Attached files

Table of Contents

As filed with the Securities and Exchange Commission on January 22, 2010.

Registration No 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

RYERSON HOLDING CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 5051 | 26-1251524 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

2621 West 15th Place

Chicago, Illinois 60608

(773) 762-2121

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Terence R. Rogers

Chief Financial Officer

Ryerson Holding Corporation

2621 West 15th Place

Chicago, Illinois 60608

(773) 762-2121

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Cristopher Greer, Esq. | Jonathan A. Schaffzin, Esq. William J. Miller, Esq. | |

| Willkie Farr & Gallagher LLP 787 Seventh Avenue New York, New York 10019 (212) 728-8000 Facsimile: (212) 728-9214 |

Cahill Gordon & Reindel LLP 80 Pine Street New York, New York 10005 (212) 701-3000 Facsimile: (212) 269-5420 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer x | Smaller reporting company ¨ | |

| (Do not check if a smaller reporting company) |

| Title of Each Class of Securities To Be Registered | Proposed Maximum Aggregate Offering |

Amount of Registration Fee(3) | ||

| Common Stock, par value $0.01 per share |

$350,000,000 | $24,955 | ||

| (1) | Estimated solely for purposes of determining the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes shares of common stock which may be purchased by the underwriters to cover over-allotments, if any. See “Underwriting.” |

| (3) | Computed in accordance with Rule 457(o) under the Securities Act of 1933. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED , 2010

PRELIMINARY PROSPECTUS

Shares

Ryerson Holding Corporation

Common Stock

$ per share

We are selling shares of our common stock. We have granted the underwriters an option to purchase up to additional shares of common stock to cover over-allotments.

This is the initial public offering of our common stock. We currently expect the initial public offering price to be between $ and $ per share. We intend to apply to have the common stock listed on the New York Stock Exchange under the symbol “RYI.”

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 15.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||

| Public Offering Price |

$ | $ | ||||

| Underwriting Discount |

$ | $ | ||||

| Proceeds to Ryerson Holding Corporation (before expenses) |

$ | $ | ||||

The underwriters expect to deliver the shares to purchasers on or about , 2010.

The date of this prospectus is , 2010

Table of Contents

You should rely only on the information contained in this prospectus and any free writing prospectus we may specifically authorize to be delivered or made available to you. We have not, and the underwriters have not, authorized anyone to provide you with different information. We are not, and the underwriters are not, making an offer of these securities in any jurisdiction where the offer is not permitted. You should not assume that the information contained in this prospectus and any free writing prospectus we may specifically authorize to be delivered or made available to you is accurate as of any date other than the date on the front of this prospectus, regardless of its time of delivery or of any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

| Page | ||

| 1 | ||

| 15 | ||

| 26 | ||

| 27 | ||

| 28 | ||

| 29 | ||

| 30 | ||

| 31 | ||

| 32 | ||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

34 | |

| 53 | ||

| 69 | ||

| 73 | ||

| 81 | ||

| 83 | ||

| 84 | ||

| 87 | ||

| 94 | ||

| 96 | ||

| 98 | ||

| 103 | ||

| 103 | ||

| 104 | ||

| F-1 |

Until , 2010 (25 days after the date of this prospectus), all dealers that buy, sell or trade our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider before investing in our common stock. You should read the entire prospectus carefully together with our consolidated financial statements and the related notes appearing elsewhere in this prospectus before making an investment decision. This prospectus contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in such forward-looking statements as a result of certain factors, including those discussed in the “Risk Factors” and other sections of this prospectus.

Except as otherwise indicated herein or as the context otherwise requires, references in this prospectus to “Ryerson Holding,” “the Company,” “we,” “our,” and “us” refer to Ryerson Holding Corporation and its direct and indirect subsidiaries (including Ryerson Inc.). The term “Ryerson” refers to Ryerson Inc., a direct wholly owned subsidiary of Ryerson Holding, together with its subsidiaries on a consolidated basis. “Platinum” refers to Platinum Equity, LLC and its affiliated investment funds, certain of which are our principal stockholders, and “Platinum Advisors” refers to Platinum Equity Advisors, LLC. Unless the context otherwise requires, information in this prospectus identified as “as adjusted” gives effect to the Ryerson Holding Offering (as defined herein) and the use of proceeds therefrom, the Services Agreement Termination (as defined herein), the issuance of our common stock offered hereby, which we refer to as the “offering,” and the use of proceeds from the offering as provided herein.

Our Company

We are a leading North American processor and distributor of metals measured in terms of sales, with operations in the United States and Canada, as well as in China. We distribute and process various kinds of metals, including stainless and carbon steel and aluminum products. We are among the largest purchasers of metals in North America. In the twelve months ended September 30, 2009, we purchased approximately 1.7 million tons of materials from many suppliers throughout the world. We currently operate approximately 90 facilities across the United States and Canada and five facilities in growth markets in China. For the twelve months ended September 30, 2009, our net sales were approximately $3.4 billion, our net income was $(124.2) million and Adjusted EBITDA was $105.8 million. See note 5 in “—Summary Historical Consolidated Financial and Other Data” for a reconciliation of Adjusted EBITDA to net income.

Our service centers are strategically located to process and deliver the volumes of metal our customers demand. Due to our scale, we are able to process and distribute standardized products in large volumes while maintaining low operating costs. Our distribution capabilities include a fleet of tractors and trailers that are owned, leased or dedicated by third party carriers. With these capabilities, we are able to efficiently meet our customers’ just-in-time delivery demands.

We carry a full line of products in stainless steel, aluminum, carbon steel and alloy steels, and a limited line of nickel and red metals. These materials are inventoried in a number of shapes, including coils, sheets, rounds, hexagons, square and flat bars, plates, structurals and tubing. More than one-half of the materials we sell are processed. We use processing and fabricating techniques such as sawing, slitting, blanking, cutting to length, leveling, flame cutting, laser cutting, edge trimming, edge rolling, roll forming, tube manufacturing, polishing and shearing to process materials to specified thickness, length, width, shape and surface quality pursuant to specific customer orders. We also use third-party fabricators and processors to outsource certain processes to enhance our value-added services.

1

Table of Contents

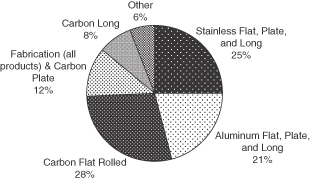

The following chart shows our percentage of sales by major product lines for the twelve months ended September 30, 2009.

We serve more than 40,000 customers across a wide range of end markets. For the twelve months ended September 30, 2009, no single customer accounted for more than 4% of our sales and our top 10 customers accounted for less than 16% of our sales. Our customer base ranges in size from large, national, original equipment manufacturers, to local independently owned fabricators and machine shops. Our geographic network and customization capabilities allow us to serve large, national manufacturing companies in North America by providing a consistent standard of products and services across multiple locations. Many of our facilities possess processing capabilities, which allow us to provide customized products and solutions to local customers on a smaller scale while maintaining just-in-time deliveries to our customers.

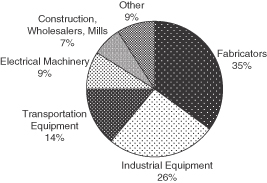

The following chart shows our percentage of sales by class of customers for 2009.

As part of securing customer orders, we also provide technical services to our customers to assure a cost effective material application while maintaining or improving the customers’ product quality. We have designed our services to reduce our customers’ costs by minimizing their investment in inventory and improving their production efficiency.

Since Platinum’s acquisition of Ryerson in October 2007, we have implemented numerous strategic initiatives aimed at reducing costs, improving working capital management, increasing efficiencies and enhancing liquidity. Our management team has decentralized our operations, improved inventory turns, rationalized facilities and reduced headcount. These changes have resulted in substantial permanent costs savings estimated at approximately $180 million annually and position Ryerson for improved profitability and future growth.

2

Table of Contents

Industry Outlook

The U.S. manufacturing sector continues to recover from the economic downturn. According to the Institute for Supply Management, the Purchasing Managers’ Index (“PMI”) rose to 55.9% in December 2009, marking the fifth consecutive month reading above 50%, which indicates that the manufacturing economy is generally expanding. We have seen an improving trend in our orders resulting from higher levels of manufacturing activities in the markets we serve. Furthermore, the overall U.S. economy is projected to resume growth in 2010 after the contraction in 2009. The U.S. Congressional Budget Office is forecasting GDP growth rates of 2.8%, 3.8% and 4.5% in 2010, 2011 and 2012, respectively. We believe any additional governmental economic stimulus programs will continue to hasten an economic recovery and that we would benefit from such recovery.

According to the Metals Service Centers Institute (“MSCI”), absolute total inventory levels of carbon and stainless steel at U.S. service centers reached a trough in August 2009 and were at the lowest levels since the data series began in 1977. Restocking activities, which indicate recovery in volume and end-user demand, have just started and are expected to be significant and protracted given the extended length of the recent destocking cycle. We believe that the industry’s months of supply (i.e., absolute inventories divided by shipments) will likely remain low as metals service centers maintain the discipline in their inventory management while volume recovers.

Metals prices have increased significantly from the trough levels in 2009. Based on data from Purchasing Magazine, market indexes on some of our products such as stainless cold rolled sheet, aluminum common alloy sheet and hot rolled carbon sheet have increased approximately 21%, 16% and 32%, respectively, in December 2009 from their low levels in the second quarter of 2009. In addition, certain metals producers have recently announced price increases for early 2010. As the economic recovery continues and demand returns despite volume still well below historical norms, we believe the rising metals prices are sustainable if producers remain disciplined in producing according to demand.

China continues to be a key driver in the growth of global metals demand. According to The Economist Intelligence Unit, China’s GDP is projected to grow at 9.3% in 2010 while CRU is forecasting Chinese steel consumption growth of 16.9% (hot-rolled sheet) in the same period. We have a significant and growing presence in China and are well positioned to benefit from the growth in this market.

We believe that our efficient operational platform, improved cost structure and flexible financial and liquidity position provide us with significant competitive advantages to benefit from the expected growth in the metals distribution industry. We also believe consolidation in the industry will continue as larger firms with financial flexibility, like ours, are able to expand into new geographies and markets through selective acquisitions.

Our Competitive Strengths

Leading Market Position with National Scale and a Strong International Presence.

According to Purchasing Magazine, we were the second largest metals service center in the United States and Canada in 2008, based on sales. We also believe we are the largest distributor of stainless steel, one of the two largest distributors of aluminum products, and one of the leading distributors of carbon flat roll, plate, bar and tubing products in the United States and Canada. For the twelve months ended September 30, 2009, we generated approximately $3.4 billion in net sales. We have a broad geographic presence with 90 locations in the United States and Canada, and we are also the only major North American service center with a significant presence in China. Our five Chinese service centers position us favorably in the largest metals market in the world.

3

Table of Contents

Our service centers are strategically located near our customer locations, enabling us to provide timely delivery to customers across numerous geographic markets. Additionally, our widespread network of locations in the United States, Canada and China utilize coordinated and consistent methodologies that allow us to target and serve customers with diverse supply chain requirements across multiple manufacturing locations. We believe our consistent network-wide operating structure, coupled with sales and customer service employees focused on the complex needs of these larger customers, provides a unique competitive advantage in serving these customers. Our ability to transfer inventory among our facilities better enables us to timely and profitably source specialized items at regional locations throughout our network than if we were required to maintain inventory of all products at each location.

Diverse Customer Base and Product Offerings.

We believe that our broad and diverse customer base provides a strong platform for growth in a recovering economy and helps protect us from regional and industry-specific downturns. We serve more than 40,000 customers across a diverse range of industries, including metals fabrication, industrial machinery, commercial transportation, electrical equipment and appliances and construction equipment. During the twelve months ended September 30, 2009, no single customer accounted for more than 4% of our sales, and our top 10 customers accounted for less than 16% of sales. Approximately 1,500 of our customers operate in multiple locations and our longstanding relationships with these customers provide us with stable demand and the ability to better manage profitability.

We carry a full range of products including stainless steel, aluminum, carbon steel and alloy steels and a limited line of nickel and red metals. In addition, we provide a broad range of processing and fabrication services such as sawing, slitting, blanking, cutting to length, leveling, flame cutting, laser cutting, edge trimming, edge rolling, roll forming, tube manufacturing, polishing and shearing to process materials to a specified thickness, length, width, shape and surface quality pursuant to specific customer orders. We also provide supply chain solutions, including just-in-time delivery, and value-added components to many original equipment manufacturers.

Transformed Operating and Cost Structure since Platinum Acquisition.

Since the October 2007 acquisition by Platinum, we have reduced our annual costs by approximately $280 million, of which we believe approximately $180 million are permanent. These organizational and operating changes were aimed at improving our operating structure, working capital management, efficiency and liquidity. Our senior management team has been instrumental in designing and implementing these changes and continues to evaluate incremental opportunities for cost savings. Specific completed initiatives include:

| • | Decentralized operations. We decentralized our operations by transitioning most corporate functions from our Chicago headquarters to five regional field offices. The decentralization process improved our customer responsiveness by moving key commercial support functions such as procurement, credit and operations support closer to our field operations. We have implemented a series of reporting, management and control processes related to sales processes, purchasing, expense management, inventory and credit to manage risk, maintain advantages of scale and share best practices. |

| • | Facility rationalization. We closed a total of 14 redundant or underperforming facilities in North America, while still maintaining the ability to service our markets and customers. Net of new facilities opened over the past year, we have reduced our warehouse space by approximately 1.7 million sq ft to 8.3 million sq ft at September 30, 2009. |

| • | Headcount reduction. We have reduced our North American headcount from 5,203 at October 19, 2007 to 3,549 at November 30, 2009. This process was achieved through the previously mentioned facility rationalization initiative as well as decentralization, which facilitated a significant reduction in total corporate overhead by eliminating or downsizing duplicative or extraneous layers of management. |

4

Table of Contents

| • | Improved inventory management. We have focused on process improvements in inventory management. Our inventory days improved from 106 days in the second quarter of 2007 to 78 days in the third quarter of 2009. We transferred many key decision making processes from headquarters to regional managers involved in day-to-day operations. We also enhanced our inventory reporting capabilities to provide more timely and detailed information, which allows senior management to more closely monitor inventory data and quickly address any potential issues that may arise. We believe this change in philosophy has resulted in a permanent improvement in inventory management. |

While some of the approximately $280 million of cost reductions are the result of volume declines and temporary expense actions, we believe that approximately $180 million of the cost reductions represent a permanent annual reduction to our fixed cost structure. We believe this will provide substantial improvement in earnings in a rising volume environment. As a result of these initiatives, we believe that we now have a more favorable cost structure compared to many of our peers. This low-cost advantage enhances our financial flexibility and positions us more strongly at all points in the cycle.

Experienced Management Team Driving a New Operating Philosophy.

Our senior management team has extensive industry and operational experience and has been instrumental in optimizing and implementing our transformation since Platinum’s acquisition of Ryerson. All of these managers, with the exception of one, were previously with us and were appointed to their current posts after Platinum’s acquisition of Ryerson. These senior managers have an average of more than 20 years of experience in the metals or service center industries and approximately 20 years with Ryerson or its predecessors. Senior management has successfully managed Ryerson through past market cycles and is uniquely positioned to manage Ryerson successfully going forward.

Broad-Based Platform for Growth.

We believe we are well-positioned to grow sales and improve profitability. While the service center industry is expected to benefit from improving general economic conditions, we expect several end-markets where we have meaningful exposure (including the heavy and medium truck/transportation, machinery, industrial equipment and appliance sectors) will likely experience stronger shipment growth in the coming years compared to overall industrial growth. In addition, a number of our other characteristics will enhance our growth.

| • | Improved sales force and strategy. We have upgraded the talent level of our sales force and are also utilizing new sales practices in order to both gain new customers and increase sales to existing customers. We have also begun to target the Mexican market through a focused sales strategy. |

| • | Extensive national network. Our leading position and extensive national facility network provides insight into nearly all domestic metals-consuming markets. This knowledge allows us to evaluate and target certain markets for expansion where we can service customers more profitably and increase market share. Since 2008, we have opened new facilities in Utah, Texas, Ohio and California and are currently evaluating several other areas for expansion. |

| • | Presence in China. We are the only major domestic service center with a significant presence in China. The Chinese market has historically grown at much higher rates compared to other major metals-consuming regions and this above-average growth is expected to continue. In 2009, our majority-owned Chinese operation opened a fifth location and we continue to evaluate additional growth opportunities in this market. |

| • | Positioned for consolidation. We believe that given our size, diversity and operating expertise, complemented by our relationship with Platinum, we can more easily identify and complete accretive acquisitions in a disciplined manner. We believe we are extremely well-positioned to capitalize on the expected increase in consolidation activity in the highly-fragmented metals service center sector. |

5

Table of Contents

Strong Relationships with Suppliers.

We are strategically aligned with high quality suppliers and also opportunistically take advantage of purchasing opportunities abroad. We believe that we are frequently one of the largest customers of our suppliers and that concentrating our orders among a core group of suppliers is an effective method for obtaining favorable pricing and service. Suppliers worldwide are consolidating and large, geographically diversified customers, such as Ryerson, are desirable partners for these larger suppliers.

Our Strategy

Achieve Organic Growth.

To achieve organic sales growth, we are focused on increasing our sales to existing customers as well as expanding our customer base. We expect to continue to increase sales and shipments through a variety of sales initiatives and by targeting attractive markets.

| • | Multiple sales initiatives. We have increased the size and upgraded the talent base of our North American sales force and adjusted our incentive plans consistent with our growth goals. We have also renewed our focus on increasing sales to transactional customers. In order to execute this strategy, we have improved our inventory profile by region, increased proactive sales practices, improved customer responsiveness and enhanced delivery capability. We believe the regional structure will facilitate quicker decision making to allow us to react more quickly to rapid changes in market conditions that drive the transactional business. |

| • | Global Account sales program. Our global account sales program, which targets those customers that are considering consolidating suppliers or outsourcing supply chain management, currently accounts for approximately 20% of annual sales and provides opportunities to increase sales to existing customers and also attract new customers. This group can manage the requirements of customers across our geographic footprint and represents a competitive advantage that allows us to reach large, multi-location customers in North America and globally through a single point of contact. |

| • | Greenfield expansion in attractive markets. While we have been consolidating redundant or underperforming facilities since the Platinum acquisition, we have also opened facilities in several new regions in the United States, including Utah, Texas, Ohio and California, where we saw an opportunity for Ryerson to open locations previously serviced from facilities further away. We are evaluating additional expansion opportunities and expect to continue selective expansion in the future. |

| • | Continued growth in international markets. We are focused on growing our business in international markets. We are enhancing the size and quality of the sales talent in our operations in China and are pursuing more value-added processing with higher margins, as well as broadening our product line. In addition, our Chinese operation opened a fifth location in 2009 in Wuhan; we are favorably positioned to add additional locations and identify possible acquisitions. Additionally, we are planning to leverage our capabilities in China to deliver products and services to our North American customers. |

We are also currently pursuing sales into the Mexican market through our locations serving customers along the U.S.-Mexico border and plan to further penetrate the Mexican market beyond our customer base along the border.

Pursue Value-Accretive Acquisitions.

The metals service center industry is highly fragmented and we believe our significant geographic presence provides a strong platform to capitalize on this fragmentation through acquisitions. Acquisitions provide various opportunities for value creation including increased sourcing opportunities, entry into new markets, cross-selling opportunities and enhanced distribution capability.

6

Table of Contents

Ryerson and Platinum have significant experience and a proven track record of identifying and executing on value-accretive acquisitions of metals service center companies. We continually evaluate potential acquisitions of service center companies, including joint venture opportunities, to complement our existing customer base and product offerings. We plan to continue to pursue our disciplined approach to acquisitions.

Continue to Improve Our Operating Efficiencies.

We are committed to improving our operating capabilities through continuous business improvements and cost reductions. We have established a field operations council that continually benchmarks and evaluates our operating cost structure and looks for opportunities to increase our operating leverage through expense improvements. In 2009, this group executed over 200 projects that, in combination, reduced annual costs by approximately $20 million. Improvements were in a variety of areas including worker compensation claims, transportation costs and maintenance expense. The group is currently working on over 100 new projects that are expected to result in additional savings in 2010 and beyond.

Expand Our Product and Service Offerings.

We are expanding revenue opportunities through downstream integration and conversion of commodity business into non-commodity, value-added processes such as first stage manufacturing and other fabrication processes. Additionally, we have assumed for certain customers the management and responsibility for complex supply chains involving numerous suppliers, fabricators and processors. During the twelve months ended September 30, 2009, we generated approximately $315 million of revenue from our fabrication and supply chain operations. We currently have strong relationships with many customers and business partners for whom we handle fabrication processes and we have established a group of experienced managers dedicated to expanding this business.

Additionally, in order to enhance our ability to compete more effectively in our long products segment, we have established regional product inventory depots to provide a broad line of stainless, aluminum, carbon and alloy long products as well as the necessary processing equipment to meet demanding requirements of these customers.

Maintain Flexible Capital Structure and Strong Liquidity Profile.

We reduced our debt by $591 million between December 31, 2007 and September 30, 2009, representing a reduction of 48% from our outstanding debt balance as of December 31, 2007. We maintained combined availability and cash-on-hand in excess of $300 million throughout the economic downturn. Availability under Ryerson’s five-year senior secured asset-based revolving credit facility with Bank of America, N.A. as administrative agent (the “Ryerson Credit Facility”) at September 30, 2009 was approximately $323 million. Our management team is focused on maintaining a strong level of liquidity while executing our various growth strategies and maintaining the flexibility to act opportunistically on acquisitions. We believe that our flexible capital structure and strong liquidity profile position us for growth in an improving market environment and give us the financial flexibility to continue paying down debt, reinvest in our business, and pursue our growth strategy.

Risk Factors

An investment in our common stock is subject to substantial risks and uncertainties. Before investing in our common stock, you should carefully consider the following, as well as the more detailed discussion of risk factors and other information included in this prospectus:

| • | the economic downturn has reduced both demand for our products and metals prices; |

7

Table of Contents

| • | the global financial and banking crises have caused a lack of credit availability that has limited and may continue to limit the ability of our customers to purchase our products or to pay us in a timely manner; |

| • | the metals distribution business is very competitive and increased competition could reduce our gross margins and net income; |

| • | we may not be able to sustain the annual cost savings realized as part of our recent cost reduction initiatives; and |

| • | we may not be able to successfully consummate and complete the integration of future acquisitions, and if we are unable to do so, we may be unable to increase our growth rates. |

Recent Developments

Ryerson Holding Offering

On January 21, 2010, we commenced an offering (the “Ryerson Holding Offering”) of Senior Discount Notes due 2015 that is expected to generate gross proceeds of approximately $200 million (the “Ryerson Holding Notes”). The Ryerson Holding Notes are being offered and sold (a) to “qualified institutional buyers” (as defined in Rule 144A under the Securities Act of 1933, as amended (the “Securities Act”)) and (b) outside the United States to non-U.S. persons in compliance with Regulation S under the Securities Act. We expect the Ryerson Holding Offering to close in the first quarter of 2010 and expect to use the proceeds from the issuance of the Ryerson Holding Notes to: (i) pay a cash dividend to our stockholders and (ii) pay fees in connection with the Ryerson Holding Offering and related expenses. We intend to use the net proceeds from the sale of shares of our common stock offered pursuant to this prospectus to redeem in full the Ryerson Holding Notes, plus pay accrued and unpaid interest and additional interest, if any, to the date of redemption and with respect to 50% of any remaining net proceeds following the redemption, subject to certain exceptions, to make an offer to repurchase Ryerson Inc.’s Floating Rate Senior Secured Notes due 2014 and 12% Senior Secured Notes due 2015 at par. This prospectus is not an offer to purchase, a solicitation of an offer to purchase or a solicitation of a consent with respect to the Ryerson Holding Notes. See “Use of Proceeds.”

Recent Acquisition

On September 16, 2009, Joseph T. Ryerson & Son, Inc. (“JT Ryerson”), one of our subsidiaries, entered into a Common Stock Purchase Agreement, pursuant to which JT Ryerson would acquire all of the issued and outstanding capital stock of a carbon and alloy steel service center, based in Texas, specializing in plate processing with plasma/flame cutting technology. The target reported net sales of approximately $40.8 million and gross profit of approximately $7.3 million in fiscal year 2008. Pursuant to the terms of the purchase agreement, JT Ryerson will pay an aggregate purchase price of approximately $11.6 million in connection with the acquisition. We expect the transaction to close by the end of January 2010. We intend to fund the purchase price for the acquisition with borrowings under the Ryerson Credit Facility.

The Sponsor

Platinum is a global acquisition firm headquartered in Beverly Hills, California with principal offices in Boston, New York and London. Since its founding in 1995, Platinum has acquired more than 90 businesses in a broad range of market sectors including technology, industrials, logistics, distribution, maintenance and service. Platinum’s current portfolio includes 30 companies with customers in more than 100 countries worldwide. The firm has a diversified capital base that includes the assets of its portfolio companies, which generated more than $11 billion in revenue in 2008, as well as capital commitments from institutional investors in private equity funds

8

Table of Contents

managed by the firm. Platinum’s M&A&O® approach to investing focuses on acquiring businesses that need operational support to realize their full potential and can benefit from Platinum’s expertise in transition, integration and operations.

JT Ryerson, one of our subsidiaries, is party to a corporate advisory services agreement (the “Services Agreement”) with Platinum Advisors, an affiliate of Platinum. In connection with this offering, Platinum Advisors and JT Ryerson intend to terminate the Services Agreement, pursuant to which JT Ryerson will pay Platinum Advisors $ million as consideration for terminating the monitoring fee payable thereunder. We refer to this as the “Services Agreement Termination.” See “Certain Relationships and Related Party Transactions—Services Agreement.”

Corporate Structure

Our current corporate structure is made up as follows: Ryerson Holding, the issuer of the common stock offered hereby, owns all of the common stock of Ryerson Inc. and all of the membership interests of Rhombus JV Holdings, LLC. Ryerson Inc. owns, directly or indirectly, all of the common stock of the following entities: JT Ryerson; Ryerson Americas, Inc.; Ryerson International, Inc.; Ryerson Pan-Pacific LLC; J.M. Tull Metals Company, Inc.; RdM Holdings, Inc.; RCJV Holdings, Inc.; Ryerson Procurement Corporation; Ryerson International Material Management Services, Inc.; Ryerson International Trading, Inc.; Ryerson (China) Limited; Ryerson Canada, Inc.; 862809 Ontario, Inc.; Leets Assurance, Ltd.; Integris Metals Mexicana, S.A. de C.V.; Servicios Empresariales Ryerson Tull, S.A. de C.V.; Servicios Corporativos RIM, S.A. de C.V.; and Ryerson Holdings (India) Pte Ltd. Platinum owns 99% of the capital stock of Ryerson Holding.

Corporate Information

Ryerson Holding and Ryerson Inc. are each incorporated under the laws of the State of Delaware. Ryerson Holding was formed in July 2007. Our principal executive offices are located at 2621 West 15th Place, Chicago, Illinois 60608. Our telephone number is (773) 762-2121.

On January 1, 2006, Ryerson Inc. changed its name from Ryerson Tull, Inc. to Ryerson Inc. On January 4, 2010, Ryerson Holding changed its name from Rhombus Holding Corporation to Ryerson Holding Corporation. Ryerson Inc.’s website is located at www.ryerson.com. Ryerson Inc.’s website and the information contained on the website or connected thereto will not be deemed to be incorporated into this prospectus and you should not rely on any such information in making your decision whether to purchase our securities.

9

Table of Contents

The Offering

| Issuer |

Ryerson Holding Corporation. |

| Common stock offered by us |

shares. |

| Underwriters’ over-allotment option to purchase additional common stock from us |

Up to shares. |

| Common stock outstanding before this offering |

shares. |

| Common stock to be outstanding immediately following this offering |

shares. |

| Use of proceeds |

We estimate that our net proceeds from this offering will be approximately $ million. |

We intend to use the net proceeds from the sale of shares of our common stock offered pursuant to this prospectus and the net proceeds from the exercise, if any, of the underwriters’ over-allotment option (i) to redeem in full the Ryerson Holding Notes, plus pay accrued and unpaid interest and additional interest, if any, up to, but not including, the redemption date, (ii) with respect to 50% of any remaining net proceeds following the redemption described in clause (i), subject to certain exceptions, to make an offer to purchase Ryerson Inc.’s Floating Rate Senior Secured Notes due 2014 and 12% Senior Secured Notes due 2015 at par, (iii) to repay approximately $ million of our outstanding indebtedness under the Ryerson Credit Facility and (iv) to pay related fees and expenses. See “Use of Proceeds.”

This prospectus is not an offer to purchase, a solicitation of an offer to purchase or a solicitation of a consent with respect to the Ryerson Holding Notes.

| Risk factors |

See “Risk Factors” on page 15 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

| Dividend policy |

We do not anticipate declaring or paying any regular cash dividends on our common stock in the foreseeable future. Any payment of cash dividends on our common stock in the future will be at the discretion of our Board of Directors and will depend upon our results of operations, earnings, capital requirements, financial condition, future prospects, contractual restrictions, including under the Ryerson Credit Facility and our secured notes, and other factors deemed relevant by our Board of Directors. |

| Proposed New York Stock Exchange symbol |

“RYI.” |

10

Table of Contents

The number of shares to be outstanding after this offering is based on shares of common stock outstanding as of , 2010 and the shares of common stock being sold by us in this offering, and assumes no exercise by the underwriters of their option to purchase shares of our common stock in this offering to cover over-allotments, if any.

Unless we specifically state otherwise, the information in this prospectus assumes:

| • | an initial public offering price of $ per share, the mid-point of the offering range set forth on the cover page of this prospectus; and |

| • | the underwriters do not exercise their over-allotment option. |

11

Table of Contents

Summary Historical Consolidated Financial and Other Data

The following table presents our summary historical consolidated financial data, as of the dates and for the periods indicated. The summary historical consolidated statements of operations data of Ryerson Inc. as predecessor for the year ended December 31, 2006 and for the period from January 1, 2007 through October 19, 2007 and of Ryerson Holding as successor for the period from October 20, 2007 to December 31, 2007 and for the year ended December 31, 2008 and the summary historical balance sheet data as of December 31, 2007 and 2008 have been derived from our audited consolidated financial statements included elsewhere in this prospectus.

Our summary historical consolidated financial data as of September 30, 2009 and for the nine months ended September 30, 2008 and 2009 have been derived from our unaudited consolidated financial statements included elsewhere in this prospectus. The September 30, 2008 and 2009 unaudited financial statements have been prepared on a basis consistent with our audited consolidated financial statements and reflect all adjustments, consisting of normal recurring adjustments that are, in the opinion of management, necessary for a fair presentation of the financial position and results of operations for the periods presented. The results of any interim period are not necessarily indicative of the results that may be expected for any other interim period or for the full fiscal year, and the historical results set forth below do not necessarily indicate results expected for any future period.

You should read the summary financial and other data set forth below along with the sections in this prospectus entitled “Use of Proceeds,” “Selected Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and related notes included elsewhere in this prospectus.

| Predecessor | Successor | |||||||||||||||||||||||||

| Year Ended December 31, 2006 |

Period from January 1 to October 19, 2007 |

Period from October 20 to December 31, 2007 |

Year Ended December 31, 2008 |

Nine Months Ended September 30, |

||||||||||||||||||||||

| 2008 | 2009 | |||||||||||||||||||||||||

| ($ in millions) | ||||||||||||||||||||||||||

| Statements of Operations Data: |

||||||||||||||||||||||||||

| Net sales |

$ | 5,908.9 | $ | 5,035.6 | $ | 966.3 | $ | 5,309.8 | $ | 4,236.9 | $ | 2,325.0 | ||||||||||||||

| Cost of materials sold |

5,050.9 | 4,307.1 | 829.1 | 4,596.9 | 3,696.6 | 1,961.5 | ||||||||||||||||||||

| Gross profit(1) |

858.0 | 728.5 | 137.2 | 712.9 | 540.3 | 363.5 | ||||||||||||||||||||

| Warehousing, selling, general and administrative |

691.2 | 569.5 | 126.9 | 586.1 | 449.4 | 362.5 | ||||||||||||||||||||

| Restructuring and plant closure costs |

4.5 | 5.1 | — | — | — | — | ||||||||||||||||||||

| Pension / post retirement curtailment gain |

— | — | — | — | — | (1.3 | ) | |||||||||||||||||||

| Gain on sale of assets |

(21.6 | ) | (7.2 | ) | — | — | — | (3.3 | ) | |||||||||||||||||

| Operating profit (loss) |

183.9 | 161.1 | 10.3 | 126.8 | 90.9 | 5.6 | ||||||||||||||||||||

| Other income and (expense), net(2) |

1.0 | (1.0 | ) | 2.4 | 29.2 | 12.8 | (8.6 | ) | ||||||||||||||||||

| Interest and other expense on debt(3) |

(70.7 | ) | (55.1 | ) | (30.8 | ) | (109.9 | ) | (82.7 | ) | (54.4 | ) | ||||||||||||||

| Income (loss) before income taxes |

114.2 | 105.0 | (18.1 | ) | 46.1 | 21.0 | (57.4 | ) | ||||||||||||||||||

| Provision (benefit) for income taxes(4) |

42.4 | 36.9 | (6.9 | ) | 14.8 | 7.2 | 86.6 | |||||||||||||||||||

| Net income (loss) |

71.8 | 68.1 | (11.2 | ) | 31.3 | 13.8 | (144.0 | ) | ||||||||||||||||||

| Less: Net income (loss) attributable to noncontrolling interest |

— | — | — | (1.2 | ) | — | (1.1 | ) | ||||||||||||||||||

| Net income (loss) attributable to Ryerson Holding. |

$ | 71.8 | $ | 68.1 | $ | (11.2 | ) | $ | 32.5 | $ | 13.8 | $ | (142.9 | ) | ||||||||||||

12

Table of Contents

| Predecessor | Successor | |||||||||||||||||||||||||

| Year Ended December 31, 2006 |

Period from January 1 to October 19, 2007 |

Period from October 20 to December 31, 2007 |

Year Ended December 31, 2008 |

Nine Months Ended September 30, |

||||||||||||||||||||||

| 2008 | 2009 | |||||||||||||||||||||||||

| ($ in millions, except per share data) | ||||||||||||||||||||||||||

| Earnings (loss) per share of common stock: |

||||||||||||||||||||||||||

| Basic earnings (loss) per share |

$ | 2.75 | $ | 2.56 | $ | (2.24 | ) | $ | 6.50 | $ | 2.76 | $ | (28.58 | ) | ||||||||||||

| Diluted earnings (loss) per share |

$ | 2.50 | $ | 2.19 | $ | (2.24 | ) | $ | 6.50 | $ | 2.76 | $ | (28.58 | ) | ||||||||||||

| Weighted average shares outstanding — Basic (in millions) |

26.1 | 26.5 | 5.0 | 5.0 | 5.0 | 5.0 | ||||||||||||||||||||

| Weighted average shares outstanding — Diluted (in millions) |

28.7 | 31.1 | 5.0 | 5.0 | 5.0 | 5.0 | ||||||||||||||||||||

| Balance Sheet Data (at period end): |

||||||||||||||||||||||||||

| Cash and cash equivalents |

$ | 55.1 | $ | 35.2 | $ | 130.4 | $ | 88.1 | $ | 43.3 | ||||||||||||||||

| Restricted cash |

0.1 | 4.5 | 7.0 | 1.8 | 6.9 | |||||||||||||||||||||

| Inventory |

1,128.6 | 1,069.7 | 819.5 | 985.8 | 639.9 | |||||||||||||||||||||

| Working capital |

1,420.1 | 1,235.7 | 1,084.2 | 1,308.5 | 691.2 | |||||||||||||||||||||

| Property, plant and equipment, net |

401.1 | 587.0 | 547.7 | 543.2 | 524.6 | |||||||||||||||||||||

| Total assets |

2,537.3 | 2,576.5 | 2,281.9 | 2,620.9 | 1,761.8 | |||||||||||||||||||||

| Long-term debt, including current maturities |

1,206.5 | 1,228.8 | 1,030.3 | 1,242.8 | 637.7 | |||||||||||||||||||||

| Other Financial Data: |

||||||||||||||||||||||||||

| Cash flows provided (used in) operations |

$ | (261.0 | ) | $ | 564.0 | $ | 54.1 | $ | 280.5 | $ | (5.5 | ) | $ | 302.6 | ||||||||||||

| Cash flows provided (used in) investing activities |

(16.7 | ) | (24.0 | ) | (1,069.6 | ) | 19.3 | 19.3 | 47.1 | |||||||||||||||||

| Cash flows provided (used in) financing activities |

305.4 | (565.6 | ) | 1,021.2 | (197.0 | ) | 40.6 | (444.5 | ) | |||||||||||||||||

| Capital expenditures |

35.7 | 51.6 | 9.1 | 30.1 | 20.3 | 16.8 | ||||||||||||||||||||

| Depreciation and amortization |

40.0 | 32.5 | 7.3 | 37.6 | 26.9 | 32.4 | ||||||||||||||||||||

| EBITDA(5) |

224.9 | 192.6 | 20.0 | 194.8 | 130.6 | 30.5 | ||||||||||||||||||||

| Adjusted EBITDA(5) |

— | — | — | 185.9 | 131.1 | 51.0 | ||||||||||||||||||||

| Adjusted EBITDA, excluding LIFO(5) |

— | — | — | 277.4 | 307.2 | (153.2 | ) | |||||||||||||||||||

| Ratio of Tangible Assets to Total Net Debt(6) |

1.9x | — | 1.9x | 2.1x | 2.0x | 2.6x | ||||||||||||||||||||

| Other Operating Data: |

||||||||||||||||||||||||||

| Tons shipped (000) |

3,292 | 2,535 | 498 | 2,505 | 1,999 | 1,435 | ||||||||||||||||||||

| Average number of employees |

5,701 | 5,430 | 5,185 | 4,663 | 4,709 | 4,239 | ||||||||||||||||||||

| Tons shipped per employee |

577 | 467 | 96 | 537 | 424 | 339 | ||||||||||||||||||||

| Average selling price per ton |

$ | 1,795 | $ | 1,987 | $ | 1,939 | $ | 2,120 | $ | 2,120 | $ | 1,620 | ||||||||||||||

| Gross profit per ton |

261 | 287 | 275 | 284 | 270 | 253 | ||||||||||||||||||||

| Operating profit per ton |

56 | 63 | 21 | 51 | 45 | 4 | ||||||||||||||||||||

| (1) | The period from January 1, 2007 to October 19, 2007 includes a LIFO liquidation gain of $69.5 million, or $42.3 million after-tax. |

| (2) | The year ended December 31, 2008 included a $18.2 million gain on the retirement of debt as well as a $6.7 million gain on the sale of corporate bonds. The nine months ended September 30, 2008 included a $2.8 million gain on the retirement of debt as well as a $6.7 million gain on the sale of corporate bonds. The nine months ended September 30, 2009 included $10.1 million of foreign exchange losses related to short-term loans from our Canadian operations, offset by the recognition of a $2.7 million gain on the retirement of debt. |

| (3) | The period from January 1 to October 19, 2007 includes a $2.9 million write off of unamortized debt issuance costs associated with the 2024 Notes that was classified as short term debt and $2.7 million write off of debt issuance costs associated with our prior credit facility upon entering into an amended revolving credit facility relating to that facility during the first quarter of 2007. |

| (4) | The period from January 1 to October 19, 2007 includes a $3.9 million income tax benefit as a result of a favorable settlement from an Internal Revenue Service examination. |

| (5) | EBITDA, for the period presented below, represents net income before interest and other expense on debt, provision for income taxes, depreciation and amortization. Adjusted EBITDA gives further effect to, among other things, gain on the sale of assets, reorganization expenses and the payment of management fees. We believe that EBITDA and Adjusted EBITDA provide additional information for measuring our performance and are measures frequently used by securities analysts and investors. EBITDA and Adjusted EBITDA do not represent, and should not be used as a substitute for, net income or cash flows from operations as determined in accordance with generally accepted accounting principles, and |

13

Table of Contents

| neither EBITDA nor Adjusted EBITDA is necessarily an indication of whether cash flow will be sufficient to fund our cash requirements. Our definitions of EBITDA and Adjusted EBITDA may differ from that of other companies. Set forth below is the reconciliation of net income to EBITDA, as further adjusted to Adjusted EBITDA and Adjusted EBITDA, excluding LIFO. |

| Predecessor | Successor | |||||||||||||||||||||||

| Year Ended December 31, 2006 |

Period from January 1 to October 19, 2007 |

Period from October 20 to December 31, 2007 |

Year Ended December 31, 2008 |

Nine Months Ended September 30, |

||||||||||||||||||||

| 2008 | 2009 | |||||||||||||||||||||||

| ($ in millions) |

||||||||||||||||||||||||

| Net income (loss) attributable to Ryerson Holding |

$ | 71.8 | $ | 68.1 | $ | (11.2 | ) | $ | 32.5 | $ | 13.8 | $ | (142.9 | ) | ||||||||||

| Interest and other expense on debt |

70.7 | 55.1 | 30.8 | 109.9 | 82.7 | 54.4 | ||||||||||||||||||

| Provision (benefit) for income taxes |

42.4 | 36.9 | (6.9 | ) | 14.8 | 7.2 | 86.6 | |||||||||||||||||

| Depreciation and amortization |

40.0 | 32.5 | 7.3 | 37.6 | 26.9 | 32.4 | ||||||||||||||||||

| EBITDA |

$ | 224.9 | $ | 192.6 | $ | 20.0 | $ | 194.8 | $ | 130.6 | $ | 30.5 | ||||||||||||

| Gain on sale of assets |

— | — | (3.3 | ) | ||||||||||||||||||||

| Reorganization |

15.3 | 9.5 | 11.4 | |||||||||||||||||||||

| Platinum management fees |

5.0 | 3.8 | 3.8 | |||||||||||||||||||||

| Foreign currency transaction (gains) losses |

(1.0 | ) | (1.0 | ) | 10.9 | |||||||||||||||||||

| Debt retirement gains |

(18.2 | ) | (2.8 | ) | (2.7 | ) | ||||||||||||||||||

| Gain on bond investment sale |

(6.7 | ) | (6.7 | ) | — | |||||||||||||||||||

| Other adjustments |

(3.3 | ) | (2.3 | ) | 0.4 | |||||||||||||||||||

| Adjusted EBITDA |

185.9 | 131.1 | 51.0 | |||||||||||||||||||||

| LIFO expense (income) |

91.5 | 176.1 | (204.2 | ) | ||||||||||||||||||||

| Adjusted EBITDA, excluding LIFO expense (income) |

$ | 277.4 | $ | 307.2 | $ | (153.2 | ) | |||||||||||||||||

| (6) | Tangible Assets are defined as accounts receivable, inventories and property, plant and equipment, net of any reserves and of accumulated depreciation. |

14

Table of Contents

Investing in our common stock involves a high degree of risk. You should carefully consider the risks described below, together with the other information contained in this prospectus, before making your decision to invest in shares of our common stock. The risks and uncertainties described below are not the only ones facing our company. Additional risks and uncertainties not presently known to us, or that we currently deem immaterial, may also impair our business operations. We cannot assure you that any of the events discussed in the risk factors below will not occur. These risks could have a material and adverse impact on our business, results of operations, financial condition and cash flows. If that were to happen, the trading price of our common stock could decline, and you could lose all or part of your investment.

Risks Relating to Our Business

We service industries that are highly cyclical, and any downturn in our customers’ industries could reduce our sales and profitability. The economic downturn has reduced demand for our products and may continue to reduce demand until an economic recovery.

Many of our products are sold to industries that experience significant fluctuations in demand based on economic conditions, energy prices, seasonality, consumer demand and other factors beyond our control. These industries include manufacturing, electrical products and transportation. We do not expect the cyclical nature of our industry to change.

The U.S. economy entered an economic recession in December 2007, which spread to many global markets in 2008 and 2009 and affected Ryerson and other metals service centers. In late 2008 and 2009, the metals industry, including Ryerson and other service centers, felt additional effects of the worsening recession and the impact of the credit market disruption. These events contributed to a rapid decline in both demand for our products and pricing levels for those products. The Company has implemented or is taking a number of actions to conserve cash, reduce costs and strengthen its competitiveness, including curtailing non-critical capital expenditures, initiating headcount reductions and reductions of certain employee benefits, among other actions. However, there can be no assurance that these actions, or any others that the Company may take in response to further deterioration in economic and financial conditions, will be sufficient.

The global financial and banking crises have caused a lack of credit availability that has limited and may continue to limit the ability of our customers to purchase our products or to pay us in a timely manner.

In climates of global financial and banking crises, such as those we are currently experiencing, the ability of our customers to maintain credit availability has become more challenging. In particular, the financial viability of many of our customers is threatened, which may impact their ability to pay us amounts due, further affecting our financial condition and results of operations.

The metals distribution business is very competitive and increased competition could reduce our gross margins and net income.

The principal markets that we serve are highly competitive. The metals distribution industry is fragmented and competitive, consisting of a large number of small companies and a few relatively large companies. Competition is based principally on price, service, quality, production capabilities, inventory availability and timely delivery. Competition in the various markets in which we participate comes from companies of various sizes, some of which have greater financial resources than we have and some of which have more established brand names in the local markets served by us. Increased competition could force us to lower our prices or to offer increased services at a higher cost, which could reduce our profitability.

15

Table of Contents

The economic downturn has reduced metals prices. Though prices have recently started rising, we cannot assure you that prices will continue to rise. Changing metals prices may have a significant impact on our liquidity, net sales, gross margins, operating income and net income.

The metals industry as a whole is cyclical and, at times, pricing and availability of metal can be volatile due to numerous factors beyond our control, including general domestic and international economic conditions, labor costs, sales levels, competition, levels of inventory held by other metals service centers, consolidation of metals producers, higher raw material costs for the producers of metals, import duties and tariffs and currency exchange rates. This volatility can significantly affect the availability and cost of materials for us.

We, like many other metals service centers, maintain substantial inventories of metal to accommodate the short lead times and just-in-time delivery requirements of our customers. Accordingly, we purchase metals in an effort to maintain our inventory at levels that we believe to be appropriate to satisfy the anticipated needs of our customers based upon historic buying practices, contracts with customers and market conditions. When metals prices decline, as they did in 2008 and 2009, customer demands for lower prices and our competitors’ responses to those demands could result in lower sale prices and, consequently, lower margins as we use existing metals inventory. Notwithstanding recent price increases, metals prices may decline in 2010, and declines in those prices or further reductions in sales volumes could adversely impact our ability to maintain our liquidity and to remain in compliance with certain financial covenants under the Ryerson Credit Facility, as well as result in us incurring inventory or goodwill impairment charges. Changing metals prices therefore could significantly impact our liquidity, net sales, gross margins, operating income and net income.

We have a substantial amount of indebtedness, which could adversely affect our financial position and prevent us from fulfilling our obligations under our notes.

We currently have a substantial amount of indebtedness. As of September 30, 2009, after giving effect to this offering and the application of net proceeds from this offering, our total indebtedness would have been approximately $ million and we would have had approximately $ million of unused capacity under Ryerson’s Credit Facility. Our substantial indebtedness may:

| • | make it difficult for us to satisfy our financial obligations, including making scheduled principal and interest payments on the notes and our other indebtedness; |

| • | limit our ability to borrow additional funds for working capital, capital expenditures, acquisitions and general corporate and other purposes; |

| • | limit our ability to use our cash flow or obtain additional financing for future working capital, capital expenditures, acquisitions or other general corporate purposes; |

| • | require us to use a substantial portion of our cash flow from operations to make debt service payments; |

| • | limit our flexibility to plan for, or react to, changes in our business and industry; |

| • | place us at a competitive disadvantage compared to our less leveraged competitors; and |

| • | increase our vulnerability to the impact of adverse economic and industry conditions. |

We may be able to incur substantial additional indebtedness in the future. The terms of the Ryerson Credit Facility and the indenture governing our notes restrict but do not prohibit us from doing so. If new indebtedness is added to our current debt levels, the related risks that we now face could intensify.

The covenants in Ryerson’s Credit Facility and the indenture governing our notes and Ryerson’s notes impose, and covenants contained in agreements governing indebtedness that we incur in the future may impose, restrictions that may limit our operating and financial flexibility.

Ryerson’s Credit Facility and the indenture governing the notes contain a number of significant restrictions and covenants that limit our ability and the ability of our restricted subsidiaries, including Ryerson Inc., to:

| • | incur additional debt; |

16

Table of Contents

| • | pay dividends on our capital stock or repurchase our capital stock; |

| • | make certain investments or other restricted payments; |

| • | create liens or use assets as security in other transactions; |

| • | merge, consolidate or transfer or dispose of substantially all of our assets; and |

| • | engage in transactions with affiliates. |

Additionally, our future indebtedness may contain covenants more restrictive in certain respects than the restrictions contained in the Ryerson Credit Facility and the indenture governing the notes. Operating results below current levels or other adverse factors, including a significant increase in interest rates, could result in our being unable to comply with financial covenants that are contained in the Ryerson Credit Facility or that may be contained in any future indebtedness. If our indebtedness is in default for any reason, our business, financial condition and results of operations could be materially and adversely affected. In addition, complying with these covenants may also cause us to take actions that are not favorable to holders of the notes and may make it more difficult for us to successfully execute our business strategy and compete against companies that are not subject to such restrictions.

We may not be able to generate sufficient cash to service all of our indebtedness.

Our ability to make payments on our indebtedness depends on our ability to generate cash in the future. Our outstanding notes, the Ryerson Credit Facility and our other outstanding indebtedness are expected to account for significant cash interest expenses. Accordingly, we will have to generate significant cash flows from operations to meet our debt service requirements. If we do not generate sufficient cash flow to meet our debt service and working capital requirements, we may be required to sell assets, seek additional capital, reduce capital expenditures, restructure or refinance all or a portion of our existing indebtedness, or seek additional financing. Moreover, insufficient cash flow may make it more difficult for us to obtain financing on terms that are acceptable to us, or at all. Furthermore, Platinum has no obligation to provide us with debt or equity financing and we therefore may be unable to generate sufficient cash to service all of our indebtedness.

Because a substantial portion of our indebtedness bears interest at rates that fluctuate with changes in certain prevailing short-term interest rates, we are vulnerable to interest rate increases.

A substantial portion of our indebtedness, including the Ryerson Credit Facility and the 2014 Notes, bears interest at rates that fluctuate with changes in certain short-term prevailing interest rates. As of September 30, 2009, Ryerson Holding’s subsidiaries had approximately $102.9 million of floating rate debt under the 2014 Notes and approximately $142.8 million of outstanding borrowings under the Ryerson Credit Facility, with an additional $323.0 million available for borrowing under such facility. Assuming a consistent level of debt, a 100 basis point change in the interest rate on our floating rate debt effective from the beginning of the year would increase or decrease our fiscal 2009 interest expense under the Ryerson Credit Facility and the 2014 Notes by approximately $2.5 million on an annual basis. We use derivative financial instruments to manage a portion of the potential impact of our interest rate risk. To some extent, derivative financial instruments can protect against increases in interest rates, but they do not provide complete protection over the long term. If interest rates increase dramatically, we could be unable to service our debt which could have a material adverse effect on our business, financial condition, results of operations or cash flows.

We may not be able to sustain the annual cost savings realized as part of our recent cost reduction initiatives.

Since 2007, we have implemented approximately $180 million of what we believe are permanent cost savings on an annualized basis. The cost savings have come primarily as a result of the following initiatives: decentralization of our operations, process improvements in inventory management, closure of under-performing

17

Table of Contents

facilities and reduction in our North American headcount. We may not be able to sustain all, or any part, of these cost savings on an annual basis in the future, which could have an adverse effect on our business, financial condition, results of operations and cash flows.

We may not be able to successfully consummate and complete the integration of future acquisitions, and if we are unable to do so, we may be unable to increase our growth rates.

We have grown through a combination of internal expansion, acquisitions and joint ventures. We intend to continue to grow through selective acquisitions, but we may not be able to identify appropriate acquisition candidates, obtain financing on satisfactory terms, consummate acquisitions or integrate acquired businesses effectively and profitably into our existing operations. Restrictions contained in the agreements governing our notes, the Ryerson Credit Facility or our other existing or future debt may also inhibit our ability to make certain investments, including acquisitions and participations in joint ventures.

Our future success will depend on our ability to complete the integration of these future acquisitions successfully into our operations. After any acquisition, customers may choose to diversify their supply chains to reduce reliance on a single supplier for a portion of their metals needs. We may not be able to retain all of our and an acquisition’s customers, which may adversely affect our business and sales. Integrating acquisitions, particularly large acquisitions, requires us to enhance our operational and financial systems and employ additional qualified personnel, management and financial resources, and may adversely affect our business by diverting management away from day-to-day operations. Further, failure to successfully integrate acquisitions may adversely affect our profitability by creating significant operating inefficiencies that could increase our operating expenses as a percentage of sales and reduce our operating income. In addition, we may not realize expected cost savings from acquisitions, which may also adversely affect our profitability.

We may not be able to retain or expand our customer base if the North American manufacturing industry continues to erode through moving offshore or through acquisition and merger or consolidation activity in our customers’ industries.

Our customer base primarily includes manufacturing and industrial firms. Some of our customers operate in industries that are undergoing consolidation through acquisition and merger activity; some are considering or have considered relocating production operations overseas or outsourcing particular functions overseas; and some customers have closed as they were unable to compete successfully with overseas competitors. Our facilities are predominately located in the United States and Canada. To the extent that our customers cease U.S. operations, relocate or move operations overseas to regions in which we do not have a presence, we could lose their business. Acquirers of manufacturing and industrial firms may have suppliers of choice that do not include us, which could impact our customer base and market share.

Certain of our operations are located outside of the United States, which subjects us to risks associated with international activities.

Certain of our operations are located outside of the United States, primarily in Canada and China. We are subject to the Foreign Corrupt Practices Act (“FCPA”), which generally prohibits U.S. companies and their intermediaries from making corrupt payments to foreign officials for the purpose of obtaining or keeping business or otherwise obtaining favorable treatment, and requires companies to maintain adequate record-keeping and internal accounting practices to accurately reflect the transactions of the company. The FCPA applies to companies, individual directors, officers, employees and agents. Under the FCPA, U.S. companies may be held liable for actions taken by strategic or local partners or representatives. If we or our intermediaries fail to comply with the requirements of the FCPA, governmental authorities in the United States could seek to impose civil and/or criminal penalties, which could have a material adverse effect on our business, operations, financial conditions and cash flows.

18

Table of Contents

Operating results may fluctuate depending on the season.

A portion of our customers experience seasonal slowdowns. Our sales in the months of July, November and December traditionally have been lower than in other months because of a reduced number of shipping days and holiday or vacation closures for some customers. Consequently, our sales in the first two quarters of the year are usually higher than in the third and fourth quarters.

Damage to our information technology infrastructure could harm our business.

The unavailability of any of our computer-based systems for any significant period of time could have a material adverse effect on our operations. In particular, our ability to manage inventory levels successfully largely depends on the efficient operation of our computer hardware and software systems. We use management information systems to track inventory information at individual facilities, communicate customer information and aggregate daily sales, margin and promotional information. Difficulties associated with upgrades, installations of major software or hardware, and integration with new systems could have a material adverse effect on results of operations. We will be required to expend substantial resources to integrate our information systems with the systems of companies we have acquired. The integration of these systems may disrupt our business or lead to operating inefficiencies. In addition, these systems are vulnerable to, among other things, damage or interruption from fire, flood, tornado and other natural disasters, power loss, computer system and network failures, operator negligence, physical and electronic loss of data, or security breaches and computer viruses.

Any significant work stoppages can harm our business.

As of September 30, 2009, we employed approximately 3,900 persons in North America and 400 persons in China. Our North American workforce was comprised of approximately 1,800 office employees and approximately 2,100 plant employees. Thirty-seven percent of our plant employees were members of various unions, including the United Steel Workers and the International Brotherhood of Teamsters unions. Our relationship with the various unions generally has been good. There have been two work stoppages at Integris Metals’ facilities over the last five years (both prior to Ryerson’s acquisition of Integris Metals): a strike by the members of the International Brotherhood of Teamsters Local #221, a union covering 69 individuals, which occurred at the Minneapolis (Integris) facility in June 2003 and lasted less than one month; and a strike by the members of the International Brotherhood of Teamsters Local #938, a union covering 81 individuals, at the Toronto (Integris) facility, which began on July 6, 2004, and ended when a settlement was reached on October 31, 2004. On January 31, 2006, the agreement with the joint United Steelworkers and the International Brotherhood of Teamsters unions, which represent approximately 540 employees at three Chicago area facilities, expired. The membership of the joint unions representing the Chicago-area employees initiated a week-long strike on March 6, 2006. On July 9, 2006, the joint United Steelworkers and Teamster unions representing the Chicago-area employees ratified a three-year collective bargaining agreement, lasting through March 31, 2009.

In 2007, we reached agreement on the renewal of 10 collective bargaining agreements covering 374 employees. Six collective bargaining agreements expired in 2008, a year in which we reached agreement on the renewal of four contracts covering 53 employees. Two contracts covering 52 employees were extended into 2009. We reached agreement in 2009 on one of the extended contracts covering 45 employees and the single remaining contract from 2008, covering approximately seven persons, remains on an extension. In addition, negotiations over a new collective bargaining agreement at a newly certified location employing four persons began in late 2008 and was concluded in 2009. Nine contracts covering 339 persons were scheduled to expire in 2009. We reached agreement on the renewal of eight contracts covering approximately 258 persons and one contract covering approximately 81 persons has been extended. Seven contracts are scheduled to expire in 2010 covering approximately 85 persons. We may not be able to negotiate extensions of these agreements or new agreements prior to their expiration date. As a result, we may experience additional labor disruptions in the future. A widespread work stoppage could have a material adverse effect on our results of operations, financial position and cash flows if it were to last for a significant period of time.

19

Table of Contents

Certain employee retirement benefit plans are underfunded and the actual cost of those benefits could exceed current estimates, which would require us to fund the shortfall.

As of December 31, 2008, our pension plan had an unfunded liability of $296 million. Our actual costs for benefits required to be paid may exceed those projected and future actuarial assessments of the extent of those costs may exceed the current assessment. Under those circumstances, the adjustments required to be made to our recorded liability for these benefits could have a material adverse effect on our results of operations and financial condition and cash payments to fund these plans could have a material adverse effect on our cash flows. We may be required to make substantial future contributions to improve the plan’s funded status, which may have a material adverse effect on our results of operations, financial condition or cash flows.

Future funding for postretirement employee benefits other than pensions also may require substantial payments from current cash flow.

We provide postretirement life insurance and medical benefits to approximately half of our employees. We paid approximately $12 million in postretirement benefits in 2008 and recorded an expense of approximately $16 million in our financial statements. Our unfunded postretirement benefit obligation as of December 31, 2008 was $194 million.