Attached files

| file | filename |

|---|---|

| EX-31.2 - EXHIBIT 31.2 - CHINA HGS REAL ESTATE INC. | ex312.htm |

| EX-31.1 - EXHIBIT 31.1 - CHINA HGS REAL ESTATE INC. | ex311.htm |

| EX-32.2 - EXHIBIT 32.2 - CHINA HGS REAL ESTATE INC. | ex322.htm |

| EX-32.1 - EXHIBIT 32.1 - CHINA HGS REAL ESTATE INC. | ex321.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10−Q

(Mark

One)

x QUARTERLY REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For

the quarterly period ended December 31, 2009

¨ TRANSITION REPORT

PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the

transition period from ____________ to _____________

Commission

File Number: 000-49687

CHINA HGS REAL ESTATE

INC.

(Exact

Name of Registrant as Specified in Its Charter)

|

Florida

|

33-0961490

|

|

|

(State

or Other Jurisdiction of Incorporation)

|

(I.R.S.

Employer Identification Number)

|

6

Xinghan Road, 19th Floor, Hanzhong City

Shaanxi

Province, PRC 723000

(Address

of Principal Executive Offices, Zip Code)

(86)

091 - 62622612

(Registrant’s

Telephone Number, including Area Code)

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Exchange Act during the past 12 months (or

for such shorter period that the registrant was required to file such reports),

and (2) has been subject to such filing requirements for the past 90 days. Yes

x No ¨

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files). Yes o No o

i

Indicate

by check mark whether the registrant is a larger accelerated filer, an

accelerated filer, or a non-accelerated filer. See definition of “accelerated

filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check

one)

|

Large

accelerated filer ¨

|

Accelerated

filer ¨

|

|

|

Non-accelerated

filer ¨ (Do

not check if a smaller reporting

company)

|

|

Smaller

reporting company x

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). Yes ¨ No x

The

number of shares outstanding of each of the issuer’s classes of common equity,

as of February 11, 2010 is as follows:

|

Class

of Securities

|

Shares

Outstanding

|

|

|

Common

Stock, $0.001 par value

|

45,050,000

|

ii

TABLE

OF CONTENTS

|

Page

|

||

|

PART

I

|

FINANCIAL

INFORMATION

|

|

|

Item

1.

|

Financial

Statements

|

1

|

|

Condensed

Consolidated Balance Sheets as of December 31, 2009 (Unaudited) and

September 30, 2009

|

1

|

|

|

Condensed

Consolidated Statements of Income For The Three Months Ended December 31,

2009 and 2008 (Unaudited)

|

2

|

|

|

Condensed

Consolidated Statements of Cash Flows For The Three Months Ended December

31, 2009 And 2008 (Unaudited)

|

3

|

|

|

Notes

To Condensed Consolidated Financial Statements (Unaudited)

|

4

|

|

|

Item

2.

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

17

|

|

Item

3.

|

Quantitative

and Qualitative Disclosures About Market Risk

|

30

|

|

Item

4.

|

Controls

and Procedures

|

31

|

|

PART

II

|

OTHER

INFORMATION

|

|

|

Item

1.

|

Legal

Proceedings

|

32

|

|

Item

1A.

|

Risk

Factors

|

32

|

|

Item

2.

|

Unregistered

Sales of Equity Securities and Use of Proceeds

|

32

|

|

Item

3.

|

Defaults

Upon Senior Securities

|

32

|

|

Item

4.

|

Submission

of Matters to a Vote of Securities Holders

|

32

|

|

Item

5.

|

Other

Information

|

32

|

|

Item

6.

|

Exhibits

|

33

|

|

Signatures

|

34

|

|

|

EX-31.1

|

||

|

EX-31.2

|

||

|

EX-32.1

|

||

|

EX-32.2

|

iii

PART

I FINANCIAL INFORMATION

ITEM

1. FINANCIAL STATEMENTS.

CHINA

HGS REAL ESTATE INC. AND SUBSIDIARIES

CONDENSED

CONSOLIDATED BALANCE SHEETS

AS OF DECEMBER 31, 2009 AND SEPTEMBER

30, 2009 (UNAUDITED)

|

December 31

|

September

30

|

|||||||

|

2009

|

2009

|

|||||||

|

(unaudited)

|

(audited)

|

|||||||

|

ASSETS

|

||||||||

|

Current

assets:

|

||||||||

|

Cash

and cash equivalents

|

$

|

1,942,513

|

$

|

820,783

|

||||

|

Restricted

cash

|

613,431

|

$

|

412,373

|

|||||

|

Loans

to outside parties, net of allowance

|

3,956,006

|

$

|

1,762,022

|

|||||

|

Due

from related party

|

||||||||

|

Real

estate property development completed

|

6,067,557

|

2,392,003

|

||||||

|

Real

estate property under development

|

38,906,520

|

42,522,287

|

||||||

|

Other

current assets

|

88,808

|

71,985

|

||||||

|

Total

current assets

|

51,574,835

|

47,981,453

|

||||||

|

Property,

plant and equipment, net

|

695,945

|

713,008

|

||||||

|

Total

assets

|

$

|

52,270,780

|

$

|

48,694,461

|

||||

|

LIABILITIES

AND STOCKHOLDERS’ EQUITY

|

||||||||

|

Current

liabilities:

|

||||||||

|

Short-term

loans

|

$

|

585,035

|

$

|

672,751

|

||||

|

Accounts

payable

|

872,997

|

730,838

|

||||||

|

Other

payables

|

1,113,839

|

1,021,147

|

||||||

|

Customer

deposits

|

13,806,359

|

14,900,334

|

||||||

|

Accrued

expenses

|

763,948

|

125,742

|

||||||

|

Taxes

payable

|

1,695,482

|

1,380,694

|

||||||

|

Total

current liabilities

|

18,837,660

|

18,831,506

|

||||||

|

Stockholders’

equity:

|

||||||||

|

Common

stock, $.001 par value, 100,000,000 shares authorized, 45,050,000 shares

issued and outstanding as of December 31, 2009 and September 30, 2009,

respectively

|

45,050

|

45,050

|

||||||

|

Additional

paid-in capital

|

17,632,348

|

17,632,348

|

||||||

|

Statutory

surplus

|

11,473,560

|

7,904,531

|

||||||

|

Retained

earnings

|

3,199,920

|

3,092,499

|

||||||

|

Accumulated

other comprehensive income

|

1,951,903

|

1,950,766

|

||||||

|

Total

stockholders’ equity

|

33,433,120

|

29,862,955

|

||||||

|

Total

liabilities and stockholders’ equity

|

$

|

52,270,780

|

$

|

48,694,461

|

||||

See

accompanying notes to condensed consolidated financial statements

1

CHINA

HGS REAL ESTATE INC. AND SUBSIDIARIES

CONDENSED

CONSOLIDATED STATEMENTS OF INCOME

FOR

THE THREE MONTHS ENDED DECEMBER 31, 2009 AND 2008 (UNAUDITED)

|

Three months ended December

31,

|

||||||||

|

2009

|

2008

|

|||||||

|

Real

estate sales, net of sales taxes of $663,246 and $545,470,

respectively

|

$

|

10,390,857

|

$

|

8,776,343

|

||||

|

Cost

of real estate sales, exclusive of depreciation

|

5,552,590

|

4,776,439

|

||||||

|

Gross

profit

|

4,838,267

|

3,999,904

|

||||||

|

Operating

expenses

|

||||||||

|

Selling

and distribution expenses

|

299,081

|

129,953

|

||||||

|

General

and administrative expenses

|

817,230

|

168,474

|

||||||

|

Total

operating expenses

|

1,116,311

|

298,427

|

||||||

|

Operating

income

|

3,721,956

|

3,701,477

|

||||||

|

Other

income (expenses)

|

||||||||

|

Interest

expenses

|

(14,752)

|

(41,571)

|

||||||

|

Other

expenses

|

0

|

(309)

|

||||||

|

Total

other income (expenses)

|

14,752

|

41,880

|

||||||

|

Income

before income taxes

|

3,707,204

|

3,659,597

|

||||||

|

Provision

for income taxes

|

138,176

|

137,250

|

||||||

|

Net

income

|

3,569,028

|

3,522,347

|

||||||

|

Other

comprehensive income

|

||||||||

|

Foreign

currency translation adjustment

|

1136

|

978

|

||||||

|

Comprehensive

income

|

$

|

3,570,164

|

$

|

3,523,325

|

||||

|

Basic

and diluted income per common share

|

||||||||

|

-

Basic

|

$

|

0.08

|

$

|

0.09

|

||||

|

-

Diluted

|

$

|

0.08

|

$

|

0.09

|

||||

|

Weighted

average common shares outstanding:

|

||||||||

|

-

Basic

|

45,050,000

|

39,000,000

|

||||||

|

-

Diluted

|

45,050,000

|

39,000,000

|

||||||

See

accompanying notes to condensed consolidated financial statements

2

CHINA

HGS REAL ESTATE INC. AND SUBSIDIARIES

CONDENSED

CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE THREE MONTHS ENDED DECEMBER 31,

2009 AND 2008 (UNAUDITED)

|

Three months ended

December 31,

|

||||||||

|

2009

|

2008

|

|||||||

|

Cash

flows from operating activities

|

||||||||

|

Net

income

|

$

|

3,569,028

|

$

|

3,522,965

|

||||

|

Adjustments

to reconcile net income to net cash provided by (used in) operating

activities:

|

||||||||

|

Depreciation

|

14,246

|

11,344

|

||||||

|

Loss

on disposal of fixed assets

|

2,861

|

308

|

||||||

|

Changes

in assets and liabilities

|

||||||||

|

(Increase)

decrease in

|

||||||||

|

Restricted

cash

|

(201,068)

|

54,437

|

||||||

|

Accounts

receivable

|

0

|

(14,784)

|

||||||

|

Loans

to outside parties

|

(2,194,256)

|

(350,664)

|

||||||

|

Real

estate property development completed

|

(3,676,043)

|

4,776,439

|

||||||

|

Real

estate property under development

|

3,618,875

|

(2,533,239)

|

||||||

|

Due

from related party

|

||||||||

|

Other

current assets

|

(16,823)

|

(214,034)

|

||||||

|

(Increase)

decrease in

|

||||||||

|

Accounts

payables

|

142,141

|

(349,649)

|

||||||

|

Other

payables

|

92,647

|

(522,620)

|

||||||

|

Customer

deposits

|

(1,095,034)

|

(6,788,087)

|

||||||

|

Accrued

expenses

|

638,308

|

(38,501)

|

||||||

|

Taxes

payable

|

314,761

|

365,454

|

||||||

|

Net

cash provided by (used in) operating activities

|

1,209,643

|

(2,081,245)

|

||||||

|

Cash

flow from investing activities

|

||||||||

|

Addition

of fixed assets

|

0

|

(343,447)

|

||||||

|

Proceeds

from disposal of fixed assets

|

0

|

0

|

||||||

|

Net

cash used in investing activities

|

0

|

(343,447)

|

||||||

|

Cash

flow from financing activities

|

||||||||

|

Proceeds

from shareholder loans

|

0

|

(412,360)

|

||||||

|

Repayment

of short-term loans

|

(87,770)

|

0

|

||||||

|

Capital

contribution

|

(437,750)

|

|||||||

|

Net

cash provided by (used in) financing activities

|

(87,770)

|

(850,111)

|

||||||

|

Effect

of changes of foreign exchange rate on cash and cash

equivalents

|

(143)

|

(504)

|

||||||

|

Net

increase (decrease) in cash and cash equivalents

|

1,121,730

|

(1,574,007)

|

||||||

|

Cash

and cash equivalents, beginning of year

|

820,783

|

2,121,060

|

||||||

|

Cash

and cash equivalents, end of period

|

$

|

1,942,513

|

$

|

546,983

|

||||

|

Supplemental

disclosure of cash flow information

|

||||||||

|

Interest

paid

|

$

|

13,337

|

$

|

42,733

|

||||

|

Income

taxes paid

|

$

|

31,411

|

$

|

78,430

|

||||

|

Non-cash

financing activities

|

||||||||

|

Capital

contribution converted from dividend payable

|

$

|

0

|

$

|

5,483,508

|

||||

|

Capital

contribution converted from retained earnings

|

$

|

0

|

$

|

10,788,349

|

||||

|

Capital

contribution converted from surplus

|

$

|

0

|

$

|

799,137

|

||||

See

accompanying notes to condensed consolidated financial statements

3

CHINA

HGS REAL ESTATE, INC.

NOTES

TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR

THE THREE MONTHS ENDED DECEMBER 31, 2009 AND 2008 (UNAUDITED)

Note

1. ORGANIZATION AND BASIS OF PRESENTATION

China HGS Real Estate Inc. (“China HGS” or

the “Company”), formerly known as China Agro Sciences Corp., is a

corporation organized under the laws of the State of Florida. The

Company is engaged in real estate development, primarily in the construction and

sale of residential apartments, car parks as well as commercial

properties. The Company focuses on real estate development in the

second-tier and third-tier cities in the People’s Republic of China

(“PRC”).

The

accompanying unaudited condensed consolidated financial statements have been

prepared in accordance with generally accepted accounting principles for interim

financial information. Accordingly, they do not include all of the

information and footnotes required by generally accepted accounting principles

for complete financial statements. In the opinion of the management,

all adjustments (consisting only of normal recurring accruals) considered

necessary for a fair presentation have been included. Operating

results for the three months ended December 31, 2009 and 2008 are not

necessarily indicative of the results that may be expected for the full

years. The information included in this Form 10-Q should be read in

conjunction with Management’s Discussion and Analysis of Financial Condition and

Results of Operations and the financial statements and notes thereto included in

the Company’s Annual Report on Form 10-K for the fiscal year ended September 30,

2009.

The

balance sheet at September 30, 2009 has been derived from the audited financial

statements at that date, but does not necessarily include all of the information

and footnotes required by GAAP for the complete financial

statements.

Note

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Reclassification

Certain

prior period amounts have been reclassified to conform to the current period

presentation. These reclassifications had no effect on reported total

assets, liabilities, stockholders’ equity or net income.

Principles

of consolidation

The

consolidated financial statements include the financial statements of the

Company, its wholly-owned subsidiaries, China HGS Investment Inc., Shaanxi HGS

Management and Consultation Limited Company (“Shaanxi HGS”) and its Variable

Interest Entity, Shannxi Guangsha Investment and Development Group Co., Ltd.

(“Guangsha”). All inter-company transactions and balances between the

Company and its subsidiaries have been eliminated upon

consolidation.

Use

of estimates

The

preparation of financial statements in conformity with U.S. GAAP (FASB ASC

275-10-50-4) requires management to make estimates and assumptions that affect

the amounts reported in the financial statements and accompanying notes, and

disclosure of contingent liabilities at the date of the consolidated financial

statements. Estimates are used for, but not limited to, the selection

of the useful lives of property and equipment, provision necessary for

contingent liabilities, fair values, revenue recognition, taxes, budgeted costs

and other similar charges. Management believes that the estimates

utilized in preparing its consolidated financial statements are reasonable and

prudent. Actual results could differ from these

estimates.

4

Fair

value of financial instruments

Financial

instruments include cash and cash equivalents, restricted cash, accounts

receivable, other current assets, short-term loans, accounts payable, customer

deposits, other payables, accrued expenses, and taxes payable. The carrying

amounts of the above accounts approximate their fair value due to the short term

maturities of these instruments.

Revenue

recognition

Real

estate sales are reported in accordance with the FASB guidance “Accounting for

Sales of Real Estate” (formerly referred to as SFAS No. 66).

Revenue

from the sales of development properties is recognized by the full accrual

method at the time of the closing of an individual unit sale. This

occurs when title to or possession of the property is transferred to the

buyer. A sale is not considered consummated until (a) the

parties are bound by the terms of a contract, (b) all consideration has

been exchanged, (c) any permanent financing of which the seller is

responsible has been arranged, (d) all conditions precedent to closing have

been performed, (e) the seller does not have substantial continuing

involvement with the property, and (f) the usual risks and rewards of

ownership have been transferred to the buyer. Further, the buyer’s

initial and continuing investment is adequate to demonstrate a commitment to pay

for the property, and the buyer’s receivable, if any, is not subject to future

subordination. Sales transactions not meeting all the conditions of

the full accrual method are accounted for using the deposit method in which all

costs are capitalized as incurred, and payments received from the buyer are

recorded as a deposit liability.

Foreign

currency translation

The

Company’s financial information is presented in US dollars. The

functional currency of the Company is Renminbi (“RMB”), the currency of the

PRC. Transactions at the Company which are denominated in currencies

other than RMB are translated into RMB at the exchange rate quoted by the

People’s Bank of China prevailing at the dates of the

transactions. Exchange gains and losses resulting from transactions

denominated in a currency other than that RMB are included in statements of

operations as exchange gains. The financial statements of the Company

have been translated into U.S. dollars in accordance with Statement of Financial

Accounting Standard “Foreign

Currency Translation.” The financial information is first

prepared in RMB and then is translated into U.S. dollars at period-end exchange

rates as to assets and liabilities and average exchange rates as to revenue and

expenses. Capital accounts are translated at their historical

exchange rates when the capital transactions occurred. The effects of

foreign currency translation adjustments are included as a component of

accumulated other comprehensive income in shareholders’ equity.

|

2009

|

2008

|

|||||||

|

Period

end RMB: USD exchange rate

|

6.8372 | 6.8542 | ||||||

|

Three

months Average RMB: USD exchange rate

|

6.836 | 6.8532 | ||||||

5

The

RMB is not freely convertible into foreign currency and all foreign exchange

transactions must take place through authorized institutions. No

representation is made that the RMB amounts could have been, or could be,

converted into US dollars at the rates used in translation.

Cash

and cash equivalents

Cash

includes cash on hand and demand deposits in accounts maintained with

state-owned and private banks within the PRC. The Company considers

all highly liquid investments with original maturities of three months or less

when purchased to be cash equivalents. The Company maintains bank

accounts in the PRC. Total cash at December 31 and September 30, 2009

amounted to $1,942,513 and $820,783, respectively, of which no deposits are

covered by insurance. The Company has not experienced any losses in

such accounts and management believes it is not exposed to any risks on its cash

in bank accounts.

Loans

to outside parties

Loans to

outside parties consist of various cash advances to unrelated companies and

individuals with which the Company has business relationships. Loans

to outside parties are reviewed periodically as to whether their carrying value

has become impaired. The Company considers the assets to be impaired

if the collectability of the balances becomes doubtful. As of

December 31 and September 30, 2009, no allowance for doubtful debts is recorded

as all of the loans are considered fully collectible.

Real

estate property development completed and under development

Real

estate property consists of finished residential unit sites, commercial offices

and residential unit sites under development. The Company leases the

land for the residential unit sites under land use right leases with various

terms from the government of China. Real estate property development

completed and real estate property under development are stated at the lower of

cost or fair value.

Expenditures

for land development, including cost of land use rights, deed tax,

pre-development costs, and engineering costs, exclusive of depreciation, are

capitalized and allocated to development projects by the specific identification

method. Costs are allocated to specific units within a project based

on the ratio of the sales area of units to the estimated total sales area times

the total project costs.

Costs of

amenities transferred to buyers are allocated as common costs of the project

that are allocated to specific units as a component of total construction

costs. For amenities retained by the Company, costs in excess of the

related fair value of the amenity are also treated as common

costs. Results of operations of amenities retained by the Company are

included in current operating results.

In

accordance to Statement of Financial Accounting Standards “ Accounting for the Impairment or

Disposal of Long-lived Assets” (formerly referred to as “SFAS No. 144”),

real estate property development completed and under development are subject to

valuation adjustments when the carrying amount exceeds fair value. An

impairment loss shall be recognized only if the carrying amount of the assets is

not recoverable and exceeds fair value. The carrying amount is not

recoverable if it exceeds the sum of the undiscounted cash flows expected to be

generated by the assets.

6

Management

evaluates, on yearly basis, the impairment of the Company’s real estate

developments based on a community level. Each community is assessed

as an individual project. The evaluation takes into account of

several factors including, but not limited to, physical condition, inventory

holding period, management’s plans for future operations, prevailing market

prices for similar properties and projected cash flows. Management

has determined that there were no impairment losses as of December 31 and

September 30, 2009.

Property

and equipment

Property

and equipment are recorded at cost less accumulated depreciation and any

impairment losses. The cost of an asset comprises of its purchase

price and any directly attributable costs of bringing the asset to its working

condition and location for its intended use. Expenditure incurred

after the fixed assets have been put into operation, such as repairs and

maintenance and overhaul costs, is normally charged to the profit and loss

account in the year in which it is incurred.

In

situations where it can be clearly demonstrated that the expenditure has

resulted in an increase in the future economic benefits expected to be obtained

from the use of the asset beyond its originally assessed standard of

performances, the expenditure is capitalized as an additional cost of the

asset.

Depreciation

is computed using the straight-line method over the estimated useful lives of

the assets, less any estimated residual value. Estimated useful

lives of the assets are as follows:

|

Buildings

|

39

years

|

|

Machinery

and equipment

|

5-10

years

|

|

Vehicles

|

8

years

|

Any gain

or loss on disposal or retirement of a fixed asset is recognized in the profit

and loss account and is the difference between the net sales proceeds and the

carrying amount of the relevant asset. When property and equipment

are retired or otherwise disposed of, the asset and accumulated depreciation are

removed from the accounts and the resulting profit or loss is reflected in

income.

Maintenance,

repairs and minor renewals are charged directly to expense as incurred unless

such expenditures extend the useful life or represent a betterment, in which

case they are capitalized.

Impairment

of long-lived assets

Long-lived

assets, which include property, plant and equipment and intangible assets, are

reviewed for impairment whenever events or changes in circumstances indicate

that the carrying amount of an asset may not be recoverable.

Recoverability

of long-lived assets to be held and used is measured by a comparison of the

carrying amount of an asset to the estimated undiscounted future cash flows

expected to be generated by the assets. If the carrying amount of an

asset exceeds its estimated undiscounted future cash flows, an impairment charge

is recognized by the amount by which the carrying amount of the asset exceeds

the fair value of the assets. Fair value is generally determined

using the asset’s expected future discounted cash flows or market value, if

readily determinable. No impairment loss is recorded as of December

31 and September 30, 2009.

7

Advance

to vendors

Advances

to vendors consist of balances paid to contractors and vendors for services and

materials that have not been provided or received and generally relate to the

development and construction of residential units in the

PRC. Advances to vendors are reviewed periodically to determine

whether their carrying value has become impaired. The Company

considers the assets to be impaired if the collectability of the services and

materials become doubtful. As of December 31 and September 30, 2009,

there was no advance to vendors.

Capitalized

interest

Capitalized

interest is accounted for in accordance with FASB guidance “Capitalization of

Interest Cost” (formerly referred to as SFAS No. 34).

For loans

to finance projects and provide for working capital, the Company charges the

borrowing costs related to working capital loans to interest expense when

incurred and capitalize interest costs related to project developments as a

component of the project costs.

The

interest to be capitalized for a project is based on the amount of borrowings

related specifically to such project. Interest for any period is

capitalized based on the amounts of accumulated expenditures and the interest

rate of the loans. Payments received from the pre-sales of units in

the project are deducted in the computation of the amount of accumulated

expenditures during a period. The interest capitalization period

begins when expenditures have been incurred and activities necessary to prepare

the asset (including administrative activities before construction) have begun,

and ends when the project is substantially completed. Interest

Capitalized is limited to the amount of interest incurred.

The

interest rate used in determining the amount of interest capitalized is the

weighted average rate applicable to the project-specific

borrowings. However, when accumulated expenditures exceed the

principal amount of project-specific borrowings, the Company also capitalizes

interest on borrowings that are not specifically related to the project, at a

weighted average rate of such borrowings.

The

Company’s significant judgments and estimates related to interest capitalization

include the determination of the appropriate borrowing rates for the

calculation, and the point at which capitalization is started and

discontinued. Changes in the rates used or the timing of the

capitalization period may affect the balance of property under development and

the costs of sales recorded. There was no capitalized interest as of

December 31 and September 30, 2009.

Customer

deposits

Customer

deposits consist of amounts received from customers relating to the sale of

residential units in the PRC. In the PRC, customers will generally

obtain permanent financing for the purchase of their residential unit prior to

the completion of the project. The lending institution will provide

the funding to the Company upon the completion of the financing rather than the

completion of the project. The Company receives these funds and

recognizes them as a current liability until the revenue can be

recognized.

Other

payables

Other

payables consist of balances for non-construction costs with unrelated companies

and individuals with which the Company has business

relationships. These amounts are unsecured, non-interest bearing and

generally are short-term in nature.

8

Property

warranty

The

Company provides customers with warranties which cover major defects of building

structure and certain fittings and facilities of properties sold. The

warranty period varies from two years to five years, depending on different

property components the warranty covers. The Company constantly

estimates potential costs for materials and labor with regard to warranty-type

claims expected to be incurred subsequent to the delivery of a

property. Reserves are determined based on historical data and trends

with respect to similar property types and geographical areas. The

Company constantly monitors the warranty reserve and makes adjustments to its

pre-existing warranties, if any, in order to reflect changes in trends and

historical data as information becomes available. The Company may

seek further recourse against its contractors or any related third parties if it

can be proved that the faults are caused by them. In addition, the

Company also withholds up to 2% of the contract cost from sub-contractors for

periods of two to five years. These amounts are included in current

liabilities, and are only paid to the extent that there has been no warranty

claim against the Company relating to the work performed or materials supplied

by the subcontractors. As of December 31 and September 30, 2009, the

Company had not recognized any warranty liability or incurred any warranty costs

in excess of the amount retained from subcontractors.

Income

taxes

The

Company accounts for income taxes in accordance with FASB ASC 740 “Income

Taxes”, (formerly SFAS No. 109, “Accounting for Income Taxes”) and FASB ASC

740-10, (formerly FASB Interpretation No. 48 “Accounting for Uncertainty in

Income Taxes, an interpretation of SFAS No. 109”). Deferred tax

assets and liabilities are recognized for the expected future tax consequences

of events that have been included in the financial statements or income tax

returns. Deferred tax assets and liabilities are determined based on

the difference between the financial statement and tax basis of assets and

liabilities using enacted rates expected to apply to taxable income in the years

in which those differences are expected to be recovered or

settled. The effect on deferred tax assets and liabilities of a

change in tax rates is recognized in income in the period that includes the

enactment date. There are no deferred tax amounts for the three months ended

December 31, 2009 and 2008.

Land

appreciation tax (“LAT”)

LAT is

prepaid on customer deposits and is expensed when the related revenue is

recognized.

Comprehensive

income

Comprehensive

income is defined to include all changes in equity except those resulting from

investments by owners and distributions to owners. The Company’s only

components of comprehensive income during the three months ended December 31,

2009 and 2008 were net income and the foreign currency translation

adjustment.

Earnings

per share

The

Company computes earnings per share (“EPS”) in accordance with the ASC 260,

“Earnings per share”

which requires companies with complex capital structures to present basic and

diluted EPS. Basic EPS is measured as net income divided by the weighted

average common shares outstanding for the period. Diluted EPS is similar

to basic EPS but presents the dilutive effect on a per share basis of potential

common shares (e.g., convertible securities, options and warrants) as if they

had been converted at the beginning of the periods presented, or issuance date,

if later. Potential common shares that have an anti-dilutive effect (i.e.,

those that increase income per share or decrease loss per share) are excluded

from the calculation of diluted EPS.

9

Advertising

expenses

Advertising

costs are expensed as incurred, or the first time the advertising takes place,

in accordance with Statement of Position No. 93-7 “ Reporting on

Advertising Costs.” For the three months ended December

31, 2009 and 2008, the Company recorded advertising expenses of $21,434 and

$876, respectively.

Concentration

of credit risk

Financial

instruments that potentially subject the Company to concentration of credit risk

consist primarily of accounts receivables and other receivables. The

Company does not require collateral or other security to support these

receivables. The Company conducts periodic reviews of its clients'

financial condition and customer payment practices to minimize collection risk

on accounts receivables.

Risks

and uncertainties

The

operations of the Company are located in the PRC. Accordingly, the

Company’s operations are subject to special considerations and significant risks

not typically associated with companies in North America and Western

Europe. These include risks associated with, among others, the

political, economic and legal environment and foreign currency

exchange. The Company’s results may be adversely affected by changes

in the political and social conditions in the PRC, and by changes in

governmental policies with respect to laws and regulations, anti-inflationary

measures, currency conversion, remittances abroad, and rates and methods of

taxation, among other things.

The

Company uses various suppliers and sells to a wide range of

customers. No single supplier or customer accounted for more than 10%

of revenue or project expenditures for the three months ended December 31, 2008

and 2009.

Recent

accounting pronouncements

In August

2009, the FASB issued ASU 2009-5, “Fair Value Measurements and Disclosures

(Topic 820) – Measuring Liabilities at Fair Value” (“FASB ASU 2009-5”), which

provides a single definition of fair value, a framework for measuring fair

value, and requires additional disclosure about the use of fair value to measure

assets and liabilities. ASU 2009-05 provides clarification for

circumstances in which a quoted price in an active market for the identical

liability is not available. In such circumstances, a reporting entity

is required to measure fair value using one or more of the following techniques:

(1) a valuation technique that uses: (a) the quoted price of the identical

liability when traded as an asset; or (b) quoted prices for similar liabilities

or similar liabilities when traded as assets; or (2) another valuation technique

that is consistent with the principles of Topic 820 such as an income approach

or a market approach. The guidance provided in ASU 2009-05 is

effective for the first reporting period (including interim periods) beginning

after issuance.

10

In

October 2009, the FASB issued ASU 2009-13, “Revenue Recognition (Topic 605) –

Multiple-Deliverable Revenue Arrangements – a Consensus of the FASB Emerging

Issues Task Force” (“ASU 2009-13”). ASU 2009-13 addresses the

accounting for multiple-deliverable arrangements to enable vendors to account

for products or services (deliverables) separately rather than as a combined

unit. The amendments in this update will be effective prospectively

for revenue arrangements entered into or materially modified in fiscal years

beginning on or after June 15, 2010. Early adoption is

permitted. The Company is currently evaluating this

update.

Note

3. RESTRICTED CASH

Restricted

cash is cash set aside for a particular use or event and is subject to

withdrawal restrictions. The Company is required to maintain certain

deposits, as restricted cash, with banks that provide mortgage loans to the

Company’s customers. These deposits are guarantees for the mortgage

loans and are normally equivalent to 5% of the mortgage proceeds paid to the

Company. As of December 31 and September 30, 2009, the balances of

restricted cash totaled $613,431 and $412,373, respectively. These

deposits are not covered by insurance. The Company has not

experienced any losses in such accounts and management believes its restricted

cash account is not exposed to any risks.

Note

4. LOANS TO OUTSIDE PARTIES

Loans to

outside parties consist of various cash advances to unrelated companies and

individuals with which the Company has business

relationships. Starting from the second half of year 2007, the price

of building materials in China increased significantly. In order to

control the development costs and maintain good relationships with suppliers,

the Company makes cash advances to its long-term contractors to support their

occasional short-term working capital needs. These advances bear no

interest and they are due on demand. As of December 31 and September

30, 2009, the Company had outstanding loans to outside parties in the amount of

$3,956,006 and $1,762,022, respectively. All these loans are

considered collectible based on the Company’s past experiences. As of

December 31 and September 30, 2009, the Company decided no bad debt reserve was

necessary.

Note

5. REAL ESTATE PROPERTY DEVELOPMENT COMPLETED AND UNDER DEVELOPMENT

The

following summarizes the components of real estate property development

completed and under development as of December 31 and September 30, 2009,

respectively:

11

|

Balance

as of

|

||||||||

|

December

31, 2009

|

September

30, 2009

|

|||||||

|

Development

completed

|

||||||||

|

Yangzhou

Pearl Garden

|

$ | 3,675,414 | $ | - | ||||

|

Central

Plaza

|

2,392,143 | 2,392,003 | ||||||

|

Real

Estate property development completed

|

$ | 6,067,557 | $ | 2,392,003 | ||||

|

Under

development:

|

||||||||

|

Mingzhu

Garden

|

$ | 13,209,981 | $ | 12,988,371 | ||||

|

Nan

Dajie

|

7,582,195 | 6,641,363 | ||||||

|

Yangzhou

Pearl Garden

|

18,114,344 | 22,892,553 | ||||||

|

Real

Estate property under development

|

$ | 38,906,520 | $ | 42,522,287 | ||||

As of

December 31 and September 30, 2009, land use rights included in the real estate

property under development totaled $13,272,244 and $14,261,781,

respectively.

Note

6. PROPERTY, PLANT AND EQUIPMENT

|

Balance

as of

|

||||||||

|

December

31, 2009

|

September

30, 2009

|

|||||||

|

Buildings

|

$ | 350,136 | $ | 350,115 | ||||

|

Machinery

|

29,764 | 29,762 | ||||||

|

Office

equipment

|

40,530 | 43,389 | ||||||

|

Automobiles

|

384,880 | 384,857 | ||||||

|

Total

|

805,310 | 808,123 | ||||||

|

Less:

accumulated depreciation

|

(109,365 | ) | (95,115 | ) | ||||

|

Property,

plant and equipment, net

|

$ | 695,945 | $ | 713,008 | ||||

Depreciation

expense for the three months ended December 31, 2009 and 2008 was $14,246 and

$11,344, respectively.

Note

7. CUSTOMER DEPOSITS

Customer

deposits consist of amounts received from customers for the pre-sale of

residential units in the PRC. The detail of customer deposits is as

follows:

|

Balance

as of

|

||||||||

|

December

31, 2009

|

September

30, 2009

|

|||||||

|

Real

estate property under development

|

||||||||

|

Hanzhong

|

$ | 9,030,748 | $ | 7,473,345 | ||||

|

Yangxian

|

4,775,611 | 7,426,989 | ||||||

|

Total

|

$ | 13,806,359 | $ | 14,900,334 | ||||

12

Customer

deposits are typically funded up to 70%~80% by mortgage loans made by banks to

the customers. Until the customer obtains legal title to the

property, the banks have a right to seek reimbursement from the Company for any

defaults by the customers. The Company, in turn, has a right to

withhold transfer of title to the customer until outstanding amounts are fully

settled.

Note

8. SHORT-TERM LOANS

Short

term bank loans represent amounts due to a local bank and are due on the dates

indicated below. These loans generally can be renewed with the bank.

Short-term bank loans at December 31 and September 30, 2009 consisted of the

following:

|

Balance

as of

|

||||||||

|

December

31, 2009

|

September

30, 2009

|

|||||||

|

a)

Loan payable to Hanzhong City Credit bank

|

- | $ | 87,750 | |||||

|

term

from 12/26/2008 to 10/26/2009,

|

||||||||

|

a

fixed interest rate of 0.7523% per month

|

||||||||

|

b)Loan

payable to Hanzhong City Credit Bank

|

585,035 | 585001 | ||||||

|

one

year term from 8/14/2009 to 8/13/2010

|

||||||||

|

Total

|

$ | 585,035 | $ | 672,751 | ||||

Interest

expense for short term loans totaled $14,752 and $41,571 for the three months

ended December 31, 2009 and 2008, respectively.

A related

party of the Company pledged a land use right in the amount of RMB 7,757,300

(approximately $1.2 million) as collateral for the loan shown above. The Company

paid off portion of the loan in the amount of RMB 600,000 by the end of October

2009.

.

Note

9. OTHER PAYABLES

Other

payables represent contract deposits and bidding deposits that are to be

refunded upon completion of the projects or satisfaction of claim-free

warranty. There were $1,113,839 and $1,021,147 of other payables as

of December 31 and September 30, 2009, respectively.

Note

10. TAXES

(A)

Business sales tax

The

Company is subject to 5% business sales tax on actual revenue. It is

the Company’s continuing practice to recognize 5% of the sales tax on estimated

revenue, and file tax return based on the actual result, as the local tax

authority may exercise broad discretion in applying the tax

amount. As a result, the Company’s accrual sales tax may differ from

the actual tax clearance.

13

(B)

Corporate income taxes (“CIT”)

The

Company is governed by the Income Tax Law of the People’s Republic of China

concerning the private-run enterprises, which are generally subject to income

tax at a new statutory rate of 25%, effective January 1, 2008, on income

reported in the statutory financial statements after appropriate tax

adjustments.

However,

as approved by the local tax authority of Hanzhong City, the Company’s CIT was

assessed annually at a pre-determined fixed rate as an incentive to stimulate

local economy and encourage entrepreneurship. The Company incurred

$138,176 and $137,250 income taxes for the three months ended December 31, 2009

and 2008, respectively.

Although

the possibility exists for reinterpretation of the application of the tax

regulations by higher tax authorities in the PRC, potentially overturning the

decision made by the local tax authority, the Company has not experienced any

reevaluation of the income taxes for prior years. Management believes

that the possibility of any reevaluation of income taxes is remote based on the

fact that the Company has obtained the written tax clearance from the local tax

authority. Thus, no additional taxes payable has been recorded for

the difference between the taxes due based on taxable income calculated

according to statutory taxable income method and the taxes due based on the

fixed rate method. It is the Company’s policy that if such

reevaluation of income taxes becomes probable and the amount of additional taxes

due can be reasonably estimated, additional taxes shall be recorded in which

period the amount can be reasonably estimated and shall not be charged

retroactively to an earlier period.

(C)

LAT

Since

January 1, 1994, LAT has been applicable at progressive tax rates ranging from

30% to 60% on the appreciation of land values, with an exemption provided for

the sales of ordinary residential properties if the appreciation values do not

exceed certain thresholds specified in the relevant tax

laws. However, the Company’s local tax authority in Hanzhong City has

not imposed the regulation on real estate companies in its area of

administration. Instead, the local tax authority has levied the LAT

at the rate of 0.8% or 1.0% against total cash receipts from sales of real

estate properties, rather than according to the progressive rates.

For the

three months ended December 31, 2009 and the fiscal year ended September 30,

2009, the Company has made full payment for LAT with respect to properties

sold in accordance with the requirements of the local tax

authorities.

(D) Tax

payables consisted of the following:

|

Balance

as of

|

||||||||

|

December

31, 2009

|

September

30, 2009

|

|||||||

|

CIT

|

$ | 69,707 | $ | - | ||||

|

Business

tax

|

$ | 1,502,785 | $ | 1,106,713 | ||||

|

Other

taxes and fees

|

122,991 | 273,981 | ||||||

|

Total

taxes payable

|

$ | 1,695,482 | $ | 1,380,694 | ||||

14

Note

11. STOCKHOLDERS’ EQUITY

(a)

Common stock

Prior to

the Share Exchange, the Company had 20,050,000 shares of common

stock issued and outstanding at $.001 per share.

Before

the closing of the Share Exchange transaction, the Company retired 14,000,000

shares of common stock in connection with the spin-off of Dalian Holding. In

connection with the Share Exchange consummated on August 31, 2009, the Company

issued 14,000,000 shares of its common stock to HGS shareholder and additional

25,000,000 shares to the management team of Guangsha.

As a

result of the reverse merger, the equity account of the Company, prior to the

share exchange date, has been retroactively restated so that the ending

outstanding share balance as of the share exchange date is equal to the number

of post share-exchange shares.

As of

December 31, 2009, there were a total of 45,050,000 shares of the Company’s

common stock issued and outstanding.

In

December 2008, the Company’s operating subsidiary, Guangsha’s Board of Directors

approved the following additional capital contribution/conversion:

|

RMB

|

Amount

in US$

|

|||||||

|

- additional

cash contribution

|

3,000,000 | 439,722 | ||||||

|

-

dividend converted to capital

|

40,000,000 | 5,483,508 | ||||||

|

-

retained earnings converted to capital

|

81,000,000 | 10,788,348 | ||||||

|

-

surplus converted to capital

|

6,000,000 | 799,137 | ||||||

As of

December 31, 2009, the total additional paid-in capital account amounted to

$17,632,348.

(b)

Statutory surplus reserves

The

Company is required to make appropriations to reserve funds, comprising the

statutory surplus reserve and discretionary surplus reserve, based on after-tax

net income determined in accordance with generally accepted accounting

principles of the PRC (“PRC GAAP”). Appropriations to the statutory

surplus reserve is required to be at least 10% of the after tax net income

determined in accordance with PRC GAAP until the reserve is equal to 50% of the

entities’ registered capital. Appropriations to the discretionary

surplus reserve are made at the discretion of the Board of

Directors.

The

statutory surplus reserve fund is non-discretionary other than during

liquidation and can be used to fund previous years’ losses, if any, and may be

utilized for business expansion or converted into share capital by issuing new

shares to existing shareholders in proportion to their shareholding or by

increasing the par value of shares currently held by them, provided that the

remaining statutory surplus reserve balance after such issue is not less than

25% of the registered capital before the conversion.

Pursuant

to the Company’s articles of incorporation, the Company is to appropriate 10% of

its net profits as statutory surplus reserve. As of December 31 and

September 30, 2009, the balance of statutory surplus reserve was

$2,330,259.

15

The

discretionary surplus reserve may be used to acquire fixed assets or to increase

the working capital to expend on production and operation of the

business. The Company’s Board of Directors decided not to make an

appropriation to this reserve for the quarter ended December 31,

2009.

NOTE

12. WEIGHTED AVERAGE NUMBER OF SHARES

In August

2009, the Company entered into share exchange transaction which has been

accounted for as a reverse merger under the purchase method of accounting since

there has been a change of control. The Company computes the

weighted-average number of common shares outstanding in accordance with FAS

141(R), which states that in calculating the weighted average shares when a

reverse merger takes place in the middle of the year, the number of common

shares outstanding from the beginning of that period to the acquisition date

shall be computed on the basis of the weighted-average number of common shares

of the legal acquiree (the accounting acquirer) outstanding during the period

multiplied by the exchange ratio established in the merger

agreement. The number of common shares outstanding from the

acquisition date to the end of that period shall be the actual number of common

shares of the legal acquirer (the accounting acquiree) outstanding during that

period.

NOTE

13. CONTIGENCY

As a

industry practice, the Company provides guarantees to PRC banks with respect to

loans procured by the purchasers of the Company’s real estate properties for the

total mortgage loan amount until the completion of the registration of the

mortgage with the relevant mortgage registration authorities, which generally

occurs within six to twelve months after the purchasers take possession of the

relevant properties. The mortgage banks require the Company to

maintain, as restricted cash, 5% to 10% of the mortgage proceeds as security for

the Company’s obligations under such guarantees. If a purchaser

defaults on its payment obligations, the mortgage bank may deduct the delinquent

mortgage payment from the security deposit and require the Company to pay the

excess amount if the delinquent mortgage payments exceed the security

deposit. The Company has made necessary reserves in its restricted

cash account to cover any potential mortgage default as required by mortgage

lenders. The Company has not experienced any losses related to this

guarantee and believes that such reserves are sufficient.

NOTE

14. SUBSEQUENT EVENT

As

required by ASC Topic 855 “Subsequent Events,” the

Company has evaluated subsequent events that have occurred through February 8,

2010, the date the consolidated financial statements were available to be

issued. The only subsequent event is described below.

On

January 6, 2010, the Board of Directors of the Company appointed Gordon H.

Silver, H. David Sherman, Yuankai Wen and Shenghuei Luo as directors of the

Company, effective immediately. In connection with the appointment, the

Company has agreed to pay (i) Mr. Silver an annual compensation in the amount of

$24,000 and option to purchase up to 12,000 shares of the Company’s common

stock, (ii) Mr. Sherman an annual compensation in the amount of $36,000 and

option to purchase up to 12,000 shares of the Company’s common stock and (iii)

Mr. Wen an annual compensation in the amount of 100,000RMB and option to

purchase up to 10,000 shares of the Company’s common stock. These

stock options will become exercisable as to 20% of the original number of Shares

on the Grant Date and 10% of the Shares at the end of every quarter

thereafter. The exercise price of such options is $2.60 per share and

such options will expire on January 6, 2015. These options are

exercisable at $2.6 per share for a term of five years and had tiered vesting

provisions.

16

ITEM

2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS.

Special

Note Regarding Forward Looking Statements

The following discussion should be

read in conjunction with the Condensed Consolidated Financial Statements and

notes thereto included in this Quarterly Report on Form 10-Q, or this

Quarterly Report, and in conjunction with our Annual Report on Form 10-K

for the fiscal year ended September 30, 2009. Certain of these

statements, including, without limitation, statements regarding the extent and

timing of future revenues and expenses and customer demand, statements regarding

the deployment of our products, statements regarding our reliance on third

parties and other statements using words such as “anticipates,” “believes,”

“could,” “estimates,” “expects,” “intends,” “may,” “plans,” “should,” “will” and

“would,” and words of similar import and the negatives thereof, constitute

forward-looking statements. These statements are predictions based

upon our current expectations about future events. Actual results

could vary materially as a result of certain factors, including but not limited

to, those expressed in these statements. We refer you to the “Risk

Factors,” “Results of Operations,” “Disclosures About Market Risk,” and

“Liquidity and Capital Resources” sections contained in this Quarterly Report,

and the risks discussed in our other Securities Exchange Commission, or SEC,

filings, which identify important risks and uncertainties that could cause

actual results to differ materially from those contained in the forward-looking

statements.

We urge you to consider these

factors carefully in evaluating the forward-looking statements contained in this

Quarterly Report. All subsequent written or oral forward-looking

statements attributable to our company or persons acting on our behalf are

expressly qualified in their entirety by these cautionary

statements. The forward-looking statements included in this Quarterly

Report are made only as of the date of this Quarterly Report. We do

not intend, and undertake no obligation, to update these forward-looking

statements.

Overview

of Our Business

Overview

We

conduct substantially all of our business through Shaanxi Guangsha Investment

and Development Group Co., Ltd., in Hanzhong, Shaanxi Province. All

of our businesses are conducted in mainland China. We were founded by

Mr. Xiaojun Zhu, our Chairman and Chief Executive Officer and commenced

operations in 1995 in Hanzhong, a prefecture-level city of Shaanxi

Province. Since the initiation of our business, we have been focused

on expanding our business in certain Tier 2 cities in China which we

strategically selected based on a set of criteria. Our selection

criteria includes population and urbanization growth rate, general economic

condition and growth rate, income and purchasing power of resident consumers,

anticipated demand for private residential properties, availability of future

land supply and land prices and governmental urban planning and development

policies. As of December 31, 2009, we have established operations in

two Tier 2 cities and one county in Hanzhong City, Shaanxi Province, comprising

of downtown area and west ring road in the city of Hanzhong, city of Weinan, a

municipality in Shaanxi Province, and Yang County.

We are a

fast-growing residential real estate developer that focuses on Tier 2 cities in

China. We utilize a standardized and scalable model that emphasizes

rapid asset turnover, efficient capital management and strict cost

control. According to datas from Shanxi Hantai Statistics

Brochure, the Company is currently ranked No.1 among all property

developers in the city of Hanzhong in terms of market shares and contracted

sales of residential units for the years of 2009 and 2008, according to

statistics prepared by the Bureau of Real Estate Management in

Hanzhong. Since 2001, we have planned to expand into strategically

selected Tier 2 cities and some counties with real estate development potential

in Shaanxi Province, and expect to benefit from rising residential housing

demand as a result of increasing income levels of consumers and growing

populations.

17

We intend

to continue our expansion into additional selected Tier 2 cities and counties as

suitable opportunities arise. We will expand to more select targeted

Tier 2 cities including cities in Sichuan Province and other Tier 2 cities in

Shaanxi Province which we are surveying for expansion in the near

future.

Organizational

History

China HGS

Real Estate Inc. (the “Company” or “China HGS”), formerly known as China Agro

Sciences Corp., is a corporation organized under the laws of the

State of Florida.

On August

21, 2009, the Company entered into a Share Exchange Agreement (“Share Exchange”)

by and among the Company, China HGS Investment Inc. (“HGS Investment”), a

corporation formed under the laws of the State of Delaware, and Rising Pilot,

Inc., a British Virgin Island business company which owns 100% issued and

outstanding capital stock of HGS Investment (the “HGS

Shareholder”). The closing of the Share Exchange transaction occurred

on August 31, 2009.

Pursuant

to the Share Exchange Agreement, the HGS Shareholder transferred and assigned to

the Company all of the issued and outstanding capital stock of HGS Investment in

exchange for the issuance of a total of 14,000,000 shares of the Company’s

common stock with $0.001 par value. As a result of this Share

Exchange, HGS Investment becomes a wholly-owned subsidiary of the

Company.

In

addition, as a part of the Share Exchange transaction, the Company entered into

an entrusted management agreement (the “Entrusted Management Agreement”) with

the management of Shaanxi Guangsha Investment and Development Group Co., Ltd.

(“Guangsha”) and issued to Mr. Zhu Xiaojun, CEO of Guangsha and his management

team an aggregate of 25,000,000 shares of common stock of the

Company.

Prior to

and in conjunction with the consummation of the Share Exchange, the Company also

entered into certain purchase and sale agreement with Mr. Zhengquan Wang, the

Company’s CEO prior to the close of the Share Exchange, to spin out the business

and operations of Dalian Holding Corp. (“Dalian Holding”), a Florida corporation

and a wholly-owned subsidiary of the Company (the “Spin-Out”), including

substantially all the assets and liabilities of Dalian Holding (the “Legacy

Business”). Pursuant to such agreement, Mr. Wang shall return

14,000,000 shares of the Company’s common stock within ninety (90) days of the

Closing of the Share Exchange for the exchange of current Dalian Holding assets

and assume all the liabilities of Dalian Holding relating to the Legacy

Business, and the Company shall be released from any and all claims whatsoever

with regard to such liabilities, whether such claim is known or unknown to

Dalian Holding on the date hereof. Prior to the Share Exchange, on

August 29, 2009, the Company also completed the spin-off of all its assets and

liabilities to Dalian Holding Corp. so the only material asset of the Company

following the Share Exchange is the ownership of HGS Investment.

As a

result of the Share Exchange transaction, the shareholders of Guangsha now own

the majority of the equity in the Company. In addition, the original

officers and directors of the Company resigned from their positions and new

directors and officers affiliated with Guangsha were appointed ten days after

the notice pursuant to Rule 14f-1 had been mailed to the shareholders of

record.

The

transaction has been accounted for as a reverse merger under the purchase method

of accounting since there has been a change of control. Accordingly,

HGS Investment and its subsidiaries will be treated as the continuing entity for

accounting purposes.

18

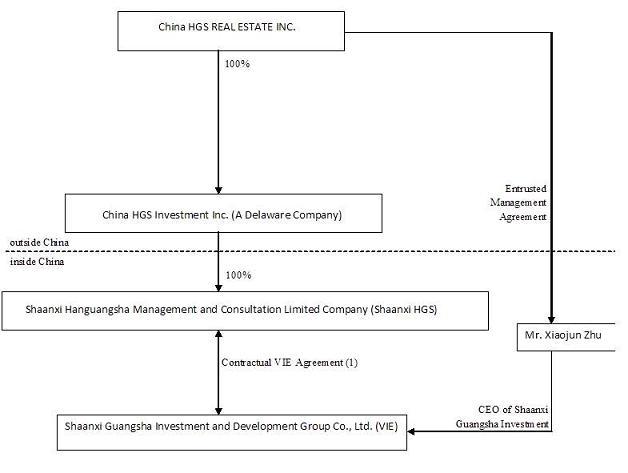

HGS

Investment is a holding company incorporated under the law of the State of

Delaware on July 17, 2008. HGS Investment owns 100% of the equity

interest of Shaanxi Hanguangsha Management and Consultation Limited Company

(“Shaanxi HGS”), a wholly foreign-owned entity incorporated under the laws of

the People’s Republic of China (“PRC” or “China”) on June 3, 2009.

China HGS

does not conduct any substantive operations of its own. Instead,

through its subsidiary, Shaanxi HGS, it had entered certain exclusive

contractual agreements with Shaanxi Guangsha Investment and Development Group

Co., Ltd. (“Guangsha”), a company incorporated in Hanzhong City, Shaanxi

Province, China in November 2007. Pursuant to these agreements,

Shaanxi HGS is obligated to absorb a majority of the risk of loss from

Guangsha’s activities and entitles it to receive a majority of its expected

residual returns. In addition, Guangsha’s shareholders have pledged

their equity interest in Guangsha to Shaanxi HGS, irrevocably granted Shaanxi

HGS an exclusive option to purchase, to the extent permitted under PRC Law, all

or part of the equity interests in Guangsha and agreed to entrust all the rights

to exercise their voting power to the person(s) appointed by Shaanxi

HGS. Through these contractual arrangements, the Company and Shaanxi

HGS hold all the variable interests of Guangsha, and the Company and Shaanxi HGS

have been determined to be the most closely associated with

Guangsha. Therefore, our Company is the primary beneficiary of

Guangsha.

Based on

these contractual arrangements, we believe that Guangsha should be considered as

Variable Interest Entity (“VIE”) under ASC 810 “Consolidation of Variable

Interest Entities, an Interpretation of ARB No. 51,” because the equity

investors in Guangsha no longer has the characteristics of a controlling

financial interest and the Company through Shaanxi HGS is the primary

beneficiary of Guangsha. Accordingly, management believes that

Guangsha should be consolidated under ASC 810.

Our

Company, along with our subsidiaries and VIE, is now engaging in real estate

development, primarily in the construction and sale of residential apartments,

car parks as well as commercial properties.

Our

Current Organizational Structure

The

following chart reflects our current organizational structure:

19

Our

Markets

We

currently operate in three local markets in Shaanxi Province — downtown area of

Hanzhong, city of Weinan, and Yang county in Hanzhong City.

The

following table sets forth our projects and the total Gross Floor Area (“GFA”)

in each location indicated as of December 31, 2009:

|

Yangzhou

Pearl Garden

|

Mingzhu

Qinju

|

Mingzhu

Garden

|

||||||||||

|

Properties

under construction(1)

|

144,049 | 42,476 | 93,209 | |||||||||

|

Properties

under planning(1)

|

113,034 | N/A | 26,705 | |||||||||

|

Completed

projects(1)

|

53,865 | N/A | 28,666 | |||||||||

|

Total

number of projects

|

3 | 2 | 3 | |||||||||

|

Total

GFA* (square

meters)

(1)(2)

|

310,948 | 42,476 | 148,580 | |||||||||

(1) Calculated by square

meters (1 square meter = 10.7 square feet).

(2) The amounts for ‘‘Total

GFA’’ in this table and elsewhere in this statement are the amounts of total

saleable residential GFA and are derived on the following basis:

|

·

|

for

properties that are sold, the stated GFA is based on the sales contracts

relating to such property;

|

|

·

|

for

unsold properties that are completed or under construction, the stated GFA

is calculated based on the detailed construction blueprint and the

calculation method approved by the PRC government for saleable GFA, after

necessary adjustments; and

|

|

·

|

for

properties that are under planning, the stated GFA is based on the land

grant contract and our internal

projection.

|

We intend

to seek attractive opportunities to expand into additional Tier 2 cities and

counties. Our selections are based on certain criteria, including

economic growth, per capita income, population, urbanization rate as well as

availability of suitable land supply and local residential property market

conditions.

Suppliers

In China,

the supply of land is controlled by the government. Since early

2000s, the real estate industry in China has been transitioning from an arranged

system controlled by the PRC government to a more market-oriented

system. At present, although the Chinese government still owns all

urban land in China, the land use rights with terms up to 70 years can be

granted to, and owned or leased by, private individuals and

companies. Generally, there are two ways the Company usually applies

to acquire the land use right.

|

·

|

Purchase

by auction held by the Land Consolidation and Rehabilitation Center;

and

|

|

·

|

Purchase

by auction held by court under bankruptcy

proceedings.

|

In 2005,

the Company acquired the land lease of a bankrupted company, Weinan Chemical

Company which covers an area of 80 acres. After the acquisition, the

Company started the construction of Lijing Garden Projects and finished all 3

projects of Lijing Garden in June 2008. In May 2008, the Company

successfully acquired a land lease covering 236 acres through bidding on an

auction held by the local Land Consolidation and Rehabilitation Center of Yang

County. After the acquisition, the Company started the construction

of Yangzhou Pearl Garden Projects on the acquired land lease, and as of December

31, 2009, most of the projects of Yangzhou Pearl Garden were still under

construction.

In July

2008, the Company acquired the land lease of another bankrupt company, Hanzhong

Energy Company which covers an area of 30 acres in Hanzhong

City. After the acquisition, the Company started the construction of

Mingzhu Qinju Garden Projects on the acquired land lease, and as of December 31,

2009, all projects of Qinju Garden were still under

construction. In 2009, the Company successfully acquired another

parcel of leased-land covering 180 acres through bidding on an auction held by

the local Land Consolidation and Rehabilitation Center of Hanzhong

City. After the acquisition, the Company started the construction of

Mingzhu Garden Projects on the acquired land lease, and as of December 31, 2009,

most of the projects of Mingzhu Garden were still under

construction.

20

All such

purchases of land are required to be reported to and authorized by the Xi’an

Bureau of Land and Natural Resources. As to the real estate project

design and construction services, the Company typically selects the lowest-cost

provider based on quality ensured through an open bidding

process. Such service providers are numerous in China and the Company

foresees no difficulties in securing alternative sources of services as

needed.

Competition

The real

estate industry in China is highly competitive. In Tier 2

cities that we focus on the markets are relatively more fragmented than

Tier I cities. We compete primarily with local and regional property

developers and an increasing number of large national property developers who

have also started to enter these markets. Competitive factors include