Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - ABRAXAS PETROLEUM CORP | pc8k.htm |

| EX-99.1 - NEWS RELEASE - ABRAXAS PETROLEUM CORP | newsrelease.htm |

Energize 2010

January 6-8

San

Francisco

Exhibit

99.2

2

Forward-Looking

Statements

The

information presented herein may contain predictions, estimates and

other forward-looking statements within the meaning of Section 27A of the

Securities Act of 1933 and Section 21E of the Securities Exchange Act of

1934. Although the Company believes that its expectations are based on

reasonable assumptions, it can give no assurance that its goals will be

achieved.

other forward-looking statements within the meaning of Section 27A of the

Securities Act of 1933 and Section 21E of the Securities Exchange Act of

1934. Although the Company believes that its expectations are based on

reasonable assumptions, it can give no assurance that its goals will be

achieved.

Important factors

that could cause actual results to differ materially from

those included in the forward-looking statements include the timing and

extent of changes in commodity prices for oil and gas, the need to develop

and replace reserves, environmental risks, competition, government

regulation and the ability of the Company to meet its stated business

goals.

those included in the forward-looking statements include the timing and

extent of changes in commodity prices for oil and gas, the need to develop

and replace reserves, environmental risks, competition, government

regulation and the ability of the Company to meet its stated business

goals.

3

Bakken

producers Abraxas

operated wells

Bakken

permits Abraxas

non-operated wells

2008-2009

Bakken

Sleeper

Numerous

additional

opportunities

opportunities

(operated and

non-operated)

NO

LEASE EXPIRATIONS -

acreage principally held by

production

acreage principally held by

production

MINIMAL

RESERVES

BOOKED TO-DATE

BOOKED TO-DATE

10% WI

NON-OP WELL -

Completing

Completing

AXAS: 3

operated lease

blocks within 1 location of

commercial Bakken /

Three Forks production with

potential of:

blocks within 1 location of

commercial Bakken /

Three Forks production with

potential of:

>100

1st gross

Bakken

wells in unit *

Bakken

wells in unit *

Montana North

Dakota

Parshall

Nesson

Anticline

Elm

Coulee

Rough

Rider

* ~90 on

1280 acre unit spacing, excludes Lewis &

Clark Three Forks potential

Clark Three Forks potential

4

The

Bakken Advantage

Total enterprise

value - Proved PV10 =

Bakken acreage value

/ Net Bakken acres = Bakken value per acre

|

Small-cap

Bakken Players

|

||

|

|

Bakken

value

per

acre

|

Q3

2009

Boepd

|

|

Company

A

|

$

3,149

|

144

|

|

Company

B

|

$

4,498

|

5,200

|

|

Company

C

|

$

6,768

|

963

|

|

Company

D

|

$

6,839

|

751

|

|

Company

E

|

$15,244

|

5,348

|

|

|

|

|

|

AXAS

|

$

1,613

|

4,430

|

AXAS

utilizing mid-year proved reserves on a typical bank

price deck

price deck

Source:

Company filings with the SEC

5

Peer

Group Analysis

Source:

Company filings with the SEC and market capitalization on December 30,

2009

E&P

analysis includes market capitalization < $1B (AEZ, AREX, ATPG, AXAS, CFW,

CPE, CRZO, CWEI, DBLE, DNE, DPTR, END, EPM, EXXI, FXEN, GDP, GEOI, GMET,

GMXR,

GPOR, GPR, GST, GSX, KOG, MCF, MHR, MMR, NGAS, NOG, PETD, PHX, PINN, PQ, PVA, RAME, REXX, SFY, SGY, TMR, VQ, WRES)

GPOR, GPR, GST, GSX, KOG, MCF, MHR, MMR, NGAS, NOG, PETD, PHX, PINN, PQ, PVA, RAME, REXX, SFY, SGY, TMR, VQ, WRES)

Mean

equates to an AXAS share price of:

$19.42

Mean

equates to an AXAS share price of:

$5.56

48%

undervalued compared to E&P in analysis

6

Peer

Group Analysis

65%

under average of E&P in analysis

In-line

with average of E&P in analysis

In-line

with average of E&P in analysis

Source:

Company filings with the SEC

E&P

analysis includes market capitalization < $1B (AEZ, AREX, ATPG, AXAS, CFW,

CPE, CRZO, CWEI, DBLE, DNE, DPTR, END, EPM, EXXI, FXEN, GDP, GEOI, GMET,

GMXR,

GPOR, GPR, GST, GSX, KOG, MCF, MHR, MMR, NGAS, NOG, PETD, PHX, PINN, PQ, PVA, RAME, REXX, SFY, SGY, TMR, VQ, WRES)

GPOR, GPR, GST, GSX, KOG, MCF, MHR, MMR, NGAS, NOG, PETD, PHX, PINN, PQ, PVA, RAME, REXX, SFY, SGY, TMR, VQ, WRES)

7

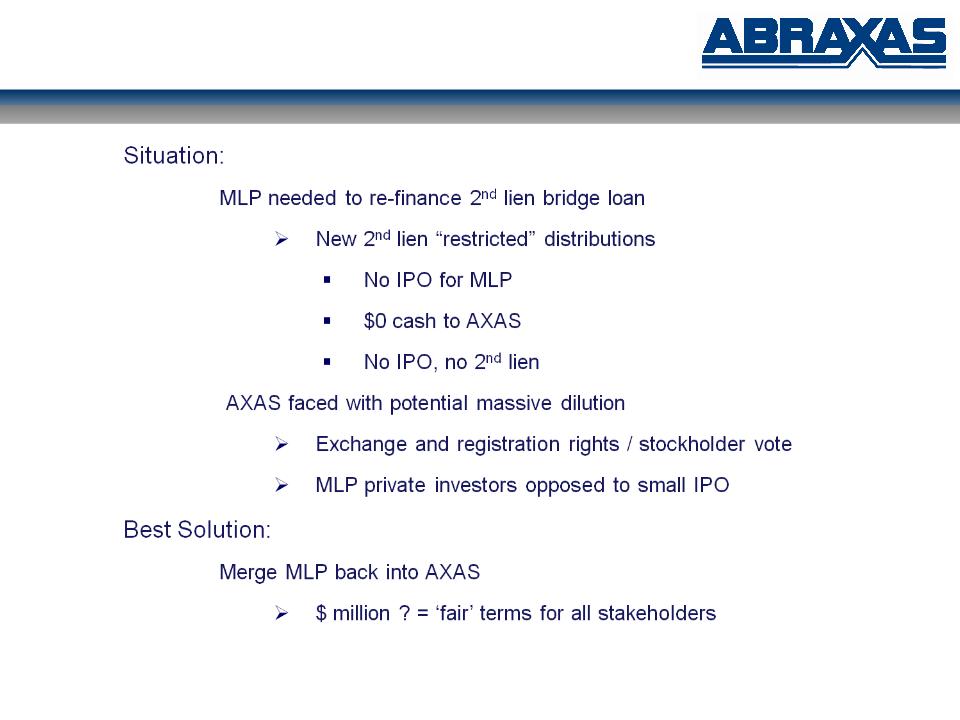

Special

Situation

§ Exciting upside (not

just the Bakken)

§ Undervalued

§ Why ?

§ 26 months in

SEC

§ Complicated

financials

§ Analyst &

investors don’t relish homework

§ Solution

!

§ Merger closed -

October 5, 2009

§ Tell the

story

§ Straight forward

financials (except MTM on commodity swaps)

8

Background

Ø Abraxas Petroleum

Corporation

§ Founded in

1977

§ NASDAQ:

AXAS

Ø 2006 - 2008:

Upstream MLPs were reincarnated

§ Attractive cost of

capital - yields < 10%

Ø Abraxas Energy was

formed in May 2007 as an upstream master limited

partnership (“MLP”) to produce, develop and acquire oil and gas properties

partnership (“MLP”) to produce, develop and acquire oil and gas properties

§ AXAS contributed

properties to MLP

– Sold 53% to

institutional investors ($100 million private placement)

§ Lehman Brothers /

Citigroup / Merrill Lynch

§ Top-tick market: 9%

yield

– AXAS retained 47% of

MLP

– AXAS owns 100% of

general partner, which manages MLP

§ MLP required to “go

public”

9

IPO

Timeline

2007

July 2007 - MLP

filed initial registration statement (S-1) for IPO

November 2007 -

cleared by the SEC (S-1/A #4)

November

2007 - won bid on large property acquisition from St. Mary - financed with

senior

bank debt & 2nd lien bridge (extension from private investors)

bank debt & 2nd lien bridge (extension from private investors)

2008

July 2008 - cleared

by the SEC (S-1/A #7)

July 2008 - lead

underwriter walked

September 2008 - new

underwriting syndicate in place (S-1/A #8)

September 2008 -

financial world started its collapse

(extension

from private investors)

2009

January 2009 -

maturity date of sub. debt extended to July 1

January 2009 - MLP

yields > 20% = downsize IPO, need 2nd lien

(underwriting

syndicate walks)

March 2009 - new

underwriting syndicate in place (S-1/A #9), launch 2nd lien

April 2009 - new

2nd lien terms

unacceptable / vicious circle / explore alternatives

(extension

from private investors)

10

Upstream MLP

Meltdown

Market darling

à ??

§ Last IPO - April

2008

§ 4 MLPs - suspended

distributions

§ Bank support

diminished for upstream MLPs

11

Alternatives

12

Merger

Events

13

New and

Improved AXAS

Abraxas

Petroleum Corporation

• High quality

assets

• Daily production of

4,430 Boe (26.6 MMcfe)

• Proved reserves of

27.9 MMBoe (167.3 Bcfe)

• Unparalleled upside

opportunities

§ 158 proved

undeveloped locations (excluding Bakken)

§ Numerous additional

identified locations

§ 85% of PDP hedged

through 2012 and 70% in 2013

§ $74.96 per barrel

and $6.38 per MMbtu

• NASDAQ:

AXAS

• Fully diluted shares

outstanding: ~76 million

§ ~50%

institutional

§ ~10%

insider

• Current average

trading volume: ~470,000 shares per day

• Total long-term

debt: ~$145

million

14

Overview of

Properties

15

Property

Overview

Ø Predictable,

long-lived production

§ R/P

ratio of 16.9 years (PD of 9.3

years)

§ Conventional and

unconventional reservoirs

Ø 1,811 gross (429

net) producing wells: average working interest 24%

§ ~690

gross (250 net) wells/units comprise top 90% by PV

Ø Substantial

inventory: 158 proved

undeveloped locations (plus Bakken)

§ Numerous additional

identified locations

Ø 307,310 gross

(160,141 net) acres

§ No

material lease expiry issues or drilling commitments

Ø Operational control

- over 80%

of PV10

§ Over 30 years of

operational history

§ Efficient, low-cost

operator

§ Long history of

drilling success

16

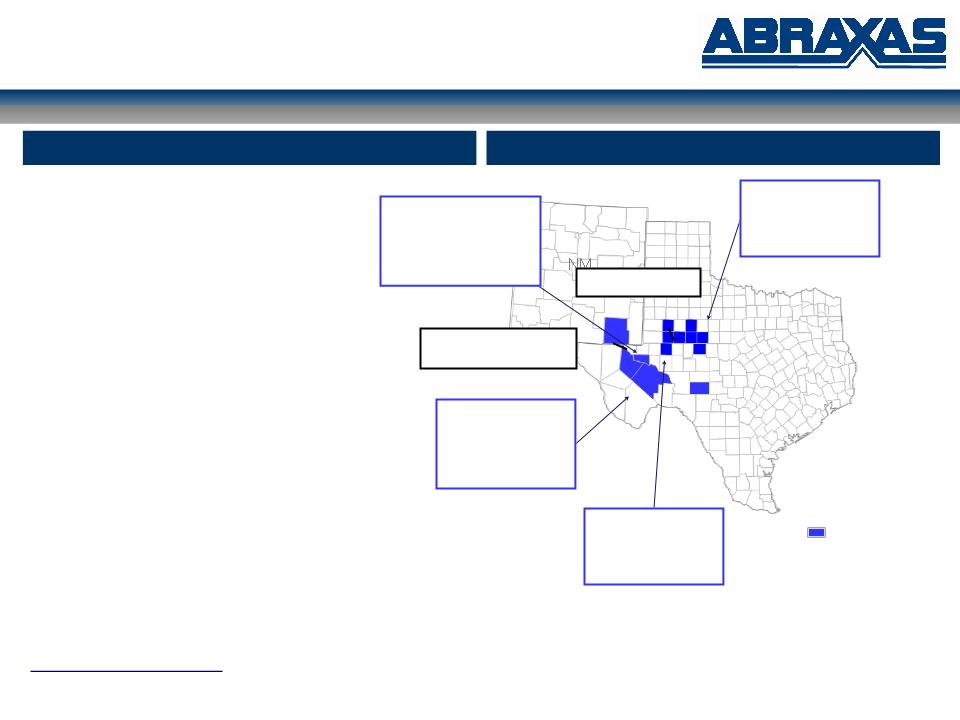

High

Quality Assets

ND

SD

MT

WY

CO

UT

TX

OK

AR

LA

Proved

Reserves (MMBoe): 27.9

-

Proved Developed: 55%

-

Gas/Oil %: 71/29%

-

Operated: 83%

Abraxas

Petroleum Corporation

Net

proved reserves as of June 1, 2009

Bakken

Shale

Play

Haynesville

Shale

Play

Central

Anadarko

Cana

- Woodford

Shale

Play

Barnett

/ Woodford

Shale

Play

Wolfberry

Trend

Rocky

Mountain

Mid-Continent

Permian

Basin

Gulf

Coast

Eagle

Ford Shale Play

17

Reserve

/ Production Summary

Proved

Reserves - 27.9 MMBoe

Production

- 4,430 Boepd

Net

proved reserves as of June 1, 2009

Daily

net production for the quarter ended September 30, 2009

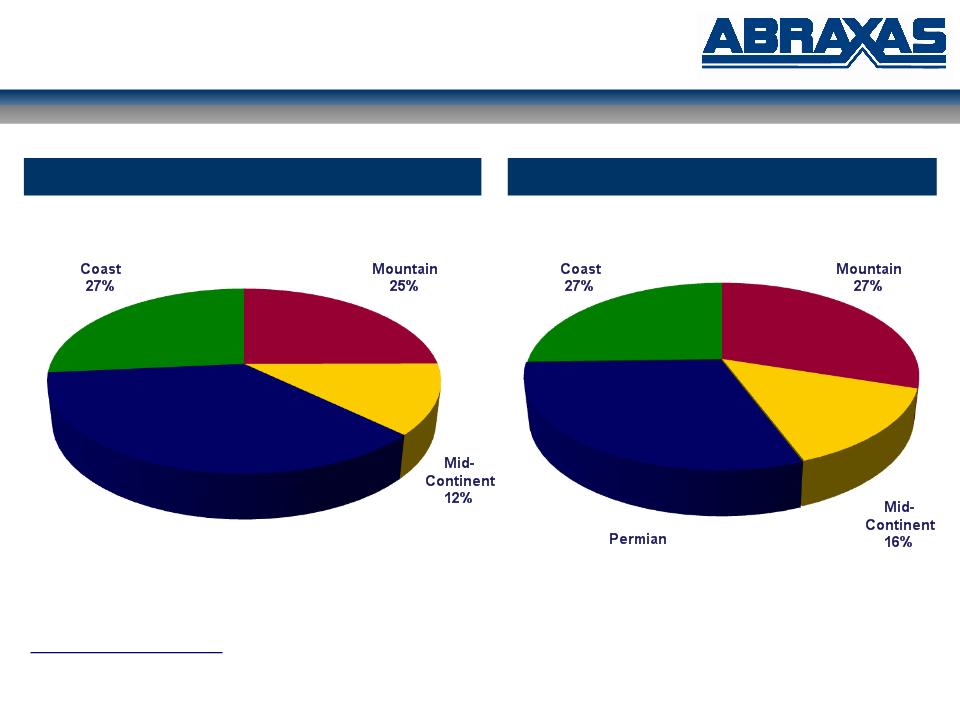

Rocky

Permian

Basin

36%

Gulf

Rocky

Basin

30%

Gulf

18

Production

Profile

Net

proved reserves as of June 1, 2009

Next

5 years - 9%

Thereafter

- 8%

Projected

Annual PDP Decline Rate

19

ND

SD

MT

WY

CO

UT

TX

OK

LA

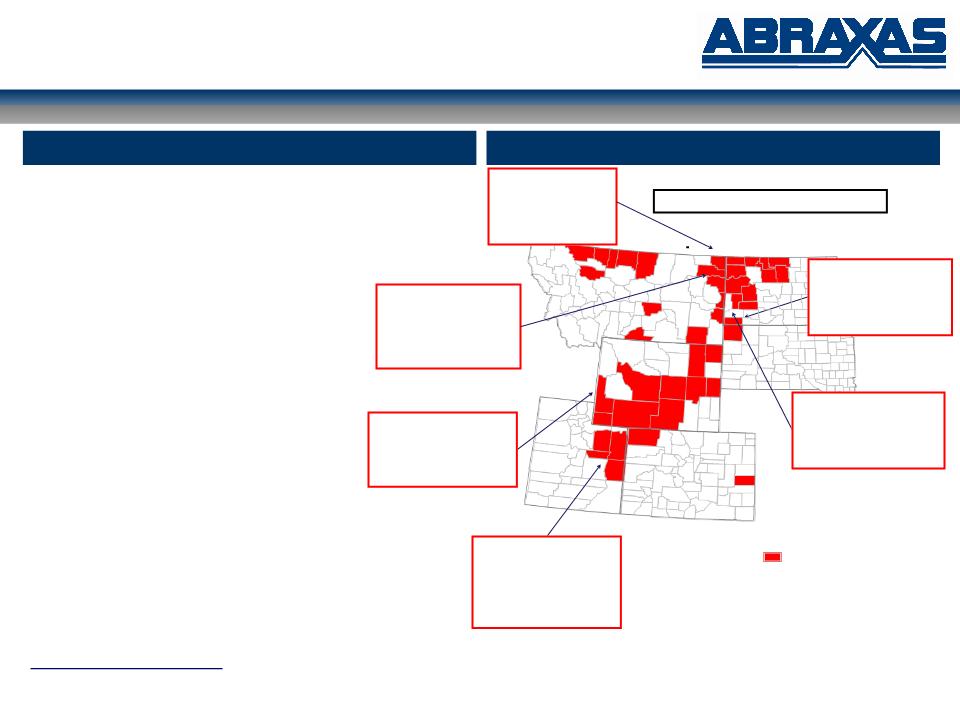

Unparalleled Upside

Potential

Rocky

Mountain

Mid-Continent

Permian

Basin

Gulf

Coast

Medicine

Pole Hills Unit

Bowman

Co., ND

2

PUD

Red

River B: 9,350’

Operator:

Continental

Cow

Hollow Field

Lincoln

Co., WY

32

PUD

Frontier:

11,000’

Operator:

Kerr-McGee

Pittsburg

County CBM

Pittsburg

Co., OK

53

PUD

Hartshorne

Coal: 3,000’

Operator:

Chesapeake / Abraxas

Edwards

Trend

DeWitt

/ Lavaca Co., TX

10

PUD (4 PDNP)

Edwards:

13,500’

Operator:

Abraxas

Portilla

Field

San

Patricio Co., TX

3

PUD (2 PDNP)

Frio:

7,000’

Vicksburg: 9,000’

Vicksburg: 9,000’

Operator:

Abraxas

Oates

SW

Pecos

Co., TX

5

PUD

Devonian:

14,000’

Montoya: 16,000’

Montoya: 16,000’

Operator:

Abraxas

ROC

Complex

Ward

Co., TX

7

PUD

Devonian:

13,000’

Montoya:

14,000’

Operator:

Abraxas

Bakken

Shale

Play

Haynesville

Shale

Play

Central

Anadarko

Cana

- Woodford

Shale

Play

Wolfberry

Trend

Natural

Buttes Field

(Chapita

Wells Unit)

Uintah

Co., UT

20

PUD

Wasatch:

7,000’

Operator:

EOG Resources

Roosevelt

Field

Billings

Co., ND

4

PUD

Nisku:

10,000’

Operator:

Abraxas/Summit

North

Fork Field

McKenzie

Co., ND

6

PUD

Bakken:

10,000’

Red

River: 14,000’

Operator:

Abraxas

Comertown

South Field

Sheridan

Co., MT

2

PUD

Red

River: 11,000’

Operator:

Abraxas

Eastern

Shelf

Coke

Co., TX

3

PUD

Strawn

6,700’

Operator:

Abraxas

Beulah

Coleman

Midland

Co., TX

5

PUD

Devonian:

11,000’

Operator:

Abraxas

Barnett

/ Woodford

Shale

Play

Eagle

Ford

Shale

Play

20

Near-Term Drilling

Catalysts

|

AXAS

OPERATED:

|

OUTSIDE

OPERATED:

|

|

Portilla,

South Texas

• 2 vertical

wells

• 9,000’

Frio

• Q1

2010

• AXAS 100%

WI

|

Bakken/Three

Forks, North Dakota

• BTA

operated

• Completing

• AXAS 10%

WI

|

|

Normanna,

South Texas

• 10,000’

Wilcox

• Q1

2010

• AXAS 20%/40%

WI

|

Granite Wash,

Texas Panhandle

• 2

wells

• Cimarex /

Mewbourne operated

• Drilling

• AXAS <1-8%

WI

|

|

Spires Ranch,

West Texas

• 7,000’

Ellenburger

• Testing

• AXAS 100%

WI

|

|

Non-op

wells gather information

21

Business

Plan

§ Closed merger -

October 5th

§ Allocate portion of

2010 CapEx to Bakken

§ Investigate Bakken

acceleration

§ Financial

partner

§ Industry

farmout

§ Non-core asset

sales

§ Pay down

debt

§ 50/50 oil/gas

production mix by end of 2010

§ Awareness of NOL

preservation

§ Increase Eagle Ford

position

§ Principally in oil

leg

§ Increase investor

interest

§ Increase analyst

coverage

22

NASDAQ:

AXAS

23

Appendix

24

Rocky

Mountain

Ø 7.0 MMBoe of proved

reserves

Ø 75% proved

developed

Ø 75% crude

oil

Ø 1,175 Boepd of

production

Ø 15.7 R/P

ratio

Ø 894 gross (110 net)

producing wells

Ø 67 PUD

locations

Ø 97,279 net

acres

Ø Primary producing

basins include:

§ Williston Basin (MT

and ND)

§ Powder River &

Green River Basins (WY)

§ Unita Basin

(UT)

Ø Bakken / Three Forks

- HBP

Rocky

Mountain

ND

SD

MT

WY

CO

UT

Medicine

Pole Hills Unit

Bowman

Co., ND

2

PUD

Red

River B: 9,350’

Operator:

Continental

Natural

Buttes Field

(Chapita

Wells Unit)

Uintah

Co., UT

20

PUD

Wasatch:

7,000’

Operator:

EOG Resources

Cow

Hollow Field

Lincoln

Co., WY

32

PUD

Frontier:

11,000’

Operator:

Kerr-McGee

Bakken

Shale Play / Three Forks / Sanish

Area

of Operations

Overview

Net

proved reserves as of June 1, 2009

Daily

net production for the quarter ended September 30, 2009

Roosevelt

Field

Billings

Co., ND

4

PUD

Nisku:

10,000’

Operator:

Abraxas/Summit

North

Fork Field

McKenzie

Co., ND

6

PUD

Bakken:

10,000’

Red

River: 14,000’

Operator:

Abraxas

Comertown

South Field

Sheridan

Co., MT

2

PUD

Red

River: 11,000’

Operator:

Abraxas

25

Mid-Continent

Ø 3.4 MMBoe of proved

reserves

Ø 73% proved

developed

Ø 85% natural

gas

Ø 711 Boepd of

production

Ø 13.0 R/P

ratio

Ø 602 gross (103 net)

producing wells

Ø 53 PUD

locations

Ø 22,937 net

acres

Ø Primary producing

basins include:

§ Anadarko Basin

(Western OK)

§ Arkoma Basin

(Eastern OK)

§ ARK-LA-TEX

Ø Cana Shale (Cimarex,

Devon, Chesapeake) - HBP

Ø Haynesville Shale -

HBP

TX

KS

OK

AR

LA

Haynesville

Shale

Play

Central

Anadarko

Cana

- Woodford

Shale

Play

Pittsburg

County CBM

Pittsburg

Co., OK

53

PUD

Hartshorne

Coal: 3,000’

Operator:

Chesapeake / AXAS

Area

of Operations

Overview

Net

proved reserves as of June 1, 2009

Daily

net production for the quarter ended September 30, 2009

26

Permian

Basin

Permian

Basin

Ø 10.1 Bcfe of proved

reserves

Ø 39% proved

developed

Ø 83% natural

gas

Ø 1,330 Boepd of

production

Ø 19.7 R/P

ratio

Ø 236 gross (161 net)

producing wells

Ø 30 PUD

locations

Ø 31,237 net

acres

Ø Primary producing

sub-basins:

§ Delaware

Basin

§ Eastern

Shelf

Ø Barnett / Woodford

Shale - fee minerals

TX

Oates

SW

Pecos

Co., TX

5

PUD

Devonian:

14,000’

Montoya: 16,000’

Montoya: 16,000’

Operator:

Abraxas

ROC

Complex

Ward

Co., TX

7

PUD

Devonian:

13,000’

Montoya:

14,000’

Operator:

Abraxas

Area

of Operations

Overview

Beulah

Coleman

Midland

Co., TX

5

PUD

Devonian: 11,500’

Operator: Abraxas

Operator: Abraxas

Millican

Reef Unit

Coke

Co., TX

3

PUD

Strawn:

6,700’

Operator: Abraxas

Operator: Abraxas

Barnett

/ Woodford

Shale

Play

Wolfberry

Trend

Net

proved reserves as of June 1, 2009

Daily

net production for the quarter ended September 30, 2009

27

Gulf

Coast

Gulf

Coast

Ø 7.4 Bcfe of proved

reserves

Ø 49% proved

developed

Ø 92% natural

gas

Ø 1,214 Boepd of

production

Ø 17.2 R/P

ratio

Ø 79 gross (55 net)

producing wells

Ø 13 PUD

locations

Ø 8,688 net

acres

Ø Primary producing

sub-basin:

§ Onshore Gulf

Coast

Ø Eagle Ford Shale -

HBP

§ Currently leasing

addtional acreage

TX

LA

AL

MS

Portilla

Field

San

Patricio Co., TX

3

PUD (2 PDNP)

Frio:

7,000’

Vicksburg: 9,000’

Vicksburg: 9,000’

Operator:

Abraxas

Edwards

Trend

DeWitt

/ Lavaca Co., TX

10

PUD (4 PDNP)

Edwards:

13,500’

Operator:

Abraxas

Area

of Operations

Overview

Eagle

Ford

Shale

Play

Net

proved reserves as of June 1, 2009

Daily

net production for the quarter ended September 30, 2009

28

2008-2009 OBO

Drilling Activity

23

wells drilled in 2008

7

wells drilled in 2009

Chapita

Wells Unit

Uintah

County, UT

Operator:

EOG Resources

Average

IP: 1.1 MMcfepd

WI:

1%

7

wells drilled in 2008

Medicine

Pole Hills West Unit

Bowman

County, ND

3

wells drilled in 2008

1

well drilled in 2009

Mansfield

Prospect

Scott

County, AR

Operator:

XTO Energy

Average

IP: 2.2 MMcfepd

2

wells drilled in 2008

1

well drilled in 2009

Bear

Creek Field

Bienville

Parish, LA

Operator:

El Paso

Average

IP: 2.3 MMcfepd

WI:

2%

1

well drilled in 2008

Red

Oak Prospect

Latimer

County, OK

Operator:

Unit Petroleum

IP:

2.1 MMcfepd

WI:

12%

2

wells drilled in 2008

Cow

Creek / Moxa Arch

Lincoln

County, WY

Operator:

Kerr McGee

Average

IP: 1.2 MMcfepd

WI:

1%

1

well drilled in 2008

2

wells drilled in 2009

Sawyer

Field

Sutton

County, TX

Operator:

Highmount

Average

IP: 0.2 MMcfepd

WI:

4%

2

wells drilled in 2009

Bakken

/ Three Forks

McKenzie

/ Divide Counties, ND

Operator:

Continental Resources / BTA

IP:

760 Boepd / completing

WI:

1-10%

3

wells drilled in 2009

Granite

Wash

Hemphill

County, TX

Operator:

Cimarex /

Mewbourne

Mewbourne

WI:

1-8%

29

NASDAQ:

AXAS