Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - DAKTRONICS INC /SD/ | a8kfy10needham.htm |

| EX-99.2 - EXHIBIT 99.2 NEWS RELEASE - DAKTRONICS INC /SD/ | ex99_2.htm |

Investor

Presentation

FY2010

Second Quarter

FY2010

Second Quarter

Cautionary

Notice

In addition to statements of fact, this presentation contains

forward-looking statements reflecting the company’s expectations or beliefs

concerning future events which could materially affect company performance in

the future. The company cautions that these and similar statements involve risk

and uncertainties including changes in economic and market conditions,

seasonality of business, timing and magnitude of future contracts, management of

growth, and other risks noted in the company’s SEC filings which may cause

actual results to differ materially. Forward-looking statements are made in the

context of information available as of the date stated. The company undertakes

no obligation to update or revise such statements to reflect new circumstances

or unanticipated events as they occur.

Why we

are No. 1 in our industry -

Executing against our mission to be the world

leader at informing people through dynamic

audio-visual communications systems

Executing against our mission to be the world

leader at informing people through dynamic

audio-visual communications systems

• 41 years of proven

track record in the industry

• Unparalleled sales

and service coverage

• Depth and breadth of

product offering

• Complete integrated

solution including software

• Engineering

capabilities

• Capacity to deliver:

5 plants in the United States

FINANCIAL

SUMMARY

Financial

History

117%

Revenue growth over the past 3 years

|

(Dollars

in thousands

except

per share data)

|

FY2005

|

FY2006

|

FY2007

|

FY2008

|

FY2009

|

|

5-Yr

CAGR |

|

Sales

|

$230,346

|

$309,370

|

$433,201

|

$499,677

|

$581,931

|

|

|

|

Operating

Income

|

$19,436

|

$31,815

|

$36,915

|

$38,243

|

$42,617

|

|

9.1%

|

|

Earnings

Per Share

|

$0.39

|

$0.52

|

$0.59

|

$0.63

|

$0.64

|

|

|

|

Dividend

Per Share

|

-

|

0.05

|

0.06

|

0.07

|

0.09

|

|

|

|

(Dollars

in thousands

except

per share data)

|

FY2005

|

FY2006

|

FY2007

|

FY2008

|

FY2009

|

|

|

|

Cash

from Operations

|

$22,377

|

$31,917

|

$14,606

|

$59,833

|

$48,730

|

|

18.3%

|

|

Capital

Expenditures,

net |

(12,981)

|

(18,588)

|

(58,528)

|

(33,393)

|

(18,221)

|

|

7.0%

|

|

Free

Cash Flow

|

$9,396

|

$13,329

|

$(43,922)

|

$26,440

|

$30,509

|

|

20.4%

|

Historical

Perspective: Revenue

more than doubled from FY2005

through FY2008 - 30% CAGR

more than doubled from FY2005

through FY2008 - 30% CAGR

During

this timeframe:

• Rapid growth:

capacity was the primary constraint

• Added two

manufacturing plants, Sioux Falls, and

Redwood Falls and reorganized existing plants to a

product focus

Redwood Falls and reorganized existing plants to a

product focus

• Set objective of

becoming world class manufacturing

organization using “lean” practices

organization using “lean” practices

Accomplishments

toward becoming

a World Class Manufacturing

Organization

a World Class Manufacturing

Organization

• Implementation of

lean practices in manufacturing

• Toyota lean

practices are the guide for this program

• Flow lines in every

factory

• Reliability lab,

quality engineering

• Decentralized

inventory

• Standardized product

design for “custom” products

• Implementation of

lean product development methods

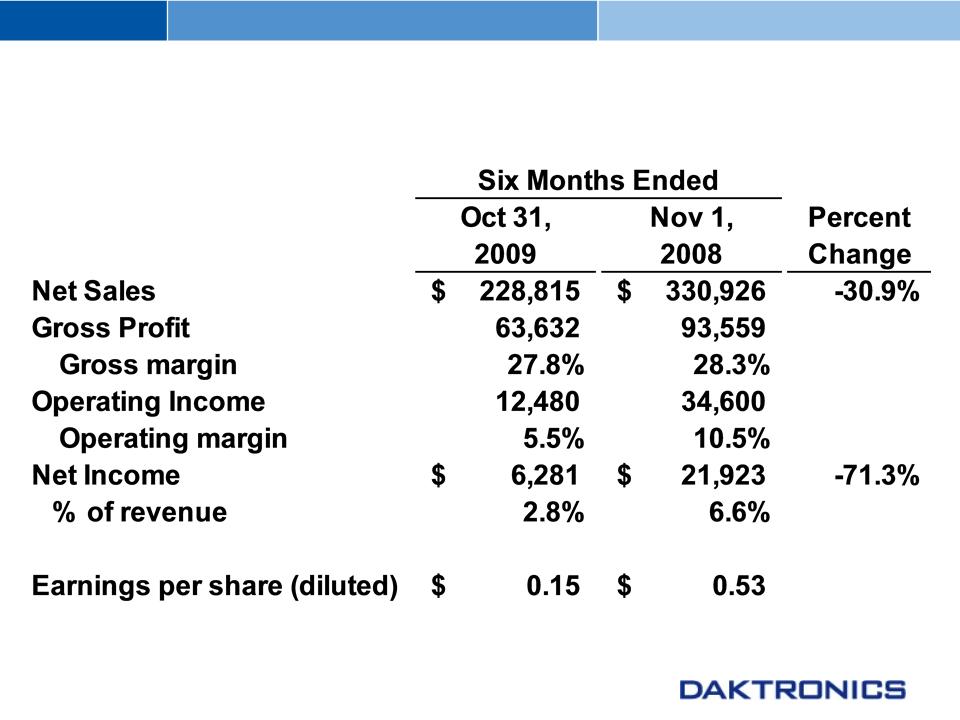

FY 2010

Second Quarter YTD Results*

*($

in thousands, except per share data)

FY2009

was a two-part story

• First half of year

revenues were $330 million, a $660

million run rate (10.5% operating margin).

million run rate (10.5% operating margin).

• Second half revenues

were $250 million, or a $500

million run rate (3.2% operating margin)

million run rate (3.2% operating margin)

• Billboard net sales

declined from $26 million in Q2 of

fiscal 2009 to $3 million in Q4 of fiscal 2009

fiscal 2009 to $3 million in Q4 of fiscal 2009

• Excess capacity in

third and fourth quarter hurt the

bottom line

bottom line

• Began cost reduction

initiatives in second half of fiscal

2009

2009

Strong

cash position

• Free cash

flow

• FY09 - $31

million

• FY10 through Q2 -

$23 million

• $57 million of net

cash at end of FY10 Q2

• Debt

free

Business is

Organized in 5

Business Units (“BU”)

Business Units (“BU”)

• Domestic (includes

Canada)

• Commercial

• Live

Events

• Schools and

Theaters

• Transportation

• International

• BUs provide focus,

but key strategy is to

leverage resources across the company

leverage resources across the company

Commercial Business

Unit

Three

main areas

• Digital

billboard

• National

accounts

•

Resellers

Main

products

• ValoTM digital

displays

• GalaxyProTM

• PS-X and

HD-X

video

27% of

FY09 net sales

FY10

net sales down 47% YTD through Q2

Commercial

Overview

Long-term

Growth Drivers

• Greater acceptance

& increasing use

• Effective

advertising medium

Competitors

• Resellers - Optec,

Watchfire, EDS

• National Accounts -

Optec, Hi-Tech

• Digital Billboards -

Yesco, Optotec

Current

Outlook for Commercial

• Expect billboard

orders to remain weak

through at least calendar 2010

through at least calendar 2010

• Adversely impacted

by

• Current economic

environment

• Credit

availability

• Increased price

pressure

Live

Events Overview

• Large sports

venues

• Professional sports

facilities

• College and

university facilities

• Mobile and

modular:

• Rental and

staging

• Touring

companies

• Pari-mutuel

• 46% of net sales in

FY09

• FY09 net sales up

60% over FY08

• FY10 net sales down

27% YTD through Q2

Live

Events Long-term Growth Drivers

• Fan

experience

• High definition

(HD)

• Competition

between

venues

venues

• Improving

price/

performance of LED

technology

performance of LED

technology

• Revenue

generation

Large

Sports Venues - New Construction

• FY2009 was big year

for new construction

• Significant increase

in spending for display systems in new venues

• Large contracts in

FY2009:

• New Meadowlands

Stadium - $45 million

• Minnesota Twins - $8

million

• Kansas City Royals

-$10 million

• Cincinnati Reds - $9

million

• Kansas City Chiefs -

$9 million

• University of

Minnesota - $9 million

• New York Mets - $11

million

• New York Yankees -

$20 million

• Few construction

projects in FY2010

• Typical volatility

in the business

• Economic pressures

and competitive environment impacting FY10

Mobile

& Modular

• Designed

for ease of use, set-up and tear down

Live

Events Competition

Large

Sports Venues

• Mitsubishi,

Lighthouse, ANC, Barco, and others

• Competition

generally must partner with others to

compete with Daktronics breadth of product

compete with Daktronics breadth of product

• Increasingly

competitive environment

Mobile

and Modular

• Barco, Lighthouse,

Toshiba, Hibino

Seeing

increased pricing pressure

Schools

& Theatres

Business Unit

Business Unit

Schools

& Theatres Overview

Customers

• Elementary and high

schools, junior colleges

• Park and recreation

departments

• Theatres

Main

Products

• Scoring

Systems

• Galaxy®

displays

• Vortek® hoist

systems

11% of

net sales in FY09

Primary

funding is through local sponsors and advertising

FY2010

net sales down 6% YTD through Q2

International

Business Unit

• Limited

manufacturing in China

• 10% of net sales in

FY09

• Large project

driven

• Similar drivers as

rest of business

• Current expectation

is for lower

sales in FY10 due to economic and

competitive factors

sales in FY10 due to economic and

competitive factors

• FY10 net sales down

50% YTD

through Q2

through Q2

• Improving pipeline,

increased

competition and pricing pressure

competition and pricing pressure

Transportation

Business Unit

Transportation

Overview

Three

main areas:

•Intelligent

transportation systems (ITS)

•Aviation, including

airports and airlines

•Mass

Transit

6% of

FY09 net sales

Strong

backlog going into FY2010

FY10

net sales up 27% YTD through Q2

Transportation

Overview

Long-term

Growth Drivers

• Government

spending

• Capacity constraints

on

highways, public transit,

airports and parking systems

highways, public transit,

airports and parking systems

• Limited ability to

build and

expand new roads

expand new roads

• Increased air

travel

• Work-zone

safety

Competitors

• ITS - Skyline,

Ledstar

• Aviation - TransLux,

AMS

• Increasing

competition

LOOKING

AHEAD

Maintaining

Long-Term Profitable Growth

Ongoing

product development - generally 4% of net

sales (higher in FY2010)

sales (higher in FY2010)

• New product for

existing markets

• Enhance existing

products while reducing costs

• Lean development

methods

Increase

market penetration in existing locations

Continued

emphasis on reducing costs and improving

quality through lean initiatives

quality through lean initiatives

• Improve

asset turns (inventory alignment, process

improvement)

improvement)

• Focus

on operating margin and free cash flow

• Leverage

service (process improvement)

Managing Through

Current Downturn

• Cost reduction is

ongoing process, not a one time event

• Overriding objective

to reduce cost without harm to

• Long-term growth

opportunities, and

• Orders

• Goal is to come out

of downturn stronger and leaner

• Focus on payroll

reductions through attrition, performance

and other measures.

and other measures.

• Strategic focus on

quality, service and process

improvements

improvements

• Expect continued

declines in costs

• Continue to generate

free cash flow

• Maintenance level

capital expenditures for FY10

Outlook

Overview - Challenging Factors

• Lighter ($90

million) backlog going into Q3

• Order bookings in Q3

lagging expectations due

to economic factors, impacting Q3 revenue

expectations

to economic factors, impacting Q3 revenue

expectations

• Now apparent that no

large (>$5 million)

baseball projects will go forward for

installation this season

baseball projects will go forward for

installation this season

• National accounts

orders slower than

anticipated

anticipated

• Large commercial

projects slow to close

• Extremely aggressive

pricing from competitors,

especially new competitors trying to enter the

market, is affecting margins

especially new competitors trying to enter the

market, is affecting margins

Outlook

Overview - Positive Factors

• Overall cost

reduction has been effective to date -

achieved 8% operating margin in Q2

achieved 8% operating margin in Q2

• Cost reduction

continues as an ongoing process

• Significant ongoing

improvements throughout the

company on lean initiatives

company on lean initiatives

• Improved

competitiveness in Live Events due to:

• New DVX outdoor

video product platform beginning to

ship Q4 - reduced cost, excellent viewing qualities,

streamlined manufacturing, increased commonality

across the product family.

ship Q4 - reduced cost, excellent viewing qualities,

streamlined manufacturing, increased commonality

across the product family.

• New Show Control

software for video systems beginning

to ship in Q4

to ship in Q4

QUESTIONS