Attached files

| file | filename |

|---|---|

| EX-99.1 - EX-99.1 - JANUS CAPITAL GROUP INC | a2196649zex-99_1.htm |

| EX-12.1 - EX-12.1 - JANUS CAPITAL GROUP INC | a2196649zex-12_1.htm |

| EX-21.1 - EX-21.1 - JANUS CAPITAL GROUP INC | a2196649zex-21_1.htm |

| EX-23.1 - EX-23.1 - JANUS CAPITAL GROUP INC | a2196649zex-23_1.htm |

| EX-32.1 - EX-32.1 - JANUS CAPITAL GROUP INC | a2196649zex-32_1.htm |

| EX-31.1 - EX-31.1 - JANUS CAPITAL GROUP INC | a2196649zex-31_1.htm |

| EX-32.2 - EX-32.2 - JANUS CAPITAL GROUP INC | a2196649zex-32_2.htm |

| EX-31.2 - EX-31.2 - JANUS CAPITAL GROUP INC | a2196649zex-31_2.htm |

| EX-10.30 - EX-10.30 - JANUS CAPITAL GROUP INC | a2196649zex-10_30.htm |

| EX-10.14.1 - EX-10.14.1 - JANUS CAPITAL GROUP INC | a2196649zex-10_141.htm |

| EX-10.17.3 - EX-10.17.3 - JANUS CAPITAL GROUP INC | a2196649zex-10_173.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2009

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File Number 001-15253

Janus Capital Group Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

43-1804048 (I.R.S. Employer Identification No.) |

|

151 Detroit Street, Denver, Colorado (Address of principal executive offices) |

80206 (Zip Code) |

(303) 333-3863

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class

|

Name of Each Exchange on Which Registered

|

|

|---|---|---|

| Common Stock, $ 0.01 Per Share Par Value Preferred Stock Purchase Rights |

New York Stock Exchange New York Stock Exchange |

|

Securities registered pursuant to Section 12(g) of the Act: None |

||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Company was required to file such reports), and (2) has been subject to the filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§209 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy of information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

As of June 30, 2009, the aggregate market value of common equity held by non-affiliates was $1,837,813,870. As of February 19, 2010, there were 183,668,927 shares of the Company's common stock, $0.01 par value per share, issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the following documents are incorporated herein by reference into Part of the Form 10-K as indicated:

Document |

Part of Form 10-K into Which Incorporated | |

| Company's Definitive Proxy Statement for the 2010 Annual Meeting of Stockholders | Part III |

JANUS CAPITAL GROUP INC.

2009 FORM 10-K ANNUAL REPORT

TABLE OF CONTENTS

1

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. In addition, Janus Capital Group Inc. and its subsidiaries (collectively, "JCG" or the "Company") may make other written and oral communications from time to time (including, without limitation, in the Company's 2009 Annual Report to Stockholders) that contain such statements. Forward-looking statements include statements as to industry trends, future expectations of the Company and other matters that do not relate strictly to historical facts and are based on certain assumptions by management. These statements are often identified by the use of words such as "may," "will," "expect," "believe," "anticipate," "intend," "could," "should," "estimate" or "continue," and similar expressions or variations. These statements are based on the beliefs and assumptions of Company management based on information currently available to management. Such forward-looking statements are subject to risks, uncertainties and other factors that could cause actual results to differ materially from future results expressed or implied by such forward-looking statements. Important factors that could cause actual results to differ materially from the forward-looking statements include, among others, the risks described in Part I, Item 1A, Risk Factors, and elsewhere in this report and other documents filed or furnished by JCG from time to time with the Securities and Exchange Commission. JCG cautions readers to carefully consider such factors. Furthermore, such forward-looking statements speak only as of the date on which such statements are made. Except to the extent required by applicable law, JCG undertakes no obligation to update any forward-looking statements to reflect events or circumstances after the date of such statements.

Janus Capital Group Inc. and its subsidiaries (collectively, "JCG" or the "Company") provide investment management, administration, distribution and related services to individual and institutional investors through mutual funds, separate accounts and subadvised relationships (collectively referred to as "investment products") in both domestic and international markets. Over the last several years, JCG has expanded its business to become a more diversified manager with increased investment product offerings and distribution capabilities. JCG provides investment advisory services through its primary subsidiaries, Janus Capital Management LLC ("Janus"), INTECH Investment Management LLC ("INTECH") and Perkins Investment Management LLC ("Perkins"). Each of JCG's three primary subsidiaries specializes in specific investment styles and disciplines. JCG's investment products are distributed through three channels: retail intermediary, institutional and international. Each distribution channel focuses on specific investor groups and the unique requirements of each group. As of December 31, 2009, JCG managed $159.7 billion of assets under management.

Revenues are generally based upon a percentage of the market value of assets under management and are calculated as a percentage of the daily average asset balance in accordance with contractual agreements with the Company's investment products or clients. Certain investment products are also subject to performance fees which vary based on a product's relative performance as compared to a benchmark index and the level of assets subject to such fees. Assets under management primarily consist of domestic and international equity and debt securities. Accordingly, fluctuations in domestic and international financial markets, relative investment performance, sales and redemptions of investment products, and changes in the composition of assets under management are all factors that have a direct effect on JCG's operating results.

2

Subsidiaries

Janus

Janus considers itself a leader in equity investing, beginning with the launch of the Janus Fund approximately 40 years ago. Janus offers growth equity, core and international equity, as well as balanced, fixed income, alternative and retail money market investment products. Janus' investment teams are led by its co-Chief Investment Officers, who are charged with driving investment performance across all disciplines while maintaining a structured investment process. Janus' investment teams seek to identify strong businesses with sustainable competitive advantages or improving returns on capital that sell at a discount to what the teams believe they are worth. Janus believes its depth of research, experienced portfolio managers and analysts, willingness to make concentrated investments when Janus believes it has a research edge, and commitment to delivering strong long-term results for its investors are what differentiate Janus from its competitors. At December 31, 2009, Janus managed $95.1 billion of long-term assets and $1.7 billion of money market assets, or 60% of total Company assets under management.

Janus-managed equity mutual funds outperformed the majority of peers with 89%, 94% and 88% of equity mutual funds ranking in the top half of their Lipper categories on a one-, three-and five-year total return basis, respectively, as of December 31, 2009. Additionally, 25%, 100% and 100% of Janus-managed fixed income funds ranked in the top half of their Lipper categories on a one-, three- and five-year total return basis, respectively, as of December 31, 2009. (See Exhibit 99.1 for complete Lipper rankings.)

INTECH

INTECH has managed institutional portfolios since 1987, establishing one of the industry's longest continuous performance records of mathematical equity investment strategies. INTECH's unique investment process is based on a mathematical theorem that seeks to add value for clients by capitalizing on the volatility in stock price movements. INTECH's goal is to achieve long-term returns that outperform a specified benchmark index while controlling risks and trading costs. At December 31, 2009, INTECH managed $48.0 billion, or 30% of total Company assets under management.

INTECH's relative performance was weak in the short- and intermediate- term, with 0%, 50% and 67% of strategies surpassing their respective benchmarks, net of fees, over the one-, three- and five-year periods ended December 31, 2009. However, from their respective inception dates through December 31, 2009, 83% of INTECH's primary investment strategies have outperformed their respective benchmarks, on a net of fees and on a gross fees basis.

Perkins

Perkins has managed value-disciplined investment products since 1980. With its industry experience, fundamental research and careful consideration for risk, Perkins has established a reputation as a respected value manager. Perkins offers value-disciplined investment products, including small, mid and large cap value investment products. On December 31, 2008, JCG purchased an additional 50% ownership stake in Perkins for $90.0 million. At December 31, 2009, Perkins' assets under management totaled $14.9 billion, or 10% of total Company assets under management.

Perkins delivered strong long-term investment performance, with 75%, 100% and 100% of mutual funds ranking in the top half of their Lipper categories on a one-, three- and five-year total return basis, respectively, as of December 31, 2009. (See Exhibit 99.1 for complete Lipper rankings.)

3

Distribution Channels

Retail Intermediary Channel

The retail intermediary channel serves financial intermediaries and retirement plans, which includes asset managers, banks and trusts, broker-dealers, independent planners, third-party administrators and insurance companies. In addition, this channel serves existing individual investors who access JCG's investment products directly. Effective July 6, 2009, JCG merged two of its domestic mutual fund trusts, Janus Investment Fund ("JIF") and Janus Advisor Series ("JAD") into a single trust. The merger was designed to simplify JCG's product offerings and provide mutual fund investors with access to a broader range of Janus investment strategies. Subsequent to the merger, new investors are not able to access JCG's investment products directly.

Assets in the advisory subchannel, a component of the retail intermediary channel, have more than tripled since 2004 and totaled $24.5 billion at December 31, 2009. Significant investments have been made in strengthening the Company's presence in the advisor subchannel over the last several years, doubling the number of external and internal wholesalers and building out robust home office coverage, including a dedicated analyst relations team. Overall assets in the retail intermediary channel totaled $104.6 billion, or 65% of total Company assets under management, at December 31, 2009.

Institutional Channel

The institutional channel serves corporations, endowments, foundations, Taft-Hartley and public fund clients and focuses on distribution direct to the plan sponsor and through consulting relationships. Investors in the institutional channel often rely on advice from third-party consultants. Accordingly, JCG has assembled a Consultant Relations team dedicated to providing information and services to third-party institutional consultants. Although the current asset base in this channel is weighted heavily toward INTECH's mathematical products, the Company is seeking increased penetration of Janus and Perkins products. Assets in the institutional channel totaled $42.8 billion, or 27% of total Company assets under management, at December 31, 2009.

International Channel

The international channel serves professional investors outside of the United States, including central and local government pension plans, corporate pension plans, multi-managers, insurance companies and private banks. International products are offered through separate accounts, subadvisory relationships and Janus Capital Funds Plc, a Dublin-domiciled trust. Assets in the international channel totaled $12.3 billion, or 8% of total Company assets under management, at December 31, 2009.

COMPETITION

The investment management industry is relatively mature and saturated with competitors that provide services similar to JCG. As such, JCG encounters significant competition in all areas of its business. JCG competes with other investment managers, mutual fund advisers, brokerage and investment banking firms, insurance companies, hedge funds, venture capitalists, banks and other financial institutions, many of which are larger, have proprietary access to distribution, have a broader range of product choices and investment capabilities, and have greater capital resources. Additionally, the marketplace for investment products is rapidly changing; investors are becoming more sophisticated; the demand for and access to investment advice and information are becoming more widespread; and more investors are demanding investment vehicles that are customized to their personal requirements.

JCG believes its ability to successfully compete in the investment management industry will be based on its ability to achieve consistently strong investment performance, maintain and build upon its distribution relationships and continue to create new ones, develop new investment products well-suited

4

for its distribution channels and attractive to underlying clients and investors, offer a diverse platform of investment choices and vehicles, provide effective shareowner servicing, retain and strengthen the confidence of its clients, and attract and retain talented investment and sales personnel.

REGULATION

The investment management industry is subject to extensive federal, state and international laws and regulations intended to benefit or protect the shareholders of investment products such as those managed by JCG's subsidiaries and advisory clients of JCG subsidiaries. The costs of complying with such laws and regulations have significantly increased and may continue to contribute significantly to the costs of doing business as an investment adviser. These laws and regulations generally grant supervisory agencies broad administrative powers, including the power to limit or restrict the conduct of businesses such as JCG's, and to impose sanctions for failure to comply with the laws and regulations. Possible consequences or sanctions for such failure to comply include, but are not limited to, voiding of investment advisory and subadvisory agreements; the suspension of individual employees (particularly investment management and sales personnel); limitations on engaging in certain lines of business for specified periods of time; revocation of registrations; disgorgement of profits; and censures and fines. Further, such laws and regulations may provide the basis for litigation that may also result in significant costs and reputational harm to covered entities such as JCG.

The Investment Advisers Act of 1940

The Securities and Exchange Commission (the "SEC") is the federal agency generally responsible for administering the U.S. federal securities laws. Certain subsidiaries of JCG are registered investment advisers under the Investment Advisers Act of 1940, as amended (the "Investment Advisers Act") and, as such, are regulated by the SEC. The Investment Advisers Act requires registered investment advisers to comply with numerous and pervasive obligations, including, among others, recordkeeping requirements, operational procedures, registration and reporting and disclosure obligations. Certain subsidiaries of JCG are also registered with regulatory authorities in various states, and thus are subject to the oversight and regulation of such states' regulatory agencies.

The Investment Company Act of 1940

Certain of JCG's subsidiaries act as adviser or subadviser to both proprietary and non-proprietary mutual funds, which are registered with the SEC pursuant to the Investment Company Act of 1940, as amended (the "1940 Act"). Certain of JCG's subsidiaries also serve as adviser or subadviser to investment products that are not required to be registered under the 1940 Act. As an adviser or subadviser to a registered investment company, these subsidiaries must comply with the requirements of the 1940 Act and related regulations including, among others, requirements relating to operations, fees charged, sales, accounting, recordkeeping, disclosure and governance. In addition, the adviser or subadviser to a registered investment company generally has obligations with respect to the qualification of the registered investment company under the Internal Revenue Code of 1986, as amended (the "Code").

Broker-Dealer Regulations

JCG's limited purpose broker-dealer subsidiary, Janus Distributors LLC ("JD"), is registered with the SEC under the Securities Exchange Act of 1934, as amended (the "Exchange Act"), and is a member of the Financial Industry Regulatory Authority ("FINRA"), the securities industry's domestic self-regulatory organization. JD is the general distributor and agent of the sale and distribution of shares of certain mutual funds that are directly advised or serviced by certain of JCG's subsidiaries. The SEC imposes various requirements on JD's operations including disclosure, recordkeeping and accounting. FINRA has established conduct rules for all securities transactions among broker-dealers

5

and private investors, trading rules for the over-the-counter markets and operational rules for its member firms. The SEC and FINRA also impose net capital requirements on registered broker-dealers.

JD is also subject to regulation under state law. The federal securities laws prohibit states from imposing substantive requirements on broker-dealers that exceed those under federal law. This does not preclude the states from imposing registration requirements on broker-dealers that operate within their jurisdiction or from sanctioning these broker-dealers and their employees for engaging in misconduct.

ERISA

Certain JCG subsidiaries are also subject to the Employee Retirement Income Security Act of 1974, as amended ("ERISA"), and related regulations to the extent they are considered "fiduciaries" under ERISA with respect to some of their clients. ERISA, related provisions of the Code and regulations issued by the U.S. Department of Labor impose duties on persons who are fiduciaries under ERISA and prohibit some transactions involving the assets of each ERISA plan that is a client of a JCG subsidiary as well as some transactions by the fiduciaries (and several other related parties) to such plans.

International Regulations

Certain JCG subsidiaries are authorized to conduct investment business in international markets and are subject to foreign regulation. JCG's international subsidiaries are subject to the regulatory supervision and requirements of various agencies, including the Financial Services Authority in the United Kingdom, the Irish Financial Services Regulatory Authority, the Securities and Futures Commission of Hong Kong, the Monetary Authority of Singapore, the Financial Services Agency of Japan, the Commissione Nazionale per le Societa e la Borsa in Italy, the Federal Financial Supervisory Authority of Germany, the Australian Securities and Investments Commission and the Canadian Provincial Securities Commissions. These regulatory agencies have broad supervisory and disciplinary powers, including, among others, the power to temporarily or permanently revoke the authorization to conduct regulated business, the suspension of registered employees, and censures and fines for both regulated businesses and their registered employees.

Many of the non-U.S. securities exchanges and regulatory authorities have imposed rules (and others may impose rules) relating to capital requirements applicable to JCG's foreign subsidiaries. These rules, which specify minimum capital requirements, are designed to measure general financial integrity and liquidity, and require that a minimum amount of assets be kept in relatively liquid form.

EMPLOYEES

As of December 31, 2009, JCG had 1,126 full-time employees. None of these employees is represented by a labor union.

AVAILABLE INFORMATION

Copies of JCG's filings with the SEC can be obtained from the SEC's Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Information can be obtained about the operation of the Public Reference Room by calling the SEC at (800) SEC-0330. The SEC also maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at http://www.sec.gov.

JCG makes available free of charge its annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K and amendments thereto as soon as reasonably practical after such filing has been made with the SEC. Reports may be obtained through the Investor Relations section of

6

JCG's website (http://ir.janus.com) or by contacting JCG at (888) 834-2536. The contents of JCG's website are not incorporated herein for any purpose.

JCG's Officer Code of Ethics for Principal Executive Officer and Senior Financial Officers (including its chief executive officer and chief financial officer) (the "Officer Code"); Corporate Code of Business Conduct and Ethics for all employees; corporate governance guidelines; and the charters of key committees of the board of directors (including the Audit, Compensation, Nominating and Corporate Governance, and Planning and Strategy committees) are available on its website (http://ir.janus.com/documents.cfm), and printed copies are available to any shareholder upon request by calling JCG at (888) 834-2536. Any future amendments to or waivers of the Officer Code will be posted to the Investor Relations section of JCG's website.

ADDITIONAL FINANCIAL INFORMATION

See additional financial information about segments and geographical areas in Part II, Item 8, Financial Statements and Supplementary Data, Note 20 — Segment and Geographic Information, of this Annual Report on Form 10-K.

JCG's revenues and profits are primarily dependent on the value, composition and relative investment performance of its investment products.

Any decrease in the value or amount of assets under management will cause a decline in revenues and operating results. Assets under management may decline for various reasons, many of which are not under JCG's control.

Factors that could cause assets under management and revenues to decline include the following:

- •

- Declines in financial markets. JCG's assets under

management are concentrated in the U.S. financial markets and, to a lesser extent, in the international financial markets. As such, declines in the financial markets or the market segments in which

JCG's investment products are concentrated will cause assets under management to decrease.

- •

- Declines in fixed income markets. In the case of fixed

income investment products, which invest in high-quality short-term instruments as well as other fixed income securities, the value of the assets may decline as a result of

changes in interest rates, available liquidity in the markets in which a security trades, an issuer's actual or perceived creditworthiness, or an issuer's ability to meet its obligations.

- •

- Redemptions and other withdrawals. Investors (in response

to adverse market conditions, inconsistent investment performance, the pursuit of other investment opportunities or other factors) may reduce their investments in specific JCG investment products or

in the market segments in which JCG's investment products are concentrated.

- •

- Political and general economic risks. The investment

products managed by JCG may have significant investments in international markets that are subject to risk of loss from political or diplomatic developments, government policies, civil unrest,

currency fluctuations and changes in legislation related to foreign ownership. International markets, particularly emerging markets, are often smaller, may not have the liquidity of established

markets, may lack established regulations and may experience significantly more volatility than established markets.

- •

- Relative investment performance. JCG's investment products are often judged on their performance as compared to benchmark indices, peer groups or on an absolute return basis. Any period of underperformance of investment products may result in the loss of existing assets and impact JCG's ability to attract new assets. In addition, approximately 19% of the Company's assets under

7

management at December 31, 2009, are subject to performance fees. Pending mutual fund shareholder approval in 2010, additional mutual funds representing approximately 26% of assets under management as of December 31, 2009, will become subject to performance fees. If approved, these mutual funds will become subject to performance fees over the next three years, with the first fee recognized in 2011. Performance fees are based on each product's investment performance as compared to an established benchmark index over a specified period of time. If investment products subject to performance fees underperform their respective benchmark index for a defined period, JCG's revenues and thus results of operations may be adversely impacted. In addition, performance fees subject JCG's revenues to increased volatility.

JCG's results are dependent on its ability to attract and retain key personnel.

The investment management business is highly dependent on the ability to attract, retain and motivate highly skilled, and often highly specialized, technical, executive, sales and investment management personnel. The market for investment and sales professionals is extremely competitive and is increasingly characterized by the frequent movement of portfolio managers, analysts and salespersons among different firms. Any cost-reduction initiative, changes to management structure, shifts in corporate culture, changes to corporate governance authority, or adjustments or reductions to compensation could impact JCG's ability to retain key personnel and could result in legal claims. If JCG is unable to retain key personnel, it could have an adverse effect on JCG's results of operations and financial condition.

JCG is dependent upon third-party distribution channels to access clients and potential clients.

JCG's ability to market and distribute its investment products is significantly dependent on access to the client base of insurance companies, defined contribution plan administrators, securities firms, broker-dealers, banks and other distribution channels. These companies generally offer their clients various investment products in addition to, and in competition with, JCG. Further, the private account business uses referrals from financial planners, investment advisers and other professionals. JCG cannot be certain that it will continue to have access to these third-party distribution channels or have an opportunity to offer some or all of its investment products through these channels. In addition, JCG's existing relationships with third-party distributors and access to new distributors could be adversely impacted by recent consolidation within the financial services industry. Consolidation may result in increased distribution costs, a reduction in the number of third parties distributing JCG's investment products or increased competition to access third-party distribution channels. The inability to access clients through third-party distribution channels could have a material adverse effect on JCG's ability to maintain or increase assets under management, its financial condition, results of operations or business prospects.

INTECH's investment process is highly dependent on key employees and proprietary software.

INTECH's investment process is based on complex and proprietary mathematical models that seek to outperform various indices by capitalizing on the volatility in stock price movements while controlling trading costs and overall risk relative to the index. The maintenance of such models for current products and the development of new products are highly dependent on certain key INTECH employees. If INTECH is unable to retain key personnel or if the mathematical investment strategies fail to produce the intended results, INTECH may not be able to maintain the historical level of investment performance and clients may redeem assets, which could have an adverse effect on JCG's results of operations and financial condition.

8

The regulatory environment in which JCG operates has changed and may continue to change.

JCG may be adversely affected as a result of new or revised legislation or regulations, or by changes in the interpretation or enforcement of existing laws and regulations. The costs and burdens of compliance with these and other new reporting and operational requirements and regulations have increased significantly and may continue to increase the cost of operating mutual funds and other investment products, which could have an adverse effect on JCG's results of operations and financial condition. (See Part I, Item 1, Business — Regulation of this Annual Report on Form 10-K.)

JCG's business may be vulnerable to failures or breaches in support systems and customer service functions.

The ability to consistently and reliably obtain securities pricing information, process shareowner transactions, and provide reports and other customer service to the shareowners of funds and other investment products managed by JCG as well as the protection of confidential information maintained by it is essential to JCG's operations. Any delays or inaccuracies in obtaining pricing information, JCG's ability to price illiquid or thinly traded securities without readily obtainable market quotes, processing shareowner transactions or providing reports, and any other inadequacies in other customer service functions could alienate customers and potentially give rise to claims against JCG. JCG's customer service capabilities as well as JCG's ability to obtain prompt and accurate securities pricing information and to process shareowner transactions and reports are dependent on communication and information systems and services provided by third-party vendors.

Although JCG has established disaster recovery plans, these systems could suffer failures or interruptions due to various natural or man-made causes, and the backup procedures and capabilities may not be adequate to avoid extended interruptions. Additionally, JCG places significant reliance on its automated systems, thereby increasing the related risks if such systems were to fail. A failure of these systems could have an adverse effect on JCG's results of operations and financial condition.

In addition, JCG maintains confidential information relating to its clients and business operations. JCG systems could be infiltrated by unauthorized users or damaged by computer viruses or other malicious software code, or authorized persons could inadvertently or intentionally release confidential or proprietary information. Such disclosure could be detrimental to JCG's reputation and lead to legal claims, regulatory action, increased costs or loss of revenue, among other things.

JCG's business is dependent on investment advisory agreements that are subject to termination, non-renewal or reductions in fees.

JCG derives revenue and net income from investment advisory agreements with mutual funds and other investment products. The termination of, or failure to renew, one or more of these agreements or the reduction of the fee rates applicable to such agreements could have a material adverse effect on revenues and profits. With respect to investment advisory agreements with mutual funds, these agreements may be terminated by either party with notice, or terminated in the event of an "assignment" (as defined in the 1940 Act), and must be approved and renewed annually by the independent members of each fund's board of directors or trustees, or its shareowners, as required by law. In addition, the board of directors or trustees of certain funds and separate accounts generally may terminate these investment advisory agreements upon written notice for any reason and without penalty.

JCG's substantial indebtedness could adversely affect its financial condition and results of operations.

JCG has a significant amount of indebtedness, which could limit its ability to obtain additional financing for working capital, capital expenditures, acquisitions, debt servicing requirements or other purposes. Debt servicing requirements will increase JCG's vulnerability to adverse economic, market and industry conditions; limit JCG's flexibility in planning for, or reacting to, changes in business

9

operations or to the asset management industry overall; and place JCG at a disadvantage in relation to competitors that have lower debt levels. In addition, all of JCG's outstanding debt, excluding its convertible debt, is subject to an increase in interest rates in the event of a credit rating downgrade by either Standard & Poor's ("S&P") or Moody's Investors Service, Inc. ("Moody's"). Certain of JCG's indebtedness is also subject to repurchase at 101% of the principal balance if the Company experiences a change of control and in connection therewith the applicable notes become rated below investment grade. (See Part II, Item 8, Financial Statements and Supplementary Data, Note 8 — Debt, of this Annual Report on Form 10-K.) Any or all of the above events and/or factors have and could continue adversely affecting JCG's results of operations and financial condition.

JCG may incur losses as a result of providing support to money market funds advised by the Company.

JCG's money market funds (the "Money Funds") seek to provide current income and limit exposure to losses by investing in high-quality, investment-grade securities with short-term durations. Adverse events or circumstances related to individual securities or the market in which the securities trade may cause other-than-temporary declines in value. In these situations, JCG may elect to support the Money Funds in a variety of means, including but not limited to, purchasing securities held by the Money Funds, reimbursing for any losses incurred or providing a letter of credit. JCG is not contractually or legally obligated to support the Money Funds. JCG has, however, provided financial support to certain Money Funds in the past and may do so in the future.

JCG is named as a defendant in class action lawsuits and other related litigation.

JCG and an affiliate of JCG are named as defendants in class action lawsuits and other litigation. (See Part II, Item 8, Financial Statements and Supplemental Data, Note 17 — Litigation, of this Annual Report on Form 10-K.) These lawsuits seek specified or unspecified compensatory and punitive damages. JCG is unable to estimate the range of potential losses that would be incurred if the plaintiffs in any of these actions were to prevail, or to determine the total potential effect that they may have on JCG's results of operations, financial position and cash flows. Any settlement or judgment on the merits of these actions could have a material adverse effect on JCG's liquidity, results of operations and financial condition.

JCG operates in a highly competitive environment and its current fee structure may be reduced.

The investment management business is highly competitive and has relatively low barriers to entry. JCG's current fee structure may be subject to downward pressure due to these factors. Moreover, in recent years there has been a trend toward lower fees in the investment management industry. Fee reductions on existing or future new business as well as changes in regulations pertaining to its fee structure could have an adverse effect on JCG's revenues and results of operations.

JCG has a significant level of intangible assets and goodwill that are subject to annual impairment review.

Intangible assets and goodwill totaled $1.8 billion at December 31, 2009. The value of these assets may not be realized for a variety of reasons, including, but not limited to, significant redemptions and unfavorable economic conditions. JCG has recorded goodwill and intangible asset impairments in the past and could incur similar charges in the future. JCG reviews the carrying value of intangible assets not subject to amortization on an annual basis, or more frequently if indications exist suggesting that the fair value of its intangible assets may be below their carrying value. JCG evaluates intangible assets subject to amortization whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Should a review indicate impairment, a write-down of the carrying value of the intangible asset could occur, resulting in a non-cash charge which would adversely affect JCG's results of operations for the period.

10

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

JCG's headquarters are located in Denver, Colorado. JCG leases office space from non-affiliated companies for administrative, investment and shareowner servicing operations in Denver and Aurora, Colorado; Chicago, Illinois; Princeton, New Jersey; West Palm Beach, Florida; London; Milan; Munich; Singapore; Hong Kong; Tokyo; and Melbourne.

In the opinion of management, the space and equipment owned or leased by the Company are adequate for existing operating needs.

The information set forth in response to Item 103 of Regulation S-K under "Legal Proceedings" is incorporated by reference from Part II, Item 8, Financial Statements and Supplemental Data, Note 17 — Litigation, of this Annual Report on Form 10-K.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

No matters were submitted to a vote of security holders during the three-month period ended December 31, 2009.

11

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

JCG Common Stock

JCG's common stock is traded on the New York Stock Exchange ("NYSE") (symbol: JNS). The following table sets forth the high and low sale prices as reported on the NYSE composite tape for each completed quarter since January 1, 2008.

| |

2009 | 2008 | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Quarter

|

High | Low | High | Low | |||||||||

First |

$ | 9.66 | $ | 3.95 | $ | 33.00 | $ | 21.65 | |||||

Second |

$ | 12.37 | $ | 6.56 | $ | 31.54 | $ | 22.65 | |||||

Third |

$ | 14.90 | $ | 9.84 | $ | 36.88 | $ | 19.70 | |||||

Fourth |

$ | 15.82 | $ | 12.60 | $ | 25.72 | $ | 5.18 | |||||

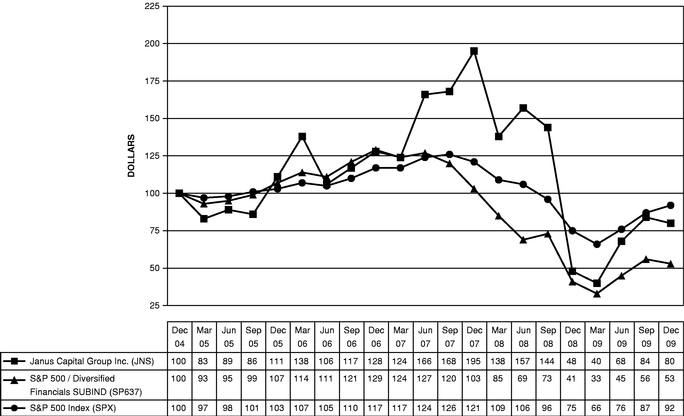

The following graph illustrates the cumulative total shareholder return (rounded to the nearest whole dollar) of JCG's common stock over the five-year period ending December 31, 2009, the last trading day of 2009, and compares it to the cumulative total return on the S&P 500 Index and the S&P Diversified Financials Index. The comparison assumes a $100 investment on December 31, 2004, in JCG's common stock and in each of the foregoing indices and assumes reinvestment of dividends, if any. This table is not intended to forecast future performance of JCG's common stock.

On December 31, 2009, there were approximately 3,580 holders of record of JCG's outstanding common stock.

12

JCG declared an annual $0.04 per share dividend in the second quarter 2009, 2008 and 2007. The payment of cash dividends is within the discretion of JCG's Board of Directors and will depend on many factors, including, but not limited to, JCG's results of operations, financial condition, capital requirements, restrictions imposed by financing arrangements, general business conditions and legal requirements.

Common Stock Repurchases

On July 22, 2008, JCG's Board of Directors authorized a fifth $500 million stock repurchase program with no expiration date to take effect when the current authorization is utilized. The amount that may yet be repurchased under current unexpired authorizations as of December 31, 2009 is $521.2 million. There were no share repurchases for the 12 months ended December 31, 2009, under the current authorization or from employees as part of a share withholding program (established under Rule 10b5-1 of the Exchange Act). JCG currently no longer repurchases shares from employees under a share withholding program. Tax withholdings on vesting employee stock-based compensation are satisfied by selling shares on the open market.

13

ITEM 6. SELECTED FINANCIAL DATA

The selected financial data below should be read in conjunction with Part II, Item 7, Management's Discussion and Analysis of Financial Condition and Results of Operations, of this Annual Report on Form 10-K and Part II, Item 8, Financial Statements and Supplementary Data, of this Annual Report on Form 10-K.

| |

Year Ended December 31, | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||

| |

(dollars in millions, except operating data and per share data) |

||||||||||||||||

Income Statement: |

|||||||||||||||||

Revenues (1) |

$ | 848.7 | $ | 1,037.9 | $ | 1,117.0 | $ | 935.8 | $ | 868.3 | |||||||

Operating expenses (2) |

1,526.2 |

704.8 |

767.7 |

696.9 |

675.1 |

||||||||||||

Operating income (loss) |

(677.5 | ) | 333.1 | 349.3 | 238.9 | 193.2 | |||||||||||

Interest expense (3) |

(74.0 | ) | (75.5 | ) | (58.8 | ) | (32.3 | ) | (28.6 | ) | |||||||

Other, net (4) |

(4.7 | ) | (50.8 | ) | 32.4 | 37.0 | 37.9 | ||||||||||

Gain on early extinguishment of debt (5) |

5.8 | — | — | — | — | ||||||||||||

Income tax provision |

6.3 | (68.8 | ) | (116.4 | ) | (90.1 | ) | (72.8 | ) | ||||||||

Equity in earnings of unconsolidated affiliates |

— | 9.0 | 7.2 | 7.1 | 7.1 | ||||||||||||

Income (loss) from continuing operations |

(744.1 | ) | 147.0 | 213.7 | 160.6 | 136.8 | |||||||||||

Discontinued operations (6) |

— | (1.5 | ) | (75.7 | ) | (5.3 | ) | (29.0 | ) | ||||||||

Net income (loss) |

(744.1 | ) | 145.5 | 138.0 | 155.3 | 107.8 | |||||||||||

Noncontrolling interest |

(13.0 | ) | (8.6 | ) | (21.7 | ) | (21.7 | ) | (20.0 | ) | |||||||

Net income (loss) attributable to JCG |

$ | (757.1 | ) | $ | 136.9 | $ | 116.3 | $ | 133.6 | $ | 87.8 | ||||||

Basic earnings (loss) per share attributable to JCG common shareholders (7) |

|||||||||||||||||

Income (loss) from continuing operations |

$ | (4.55 | ) | $ | 0.87 | $ | 1.09 | $ | 0.69 | $ | 0.53 | ||||||

Discontinued operations |

— | (0.01 | ) | (0.43 | ) | (0.03 | ) | (0.13 | ) | ||||||||

Net income (loss) |

$ | (4.55 | ) | $ | 0.86 | $ | 0.66 | $ | 0.66 | $ | 0.40 | ||||||

Diluted earnings (loss) per share attributable to JCG common shareholders (7) |

|||||||||||||||||

Income (loss) from continuing operations |

$ | (4.55 | ) | $ | 0.86 | $ | 1.07 | $ | 0.68 | $ | 0.53 | ||||||

Discontinued operations |

— | (0.01 | ) | (0.42 | ) | (0.03 | ) | (0.13 | ) | ||||||||

Net income (loss) |

$ | (4.55 | ) | $ | 0.85 | $ | 0.65 | $ | 0.66 | $ | 0.40 | ||||||

Dividends Declared per Share |

$ | 0.04 | $ | 0.04 | $ | 0.04 | $ | 0.04 | $ | 0.04 | |||||||

Balance Sheet (as of December 31): |

|||||||||||||||||

Total assets |

$ | 2,530.3 | $ | 3,336.7 | $ | 3,564.1 | $ | 3,537.9 | $ | 3,628.5 | |||||||

Long-term debt obligations |

$ | 792.0 | $ | 1,106.0 | $ | 1,127.7 | $ | 537.2 | $ | 262.2 | |||||||

Other long-term liabilities |

$ | 438.5 | $ | 450.5 | $ | 470.0 | $ | 490.9 | $ | 501.5 | |||||||

Redeemable noncontrolling interests |

$ | 101.1 | $ | 106.8 | $ | 245.8 | $ | 329.0 | $ | 382.4 | |||||||

Operating Data (in billions): |

|||||||||||||||||

Year-end assets under management |

$ | 159.7 | $ | 123.5 | $ | 206.7 | $ | 167.7 | $ | 148.5 | |||||||

Average assets under management |

$ | 134.5 | $ | 174.2 | $ | 190.4 | $ | 156.7 | $ | 135.2 | |||||||

Long-term net flows (8) |

$ | 0.9 | $ | (0.6 | ) | $ | 9.8 | $ | 2.3 | $ | 2.0 | ||||||

- (1)

- Revenues generally vary with average assets under management. However, revenues also include performance fees, which vary with relative investment performance and the amount of assets subject to

14

such fees. Beginning in 2007, certain mutual funds became subject to performance fees. JCG earned $16.5 million of performance fees from mutual funds during the year ended December 31, 2009, and $11.2 million of performance fees from mutual funds during each of the years ended December 31, 2008 and 2007.

- (2)

- Operating expenses include impairments, restructuring, legal fees and settlement costs (net of insurance recoveries). Impairment

charges are related to terminated investment management relationships with assigned intangible values and facility closures. Restructuring and impairment charges totaled $856.7 million,

$11.0 million and $5.5 million in 2009, 2006 and 2005, respectively. Legal fees and settlement costs (net of insurance recoveries), totaled $31.4 million, $(14.1) million and

$(9.3) million in 2009, 2006 and 2005, respectively.

- (3)

- Interest expense for 2007 increased from 2006 as a result of issuing $748.4 million of additional debt in

2007.

- (4)

- During 2007, JCG classified certain investment securities as trading. Net gains/(losses) on trading securities of

$10.6 million, $(41.1) million and $17.6 million were recognized in earnings for 2009, 2008 and 2007, respectively. In addition, JCG recognized impairment charges of $5.2 million

on available-for-sale securities in 2009 and $21.0 million and $18.2 million in 2008 and 2007, respectively, associated with structured investment vehicle ("SIV")

securities acquired from money market funds advised by Janus.

- (5)

- During 2009, JCG recognized a $5.8 million net gain on early extinguishment of debt related to the repurchase of a portion of

the Company's outstanding 2011, 2012 and 2017 senior notes in a tender offer.

- (6)

- During the third quarter 2007, JCG initiated a plan to dispose of Rapid Solutions Group ("RSG"), previously reported as the Printing

and Fulfillment segment. Prior periods have been reclassified to separately present the results of continuing and discontinued operations. The results of discontinued operations for 2007 include

impairment charges totaling $67.1 million (net of a $6.2 million tax benefit) to write down the carrying value of RSG to estimated fair value less costs to

sell.

- (7)

- Each component of earnings per share presented has been individually rounded.

- (8)

- Money market flows have been excluded due to the short-term nature of such investments.

15

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

2009 SUMMARY

The deterioration in global market conditions in the fourth quarter 2008 and first quarter 2009 significantly impacted JCG's assets under management, revenues, operating margin and net income. JCG responded to declining market conditions by reducing its workforce in the fourth quarter 2008 and by implementing other cost-reduction measures, which resulted in fixed and discretionary cost savings of approximately $45 million in 2009.

Based on the decline in global markets, JCG's stock price, assets under management and revenues in the first quarter 2009, JCG revised its operating forecast downward and evaluated intangible assets and goodwill for impairment as of March 31, 2009. As a result of these assessments, JCG recognized impairment charges of $109.7 million and $747.0 million on mutual fund advisory contracts and goodwill, respectively, in the first quarter 2009.

Improving market conditions in the second quarter 2009 provided JCG with an opportunity to strengthen its balance sheet. In July 2009, JCG issued 20.9 million shares of common stock, par value $0.01, at $11.00 per share and concurrently issued 3.250% convertible senior notes ("convertible senior notes"). Proceeds, net of issuance costs from the common stock and convertible senior notes offerings totaled approximately $218.1 million and $164.3 million, respectively. The combined proceeds of the common stock and convertible senior notes offerings, together with available cash, were used to repurchase $443.3 million aggregate principal amount of the Company's outstanding 2011, 2012 and 2017 senior notes in a tender offer, with the focus on the 2011 and 2012 senior notes. JCG recognized a $5.8 million net gain on early extinguishment of debt related to the tender of these notes.

At the time of the common stock and convertible debt offerings, JCG announced the departure of Gary D. Black and the appointment of Timothy K. Armour as interim Chief Executive Officer. In connection with Mr. Black's departure, JCG incurred a $12.1 million charge, including approximately $6.8 million of cash and $5.3 million for the acceleration of unvested stock, options and mutual fund share awards.

The Company's 2009 operating results were also impacted by litigation settlements and an unfavorable judgment totaling $31.4 million.

On January 7, 2010, JCG announced the appointment of Richard M. Weil as Chief Executive Officer effective February 1, 2010.

INVESTMENT PERFORMANCE

Relative long-term investment performance remained strong with approximately 75%, 88% and 86% of JCG's complex-wide mutual funds in the top half of their Lipper categories on a one-, three- and five-year total return basis, respectively, as of December 31, 2009. (See Exhibit 99.1 for complete Lipper rankings.)

Janus-managed equity mutual funds outperformed the majority of peers with 89%, 94% and 88% of equity mutual funds in the top half of their Lipper categories on a one-, three- and five-year total return basis, respectively, as of December 31, 2009. Additionally, Janus-managed fixed income funds had strong long-term investment performance with 25%, 100% and 100% of fixed income mutual funds in the top half of their Lipper categories on a one-, three- and five-year total return basis, respectively, as of December 31, 2009. (See Exhibit 99.1 for complete Lipper rankings.)

INTECH's relative investment performance continued to be weak in the short- and intermediate-term, with 0%, 50% and 67% of strategies outperforming their respective benchmarks, net of fees, over the one-, three- and five-year periods ended December 31, 2009. Continued underperformance in key

16

investment strategies, particularly in large cap growth strategies, may lead to additional INTECH outflows.

Perkins delivered strong long-term investment performance with 75%, 100% and 100% of mutual funds ranking in the top half of their Lipper categories on a one-, three- and five-year total return basis, respectively, as of December 31, 2009. (See Exhibit 99.1 for complete Lipper rankings.)

INVESTMENT MANAGEMENT OPERATIONS (CONTINUING OPERATIONS)

Assets Under Management and Flows

Valuation

The value of assets under management is derived from the cash and investment securities underlying JCG's investment products. Investment security values are determined using unadjusted or adjusted quoted market prices and independent third-party price quotes in active markets. For debt securities with maturities of 60 days or less, the amortized cost method is used to determine the value. Securities for which market prices are not readily available or are considered unreliable are internally valued using appropriate methodologies for each security type or by engaging third-party specialists. The value of the majority of the securities underlying JCG's investment products is derived from readily available and reliable market price quotations.

The pricing policies for mutual funds advised by JCG's subsidiaries (the "Funds") are established by the Funds' Independent Board of Trustees and are designed to test and validate fair value measurements. Responsibility for pricing securities held within separate and subadvised accounts may be delegated by the separate or subadvised client to JCG or another party.

Assets Under Management and Flows

Total Company assets under management increased $36.2 billion, or 29.3%, from 2008. The increase was primarily driven by net market appreciation of $41.5 billion as a result of improving market conditions in the last half of 2009. Total Company long-term net inflows were $0.9 billion in 2009 compared to long-term net outflows of $0.6 billion in 2008.

JCG gained market share in the equity and fixed income markets through positive long-term net flow generation at Janus and Perkins in 2009. Janus and Perkins equity funds had a combined organic growth rate of 5% in 2009 compared to 2% organic growth for the equity industry. Additionally, Janus fixed income funds posted an organic growth rate of 88% in 2009 compared to 25% organic growth for the fixed income industry.

Janus' long-term net inflows were $3.9 billion in 2009 compared to long-term net outflows of $1.2 billion in 2008. The increase from 2008 is primarily due to lower redemptions in the retail intermediary channel as market conditions improved combined with strong investment performance. Additionally, 72% of Janus' long-term net inflows were derived from fixed income products.

INTECH's long-term net outflows were $5.6 billion in 2009 and $1.7 billion in 2008. Net outflows in 2009 were primarily due to a decrease in long-term sales of $6.5 billion as a result of the challenging institutional environment that persisted throughout 2009, and relative underperformance in the large cap growth strategies.

Perkins' long-term net inflows were $2.6 billion in 2009 and $2.3 billion in 2008. Perkins' 2009 positive long-term net flows were primarily derived through the retail intermediary channel.

Net money market outflows were $6.2 billion in 2009 compared to $5.0 billion in 2008. Money market assets declined from 2008 as a result of JCG exiting its institutional money market business in early 2009.

17

The following table presents the components of JCG's assets under management (in billions):

| |

Year Ended December 31, | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2009 | 2008 | 2007 | ||||||||||

Beginning of period assets |

$ | 123.5 | $ | 206.7 | $ | 167.7 | |||||||

Long-term sales |

|||||||||||||

Janus |

21.0 | 29.9 | 30.9 | ||||||||||

INTECH |

5.8 | 12.3 | 15.5 | ||||||||||

Perkins |

6.6 | 6.3 | 2.9 | ||||||||||

Long-term redemptions |

|||||||||||||

Janus |

(17.1 | ) | (31.1 | ) | (22.7 | ) | |||||||

INTECH |

(11.4 | ) | (14.0 | ) | (13.2 | ) | |||||||

Perkins |

(4.0 | ) | (4.0 | ) | (3.6 | ) | |||||||

Long-term net flows* |

|||||||||||||

Janus |

3.9 | (1.2 | ) | 8.2 | |||||||||

INTECH |

(5.6 | ) | (1.7 | ) | 2.3 | ||||||||

Perkins |

2.6 | 2.3 | (0.7 | ) | |||||||||

Total long-term net flows |

0.9 | (0.6 | ) | 9.8 | |||||||||

Net money market flows |

(6.2 | ) | (5.0 | ) | 5.2 | ||||||||

Market/fund performance |

41.5 | (77.6 | ) | 24.0 | |||||||||

End of period assets |

$ | 159.7 | $ | 123.5 | $ | 206.7 | |||||||

Long-term net flows by distribution channel |

|||||||||||||

Retail intermediary |

$ | 6.0 | $ | 0.8 | $ | 6.9 | |||||||

Institutional |

(5.1 | ) | (3.1 | ) | 1.7 | ||||||||

International |

— | 1.7 | 1.2 | ||||||||||

Total |

$ | 0.9 | $ | (0.6 | ) | $ | 9.8 | ||||||

Average assets under management |

|||||||||||||

Janus |

$ | 76.8 | $ | 95.6 | $ | 100.1 | |||||||

INTECH |

43.9 | 57.4 | 68.1 | ||||||||||

Perkins |

11.2 | 10.2 | 11.6 | ||||||||||

Money market |

2.6 | 11.0 | 10.6 | ||||||||||

Total |

$ | 134.5 | $ | 174.2 | $ | 190.4 | |||||||

- *

- Excludes money market flows. Sales and redemptions are presented net on a separate line due to the short-term nature of the investments.

Assets and Flows by Investment Discipline

JCG, through its primary subsidiaries, offers investment products based on a diversified set of investment disciplines. Janus offers growth/blend and global/international equity as well as fixed income, alternative and money market investment products. INTECH offers mathematical-based investment

18

products and Perkins offers value-disciplined investments. Assets and flows by investment discipline are as follows (in billions):

| |

Years ended December 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2009 | 2008 | 2007 | ||||||||

Growth/Blend |

|||||||||||

Beginning of period assets |

$ | 49.5 | $ | 83.4 | $ | 64.4 | |||||

Sales |

12.1 | 24.2 | 20.9 | ||||||||

Redemptions |

12.4 | 21.4 | 15.9 | ||||||||

Net sales (redemptions) |

(0.3 | ) | 2.8 | 5.0 | |||||||

Market / fund performance |

19.4 | (36.7 | ) | 14.0 | |||||||

End of period assets |

$ | 68.6 | $ | 49.5 | $ | 83.4 | |||||

Global/International |

|||||||||||

Beginning of period assets |

$ | 10.9 | $ | 24.9 | $ | 18.4 | |||||

Sales |

4.3 | 3.4 | 7.4 | ||||||||

Redemptions |

2.6 | 5.8 | 5.0 | ||||||||

Net sales (redemptions) |

1.7 | (2.4 | ) | 2.4 | |||||||

Market / fund performance |

6.8 | (11.6 | ) | 4.1 | |||||||

End of period assets |

$ | 19.4 | $ | 10.9 | $ | 24.9 | |||||

Mathematical |

|||||||||||

Beginning of period assets |

$ | 42.4 | $ | 69.7 | $ | 62.3 | |||||

Sales |

5.8 | 12.3 | 15.5 | ||||||||

Redemptions |

11.4 | 14.0 | 13.2 | ||||||||

Net sales (redemptions) |

(5.6 | ) | (1.7 | ) | 2.3 | ||||||

Market / fund performance |

11.2 | (25.6 | ) | 5.1 | |||||||

End of period assets |

$ | 48.0 | $ | 42.4 | $ | 69.7 | |||||

Fixed Income |

|||||||||||

Beginning of period assets |

$ | 3.2 | $ | 4.9 | $ | 4.6 | |||||

Sales |

4.5 | 1.5 | 1.9 | ||||||||

Redemptions |

1.7 | 3.1 | 1.8 | ||||||||

Net sales (redemptions) |

2.8 | (1.6 | ) | 0.1 | |||||||

Market / fund performance |

0.8 | (0.1 | ) | 0.2 | |||||||

End of period assets |

$ | 6.8 | $ | 3.2 | $ | 4.9 | |||||

Alternatives |

|||||||||||

Beginning of period assets |

$ | 0.5 | $ | 0.8 | $ | 0.3 | |||||

Sales |

0.1 | 0.8 | 0.5 | ||||||||

Redemptions |

0.4 | 0.8 | — | ||||||||

Net sales (redemptions) |

(0.3 | ) | — | 0.5 | |||||||

Market / fund performance |

0.1 | (0.3 | ) | — | |||||||

End of period assets |

$ | 0.3 | $ | 0.5 | $ | 0.8 | |||||

Value |

|||||||||||

Beginning of period assets |

$ | 9.1 | $ | 10.1 | $ | 10.2 | |||||

Sales |

6.6 | 6.3 | 2.9 | ||||||||

Redemptions |

4.0 | 4.0 | 3.6 | ||||||||

Net sales (redemptions) |

2.6 | 2.3 | (0.7 | ) | |||||||

19

| |

Years ended December 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2009 | 2008 | 2007 | ||||||||

Market / fund performance |

3.2 | (3.3 | ) | 0.6 | |||||||

End of period assets |

$ | 14.9 | $ | 9.1 | $ | 10.1 | |||||

Money Market |

|||||||||||

Beginning of period assets |

$ | 7.9 | $ | 12.9 | $ | 7.7 | |||||

Sales |

3.6 | 91.7 | 116.5 | ||||||||

Redemptions |

9.8 | 96.7 | 111.3 | ||||||||

Net sales (redemptions) |

(6.2 | ) | (5.0 | ) | 5.2 | ||||||

Market / fund performance |

— | — | — | ||||||||

End of period assets |

$ | 1.7 | $ | 7.9 | $ | 12.9 | |||||

Revenues

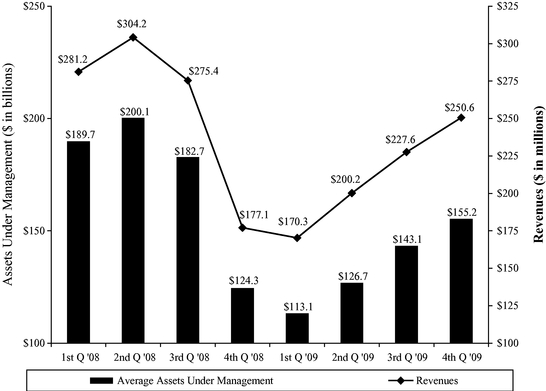

Revenues are generally based upon a percentage of the market value of assets under management and are calculated as a percentage of the daily average asset balance in accordance with contractual agreements with the Company's investment products or clients. Certain investment products are also subject to performance fees which vary based on a product's relative performance as compared to an established benchmark index over a specified period of time and the level of assets subject to such fees. Assets under management primarily consist of domestic and international equity and debt securities. Accordingly, fluctuations in domestic and international financial markets, relative investment performance, sales and redemptions of investment products, and changes in the composition of assets under management are all factors that have a direct effect on JCG's operating results. The following graph depicts the direct relationship between average assets under management and investment management revenues:

20

Results of Operations

JCG's results of operations for the year ended December 31, 2009, include an impairment charge on intangible assets and goodwill of $856.7 million, which is included in operating expenses. The following table summarizes JCG's results of operations (in millions):

| |

Year Ended December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2009 | 2008 | 2007 | |||||||

| |

(dollars in millions, except per share data) |

|||||||||

Continuing Operations |

||||||||||

Revenues |

$ | 848.7 | $ | 1,037.9 | $ | 1,117.0 | ||||

Operating Expenses |

1,526.2 | 704.8 | 767.7 | |||||||

Non-operating Expenses |

79.6 | 194.7 | 157.3 | |||||||

Net income (loss) |

$ | (757.1 | ) | $ | 138.4 | $ | 192.0 | |||

Operating Margin |

-79.8 | % | 32.1 | % | 31.3 | % | ||||

Basic Earnings (Loss) Per Share |

$ | (4.55 | ) | $ | 0.87 | $ | 1.09 | |||

Diluted Earnings (Loss) Per Share |

$ | (4.55 | ) | $ | 0.86 | $ | 1.07 | |||

2009 Compared to 2008

Investment management fees decreased $142.7 million, or 17.3%, primarily as a result of the 22.8% decrease in average assets under management. Revenue declined at a lower rate than average assets under management as a result of the impact of the consolidation of Perkins beginning January 1, 2009, and a decrease in lower yielding money market assets. The equity method of accounting was used for Perkins prior to December 31, 2008, as JCG had significant influence but did not have the ability to exercise control. The decline in money market assets reflects JCG's previously announced plan to exit its institutional money market business by April 30, 2009.

Performance fee revenue is derived from certain mutual funds and separate accounts. The increase in performance fee revenue of $1.3 million, or 4.7%, was primarily due to a $5.3 million increase in fees earned on mutual funds from improved performance. The increase was partially offset by a decline of $3.8 million on INTECH private accounts as a result of investment underperformance. Pending mutual fund shareholder approval in 2010, additional mutual funds representing $42.0 billion, or approximately 26% of assets under management as of December 31, 2009, will become subject to performance fees. If approved, these mutual funds will become subject to performance fees over the next three years, with the first fee recognized in 2011.

Shareowner servicing fees and other revenue decreased $47.8 million, or 26.0%, over the prior year primarily from lower transfer agent fees and money market administration fees. Transfer agent fees are based on average assets under management distributed directly to investors by Janus, excluding money market assets, which decreased 22.0% over the prior year. Money market administration fees declined as a result of lower money market assets due to exiting the institutional money market business in early 2009.

Employee compensation and benefits decreased $21.3 million, or 6.7%, principally due to lower incentive compensation, base salaries and commissions, partially offset by the consolidation of Perkins. Investment team compensation decreased $11.3 million primarily as a result of lower revenue. The investment team compensation plan is linked to individual long-term investment performance, but also ties the aggregate level of compensation to revenue. Base salaries declined $4.9 million primarily as a result of the workforce reduction in the fourth quarter 2008. Commission expense decreased $4.7 million, reflecting lower sales volumes across all channels.

21

Long-term incentive compensation increased $17.5 million, or 40.2%, primarily from new awards granted in 2009 and the $5.3 million departure-related acceleration of the former Chief Executive Officer's awards, partially offset by the accelerated vesting of awards granted in prior years.

Long-term incentive grants made during 2009 totaled $73.3 million and will be recognized ratably over a four-year period and are not subject to performance-based accelerated vesting. In addition to these awards, Perkins granted $5.0 million of interests that vest ratably over four years, and INTECH granted $5.5 million of interests which generally vest over 10 years. Future long-term incentive amortization will also be impacted by the 2010 annual grant totaling $68.9 million, which will be recognized ratably over a four-year period and is not subject to performance-based accelerated vesting. In addition, JCG granted a $10.0 million restricted stock award to the new Chief Executive Officer on February 5, 2010. This award is not subject to performance-based accelerated vesting and will vest 50% in the first year and 25% in each of the second and third years. Long-term incentive compensation in 2010 may include approximately $5 million to $10 million of expense related to Perkins senior profit interest awards. These awards have a formula-driven terminal value based on revenue growth and relative investment performance of products managed by Perkins.

Marketing and advertising declined $5.3 million, or 16.0%, primarily from cost-reduction measures implemented in the fourth quarter 2008, partially offset by costs associated with JCG's merging of its two domestic mutual fund trusts effective July 6, 2009. Marketing expense in the first half of 2010 will include approximately $10 million of fund proxy costs for the election of the mutual fund trustees in JCG's domestic mutual funds. Janus is required by the SEC to pay for such election every five years.

Distribution expenses decreased $27.3 million, or 20.2%, as a result of a similar decrease in assets under management subject to third-party concessions. Distribution fees are calculated based on a contractual percentage of the market value of assets under management distributed through third-party intermediaries.

Depreciation and amortization expense decreased $4.3 million, or 10.7%, primarily as a result of lower amortization of deferred commissions from a decline in sales of certain mutual fund shares.

General, administrative and occupancy expense increased $5.4 million, or 4.0%, primarily from litigation settlements and an unfavorable judgment totaling $31.4 million, partially offset by the impact of cost-reduction measures implemented in the fourth quarter 2008.

Goodwill and intangible asset impairment charges of $747.0 million and $109.7 million, respectively, were recognized as of March 31, 2009. JCG revised its operating forecast downward as a result of continued deterioration in global market conditions, assets under management and revenues during the first quarter 2009. These conditions, combined with JCG's net book value exceeding its market capitalization, caused management to assess goodwill and intangible assets for impairment as of March 31, 2009. Based on these assessments, JCG partially impaired goodwill and mutual fund advisory contracts associated with the 2001 contractual obligation to buy out Janus' founder. The goodwill impairment charge is not deductible for income tax purposes. A tax benefit of $40.6 million was recognized as a result of the impairment of mutual fund advisory contracts.

JCG recognized a $5.8 million net gain on early extinguishment of debt as a result of the retirement of $443.3 million of outstanding debt in August 2009. The extinguishment of debt, offset by the convertible senior notes issuance of $170.0 million, is expected to result in lower annualized interest expense of approximately $16 million.

Net investment losses totaling $5.6 million include other-than-temporary impairment charges of $5.2 million on available-for-sale securities for the year ended December 31, 2009. Mark-to-market gains on trading securities for 2009 were largely offset by losses generated by a hedging strategy implemented in late 2008, covering the majority of seed capital, to mitigate a portion of the earnings volatility created by the mark-to-market accounting of seed capital investments. In December 2007,

22

JCG purchased securities originally issued by Stanfield Victoria Funding LLC ("Stanfield") from certain Money Funds in response to Moody's downgrading these securities to a rating below what is generally permitted to be held by the Money Funds. Net investment losses totaled $60.4 million in 2008 and include a $21.0 million impairment charge on the Stanfield securities and $41.1 million of mark-to-market losses on consolidated investment products, net of $1.7 million of realized gains.

During September 2009, Stanfield was restructured whereby security holders were given the option to participate in a new structure, receive their proportionate share of each investment position underlying Stanfield or auction their position. JCG, along with a majority of Stanfield security holders, elected to participate in the new structure under which each participating security holder's proportionate share of positions underlying Stanfield were transferred to VFNC Trust ("VFNC") and their Stanfield security interests were exchanged for VFNC security interests. The restructuring has not impacted the valuation of the securities.

Other income, net, decreased $8.7 million, or 90.6%, from a decline in interest and dividend income earned on corporate cash and investments.

Noncontrolling interest increased $4.4 million, or 51.2%, primarily from the consolidation of Perkins' noncontrolling interest beginning January 1, 2009, and $1.1 million of gains associated with the noncontrolling interest in consolidated investment products. This increase was partially offset by a decline in INTECH earnings associated with lower performance fees earned on separate accounts and lower average assets under management in the relevant investment products.

JCG's statutory tax rate decreased by approximately 1.25% effective January 1, 2009, as a result of a legislative change in Colorado state taxes enacted during the second quarter 2008. JCG's effective tax rate differs from the statutory tax rate primarily due to the goodwill impairment charge in the first quarter 2009 not being tax-deductible.

2008 Compared to 2007

Investment management fees decreased $71.2 million, or 7.9%, as a result of a decrease in average assets under management driven primarily by declining markets.

The increase in performance fee revenue of $8.1 million, or 41.5%, was principally due to one separate account reaching its one-year anniversary during the second quarter 2008 on which the first contractual performance fee was recognized for the previous 12 months.

Shareowner servicing fees and other revenue decreased $16.0 million, or 8.0%, over the prior year primarily from a decrease in transfer agent fees. Transfer agent fees are based on average assets under management distributed directly to investors by Janus, excluding money market assets, which decreased at a comparable rate.

Employee compensation and benefits decreased $42.8 million, or 11.9%, principally due to lower incentive compensation partially offset by $8.0 million in severance incurred primarily as a result of the 9% workforce reduction in October 2008. Investment team compensation decreased $33.7 million as a result of lower revenue and a decline in short-term relative investment performance. Commission expense decreased $9.9 million due to lower sales volume, and the companywide bonus accrual declined $16.7 million as a result of the impact of adverse market conditions on the Company's operating results.

Long-term incentive compensation decreased $36.4 million, or 45.6%, primarily as a result of the performance-based acceleration and contractual acceleration of awards in 2007, and a $2.9 million net benefit from revising JCG's forfeiture estimate in the fourth quarter 2008 due to higher than projected employee departures. Long-term incentive compensation in 2007 also included a $17.0 million charge for the contractual acceleration of awards related to certain portfolio managers who resigned.

23

Distribution expenses decreased $6.8 million, or 4.8%, as a result of a similar decrease in assets under management subject to third-party concessions.

Interest expense increased $16.7 million, or 28.4%, from the issuance of additional debt in June 2007.

Net investment losses totaled $60.4 million in 2008 and include a $21.0 million impairment charge on the Stanfield securities and $41.1 million of mark-to-market losses on consolidated investment products, net of $1.7 million of realized gains. Net investment gains of $4.7 million in 2007 include $17.6 million of income previously recorded as unrealized gains in equity partially offset by an $18.2 million impairment charge on the Stanfield securities.

The decrease in noncontrolling interest is largely the result of a decline in INTECH earnings associated with lower average assets under management in the relevant investment products and approximately $4.0 million of losses associated with the noncontrolling interest in consolidated investment products.

JCG's tax rate decreased effective January 1, 2009, as a result of a legislative change in Colorado state taxes enacted during the second quarter 2008. The income tax provision for 2008 includes a $12.9 million tax benefit as a result of applying the lower tax rate to deferred tax assets and liabilities expected to be realized or settled on or after January 1, 2009.

DISCONTINUED OPERATIONS

During the second quarter 2008, JCG disposed of its Printing and Fulfillment operations for $14.5 million.

LIQUIDITY AND CAPITAL RESOURCES

Cash Flows

A summary of cash flow data from continuing operations for the years ended December 31 is as follows (in millions):

| |

2009 | 2008 | 2007 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

Cash flows provided by (used for): |

|||||||||||

Operating activities |

$ | 176.5 | $ | 238.2 | $ | 290.8 | |||||

Investing activities |

(9.6 | ) | (148.8 | ) | (103.3 | ) | |||||

Financing activities |

(124.8 | ) | (287.5 | ) | (213.9 | ) | |||||

Net increase (decrease) in cash and cash equivalents |

42.1 | (198.1 | ) | (26.4 | ) | ||||||

Balance at beginning of year |

282.6 | 480.7 | 507.1 | ||||||||

Balance at end of year |