Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| x | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2009

OR

| ¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission file number 1-13782

WESTINGHOUSE AIR BRAKE TECHNOLOGIES CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 25-1615902 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

| 1001 Air Brake Avenue Wilmerding, Pennsylvania 15148 |

(412) 825-1000 | |

| (Address of principal executive offices, including zip code) | (Registrant’s telephone number) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of Class |

Name of Exchange on which registered | |

| Common Stock, par value $.01 per share | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files) Yes ¨ No ¨.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act. Yes ¨ No x.

The registrant estimates that as of June 30, 2009, the aggregate market value of the voting shares held by non-affiliates of the registrant was approximately $1.4 billion based on the closing price on the New York Stock Exchange for such stock.

As of February 22, 2010, 47,619,699 shares of Common Stock of the registrant were issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the Proxy Statement for the registrant’s Annual Meeting of Stockholders to be held on May 12, 2010 are incorporated by reference into Part III of this Form 10-K.

Table of Contents

2

Table of Contents

PART I

| Item 1. | BUSINESS |

General

Westinghouse Air Brake Technologies Corporation, doing business as Wabtec Corporation, is a Delaware corporation with headquarters at 1001 Air Brake Avenue in Wilmerding, Pennsylvania. Our telephone number is 412-825-1000, and our website is located at www.wabtec.com. All references to “we”, “our”, “us”, the “Company” and “Wabtec” refer to Westinghouse Air Brake Technologies Corporation and its subsidiaries. Westinghouse Air Brake Company (“WABCO”) was formed in 1990 when it acquired certain assets and operations from American Standard, Inc., now known as Trane (“Trane”). In 1999, WABCO merged with MotivePower Industries, Inc. (“MotivePower”) and adopted the name Wabtec.

Today, Wabtec is one of the world’s largest providers of value-added, technology-based equipment and services for the global rail industry. We believe we hold approximately a 50% market share in North America for our primary braking-related equipment and a leading position in North America for most of our other product lines. Our highly engineered products, which are intended to enhance safety, improve productivity and reduce maintenance costs for customers, can be found on virtually all U.S. locomotives, freight cars, subway cars and buses. In 2009, the Company had sales of about $1.4 billion and net income of about $115.1 million. In 2009 sales of aftermarket parts and services represented about 54% of total sales, while sales to customers outside of the U.S. accounted for about 40% of total sales.

Industry Overview

The Company primarily serves the worldwide freight rail and passenger transit industries. As such, our operating results are largely dependent on the level of activity, financial condition and capital spending plans of the global railroad and transit industries. Many factors influence these industries, including general economic conditions; rail traffic, as measured by freight tonnage and passenger ridership; government spending on public transportation; and investment in new technologies by freight rail and passenger transit systems.

According to a 2008 study by UNIFE, the Association of the European Rail Industry, the global market for railway products and services is more than $100.0 billion. The three largest markets, which represent about 85% of the total market, are Europe, North America and Asia-Pacific. Over the next decade, Asia-Pacific is expected to be the fastest-growing region and to surpass the North American market.

In North America, railroads carry about 43% of intercity freight, as measured by ton-miles, which is more than any other mode of transportation. They are an integral part of the continent’s economy and transportation system, serving nearly every industrial, wholesale and retail sector. Through direct ownership and operating partnerships, U.S. railroads are part of an integrated network that includes railroads in Canada and Mexico, forming what is regarded as the world’s most-efficient and lowest-cost freight rail service. There are more than 500 railroads operating in North America, with the largest railroads, referred to as “Class I,” accounting for more than 90% of the industry’s revenues. Although the railroads carry a wide variety of commodities and goods, coal is the single-largest item, representing about 40% of carloadings in 2009. Intermodal traffic—the movement of trailers or containers by rail in combination with another mode of transportation—has been the railroads’ fastest-growing market segment in the past 10 years. Railroads operate in a competitive environment, especially with the trucking industry, and are always seeking ways to improve safety, cost and reliability. New technologies offered by Wabtec and others in the industry can provide some of these benefits.

Demand for our freight related products and services in North America are driven by a number of factors, including:

| • | Rail traffic. The Association of American Railroads (AAR) compiles statistics that gauge the level of activity in the freight rail industry. Two important statistics are revenue ton-miles and |

3

Table of Contents

| carloadings, which are generally referred to as “rail traffic”. In 2009, revenue ton-miles decreased 15.1% and carloadings decreased 16.1% as rail traffic was negatively impacted by the economic recession in the U.S. Although rail traffic was down for the year, revenue ton-miles increased 6% and carloadings increased 3% in the second half of the year, compared to the first half of the year, reflecting some improvement in the overall economy. |

| • | Demand for new locomotives. Currently, the active locomotive fleet for Class I railroads in North America is about 24,000 units. The average number of new locomotives delivered over the past 10 years was about 1,100 annually. In 2009, about 700 new, heavy-haul locomotives were delivered, compared to about 1,500 in 2008. |

| • | Demand for new freight cars. Currently, the active freight car fleet in North America is about 1.4 million. The average number of new freight cars delivered over the past 10 years was about 47,000 annually. In 2009, about 21,000 new freight cars were delivered, compared to about 60,000 cars in 2008. |

In the U.S., the passenger transit industry is dependent largely on funding from federal, state and local governments, and from fare box revenues. With about 40% of the nation’s passenger transit vehicles, the New York City region is the largest passenger transit market in the U.S., but most major cities also offer either rail or bus transit services.

Demand for North American passenger transit products is driven by a number of factors, including:

| • | Government funding. The U.S. federal government provides money to local transit authorities, primarily to fund the purchase of new equipment and infrastructure for their transit systems. Under a multi-year spending bill known as SAFETEA-LU, federal government funding has increased on average by 6-8% annually since 2005. Due in part to this increased government funding, the number of cars delivered in 2009 remained well above the ten year average, at about 1,300, compared to 1,569 in 2008; and the number of new buses delivered in 2009 increased to about 5,800, compared to about 5,100 in 2008. In the past 10 years, the average number of new transit cars delivered is about 600, and the average number of new buses delivered is about 4,800. SAFETEA-LU expired in September 2009 but funding has been maintained at current levels until a new bill is completed. In February 2009, the U.S. federal government passed additional spending legislation designed to stimulate the U.S. economy. Of the $789 billion spending package, up to $20 billion is to be spent on freight and passenger transportation, as follows: $8.4 billion for public transportation, $8.0 billion for high-speed rail, $1.5 billion for discretionary intermodal projects, and $1.3 billion for AMTRAK. Wabtec expects to benefit from this additional spending, as transit authorities invest in expansion, new equipment and other related projects. |

| • | Ridership. Ridership provides fare box revenues to transit authorities, which use these funds, along with state and local money, primarily for equipment and system maintenance. Based on preliminary figures from the American Public Transportation Association, ridership on U.S. transit vehicles decreased about 4% in 2009, mainly due to the economic recession. Prior to 2009, ridership had increased for six consecutive years. |

Outside of North America, many of the rail systems have historically been focused on passenger transit, rather than freight. In recent years, however, railroads in countries such as Australia, India and China have been investing capital to expand and improve both their freight and passenger rail systems. Throughout the world, some government-owned railroads are being sold to private owners, who often look to improve the efficiency of the rail system by investing in new equipment and new technologies. These investment programs represent opportunities for Wabtec to provide products and services.

In Europe, the majority of the rail system serves the passenger transit market, which is expected to continue growing as high fuel costs and environmental factors encourage investment in public mass transit. France,

4

Table of Contents

Germany, the United Kingdom and Italy are the largest transit markets, representing about two-thirds of passenger traffic in the European Union. About 75% of freight traffic in Europe is hauled by truck, while rail accounts for about 20%. The largest freight markets in Europe are Germany, Poland and the United Kingdom. According to UNIFE, the European market consists of about 33,000 locomotives, about 700,000 freight cars and about 150,000 passenger transit cars. In recent years, the European market purchased on average about 1,300 new locomotives, about 1,000 new freight cars and about 7,500 new passenger transit cars annually.

The Asia/Pacific market is expected to be the second-largest geographic segment by 2016, according to the UNIFE study. Growth is expected to be driven by the continued urbanization of countries such as China and India, and by investment in freight rail infrastructure to serve the mining and natural resources markets in those countries, as well as in Australia. According to UNIFE, this market consists of about 34,000 locomotives and about 1.0 million freight cars. In recent years, China has embarked on a major rail capital investment program, and is expected to spend a record amount of about $120 billion in 2010.

Business Segments and Products

We provide our products and services through two principal business segments, the Freight Group and the Transit Group, both of which have different market characteristics and business drivers.

The Freight Group primarily manufactures and services components for new and existing freight cars and locomotives, builds new switcher locomotives, rebuilds freight locomotives and provides related heat exchange and cooling systems. Customers include large, publicly traded railroads, leasing companies, manufacturers of original equipment such as locomotives and freight cars and utilities. As discussed previously, demand in the freight market is primarily driven by rail traffic, and deliveries of new locomotives and freight cars. In 2009, the Freight Group accounted for 42% of our total sales, with about two-thirds of its sales in North America and the remainder to International customers. About two-thirds of the Freight Group’s sales are in the aftermarket and the remainder in the original equipment market.

The Transit Group primarily manufactures and services components for new and existing passenger transit vehicles, typically subway cars and buses, builds new commuter locomotives and refurbishes subway cars. Customers include public transit authorities and municipalities, leasing companies and manufacturers of subway cars and buses around the world. As discussed previously, demand in the transit market is primarily driven by government funding at all levels and passenger ridership. In 2009, the Transit Group accounted for 58% of our total sales, with about half of its sales in North America and the remainder to International customers and about half in the aftermarket and half in the original equipment market.

Following is a summary of our leading product lines across both of our business segments:

| • | Railway braking equipment and related components |

| • | Freight car truck components and undercarriage components |

| • | Draft gears, couplers and slack adjusters |

| • | Air compressors and dryers |

| • | Positive train control equipment and electronically controlled pneumatic braking products |

| • | Railway electronics, including event recorders, monitoring equipment and end of train devices |

| • | Friction products, including brake shoes and pads |

| • | Rail and bus door assemblies |

| • | Accessibility lifts and ramps for buses and subway cars |

5

Table of Contents

| • | Heat exchangers and cooling products for locomotives and power generation equipment |

| • | Commuter and switcher locomotives |

| • | Transit car and locomotive overhauls |

We have become a leader in the rail industry by capitalizing on the strength of our existing products, technological capabilities and new product innovation, and by our ability to harden products to protect them from severe conditions, including extreme temperatures and high-vibration environments. Over the past several years, we introduced a number of significant new products including electronic braking equipment and train control equipment that encompasses onboard digital data and global positioning communication protocols. In 2007, for example, the Federal Railroad Administration (FRA) approved the use of our Electronic Train Management System®, which offers safety benefits to the rail industry. In 2008, the U.S. federal government enacted a rail safety bill that mandates the use of positive train control technology on a majority of the locomotives and track in the U.S. by December 31, 2015. As the only supplier with a train control product that has received FRA approval, Wabtec is working with the railroads and transit authorities to implement this technology. Supported by our technical staff of over 475 engineers and specialists, we have extensive experience in a broad range of product lines, which enables us to provide comprehensive, systems-based solutions for our customers. We currently own over 1,250 active patents worldwide and over 500 U.S. patents. During the last three years, we have filed for more than 350 patents worldwide in support of our new and evolving product lines.

For additional information on our business segments, see Note 20 of “Notes to Consolidated Financial Statements” included in Part IV, Item 15 of this report.

Competitive Strengths

Our key strengths include:

| • | Leading market positions in core products. Dating back to 1869 and George Westinghouse’s invention of the air brake; we are an established leader in the development and manufacture of pneumatic braking equipment for freight and passenger transit vehicles. We have leveraged our leading position by focusing on research and engineering to expand beyond pneumatic braking components to supplying integrated parts and assemblies for the locomotive through the end of the train. We are a recognized leader in the development and production of electronic recording, measuring and communications systems, highly engineered compressors and heat exchangers for locomotives and a leading manufacturer of freight car components, including electronic braking equipment, draft gears, trucks, brake shoes and electronic end-of-train devices. We are also the leading manufacturer of commuter locomotives and a leading provider of braking equipment, door assemblies, lifts and ramps, and couplers for passenger transit vehicles. |

| • | Breadth of product offering with a stable mix of original equipment market (OEM) and aftermarket business. Our product portfolio is one of the broadest in the rail industry, as we offer a wide selection of quality parts, components and assemblies across the entire train. We believe this comprehensive product offering enables us to leverage our installed base to maintain our leadership position with OEMs and the Class I railroads. We provide our products in both the original equipment market and the aftermarket. Our substantial installed base of products with end-users such as the railroads and the passenger transit authorities is a significant competitive advantage for providing products and services to the aftermarket because these customers often look to purchase safety and performance-related replacement parts from the original equipment components supplier. In addition, as OEMs and Class I railroad operators attempt to modernize fleets with new products designed to improve and maintain safety and efficiency, these products must be designed to be interoperable with existing equipment. Over the last several years, more than 50% of our total net sales have come from our aftermarket products and services business. |

6

Table of Contents

| • | Leading design and engineering capabilities. We believe a hallmark of our relationship with our customers has been our leading design and engineering practice, which has, in our opinion, assisted in the improvement and modernization of global railway equipment. We believe both our customers and the government authorities value our technological capabilities and commitment to innovation, as we seek not only to enhance the efficiency and profitability of our customers, but also to improve the overall safety of the railways through continuous improvement of product performance. The Company has an established record of product improvements and new product development. We have assembled a wide range of patented products, which we believe provides us with a competitive advantage. Wabtec currently owns over 1,250 active patents worldwide and over 500 U.S. patents. During the last three years, we have filed for more than 350 patents worldwide in support of our new and evolving product lines. |

| • | Experience with industry regulatory requirements. The U.S. rail industry is governed by the AAR and by the FRA. These groups mandate rigorous manufacturer certification and new product testing and approval processes that we believe are difficult for new entrants to meet cost-effectively and efficiently without the scale and extensive experience we possess. |

| • | Experienced management team and the Wabtec Performance System. Our executive management team has over 50 years of combined experience with the Company and has implemented numerous initiatives that enable us to manage successfully through cycles in the rail supply market. For example, the Wabtec Performance System (WPS), an ongoing program that focuses on lean manufacturing principles and continuous improvement across all aspects of our business, has been a part of the company’s culture for more than 20 years. As a result, our management team has improved our cost structure, operating leverage and financial flexibility and placed the Company in an excellent position to benefit from growth opportunities. |

Business strategy

Using WPS, we strive to generate sufficient cash to invest in our growth strategies and to build on what we consider to be a leading position as a low-cost producer in the industry while maintaining world-class product quality, technology and customer responsiveness. Through WPS and employee-directed initiatives such as Kaizen, a Japanese-developed team concept, we strive to improve quality, delivery and productivity continuously, and to reduce costs. These efforts enable us to streamline processes, improve product reliability and customer satisfaction, reduce product cycle times and respond more rapidly to market developments. Over time, these lean initiatives have enabled us to increase operating margins, improve cash flow and strengthen our ability to invest in the following growth strategies:

| • | Expand globally and into new product markets. We believe that international markets represent a significant opportunity for future growth. In 2009, sales to non-U.S. customers were $563.4 million, including export sales from the Company’s U.S. operations of $241.3 million. We intend to increase our existing international sales through strategic acquisitions, direct sales of products through our existing subsidiaries and licensees, and joint ventures with railway suppliers which have a strong presence in their local markets. We are specifically targeting markets that operate significant fleets of U.S.-style locomotives and freight cars, including Australia, China, India, Russia, South Africa, and select areas within Europe and South America. In addition, we have opportunities to sell certain products that we currently manufacture for the rail industry into other industrial markets, such as mining, off-highway and energy. These products include heat exchangers and friction materials. |

| • | Expand aftermarket sales. Historically, aftermarket sales are less cyclical than OEM sales because a certain level of aftermarket maintenance and service work must be performed, even during an industry slowdown. In 2009, Wabtec’s aftermarket sales and services represented approximately 54% of the Company’s total sales. Wabtec provides aftermarket parts and services for its components, and the Company is seeking to expand this business with new customers such as short-line and regional railroads, or with customers who currently perform the work in-house. In this way, we expect to take |

7

Table of Contents

| advantage of the rail industry trend toward outsourcing, as railroads and transit authorities focus on their core function of transporting goods and people, rather than maintaining and servicing their equipment. |

| • | Accelerate new product development. We continue to emphasize research and development funding to create new and improved products. We are focusing on technological advances, especially in the areas of electronics, braking products and other on-board equipment, as a means of new product growth. We seek to provide customers with incremental technological advances that offer immediate benefits with cost-effective investments. In 2008, the U.S. federal government enacted a rail safety bill that mandates the use of positive train control technology on a majority of the locomotives and track in the U.S. by December 31, 2015. As the only supplier with a train control product that has received FRA approval, Wabtec is working with the railroads and transit authorities to implement this technology. |

| • | Seek acquisitions, joint ventures and alliances. We are exploring acquisition, joint venture and alliance opportunities using a disciplined, selective approach and rigorous financial criteria. We seek companies that will help Wabtec to grow profitably and expand geographically, while helping to dampen any impact from potential cycles in the North American rail industry. In 2009, Wabtec acquired Unifin, a leading manufacturer of cooling systems and related equipment for the power generation and transmission industry. |

Recent Acquisitions and Joint Ventures

Wabtec has completed certain acquisitions in support of its growth strategies. On October 1, 2009, the Company used cash to acquire Unifin International LP, and its affiliate, Cardinal Pumps and Exchangers, Inc. (“Unifin”), a manufacturer of cooling systems and related equipment for the power generation and transmission industry for a net purchase price of $92.9 million.

In December 2008, the Company acquired 100% of the stock of Standard Car Truck Company (“SCT”), for $302.6 million, net of cash. SCT is a manufacturer and designer of stabilization systems for freight cars, including engineered truck (undercarriage) components such as springs, friction wedges and wear plates. Its Barber® brand truck design is used throughout the world and holds a leading share of the North American market. The company also manufactures and services locomotives components, including compressors and pumps. In October 2008, the Company acquired certain assets related to the development, sale, service, and maintenance of software programs used in train management systems for $4.5 million. In June 2008, the Company acquired 100% of the stock of POLI S.p.A. (“POLI”) for €55.2 million ($87.0 million), net of cash received. POLI is a European-based manufacturer of rail braking equipment including brake discs for high-speed applications, as well as tread brake units and pneumatic brake valves that meet International Union of Railways (“UIC”) standards.

In June 2007, the Company acquired 100% of the stock of Ricon Corporation (“Ricon”), a manufacturer of a variety of electro-mechanical wheelchair lifts and ramps and anti-graffiti windows for $73.6 million.

During 2008, Wabtec expanded its presence in key geographic areas. Wabtec acquired the majority of Beijing Wabtec Huaxia Technology Company, Ltd, which manufactures friction products for the freight car market and invested in a joint venture in China to manufacture other braking-related components. In addition, the Company formed a joint venture in South Africa to manufacture friction products.

Backlog

The Company’s backlog was about $951 million at December 31, 2009.

In 2009, about 54% of our sales came from aftermarket orders, which typically carry lead times of less than 30 days, so they are not recorded in backlog for a significant period of time. As such, the Company’s backlog is mostly an indicator of future original equipment sales, primarily for the Transit Group, and not aftermarket sales.

8

Table of Contents

The Company’s contracts are subject to standard industry cancellation provisions, including cancellations on short notice or upon completion of designated stages. Substantial scope-of-work adjustments are common. For these and other reasons, completion of the Company’s backlog may be delayed or cancelled. The railroad industry, in general, has historically been subject to fluctuations due to overall economic conditions and the level of use of alternative modes of transportation.

The backlog of firm customer orders as of December 31, 2009, and December 31, 2008, and the expected year of completion are as follows:

| In thousands |

Total Backlog 12/31/09 |

Expected Delivery | Total Backlog 12/31/08 |

Expected Delivery | ||||||||||||||

| 2010 | Other Years |

2009 | Other Years | |||||||||||||||

| Freight Group |

$ | 211,339 | $ | 126,177 | $ | 85,162 | $ | 195,717 | $ | 148,617 | $ | 47,100 | ||||||

| Transit Group |

739,330 | 425,517 | 313,813 | 865,005 | 417,014 | 447,991 | ||||||||||||

| Total |

$ | 950,669 | $ | 551,694 | $ | 398,975 | $ | 1,060,722 | $ | 565,631 | $ | 495,091 | ||||||

Engineering and Development

To execute our strategy to develop new products, we invest in a variety of engineering and development activities. For the fiscal years ended December 31, 2009, 2008, and 2007, we invested about $42.4 million, $39.0 million and $37.4 million, respectively, on product development and improvement activities. Sometimes we conduct specific research projects in conjunction with universities, customers and other railroad product suppliers.

Our engineering and development program is largely focused upon train control and new braking technologies, with an emphasis on applying electronics to traditional pneumatic equipment. Electronic braking has been used in the transit industry for years, and freight railroads are beginning to conduct pilot programs to test its reliability and benefits. Freight railroads have generally been slower to accept the technology due to issues over interoperability, connectivity and durability. We are proceeding with efforts to enhance the major components for existing hard-wired braking equipment and development of new electronic technologies for the freight railroads.

We use our Product Development System (PDS) to develop and monitor new product programs. The system requires the product development team to follow consistent steps throughout the development process, from concept to launch, to ensure the product will meet customer expectations and internal profitability targets.

Intellectual Property

We have more than 1,250 active patents worldwide. We also rely on a combination of trade secrets and other intellectual property laws, nondisclosure agreements and other protective measures to establish and protect our proprietary rights in our intellectual property.

Certain trademarks, among them the name WABCO®, were acquired or licensed from American Standard Inc., now known as Trane, in 1990 at the time of our acquisition of the North American operations of the Railway Products Group of Trane. Other trademarks have been developed through the normal course of business, or acquired as a part of our ongoing merger and acquisition program.

We have entered into a variety of license agreements as licensor and licensee. We do not believe that any single license agreement is of material importance to our business or either of our business segments as a whole.

We have issued licenses to the two sole suppliers of railway air brakes and related products in Japan, Nabtesco and Mitsubishi Electric Company. The licensees pay annual license fees to us and also assist us by

9

Table of Contents

acting as liaisons with key Japanese passenger transit vehicle builders for projects in North America. We believe that our relationships with these licensees have been beneficial to our core transit business and customer relationships in North America.

Customers

Our customers include railroads and passenger transit authorities throughout North America, as well as in the United Kingdom, Australia, Europe, Asia and South Africa; manufacturers of transportation equipment, such as locomotives, freight cars, subway vehicles and buses and lessors of such equipment.

In 2009, about 40% of our sales were to customers outside the U.S. and to approximately 100 countries throughout the world. About 54% of our sales were in the aftermarket, with a majority of our remaining sales to OEMs of locomotives, freight cars, subway vehicles and buses.

Our top customers can change from year to year. For the fiscal year ended December 31, 2009, our top five customers, Alstom, Metrolinx (formerly GO Transit (“Greater Toronto Transit Authority”), Kawasaki Railcar Inc., GE Transportation Systems and HSBC Rail, accounted for 22% of our net sales. No one customer represents 10% or more of consolidated sales. We believe that we have strong relationships with all of our key customers.

Competition

We believe that we hold approximately a 50% market share in North America for our primary braking-related equipment and a leading market position in North America for most of our other product lines. On a global basis, our market shares are generally much smaller. We operate in a highly competitive marketplace. Price competition is strong because we have a relatively small number of customers and they are very cost-conscious.

In addition to price, competition is based on product performance and technological leadership, quality, reliability of delivery, and customer service and support.

Our principal competitors vary across product lines, but most competitors tend to be privately held companies. Within North America, New York Air Brake Company, a subsidiary of the German air brake producer Knorr-Bremse AG, is our principal overall OEM competitor. Our competition for locomotive, freight and passenger transit service and repair is primarily from the railroads’ and passenger transit authorities’ in-house operations, Electro-Motive Diesel, GE Transportation Systems, and New York Air Brake/Knorr. We believe our key strengths, which include leading market positions in core products, breadth of product offering with a stable mix of OEM and aftermarket business, leading design and engineering capabilities, significant barriers to entry and an experienced management team, enable us to compete effectively in this marketplace.

Employees

At December 31, 2009, we had 5,812 full-time employees, approximately 37% of whom were unionized. A majority of the employees subject to collective bargaining agreements are within North America and these agreements generally extend through 2010, 2011, 2012, and 2013. Agreements expiring in 2010 cover approximately 21% of the Company’s workforce. We consider our relations with our employees and union representatives to be good, but cannot assure that future contract negotiations will be favorable to us.

Regulation

In the course of our operations, we are subject to various regulations of agencies and other entities. In the United States, these include principally the FRA and the AAR. The FRA administers and enforces federal laws and regulations relating to railroad safety. These regulations govern equipment and safety standards for freight

10

Table of Contents

cars and other rail equipment used in interstate commerce. The AAR oversees a wide variety of rules and regulations governing safety and design of equipment, relationships among railroads with respect to railcars in interchange and other matters. The AAR also certifies railcar builders and component manufacturers that provide equipment for use on railroads in the United States. New products generally must undergo AAR testing and approval processes. As a result of these regulations and those stipulated in other countries in which we derive our revenues, we must maintain certain certifications as a component manufacturer and for products we sell.

Effects of Seasonality

Our business is not typically seasonal, although the third quarter results may be impacted by vacation and plant shutdowns at several of our major customers during this period.

Environmental Matters

Information on environmental matters is included in Note 19 of “Notes to Consolidated Financial Statements” included in Part IV, Item 15 of this report.

Available Information

We maintain an Internet site at www.wabtec.com. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to such reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as well as the annual report to stockholders and other information, are available free of charge on this site. The Internet site and the information contained therein or connected thereto are not incorporated by reference into this Form 10-K. Our Corporate Governance Guidelines, the charters of our Audit, Compensation and Nominating and Corporate Governance Committees, our Code of Conduct, which is applicable to all employees, and our Code of Ethics for Senior Officers, which is applicable to all of our executive officers, are also available free of charge on this site and are available in print to any shareholder who requests them.

| Item 1A. | RISK FACTORS |

Prolonged unfavorable economic and market conditions could adversely affect our business.

Unfavorable general economic and market conditions in the United States and internationally could have a negative impact on our sales and operations. To the extent that these factors result in continued instability of capital markets, shortages of raw materials or component parts, longer sales cycles, deferral or delay of customer orders or an inability to market our products effectively, our business and results of operations could be materially adversely affected.

We are dependent upon key customers.

We rely on several key customers who represent a significant portion of our business. Our top customers can change from year to year. For the fiscal year ended December 31, 2009, our top five customers, Alstom, Metrolinx (formerly GO Transit (“Greater Toronto Transit Authority”), Kawasaki Railcar Inc., GE Transportation Systems and HSBC Rail, accounted for 22% of our net sales. While we believe our relationships with our customers are generally good, our top customers could choose to reduce or terminate their relationships with us. In addition, many of our customers place orders for products on an as-needed basis and operate in cyclical industries. As a result, their order levels have varied from period to period in the past and may vary significantly in the future. Such customer orders are dependent upon their markets and customers, and may be subject to delays and cancellations. As a result of our dependence on our key customers, we could experience a material adverse effect on our business, results of operations and financial condition if we lost any one or more of our key customers or if there is a reduction in their demand for our products.

11

Table of Contents

Our business operates in a highly competitive industry.

We operate in a competitive marketplace and face substantial competition from a limited number of established competitors in the United States and abroad, some of which may have greater financial resources than we do. Price competition is strong and, coupled with the existence of a number of cost conscious purchasers, has historically limited our ability to increase prices. In addition to price, competition is based on product performance and technological leadership, quality, reliability of delivery and customer service and support. There can be no assurance that competition in one or more of our markets will not adversely affect us and our results of operations.

We intend to pursue acquisitions, joint ventures and alliances that involve a number of inherent risks, any of which may cause us not to realize anticipated benefits.

One aspect of our business strategy is to selectively pursue acquisitions, joint ventures and alliances that we believe will improve our market position, and provide opportunities to realize operating synergies. These transactions involve inherent risks and uncertainties, any one of which could have a material adverse effect on our business and results of operations, including:

| • | difficulties in achieving identified financial and operating synergies, including the integration of operations, services and products; |

| • | diversion of Management’s attention from other business concerns; |

| • | the assumption of unknown liabilities; and |

| • | unanticipated changes in the market conditions, business and economic factors affecting such an acquisition. |

We cannot assure that we will be able to consummate any future acquisitions, joint ventures or other business combinations. If we are unable to identify suitable acquisition candidates or to consummate strategic acquisitions, we may be unable to fully implement our business strategy, and our business and results of operations may be adversely affected as a result. In addition, our ability to engage in strategic acquisitions will be dependent on our ability to raise substantial capital, and we may not be able to raise the funds necessary to implement our acquisition strategy on terms satisfactory to us, if at all.

As we introduce new products and services, a failure to predict and react to consumer demand could adversely affect our business.

We have dedicated significant resources to the development, manufacturing and marketing of new products. Decisions to develop and market new transportation products are typically made without firm indications of customer acceptance. Moreover, by their nature, new products may require alteration of existing business methods or threaten to displace existing equipment in which our customers may have a substantial capital investment. There can be no assurance that any new products that we develop will gain widespread acceptance in the marketplace or that such products will be able to compete successfully with other new products or services that may be introduced by competitors. In addition, we may incur additional warranty or other costs as new products are tested and used by customers.

Our revenues are subject to cyclical variations in the railway and passenger transit markets and changes in government spending.

The railway industry historically has been subject to significant fluctuations due to overall economic conditions, the use of alternate methods of transportation and the levels of federal, state and local government spending on railroad transit projects. In economic downturns, railroads have deferred, and may defer, certain expenditures in order to conserve cash in the short term. Reductions in freight traffic may reduce demand for our replacement products.

12

Table of Contents

The passenger transit railroad industry is also cyclical. New passenger transit car orders vary from year to year and are influenced greatly by major replacement programs and by the construction or expansion of transit systems by transit authorities. A substantial portion of our net sales have been, and we expect that a material portion of our future net sales may be, derived from contracts with metropolitan transit and commuter rail authorities and Amtrak. To the extent that future funding for proposed public projects is curtailed or withdrawn altogether as a result of changes in political, economic, fiscal or other conditions beyond our control, such projects may be delayed or cancelled, resulting in a potential loss of business for us, including transit aftermarket and new transit car orders. There can be no assurance that economic conditions will be favorable or that there will not be significant fluctuations adversely affecting the industry as a whole and, as a result, us.

A growing portion of our sales may be derived from our international operations, which exposes us to certain risks inherent in doing business on an international level.

In fiscal year 2009, approximately 40% of our consolidated net sales were to customers outside of the U.S. and we intend to continue to expand our international operations in the future. We currently conduct our international operations through a variety of wholly and majority-owned subsidiaries and joint ventures in Australia, Brazil, Canada, China, Czech Republic, France, Germany, India, Italy, Macedonia, Malaysia, Mexico, Poland, Spain, South Africa, and the United Kingdom. As a result, we are subject to various risks, any one of which could have a material adverse effect on those operations and on our business as a whole, including:

| • | lack of complete operating control; |

| • | lack of local business experience; |

| • | currency exchange fluctuations and devaluations; |

| • | foreign trade restrictions and exchange controls; |

| • | difficulty enforcing agreements and intellectual property rights; |

| • | the potential for nationalization of enterprises; and |

| • | economic, political and social instability and possible terrorist attacks against American interests. |

In addition, certain jurisdictions have laws that limit the ability of non-U.S. subsidiaries and their affiliates to pay dividends and repatriate cash flows.

We may incur increased costs due to fluctuations in interest rates and foreign currency exchange rates.

In the ordinary course of business, we are exposed to increases in interest rates that may adversely affect funding costs associated with variable-rate debt and changes in foreign currency exchange rates. We may seek to minimize these risks through the use of interest rate swap contracts and currency hedging agreements. There can be no assurance that any of these measures will be effective. Any material changes in interest or exchange rates could result in material losses to us.

We may have liability arising from asbestos litigation.

Claims have been filed against the Company and certain of its affiliates in various jurisdictions across the United States by persons alleging bodily injury as a result of exposure to asbestos-containing products. Most of these claims have been made against our wholly owned subsidiary, Railroad Friction Products Corporation (RFPC), and are based on a product sold by RFPC prior to the time that the Company acquired any interest in RFPC.

Most of these claims, including all of the RFPC claims, are submitted to insurance carriers for defense and indemnity or to non-affiliated companies that retain the liabilities for the asbestos-containing products at issue. We cannot, however, assure that all these claims will be fully covered by insurance or that the indemnitors or insurers will remain financially viable. Our ultimate legal and financial liability with respect to these claims, as is the case with other pending litigation, cannot be estimated.

13

Table of Contents

It is Management’s belief that the potential range of loss for asbestos-related bodily injury cases is not reasonably determinable at present due to a variety of factors, including: (1) the asbestos case settlement history of the Company’s wholly owned subsidiary, RFPC; (2) the unpredictable nature of personal injury litigation in general; and (3) the uncertainty of asbestos litigation in particular. Despite this uncertainty, and although the results of the Company’s operations and cash flows for any given period could be adversely affected by asbestos-related lawsuits, Management believes that the final resolution of the Company’s asbestos-related cases will not be material to the Company’s overall financial position, results of operations and cash flows. In general, this belief is based upon: (1) Wabtec’s and RFPC’s history of settlements and dismissals of asbestos-related cases to date; (2) the inability of many plaintiffs to establish any exposure or causal relationship to RFPC’s product; and (3) the inability of many plaintiffs to demonstrate any identifiable injury or compensable loss.

More specifically, as to RFPC, Management’s belief that any losses due to asbestos-related cases would not be material is also based on the fact that RFPC owns insurance which provides coverage for asbestos-related bodily injury claims. To date, RFPC’s insurers have provided RFPC with defense and indemnity in these actions. The overall number of new claims being filed against RFPC has dropped significantly in recent years; however, these new claims, and all previously filed claims, may take a significant period of time to resolve. As to Wabtec and its divisions, Management’s belief that asbestos-related cases will not have a material impact is also based on its position that it has no legal liability for asbestos-related bodily injury claims, and that the former owners of Wabtec’s assets retained asbestos liabilities for the products at issue. To date, Wabtec has been able to successfully defend itself on this basis, including two arbitration decisions and a judicial opinion, all of which confirmed Wabtec’s position that it did not assume any asbestos liabilities from the former owners of certain Wabtec assets. Although Wabtec has incurred defense and administrative costs in connection with asbestos bodily injury actions, these costs have not been material, and the Company has no information that would suggest these costs would become material in the foreseeable future.

We are subject to a variety of environmental laws and regulations.

We are subject to a variety of environmental laws and regulations governing discharges to air and water, the handling, storage and disposal of hazardous or solid waste materials and the remediation of contamination associated with releases of hazardous substances. We believe our operations currently comply in all material respects with all of the various environmental laws and regulations applicable to our business; however, there can be no assurance that environmental requirements will not change in the future or that we will not incur significant costs to comply with such requirements.

Future climate change regulation could result in increased operating costs, affect the demand for our products or affect the ability of our critical suppliers to meet our needs.

The Company has followed the current debate over climate change and the related policy discussion and prospective legislation. The potential challenges for the Company that climate change policy and legislation may pose have been reviewed by the Company. Any such challenges are heavily dependent on the nature and degree of climate change legislation and the extent to which it applies to our industry. At this time, the Company cannot predict the ultimate impact of climate change and climate change legislation on the Company’s operations. Further, when or if these impacts may occur cannot be assessed until scientific analysis and legislative policy are more developed and specific legislative proposals begin to take shape. Any laws or regulations that may be adopted to restrict or reduce emissions of greenhouse gas could require us to incur increased operating costs, and could have an adverse effect on demand for our products. In addition, the price and availability of certain of the raw materials that we use could vary in the future as a result of environmental laws and regulations affecting our suppliers. An increase in the price of our raw materials or a decline in their availability could adversely affect our operating margins or result in reduced demand for our products.

14

Table of Contents

Our manufacturer’s warranties or product liability may expose us to potentially significant claims.

We warrant the workmanship and materials of many of our products. Accordingly, we are subject to a risk of product liability or warranty claims in the event that the failure of any of our products results in personal injury or death, or does not conform to our customers’ specifications. In addition, in recent years, we have introduced a number of new products for which we do not have the same level of historical warranty experience. Although we have not had any material product liability or warranty claims made against us and we currently maintain liability insurance coverage, we cannot assure that product liability claims, if made, would not exceed our insurance coverage limits or that insurance will continue to be available on commercially acceptable terms, if at all. The possibility exists for these types of warranty claims to result in costly product recalls, significant repair costs and damage to our reputation.

Labor disputes may have a material adverse effect on our operations and profitability.

We collectively bargain with labor unions that represent approximately 37% of our employees. Our current collective bargaining agreements generally extend through 2010, 2011, 2012, and 2013. Agreements expiring in 2010 cover approximately 21% of the Company’s workforce. Failure to reach an agreement could result in strikes or other labor protests which could disrupt our operations. If we were to experience a strike or work stoppage, it would be difficult for us to find a sufficient number of employees with the necessary skills to replace these employees. We cannot assure that we will reach any such agreement or that we will not encounter strikes or other types of conflicts with the labor unions of our personnel. Such labor disputes could have an adverse effect on our business, financial condition or results of operations, could cause us to lose revenues and customers and might have permanent effects on our business.

From time to time we are engaged in contractual disputes with our customers.

From time to time, we are engaged in contractual disputes with our customers regarding routine delivery and performance issues as well as adjustments for design changes and related extra work. These disputes are generally resolved in the ordinary course of business without having a material adverse impact on us.

Our indebtedness could adversely affect our financial health.

At December 31, 2009, we had total debt of $391.8 million. If it becomes necessary to access our available borrowing capacity under the 2008 Refinancing Credit Agreement, along with carrying the $241.0 million currently borrowed under this facility and the $150.0 million 6.875% senior notes, being indebted could have important consequences to us. For example, it could:

| • | increase our vulnerability to general adverse economic and industry conditions; |

| • | require us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures, acquisitions and other general corporate purposes; |

| • | limit our flexibility in planning for, or reacting to, changes in our business and the industries in which we operate; |

| • | place us at a disadvantage compared to competitors that have less debt; and |

| • | limit our ability to borrow additional funds. |

The indenture for our $150 million 6.875% senior notes due in 2013 and our 2008 Refinancing Credit Agreement contain various covenants that limit our Management’s discretion in the operation of our businesses.

The indenture governing the notes and our credit agreement contain various covenants that limit our Management’s discretion.

15

Table of Contents

The 2008 Refinancing Credit Agreement limits the Company’s ability to declare or pay cash dividends and prohibits the Company from declaring or making other distributions, subject to certain exceptions. The 2008 Refinancing Credit Agreement contains various other covenants and restrictions including the following limitations: incurrence of additional indebtedness; mergers, consolidations and sales of assets and acquisitions; additional liens; sale and leasebacks; permissible investments, loans and advances; certain debt payments; capital expenditures; and imposes a minimum interest expense coverage ratio and a maximum debt to cash flow ratio.

The indenture under which the senior notes were issued contains covenants and restrictions which limit among other things, the following: the incurrence of indebtedness, payment of dividends and certain distributions, sale of assets, change in control, mergers and consolidations and the incurrence of liens.

The integration of our recently completed acquisitions may not result in anticipated improvements in market position or the realization of anticipated operating synergies or may take longer to realize than expected.

In 2008 and 2009, we completed the acquisition of Poli, SCT and Unifin for a combined $482.6 million, net of cash received. Although we believe that the acquisitions will improve our market position and realize positive operating results, including operating synergies, operating expense reductions and overhead cost savings, we cannot be assured that these improvements will be obtained. The management and acquisition of businesses involves substantial risks, any of which may result in a material adverse effect on our business and results of operations, including:

| • | the uncertainty that an acquired business will achieve anticipated operating results; |

| • | significant expenses to integrate; |

| • | diversion of Management’s attention; |

| • | departure of key personnel from the acquired business; |

| • | effectively managing entrepreneurial spirit and decision-making; |

| • | integration of different information systems; |

| • | unanticipated costs and exposure to unforeseen liabilities; and |

| • | impairment of assets. |

| Item 1B. | UNRESOLVED STAFF COMMENTS |

None.

16

Table of Contents

| Item 2. | PROPERTIES |

Facilities

The following table provides certain summary information about the principal facilities owned or leased by the Company. The Company believes that its facilities and equipment are generally in good condition and that, together with scheduled capital improvements, they are adequate for its present and immediately projected needs. Leases on the facilities are long-term and generally include options to renew. The Company’s corporate headquarters are located at the Wilmerding, PA site.

| Location |

Primary Use |

Segment |

Own/Lease |

Approximate Square Feet |

|||||

| Domestic |

|||||||||

| Wilmerding, PA |

Manufacturing/Service | Freight | Own | 365,000 | (1) | ||||

| Lexington, TN |

Manufacturing | Freight | Own | 170,000 | |||||

| Jackson, TN |

Manufacturing | Freight | Own | 150,000 | |||||

| Chicago, IL |

Manufacturing/Service | Freight | Own | 123,140 | |||||

| Warren, OH |

Manufacturing | Freight | Own | 102,650 | |||||

| Greensburg, PA |

Manufacturing | Freight | Own | 97,800 | |||||

| Coshocton, OH |

Manufacturing/Warehouse/Office | Freight | Own | 83,000 | |||||

| Germantown, MD |

Manufacturing | Freight | Own | 80,000 | |||||

| Salem, OH |

Manufacturing | Freight | Own | 20,000 | |||||

| Gibsonia, PA |

Manufacturing/Office | Freight | Own | 16,160 | (2) | ||||

| Chillicothe, OH |

Manufacturing/Office | Freight | Lease | 104,000 | |||||

| Kansas City, MO |

Service Center | Freight | Lease | 95,900 | |||||

| Strongsville, OH |

Manufacturing/Warehouse/Office | Freight | Lease | 92,000 | |||||

| Pittsburgh, PA |

Manufacturing | Freight | Lease | 90,000 | |||||

| Bensenville, IL |

Manufacturing/Warehouse/Office | Freight | Lease | 58,000 | |||||

| Columbia, SC |

Service Center | Freight | Lease | 40,250 | |||||

| Cedar Rapids, IA |

Manufacturing | Freight | Lease | 37,000 | |||||

| St. Joseph, MI |

Manufacturing/Warehouse | Freight | Lease | 33,625 | (2) | ||||

| Chesapeake, VA |

Manufacturing/Office | Freight | Lease | 22,630 | |||||

| Carson City, NV |

Service Center | Freight | Lease | 22,000 | |||||

| Montgomery, IL |

Warehouse/Office | Freight | Lease | 20,000 | (2) | ||||

| Park Ridge, IL |

Office | Freight | Lease | 15,150 | |||||

| Jackson, TN |

Warehouse | Freight | Lease | 6,000 | |||||

| Oak Creek, WI |

Engineering/Admin | Freight | Lease | 5,000 | |||||

| Twinsburg, OH |

Manufacturing/Office | Freight | Lease | 1,700 | |||||

| Azle, TX |

Office | Freight | Lease | 1,400 | |||||

| Boise, ID |

Manufacturing | Freight /Transit | Own | 326,000 | |||||

| Maxton, NC |

Manufacturing | Freight /Transit | Own | 105,000 | |||||

| Willits, CA |

Manufacturing | Freight /Transit | Own | 70,000 | |||||

| Panorama City, CA |

Manufacturing | Transit | Lease | 200,000 | |||||

| Spartanburg, SC |

Manufacturing/Service | Transit | Lease | 183,600 | |||||

| Buffalo Grove, IL |

Manufacturing | Transit | Lease | 115,570 | |||||

| Plattsburgh, NY |

Manufacturing | Transit | Lease | 64,000 | |||||

| Elmsford, NY |

Service Center | Transit | Lease | 28,000 | |||||

| Spartanburg, SC |

Warehouse | Transit | Lease | 20,000 | |||||

| Green, SC |

Warehouse | Transit | Lease | 17,000 | |||||

| Elkhart, IN |

Warehouse | Transit | Lease | 8,000 | |||||

| Green, SC |

Warehouse | Transit | Lease | 6,000 | |||||

| Avondale, GA |

Sales Office | Transit | Lease | 1,720 | |||||

| San Pablo, CA |

Office | Transit | Lease | 550 |

17

Table of Contents

| Location |

Primary Use |

Segment |

Own/Lease |

Approximate Square Feet | ||||

| New Castle, DE |

Sales Office | Transit | Lease | 400 | ||||

| Baltimore, MD |

Sales Office | Transit | Lease | 350 | ||||

| Mountaintop, PA |

Vacant Land Available for Sale | Own | N/A | |||||

| International |

||||||||

| Wallaceburg (Ontario), Canada |

Foundry | Freight | Own | 126,600 | ||||

| San Luis Potosi, Mexico |

Manufacturing/Service | Freight | Own | 73,100 | ||||

| Skopje, Macedonia |

Manufacturing/Office | Freight | Own | 20,000 | ||||

| Shenyang City, Liaoning Province, China |

Manufacturing | Freight | Lease | 290,550 | ||||

| London (Ontario), Canada |

Manufacturing | Freight | Lease | 103,540 | ||||

| Beijing, China |

Manufacturing | Freight | Lease | 75,347 | ||||

| Stoney Creek (Ontario), Canada |

Manufacturing/Service | Freight | Lease | 47,940 | ||||

| Kolkata, India |

Manufacturing | Freight | Lease | 36,965 | ||||

| Lachine (Quebec), Canada |

Service Center | Freight | Lease | 17,000 | ||||

| Rydalmere, Australia |

Office | Freight | Lease | 14,786 | ||||

| Beijing, China |

Office | Freight | Lease | 3,552 | ||||

| Kuala Lumpur, Malaysia |

Office | Freight | Lease | 2,655 | ||||

| Calgary (Alberta), Canada |

Service Center | Freight | Lease | 984 | ||||

| Kutna Hora, Czech Republic |

Warehouse | Freight | Lease | 532 | ||||

| Kirkcaldy, UK |

Office | Freight | Lease | 200 | ||||

| Nepean (Ontario), Canada |

Office | Freight | Lease | 120 | ||||

| Doncaster, UK |

Manufacturing/Service | Freight /Transit | Own | 330,000 | ||||

| Wetherill Park, Australia |

Manufacturing | Freight /Transit | Lease | 70,600 | ||||

| Kempton Park, South Africa |

Manufacturing | Freight /Transit | Lease | 11,840 | ||||

| Avellino, Italy |

Manufacturing/Office | Transit | Own | 132,495 | ||||

| St. Laurent (Quebec), Canada |

Manufacturing | Transit | Own | 106,000 | ||||

| Recklinghausen, Germany |

Manufacturing | Transit | Own | 86,390 | ||||

| Camisano, Italy |

Manufacturing/Office | Transit | Lease | 136,465 | ||||

| Hangzhou City, Zhejiang Province, China |

Manufacturing | Transit | Lease | 31,032 | ||||

| Belo Horizonte, Brazil |

Manufacturing/Service | Transit | Lease | 33,992 | ||||

| Sassuolo, Italy |

Manufacturing | Transit | Lease | 30,000 | ||||

| Droylsden, UK |

Manufacturing/Office | Transit | Lease | 22,500 | ||||

| Aachen, Germany |

Office | Transit | Lease | 1,615 | ||||

| Munich, Germany |

Office | Transit | Lease | 1,615 | ||||

| Vierzon, France |

Office | Transit | Lease | 1,076 | ||||

| Milan, Italy |

Office | Transit | Lease | 1,000 | ||||

| Derby, UK |

Office | Transit | Lease | 850 | ||||

| Warsaw, Poland |

Office | Transit | Lease | 775 | ||||

| Barcelona, Spain |

Office | Transit | Lease | 110 | ||||

| (1) | Approximately 250,000 square feet are currently used in connection with the Company’s corporate and manufacturing operations. The remainder is leased to third parties. |

| (2) | These facilities were part of the SCT purchase and the operations have been consolidated at other existing plants and are no longer in service. |

| Item 3. | LEGAL PROCEEDINGS |

Information with respect to legal proceedings is included in Note 19 of “Notes to Consolidated Financial Statements” included in Part IV, Item 15 of this report.

| Item 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

None.

18

Table of Contents

EXECUTIVE OFFICERS OF THE REGISTRANT

The following table provides information on our executive officers. They are elected periodically by our Board of Directors and serve at its discretion.

| Officers |

Age |

Position | ||

| Albert J. Neupaver | 59 | President and Chief Executive Officer | ||

| Alvaro Garcia-Tunon | 57 | Senior Vice President, Chief Financial Officer and Secretary | ||

| Raymond T. Betler | 54 | Vice President, Group Executive | ||

| R. Mark Cox | 42 | Vice President, Corporate Development | ||

| Patrick D. Dugan | 43 | Vice President, Finance and Corporate Controller | ||

| Keith P. Hildum | 47 | Vice President and Treasurer | ||

| Charles F. Kovac | 53 | Vice President, Group Executive | ||

| Richard A. Mathes | 55 | Vice President, Group Executive | ||

| David M. Seitz | 45 | Vice President, Senior Counsel and Assistant Secretary | ||

| Scott E. Wahlstrom | 46 | Vice President, Human Resources | ||

| Timothy R. Wesley | 48 | Vice President, Investor Relations and Corporate Communications |

Albert J. Neupaver was named President and Chief Executive Officer of the Company in February, 2006. Prior to joining Wabtec, Mr. Neupaver served in various positions at AMETEK, Inc., a leading global manufacturer of electronic instruments and electric motors. Most recently he served as President of its Electromechanical Group for nine years.

Alvaro Garcia-Tunon has been Senior Vice President, Chief Financial Officer and Secretary of the Company since March 2003. Mr. Garcia-Tunon was Senior Vice President, Finance of the Company from November 1999 until March 2003 and Treasurer of the Company from August 1995 until November 1999.

Raymond T. Betler has been Vice President, Group Executive since August 2008. Prior to joining Wabtec, Mr. Betler served in various positions of increasing responsibility at Bombardier Transportation since 1979. Most recently, Mr. Betler served as President, Total Transit Systems from 2004 until 2008 and before that as President, London Underground Projects from 2002 to 2004.

R. Mark Cox was named Vice President, Corporate Development in September 2006. Prior to joining Wabtec, Mr. Cox served as Director of Business Development for the Electrical Group of Eaton Corporation since 2002. Prior to joining Eaton, Mr. Cox was an investment banker with UBS Warburg, Prudential and Stephens.

Patrick D. Dugan was named Vice President, Finance and Corporate Controller in January 2007. He has served as Corporate Controller since November 2003. Prior to joining Wabtec, Mr. Dugan served as Vice President and Chief Financial Officer of CWI International, Inc. from December 1996 to November 2003. Prior to 1996, Mr. Dugan was a Manager with PricewaterhouseCoopers.

Keith P. Hildum was named Vice President and Treasurer in October 2006. He had been serving as Treasurer of the Company since 2001, and prior to that was Vice President, Finance and Administration—Railroad Operations. He has been with Wabtec since 1999, having held various positions with MotivePower Industries. Prior to MotivePower, Mr. Hildum was a Senior Manager with Deloitte & Touche.

Charles F. Kovac was named Vice President, Group Executive in September 2007. Prior to joining Wabtec, Mr. Kovac served as General Manager of the Global Floor Care/Specialty Motors Division of AMETEK, Inc. since 2003. Prior to joining AMETEK, Inc., Mr. Kovac was Chief Operating Officer of The Teleios Group, LLC from 1999 to 2003.

19

Table of Contents

Richard A. Mathes was named Vice President, Group Executive of Wabtec in December, 2008. Prior to joining Wabtec Mr. Mathes was CEO of SCT from 1995 to 2008, having rejoined SCT in 1989 as President. Mr. Mathes had previously been in sales and marketing with SCT from 1979 through 1984 before leaving to pursue other opportunities in the rail industry. He began his 36 year career in the transportation industry in 1972 with the Missouri Pacific Railroad in St. Louis, MO.

David M. Seitz was promoted to Vice President, Senior Counsel and Assistant Secretary in January 2008. He had served as Senior Counsel and Assistant Secretary of Wabtec since 2000 and was appointed as an executive officer in 2006. Prior to joining Wabtec, Mr. Seitz was General Attorney and Assistant Secretary at Transtar, Inc., and had also been an electrical engineer with Westinghouse Electric Company.

Scott E. Wahlstrom has been Vice President, Human Resources, since November 1999. Previously, Mr. Wahlstrom was Vice President, Human Resources & Administration of MotivePower Industries, Inc. from August 1996 until November 1999.

Timothy R. Wesley has been Vice President, Investor Relations and Corporate Communications since November 1999. Previously, Mr. Wesley was Vice President, Investor and Public Relations of MotivePower Industries, Inc. from August 1996 until November 1999.

PART II

| Item 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

The Common Stock of the Company is listed on the New York Stock Exchange. As of February 22, 2010, there were 47,619,699 shares of Common Stock outstanding held by 794 holders of record. The high and low sales price of the shares and dividends declared per share were as follows:

| 2009 |

High | Low | Dividends | ||||||

| First Quarter |

$ | 40.74 | $ | 23.14 | $ | 0.01 | |||

| Second Quarter |

$ | 39.94 | $ | 25.19 | $ | 0.01 | |||

| Third Quarter |

$ | 40.18 | $ | 29.84 | $ | 0.01 | |||

| Fourth Quarter |

$ | 42.91 | $ | 36.00 | $ | 0.01 | |||

| 2008 |

High | Low | Dividends | ||||||

| First Quarter |

$ | 37.37 | $ | 28.72 | $ | 0.01 | |||

| Second Quarter |

$ | 51.50 | $ | 36.49 | $ | 0.01 | |||

| Third Quarter |

$ | 60.75 | $ | 43.29 | $ | 0.01 | |||

| Fourth Quarter |

$ | 55.81 | $ | 28.86 | $ | 0.01 | |||

The Company’s credit agreement restricts the ability to make dividend payments, with certain exceptions. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and see Note 9 of “Notes to Consolidated Financial Statements” included in Part IV, Item 15 of this report.

At the close of business on February 22, 2010, the Company’s Common Stock traded at $39.36 per share.

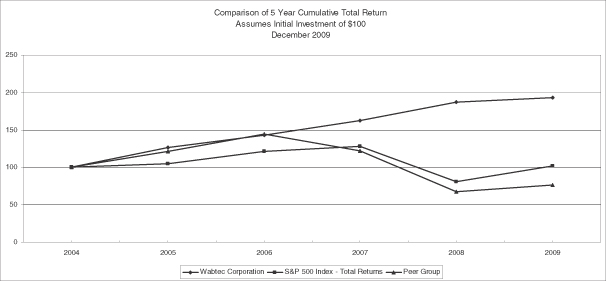

The following performance graph and related information shall not be deemed “soliciting material” or to be “filed” with the Securities and Exchange Commission, nor shall such information be incorporated by reference to any future filings under the Securities Act of 1933 and the Securities Exchange Act of 1934, each as amended, except to the extent that Wabtec specifically incorporates it by reference into such filing. The graph below compares the total stockholder return through December 31, 2009, of Wabtec’s common stock, (i) the S&P 500,

20

Table of Contents

(ii) and our peer group of manufacturing companies consisting of the following publicly traded companies: The Greenbrier Companies, Inc., L.B. Foster Company, Trinity Industries, Portec Rail Products, Inc. and Freight Car America, Inc.

On July 31, 2006, the Board of Directors authorized the repurchase of up to $50 million of the Company’s outstanding shares. On February 20, 2008 the Board of Directors authorized the repurchase of up to an additional $100 million of the Company’s outstanding shares. The Company intends to purchase these shares on the open market or in negotiated or block trades. No time limit was set for the completion of the program. The program qualifies under the 2008 Refinancing Credit Agreement, as applicable, as well as the 6.875% Senior Notes currently outstanding.

During the first quarter of 2008, the Company repurchased 712,900 shares at an average price of $34.29 per share, exhausting the $50.0 million authorization made in 2006. During the second quarter of 2008, the Company repurchased 5,200 shares at an average price of $35.97 per share. No additional shares were repurchased during the third quarter of 2008. During the fourth quarter of 2008, the Company repurchased 599,800 shares at an average price of $35.22 per share. All purchases were on the open market.

During the first quarter of 2009, the Company repurchased 290,000 shares at an average price of $25.08 per share. During the second quarter of 2009, the Company repurchased 379,700 shares at an average price of $32.61 per share. No additional shares were repurchased during the third and fourth quarters of 2009. All purchases were on the open market.

21

Table of Contents

| Item 6. | SELECTED FINANCIAL DATA |

The following table shows selected consolidated financial information of the Company and has been derived from audited financial statements. This financial information should be read in conjunction with, and is qualified by reference to, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the Consolidated Financial Statements of the Company and the Notes thereto included elsewhere in this Form 10-K.

| Year Ended December 31, | ||||||||||||||||||||

| In thousands, except per share amounts |

2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||||||

| Income Statement Data |

||||||||||||||||||||

| Net sales |

$ | 1,401,616 | $ | 1,574,749 | $ | 1,360,088 | $ | 1,087,620 | $ | 1,034,024 | ||||||||||

| Gross profit |

393,326 | 427,186 | 369,619 | 296,777 | 259,646 | |||||||||||||||

| Operating expenses |

(213,294 | ) | (214,670 | ) | (189,878 | ) | (166,626 | ) | (157,717 | ) | ||||||||||

| Income from operations (1) |

$ | 180,032 | $ | 212,516 | $ | 179,741 | $ | 130,151 | $ | 101,929 | ||||||||||

| Interest expense, net |

$ | (16,674 | ) | $ | (8,508 | ) | $ | (3,637 | ) | $ | (2,177 | ) | $ | (9,358 | ) | |||||

| Other income (expense), net |

1 | 292 | (3,650 | ) | (1,417 | ) | (3,055 | ) | ||||||||||||

| Income from continuing operations |

115,055 | 130,554 | 109,387 | 86,494 | 57,685 | |||||||||||||||

| Income (loss) from discontinued operations (net of tax) (2) |

— | (3 | ) | 183 | (1,690 | ) | (1,909 | ) | ||||||||||||

| Net income attributable to Wabtec shareholders (3) |

$ | 115,055 | $ | 130,551 | $ | 109,570 | $ | 84,804 | $ | 55,776 | ||||||||||

| Diluted Earnings per Common Share |

||||||||||||||||||||

| Income from continuing operations |

$ | 2.39 | $ | 2.66 | $ | 2.24 | $ | 1.76 | $ | 1.21 | ||||||||||

| Net income attributable to Wabtec shareholders (3) |

$ | 2.39 | $ | 2.66 | $ | 2.24 | $ | 1.73 | $ | 1.17 | ||||||||||

| Cash dividends declared per share |

$ | 0.04 | $ | 0.04 | $ | 0.04 | $ | 0.04 | $ | 0.04 | ||||||||||

| Fully diluted shares outstanding |

47,977 | 48,847 | 48,873 | 49,108 | 47,595 | |||||||||||||||

| Balance Sheet Data |

||||||||||||||||||||

| Total assets |

$ | 1,585,835 | $ | 1,507,520 | $ | 1,158,702 | $ | 972,842 | $ | 836,357 | ||||||||||

| Cash |

188,659 | 141,805 | 234,689 | 187,979 | 141,365 | |||||||||||||||

| Total debt |

391,780 | 387,080 | 150,250 | 150,000 | 150,000 | |||||||||||||||

| Shareholders’ equity |

778,913 | 645,807 | 617,268 | 469,889 | 379,207 | |||||||||||||||

| (1) | In 2009, includes $3.9 million royalty charge related to the Final Award in the arbitration proceeding between Faiveley Transport Malmo AB and Wabtec. |

| (2) | In 2006, includes $1.7 million relating to the sale of a non-core product division of Rütgers Rail, S.p.A. In 2005, includes $1.6 million relating to the liquidation of the bus door joint venture in China. |

| (3) | In 2009, 2008 and 2006, tax benefits of $9.7 million, $1.0 million and $700,000 were recognized, respectively, primarily related to resolving certain tax issues from prior years that have been closed from further regulatory examination. In 2007 and 2006, a tax benefit of $3.1 million and $5.3 million, respectively, was recognized related to deferred taxes, primarily due to the reversal of previously established valuation allowances on deferred tax assets. |

22

Table of Contents

| Item 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

OVERVIEW