Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2009 |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

001-14223

Commission File Number

KNIGHT CAPITAL GROUP, INC.

(Exact name of registrant as specified in its charter)

DELAWARE

(State or other jurisdiction of incorporation or organization)

22-3689303

(I.R.S. Employer Identification Number)

545 Washington Boulevard, Jersey City, NJ 07310

(Address of principal executive offices and zip code)

Registrant’s telephone number, including area code: (201) 222-9400

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Class A Common Stock, $0.01 par value | The Nasdaq Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the Class A Common Stock held by nonaffiliates of the Registrant was approximately $1.32 billion at June 30, 2009 based upon the closing price for shares of the Registrant’s Class A Common Stock as reported by the Nasdaq Global Select Market on that date. For purposes of this calculation, affiliates are considered to be officers, directors and holders of 10% or more of the outstanding common stock of the Registrant.

At February 24, 2010 the number of shares outstanding of the Registrant’s Class A Common Stock was 94,428,957 and there were no shares outstanding of the Registrant’s Class B Common Stock as of such date.

DOCUMENTS INCORPORATED BY REFERENCE

Definitive Proxy Statement relating to the Company’s 2010 Annual Meeting of Stockholders to be filed hereafter (incorporated, in part, into Part III hereof).

Table of Contents

KNIGHT CAPITAL GROUP, INC.

FORM 10-K ANNUAL REPORT

For the Year Ended December 31, 2009

| Page | ||||

| Item 1. |

Business | 4 | ||

| Item 1A. |

Risk Factors | 15 | ||

| Item 1B. |

Unresolved Staff Comments | 23 | ||

| Item 2. |

Properties | 23 | ||

| Item 3. |

Legal Proceedings | 23 | ||

| Item 4. |

Submission of Matters to a Vote of Security Holders | 25 | ||

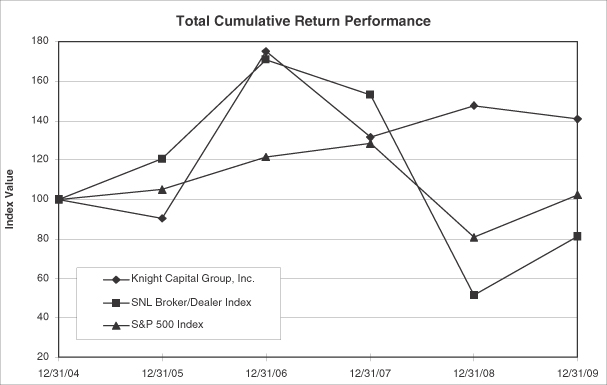

| Item 5. |

26 | |||

| Item 6. |

Selected Financial Data | 30 | ||

| Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

32 | ||

| Item 7A. |

53 | |||

| Item 8. |

56 | |||

| Item 9. |

Changes in and Disagreements With Accountants on Accounting and Financial Disclosures |

98 | ||

| Item 9A. |

98 | |||

| Item 9B. |

98 | |||

| Item 10. |

98 | |||

| Item 11. |

98 | |||

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

98 | ||

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

98 | ||

| Item 14. |

98 | |||

| Item 15. |

99 | |||

| 103 | ||||

| Certifications |

||||

| Exhibit Index |

||||

2

Table of Contents

FORWARD LOOKING STATEMENTS

Certain statements contained in this Annual Report on Form 10-K, including without limitation, those under “Legal Proceedings” in Part I, Item 3, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II, Item 7 (“MD&A”), and “Quantitative and Qualitative Disclosures About Market Risk” in Part II, Item 7A, and the documents incorporated by reference herein may constitute forward-looking statements as defined in the Private Securities Litigation Reform Act of 1995. These forward-looking statements are not historical facts and are based on current expectations, estimates and projections about the Company’s industry, management’s beliefs and certain assumptions made by management, many of which, by their nature, are inherently uncertain and beyond our control. Accordingly, readers are cautioned that any such forward-looking statements are not guarantees of future performance and are subject to certain risks, uncertainties and assumptions that are difficult to predict including, without limitation, risks associated with changes in market structure, legislative or regulatory rule changes, the costs, integration, performance and operation of businesses recently acquired or developed organically, or that may be acquired in the future, by the Company and risks related to the costs and expenses associated with the Company's exit from the Asset Management business. Since such statements involve risks and uncertainties, the actual results and performance of the Company may turn out to be materially different from the results expressed or implied by such forward-looking statements. Given these uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements. Unless otherwise required by law, the Company also disclaims any obligation to update its view of any such risks or uncertainties or to announce publicly the result of any revisions to the forward-looking statements made in this report. Readers should carefully review the risks and uncertainties disclosed in the Company’s reports with the U.S. Securities and Exchange Commission (“SEC”), including those detailed under “Certain Factors Affecting Results of Operations” in MD&A and in “Risk Factors” in Part I, Item 1A herein, and in other reports or documents the Company files with, or furnishes to, the SEC from time to time. This discussion should be read in conjunction with the Company’s Consolidated Financial Statements and the Notes thereto contained in this Form 10-K, and in other reports or documents the Company files with, or furnishes to, the SEC from time to time.

3

Table of Contents

| Item 1. | Business |

Overview

Knight Capital Group, Inc., a Delaware corporation (collectively with its subsidiaries, “Knight” or the “Company”), is a financial services firm that provides market access and trade execution services across multiple asset classes to buy- and sell-side firms as well as offers capital markets services to corporate issuers and private companies.

The Company was organized in January 2000 as the successor to the business of Knight/Trimark Group, Inc. (the “Predecessor”). The Predecessor was organized in April 1998 as the successor to the business of Roundtable Partners, LLC, which was formed in March 1995. In May 2000, the Company changed its name from Knight/Trimark Group, Inc. to Knight Trading Group, Inc., and in May 2005 the Company further changed its name to Knight Capital Group, Inc. Our corporate headquarters are located at 545 Washington Boulevard, Jersey City, New Jersey 07310. Our telephone number is (201) 222-9400.

Financial information concerning our business segments for each of 2009, 2008 and 2007, respectively, is set forth in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Part II, Item 7 (“MD&A”) and the Consolidated Financial Statements and Notes thereto located in Part II, Item 8 entitled “Financial Statements and Supplementary Data.”

Available Information

Our Internet address is www.knight.com. We make available free of charge, on or through the “Investor Relations” section of our corporate website under “SEC Filings”, annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, Forms 3, 4 and 5 filed on behalf of directors and executive officers, and any amendments to those reports filed or furnished pursuant to the Securities Exchange Act of 1934, and our proxy statement as soon as reasonably practicable after such materials are electronically filed with, or furnished to, the SEC. Also posted on our corporate website is our Code of Business Conduct and Ethics (the “Code”) governing our directors, officers and employees. Within the time period required by the SEC, we will post on our corporate website any amendments and waivers to such Code applicable to our executive officers and directors, as defined in the Code.

Our Board of Directors (the “Board”) has standing Finance and Audit, Compensation and Nominating and Corporate Governance committees. Each of these Board committees has a written charter approved by the Board. Our Board has also adopted a set of Corporate Governance Guidelines. Copies of each committee charter, along with the Corporate Governance Guidelines, are posted on the Company’s website. None of the information on our corporate website is incorporated by reference into this report.

All of the above materials are also available in print, without charge, to any person who requests them by writing or telephoning:

Knight Capital Group, Inc.

Communications, Marketing and Investor Relations

545 Washington Boulevard, 3rd Floor

Jersey City, NJ 07310

(201) 222-9400

Unless otherwise indicated, references to the “Company,” “Knight,” “We,” “Us,” or “Our” shall mean Knight Capital Group, Inc. and its subsidiaries.

4

Table of Contents

Operating Segments

Due to the general growth and evolution of our business, effective the fourth quarter of 2009, we separated our former Global Markets segment into two operating segments: i) Equities and ii) Fixed Income, Currencies and Commodities (“FICC”). This breakout is consistent with the organizational structure of our businesses. As a result of this change in segment reporting, we now have three operating segments within our continuing operations, Equities, FICC and Corporate. Effective March 31, 2009 the Company’s former Asset Management segment was classified as a discontinued operation.

| • | Equities—Our Equities segment includes equity market-making, and electronic and voice institutional sales and trading in global equities, futures and options. In the course of market-making and trading, we provide capital facilitation and a range of complementary services. Within our Equities segment, we also offer equity capital markets services. |

| • | FICC—Our FICC segment includes global research, voice sales and trading in fixed income, as well as electronic trading in fixed income and foreign exchange. Fixed income research generates analytical reports containing recommendations across a wide range of securities and sectors. Within our FICC segment, we also offer debt capital markets services. |

| • | Corporate—Our Corporate segment invests in strategic financial services-oriented opportunities, allocates, deploys and monitors all capital, and maintains all corporate overhead expenses and all other expenses that are not attributable to the Equities and FICC segments. |

The following table sets forth: (i) Revenues, (ii) Expenses, (iii) Other income and (iv) Pre-tax earnings (loss) from continuing operations of our segments and on a consolidated basis (in millions):

| For the years ended December 31, | ||||||||||||

| 2009 | 2008 | 2007 | ||||||||||

| Equities |

||||||||||||

| Revenues |

$ | 891.0 | $ | 851.5 | $ | 653.6 | ||||||

| Expenses |

663.7 | 505.0 | 470.1 | |||||||||

| Pre-tax earnings |

227.3 | 346.4 | 183.5 | |||||||||

| FICC |

||||||||||||

| Revenues |

266.7 | 79.3 | 32.1 | |||||||||

| Expenses |

218.8 | 67.0 | 29.0 | |||||||||

| Pre-tax earnings |

47.8 | 12.3 | 3.1 | |||||||||

| Corporate |

||||||||||||

| Revenues |

4.7 | 8.1 | 31.5 | |||||||||

| Expenses |

47.1 | 49.1 | 42.0 | |||||||||

| Other income |

— | 15.9 | 8.8 | |||||||||

| Pre-tax (loss) |

(42.3 | ) | (25.1 | ) | (1.8 | ) | ||||||

| Consolidated |

||||||||||||

| Revenues |

1,162.4 | 938.9 | 717.2 | |||||||||

| Expenses |

929.6 | 621.2 | 541.2 | |||||||||

| Other income |

— | 15.9 | 8.8 | |||||||||

| Pre-tax earnings |

$ | 232.8 | $ | 333.6 | $ | 184.7 | ||||||

Totals may not add due to rounding.

5

Table of Contents

Equities Segment

Business Segment Overview

We provide market access and trade execution services in global equities as well as futures and options. Our approach to trading combines deep liquidity with robust trading technology and capital facilitation, when necessary, to deliver high quality trade executions consistent with client-defined measures. Our hybrid market model features an array of electronic and voice services that allow buy- and sell-side clients to interact with the market based on their specific needs and preferences. This model allows us to attract a larger base of clients with diverse investment styles and strategies, while at the same time, capture a greater share of client order flow. To do so, our model requires that we manage risk and deploy capital effectively as well as maintain efficient and reliable trading technology. Knight is connected to a large number of external market centers including electronic communication networks (“ECN”), alternative trading systems (“ATS”), dark liquidity pools, alternative display facilities (“ADF”), multilateral trading facilities (“MTF”), exchanges and other broker-dealers.

The majority of our Equities revenue is derived from trade executions, making markets and providing market access services in U.S. equities. Generally, market makers display the prices at which they are willing to bid, meaning buy, or offer, meaning sell, securities and adjust their bid and offer prices in response to the forces of supply and demand for each security. As a market maker operating in Nasdaq, the over-the-counter (“OTC”) market for New York Stock Exchange (“NYSE”), NYSE Amex Equities and NYSE Arca listed securities, the OTC Bulletin Board, and the Pink Sheets, we provide trade executions by offering to buy securities from, or sell securities to, institutions and broker-dealers. When acting as principal, we commit our own capital and derive revenues from the difference between the price paid when securities are bought and the price received when securities are sold. We conduct the vast majority of market-making activity as principal through the use of automated quantitative models. Our traders offer execution services for complex trades and a variety of order types. We also provide trade executions for institutions on an agency or riskless principal basis, generating commissions or commission equivalents, respectively. Our trading strategy also employs the use of high velocity algorithmic principal trading models which interact with street flow. These principal models buy and sell equities with high frequency and very short holding periods and are generally designed to benefit from pricing and arbitrage opportunities within the marketplace, while leveraging our robust trading technology.

Our domestic Equities activities are primarily transacted out of the following subsidiaries: Knight Equity Markets, L.P. (“KEM”), Knight Capital Markets LLC (“KCM”) and Knight Direct LLC (“Knight Direct”). KEM, KCM and Knight Direct are broker-dealers registered with the SEC and members of the Financial Industry Regulatory Authority (“FINRA”).

Our international Equities activities are primarily operated through Knight Capital Europe Limited (“KCEL,” formerly known as Knight Equity Markets International Limited). KCEL is a U.K. registered broker-dealer authorized and regulated by the U.K. Financial Services Authority (“FSA”) and provides execution services for institutional and broker-dealer clients in global equities. Knight Capital Asia Limited (“KCAL”, formerly Knight Equity Markets Hong Kong Limited) offers trade execution services in Asian, U.S. and European equities to institutional clients worldwide. KCAL is a broker-dealer registered as an exchange participant with the Hong Kong Stock Exchange and is regulated by the Hong Kong Securities and Futures Commission (“SFC”). We intend to continue to expand our equities business and product offerings in Europe and Asia in 2010.

In addition to our organic initiatives to expand and diversify our products and services within our Equities segment, over the past five years, we have completed the following acquisitions (and subsequent sales of equity interests) of complementary businesses to strengthen our Equities business segment and expand and diversify our products and services:

6

Table of Contents

| • | In June 2005, we acquired the business of Direct Trading Institutional, now operating as Knight Direct. The acquired business was a privately held firm specializing in providing institutions with direct market access (“DMA”). Since the acquisition, we have developed our own advanced electronic platform, Knight DirectTM, which handles all of Knight’s DMA activity. Upon the close of the transaction, the Company made a $40 million initial cash payment. The transaction also contained a two-year contingency from the date of closing for the payment of additional consideration based on the profitability of the business. In the third quarters of 2007 and 2006, the Company paid $10.4 million and $12.7 million, respectively, in additional cash consideration based on the profitability of the business during each of the first two years of operation after the closing of the acquisition. |

| • | In October 2005, we acquired the business of the ATTAIN ECN (now operating as Direct Edge), an ATS that operates an ECN. Direct Edge provides a liquidity destination with the ability to match and route trades in Nasdaq, NYSE, NYSE Amex Equities and NYSE Arca listed securities. |

After the close of business on July 23, 2007 and September 28, 2007, Direct Edge Holdings LLC (“Direct Edge Holdings”), the parent company of Direct Edge, issued equity interests to Citadel Derivatives Group LLC (“Citadel”) in exchange for cash. Immediately following the September 28, 2007 issuance to Citadel, the Company and Citadel sold a portion of their equity interests in Direct Edge Holdings to The Goldman Sachs Group, Inc. for cash. At the close of business on September 28, 2007 (the “Deconsolidation Date”), the Company deconsolidated Direct Edge Holdings as it no longer controlled Direct Edge Holdings as of that date. The results of Direct Edge’s operations have been included in the Consolidated Statements of Operations for all periods presented from the original acquisition date through the Deconsolidation Date. We account for our interest in Direct Edge Holdings under the equity method for periods subsequent to the Deconsolidation Date. In December 2008, we sold part of our remaining interest in Direct Edge Holdings. As a result of that sale we own a 19.9% interest in Direct Edge Holdings.

| • | In January 2008, we acquired EdgeTrade Inc. (“EdgeTrade”) for $58.2 million comprising $28.2 million of cash and approximately 2.3 million shares of unregistered Knight common stock. EdgeTrade was an agency-only trade execution and algorithmic software firm that allowed buy- and sell-side clients to more effectively source liquidity and manage the trading process as well as maintain anonymity, reduce market impact and lower transaction costs. EdgeTrade merged into Knight Direct in August 2008. |

Clients and Products

Clients

Within Equities, we offer products and provide services via electronic and voice access points primarily to two main client groups: sell-side (also referred to as broker-dealers) and buy-side (also referred to as institutions). Our sell-side clients include global, national, regional and on-line broker-dealers, private wealth managers and traditional investment banks in North America and Europe. Knight provides sell-side clients with deep liquidity, high fulfillment rates and high-quality trade executions according to client-defined and regulatory measures. Our buy-side clients include mutual funds, pension plans, plan sponsors, hedge funds, trusts and endowments across North America, Europe and the Asia-Pacific region. Knight provides buy-side clients with deep liquidity, actionable market insights, anonymity and trade executions with minimal market impact.

In 2009, our Equities business did not have any client that accounted for more than 10% of our U.S. equity dollar value traded.

7

Table of Contents

We offer capital markets services to small- and mid-cap corporate issuers as well as private companies in the U.S. We offer corporate issuers and private companies with capital structure advisory services and access to our large equity distribution network.

Products and Services

Our strategy for our Equities segment is to continue to differentiate ourselves from competitors by providing high quality and competitive trade execution services combined with superior client service. Over the past several years we have worked to expand our products and services.

For our buy-side clients, we offer comprehensive, unbundled trade execution services covering the depth and breadth of the market. We handle large complex trades, accessing liquidity from our order flow, as well as other sources. When liquidity is not naturally present in the equities market, we offer capital facilitation, when necessary, to complete our clients’ trades. Our institutional products include access to our global sales and trading team, as well as our electronic trading products. Our institutional equity products and services include global equity, option and futures trade execution solutions, block trading, program trading, special situations/risk arbitrage, soft dollar and commission recapture programs, corporate access services, direct market access through Knight DirectTM, EdgeTrade algorithms and internal crossing through our Knight Match product. In 2009 we added exchange-traded fund (“ETF”) sales and trading and Knight Strategic Research to our institutional equity client offering. The majority of our revenues from institutional clients are commissions on agency transactions or commission-equivalents on riskless principal transactions.

We seek to provide sell-side clients with high quality and competitive trade executions that enable them to satisfy their fiduciary obligations to their customers to seek to obtain the best execution reasonably available in the marketplace. Most of our equity order flow is executed as principal and handled electronically using sophisticated algorithms to optimize the execution of client order flow, including access to our off-exchange liquidity through Knight Link. We maintain a team of cash traders to handle oversized or difficult-to-handle executions. The majority of the revenues we earn from broker-dealer clients are net trading revenues, generated from the difference between the price paid when we buy securities and the price received when we sell securities. We also interact directly with street flow through our high velocity algorithmic principal trading models. We have also begun the process of developing capabilities in electronic options market-making.

During 2009, we commenced the implementation of self-clearing for our equities trades. In connection with this initiative, we have developed, and continue to enhance, a proprietary platform and have enhanced our operational processes and infrastructure. We began clearing a limited number of proprietary trades in the second half of 2009 and expect to increase the number of trades we self-clear in 2010, with the intention to fully self-clear in the future.

Equities Competition

Since the second half of 2008, the securities markets endured unprecedented market conditions with high volatility, dramatic credit tightening and increased counterparty risk, requiring us to continue to adapt to our clients’ needs amidst an evolving competitive landscape. Our client offerings, including our trade execution services, compete primarily with similar products offered by domestic and international broker-dealers, exchanges, ATSs, crossing networks, ECNs and dark liquidity pools. We also compete with various market participants who utilize highly automated, electronic trading models. Another source of competition is broker-dealers who execute portions of their client flow through internal market-making desks rather than sending the client flow to third party execution destinations, such as Knight.

8

Table of Contents

We compete primarily on the basis of our execution standards (including price, liquidity, speed and other client-defined measures), client relationships, client service, payments for order flow and technology. Over the past several years, regulatory changes, competition and the continued focus by regulators and investors on execution quality and overall transaction costs have resulted in a market environment characterized by narrowed spreads and reduced revenue capture metrics. Consequently, maintaining profitability has become extremely difficult for many firms similarly situated to Knight. Generally, improvements in execution quality, such as faster execution speed and greater price improvement, negatively impact the ability to derive revenues from executing client order flow. For example, we have made, and continue to make, changes to our execution protocols and quantitative models, which have had, or could have, a significant impact on our profitability. To remain profitable, some competitors have limited or ceased activity in illiquid or marginally profitable securities or, conversely, have sought to execute a greater volume of trades at a lower cost by increasing the automation and efficiency of their operations.

Competition for order flow in the U.S. equity markets continues to be intense and is evolving rapidly as reflected in publicly disclosed execution metrics; i.e., SEC Rules 605 and 606. These rules, applicable to broker-dealers, add greater disclosure to execution quality and order-routing practices. Rule 605 requires market centers that trade national market system securities to make available to the public monthly electronic reports that include uniform statistical measures of execution quality on a security-by-security basis. Rule 606 requires broker-dealers that route equity and option orders on behalf of their customers to make publicly available quarterly reports that describe their order routing practices and disclose the venues to which customer orders are routed for execution. These statistics on execution quality vary by order sender based on their mix of business. This rule also requires the disclosure of payment for order flow arrangements and internalization practices. The intent of this rule is to encourage routing of order flow to destinations based primarily on the demonstrable quality of executions at those destinations, supported by the order entry firms’ fiduciary obligations to seek to obtain best execution for their customers’ orders.

Commission rates have been under pressure for a number of years, and the ability to execute trades electronically through various competitive trading venues (including both domestic and international broker-dealers, exchanges, ATSs, crossing networks, ECNs and dark liquidity pools) has placed increased pressure on trading commissions. We believe the trend toward increased competition and the growth of these and other alternative trading venues will continue. We may experience competitive pressures in these and other areas in the future as some of our competitors seek to obtain greater market share by reducing prices. Competition for business with institutional clients is based on a variety of factors, including execution quality, research, reputation, soft dollar and commission recapture services, technology, market access (including direct market access and execution algorithms), client relationships, client service, cost and capital facilitation.

Other factors contributing to increasing competition for order flow are the significant mergers among U.S. market centers over the past several years and the launch of independent ECNs, dark liquidity pools and joint ventures with regional stock exchanges.

In the equities capital markets space, we seek to compete against traditional investment banks and smaller boutique-sized firms.

9

Table of Contents

FICC Segment

Business Segment Overview

We provide global research, voice sales and trading in fixed income, as well as electronic trading in fixed income and foreign exchange. Our approach to trading involves traditional sales and trading on behalf of our clients as well as operating neutral platforms with robust trading technology that electronically match buyers and sellers.

We engage in sales and trading for buy-side clients on a riskless principal basis in a variety of fixed income products. We also operate a fixed income ECN that allows sell-side clients to engage in electronic trading of municipals, corporates, agencies, treasuries and certificates of deposit and a foreign exchange ECN that allows buy-side clients to engage in electronic trading in various currencies as well as precious metals.

Our specialized products and services allow us to deepen relationships with existing clients, build liquidity across asset classes and establish relationships with new clients.

Our domestic FICC activities are primarily transacted out of the following subsidiaries: Knight Libertas Holdings LLC and its affiliates (collectively, “Knight Libertas”), Hotspot Holdings FX, Inc. and its subsidiaries (collectively, “Hotspot”) and Knight BondPoint, Inc. (“Knight BondPoint”). Knight BondPoint and one Knight Libertas subsidiary are broker-dealers registered with the SEC and members of FINRA and registered with the Municipal Securities Rulemaking Board (“MSRB”).

Our international FICC activities are primarily operated through KCEL, a U.K. registered broker-dealer authorized and regulated by the FSA. Hotspot and Knight Libertas each has businesses that operate and are regulated in the U.K. and Hong Kong. We intend to continue to expand our FICC business and product offerings in Europe and Asia in 2010.

Over the past four years, we have built up our FICC segment through acquisitions of complementary businesses in an effort to expand and diversify our products and services:

| • | In April 2006, we acquired Hotspot for $77.5 million in cash. Hotspot is an electronic foreign exchange marketplace that provides access to electronic foreign exchange spot trade executions through an advanced ECN-based platform. |

| • | In October 2006, we acquired Knight BondPoint for $18.2 million in cash. Knight BondPoint provides electronic access and trade execution services for the fixed income market. |

| • | In July 2008, we acquired Knight Libertas, for an upfront payment of $50.3 million in cash and approximately 1.5 million shares of unregistered Knight common stock valued at $25.0 million. The terms of the agreement include a potential earn-out to the sellers of up to $75.0 million of unregistered Knight common stock based on the future performance of Knight Libertas during the three-year period following the closing of the transaction. In 2009, Knight Libertas achieved its first year performance target which entitled the sellers to receive $33.3 million of the aforementioned earn-out in 1.6 million shares of unregistered Knight common stock, of which 50% of such shares will be issued in July 2010 and the remaining 50% will be issued in July 2011. Knight Libertas is a riskless principal fixed income broker-dealer specializing in a variety of fixed income products. |

Clients and Products

Clients

Within our FICC segment, we serve a broad range of buy-side and sell-side firms across fixed income, foreign exchange and precious metals.

10

Table of Contents

In 2009, our FICC segment did not have any client that accounted for more than 10% of our fixed income notional value traded.

In fixed income, our buy-side clients include mutual funds, insurance companies, pension funds, hedge funds and banks across North America, Europe and the Asia-Pacific region. Knight Libertas provides buy-side clients with access to investment research, a broad range of securities and products, trading expertise and an extensive client network to match buyers and sellers. Knight BondPoint’s sell-side clients include broker-dealers, financial advisors and private wealth managers in the U.S. Knight BondPoint provides sell-side clients with centralized liquidity, connectivity, price discovery and trading efficiencies.

In foreign exchange and precious metals, Hotspot’s buy-side clients include mutual funds, pension funds, hedge funds, banks and commodity trade advisors across North America, Europe and the Asia-Pacific region. Hotspot provides buy-side clients with access to liquidity and fast anonymous trade executions.

In FICC, we offer debt capital markets services to small- and mid-cap corporate issuers as well as private companies in the U.S. We offer corporate issuers and private companies with capital structure advisory services and access to our large debt distribution network.

Products and Services

The FICC business segment includes fixed income research, voice sales and trading, as well as capital markets activities. This segment also includes electronic fixed income and foreign exchange trading.

Knight Libertas is a fixed income broker-dealer providing buy-side firms with research, sales and riskless principal trading across a broad range of fixed income securities, including high-yield and high-grade corporate bonds, distressed debt, asset- and mortgage-backed securities, federal agency securities, convertible bonds, hybrid securities, syndicated bank loans and emerging markets. Fixed income research generates analytical reports that span the capital structure of fixed income issuers across 30 industry sectors in the U.S. and emerging markets.

Knight BondPoint provides electronic fixed income trading solutions to sell-side firms. Knight BondPoint operates a fixed income ECN that serves as an electronic inter-dealer system and allows clients to access live and executable offerings. Knight BondPoint also provides a front-end application for brokers and advisors as well as a trading application for traders.

Hotspot provides electronic foreign exchange trading solutions to buy-side firms through a foreign exchange ECN that provides clients with access to live, executable prices for 51 currency pairs as well as spot gold and silver streamed by market maker banks and other clients. Hotspot offers clients several access options including direct, high-speed connection and a traditional front-end application.

FICC Competition

During 2009, there was new competition in the fixed income industry, tightening spreads and increased competitive pressure on a global basis. Our institutional fixed income offering, including sales, trading and independent research, competes with traditional investment banks and boutique firms.

There was also increased competition among traditional investment banks with talent moving to smaller boutique-sized firms. Demand for experienced professionals is expected to remain high in 2010.

11

Table of Contents

The tightening of spreads in the fixed income market has put pressure on firms to expand their global presence and to expand into other asset classes. We have continued to expand our offering to include emerging markets, convertibles, syndicated bank loans and ABS/MBS and have broadened our geographical reach by increasing our European sales and trading team. Geographic growth and expansion of our product offering will remain key focuses in 2010.

Independent research remains one of our competitive advantages as many other firms have stopped delivering this type of research to their clients. Our offering of fundamental research across an issuer’s capital structure including bank debt, corporate bonds, convertible bonds, preferred shares and common stock, provides our clients with the ability to make informed decisions.

In the debt capital markets space, we seek to compete against traditional investment banks and smaller boutique-sized firms.

There is increasing pressure in the retail bond space to deliver best execution similar to the equity markets. By delivering centralized liquidity and an electronic inter-dealer system, we offer clients greater price discovery.

In foreign exchange, market conditions are dictated by fluctuations in interest rates, risk and volatility. During 2009, market conditions produced heightened trade volumes across the industry. Hotspot operates a foreign exchange ECN that provides live, executable prices on currency pairs streamed by market maker banks and institutional firms. Hotspot competes with other electronic trading platforms for orders from institutional firms and, to a lesser extent, with foreign exchange sales and trading teams at larger firms. Hotspot provides clients with anonymity, speed, market data and an array of order types. Hotspot competes on the basis of full market transparency, centralized price discovery and full depth-of-book display.

Corporate Segment

Our Corporate segment invests in strategic financial service-oriented opportunities, allocates, deploys and monitors all capital, and maintains all corporate overhead expenses and all other expenses that are not attributable to the Equities and FICC segments. The Corporate segment includes investment income earned on strategic investments and our corporate investment in the Deephaven Funds. Corporate overhead expenses primarily consist of compensation for certain senior executives and other individuals employed at the corporate holding company, legal and other professional expenses related to corporate matters, directors’ fees, investor and public relations expenses and directors’ and officers’ insurance. The results from our Corporate segment for 2008 and 2007 were positively impacted by gains resulting from the partial sales of equity interests in Direct Edge.

Discontinued Operations

During the first quarter of 2009, we exited our Asset Management segment by completing the sale of substantially all of Deephaven’s assets to Stark & Roth, Inc. (together with its affiliates, “Stark”). Stark also replaced Deephaven as the managing member and general partner for the Deephaven Funds. The results of our Asset Management segment have been included within discontinued operations.

Infrastructure

We have invested significant resources to expand our execution capacity and upgrade our trading systems and infrastructure and plan to make additional investments in technology and infrastructure in the future. Our ability to identify and deploy emerging technologies that facilitate the execution of trades, including developing and enhancing our quantitative models, is key to the successful execution of our business model. Technology has enhanced our capacity and ability to handle order flow faster

12

Table of Contents

and also has been an important component of our strategy to comply with government and industry regulations, achieve competitive execution standards, increase trading automation and provide superior client service. We continually enhance our use of technology and quantitative models to further refine our execution services. We also continue to develop and enhance our high velocity algorithmic principal trading models.

We use our proprietary technology and technology licensed from third parties to execute trades, monitor the performance of our traders, assess our inventory positions, manage risk and provide ongoing information to our clients. We are electronically linked to institutions and broker-dealers to provide immediate access to our trading operations and to facilitate the handling of client orders. Our business-to-business portal, and our Knight Link, Knight Match, Knight BondPoint, Hotspot and Knight Direct™ platforms and EdgeTrade algorithms, provide our clients with an array of tools to interact with our trading systems, many marketplaces throughout the globe, and most U.S. equity, futures and options market centers. In addition, we clear the majority of our trade executions through unaffiliated clearing brokers with whom we are electronically linked.

In connection with the implementation of our self-clearing initiative for equities, we developed, and continue to enhance, a proprietary clearing platform. We have deployed a dedicated team of technology, operations, finance and compliance professionals to support these efforts. In the second half of 2009, we began self-clearing a limited number of proprietary equities transactions on a daily basis. We expect to increase the number of trades we self-clear in 2010, with the intention to fully self-clear in the future.

Alternative trading and data center facilities are in place for our primary domestic Equities and FICC operations. These facilities have been designed to allow us to continue a substantial portion of our operations if we are prevented from accessing or utilizing our primary office locations for an extended period of time. While we employ significant steps to develop, implement and maintain reasonable business continuity plans, we cannot guarantee our alternative systems and facilities will provide full continuity of operations after a significant business disruption.

Intellectual Property and Other Proprietary Rights

Our success and ability to compete are dependent to a degree on our intellectual property, which includes our proprietary trading and execution technology, trade secrets and client base. We rely primarily on trade secret, trademark, domain name, patent and contract law to protect our intellectual property. It is our policy to enter into confidentiality, intellectual property invention assignment and/or non-competition and non-solicitation agreements or restrictions with our employees, independent contractors and business partners, and to control access to and distribution of our intellectual property.

Government Regulation and Market Structure

Most aspects of the Company’s business are subject to extensive securities regulation under federal, state and international laws. The SEC, Commodity Futures Trading Commission (“CFTC”), FSA, SFC, FINRA, NYSE, MSRB, National Futures Association (“NFA”), other self-regulatory organizations (“SRO”), and other regulatory bodies, such as state securities commissions and foreign regulators, promulgate numerous rules and regulations that may impact our business. As a matter of public policy, regulatory bodies are charged with safeguarding the integrity of the securities and other financial markets and with protecting the interests of investors in those markets. Regulated entities are subject to regulations concerning all aspects of their business, including trade practices, best execution practices, capital structure, record retention and the conduct of officers, supervisors and registered employees. Failure to comply with any of these laws, rules or regulations could result in administrative or court proceedings, censures, fines, the issuance of cease-and-desist orders or injunctions, or the

13

Table of Contents

suspension or disqualification of the entity and/or its officers, supervisors or registered employees. We, and certain of our past and present officers, directors and employees, have in the past been subject to claims alleging the violation of such laws, rules and regulations. We are currently subject to such matters as further described in Part I, Item 3 “Legal Proceedings” herein. Certain aspects of the Company’s public disclosure, corporate governance principles, internal control environment and the roles of auditors and counsel are subject to the Sarbanes-Oxley Act of 2002 and related regulations and rules of the SEC and Nasdaq.

Rule-making by the SEC, CFTC, FSA, SFC, FINRA, NYSE, MSRB, NFA, other SRO or foreign regulators and corresponding market structure changes has an impact on the Company’s regulated subsidiaries by directly affecting our method of operation and, at times, our profitability. Legislation can impose, and has imposed, significant obligations on broker-dealers, including those of our regulated subsidiaries. These increased obligations require the implementation and maintenance of internal practices, procedures and controls which have increased our costs and may subject us to regulatory inquiries, claims or penalties.

The regulatory environment in which we operate our Equities and FICC business is subject to constant change. Our business, financial condition and operating results may be adversely affected as a result of new or revised legislation or regulations imposed by the U.S. Congress, SEC, CFTC, FSA, SFC, FINRA, NYSE, MSRB, NFA, other SROs, other United States or foreign governmental regulatory authorities, and other regulatory bodies. Additional regulations, changes in existing laws and rules, or changes in interpretations or enforcement of existing laws and rules often directly affect the method of operation and profitability of regulated broker-dealers. We cannot predict what effect, if any, such changes might have. However, there were, and could be, significant technological, operational and compliance costs associated with the obligations which derive from compliance with such regulations.

The market structure in which the Equities and FICC business segments operates is rapidly changing. The expansion of many regional or national exchanges, in which several exchanges have created their own ATSs (e.g., ECNs) and now compete in the OTC, listed, and derivative trading venues, as well as the consolidation of exchanges (e.g., Nasdaq’s acquisition of the Boston and Philadelphia Stock Exchanges, as well as the NYSE’s acquisition of the American Stock Exchange) and the global expansion of exchanges (e.g., Nasdaq and the OMX, and NYSE and Euronext), have altered the landscape of the marketplace and intensified competition.

We have foreign based subsidiaries and plan to continue to expand our international presence. The brokerage industry in many foreign countries is heavily regulated, much like the U.S. The varying compliance requirements of these different regulatory jurisdictions and other factors may limit our ability to conduct business or expand internationally. For example, the Markets in Financial Instruments Directive (“MiFID”) adopted by the European Commission was implemented in November 2007. MiFID represented one of the more significant changes to take place in the operation of European capital markets. There were, and could be, significant technological and compliance costs associated with the obligations which derive from compliance with this regulation.

Net Capital Requirements

Certain of our subsidiaries are subject to the SEC’s Uniform Net Capital Rule. This rule, which specifies minimum net capital requirements for registered broker-dealers, is designed to measure the general financial integrity and liquidity of a broker-dealer and requires that at least a minimum part of its assets be kept in relatively liquid form. In general, net capital is defined as net worth (assets minus liabilities), plus qualifying subordinated borrowings and certain discretionary liabilities, less certain mandatory deductions that result from excluding assets that are not readily convertible into cash and

14

Table of Contents

from valuing conservatively certain other assets. Among these deductions are adjustments, commonly called haircuts, which reflect the possibility of a decline in the market value of an asset before disposition, and non-allowable assets.

Failure to maintain the required net capital may subject a firm to suspension or revocation of registration by the SEC, and suspension or expulsion by FINRA and other regulatory bodies, and ultimately could require the relevant entity’s liquidation. The Uniform Net Capital Rule prohibits payments of dividends, redemption of stock, the prepayment of subordinated indebtedness and the making of any unsecured advance or loan to a stockholder, employee or affiliate, if such payment would reduce the firm’s net capital below required levels.

A change in the Uniform Net Capital Rule, the imposition of new rules or any unusually large charges against net capital could limit those operations that require the intensive use of capital and also could restrict our ability to withdraw capital from our broker-dealer subsidiaries. A significant operating loss or any unusually large charge against net capital could adversely affect our ability to expand or even maintain our present levels of business.

Certain of our foreign subsidiaries are subject to capital adequacy requirements set by their respective regulators.

We believe that during 2009, all of our broker-dealer subsidiaries were in compliance with their capital adequacy requirements. In connection with an ongoing regulatory examination of one of our broker-dealer subsidiaries, an issue has been identified as to whether a cash balance had been maintained in an acceptable control location within a bank, and therefore whether such balance should be considered an allowable asset in determining net capital of the broker-dealer. Several of our broker-dealer subsidiaries maintained balances in similar accounts at the bank. Due to the uncertainty as to the ultimate outcome of the examiner’s findings, we have closed the accounts in question and moved the cash balances to a more commonly used control location. In the event that FINRA and/or the SEC conclude that such balances are deemed to be non-allowable assets, three of our broker-dealer subsidiaries may be considered to have had inadequate regulatory capital at December 31, 2009 due to this administrative matter. While it may be determined that the affected broker-dealers were in technical violation at December 31, 2009, the capital existed within the affected broker-dealers at that time and has subsequently been transferred to a more commonly used control location.

For additional discussion related to net capital, see Footnote 18 “Net Capital Requirements” included in Part II, Item 8 “Financial Statements and Supplementary Data” of this document.

Employees

At December 31, 2009, our headcount from continuing operations was 1,126 full-time employees, compared to 910 full-time employees at December 31, 2008. The increase in headcount is primarily related to personnel additions related to prior acquisitions, new products and geographic expansion throughout the year. Of our 1,126 full-time employees at December 31, 2009, 976 were employed in the U.S. and 150 outside the U.S., primarily in London. None of our employees is subject to a collective bargaining agreement. We believe that our relations with our employees are good.

We face a number of risks that may adversely affect our business, financial condition and operating results. The risks described below are not the only risks facing our Company. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial also may adversely affect our business, financial condition and/or operating results in a material manner.

15

Table of Contents

RISKS RELATED TO OUR BUSINESSES

| • | Conditions in the financial services industry and the securities markets may adversely affect our trading volumes and market liquidity |

Our Equities and FICC operating segments are primarily transaction-based, and declines in trading volumes, prices and market liquidity would adversely affect our business and profitability. Declines in the volume of equities and fixed income securities transactions and in market liquidity generally result in lower revenues from transaction execution activities. Lower price levels of securities and other instruments and tightening spreads may also result in reduced revenue capture, and thereby reduced revenues from trade executions. Declines in market values of securities or other instruments can result in illiquid markets, losses on securities or other instruments held in inventory, the failure of buyers and sellers to fulfill their obligations and settle their trades, and increases in claims and litigation.

During the second half of 2008, the global financial services industry and securities markets experienced unprecedented conditions including substantially increased volatility, losses resulting from declining asset values, defaults on securities, and reduced liquidity. Some of these conditions have continued in 2009 and 2010. These events resulted in the failure of certain financial services firms, have led other firms to seek mergers with commercial banks and forced other firms to become bank holding companies that are regulated by the Federal Reserve Bank. While uncertainty surrounding the credit crisis and expectations for economic recovery led to high overall market volatility in the first half of 2009 and increased trading volume in certain markets, this trend may not continue. If the levels of trading volume decrease as a result of events stemming from the current economic crisis, our transaction-based revenues will decrease. Accordingly, any reduction in trading volumes, market liquidity or volatility could adversely affect our business and financial results in a material fashion.

| • | Our future operating results may fluctuate significantly as a result of numerous factors |

We may experience significant variation in our future results of operations. These fluctuations may result from numerous factors. These factors include, among other things, market conditions and the resulting volatility and credit and counterparty risks that may result; introductions of, or enhancements to, trade execution services by us or our competitors; the value of our securities positions and other instruments and our ability to manage the risks attendant thereto; the volume of our trade execution activities; the dollar value of securities and other instruments traded; the composition and profile of our order flow; our market share with institutional and broker-dealer clients; the performance and size of, and volatility in, our quantitative market-making and program trading portfolios; the performance of our high velocity algorithmic principal trading models; the performance of our international operations; costs associated with international expansion and domestic growth; our ability to manage personnel, overhead and other expenses, including our occupancy expenses under our office leases and expenses and charges relating to legal and regulatory proceedings; the strength of our client relationships; changes in payments for order flow, changes in execution quality and changes in clearing, execution and regulatory transaction costs; the addition or loss of executive management, sales, electronic and voice trading and technology professionals; legislative, legal and regulatory changes; legal and regulatory matters or proceedings; geopolitical risk; the amount and timing of capital expenditures, acquisitions and divestitures; the integration, performance and operation of acquired businesses; the incurrence of costs associated with acquisitions and dispositions; investor sentiment; technological changes and events; seasonality; competition; and market and economic conditions.

Such factors may also have an impact on our ability to achieve our strategic objectives, including, without limitation, increases in our market share, growth and profitability in our Equities and FICC

16

Table of Contents

segments. If demand for our services declines in our Equities or FICC business segments due to any of the above factors, and we are unable to adjust our cost structure on a timely basis, our operating results could be materially and adversely affected. As a result of the foregoing factors, period-to-period comparisons of our revenues and operating results are not necessarily meaningful and such comparisons cannot be relied upon as indicators of future performance. There also can be no assurance that we will be able to continue the rates of revenue growth that we have experienced in the past or that we will be able to improve our operating results.

| • | Our trading activities expose us to the risk of significant losses |

We conduct our trading activities predominantly as principal, which subjects our capital to significant risks. These activities involve the purchase, sale or short sale of securities and other instruments for our own account and, accordingly, involve risks of price fluctuations and illiquidity, or rapid changes in the liquidity of markets that may limit or restrict our ability to either resell securities or other instruments we purchase or to repurchase securities or other instruments we sell in such transactions. From time to time, we may have large position concentrations in securities or other instruments of a single issuer or issuers engaged in a specific industry, which might result in higher trading losses than would occur if our positions and activities were less concentrated. The success of our trading activities primarily depends upon our ability to attract order flow, the performance and size of, and volatility in, our quantitative market-making and program trading portfolios, the performance of our high velocity algorithmic principal trading models, market interaction, the skill of our trading personnel, general market conditions, effective hedging strategies and risk management processes, the price volatility of specific securities or other instruments, and the availability and allocation of capital. To attract order flow, we must be competitive on price, size of securities positions and other instruments traded, liquidity offerings, order execution speed, technology, reputation, and client relationships and service. In our role as a market maker, we attempt to derive a profit from the difference between the prices at which we buy and sell securities. However, competitive forces often require us to match, or improve upon, the quotes other market makers display and to hold varying amounts of securities in inventory. By having to maintain inventory positions, we are subject to a high degree of risk. There can be no assurance that we will be able to manage such risk successfully or that we will not experience significant losses from such activities. All of the above factors could have a material adverse effect on our business, financial condition and operating results.

| • | Regulatory and legal uncertainties could harm our business |

The capital markets industry in the United States and other jurisdictions where we conduct our business, is subject to extensive oversight under federal, state and applicable international laws as well as SRO rules. Broker-dealers and financial services firms are subject to regulations concerning all aspects of their business, including trade practices, best execution practices, capital structure, record-keeping, anti-money laundering and the conduct of their officers, supervisors and registered employees. Our operations and profitability may be directly affected by, among other things, additional legislation or regulation; changes in rules promulgated by the U.S Congress, SEC, CFTC, FSA, SFC, FINRA, NYSE, MSRB, NFA and other regulatory bodies or SROs; and changes in the interpretation or enforcement of existing laws, regulations and rules (including those related to the Foreign Corrupt Practices Act). Failure to comply with these laws, rules or regulations could result in, among other things, administrative or court proceedings, censure, fines, the issuance of cease-and-desist orders or injunctions, loss of membership, or the suspension or disqualification of the market participant or broker-dealer, and/or their officers, supervisors or registered employees. Our ability to comply with applicable laws, regulations and rules is largely dependent on our internal systems to ensure compliance, as well as our ability to attract and retain qualified compliance personnel. We are currently the subject of regulatory reviews and investigations that may result in disciplinary actions in the future due to alleged noncompliance.

17

Table of Contents

The events of 2007, 2008 and 2009 have led to various suggestions of an overhaul in financial regulation. Additional legislation, changes in rules, changes in the interpretation or enforcement of existing laws and rules, or the entering into businesses that subject us to new rules and regulations, may directly affect our mode of operation and our profitability.

The SEC, CFTC, FSA, SFC, FINRA, NYSE, MSRB, NFA and other regulatory bodies and SROs are constantly proposing, or enacting, new regulations for the marketplace. For example, the SEC has proposed a number of new regulations relating to the trading of securities, including: further short sale restrictions, elimination of flash orders, and limitations on the use of indications of interest; most recently, the SEC issued a Concept Release seeking public comment on certain market structure issues such as high frequency trading, co-location, and markets that do not publicly display priced quotations including dark liquidity pools. The SEC has stated that it is seeking to ensure that the current market structure is fair and serves the interests of “long-term investors.” Additionally, there continues to be a debate within Congress as to whether a transaction tax should be imposed on all (or some portion) of equity transactions. Any of these proposed laws, rules or regulations, as well as any regulatory or legal actions or proceedings, changes in legislation or regulation, and changes in market customs and practices could have a material adverse effect on the Company’s business, financial condition and operating results.

| • | Substantial competition could reduce our market share and harm our financial performance |

During the second half of 2008, the securities markets endured unprecedented market conditions with high volatility, dramatic credit tightening and increased counterparty risk. Some of these difficult conditions have continued into 2009 and beyond, requiring us to continue to adapt to our clients’ needs amidst an evolving competitive landscape. All aspects of our business are intensely competitive. We face competition in our Equities business primarily from global, national and regional broker-dealers, exchanges, ATSs, crossing networks, ECNs and dark liquidity pools. Equities competition is based on a number of factors, including our execution standards (e.g., price, liquidity, speed and other client-defined measures), client relationships and service, reputation, market structure, product and service offerings, and technology. In our FICC business, we face competition from global, national and regional broker-dealers who provide fixed income trade execution services, fixed income research firms, spot foreign exchange execution firms and capital market service firms. Competition in our fixed income business is primarily on the basis of the quality of trade execution services, quality of research, market intelligence, quality of professional personnel, price execution, consistency of performance, ability to make markets in a variety of securities and reputation. A number of competitors of our Equities and FICC businesses have greater financial, technical, marketing and other resources than we do. Some of our competitors offer a wider range of services and financial products than we do and have greater name recognition and a more extensive client base. These competitors may be able to respond more quickly than we do to new or evolving opportunities and technologies, market changes, and client requirements and may be able to undertake more extensive promotional activities and offer more attractive terms to clients. Moreover, current and potential competitors have established or may establish cooperative relationships among themselves or with third parties or may consolidate to enhance their services and products. It is possible that new competitors, or alliances among competitors, may also emerge and they may acquire significant market share. The trend toward increased competition in our businesses is expected to continue and it is possible that our competitors may acquire increased market share.

As a result of the above, there can be no assurance that we will be able to compete effectively with current or future competitors, which could have a material adverse effect on our business, financial condition and operating results.

18

Table of Contents

| • | We could lose significant sources of revenues if we lose any of our larger clients |

At times, a limited number of clients has accounted for a significant portion of our order flow, revenues and profitability, and we expect a large portion of the future demand for, and profitability from, our trade execution services to remain concentrated within a limited number of clients. None of our clients is contractually obligated to utilize us for trade execution services and, accordingly, these clients may direct their trade execution activities to other execution providers or market centers at any time. Some of these clients have acquired market makers and specialist firms to internalize order flow or have entered into strategic relationships with competitors. There can be no assurance that we will be able to retain these major clients or that such clients will maintain or increase their demand for our trade execution services. The loss, or a significant reduction, of demand for our services from any of these clients could have a material adverse effect on our business, financial condition and operating results.

| • | Exposure to credit risk and the increased risk of defaults by counterparties may adversely affect our results of operations |

Since the second half of 2008, the market has experienced unprecedented levels of defaults and uncertainty among participants in the financial services industry, with the failure of some firms and the bailout of other distressed institutions. We are at risk if issuers whose securities or other instruments we hold, customers, trading counterparties, counterparties under derivative contracts, clearing agents, exchanges, clearing houses or other financial intermediaries or guarantors default on their obligations to us due to bankruptcy, insolvency, lack of liquidity, adverse economic conditions, operational failure, fraud or other reasons. Such defaults could have a material adverse effect on our results of operations, financial condition and cash flows.

We conduct the majority of our trade executions as principal or riskless-principal with broker-dealers, financial services firms and institutional counterparties. We clear the majority of our trade executions through unaffiliated clearing brokers. Under the terms of the agreements between us and our clearing brokers, the clearing brokers have the right to charge us for losses that result from a counterparty’s failure to fulfill its contractual obligations. No assurance can be given that any such counterparty will not default on its obligations, which default could have a material adverse effect on our business, financial condition and operating results. At any time, a substantial portion of our assets are held at one or more clearing brokers and, accordingly, we are subject to credit risk with respect to such clearing brokers. One firm clears the majority of our trades and holds the majority of our assets. Consequently, we are reliant on the ability of our clearing brokers to adequately discharge their obligations on a timely basis. We are also dependent on the solvency of such clearing brokers. Any failure by the clearing brokers to adequately discharge their obligations on a timely basis, the insolvency of a clearing broker, or any event adversely affecting the clearing brokers could have a material adverse effect on our business, financial condition and operating results.

| • | The move to a self-clearing environment exposes us to significant operational, financial, and liquidity risks |

We have undertaken an initiative to self-clear our securities transactions using an internally-developed platform and currently self-clear a limited number of proprietary equities transactions on a daily basis. We expect to increase the number of trades we self-clear in 2010, with the intention to fully self-clear in the future. The conversion to self-clearing exposes our business to operational risks, including business disruption, operational inefficiencies, liquidity and financing risks and potentially increased expenses and lost revenue opportunities. While our conversion process, including the design and implementation of the clearing platform, redesigned operational processes, enhanced infrastructure, and current and future financing arrangements, has been carefully planned, we may nevertheless encounter difficulties in the process that may lead to operating inefficiencies, including

19

Table of Contents

delays in implementation, dissatisfaction amongst our client base, disruption in the infrastructure that supports the business, inadequate liquidity and financial loss. Any such delay, disruption or failure could adversely affect our ability to effect transactions and manage our exposure to risk.

| • | We may not be able to keep up with rapid technological and other changes or adequately protect our intellectual property |

The markets in which we compete are characterized by rapidly changing technology, evolving industry standards, frequent new product and service announcements, introductions and enhancements, and changing client demands. If we are not able to keep up with these rapid changes on a timely and cost-effective basis, we may be at a competitive disadvantage. The widespread adoption of new internet, networking or telecommunications technologies or other technological changes could require us to incur substantial expenditures to modify or adapt our services or infrastructure. Any failure by us to anticipate or respond adequately to technological advancements, client requirements or changing industry standards or to adequately protect our intellectual property, or any delays in the development, introduction or availability of new services, products or enhancements, could have a material adverse effect on our business, financial condition and operating results.

| • | Capacity constraints, systems failures and delays could harm our business |

Our business activities are heavily dependent on the integrity and performance of the computer and communications systems supporting them and the services of certain third parties. Our systems and operations are vulnerable to damage or interruption from human error, natural disasters, power loss, computer viruses, intentional acts of vandalism, terrorism and other similar events. Extraordinary trading volumes or other events could cause our computer systems to operate at an unacceptably low speed or even fail. While we have invested significant amounts of capital to upgrade the capacity, reliability and scalability of our systems, there can be no assurance that our systems will be sufficient to handle such extraordinary trading volumes. Many of our systems are, and much of our infrastructure is, designed to accommodate additional growth without redesign or replacement; however, we may need to make significant investments in additional hardware and software to accommodate growth. Failure to make necessary expansions and upgrades to our systems and infrastructure could lead to failures and delays. Such failures and delays could cause substantial losses for our clients and could subject us to claims from our clients for losses, including litigation claiming fraud or negligence. In the past, high trading volume has caused significant delays in executing some trading orders, resulting in some clients’ orders being executed at prices they did not anticipate. From time to time, we have reimbursed our clients for losses incurred in connection with systems failures and delays.

Capacity constraints, systems failures and delays may occur again in the future and could cause, among other things, unanticipated disruptions in service to our clients, slower system response times resulting in transactions not being processed as quickly as our clients desire, decreased levels of client service and client satisfaction, and harm to our reputation. If any of these events were to occur, we could suffer a loss of clients, including our largest clients, or a reduction in the growth of our client base, increased operating expenses, financial losses, litigation or other client claims, and regulatory sanctions or additional regulatory burdens.

We have developed business continuity capabilities that can be utilized in the event of a disaster or disruption. Since the timing and impact of disasters and disruptions are unpredictable, we have to be flexible in responding to actual events as they occur. Significant business disruptions can vary in their scope. A disruption might only affect the Company, a building housing the Company, a business district in which the Company is located, a city in which the Company is located or an entire region. Within each of these areas, the severity of the disruption can also vary from minimal to severe. Our business continuity facilities are designed to allow us to substantially continue operations if we are prevented from accessing or utilizing our primary offices for an extended period of time. Although we

20

Table of Contents

have employed significant effort to develop, implement and maintain reasonable business continuity plans, the Company cannot guarantee our systems will fully recover after a significant business disruption in a timely fashion. If we are prevented from using any of our current trading operations or any third party services, or if our business continuity operations do not work effectively, we may not have complete business continuity. This could have a material adverse effect on our business, financial condition and operating results.

| • | Our business is subject to substantial risk from litigation, regulatory investigations and potential liability under federal, state and international laws, rules and regulations |

Many aspects of our business involve substantial risks of liability. We are exposed to liability under federal and state securities laws, other federal and state laws and court decisions, as well as rules and regulations promulgated by the SEC, CFTC, FSA, SFC, FINRA, NYSE, MSRB, NFA, Department of Labor and other U.S. and non-U.S. regulatory bodies and SROs. We are also subject to the risk of litigation. From time to time, we, and certain of our past and present officers, directors and employees, have been named as parties in legal actions, regulatory investigations and proceedings, arbitrations and administrative claims and have been subject to claims alleging the violation of such laws, rules and regulations, some of which have resulted in the payment of fines and settlements. Moreover, we may be required to indemnify past and present officers, directors and employees in regards to these matters. We are subject to such matters as further described in “Legal Proceedings” in Part I, Item 3 herein. Certain corporate events, such as a reduction in our workforce, could also result in additional litigation or arbitration.

As we intend to defend vigorously any such litigation or proceeding, we could incur significant legal expenses. An adverse resolution of any current or future lawsuits, legal or regulatory proceedings or claims against us could have a material adverse effect on the Company’s business and reputation, financial condition and operating results.

| • | We have incurred substantial debt obligations under our Credit Agreement that could adversely affect our operations and financial condition |