Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-34088

Brink’s Home Security Holdings, Inc.

(Exact name of registrant as specified in its charter)

| Virginia | 80-0188977 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

8880 Esters Boulevard, Irving, TX 75063

(Address of principal executive offices) (Zip Code)

(972) 871-3500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, no par value | New York Stock Exchange |

Securities registered pursuant to section 12(g) of the Act: None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | x | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of June 30, 2009, the aggregate market value of the voting and non-voting common equity held by non-affiliates was $1,292,671,261. For purposes of this calculation, the registrant has assumed that stockholders that are not officers or directors of the registrant are not affiliates of the registrant.

As of February 23, 2010, there were issued and outstanding 45,872,480 shares of common stock.

Documents incorporated by reference: Part III incorporates information by reference from portions of the Registrant’s definitive 2010 Proxy Statement.

Table of Contents

BRINK’S HOME SECURITY HOLDINGS, INC.

FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2009

TABLE OF CONTENTS

Table of Contents

PART I

| ITEM 1. | BUSINESS |

Overview

Brink’s Home Security Holdings, Inc., which was incorporated in Virginia in 2008, is a full service provider of residential and business security systems. We conduct business in one operating segment primarily through our operating subsidiary, Broadview Security, Inc. (“Broadview Security”), which markets, installs, services, and monitors security alarm systems throughout North America. We serve approximately 1.4 million customers in the United States and two Canadian provinces. We have developed a reputation for reliability and superior service by making high quality and affordable monitored alarm systems widely available to homeowners and businesses. We believe we are the second largest provider of security alarm monitoring services for residential and commercial properties in North America.

As used in this Report, (a) references to “Holdings,” “Company,” “we,” “us” and “our” refer to Brink’s Home Security Holdings, Inc. and its consolidated subsidiaries, including Broadview Security, after the spin-off transaction described below, and (b) references to the “Company” on a historical basis, prior to the spin-off, refer to Brink’s Home Security, Inc. and its consolidated subsidiaries, in each case unless the context requires otherwise.

Recent Developments

On January 18, 2010, we announced that we signed a definitive agreement and plan of merger (“Merger Agreement”) to be merged into a wholly-owned subsidiary of Tyco International Ltd (“Tyco”) in a transaction valued at approximately $2.0 billion (the “Merger”). Under the terms of the Merger Agreement, for each share of our common stock outstanding, our shareholders will generally have the right to receive, at the election of the shareholder, (a) 42.50 in cash (subject to proration to reflect an overall cap on the amount of cash to be paid by Tyco), (b) a combination of $12.75 in cash and a fraction of a Tyco share equal to $29.75 divided by the volume weighted-average price of Tyco’s shares on the New York Stock Exchange (“NYSE”) during the 10-trading day period ending on the fourth full day prior to the closing date, subject to collar between $32.97 and $40.29, or (c) Tyco shares equal to $42.50 divided by the volume weighted-average price detailed in (b) above, subject to the same collar. The Merger is subject to customary closing conditions, various regulatory approvals and approval of our shareholders. We currently expect the Merger to close in the second or third quarter of calendar year 2010. Upon closing of the Merger, we anticipate that Broadview Security will be combined with Tyco’s ADT security business under the ADT brand.

History of Our Business

Broadview Security, formerly Brink’s Home Security, Inc., was incorporated in Delaware in 1983 as a wholly owned subsidiary of The Brink’s Company (“BCO”) to address the growing home security market. Broadview Security became a wholly-owned subsidiary of Holdings upon completion of the spin-off transaction described below.

On September 12, 2008, the Board of Directors of BCO approved the separation of BCO into two independent, publicly traded companies through the distribution of 100% of the common stock of Brink’s Home Security, a wholly-owned subsidiary of BCO, to shareholders of BCO (the “Spin-off”). To effect the Spin-off, BCO transferred all outstanding shares of Brink’s Home Security to Holdings, another wholly owned subsidiary of BCO, through a series of transactions pursuant to a Separation and Distribution Agreement between BCO and Holdings. On October 31, 2008, BCO distributed all of the shares of Holdings to the stockholders of BCO at a ratio of one share of Holdings common stock for each share of BCO common stock held by each such holder as of the record date of October 21, 2008. On November 3, 2008, after completion of the Spin-off, we began trading “regular way” as an independent public company on the NYSE under the symbol “CFL”, reflecting our corporate mission of creating “Customers For Life.”

In connection with the Spin-off, we entered into a Brand Licensing Agreement with a subsidiary of BCO. Under the agreement, we are entitled to use certain BCO trademarks for no more than three years from the Spin-off date. We announced Broadview Security as our new brand name on June 30, 2009 and have begun the process to transition away from our heritage name. The change was a name change only. The corporate structure and management of the Company remain the same. We began marketing efforts in July 2009 to promote brand awareness through advertisements via television media, internet, direct mail, yellow pages, and messaging to our existing subscriber base (the “Brand Introduction”). The Brand Introduction also includes costs to create the new brand, convert building signage, re-decal our vehicle fleet, issue new technician uniforms, change customer yard signs, and other similar brand conversion activities. We monitor the awareness, perception, and acceptance of the Broadview Security brand name periodically to guide us on the method, extent, and duration of the Brand Introduction and to determine if we will cease to use our heritage brand name prior to the termination of the Brand Licensing Agreement with BCO on October 31, 2011. Future spending on the Brand Introduction and use of our heritage name is contingent on the outcome of the Merger.

3

Table of Contents

Business Fundamentals

We serve a geographically diverse customer base of approximately 1.4 million subscribers located throughout the United States and Western Canada. Our primary customers are residents of single-family homes, which comprise more than 93% of our subscriber base. The majority of new customers are generated organically through our internal sales force, while the remainder is acquired through our authorized dealer program and, to a lesser extent, through partnerships with leading home builders.

We view our business as having two key activities: managing our existing customer base and acquiring new customers. We operate our business with the goal of retaining customers for long periods of time to recoup the initial investment in new subscribers, achieving cash flow break-even in approximately four years. Management of the existing subscriber base is focused on low customer attrition, or customer disconnect rate, which has ranged from 7.0% to 8.2% annually over the past three years.

The predictability of our revenues has enabled us to generate stable cash flow from operations, a substantial portion of which is reinvested each year, at our discretion, to grow the subscriber base. Our ending subscriber base grew 4.4% in 2009, as compared to 6.3% growth in 2008. Growing the subscriber base requires significant upfront cash investment, consisting primarily of direct materials and labor to install the security systems, direct sales costs, indirect sales costs, marketing costs, and administrative costs related to installation activities. For the last few years, our average total upfront cash outlay for a new customer security system installed by one of our field offices, including amounts expensed and capitalized, has ranged from approximately $1,350 to $1,700. This amount does not take into account upfront installation fees collected from customers, which, on average, have ranged from $250 to $340. Including these payments, our net cash cost per new installation in recent periods has ranged from $1,100 to $1,360. The economics of our installation business varies slightly depending on the customer acquisition channel.

On average, each of our existing subscribers pays us approximately $33 per month in recurring cash revenue. The average recurring cash revenue per customer has grown consistently each year as new customers acquired have higher average cash revenue rates. In 2009, the average cash revenue per customer grew 4.5%. We use the cash margin generated on that revenue to offset the initial investment made in new subscribers. Our focus on keeping customer disconnect rates low is fundamental to the success of our economic model.

We are subject to a certain level of seasonality in our operations. Since more household moves take place during the second and third quarters of each year, our disconnect rate and related non-cash expenses are typically higher in those quarters than in the first and fourth quarters. There is a slight seasonal effect on our new customer installation volume and related cash expenses incurred in investment in new subscribers; however, other factors, such as the level of marketing expense, can offset that effect of seasonality.

See Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 14 – Geographic Information, for more information regarding monthly recurring revenue, subscriber growth, disconnect rates, adjusted EBITDA from recurring services, adjusted cash invested in new subscribers, and financial information about geographic areas over the past three years.

Marketing and Sales

To grow the subscriber base and to create brand awareness, we market our security systems through national television advertisements, internet advertising, yellow pages, direct mail, alliances with other consumer-based companies, inbound telemarketing, and sales specialists in both Company field offices and our dealer network. Our “direct response” marketing efforts are designed to generate and direct telephone calls and internet traffic into our centralized inbound telemarketing sales group. In addition, on a localized basis, we participate in many different types of local events to promote our services to prospective customers, including home shows, family expos, retail events, and various industry trade shows and meetings. Our marketing efforts primarily focus on credit worthy homeowners that are desirous of security monitoring services.

4

Table of Contents

Sales are generally closed over the telephone by the centralized sales group or by field sales personnel during on-site consultations with prospective customers. Our reliance on strict standards for our internal sales force and our dealers enables us to better control the sales process from inception to installation and manage the quality of customer service over the life of the contract. Other sales distribution channels include:

| • | our field sales force, which self-generates additional sales from prospective residential and commercial customers; |

| • | our authorized dealer network, which cost-effectively extends our reach into new geographic areas by aligning with select independent security installers; strategic alliances with other service companies, including home inspection firms, which target new home owners early in the home buying process; |

| • | our new housing construction customer acquisition (“Builder”) division. Builder, which partners with large national and regional homebuilders to install home security systems, home networking, communications, and home theater and entertainment systems, directly for the owners of new homes and homes under construction; |

| • | and our national account team, which generates sales from commercial clients with multiple locations. |

Although our business is concentrated in residential security, we also market and sell security systems and monitoring services to the commercial market. We believe that expansion of our commercial customer base is a significant growth opportunity for us. Commercial security customers represented approximately 5% of our total customer base as of December 31, 2009. Although we have recently focused on developing the commercial mid-market, historically our commercial business has consisted of primarily small business clients. We are continuing to develop additional capabilities and geographic reach in commercial security to expand beyond small business into more sophisticated, complex installations and services. During 2009, commercial installation volume, representing approximately 7% of total new customer installations, decreased by 10% from prior year due to the economic downturn.

Services and Products

Monitoring services are generally governed by our standard Protective Service Agreement. Under this agreement, the customer pays the initial installation fee and is then obligated to make monthly payments for the remainder of the initial contract term. The standard term for our Protective Service Agreement is three years, which automatically renews for additional one year periods unless cancelled by either party, except in six states where state law requires the renewal period to be month-to-month. If a customer cancels the contract prior to the end of the initial or roll-over contract term or is otherwise in default, we have the right under the contract to receive from the customer an amount equal to all remaining monthly payments.

Monitoring services are generally billed monthly in advance. Approximately 47% of our subscribers pay us through automated payment methods. We periodically adjust the standard monthly monitoring rate charged to new subscribers. From time to time, we also may adjust the monthly rates of our existing subscribers who have completed their initial contract terms.

In addition to monitoring service, we provide technical service to our subscriber base for routine maintenance and installation of additional equipment. More than half of the subscriber base is enrolled in a service plan which generates incremental recurring monthly revenues. Service contracts comprise the majority of service revenue, with on-call service fees constituting the balance of service revenue.

Generally, we retain ownership of the security equipment used in our monitoring services. However, certain products, installed primarily through our Builder and commercial distribution channels, may be sold directly to the customer. These products include video surveillance equipment, access control, commercial fire alarm systems, wiring for home communications networks, home theater systems, intercom, multi-room sound systems and some security systems.

We select, install and service high quality security products. Our customized control panel is manufactured by a third party to our rigorous specifications. This enhanced control panel and its family of related peripheral components are capable of supporting the vast majority of residential applications and a significant number of commercial applications. We offer a wide variety of high quality detection sensors which communicate with our control panel. These include motion detectors, glass break detectors, perimeter door and window sensors, and smoke and carbon monoxide detectors.

The majority of our subscribers use standard land-line telephone service as the primary communication method for alarm signals from their sites. However, the capability to provide alternative communication methods from a subscriber’s control panel to our central monitoring stations has become increasingly important. We currently offer a variety of alternate alarm communication methods including cellular, digital radio and broadband internet.

5

Table of Contents

Field Operations

We operate 67 field offices located throughout the United States and Western Canada, from which locations we provide services for pre-defined ZIP code-based territories including sales calls, security system installations, and field service and repair. Our technical staff of approximately 1,100 technicians provides installation and service support from our field office locations. We have approximately 500 field sales consultants, each of whom completes comprehensive centralized training prior to conducting customer sales presentations. We staff our field offices to efficiently and effectively make sales calls, install security systems, and provide service support based on near-term activity forecasts for each market.

Dealer Network

To expand our geographic coverage and leverage our national advertising, we have an extensive dealer network, which consists of approximately 248 authorized dealers operating in over 40 states. In 2009, our dealer network accounted for 27% of new customer installations and 14% of the total subscriber base. We purchase newly installed security systems and related monitoring contracts from our dealers. We conduct thorough due diligence on each dealer to ensure reliability and consistent high quality installations. Authorized dealers are generally required to adhere to the same high quality standards for both installation and service support as Company-owned field offices. Subscribers secured by our dealers are geographically diverse and are primarily single-family homeowners.

We provide dealers with a full range of services designed to assist them in all aspects of their business including sales opportunities, sales and technician training, detailed weekly account summaries, sales support materials, and discounts on security system hardware and installation supplies purchased through our third-party distributor.

Typically, we have a right of first refusal to purchase sites and related customer relationships sold by authorized dealers, but are not obligated to acquire these sites. Subscriber contracts typically have an initial term of three years and automatically renew on an annual basis. If a contract is canceled during an initial guarantee period, generally 12 to 18 months, the dealer is required to reactivate the site and contract, or refund the purchase price. To help ensure the dealers’ obligations, we typically withhold a portion of the purchase price for each site.

Monitoring Facilities and Services

We have two monitoring facilities located in Irving, Texas and Knoxville, Tennessee. We employ approximately 700 customer care and monitoring professionals who have completed extensive initial training and continue to receive ongoing training. Both facilities hold Underwriters’ Laboratories (“UL”) listings as protective signaling services stations. UL specifications for monitoring centers cover building integrity, back-up computer and power systems, staffing, and standard operating procedures. Many jurisdictions have laws requiring that security alarms for certain buildings be monitored by UL-listed facilities. In addition, a UL listing is required by insurers of certain commercial customers as a condition of coverage. In the event of an emergency at one of our two monitoring facilities (e.g., fire, tornado, major interruption in telephone or computer service, or any other event affecting the functionality of the facility), all monitoring operations can be automatically transferred to the other facility. Additionally, many non-operator employees at each facility are cross-trained as operators, should there be a short-term or emergency need for additional monitoring operators.

Both of our monitoring facilities operate 24 hours a day on a year-round basis. Incoming alarm signals are routed via an internal communications network to the next available operator in either facility. Operators are quickly updated with information including the name and location of the customer and site, and the nature of the alarm signal. Depending upon the type of service specified by the customer contract, operators respond to emergency-related alarms by calling the customer by telephone (for verification purposes) and relaying information to local fire or police departments, as necessary. Additional action may be taken by the operators as needed, depending on the specific situation.

Customer Care

We maintain a service culture aimed at creating “Customers for Life,” the basis for our stock market ticker “CFL,” because developing customer loyalty and retention are critical to our long-term success. We take a disciplined approach to selecting the right customers and providing high quality customer service. The customer selection process focuses on evaluating the customer’s ability to honor the standard three-year contract through pre-sale credit evaluation. To maintain our high standard of customer service, we provide high quality training to call center employees, field employees, and dealer personnel. We also continually measure and monitor key operating and financial metrics. We have received awards for our monitoring and customer service, including six consecutive years of recognition by J.D. Power and Associates for delivering “An Outstanding Customer Service Experience” for call center operations and customer satisfaction excellence.

6

Table of Contents

Our employees are trained to provide high quality service through prompt handling of calls and quick resolution of most subscriber issues. We use a customized information system that quickly and accurately provides our customer care specialists with technical and administrative information regarding customers and their security systems, including detailed account and site history. This system enables our personnel to resolve most customer issues with a single contact. Our emphasis on customer service results in fewer false alarms, more satisfied customers, and better customer retention rates. Customer care specialists answer non-emergency telephone calls regarding service, billing and alarm activation issues. Our two monitoring centers provide telephone and Internet coverage 24 hours a day on a year-round basis. To ensure that technical service requests are handled promptly and professionally, all requests are routed through our customer contact centers. Customer care specialists help customers resolve minor service and operating issues related to security systems. In many cases, the customer care specialist is able to remotely resolve technical issues by downloading data directly into the alarm panel at the site. When an issue is not correctable from the customer contact center, our specialist can schedule a field technician service appointment during the same telephone call.

Suppliers

We do not manufacture the equipment used in our security systems. Equipment is purchased from a limited number of suppliers and distributors. We maintain minimal inventories of equipment at each field office. Safety stock on certain key items is maintained by third-party distributors to cover minor supply chain disruptions. We do not anticipate any major interruptions in our supply chain.

Industry Trends and Competition

The monitored security industry has historically been growing steadily, with revenue growth at an estimated compounded annual rate of 7% over the 2004-2008 timeframe. We have grown revenue at an average annual rate of 11% over the 2004-2008 timeframe. This time period includes the housing correction that began in 2006. We believe the factors driving this growth include heightened security concerns about crime rates, an aging and wealthier population, an increase in dual income households, an increase in business travel, and changes in personal time away from the home.

The security monitoring industry is highly fragmented, with the top five companies comprising only about 40% of the total market. Remaining competitors include more than 10,000 local and regional companies, the vast majority of which generate annual revenue of less than $500,000. We believe our primary competitors with national scope include:

| • | ADT Security Services, Inc., a wholly owned subsidiary of Tyco International, Ltd. |

| • | Protection One, Inc. |

| • | Monitronics International, Inc. |

| • | Stanley Security Solutions, a part of The Stanley Works |

We generally are recognized as the second largest provider of monitored security services to residential and commercial properties in North America. The North American monitored residential and commercial security industry was estimated to have revenues of approximately $14 billion in 2008. We believe that security industry penetration of U.S. Households is relatively low, estimated to be from 17% to 22%, providing significant opportunity for future growth and increased market share. We believe the differentiating factors contributing to our growth over the past several years are our high quality customers, centralized training to all field personnel and dealer representatives, standardized security systems, and service culture aimed at creating “Customers for Life.” At an estimated $8 billion, the commercial market is larger than the estimated $6 billion residential market, but commercial customers comprise only about 5% of our subscriber base.

Success in the residential and commercial markets depends on a variety of factors including company reputation, market visibility, service quality, product quality, price, and the ability to identify and solicit prospective customers. There is substantial competitive pressure on installation fees and monitoring rates. Several significant competitors offer installation prices that match or are lower than our prices. Other competitors charge significantly more for installation but may charge less for monitoring. We believe that our monitoring and service rates are competitive compared to rates offered by other major security companies.

7

Table of Contents

Employees

As of December 31, 2009, we employed approximately 3,400 people, and we believe our employee relations are good.

Government Regulation and Other Regulatory Matters

Our U.S. operations are subject to various federal, state and local consumer protection laws, licensing laws, and other laws and regulations. Most states have licensing laws that apply specifically to the alarm industry. In certain jurisdictions, we must obtain licenses or permits in order to comply with standards governing employee selection, training and business conduct. Our Canadian operations are subject to the national laws of Canada, and the provincial laws of British Columbia and Alberta.

Our business relies primarily on the use of standard fixed-wireline telephone service to transmit alarm signals. Fixed-wireline telephone companies, the cost of telephone lines, and the type of equipment used in telephone line transmission are regulated by the federal and state governments. The Federal Communications Commission and state public utilities’ commissions regulate the operation and use of wireless telephone and radio frequencies.

Our advertising and sales practices are regulated by the U.S. Federal Trade Commission and state consumer protection laws. In addition, we are subject to certain administrative requirements and laws of the jurisdictions in which we operate. These laws and regulations include restrictions on the manner in which we promote the sale of our security alarm services and require us to provide purchasers of our services with rescission rights.

Some local government authorities have adopted or are considering various measures aimed at reducing false alarms. Such measures include requiring permits for individual alarm systems, revoking such permits following a specified number of false alarms, imposing fines on alarm customers or alarm monitoring companies for false alarms, limiting the number of times police will respond to alarms at a particular location after a specified number of false alarms, and requiring additional verification of an alarm signal before the police respond.

The alarm industry is also subject to requirements imposed by various insurance, approval, and listing and standards organizations. Depending upon the type of customer, security service provided, and requirements of the applicable local governmental jurisdiction, adherence to the requirements and standards of such organizations is mandatory in some instances and voluntary in others.

There can be no assurance that new or revised laws will not impact our business, as change in regulation could have a material and adverse effect on us. New or revised regulations could require us to alter our business practices in a manner that we may deem to be unacceptable which could slow our growth opportunities. The failure to comply with such regulations could result in the imposition of material fines, penalties, or injunctions.

Available Information

We maintain internet websites under the names www.broadviewsecurity.com and www.brinkshomesecurity.com. We make available, free of charge, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports, on our websites as soon as reasonably practicable after providing such reports to the SEC.

We file annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements, and other documents with the Securities and Exchange Commission (“SEC”) under the Securities Exchange Act, as amended. The public may read and copy any materials that we file with the SEC at the SEC’s Public Reference Room at 450 Fifth Street, N.W., Washington DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. Also, the SEC maintains an internet website that contains reports, proxy and information statements, and other information regarding issuers, including Brink’s Home Security Holdings, Inc., that file electronically with the SEC. The public can obtain any document we file with the SEC at www.sec.gov. Information contained on, or connected to, our websites is not incorporated by reference into this Form 10-K and should not be considered part of this report or any other filing that we make with the SEC.

8

Table of Contents

| ITEM 1A. | RISK FACTORS |

We are exposed to risks in the operation of our business. Some of these risks are common to all companies doing business in the industry in which we operate and some are unique to our business. These risk factors should be considered carefully when evaluating our business. The occurrence of one or more of these events could significantly and adversely affect our business, prospects, financial condition, and results of operations or cash flows.

RISKS RELATED TO COMPLETION OF THE MERGER

The pendency of the Merger could materially, adversely affect our future business and operations or result in a loss of our employees or dealers.

In connection with the pending Merger with Tyco, it is possible that some customers, suppliers and other persons with whom we have a business relationship may delay or defer certain business decisions, which could negatively impact our revenues, earnings and cash flows, and the market price of our common stock, regardless of whether the Merger is completed. Similarly, our current and prospective employees or dealers operating in our dealer network may experience uncertainty about their future roles with us following the completion of the Merger, which may materially adversely affect our ability to attract and retain key employees or dealers. In addition, the Merger Agreement restricts our ability to take certain specified actions without the consent of Tyco until the Merger occurs. These restrictions may prevent us from pursuing attractive business opportunities that may arise prior to the completion of the Merger.

The Merger may adversely impact the tax-free status of our spin-off from BCO, which could result in material liabilities to us under the tax matters agreement with BCO.

Although we believe that the Merger will not adversely impact the tax-free status of our spin-off from BCO, it is possible that the Internal Revenue Service (the “IRS”) may assert that the Merger would cause the spin-off to be treated as a taxable transaction for U.S. federal income tax purposes to BCO. If the IRS were to be successful in any such contention, or if for any other reason we were to take actions that would cause the spin-off to be treated as a taxable transaction, under the tax matters agreement entered into between us and BCO at the time of the spin-off, we would be obligated to indemnify BCO as a result of the failure of the tax-free status of the spin-off to be preserved, which would result in material liabilities to us.

If the Merger is not completed, our ongoing business may be adversely affected and we will be subject to several risks and consequences, including the following:

| • | we may be required, under certain circumstances, to pay Tyco a termination fee of either $45.0 million or $87.5 million under the Merger Agreement; |

| • | we will be required to pay certain costs relating to the Merger, whether or not the Merger is completed, such as legal, accounting, financial advisor, and printing fees; |

| • | under the Merger Agreement, we are subject to certain restrictions on the conduct of our business prior to completing the Merger which may adversely affect our ability to execute our business strategies; and |

| • | matters relating to the Merger may require our management team to commit substantial time and resources, which could otherwise have been devoted to other opportunities that may have been beneficial to us. |

In addition, if the Merger is not completed, we may experience negative reactions from the financial markets and from our customers, employees or dealers. We also could be subject to litigation related to any failure to complete the Merger or to enforcement proceedings commenced against us to perform our obligations under the Merger Agreement.

The proposed Merger is subject to the receipt of consents and approvals from government entities that may impose conditions that could have an adverse effect on us or could delay or prevent the completion of the Merger.

Completion of the Merger is conditioned upon, among other things, the expiration or termination of the required waiting period under the Hart-Scott-Rodino Antitrust Improvements Act of 1976. The reviewing authorities may not permit the Merger at all or may impose restrictions or conditions on the completion of the Merger. There is no assurance that we will obtain these necessary governmental approvals to complete the Merger. In addition, any delay in the completion of the Merger from the failure to obtain such approvals could diminish the anticipated benefits of the Merger or result in additional transaction costs, loss of revenue or other effects associated with uncertainty about the proposed Merger.

9

Table of Contents

OTHER RISK FACTORS

We are subject to contractual limitations on the use of certain BCO trademarks which have required us to develop a new brand for our business.

Prior to the Spin-off, we operated as a subsidiary of BCO, and marketed our products and services using BCO’s brand name and logos. In connection with the Spin-off, we entered into a Brand Licensing Agreement with a subsidiary of BCO that grants us the right to use certain trademarks, in the United States, Canada and Puerto Rico in connection with the provision of certain products and services. These rights will extend for a period no longer than three years (that is, until October 31, 2011), subject to certain terms and conditions, after which we will no longer have the right to use BCO’s brand name. In addition, following the expiration of a five-year non-compete agreement between us and BCO on October 31, 2013, BCO will be able to operate a separate alarm monitoring business using their brand name in the United States, Canada and Puerto Rico.

We have incurred and may continue to incur significant expense in connection with building recognition of our new brand.

On June 30, 2009, we announced our new brand name, Broadview Security. In doing so, we have incurred costs associated with developing our new brand and will incur substantial costs in building recognition of our new brand. There is uncertainty regarding the timing, duration and the amount of the total expenses that may be incurred in the brand building effort. These expenses are dependent, among other things, on general economic and strategic marketing decisions that will be made during the transition to the new brand, and are therefore subject to change.

Our new brand may not achieve similar brand recognition as our heritage brand, which could adversely affect our business and profitability.

As we continue to develop the Broadview Security brand name for potential and existing customers, there is some risk that the volume of new installations and the disconnect rate could be negatively impacted. Despite our efforts, we may not be successful in achieving an acceptable level of recognition of our new brand. If we are not successful in achieving recognition for our new brand, our competitive position may be weakened and we may lose market share.

If our Spin-off from BCO were to lose its tax-free status due to actions taken by us, we would be required to indemnify BCO for certain liabilities under our Tax Matters Agreement with BCO.

BCO received a private letter ruling from the IRS to the effect that, among other things, the Spin-off qualified for tax-free treatment under Section 355 of the Internal Revenue Code. The ruling was based upon representations by BCO that necessary conditions had been satisfied, and any inaccuracy in such representations could invalidate the ruling. If the IRS were to determine that the Spin-off does not qualify for tax-free treatment under Section 355 of the Code, then a U.S. holder that received our shares in the Spin-off would be treated as having received a distribution to the extent of the fair market value of the shares received on the Spin-off date. That distribution would be treated as taxable dividend income to the extent of such holder’s ratable share of the current and accumulated earnings and profits of BCO, if any. Any amount that exceeds such share of earnings and profits of BCO would be treated first as a tax-free return of capital to the extent of the U.S. holder’s adjusted tax basis in its shares of common stock of BCO (thus reducing such adjusted tax basis) with any remaining amounts being treated as capital gains.

Generally, taxes resulting from the Spin-off failing to qualify for tax-free treatment for U.S. Federal income tax purposes would be imposed on BCO and BCO’s shareholders. Under the Tax Matters Agreement, however, we would be required to indemnify BCO and its affiliates against all tax-related liabilities caused by such failure to the extent those liabilities arose as a result of an action taken by us or our affiliates or otherwise resulted from any breach of any representation, covenant or obligation of us or our affiliates under the Tax Matters Agreement or any other agreement entered into by us in connection with the Spin-off.

We are contingently responsible for certain of BCO’s contingent and other corporate liabilities.

As a former subsidiary of BCO, we are jointly and severally liable with BCO, and with certain other current and former subsidiaries of BCO, for two kinds of health benefits for employees of BCO former coal operations. First, we and BCO are jointly and severally liable for the ongoing provision of postretirement health benefits. To fund the considerable costs of these benefits, BCO established a Voluntary Employees’ Beneficiary Associate trust (“VEBA”). It is possible that the VEBA may be underfunded, in which case we and BCO could be required to provide additional funding. Second, we are jointly and severally liable to pay certain postretirement health premiums through September 2010. Although we continue to be jointly and severally liable with BCO for these liabilities and expenses, BCO has agreed to indemnify us for any and all costs relating to these liabilities and expenses. However, it is possible that BCO will be unwilling or unable to make these payments in which case we could be required to do so.

10

Table of Contents

As a former subsidiary of BCO, and with certain other current and former subsidiaries of BCO, we have a joint and several liability with BCO to the IRS for the consolidated federal income taxes of the BCO group relating to the taxable periods ending on or prior to the Spin-off. Although we continue to be jointly and severally liable with BCO for this liability under the Tax Matters Agreement, BCO has agreed to indemnify us for amounts relating to this liability to the extent not attributable to our liabilities. However, it is possible that BCO will be unwilling or unable to make these payments in which case we could be required to do so. Under the Tax Matters Agreement, we are required to indemnify BCO and its affiliates for tax liabilities attributable to us and resulting from audit adjustments for taxable periods during which we were a member of the BCO consolidated group.

We are susceptible to downturns in the housing market and consumer discretionary income, which may inhibit our ability to sustain subscriber base growth rates.

Demand for alarm monitoring services is affected by the turnover in the housing market. Downturns in the rate of the sale of new and existing homes, which we believe drives a substantial portion of our new customer volume in any given year, would reduce opportunities to make sales of new security systems and services and reduce opportunities to take over existing security systems. With the extended slowdown in housing sales and the deterioration in the overall consumer environment, our new installation growth rate has progressively slowed during the last three years. We sustained a decline in new customer installations in 2009 as compared to 2008 and 2007. In addition, because of personal economic circumstances, current security alarm customers may decide to disconnect our services in an effort to reduce their monthly spending and may default on their remaining contractual obligations to us. Our long-term revenue growth rate depends on installations exceeding disconnects. If the housing market downturn is prolonged, our revenues and cash flow may be adversely affected. If the general economic downturn is prolonged, this could lead to an increase in customer disconnects and defaults, and may also adversely affect our revenues and cash flow.

Our financial results may be negatively impacted by recent financial events.

Recent financial events have resulted in the consolidation, failure or near failure of a number of institutions in the banking, insurance and investment banking industries and have substantially reduced the ability of companies to obtain financing. These events have also led to a substantial reduction in stock market valuations and job losses, and could have a number of different effects on our business, including:

| • | a reduction in consumer spending, which could result in increased customer disconnects and/or a reduction in new customer additions; |

| • | a negative impact on the ability of our existing customers to timely pay their obligations to us, thus reducing our cash flow; |

| • | an increased likelihood that one or more of our banking institutions may be unable or unwilling to honor its commitments under our revolving credit facility; and |

| • | restricted access to capital markets that may limit our ability to take advantage of business opportunities, such as acquisitions. |

Other events or conditions may arise directly or indirectly from financial events that could negatively impact our business.

We rely on a significant number of our subscribers remaining with us as customers for long periods of time.

We incur significant upfront cash costs for each new subscriber. It requires a substantial amount of time for us to receive cash payments (net of our recurring cash costs) from a particular subscriber that are sufficient to offset this upfront cost, with that period currently averaging approximately four years. Accordingly, our long-term profitability is dependent on our subscribers remaining with us as customers for long periods of time. This requires that we minimize our rate of subscriber disconnects, or attrition. Factors that can increase disconnects include customers who relocate and do not reconnect, problems with our service quality, an economic slowdown and the affordability of our service. If we fail to keep our subscribers for a sufficiently long period of time, our financial position and results of operations could be adversely affected.

Shifts in our customers’ choice of telecommunications services and equipment could adversely impact our business and require significant capital expenditures.

Certain elements of our operating model have historically relied on our customers’ continued selection and use of traditional land-line telecommunications to transmit alarm signals to our monitoring centers. There is a growing trend for customers to switch to the exclusive use of cell-phone, satellite, or internet communication technology in their homes and businesses, and we anticipate telecommunication providers to permanently switch from land-line to broadband communications in the future. The use of communications other than land-line would require customers to upgrade to alternative, and often more expensive, technologies to transmit alarm signals, which generally result in increased recurring revenues for us. This, however, could increase our customer attrition rates, slow down our new subscriber rates, or reduce our ability to attract a sufficient volume of new customers. In the future, we may not be able to successfully implement new technologies or adapt existing technologies to changing market demands. If we are unable to adapt timely to changing technologies, market conditions, or customer preferences, it could adversely affect our business.

11

Table of Contents

We operate in a highly competitive industry.

The monitored security alarm industry is subject to significant competition and pricing pressures. We experience competitive pricing pressures on both installation fees and monitoring rates. Several significant competitors offer installation fees that match or are lower than our prices. Other competitors charge significantly more for installation but, in many cases, less for monitoring. Competitive pressure on monitoring and service fees is significant. We believe that the monitoring and service fees we offer are generally competitive with rates offered by other major security companies. Continued pricing pressure could adversely impact our customer base or pricing structure and have an adverse effect on our results of operations.

We also face potential competition from improvements in self-monitoring systems, which enable customers to monitor their home environment without third-party involvement. Advances in self-monitoring systems could progress to the point where we could be at a competitive disadvantage. Similarly, it is possible that one or more of our competitors could develop a significant technical advantage over us that allows them to provide additional service or better quality service or to lower their price, which could put us at a competitive disadvantage. Either development could adversely affect our growth and results of operations.

We may pursue additional customer acquisition channels and strategic alliances, which may cause operating margins to suffer.

We may expand our presence in the commercial alarm installation and monitoring market. We may also continue to evaluate other business opportunities, including expanding our services, adding customer acquisition channels, and forming new alliances with companies to market our security systems and services. This could result in our cost of investment in new subscribers growing at a faster rate than installations and related recurring revenue. Additionally, any new alliances or customer acquisition channels could have higher cost structures than our current arrangements, which could reduce operating margins and require more working capital. In the event that working capital requirements exceeded operating cash flow, we might be required to draw on our credit facility or pursue other external financing, which may not be readily available.

We rely on third party providers for the components of our security systems and any failure or interruption in products or services provided by these third parties could harm our ability to operate our business.

The components for the security systems that we install are manufactured by third parties. We are therefore susceptible to interruptions in supply and to the receipt of components that do not meet our high standards. Any financial or other difficulties our providers face may have negative effects on our business. We exercise little control over our suppliers, which increases our vulnerability to problems with the products and services they provide. Any interruption in supply could cause delays in installations and repairs and the loss of current and potential customers. Also, if a previously installed component were found to be defective, we might not be able to recover the costs associated with its repair or replacement, and the diversion of technical personnel to address such an issue could affect subscriber, revenue, and profit growth.

An interruption to our monitoring facilities from a disaster could adversely affect our business.

A disruption to our monitoring facilities could disrupt our ability to provide alarm monitoring services and serve our customers which could have a material adverse effect on our business. The disruption could occur for many reasons, including fire, natural disasters, weather, disease, transportation interruption, or terrorism. However, these risks are mitigated through the existence of our two fully redundant monitoring facilities. In the event of an emergency at one of our two monitoring facilities, all monitoring operations can be quickly transferred to the other facility. Additionally, many non-operator employees at each facility are cross-trained as monitoring operators, should there be a short-term or emergency need for additional monitoring operators. Both facilities hold Underwriters’ Laboratories (“UL”) listings as protective signaling services stations and maintain certain standards of building integrity and power backup, among other safeguards.

12

Table of Contents

We are exposed to greater risks of liability for employee acts or omissions, or system failure, than may be inherent in other businesses.

If a subscriber believes that he or she has suffered harm to person or property due to an actual or alleged act or omission of one of our employees or security system failure, he or she may pursue legal action against us, and the cost of defending the legal action and of any judgment could be substantial. Substantially all of our customer contracts contain provisions limiting our liability; however, in the event of litigation with respect to such matters, it is possible that these limitations may be deemed not applicable.

We carry insurance of various types, including general liability and professional liability insurance in amounts we consider adequate and customary for our industry. Some of our insurance policies, and the laws of some states, may limit or prohibit insurance coverage for punitive or certain other types of damages, or liability arising from gross negligence. If we incur increased losses related to employee acts or omissions, or system failure, or if we are unable to obtain adequate insurance coverage at reasonable rates, or if we are unable to receive reimbursements from insurance carriers, our financial condition and results of operations could be adversely affected.

We could be assessed penalties for false alarms.

Some local governments impose assessments, fines, penalties and limitations on either subscribers or the alarm companies for false alarms. A few municipalities have adopted ordinances under which both permit and alarm dispatch fees are charged directly to the alarm companies. Our alarm service contracts generally allow us to pass these charges on to customers. If more local governments were to impose assessments, fines or penalties, our customers might find these additional charges prohibitive and the growth of our subscriber base could be adversely affected. Further, to the extent we are unable to pass assessments, fines and penalties on to our customers, our operating results could be adversely affected.

Police departments could refuse to respond to calls from monitored security service companies.

Police departments in a limited number of U.S. cities do not respond to calls from monitored security service companies, either as a matter of policy or by local ordinance. We have offered affected customers the option of receiving response from private guard companies, in most cases through contracts with us, which increases the overall cost to customers. If more police departments were to refuse to respond or be prohibited from responding to calls from monitored security service companies, our ability to attract and retain subscribers could be negatively impacted and our results of operations and cash flow could be adversely affected.

Our business operates in a regulated industry.

Our operations and employees are subject to various U.S. federal, state and local consumer protection, licensing and other laws and regulations. Most states in which we operate have licensing laws directed specifically toward the monitored security services industry. Our business relies heavily upon wireline telephone service to communicate signals. Wireline telephone companies are currently regulated by both the federal and state governments. Our Canadian operation is subject to the laws of Canada, British Columbia and Alberta.

Changes in laws or regulations could require us to change the way we operate, which could increase costs or otherwise disrupt operations. In addition, failure to comply with any applicable laws or regulations could result in substantial fines or revocation of our operating permits and licenses. If laws and regulations were to change or we failed to comply, our business, financial condition and results of operations could be materially and adversely affected.

FORWARD-LOOKING INFORMATION

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (which Sections were adopted as part of the Private Securities Litigation Reform Act of 1995). Statements preceded by, followed by or that otherwise include the words “believe,” “anticipate,” “estimate,” “expect,” “intend,” “plan,” “project,” “prospects,” “outlook,” and similar words or expressions, or future or conditional verbs such as “will,” “should,” “would,” “may,” and “could” are generally forward-looking in nature and not historical facts. These forward looking statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any anticipated results, performance or achievements. Except as required by law, we disclaim any intention, and undertake no obligation, to revise any forward-looking statements, whether as a result of new information, a future event, or otherwise. These risks, uncertainties and contingencies, many of which are beyond our control, include, but are not limited to risks related to the Merger, risks inherent in the Spin-off from our former parent corporation, the demand for our products and services, the ability to identify and execute further cost and operational improvements and efficiencies in our core business, the actions of competitors, our ability to successfully build and market a new brand, our ability to identify strategic opportunities and integrate them successfully, our ability to maintain subscriber growth, the number of household moves, the level of home sales or new home construction, potential instability in housing credit markets, our ability to cost-effectively develop or incorporate new systems or technology in a timely manner, our ability to balance the cost of acquiring customers with the profit from serving existing customers, our ability to keep disconnect rates relatively low, the availability and cost of capital, and general business conditions.

13

Table of Contents

Certain of these factors and other factors, risk and uncertainties are discussed in Part I, Item 1A of this Annual Report on Form 10-K. Other unknown or unpredictable factors may also cause actual results to differ materially from those projected by the forward looking statements. Most of these factors are difficult to anticipate and may be beyond our control. You should consider the areas of risk described above, and also consider those set forth in Part I, Item 1A of this Annual Report on Form 10-K, in connection with considering any forward looking statements that may be made by us in this report.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

None.

| ITEM 2. | PROPERTIES |

We have 74 leased field offices and other facilities located throughout the U.S. and one leased office in British Columbia, Canada. Our headquarters are located in Irving, Texas in a facility we own. This owned facility houses some of our administrative and technical support personnel. Additional personnel are located in portions of three nearby buildings in office spaces that are leased. Our headquarters also serve as one of our two central monitoring facilities. The second monitoring and service center, which we also own, is located near Knoxville, Tennessee.

The following table discloses our leased and owned facilities as of December 31, 2009.

| Facilities | ||||||

| Region |

Leased | Owned | Total | |||

| U. S. |

73 | 2 | 75 | |||

| Canada |

1 | — | 1 | |||

| Total |

74 | 2 | 76 | |||

| ITEM 3. | LEGAL PROCEEDINGS |

The Company is involved in various lawsuits and claims in the ordinary course of business. The Company has recorded accruals for losses that are considered probable and reasonably estimable associated with these matters. The Company believes that the ultimate disposition of these matters will not have a material adverse effect on its liquidity or financial position; however, losses from these matters or changes in estimates of losses for these matters may result in income or expense in any one accounting period that is material in comparison to the earnings of that period.

In April 2009, a Michigan state circuit court jury rendered a verdict against the Company for $4.2 million pertaining to claims made by a terminated employee of the Company. On July 7, 2009, the trial court entered judgment in favor of the plaintiff for $4.7 million. This amount included approximately $0.5 million in pre-judgment interest and attorney fees. After post-trial proceedings, on September 25, 2009, the trial court entered a revised judgment in the amount of approximately $3.5 million. The amount of the revised judgment has been included in other accrued liabilities as of December 31, 2009. On October 16, 2009, the Company filed an appeal seeking reversal of the judgment or in the alternative a new trial, based on various alleged points of error by the trial court. In connection with the appeal, the trial court ordered a stay of execution on the judgment which requires the Company to post an appeal bond. The Company has filed its initial appeal brief but no date has yet been set for oral argument.

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS |

None.

14

Table of Contents

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED SHAREHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information and Holders

Our common stock began trading “regular way” on the New York Stock Exchange under the symbol “CFL” on November 3, 2008. As of February 23, 2010, there were approximately 2003 holders of record of our common stock.

The table below sets forth for each of the quarters indicated the reported high and low sales prices for our common stock on the New York Stock Exchange for the period from November 3, 2008 through December 31, 2009.

| High | Low | |||||

| 2008: |

||||||

| Fourth Quarter (Beginning November 3, 2008) |

$ | 23.10 | $ | 13.15 | ||

| 2009: |

||||||

| First Quarter |

$ | 25.36 | $ | 19.27 | ||

| Second Quarter |

31.30 | 21.79 | ||||

| Third Quarter |

32.42 | 26.51 | ||||

| Fourth Quarter |

34.11 | 29.89 | ||||

Dividend Policy

We have not paid any cash dividends on our common stock since the Spin-off. Any change in our dividend policy will be made at the discretion of our Board of Directors and will depend on a number of factors, including future earnings, capital requirements, contractual restrictions, financial condition, future prospects and any other factors our Board of Directors may deem relevant.

The payment of cash dividends are subject to the restrictions and limitations in the credit agreement governing our unsecured revolving credit facility. In addition, the Merger Agreement restricts our ability to pay dividends to holders of our common stock without Tyco’s consent.

Equity Compensation Plan Information

The following table sets forth information about our common stock that may be issued upon the exercise of options, warrants and rights under all of our existing equity compensation plans as of December 31, 2009.

| Plan Category |

Number of Securities to be Issued upon Exercise of Outstanding Options, RSU’s, DSU’s, and Deferred Compensation (a) |

Weighted-Average Exercise Price of Outstanding Options (b) |

Number of Securities Remaining Available for Future Issuance Under Equity Compensation Plans (Excluding Securities Reflected in Column (a)) (c) | |||

| Equity compensation plans |

1,506,966 (2) | $23.66 (3) | 931,249 (4) |

| (1) | Includes common shares to be issued as awards under The Brink’s Home Security 2008 Equity Incentive Plan (“2008 Equity Plan”), Non-Employee Directors’ Equity Plan, Key Employees’ Deferred Compensation Program, and the Directors’ Stock Accumulation Plan. See Note 10 – Share-Based Compensation Plans to the consolidated financial statements for additional information regarding these equity compensation plans. There have been no repurchases of common stock under the Company’s plans as of December 31, 2009. |

| (2) | Included within the number of securities to be issued upon exercise are 857,436 unvested options as of December 31, 2009. |

| (3) | Does not include deferred compensation units, units under the Directors’ Stock Accumulation Plan, restricted stock units, and deferred stock units. |

| (4) | The 2008 Equity Plan provides for a maximum of 1,000,000 common shares to be issued as awards plus the aggregate number of shares subject to converted awards. The Non-Employee Directors’ Equity Plan provides for a maximum of the sum of 500,000 shares to be issued as awards, the aggregate number of shares subject to the converted options, and the aggregate number of shares subject to the replacement deferred stock units. Restricted stock units are counted against the limit as two shares for every one share covered by the award under each of these plans. The Directors’ Stock Accumulation Plan provides for a maximum of 100,000 common shares to be issued as awards. The Key Employees’ Deferred Compensation Program does not have a limit on the number of shares to be issued as awards. |

15

Table of Contents

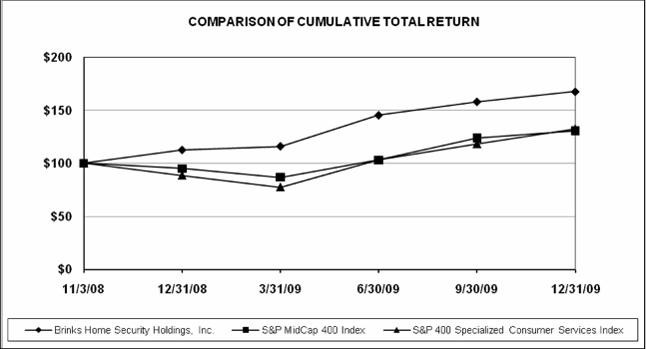

Performance Graph

The following graph compares the relative performance of the our common stock, the Standard & Poor’s Midcap 400 Stock Index and the Standard & Poor’s Midcap 400 GICS Specialized Consumer Services Sub-Index. This graph covers the period from November 3, 2008 (the first trade date immediately following the Spin-off), through December 31, 2009.

| Company/Index |

Nov. 3, 2008 |

Dec. 31, 2008 |

Mar. 31, 2009 |

Jun. 30, 2009 |

Sep. 30, 2009 |

Dec. 31, 2009 | ||||||||||||

| Brink’s Home Security Holdings, Inc. |

$ | 100.00 | $ | 112.58 | $ | 116.08 | $ | 145.40 | $ | 158.14 | $ | 167.64 | ||||||

| S&P MidCap 400 Index |

100.00 | 95.13 | 86.90 | 103.19 | 123.81 | 130.69 | ||||||||||||

| S&P 400 Specialized Consumer Services Index |

100.00 | 88.56 | 77.50 | 103.20 | 118.32 | 132.58 | ||||||||||||

In each case, the data above assumes a $100 investment immediately following November 3, 2008, the first trading day following the Spin-off, and reinvestment of all dividends, if any.

| ITEM 6. | SELECTED FINANCIAL DATA |

The selected historical financial data and operating statistics presented below reflect financial information prepared with the Company’s historical financial results. For periods prior to the Spin-off on October 31, 2008, the financial information includes allocations of certain BCO corporate expenses and higher royalty rate charges. See Note 1- Description of Business, The Spin-off, Basis of Presentation, and Significant Accounting Policies and Note 2 – Transactions with Related Parties to the consolidated financial statements for further discussion regarding the Spin-off and BCO related costs.

The data below should be read in conjunction with our audited consolidated financial statements and accompanying notes, included in Item 8 herein, and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” as seen in Item 7. The financial information below may not be indicative of our future performance and, for periods prior to the Spin-off, does not necessarily reflect what the financial position and results of operations would have been had we operated as a separate, stand-alone entity.

16

Table of Contents

Five Years in Review

| (in millions, except where indicated) | December 31, | |||||||||||||||||||

| 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

| Statement of Income Data |

||||||||||||||||||||

| Revenues |

$ | 565.1 | $ | 532.3 | $ | 484.4 | $ | 439.0 | $ | 392.1 | ||||||||||

| Operating profit |

101.4 | 94.0 | 73.0 | 63.2 | 57.1 | |||||||||||||||

| Net income |

62.7 | 57.1 | 44.2 | 36.3 | 36.0 | |||||||||||||||

| Earnings per Share(a) |

||||||||||||||||||||

| Basic (per share) |

$ | 1.37 | $ | 1.25 | $ | 0.96 | $ | 0.79 | $ | 0.79 | ||||||||||

| Diluted (per share) |

1.36 | 1.25 | 0.96 | 0.79 | 0.78 | |||||||||||||||

| Diluted weighted average common shares outstanding |

46.0 | 45.8 | 45.9 | 45.9 | 45.9 | |||||||||||||||

| Balance Sheet Data |

||||||||||||||||||||

| Cash and cash equivalents |

$ | 113.2 | $ | 63.6 | $ | 3.3 | $ | 2.6 | $ | 3.4 | ||||||||||

| Property and equipment, net |

710.1 | 659.3 | 606.0 | 536.7 | 467.7 | |||||||||||||||

| Total assets |

970.6 | 876.9 | 763.7 | 689.4 | 605.0 | |||||||||||||||

| Shareholders’ equity |

523.4 | 482.0 | 405.5 | 357.6 | 318.9 | |||||||||||||||

| Cash Flow data |

||||||||||||||||||||

| Cash flow from operating activities |

$ | 240.1 | $ | 224.0 | $ | 183.7 | $ | 155.9 | $ | 119.1 | ||||||||||

| Cash flow from investing activities |

(192.1 | ) | (177.8 | ) | (175.8 | ) | (163.9 | ) | (162.2 | ) | ||||||||||

| Cash flow from financing activities |

1.4 | 14.2 | (7.3 | ) | 7.2 | 45.2 | ||||||||||||||

| Key Performance Measures |

||||||||||||||||||||

| Monthly recurring revenue(b) |

$ | 44.2 | $ | 40.5 | $ | 37.2 | $ | 33.1 | $ | 29.1 | ||||||||||

| Ending number of subscribers (in thousands) |

1,359.0 | 1,301.6 | 1,223.9 | 1,124.9 | 1,018.8 | |||||||||||||||

| Ending subscriber base growth (percentage)(c) |

4.4 | 6.3 | 8.8 | 10.4 | 10.6 | |||||||||||||||

| Average number of subscribers (in thousands) |

1,334.5 | 1,267.5 | 1,176.1 | 1,072.5 | 972.8 | |||||||||||||||

| Average subscriber base growth (percentage) |

5.3 | 7.8 | 9.7 | 10.2 | 11.1 | |||||||||||||||

| Disconnect rate (percentage)(d) |

8.2 | 7.5 | 7.0 | 6.4 | 7.2 | |||||||||||||||

| Adjusted EBITDA from recurring services (e) |

$ | 341.5 | $ | 318.3 | $ | 286.3 | $ | 255.4 | $ | 233.1 | ||||||||||

| Adjusted cash invested in new subscribers(f) |

$ | (257.3 | ) | $ | (248.5 | ) | $ | (237.5 | ) | $ | (217.6 | ) | $ | (204.4 | ) | |||||

| (a) | For 2009, basic earnings per share (“EPS”) was computed by dividing net income by the weighted average number of common shares outstanding during the year. Diluted EPS was calculated in a similar manner but included the dilutive effect of stock options and restricted stock units outstanding during the year. For periods prior to the Spin-off, no common stock of Holdings and none of Holdings’ equity awards were outstanding. Basic and diluted earnings per share were computed on a pro forma basis using the average number of shares of the Company’s common stock outstanding from October 31, 2008 to December 31, 2008. The number of diluted shares used in the calculation was based on the number of shares of the Company’s common stock outstanding plus the estimated potential dilution that could have occurred if options and restricted stock units granted under the Company’s equity-based compensation arrangements were exercised or converted into the Company’s common stock. |

| (b) | Monthly recurring revenue (“MRR”), a non-GAAP measure, is calculated based on the number of subscribers at period end multiplied by the average fee per subscriber earned in the last month of the period for contractual monitoring and maintenance services as discussed under the caption “Key Performance Measures — Monthly Recurring Revenues.” |

| (c) | Calculated based on period ending subscribers. |

| (d) | Calculated as a ratio, the numerator of which is customer cancellations, on an annualized basis, and the denominator of which is the average number of customers during the period. Customer relocations, reactivations and dealer charge backs of contract cancellations are excluded from the calculation. |

| (e) | Adjusted EBITDA from recurring services, a non-GAAP measure, is normalized as if the royalty rate had been 1.25% of net revenues, instead of the royalty rate of approximately 7% of revenues charged by BCO before the Spin-off, for all periods presented. Upfront royalty expense is excluded from this metric. This measure is discussed under the caption “Key Performance Measures — Adjusted EBITDA from Recurring Services.” |

| (f) | Adjusted cash invested in new subscribers, a non-GAAP measure, represents cash used to acquire new subscribers during the period and excludes costs related to the Brand Introduction. This measure is discussed in “Key Performance Measures — Adjusted Cash Invested in New Subscribers.” |

17

Table of Contents

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Introduction

The following discussion, which presents the results of Brink’s Home Security Holdings, Inc. and its consolidated subsidiaries, should be read in conjunction with the accompanying consolidated financial statements and notes thereto for the years ended December 31, 2009 and 2008, and each of the years in the three-year period ended December 31, 2009, along with the five-year financial summary and operating statistics presented in Part II, Item 6, “Selected Financial Data,” the risk factors discussed in Part I, Item 1A, “Risk Factors,” and the cautionary statement regarding forward-looking information.

As used in this Report, (a) references to “Holdings,” “Company,” “we,” “us,” and “our” refer to Brink’s Home Security Holdings, Inc. and its consolidated subsidiaries, including Broadview Security, Inc. (“Broadview Security,” formerly named Brink’s Home Security, Inc.), after the spin-off transaction described below, and (b) references to the “Company” on a historical basis, prior to the spin-off transaction, refer to Brink’s Home Security and its consolidated subsidiaries, in each case unless the context requires otherwise.

This discussion is intended to provide the reader with information that will assist in understanding our financial statements, the changes in certain key items in those financial statements from period to period, and the primary factors that accounted for those changes, how operating results affect our financial condition and results of our operations of the Company as a whole, and how certain accounting principles and estimates affect our financial statements. Unless otherwise indicated, all references to earnings per share (“EPS”) are on a diluted basis.

Recent Developments

On January 18, 2010, we signed a definitive agreement and plan of merger (“Merger Agreement”) to be merged into a wholly-owned subsidiary of Tyco International Ltd (“Tyco”) in a transaction valued at approximately $2.0 billion (the “Merger”). The Merger is subject to customary closing conditions, various regulatory approvals and approval of our shareholders. We currently expect the Merger to close in the second or third quarter of calendar year 2010. Upon closing of the Merger, we anticipate that Broadview Security will be combined with Tyco’s ADT security business under the ADT brand. Refer to Part 1, Item 1, Business, for further discussion of the Merger. The uncertainty of this pending transaction and the ultimate resolution may significantly impact our operations and continuation of historical trends in future periods as it becomes more difficult to reasonably estimate trends affecting our company, capital resource needs, and other items that may vary depending on the timing or completion of the proposed transaction.

History

On September 12, 2008, the Board of Directors of The Brink’s Company (“BCO”) approved the separation of BCO into two independent, publicly traded companies through the spin-off of the Company to shareholders of BCO (the “Spin-off”). To affect the Spin-off, BCO transferred all outstanding shares of Brink’s Home Security, Inc. to Holdings, another wholly-owned subsidiary of BCO, through a series of transactions pursuant to a Separation and Distribution Agreement between BCO and Holdings. On October 31, 2008, BCO distributed all of the shares of Holdings to the stockholders of BCO at a ratio of one share of Holdings common stock for each share of BCO common stock held by each such holder as of the record date of October 21, 2008. On November 3, 2008, after completion of the Spin-off, our stock began trading “regular way” as an independent public company on the New York Stock Exchange under the symbol “CFL”, reflecting our corporate mission of creating “Customers For Life.”