team member performance goals and financial rewards are linked to our strategy. In addition, we link a component of the compensation of each of our senior leaders to our overall financial results. Our leadership development process also enables team members, which include our management and employees, to receive ongoing feedback on their performance goals and on their leadership. All

4

Table of Contents

team members are expected to have personal leadership action plans that are focused on their own personal development, building on their leadership strengths and working on their areas of development.

We have a talent assessment process that provides a framework to assess and improve skill levels and performance across the organization and which acts as a tool to aid talent development and succession planning. We also administer an employee engagement survey that enables team members worldwide to provide feedback on areas that will improve their performance, drive customer satisfaction and evolve our winning culture.

Financial Flexibility

Financial Flexibility is an ongoing process that reallocates our spending from low-growth or low-value activities to activities that will create greater value for shareholders through enhanced revenue growth, improved profitability and/or quality improvements. We are committed through this process to examining how every dollar is spent, and optimizing between variable and fixed costs to ensure flexibility in changes to our operating expense base as we make strategic choices. This enables us to continually and systematically identify improvement opportunities in terms of quality, cost and customer experience. In executing our Financial Flexibility process we seek to improve, standardize, consolidate and automate our business functions.

Segments

We currently manage and report our business globally through two segments:

| • | North America (which consists of our operations in the United States (“U.S.”) and Canada); and |

| • | International (which consists of our operations in Europe, Asia Pacific and Latin America). |

As of January 1, 2009, we began managing our operations in Canada as part of our renamed “North America” segment (formerly our U.S. segment) and have reclassified our historical results set forth in this Annual Report on Form 10-K to reflect this change. Prior to January 1, 2009, we reported the results of our Canadian operations together with our International segment.

North America. Our North America segment accounted for 78%, 79% and 81% of our total revenue for the years ended December 31, 2009, 2008 and 2007, respectively.

International. We conduct business internationally through our wholly-owned subsidiaries, joint ventures that we hold a majority interest in, independent correspondents, strategic relationships through our D&B Worldwide Network® and minority equity investments. The International segment, which primarily represents revenue generated through our subsidiaries, accounted for 22%, 21% and 19 % of our total revenue for the years ended December 31, 2009, 2008 and 2007, respectively.

Since 2000, we have entered into strategic relationships with strong local players throughout the world that we do not control and who have become part of our D&B Worldwide Network, operating under commercial agreements. Our D&B Worldwide Network enables our customers globally to make business decisions with confidence, because we incorporate data from the members of the D&B Worldwide Network that has been put through the DUNSRight Quality Process into our database and utilize it in our customer solutions. Our customers, therefore, have access to a more powerful database and global solution sets they can rely on to make their risk management, sales and marketing decisions. Over the last few years, we have strengthened our position in our International segment through majority-owned joint ventures in Japan, China and India.

In addition, we have from time-to-time, acquired complementary businesses, products and technologies. For example:

| • | In 2007, we acquired First Research, Inc., Purisma Incorporated, AllBusiness.com, Inc. and substantially all of the assets of n2 Check Limited and substantially all of the assets and certain liabilities of the Education Division of Automation Research, Inc., d/b/a MKTG Services; |

5

Table of Contents

| • | In 2007, we established majority owned joint ventures in China with Huaxia International Credit Consulting Co. Ltd. and in Japan with Tokyo Shoko Research; |

| • | In 2008, we established majority-owned joint ventures in China with Beijing Huicong International Information Co., Ltd., and we increased our indirect minority ownership stake in Dun & Bradstreet Information Services India Private Limited (“D&B India”) to a 53% direct majority ownership; and |

| • | In 2009, we acquired substantially all of the assets of Bisnode’s UK operations and a 100% equity interest in Bisnode’s Irish operations (“ICC”), we acquired all of the assets and assumed certain liabilities related to Quality Education Data and we acquired a 90% equity interest in RoadWay International Limited (“RoadWay”), the leading provider of integrated services of direct marketing in China. As part of the RoadWay transaction, D&B Huaxia, our existing joint venture company with Huaxia in China, transferred its Sales & Marketing Solutions business to RoadWay. |

Segment data and other information for the years ended December 31, 2009, 2008 and 2007 are included in Note 14 to our consolidated financial statements included in Item 8. of this Annual Report on Form 10-K.

Our Customer Solutions and Services

Risk Management Solutions

Risk Management Solutions is our largest customer solution set, accounting for 64%, 62% and 62% of our total revenue for the years ended December 31, 2009, 2008 and 2007, respectively. Within this customer solution set we offer traditional and value-added solutions. Our traditional solutions, which includes our DNBi® Solution and also consists of reports from our database used primarily for making decisions about new credit applications, constituted 75% of our Risk Management Solutions revenue and 48% of our total revenue for the year ended December 31, 2009. Our value-added solutions, which constituted 20% of our Risk Management Solutions revenue and 12% of our total revenue for the year ended December 31, 2009, generally support automated decision-making and portfolio management through the use of scoring and integrated software solutions. See Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations of this Annual Report on Form 10-K for a discussion of trends in this customer solutions set.

On January 1, 2008, we began managing our Supply Management business as part of our Risk Management Solutions business. This is consistent with our overall strategy and also reflects customers’ needs to better understand the financial risk of their supply chain. As a result, the contributions of the Supply Management business are now reported as a part of Risk Management Solutions, as set forth above.

Our Risk Management Solutions help customers increase cash flow and profitability while mitigating credit, operational and regulatory risks by helping them answer questions such as:

| • | Should I extend credit to this new customer? |

| • | What credit limit should I set? |

| • | Will this customer pay me on time? |

| • | How can I avoid supply chain disruption? |

| • | How do I know whether I am in compliance with regulatory acts? |

Our principal Risk Management Solutions are:

| • | DNBi, our interactive, customizable online application that offers our customers real time access to our most complete and up-to-date global DUNSRight information, comprehensive monitoring and portfolio analysis; |

6

Table of Contents

| • | Our Business Information Report, our Comprehensive Report, and our International Report, which provide overall profiles of a company, including, based on the report type, financial information, payment information, history of a business, ownership details, operational information and similar information; |

| • | Our Self Awareness Solutions, which allow our small business customers to establish, improve and protect their own credit; |

| • | Our decisioning scores, which help assess the credit risk of a business by assigning a rating or score; and |

| • | Supply Lifecycle Risk Management™, which is an online solution that allows customers to standardize their supplier registration and evaluation process by creating a single point of entry with consistent procedures. |

Certain of our solutions are available on a subscription pricing basis, such as our Preferred Pricing Agreement with DNBi. Our subscription pricing plans, which continue to represent an increasing proportion of our revenue, provide increased access to our Risk Management reports and data to help customers increase their profitability while mitigating their risk.

Sales & Marketing Solutions

Sales & Marketing Solutions is our second-largest customer solution set accounting for 28% of our total revenue for each of the years ended December 31, 2009, 2008 and 2007. Within this customer solution set we offer traditional and value-added solutions. Our traditional solutions generally consist of marketing lists, labels and customized data files used by our customers in their direct mail and marketing activities. These solutions constituted 40% of our Sales & Marketing Solutions revenue and 11% of our total revenue for the year ended December 31, 2009. Our value-added solutions generally include decision-making and customer information management solutions. These value-added solutions constituted 60% of Sales & Marketing Solutions revenue and 17% of our total revenue for the year ended December 31, 2009. See Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations of this Annual Report on Form 10-K for a discussion of trends in this customer solutions set.

Our Sales & Marketing Solutions help customers increase revenue from new and existing customers by helping them answer questions such as:

| • | Who are my best customers? |

| • | How can I find prospects that look like my best customers? |

| • | How can I exploit untapped opportunities with my existing customers? |

| • | How can I allocate sales force resources to revenue growth potential? |

Our principal Sales & Marketing Solutions are:

| • | Our solutions for Customer Data Integration, which are a suite of solutions that cleanse, identify, link and enrich customer information with our DUNSRight Quality Process. Our D&B Optimizer™ solution, for example, uses our DUNSRight Quality Process to transform customer prospects and files into up-to-date, accurate and actionable commercial insight, enabling a single customer view across multiple systems and touchpoints, such as marketing and billing databases and better enabling a customer to make sales and marketing decisions; and |

| • | Our Direct Marketing Lists, which benefit from our DUNSRight Quality Process to enable our customers to create an accurate and comprehensive marketing campaign. |

7

Table of Contents

Internet Solutions

Our Internet Solutions business provides highly organized, efficient and easy-to-use products that address the online business intelligence needs of professionals and small businesses, including information on companies, industries and executives, integration tools that bring this information into the day-to-day workflow of our customers, and research and advice regarding starting up and managing a business.

Internet Solutions represent the results of our Hoover’s business, including both the First Research division and the AllBusiness.com division. Internet Solutions accounted for 7% of our total revenue for the each of the years ended December 31, 2009, 2008 and 2007. See Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations of this Annual Report on Form 10-K for a discussion on trends in this customer solutions set.

Growth to our Internet Solutions business depends upon the development of improved and new products targeted to our primary customer segments, as well as the development of Internet products targeted to the needs of customer segments outside our core audience.

Hoover’s provides information on public and private companies, and on industries and executives, sales, marketing and research professionals worldwide. The database includes industry and company briefs, information on competitors, corporate financials, executive contact information, current news and research, family trees, and contact information including biographies. Hoover’s subscribers primarily access the data online via Hoover’s Online®.

First Research is a leading Internet provider of editorial-based industry insight, specifically tailored toward sales professionals. Through First Research, D&B has been able to enhance its Hoover’s solutions with deeper industry-specific content, providing sales professionals with higher quality data and more comprehensive insight.

AllBusiness.com is an online media and e-commerce company that leverages its proprietary publishing platform and a broad range of content to help users run their small businesses. AllBusiness.com operates one of the leading business information sites on the Internet. Its content helps professionals save time and money by addressing real-world business questions with practical solutions.

Our Internet Solutions help customers convert prospects to clients faster by helping them answer questions such as:

| • | How do I identify prospects and better prepare for sales calls? |

| • | Who are the key senior-level decision makers? |

| • | How does the prospect compare to others in their industry? |

Our principal Internet Solutions are:

| • | Our subscription solutions delivered online through Hoover’s Online (such as “Researcher,” “Prospector,” “Relationship Manager,” “Executive,” and our First Research industry data solution) and via electronic data feeds; |

| • | Our advertising and e-marketing solutions provided through www.hoovers.com, www.AllBusiness.com, www.firstresearch.com and related Internet sites; and |

| • | Licensing of Hoover’s proprietary content to third-party content providers. |

Our Sales Force

We rely primarily on our sales force of approximately 2,250 team members worldwide to sell our customers solutions, of which approximately 1,400 were in our North America segment and 850 were in our International segment as of December 31, 2009. Our sales force includes relationship managers and solution specialists who

8

Table of Contents

sell to our strategic and commercial customers, telesales teams, a team that sells to federal, state and local governments, and a team that sells to resellers of our solutions and our data. Our global sales force is also a source of competitive advantage, which allows us to go-to-market across three key customer segments. We identify these segments as strategic customers; commercial customers (or middle market in our International segment); and small businesses.

In 2009, we redesigned the “Go-To-Market” approach for our North America sales organization to increase performance and drive efficiencies. We reorganized the sales force, consolidated channels, reallocated accounts and simplified account teaming structures to get closer to our customers and to improve the efficiency of our sales force. We consolidated sales support functions, realigned around key industries in the strategic customer segment to increase cross-sell opportunities and account penetration, and will leverage telesales to drive new customer acquisition more efficiently. As a result of this reengineering initiative, we reduced the overall size of the North America sales force by approximately 10%.

Our Customers

We believe that different size customers have different needs and require different skill sets to service them. Accordingly, we have adopted a go-to-market sales strategy that focuses on distinct groups categorized internally as large customers, middle market customers and small business customers. Our principal customers within these groups are banks and other credit and financial institutions, manufacturers, wholesalers, retailers, government agencies, insurance companies and telecommunication companies, as well as sales, marketing and business development professionals. None of our customers accounted for more than 10% of our 2009 total revenue or of the revenue of our North American or International segments. Accordingly, neither we nor either of our segments is dependent on a single customer, such that a loss of any one would have a material adverse effect on our consolidated annual results of operations or the annual results of either of our segments.

Competition

We are subject to highly competitive conditions in all aspects of our business. However, we believe no competitor offers our complete line of solutions or can match our global data quality resulting from our DUNSRight Quality Process.

In North America, we are a market leader in our Risk Management Solutions business in terms of market share and revenue. We compete with our customers’ own internal business practices by continually developing more efficient alternatives to our customers’ risk management processes to capture more of their internal spend. We also directly compete with a broad range of companies, including consumer credit companies such as Equifax, Inc. and Experian Information Solutions, Inc. (“Experian”), which have traditionally offered primarily consumer information services, but now offer products that combine consumer information with business information as a tool to help customers make credit decisions with respect to small businesses.

We also compete in North America with a broad range of companies offering solutions similar to our Sales & Marketing Solutions. Our direct competitors in Sales & Marketing Solutions include companies such as Experian and infoGROUP (“infoUSA”).

In our Internet Solutions, Hoover’s competition varies based on the size of the customer and the level of spending available for services such as Hoover’s Online. On the high end of product pricing, Hoover’s Researcher, Hoover’s Prospector and Hoover’s Relationship Manager products compete with other business information providers such as infoUSA. New, less established entrants are also pursuing some of these same customers. On the lower end of product pricing, our Hoover’s Exec and Lite solutions mainly competes with advertising-supported Internet sites and other free or low-priced information sources, such as Yahoo! Finance and MarketWatch, Inc.

9

Table of Contents

Outside the U.S., the competitive environment varies by region and country. In Europe, our direct competition is primarily local, such as Experian in the United Kingdom (“UK”). In addition, we compete with certain companies such as Coface for cross border business. However, we believe we offer superior solutions when compared to these networks because of our DUNSRight Quality Process. In addition, the Sales & Marketing Solutions landscape is both localized and fragmented throughout Europe, where numerous local players of varying size compete for business.

In Asia, we face competition in our Risk Management Solutions business from a mix of local and global providers. For example, we compete with Sinotrust in China which is majority owned by Experian, with Teikoku Data Bank (“TDB”) in Japan and with Experian in India. In addition, as in Europe, the Sales & Marketing Solutions landscape throughout Asia is localized and fragmented.

We also face significant competition from the in-house operations of the businesses we seek as customers, other general and specialized credit reporting and business information services, and credit insurers. For example, in certain International markets, such as Europe, some credit insurers have identified the provision of credit information as an additional revenue stream. In addition, business information solutions and services are becoming more readily available, principally due to the expansion of the Internet, greater availability of public data and the emergence of new providers of business information solutions and services.

As discussed in “Our Aspiration and Our Strategy” above, we believe that our Trusted Brand, our DUNSRight Quality Process, our Winning Culture and our Financial Flexibility form a powerful competitive advantage.

Our ability to continue to compete effectively will be based on a number of factors, including our ability to:

| • | Communicate and demonstrate to our customers the value of our products and services based upon our proprietary DUNSRight Quality Process and, as a result, improve customer satisfaction; |

| • | Maintain and develop proprietary information and services such as analytics (e.g., scoring) and sources of data not publicly available; |

| • | Leverage our brand perception and the value of our D&B Worldwide Network; |

| • | Maintain those third-party relationships on whom we rely for data and certain operational services; and |

| • | Attract and retain a high-performing workforce. |

Intellectual Property

We own and control various intellectual property rights, such as trade secrets, confidential information, trademarks, service marks, trade names, copyrights, patents and applications therefor. These rights, in the aggregate, are of material importance to our business. We also believe that the D&B name and related trade names, marks and logos are of material importance to our business. We are licensed to use certain technology and other intellectual property rights owned and controlled by others, and other companies are licensed to use certain technology and other intellectual property rights owned and controlled by us. We consider our trademarks, service marks, databases, software, patents, patent applications and other intellectual property to be proprietary, and we rely on a combination of statutory (e.g., copyright, trademark, trade secret, patent, etc.) and contract and liability safeguards for protection thereof throughout the world.

Unless the context indicates otherwise, the names of our branded solutions and services referred to in this Annual Report on Form 10-K are trademarks, service marks or registered trademarks or service marks owned by or licensed to us or one or more of our subsidiaries.

We own patents and patent applications both in the U.S. and in other selected countries of importance to us. The patents and patent applications include claims which pertain to certain technologies which we have determined are proprietary and warrant patent protection. We believe that the protection of our innovative

10

Table of Contents

technology, especially technology pertaining to our proprietary DUNSRight Quality Process, through the filing of patent applications is a prudent business strategy, and we will continue to seek to protect those assets for which we have expended substantial capital. Filing of these patent applications may or may not provide us with a dominant position in the fields of technology. However, these patent applications may provide us with legal defenses should subsequent patents in these fields be issued to third parties and later asserted against us. Where appropriate, we may also consider asserting or cross-licensing our patents.

Employees

As of December 31, 2009, we employed approximately 5,000 team members worldwide, of which approximately 3,000 were in our North America segment and Corporate and approximately 2,000 were in our International segment. We believe that we have good relations with our employees. There are no unions in the North America segment. Works Councils and Trade Unions represent a portion of our employees in the European and Latin American operations of our International segment.

Available Information

We are required to file annual, quarterly and current reports, proxy statements and other information with the Securities and Exchange Commission (“SEC”). Investors may read and copy any document that we file, including this Annual Report on Form 10-K, at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Investors may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. In addition, the SEC maintains an Internet site at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, from which investors can electronically access our SEC filings.

We make available free of charge on or through our Internet site (www.dnb.com) our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after we electronically file such material with, or furnish the material to, the SEC. The information on our Internet site, on our Hoover’s Internet site or on our related Internet sites is not, and shall not be deemed to be, a part of this Annual Report on Form 10-K or incorporated into any other filings we make with the SEC.

Organizational Background of Our Company

As used in this report, except where the context indicates otherwise, the terms “D&B,” “Company,” “we,” “us,” or “our” refer to The Dun & Bradstreet Corporation and our subsidiaries.

We were incorporated in 2000 in the State of Delaware. For more information on our history, including the various spin-offs leading to our formation and our becoming a public company in September 2000, see Note 13 in Item 8. of this Annual Report on Form 10-K.

| Item 1A. | Risk Factors |

Our business model is dependent upon third parties to provide data and certain operational services, the loss of which would materially impact our business and financial results.

We rely significantly on third parties to support our business model. For example:

| • | We obtain much of the data that we use from third parties, including public record sources; |

| • | We utilize single source providers in certain countries that support the needs of our customers around the globe and rely on members of our D&B Worldwide Network to provide local data in countries in which we do not directly operate; |

11

Table of Contents

| • | We have also outsourced certain portions of our data acquisition, processing and delivery and customer service processes; and |

| • | We have outsourced various functions, such as our technology help desk and network management functions in the U.S. and the UK. |

If one or more data providers were to experience financial or operational difficulties or were to withdraw their data, cease making it available, be unable to make it available due to changing industry standards, substantially increase the cost of their data, not adhere to our data quality standards, or be acquired by a competitor who would cause this to occur, our ability to provide solutions and services to our customers could be materially adversely impacted, which could have a material adverse effect on our business and financial results. Similarly, if one of our outsource providers, including third parties with whom we have strategic relationships, were to experience financial or operational difficulties, their services to us would suffer or they may no longer be able to provide services to us at all, having a material adverse effect on our business and financial results. We cannot be certain that we could replace our large third-party vendors in a timely manner or on terms commercially reasonable to us. In addition, if we change a significant outsource provider, an existing provider makes significant changes to the way they conduct their operations, or we seek to bring in-house certain services performed today by third parties, we may experience unexpected disruptions in the provision of our solutions, which could have a material adverse effect on our business and financial results.

Our business performance is dependent upon successful implementation and the ongoing operation of our recently announced two-year Strategic Technology Initiative, the failure of which could materially impact our business and financial results.

In February 2010, we announced an approximately two-year strategic technology initiative to be implemented at an aggregate cost of approximately $110 million to $130 million. We will rely in part on third-party providers to implement a new data supply chain and update our technology infrastructure and to thereafter run such operations both within D&B and from their own remote locations. We have started the detailed planning of this initiative and upon completion we expect that it will:

| • | Simplify and re-architect our data supply chain in order to, among other things, supply intra-day updates; |

| • | Create a services layer to optimize access to our data for customers and third parties; |

| • | Consolidate our legacy products to provide fewer more impactful applications for customers; |

| • | Accelerate revenue growth in our North America segment upon the completion of the initiative; and |

| • | Significantly reduce our technology costs upon completion of the initiative. |

In the event we fail to successfully develop the plan, and execute on the initiative, including hiring and retaining appropriate technology personnel, engage and manage third parties, re-architect our data supply chain, and simplify our product portfolio while migrating our customers to new products, and maintain such data and technology operations on an ongoing basis, we will not achieve our expected revenue acceleration or growth, or the anticipated cost savings from this initiative, and we could experience a significant competitive disadvantage in the marketplace, which could have a material adverse effect on our business and financial results.

We face competition that may cause price reductions or loss of market share.

We are subject to competitive conditions in all aspects of our business. We compete directly with a broad range of companies offering business information services to customers. We also face competition from:

| • | The in-house operations of the businesses we seek as customers; |

| • | Other general and specialized credit reporting and other business information services; and |

| • | Credit insurers. |

12

Table of Contents

In addition, business information solutions and services are becoming more readily available, principally due to the expansion of the Internet, greater availability of public data and the emergence of new providers of business information solutions and services. Large Internet search engine companies can provide low-cost alternatives to data gathering and change how our customers perform key activities such as marketing campaigns. Such companies, and other third parties which may not be readily apparent today, may become significant low-cost competitors and adversely impact the demand for our solutions and services.

Weak economic conditions also can result in customers seeking to utilize free or lower-cost information that is available from alternative sources such as the Internet and European Commission-sponsored projects like the European Business Register. Intense competition could harm us by causing, among other things, price reductions, reduced gross margins and loss of market share.

We are facing competition outside the U.S., and our competitors could develop an alternative to our D&B Worldwide Network.

We are also facing competition from consumer credit companies that offer consumer information solutions to help their customers make credit decisions regarding small businesses. In addition, consumer information companies are seeking to expand their operations more broadly into aspects of the business information space. While their presence is currently small in the business information market, given the size of the consumer market in which they play, they have scale advantages in terms of scope of operations and size of relationship with customers, which they can potentially leverage to an advantage.

Our ability to continue to compete effectively will be based upon a number of factors, including our ability to:

| • | Communicate and demonstrate to our customers the value of our products and services based upon our proprietary DUNSRight Quality Process and, as a result, improve customer satisfaction; |

| • | Maintain and develop proprietary information and services such as analytics (e.g., scoring), and sources of data not publicly available, such as detailed trade data; |

| • | Demonstrate value through our decision-making tools and integration capabilities; |

| • | Leverage our brand perception and the value of our D&B Worldwide Network; |

| • | Continue to implement the Financial Flexibility component of our strategy and effectively reallocate our spending; |

| • | Obtain and deliver reliable and high-quality business information through various media and distribution channels in formats tailored to customer requirements; |

| • | Adopt and maintain an effective information technology infrastructure to support product delivery as customer needs and preferences change and competitors offer more sophisticated products; |

| • | Attract and retain a high-performance workforce; |

| • | Enhance our existing services and introduce new services; and |

| • | Improve our International business model and data quality through the successful management in our International segment of the members of our D&B Worldwide Network. |

Our business performance might not be sufficient for us to meet the full-year financial guidance that we provide publicly.

We provide full-year financial guidance to the public which is based upon our assumptions regarding our expected financial performance. This includes, for example, assumptions regarding our ability to grow revenue, to grow operating income, to achieve desired tax rates and to generate cash. We believe that our financial

13

Table of Contents

guidance provides investors and analysts with a better understanding of our view of our near-term financial performance. Such financial guidance may not always be accurate, due to our inability to meet the assumptions we make and the impact on our financial performance that could occur as a result of the various risks and uncertainties to our business as set forth in these risk factors and in our public filings with the SEC or otherwise. If we fail to meet the full-year financial guidance that we provide or if we find it necessary to revise such guidance as we conduct our operations throughout the year, the market value of our common stock could be materially adversely affected.

We may lose key business assets or suffer interruptions in product delivery, including loss of data center capacity or the interruption of telecommunications links, the Internet, or power sources which could significantly impede our ability to do business.

Our operations depend on our ability, as well as that of third-party service providers to whom we have outsourced several critical functions, to protect data centers and related technology against damage from hardware failure, fire, power loss, telecommunications failure, impacts of terrorism, breaches in security (such as the actions of computer hackers), natural disasters, or other disasters. The online services we provide are dependent on links to telecommunications providers. In addition, we generate a significant amount of our revenue through telesales centers and Internet sites that we use in the acquisition of new customers, fulfillment of solutions and services and responding to customer inquiries. We may not have sufficient redundant operations or change management processes in connection with our introduction of new online products or services to prevent a loss or failure in all of these areas in a timely manner. Any damage to our data centers, failure of our telecommunications links or inability to access these telesales centers or Internet sites could cause interruptions in operations that adversely affect our ability to meet customers’ requirements and materially adversely affect our business and financial results.

A failure in the integrity of our database could harm our brand and result in a loss of sales and an increase in legal claims.

The reliability of our solutions is dependent upon the integrity of the data in our global database. We have in the past been subject to customer and third-party complaints and lawsuits regarding our data, which have occasionally been resolved by the payment of money damages. A failure in the integrity of our database, whether inadvertently or through the actions of a third party, which may be on the rise, could harm us by exposing us to customer or third-party claims or by causing a loss of customer confidence in our solutions. In addition, we must continue to invest in our database to improve and maintain the quality, timeliness and coverage of the data contained therein if we are to maintain our competitive positioning in the marketplace.

Also, we have licensed, and we may license in the future, proprietary rights to third parties. While we attempt to ensure that the quality of our brand is maintained by the third parties to whom we grant non-exclusive licenses and by customers, they may take actions that could materially adversely affect the value of our proprietary rights or our reputation. In addition, it cannot be assured that these licensees and customers will take the same steps we have taken to prevent misappropriation of our data solutions or technologies.

Our brand and reputation are key assets and competitive advantages of our Company and our business may be affected by how we are perceived in the marketplace.

Our brand and its attributes are key assets of the Company. Our ability to attract and retain customers is highly dependent upon the external perceptions of our level of data quality, business practices and overall financial condition. Negative perceptions or publicity regarding these matters could damage our reputation with customers and the public, which could make it difficult for us to attract and maintain customers. Adverse developments with respect to our industry may also, by association, negatively impact our reputation, or result in higher regulatory or legislative scrutiny. Although we monitor developments for areas of potential risk to our reputation and brand, negative perceptions or publicity could have a material adverse effect on our business and financial results.

14

Table of Contents

We rely on annual contract renewals for a substantial part of our revenue, and our quarterly results may be significantly impacted by the timing of these renewals or a shift in product mix that results in a change in the timing of revenue recognition.

We derive a substantial portion of our revenue from annual customer contracts. If we are unable to renew a significant number of these contracts, our revenue and results of operations would be harmed. In addition, our results of operations from period-to-period may vary due to the timing of customer contract renewals. As contracts are renewed, we have, and may continue to experience, a shift in product mix underlying such contracts. This could result in the deferral of increased amounts of revenue into future periods as a larger portion of revenue is recognized over the term of our contracts rather than upfront at contract signing. Although this may cause our financial results from period-to-period to vary substantially, such change in revenue recognition will not change the total revenue recognized over the life of our contracts.

We may be adversely affected by the current economic environment.

As a result of the macro-economic challenges currently affecting the economy of the United States and other parts of the world, our customers or vendors may experience problems with their earnings, cash flow, or both. This may cause our customers to delay, cancel or significantly decrease their purchases from us, and we may experience delays in payment or their inability to pay amounts owed to us. In addition, our vendors may substantially increase their prices without notice. Any such change in the behavior of our customers or vendors may materially adversely affect our earnings and cash flow. If economic conditions in the United States and other key markets deteriorate further or do not show improvement, we may experience material adverse impacts to our business, operating results, and/or access to credit markets.

Changes in the legislative, regulatory and commercial environments in which we operate may adversely impact our ability to collect, manage, aggregate and use data and may impact our financial results.

Certain types of information we gather, compile and publish are subject to regulation by governmental authorities in certain markets in which we operate, particularly in our international markets. In addition, there is increasing awareness and concern among the general public and companies regarding marketing and privacy matters, particularly as they relate to individual privacy interests and the ubiquity of the Internet. These concerns may result in new laws and regulations. In general, compliance with existing laws and regulations has not to date materially impacted our business and financial results. Nonetheless, future laws and regulations with respect to the collection, management and use of information, and adverse publicity or litigation concerning the commercial use of such information could result in limitations being imposed on our operations, increased compliance or litigation expense and/or loss of revenue, which could have a material adverse effect on our business and financial results.

In addition, governmental agencies may seek, from time-to-time, to increase the fees or taxes that we must pay to acquire, use and/or redistribute data that such governmental agencies collect. While we would seek to pass along any such price increases to our customers or provide alternative services, there is no guarantee that we would be able to do so, given competitive pressures or other considerations. In addition, any such price increases or alternative services may result in reduced usage by our customers and/or loss of market share.

We may be unable to adapt successfully to changes in our customers’ preferences for our solutions, which could materially adversely affect our revenues.

Our success depends in part on our ability to adapt our solutions to our customers’ preferences. Advances in information technology and uncertain or changing economic conditions are changing the way our customers use and purchase business information. As a result, our customers are demanding both lower prices and more features from our solutions, such as decision-making tools like credit scores and electronic delivery formats. If we do not successfully adapt our solutions to our customers’ preferences, our business and financial results

15

Table of Contents

would be materially adversely affected. Specifically, for our larger customers, our continued success will be dependent on our ability to satisfy more of their needs by providing solutions beyond data, such as enhanced analytics and assisting with their data integration efforts. For our smaller customers, our success will depend in part on our ability to develop a strong value proposition, including simplifying our solutions and pricing offerings, to enhance our marketing efforts to these customers and to improve our service to them.

To address customer needs for pricing certainty and increased access to our solutions, we provide subscription pricing plans through our Preferred Pricing Agreement and our Preferred Pricing Agreement with DNBi. These subscription pricing plans provide expanded access to our Risk Management Solutions in a way that provides more certainty over related costs to the customer, which, in turn, generally results in customers increasing their spend on our solutions. These plans have been an important driver of our growth from inception in 2005 to date. Our success moving forward is dependent, in part, on the continued penetration of these offerings and the successful rollout of similar programs in various markets around the world. Similarly, our continued success is dependent on customers’ acceptance of our DNBi offering.

Acquisitions, joint ventures or similar strategic relationships may disrupt or otherwise have a material adverse effect on our business and financial results.

As part of our strategy, we may seek to acquire other complementary businesses, products and technologies or enter into joint ventures or similar strategic relationships. These transactions are subject to the following risks:

| • | Acquisitions, joint ventures or similar relationships may cause a disruption in our ongoing business, distract our management and make it difficult to maintain our standards, controls and procedures; |

| • | We may not be able to integrate successfully the services, content, products and personnel of any such transaction into our operations; |

| • | We may not derive the revenue improvements, cost savings and other intended benefits of any such transaction; and |

| • | Risks, exposures and liabilities of acquired entities or other third parties with whom we undertake a transaction, that arise from such third parties’ activities prior to undertaking a transaction with us. |

We have no direct management control over third-party members of the D&B Worldwide Network who conduct business under the D&B brand name in local markets.

The D&B Worldwide Network is comprised of wholly-owned subsidiaries, joint ventures that we either control or hold a minority interest in, and third-party members who conduct business under the D&B brand name in local markets. While third-party member participation in the D&B Worldwide Network is controlled by commercial services agreements and the use of our trademarks is controlled by license agreements, we have no direct management control over these members beyond the terms of the agreements. As a result, actions or inactions taken by these third-party members may have a material impact on our business and financial results. For example, one or more third-party members may:

| • | Provide a product or service that does not adhere to our data quality standards; |

| • | Fail to comply with D&B brand and communication standards; |

| • | Engage in illegal or unethical business practices; |

| • | Elect not to support new or revised products and services or other strategic initiatives; or |

| • | Fail to execute other data or distribution contract requirements. |

Such actions or inactions may have an impact on customer confidence in the D&B brand globally, which could materially adversely impact our business and financial results.

16

Table of Contents

We may not be able to attract and retain qualified personnel, including members of our sales force and technology team, which could impact the quality of our performance and customer satisfaction.

Our success and financial results also depend on our continuing ability to attract, retain and motivate highly qualified personnel at all levels. This includes members of our sales force on whom we rely for the vast majority of our revenue, and members of our technology team on whom we rely to continually maintain and upgrade all of our technology operations and maintain and develop our products, and to appropriately use the time and resources of such individuals. Competition for these individuals is intense, and we may not be able to retain our key personnel or key members of our sales or technology teams, or attract, assimilate or retain other highly qualified individuals in the future. We have from time-to-time experienced, and we expect to continue to experience, difficulty in hiring and retaining employees, including members of our sales force and technology team, with appropriate qualifications.

Our operations in the International segment are subject to various risks associated with operations in foreign countries, which could materially adversely affect our business and financial results.

Our success depends in part on our various operations outside North America. For the three years ended December 31, 2009, 2008 and 2007, our International segment accounted for 22%, 21% and 19% of total revenue, respectively. Our International business is subject to many challenges, the most significant being:

| • | Our competition is primarily local, and our customers may have greater loyalty to our local competitors who may have a competitive advantage with us because they are not restricted by U.S. laws with which we require our International segment to comply, such as the Foreign Corrupt Practices Act; |

| • | Credit insurance is a significant credit risk mitigation tool in certain markets, thus reducing the demand for our Risk Management Solutions; and |

| • | In some markets, key data elements are generally available from public-sector sources, thus reducing a customer’s need to purchase our data. |

Our International strategy includes the leveraging of our D&B Worldwide Network to improve our data quality. We form and manage these strategic alliances to create a competitive advantage for us over the long term; however, these strategic relationships may not be successful or may be subject to ownership change.

The issue of data privacy is an increasingly important area of public policy in various International markets, and we operate in an evolving regulatory environment that could adversely impact aspects of our business or the business of third parties on whom we depend.

Our operating results could also be negatively affected by a variety of other factors affecting our foreign operations, many of which are beyond our control. These factors may include currency fluctuations, economic, political or regulatory conditions, competition from government agencies in a specific country or region, trade protection measures and other regulatory requirements. Additional risks inherent in International business activities generally include, among others:

| • | Longer accounts receivable payment cycles; |

| • | The costs and difficulties of managing International operations and strategic alliances, including the D&B Worldwide Network; and |

| • | The need to comply with a broader array of regulatory and licensing requirements, the failure of which could result in fines, penalties or business suspensions. |

17

Table of Contents

We may be unable to reduce our expense base through our Financial Flexibility, and the related reinvestments from savings from this program may not produce the level of desired revenue growth which would materially adversely affect our business and financial results.

Successful execution of our strategy includes reducing our expense base through our Financial Flexibility initiatives, and reallocating our expense base reductions into initiatives to produce our desired revenue growth. The success of this program may be affected by:

| • | Our ability to continually adapt and improve our organizational design and efficiency to meet the changing needs of our business and our customers; |

| • | Our ability to implement all of the actions required under this program within the established time frame; |

| • | Our ability to implement actions that require process or technology changes to reduce our expense base; |

| • | Entering into or amending agreements with third-party vendors to renegotiate terms beneficial to us; |

| • | Managing third-party vendor relationships effectively; |

| • | Completing agreements with our local works councils and trade unions related to potential reengineering actions in certain International markets; and |

| • | Maintaining quality around key business processes utilizing our reduced and/or outsourced resources. |

If we fail to reduce our expense base, or if we do not achieve our desired level of revenue growth from new initiatives, our business and financial results would be materially adversely affected.

We are involved in tax and legal proceedings that could have a material adverse impact on us.

We are involved in tax and legal proceedings, claims and litigations that arise in the ordinary course of business. As discussed in greater detail under “Note 13. Contingencies” in “Notes to Consolidated Financial Statements” in Part II, Item 8. of this Annual Report on Form 10-K, certain of these matters could materially adversely affect our business and financial results.

| Item 1B. | Unresolved Staff Comments |

Not applicable.

| Item 2. | Properties |

Our corporate office is located at 103 JFK Parkway, Short Hills, New Jersey 07078, in a 123,000-square-foot property that we lease. This property also serves as the executive offices of our North America segment.

Our other properties are geographically distributed to meet sales and operating requirements worldwide. We generally consider these properties to be both suitable and adequate to meet current operating requirements. As of December 31, 2009, the most important of these other properties include the following sites:

| • | A 178,000 square-foot leased office building in Center Valley, Pennsylvania, which houses various sales, finance, fulfillment and data acquisition personnel; |

| • | A 147,000 square-foot office building that we own in Parsippany, New Jersey, housing personnel from our North American sales, marketing and technology groups (approximately one-third of this building is leased to a third party); |

| • | A 78,000 square-foot leased office building in Austin, Texas, which houses a majority of our Hoover’s employees; and |

| • | A 79,060 square-foot leased space in Marlow, England, which houses our United Kingdom business, International technology and certain other International teams. |

18

Table of Contents

In addition to the above locations, we also conduct operations in other offices across the globe, most of which are leased.

| Item 3. | Legal Proceedings |

Information in response to this Item is included in Part II, Item 8. “Note 13. Contingencies” and is incorporated by reference into Part I of this Annual Report on Form 10-K.

| Item 4. | Submission of Matters to a Vote of Security Holders |

No matters were submitted to a vote of security holders in the fourth quarter of fiscal year 2009.

19

Table of Contents

PART II

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Our common stock is listed on the New York Stock Exchange and trades under the symbol DNB. We had 2,919 shareholders of record as of December 31, 2009.

The following table summarizes the high and low sales prices for our common stock, as reported in the periods shown:

| 2009 | 2008 | |||||||||||

| High | Low | High | Low | |||||||||

| First Quarter |

$ | 81.40 | $ | 69.80 | $ | 93.94 | $ | 81.02 | ||||

| Second Quarter |

$ | 84.18 | $ | 76.67 | $ | 94.10 | $ | 80.44 | ||||

| Third Quarter |

$ | 83.16 | $ | 71.33 | $ | 98.78 | $ | 85.50 | ||||

| Fourth Quarter |

$ | 84.64 | $ | 73.26 | $ | 93.57 | $ | 64.40 | ||||

We paid quarterly dividends to our shareholders totaling $71.5 million, $65.6 million and $58.4 million during the years ended December 31, 2009, 2008 and 2007, respectively. On February 4, 2010, our Board of Directors approved the declaration of a $0.35 per share dividend for the first quarter of 2010. This cash dividend is payable March 18, 2010, to shareholders of record at the close of business on March 3, 2010.

Issuer Purchases of Equity Securities

The following table provides information about purchases made by us or on our behalf during the quarter ended December 31, 2009 of shares of equity that are registered pursuant to Section 12 of the Exchange Act:

| Period |

Total Number of Shares Purchased (a)(b) |

Average Price Paid Per Share |

Total Number of Shares Purchased as part of Publicly Announced Plans or Programs(a)(b) |

Maximum Number of Currently Authorized Shares that May Yet Be Purchased Under the Plans or Programs(a) |

Approximate Dollar Value of Currently Authorized Shares that May Yet Be Purchased Under the Plans or Programs(b) | |||||||

| (Amounts in millions, except per share data) | ||||||||||||

| October 1 - 31, 2009 |

— | $ | — | — | — | $ | — | |||||

| November 1 - 30, 2009 |

0.2 | $ | 79.30 | 0.2 | — | $ | — | |||||

| December 1 - 31, 2009 |

0.8 | $ | 81.59 | 0.8 | — | $ | — | |||||

| 1.0 | $ | 81.16 | 1.0 | 0.8 | $ | 177.3 | ||||||

| (a) | During the three months ended December 31, 2009, we repurchased 0.5 million shares of common stock for $34.7 million under our Board of Directors approved repurchase program to mitigate the dilutive effect of the shares issued under our stock incentive plans and Employee Stock Purchase Plan. This program was announced in August 2006 and expires in August 2010. The maximum amount authorized under the program is 5.0 million shares, of which 4.2 million shares have been repurchased as of December 31, 2009. We anticipate that this program will be completed prior to maturity in August 2010. |

| (b) | During the three months ended December 31, 2009, we repurchased 0.3 million shares of common stock for $24.8 million related to a previously announced $400 million, two-year share repurchase program approved by our Board of Directors in December 2007. This program was completed in December 2009. |

In addition, during the three months ended December 31, 2009, we repurchased 0.2 million shares of common stock for $22.7 million related to a previously announced $200 million share repurchase program approved by our Board of Directors in February 2009. We anticipate that this program will be completed by December 2011.

20

Table of Contents

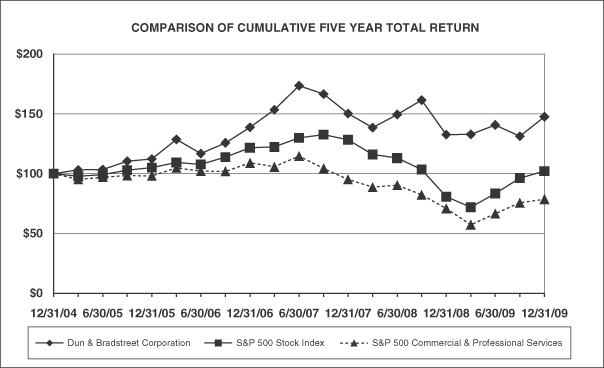

FINANCIAL PERFORMANCE COMPARISON GRAPH*

SINCE DECEMBER 31, 2004

In accordance with SEC rules, the graph below compares the Company’s cumulative total shareholder return against the cumulative total return of the Standard & Poor’s 500 Stock Index and a published industry index starting on December 31, 2004. Our past performance may not be indicative of future performance.

As an industry index, the Company chose the S&P 500 Commercial & Professional Services Index, a subset of the S&P 500 Stock Index that includes companies that provide business-to-business services.

COMPARISON OF FIVE YEAR CUMULATIVE TOTAL RETURN

AMONG D&B, S&P 500 STOCK INDEX AND THE S&P 500 COMMERCIAL &

PROFESSIONAL SERVICES INDEX

| * | Assumes $100 invested on December 31, 2004, and reinvestment of dividends. |

21

Table of Contents

| Item 6. | Selected Financial Data |

| For the Years Ended December 31, | ||||||||||||||||||||

| 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

| (Amounts in millions, except per share data) | ||||||||||||||||||||

| Results of Operations: |

||||||||||||||||||||

| Operating Revenues |

$ | 1,687.0 | $ | 1,726.3 | $ | 1,599.2 | $ | 1,474.9 | $ | 1,380.0 | ||||||||||

| Costs and Expenses |

1,222.5 | 1,256.6 | 1,173.6 | 1,081.2 | 1,015.4 | |||||||||||||||

| Operating Income(1) |

464.5 | 469.7 | 425.6 | 393.7 | 364.6 | |||||||||||||||

| Non-Operating Income (Expense)—Net(2) |

(32.0 | ) | (30.8 | ) | 0.7 | (13.3 | ) | (9.7 | ) | |||||||||||

| Income from Continuing Operations Before Provision for Income Taxes and Equity in Net Income of Affiliates |

432.5 | 438.9 | 426.3 | 380.4 | 354.9 | |||||||||||||||

| Provision for Income Taxes(3) |

112.1 | 128.0 | 135.8 | 142.1 | 133.1 | |||||||||||||||

| Equity in Net Income (Loss) of Affiliates |

1.6 | 1.0 | 1.3 | 0.4 | 0.7 | |||||||||||||||

| Income from Continuing Operations |

322.0 | 311.9 | 291.8 | 238.7 | 222.5 | |||||||||||||||

| Income from Discontinued Operations, Net of Income Taxes |

— | 0.7 | 5.4 | 2.0 | (1.3 | ) | ||||||||||||||

| Gain on Disposal of Italian Real Estate Business, Net of Tax Impact |

— | 0.4 | — | — | — | |||||||||||||||

| Income from Discontinued Operations, Net of Income Taxes(4) |

— | 1.1 | 5.4 | 2.0 | (1.3 | ) | ||||||||||||||

| Net Income |

322.0 | 313.0 | 297.2 | 240.7 | 221.2 | |||||||||||||||

| Less: Net (Income) Loss Attributable to the Noncontrolling Interest |

(2.6 | ) | (2.4 | ) | 0.9 | — | — | |||||||||||||

| Net Income Attributable to D&B |

$ | 319.4 | $ | 310.6 | $ | 298.1 | $ | 240.7 | $ | 221.2 | ||||||||||

| Basic Earnings Per Share of Common Stock: |

||||||||||||||||||||

| Income from Continuing Operations Attributable to D&B Common Shareholders |

$ | 6.06 | $ | 5.65 | $ | 4.99 | $ | 3.75 | $ | 3.31 | ||||||||||

| Income from Discontinued Operations Attributable to D&B Common Shareholders |

— | 0.02 | 0.09 | 0.04 | (0.02 | ) | ||||||||||||||

| Net Income Attributable to D&B Common Shareholders |

$ | 6.06 | $ | 5.67 | $ | 5.08 | $ | 3.79 | $ | 3.29 | ||||||||||

| Diluted Earnings Per Share of Common Stock: |

||||||||||||||||||||

| Income from Continuing Operations Attributable to D&B Common Shareholders |

$ | 5.99 | $ | 5.56 | $ | 4.88 | $ | 3.66 | $ | 3.19 | ||||||||||

| Income from Discontinued Operations Attributable to D&B Common Shareholders |

— | 0.02 | 0.09 | 0.03 | (0.02 | ) | ||||||||||||||

| Net Income Attributable to D&B Common Shareholders |

$ | 5.99 | $ | 5.58 | $ | 4.97 | $ | 3.69 | $ | 3.17 | ||||||||||

| Other Data: |

||||||||||||||||||||

| Weighted Average Number of Shares Outstanding—Basic |

52.3 | 54.4 | 58.3 | 63.2 | 66.8 | |||||||||||||||

| Weighted Average Number of Shares Outstanding—Diluted |

52.9 | 55.3 | 59.6 | 64.8 | 69.4 | |||||||||||||||

| Amounts Attributable to D&B Common Shareholders |

||||||||||||||||||||

| Income from Continuing Operations, Net of Income Taxes |

$ | 319.4 | $ | 309.5 | $ | 292.7 | $ | 238.7 | $ | 222.5 | ||||||||||

| Income from Discontinued Operations, Net of Income Taxes |

— | 1.1 | 5.4 | 2.0 | (1.3 | ) | ||||||||||||||

| Net Income Attributable to D&B |

$ | 319.4 | $ | 310.6 | $ | 298.1 | $ | 240.7 | $ | 221.2 | ||||||||||

| Cash Dividends Paid per Common Share |

$ | 1.36 | $ | 1.20 | $ | 1.00 | $ | — | $ | — | ||||||||||

| Cash Dividends Declared per Common Share |

$ | 1.36 | $ | 0.90 | $ | 1.30 | $ | — | $ | — | ||||||||||

| Balance Sheet: |

||||||||||||||||||||

| Total Assets |

$ | 1,749.4 | $ | 1,586.0 | $ | 1,658.8 | $ | 1,360.1 | $ | 1,613.4 | ||||||||||

| Long-Term Debt |

$ | 961.8 | $ | 904.3 | $ | 724.8 | $ | 458.9 | $ | 0.1 | ||||||||||

| Total D&B Shareholders’ Equity (Deficit) |

$ | (745.7 | ) | $ | (856.7 | ) | $ | (440.1 | ) | $ | (399.1 | ) | $ | 77.6 | ||||||

| Noncontrolling Interest |

$ | 11.7 | $ | 6.1 | $ | 3.6 | $ | — | $ | — | ||||||||||

| Total Equity (Deficit) |

$ | (734.0 | ) | $ | (850.6 | ) | $ | (436.5 | ) | $ | (399.1 | ) | $ | 77.6 | ||||||

22

Table of Contents

| (1) | Non-core gain and (charges)(a) included in Operating Income: |

| For the Years Ended December 31, | ||||||||||||||||||||

| 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

| Restructuring Charges |

$ | (23.1 | ) | $ | (31.4 | ) | $ | (25.1 | ) | $ | (25.5 | ) | $ | (30.7 | ) | |||||

| Impaired Intangible Assets |

$ | (3.0 | ) | $ | — | $ | — | $ | — | $ | — | |||||||||

| Settlement of International Payroll Tax Matter Related to a Divested Entity |

$ | — | $ | — | $ | (0.8 | ) | $ | — | $ | — | |||||||||

| Charge Related to a Dispute on the Sale of the Company’s French Business |

$ | — | $ | — | $ | — | $ | — | $ | (0.4 | ) | |||||||||

| (a) | See Item 7. included in this Annual Report on Form 10-K for definition of non-core gains and (charges). |

| (2) | Non-core gains and (charges)(a) included in Non-Operating Income (Expense)—Net: |

| For the Years Ended December 31, | |||||||||||||||||

| 2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||||

| Effect of Legacy Tax Matters |

$ | 1.0 | $ | 1.2 | $ | 1.6 | $ | — | $ | — | |||||||

| Gain Associated with Huaxia/D&B China Joint Venture |

$ | — | $ | — | $ | 5.8 | $ | — | $ | — | |||||||

| Gain Associated with Beijing D&B HuiCong Market Research Co., Ltd Joint Venture |

$ | — | $ | 0.6 | $ | — | $ | — | $ | — | |||||||

| Gain Associated with Tokyo Shoko Research/D&B Japan Joint Venture |

$ | — | $ | — | $ | 13.2 | $ | — | $ | — | |||||||

| Net Gain (Loss) on the Sale of Other Investments |

$ | — | $ | — | $ | 0.9 | $ | — | $ | — | |||||||

| Tax Reserve true-up for the Settlement of 2003 tax year, related to the “Amortization and Royalty Expense Deductions” transaction |

$ | — | $ | (7.7 | ) | $ | — | $ | — | $ | — | ||||||

| Settlement of Legacy Tax Matter Arbitration |

$ | 4.1 | $ | 8.1 | $ | — | $ | — | $ | — | |||||||

| Gain on Disposal of Italian Domestic Business |

$ | 6.5 | $ | — | $ | — | $ | — | $ | — | |||||||

| Gain on Sale of a 5% Investment in a South African Company |

$ | — | $ | — | $ | — | $ | — | $ | 3.5 | |||||||

| Lower Costs Related to the Sale of Iberia (Spain and Portugal) Business |

$ | — | $ | — | $ | — | $ | — | $ | 0.8 | |||||||

| Charge Related to a Dispute on the Sale of the Company’s French Business |

$ | — | $ | — | $ | — | $ | — | $ | (3.7 | ) | ||||||

| (a) | See Item 7. included in this Annual Report on Form 10-K for definition of non-core gains and (charges). |

23

Table of Contents

| (3) | Non-core gains and (charges)(a) included in Provision for Income Taxes: |

| For the Years Ended December 31, | ||||||||||||||||||||

| 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

| Restructuring Charges |

$ | 8.4 | $ | 11.2 | $ | 9.4 | $ | 8.6 | $ | 8.1 | ||||||||||

| Impaired Intangible Assets |

$ | 1.2 | $ | — | $ | — | $ | — | $ | — | ||||||||||

| Gain Associated with Beijing D&B HuiCong Market Research Co., Ltd Joint Venture |

$ | — | $ | (0.1 | ) | $ | — | $ | — | $ | — | |||||||||

| Effect of Legacy Tax Matters |

$ | (1.0 | ) | $ | (1.2 | ) | $ | (1.6 | ) | $ | — | $ | — | |||||||

| Gain Associated with Huaxia/D&B China Joint Venture |

$ | — | $ | — | $ | (2.9 | ) | $ | — | $ | — | |||||||||

| Gain Associated with Tokyo Shoko Research/D&B Japan Joint Venture |

$ | — | $ | — | $ | (8.3 | ) | $ | — | $ | — | |||||||||

| Settlement of International Payroll Tax Matter Related to a Divested Entity |

$ | — | $ | — | $ | 0.2 | $ | — | $ | — | ||||||||||

| Settlement of Legacy Tax Matter Arbitration |

$ | (3.1 | ) | $ | (3.1 | ) | $ | — | $ | — | $ | — | ||||||||

| Benefits Derived From Worldwide Legal Entity Simplification |

$ | 36.2 | $ | — | $ | — | $ | — | $ | — | ||||||||||

| Gain on Disposal of Italian Domestic Business |

$ | 3.5 | $ | — | $ | — | $ | — | $ | — | ||||||||||

| Net Gain (Loss) on the Sale of Other Investments |

$ | — | $ | — | $ | (0.3 | ) | $ | — | $ | — | |||||||||

| Tax Reserve true-up for the Settlement of 1997-2002 tax years, primarily related to the “Amortization and Royalty Expense Deductions/Royalty Income 1997-2007” transaction |