Attached files

| file | filename |

|---|---|

| EX-12 - EXHIBIT 12 - TORO CO | a2195867zex-12.htm |

| EX-23 - EXHIBIT 23 - TORO CO | a2195867zex-23.htm |

| EX-32 - EXHIBIT 32 - TORO CO | a2195867zex-32.htm |

| EX-21 - EXHIBIT 21 - TORO CO | a2195867zex-21.htm |

| EX-31.1 - EXHIBIT 31.1 - TORO CO | a2195867zex-31_1.htm |

| EX-31.2 - EXHIBIT 31.2 - TORO CO | a2195867zex-31_2.htm |

| EX-10.16 - EXHIBIT 10.16 - TORO CO | a2195867zex-10_16.htm |

QuickLinks -- Click here to rapidly navigate through this document

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For Fiscal Year Ended October 31, 2009

THE TORO COMPANY

(Exact name of registrant as specified in its charter)

| Delaware | 1-8649 | 41-0580470 | ||

| (State of incorporation) | (Commission File Number) | (I.R.S. Employer Identification Number) |

8111 Lyndale Avenue South

Bloomington, Minnesota 55420-1196

Telephone number: (952) 888-8801

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class

|

Name of Each Exchange on Which Registered

|

|

|---|---|---|

Common Stock, par value $1.00 per share |

New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of the voting stock held by non-affiliates of the registrant, based on the closing price of the Common Stock on May 1, 2009, the last business day of the registrant's most recently completed second fiscal quarter, as reported by the New York Stock Exchange, was approximately $1.1 billion.

The number of shares of Common Stock outstanding as of December 16, 2009 was 33,464,325.

Documents Incorporated by Reference

Portions of the registrant's Proxy Statement for the Annual Meeting of Shareholders to be held March 16, 2010 are incorporated by reference into Part III.

THE TORO COMPANY

FORM 10-K

TABLE OF CONTENTS

| |

Description |

Page Number |

||

|---|---|---|---|---|

PART I |

||||

ITEM 1. |

Business |

3 |

||

ITEM 1A. |

Risk Factors |

11 | ||

ITEM 1B. |

Unresolved Staff Comments |

18 | ||

ITEM 2. |

Properties |

19 | ||

ITEM 3. |

Legal Proceedings |

19 | ||

ITEM 4. |

Submission of Matters to a Vote of Security Holders |

20 | ||

|

Executive Officers of the Registrant |

21 | ||

PART II |

||||

ITEM 5. |

Market for Registrant's Common Equity, Related Stockholder Matters, and Issuer Purchases of Equity Securities |

22 |

||

|

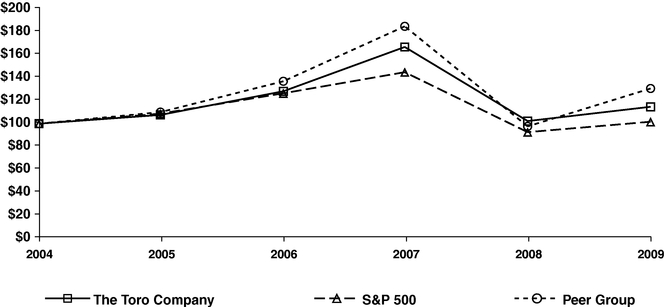

The Toro Company Common Stock Comparative Performance Graph |

23 | ||

ITEM 6. |

Selected Financial Data |

24 | ||

ITEM 7. |

Management's Discussion and Analysis of Financial Condition and Results of Operations |

24 | ||

ITEM 7A. |

Quantitative and Qualitative Disclosures about Market Risk |

37 | ||

ITEM 8. |

Financial Statements and Supplementary Data |

39 | ||

|

Management's Report on Internal Control over Financial Reporting |

39 | ||

|

Report of Independent Registered Public Accounting Firm |

40 | ||

|

Consolidated Statements of Earnings for the fiscal years ended October 31, 2009, 2008, and 2007 |

41 | ||

|

Consolidated Balance Sheets as of October 31, 2009 and 2008 |

42 | ||

|

Consolidated Statements of Cash Flows for the fiscal years ended October 31, 2009, 2008, and 2007 |

43 | ||

|

Consolidated Statements of Stockholders' Equity and Comprehensive Income for the fiscal years ended October 31, 2009, 2008, and 2007 |

44 | ||

|

Notes to Consolidated Financial Statements |

45 | ||

ITEM 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

64 | ||

ITEM 9A. |

Controls and Procedures |

64 | ||

ITEM 9B. |

Other Information |

64 | ||

PART III |

||||

ITEM 10. |

Directors, Executive Officers and Corporate Governance |

64 |

||

ITEM 11. |

Executive Compensation |

64 | ||

ITEM 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

65 | ||

ITEM 13. |

Certain Relationships and Related Transactions, and Director Independence |

65 | ||

ITEM 14. |

Principal Accounting Fees and Services |

65 | ||

PART IV |

||||

ITEM 15. |

Exhibits, Financial Statement Schedules |

65 |

||

|

Signatures |

69 | ||

2

Introduction

The Toro Company was incorporated in Minnesota in 1935 as a successor to a business founded in 1914 and reincorporated in Delaware in 1983. Unless the context indicates otherwise, the terms "company," "Toro," "we," "us," and "our" refer to The Toro Company and its consolidated subsidiaries. Our executive offices are located at 8111 Lyndale Avenue South, Bloomington, Minnesota, 55420-1196, telephone number (952) 888-8801. Our Internet address for corporate and investor information is www.thetorocompany.com, which also contains links to our branded product sites. The information contained on our web sites or connected to our web sites is not incorporated by reference into this Annual Report on Form 10-K and should not be considered part of this report.

We design, manufacture, and market professional turf maintenance equipment and services, turf and agricultural micro-irrigation systems, landscaping equipment, and residential yard and snow removal products. We produced our first mower for golf course use in 1921 when we mounted five reel mowers on a Toro tractor, and we introduced our first lawn mower for residential use in 1935. We have continued to enhance our product lines ever since. We classify our operations into three reportable business segments: professional, residential, and distribution. Our distribution segment, which consists of our company-owned domestic distributorship, has been combined with our corporate activities and financing functions that is shown as "Other." Net sales of our segments accounted for the following approximate percentages of our consolidated net sales for fiscal 2009: Professional, 63 percent; Residential, 35 percent; and Other, 2 percent.

Our products are advertised and sold at the retail level under the primary trademarks of Toro®, Exmark®, Irritrol®, Hayter®, Pope®, Lawn-Boy®, and Lawn Genie®, most of which are registered in the United States and/or in the principal foreign countries where we market such products. This report also contains trademarks, trade names, and service marks that are owned by other persons or entities, such as The Home Depot®.

We emphasize quality and innovation in our products, customer service, manufacturing, and marketing. We strive to provide well-built, dependable products supported by an extensive service network. We have committed funding for engineering and research in order to improve existing products and develop new products. Through these efforts, we seek to be responsive to trends that may affect our target markets now and in the future. A significant portion of our revenue has historically been, and we expect it to continue to be, attributable to new and enhanced products. At the same time, we plan to pursue targeted acquisitions using a disciplined approach that adds value while considering our existing brands and product portfolio. Our mission is to be the leading worldwide provider of outdoor landscaping products, support services, and integrated systems that help customers preserve and beautify their outdoor landscapes with environmentally responsible solutions of customer-valued quality and innovation.

Products by Market

We strive to be a leader in adapting advanced technologies to products and services that provide solutions for landscapes, agricultural fields, turf care maintenance, and residential demands. The following is a summary of our products, by market, for the professional segment and our products for the residential segment:

Professional – We design professional turf and agricultural products and market them worldwide through a network of distributors and dealers as well as directly to government customers, rental companies, and large retailers. Products are sold to professional users engaged in creating landscapes, irrigating turf and agricultural fields, and maintaining turf, such as golf courses, sports fields, municipal properties, and residential and commercial landscapes.

Landscape Contractor Market. Products for the landscape contractor market include zero-turn radius riding mowers, heavy-duty walk behind mowers, mid-size walk behind mowers, stand-on mowers, compact utility loaders, and walk-behind trenchers. These products are sold through dealers and are also available through rental centers to individuals and companies who maintain and create residential and commercial landscapes on behalf of property owners. We market products to landscape contractors under the Toro and Exmark brands. In fiscal 2009, we introduced the next generation of Toro and Exmark zero-turn radius riding mowers. The Toro brand Z Master® G3 and the Exmark brand Next Lazer Z® feature more efficient designs with fewer parts and a complete set of redesigned performance, comfort, and convenience features. In fiscal 2009, we also introduced the Toro GrandStand™ premium stand-on mower that features our versatile fold-up platform and fatigue-reducing suspension.

Our compact utility loaders are cornerstone products for the Toro Sitework Systems product line, which are designed to improve efficiency in the creation of landscapes. We offer over 35 attachments for our compact utility loaders, including trenchers, augers, vibratory plows, and backhoes.

Sports Fields and Grounds Market. Products for the sports fields and grounds market include riding rotary mowers and attachments; aerators; and debris management products, which include versatile debris vacuums, blowers, and sweepers. Other products include multipurpose vehicles, such as the Toro Workman®, that can be used for turf maintenance, towing, and industrial hauling. These

3

products are sold through distributors, who then sell to owners and/or managers of sports fields, municipal properties, and residential and commercial landscapes. In fiscal 2009, we introduced the redesigned Groundsmaster® 4500-D and 4700-D that features our Contour Plus™ rotary cutting units, SmartCool™ system with auto-reversing cooling fan, and full-length striping rear rollers. In fiscal 2009, we also introduced the redesigned Toro Workman® HD series of utility vehicles, featuring increased hauling and towing capacity.

Golf Course Market. Products for the golf course market include large reel and rotary riding products for fairway, rough and trim cutting; riding and walking mowers for putting greens and specialty areas; turf sprayer equipment; utility vehicles; aeration equipment; and bunker maintenance equipment. We also manufacture and market underground irrigation systems, including sprinkler heads; controllers; turf sensors; and electric, battery-operated, and hydraulic valves. Our golf course irrigation systems are designed to use computerized management systems and a variety of technologies to help customers manage their consumption of water. Our 835S/855S Series golf sprinklers are equipped with a unique TruJectory™ feature that provides enhanced water distribution control as well as uniformity, nozzle flexibility, and system efficiency. Our Network VP® Satellite combines modular flexibility, ease of use, and increased control in a single controller with programming to the individual station level that supports station-based flow management. Our Turf Guard® wireless soil monitoring systems are designed to measure soil moisture, salinity, and temperature through buried wireless sensors that communicate through an Internet server for processing and presentation to a user through the web. In fiscal 2009, we introduced the ProCore® SR series of deep-tine aerators that feature remote depth adjustment for aeration depths of up to 16 inches. Late in fiscal 2009, we acquired a versatile line of topdressing and material handling equipment that enhances our product offering of application and cultivation equipment to help customers achieve improved agronomic conditions of turf.

Residential/Commercial Irrigation Market. Turf irrigation products marketed under the Toro and Irritrol brands include sprinkler heads, plastic and brass valves, and electric and hydraulic control devices designed to be used in residential and commercial turf irrigation systems. These products are professionally installed as new systems and can also be used to replace or retrofit existing systems. Most of the product line is designed for underground irrigation systems. Electric and hydraulic controllers activate valves and sprinkler heads in a typical irrigation system. We also offer wired and wireless rain and freeze switches on some products in an effort to conserve water usage. Our IntelliSense™ and Rain Master® controllers self-adjust their watering schedules based on current environmental conditions. In fiscal 2009, we introduced a new line of Precision™ Series Spray nozzles, featuring our patented H2O Chip Technology that reduces runoff and water use without affecting plant health.

Our retail irrigation products are marketed under the Toro and Lawn Genie brand names. These products are designed for homeowner installation and include sprinkler heads, valves, timers, and drip irrigation systems. Our ECXTRA™ sprinkler timers can be used with a home computer, and our Scheduling Advisor™ recommends the proper watering schedule based on the local weather, plant type, and sprinkler.

Micro-Irrigation Market. Products for the micro-irrigation market include products that regulate the flow of water for drip irrigation, including Aqua-TraXX® PBX drip tape, Aqua-TraXX® PC (pressure-compensating) drip tape, Blue Stripe® polyethylene tubing, and Drip In® drip line, all used in agriculture, mining, and landscape applications. In addition to these core products, we offer a full complement of control devices and connection options to complete the system. These products are sold primarily through dealers and distributors who then sell to end-users for use primarily in vegetable fields, fruit and nut orchards, vineyards, landscapes, and mines.

Residential – We market our residential products to homeowners through a variety of distribution channels, including outdoor power equipment dealers, hardware retailers, home centers, mass retailers, and over the Internet. These products are sold mainly in North America, Europe, and Australia, with the exception of snow removal products that are sold primarily in North America and Europe. We also license our trade name to other manufacturers and retailers on certain products as a means of expanding our brand presence.

Walk Power Mower Products. We manufacture and market numerous walk power mower models under our Toro and Lawn-Boy brand names, as well as the Pope brand in Australia and the Hayter brand in the United Kingdom. Models differ as to cutting width, type of starter mechanism, method of grass clipping discharge, deck type, operational controls, and power sources, and are either self-propelled or push mowers. We also offer a line of rear roller walk power mowers, a design that provides a striped finish, for the United Kingdom market. In fiscal 2009, we introduced a new line of Lawn-Boy walk-power mowers, designed for price sensitive buyers seeking the quality and features of a Lawn-Boy. In fiscal 2009, we also introduced a new line of Toro Recycler® walk-power mowers with our innovative Bag on Demand feature and a line of Toro Super Bagger walk-power mowers with our newly designed Superior Bagging System.

Riding Products. We manufacture and market riding products under the Toro brand name worldwide and under the Hayter brand name in the United Kingdom. We also manufacture riding mower products and attachments for a third party under a private label

4

agreement. Riding products primarily consist of zero-turn radius mowers that save homeowners time by using their superior maneuverability to cut around obstacles more quickly and easily than tractor technology. We also sell lawn and garden tractor models, as well as a rear engine riding mower manufactured and sold in the European market. Many models are available with a variety of engines, decks, transmissions, and accessories. In fiscal 2009, we introduced the all new Toro TITAN® heavy-duty residential zero-turn mowers, combining user-friendly features with features inspired by those found on our commercial zero-turn mowers.

Home Solutions Products. We design and market home solutions products under the Toro and Pope brand names, including electric and battery operated flexible line grass trimmers, electric blower-vacuums, electric blowers, and electric snow throwers. In Australia, we also design and market underground and hose-end retail irrigation products under the Pope brand name.

Gas Snow Removal Products. We manufacture and market a range of gas-powered single-stage and two-stage snow thrower models. Single-stage snow throwers are walk behind units with lightweight two- and four-cycle gasoline engines. Most single-stage snow thrower models include Power Curve® snow thrower technology and some feature our Quick Shoot™ control system that enables operators to quickly change snow throwing direction. Our innovative pivoting scraper also keeps the rotor in constant contact with the pavement. Our two-stage snow throwers are generally designed for relatively large areas of deep, heavy snow and use four-cycle engines. Our two-stage snow throwers include a line of innovative models featuring the Power Max® auger system for enhanced performance and the Quick Stick® chute control technology.

Financial Information about Foreign Operations

and Business Segments

We manufacture our products in the United States, Mexico, Australia, Italy, and the United Kingdom for sale throughout the world and maintain sales offices in the United States, Belgium, the United Kingdom, France, Australia, Singapore, Japan, China, Italy, and Korea. New product development is pursued primarily in the United States. Our net sales outside the United States were 32.0 percent, 32.4 percent, and 29.0 percent of total consolidated net sales for fiscal 2009, 2008, and 2007, respectively.

A portion of our cash flow is derived from sales and purchases denominated in foreign currencies. To reduce the uncertainty of foreign currency exchange rate movements on these sales and purchase commitments, we enter into foreign currency exchange contracts for select transactions. For additional information regarding our foreign currency exchange contracts, see Part II, Item 7A, "Quantitative and Qualitative Disclosures about Market Risk" of this report. For additional financial information regarding our foreign operations and each of our three reportable business segments, see Note 12 of the notes to our consolidated financial statements, in the section entitled "Segment Data," included in Part II, Item 8, "Financial Statements and Supplementary Data" of this report.

Engineering and Research

We are committed to an ongoing engineering program dedicated to developing innovative new products and improvements in the quality and performance of existing products. However, a focus on innovation also carries certain risks that new technology could be slow to be accepted or not accepted by the marketplace. We attempt to mitigate this risk through our focus on and commitment to understanding our customers' needs and requirements. We are investing more time upfront with customers, using "Voice of the Customer" tools to ensure we develop innovative products that meet or exceed customer expectations. We also use Design for Manufacturing and Assembly (DFMA) tools to ensure early manufacturing involvement in new product designs to reduce production costs. DFMA focuses on reducing the number of parts required to assemble new products as well as designing products to move more efficiently through the manufacturing process. We are also making improvements to our new product development system as part of our Lean initiatives to shorten development time, reduce costs, and improve quality.

Our engineering expenses are primarily incurred in connection with the development of new products that may have additional applications or represent extensions of existing product lines, improvements to existing products, and cost reduction efforts. Our expenditures for engineering and research were $52.7 million (3.5 percent of net sales) in fiscal 2009, $63.0 million (3.4 percent of net sales) in fiscal 2008, and $59.9 million (3.2 percent of net sales) in fiscal 2007.

Manufacturing and Production

In some areas of our business we serve as a fully integrated manufacturer, while in others we are primarily an assembler. We have strategically identified specific core manufacturing competencies for vertical integration and have chosen outside vendors to provide other services. We design component parts in cooperation with our vendors, contract with them for the development of tooling, and then enter into agreements with these vendors to purchase component parts manufactured using the tooling. In addition, our vendors regularly test new technologies to be applied to the design and production of component parts. Manufacturing operations include robotic and computer-automated equipment to speed production, reduce costs, and improve the quality, fit, and finish of products. Operations are also designed to be flexible enough to accommodate product design changes that are necessary to respond to market demand.

In order to utilize our manufacturing facilities and technology more effectively, we pursue continuous improvements in our manufacturing processes with the use of Lean methods that are

5

intended to streamline work and eliminate waste. We also have flexible assembly lines that can handle a wide product mix and deliver products to meet customer demand. Additionally, we spend considerable effort to reduce manufacturing costs through Lean methods and process improvement, product and platform design, application of advanced technologies, enhanced environmental management systems, SKU consolidation, safety improvements, and improved supply-chain management. We also manufacture products sold under a private label agreement to a third party on a competitive basis, and we have agreements with other third party manufacturers to manufacture products on our behalf.

Our professional products are manufactured throughout the year. Our residential lawn and garden products are also generally manufactured throughout the year. However, our residential snow removal equipment products are generally manufactured in the summer and fall months but may be extended into the winter months depending upon demand. Our products are tested in conditions and locations similar to those in which they are used. We use computer-aided design and manufacturing systems to shorten the time between initial concept and final production. DFMA principles are used throughout the product development process to optimize product quality and cost.

Our production levels and inventory management goals are based on estimates of retail demand for our products, taking into account production capacity, timing of shipments, and field inventory levels. In fiscal 2009, we continued to roll-out a pull-based production system at some of our manufacturing facilities to better synchronize the production of our products to meet customer demand at just the right time. Along with improved service levels for our participating suppliers, distributors, and dealers, the program has resulted in inventory reductions for us and throughout the distribution system.

We periodically shut down production at our manufacturing facilities in order to allow for maintenance, rearrangement, capital equipment installation, and as needed to adjust for market demand. Capital expenditures for fiscal 2010 are planned to be approximately $40 to $45 million as we expect to continue to invest in new product tooling, replacement production equipment, and expansion of our vertical integration capabilities.

Raw Materials

During the first half of fiscal 2009, we experienced higher average commodity costs compared to the average prices paid for commodities in fiscal 2008. During the second half of fiscal 2009, prices paid for commodities declined, which offset the negative impact of higher commodity costs on our gross margin rate during the first half of fiscal 2009. We have offset, and expect to continue to mitigate, commodity cost increases in part by continuing efforts to engage in proactive vendor negotiations, review alternative sourcing options, substitute materials, engage in internal cost reduction efforts, and increase prices on some of our products, as appropriate.

Most of the components of our products are also affected by commodity cost pressures and are commercially available from a number of sources. In fiscal 2009, we experienced no significant work stoppages as a result of shortages of raw materials or commodities. The highest raw material and component costs are generally for steel, engines, hydraulic components, transmissions, plastic resin, and electric motors, which are purchased from several suppliers around the world.

Service and Warranty

Our products are warranted to ensure customer confidence in design, workmanship, and overall quality. Warranty length varies depending on whether product usage is for "residential" or "professional" applications within individual product lines. Warranty coverage ranges from a period of six months to seven years and generally covers parts, labor, and other expenses for non-maintenance repairs. Warranty coverage generally does not cover operator abuse or improper use. An authorized distributor or dealer must perform warranty work. Distributors and dealers submit claims for warranty reimbursement and are credited for the cost of repairs, labor, and other expenses as long as the repairs meet our prescribed standards. Warranty expense is accrued at the time of sale based on the type and estimated number of products under warranty, historical average costs incurred to service warranty claims, the trend in the historical ratio of claims to sales, the historical length of time between the sale and resulting warranty claim, and other minor factors. Special warranty reserves are also accrued for major rework campaigns. Service support outside of the warranty period is provided by distributors and dealers at the customer's expense. We also sell extended warranty coverage on select products for a prescribed period after the factory warranty period expires.

Product Liability

We have rigorous product safety standards and work continually to improve the safety and reliability of our products. We monitor for accidents and possible claims and establish liability estimates with respect to claims based on internal evaluations of the merits of individual claims. We purchase excess insurance coverage for catastrophic product liability claims for incidents that exceed our self-insured retention levels.

Patents and Trademarks

We hold patents in the United States and foreign countries and apply for patents as applicable. Although we believe our patents are valuable and patent protection is beneficial, our patent protection will not necessarily deter or prevent competitors from attempting to develop similar products. We are not materially dependent on any one or more of our patents.

6

To prevent possible infringement of our patents by others, we periodically review competitors' products. To help avoid potential liability with respect to others' patents, we regularly review certain patents issued by the United States Patent and Trademark Office (USPTO) and foreign patent offices. We believe these activities help us minimize our risk of being a defendant in patent infringement litigation. We are currently involved in patent litigation cases, both where we are asserting patents and where we are defending against charges of infringement. While the ultimate result of our current cases are unknown at this time, we believe that the outcome of these cases is unlikely to have a material effect on our consolidated financial condition or results of operations.

Seasonality

Sales of our residential products, which accounted for approximately 35 percent of total consolidated net sales in fiscal 2009, are seasonal, with sales of lawn and garden products occurring primarily between February and May, and sales of snow removal equipment occurring primarily between July and January. Opposite seasons in some global markets somewhat moderate this seasonality of residential product sales. Seasonality of professional product sales also exists but is tempered because the selling season in the Southern states and in our markets in the Southern hemisphere continues for a longer portion of the year than in Northern regions of the world.

Overall, worldwide sales levels are historically highest in our fiscal second quarter and retail demand is generally highest in our fiscal third quarter. Typically, accounts receivable balances increase between January and April as a result of higher sales volumes and extended payment terms made available to our customers. Accounts receivable balances decrease between May and December when payments are received. Our financing requirements are subject to variations due to seasonal changes in working capital levels which typically increase in the first half of our fiscal year and then decrease in the second half of our fiscal year. Seasonal cash requirements of our business are financed from a combination of cash balances, cash flows from operations, and our bank credit lines. Peak borrowing generally occurs between January and April.

The following table shows total consolidated net sales and net earnings for each fiscal quarter as a percentage of the total fiscal year.

|

Fiscal 2009 | Fiscal 2008 | |||||||||||

|

Net Sales |

Net Earnings (Loss) |

Net Sales | Net Earnings |

|||||||||

First |

22 | % | 11 | % | 22 | % | 16 | % | |||||

Second |

33 | 59 | 34 | 52 | |||||||||

Third |

26 | 31 | 26 | 32 | |||||||||

Fourth |

19 | (1 | ) | 18 | – | ||||||||

Effects of Weather

From time to time, weather conditions in a particular region or market may adversely or positively affect sales of some of our products and field inventory levels and result in a negative or positive impact on our future net sales. As the percentage of our net sales from outside the United States increases, our dependency on weather in any one part of the world decreases. Nonetheless, weather conditions could materially affect our future net sales.

Working Capital

We fund our operations through a combination of cash and cash equivalents, cash flows from operations, short-term borrowings under our credit facilities, and long-term debt. Wherever possible, cash management is centralized and intercompany financing is used to provide working capital to subsidiaries as needed. In addition, our credit facilities are available for additional working capital needs, acquisitions, or other investment opportunities.

Distribution and Marketing

We market the majority of our products through approximately 40 domestic and 110 foreign distributors, as well as a large number of outdoor power equipment dealers, hardware retailers, home centers, and mass retailers in more than 90 countries worldwide.

Residential products, such as walk power mowers, riding products, and snow throwers, are mainly sold directly to home centers, dealers, hardware retailers, and mass retailers. In certain markets, these same products are sold to distributors for resale to retail dealers. Home solutions products are primarily sold directly to home centers, mass retailers, hardware retailers, and dealers. We also sell selected residential products over the Internet. Internationally, residential products are sold directly to dealers and mass merchandisers in Australia, Belgium, Canada, and the United Kingdom. In most other countries, products are mainly sold to distributors for resale to dealers and mass retailers.

Professional products are sold mainly to distributors for resale to dealers, sports complexes, industrial facilities, contractors, municipalities, rental stores, and golf courses. We also sell some professional segment products directly to government customers and rental companies, as well as directly to end-users in certain international markets. Select residential/commercial irrigation products are also sold directly to professional irrigation distributors and certain retail irrigation products are sold directly to home centers. Compact utility loaders and attachments are sold to dealers and directly to large rental companies. Toro and Exmark landscape contractor products are also sold directly to dealers in certain regions of the United States.

During fiscal 2009, we owned one domestic distribution company. During the first quarter of fiscal 2010, our wholly owned distribution company completed the purchase of certain assets and assumed certain liabilities of an independent Midwestern-based distribution company. Our primary purposes in owning domestic

7

distributorships are to facilitate ownership transfers while improving operations and to test and deploy new strategies and business practices that could be replicated by our independent distributors.

Our distribution systems are intended to assure quality of sales and market presence as well as effective after-purchase service and support. We believe our distribution network provides a competitive advantage in marketing and selling our products in part because our primary distribution network is focused on selling and marketing our products and also because of long-term relationships they have established and experienced personnel they utilize to deliver high levels of customer satisfaction.

Our current marketing strategy is to maintain distinct brands and brand identification for Toro®, Exmark®, Irritrol®, Hayter®, Pope®, Lawn-Boy®, and Lawn Genie® products.

We advertise our residential products during appropriate seasons throughout the year on television, on the radio, in print, and via the Internet. Professional products are advertised in print and through direct mail programs, as well as on the Internet. Most of our advertising emphasizes our brand names. Advertising is purchased by us as well as through cooperative programs with distributors, dealers, hardware retailers, home centers, and mass retailers.

Customers

Overall, we believe that in the long-term we are not dependent on any single customer. However, The Home Depot accounted for approximately 14 percent of our total consolidated gross sales in fiscal 2009. The residential segment of our business is dependent on The Home Depot as a customer. While the loss of any substantial customer, including The Home Depot, could have a material adverse short-term impact on our business, we believe that our diverse distribution channels and customer base should reduce the long-term impact of any such loss.

Backlog of Orders

Our backlog of orders is dependent upon when customers place orders, and not necessarily an indicator of our expected results for the first quarter of fiscal 2010 or our fiscal 2010 net sales. The approximate backlog of orders believed to be firm as of October 31, 2009 and 2008 was $85.1 million and $77.9 million, respectively, an increase of 9.2 percent. This increase was primarily the result of open orders for snow thrower products due to the timing of the introduction for a new redesigned offering of snow thrower products that shipped in the first quarter of fiscal 2010. We expect the existing backlog of orders will be filled in early fiscal 2010.

Competition

Our products are sold in highly competitive markets throughout the world. The principal competitive factors in our markets are product innovation, quality and reliability, product support and customer service, pricing, warranty, brand awareness, reputation, distribution, shelf space, and financing options. Pricing volatility has become an increasingly important competitive factor for a majority of our products. We believe we offer total solutions and full service packages with high quality products that have the latest technology and design innovations. Also, by selling our products through a network of distributors, dealers, hardware retailers, home centers, and mass retailers, we offer comprehensive service support during and after the warranty period. We compete in many product lines with numerous manufacturers, many of which have greater operations and financial resources than us. We believe that we have a competitive advantage because we manufacture a broad range of product lines, we are committed to product innovation and customer service, we focus on Lean manufacturing methods, we have a strong focus in maintaining landscapes, and our distribution channels position us well to compete in various markets.

Internationally, residential segment products face more competition where foreign competitors manufacture and market products in their respective countries. We experience this competition primarily in Europe. In addition, fluctuations in the value of the U.S. dollar may affect the price of our products in foreign markets, thereby impacting their competitiveness. We provide pricing support to foreign customers, as needed, to remain competitive in international markets.

Environmental Matters and

Other Governmental Regulation

We are subject to numerous federal, state, international, and other governmental laws, rules, and regulations relating to, among others, climate change; emissions to air and discharges to water; product and associated packaging; import and export compliance, including country of origin certification requirements; worker and product user health and safety; and the generation, use, handling, labeling, collection, management, storage, transportation, treatment, and disposal of hazardous substances, wastes, and other regulated materials. For example:

- •

- The United States Environmental Protection Agency (EPA), the California Air Resources Board, and similar regulators in other U.S. states and foreign jurisdictions in which we sell our products have phased in, or are phasing in, certain emission regulations setting maximum emission standards for certain equipment.

- •

- Certain U.S. states and foreign jurisdictions in which we sell our products, including the European Union (EU), and each of its member states, have implemented (i) the Waste Electrical and Electronic Equipment (WEEE) directive or similar substance level laws, rules, or regulations, which mandate the labeling, collection, and disposal of certain waste electrical and electronic equipment, (ii) the Restriction on the use of Hazardous Substances (RoHS) directive or similar substance level laws, rules, or regulations, which restrict the use of several specified hazardous materials in the manufacture of specific types of electrical

8

and electronic equipment, and (iii) country of origin laws, rules, or regulations, which require certification of the geographic origin of finished goods and/or components through documentation and/or physical markings, as applicable.

- •

- Our residential products are subject to various federal, state, and international laws, rules, and regulations that are designed to protect consumers and we are subject to the administrative jurisdiction of the Consumer Product Safety Commission.

Although we believe that we are in substantial compliance with applicable laws, rules, and regulations, we are unable to predict the ultimate impact of adopted or future laws, rules, and regulations on our business. Such laws, rules, or regulations may cause us to incur significant expenses to achieve or maintain compliance, may require us to modify our products, may adversely affect the demand for some of our products, and may ultimately affect the way we conduct our operations. Failure to comply with these regulations could lead to fines and other penalties, including restrictions on the importation of our products into, or the sale of our products in, one or more jurisdictions until compliance is achieved.

We are also involved in the evaluation and clean-up of a limited number of properties currently and previously owned. We do not expect that these matters will have a material adverse effect on our consolidated financial position or results of operations.

Customer Financing

Wholesale Financing. Toro Credit Company (TCC), our wholly owned finance subsidiary, provided financing throughout most of fiscal 2009 for select products that we manufacture and sell to our U.S. distributors, select distributors of our products in Canada, and approximately 150 select U.S. dealers. In October 2009, TCC sold its receivable portfolio to Red Iron Acceptance, LLC (Red Iron), a recently established joint venture between Toro and TCF Inventory Finance, Inc. (TCFIF), a subsidiary of TCF National Bank. Red Iron provides inventory financing, including floor plan financing, to distributors and dealers of our products in the U.S. and to select distributors of our products in Canada. Under a separate arrangement, TCF Commercial Finance Canada, Inc. (TCFCFC) implemented a program to provide inventory financing to dealers of our products in Canada during the first quarter of fiscal 2010. In connection with the establishment of the joint venture, we terminated our agreement with a third party financing company that previously provided floor plan financing to dealers of our products in the U.S. and Canada. Red Iron began financing open account receivables, as well as floor plan receivables previously financed by such third party financing company, during our first quarter of fiscal 2010. Under these financing arrangements, down payments are not required and, depending on the finance program for each product line, finance charges are incurred by us, shared between us and the distributor and/or the dealer, or paid by the distributor or dealer. Red Iron retains a security interest in the distributors' and dealers' financed inventories, and those inventories are monitored regularly. Floor plan terms to the distributors and dealers require payment as the equipment, which secures the indebtedness, is sold to customers, or when payment terms become due, whichever occurs first. Rates are generally indexed to LIBOR plus a fixed percentage that differs based on whether the financing is for a distributor or dealer. Rates may also vary based on the product that is financed.

We continue to provide inventory financing to mass market retail customers; general line irrigation dealers; wholly owned distributors; international distributors and dealers, excluding the Canadian distributors and dealers that Red Iron provides financing arrangements; and government entity customers. Some independent international dealers continue to finance their products with third party sources.

End-User Financing. We have agreements with third party financing companies to provide lease-financing options to golf course and sports fields and grounds equipment customers in the U.S. and Europe. The purpose of these agreements is to increase sales by giving buyers of our products alternative financing options when purchasing our products.

We also have agreements with third party financing companies to provide financing programs under a private label program in the U.S. This program, offered primarily to Toro and Exmark dealers, provides end-user customers a revolving line of credit for Toro and Exmark products, parts, and services.

Distributor Financing. Occasionally, we enter into long-term loan agreements with some distributors. These transactions are used for expansion of the distributors' businesses, acquisitions, refinancing working capital agreements, or ownership transitions.

Employees

During fiscal 2009, we employed an average of 4,612 employees. The total number of employees as of October 31, 2009 was 4,414. We consider our employee relations to be good. Three collective bargaining agreements cover approximately 17 percent of these employees. These three agreements expire in May 2010, October 2010, and October 2011. From time to time, we also retain temporary and part-time workers, independent contractors, and consultants.

Available Information

Filings with the SEC. We are a reporting company under the Securities Exchange Act of 1934, as amended, and file reports, proxy statements, and other information with the Securities and Exchange Commission (SEC). Copies of these reports, proxy statements, and other information can be inspected and copied at the SEC's Public Reference Room at 100 F Street N.E., Washington, D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at

9

1-800-SEC-0330. Because we make filings to the SEC electronically, you may also access this information from the SEC's home page on the Internet at http://www.sec.gov.

We make available, free of charge on our Internet web site www.thetorocompany.com (select the "Investor Information" link and then the "Financials" link), our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements on Schedule 14A, amendments to those reports, and other documents filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The information contained on our web site or connected to our web site is not incorporated by reference into this Annual Report on Form 10-K and should not be considered part of this report.

Corporate Governance. We have a Code of Ethics for our CEO and Senior Financial Officers, a Code of Conduct for all employees, and a Board of Directors Business Ethics Policy Statement. Copies of these documents are posted on our website at www.thetorocompany.com (select the "Investor Information" link and then the "Corporate Governance" link).

We also make available, free of charge on our web site at www.thetorocompany.com (select the "Investor Information" link and then the "Corporate Governance" link) and in print to any shareholder who requests, our Corporate Governance Guidelines and the charters of our Audit Committee, Compensation and Human Resources Committee, Nominating and Governance Committee, and Finance Committee of our Board of Directors. Requests for copies can be directed to Investor Relations at 888-237-3054.

We have furnished to the SEC the required certifications under Section 302 of the Sarbanes-Oxley Act of 2002 regarding the quality of our public disclosures as Exhibits 31.1 and 31.2 to this report. We have filed with the New York Stock Exchange (NYSE) the CEO certification regarding our compliance with the NYSE's corporate governance listing standards as required by NYSE Rule 303A.12(a) on March 18, 2009.

Forward-Looking Statements

This Annual Report on Form 10-K contains, or incorporates by reference, not only historical information, but also forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, and that are subject to the safe harbor created by those sections. In addition, we or others on our behalf may make forward-looking statements from time to time in oral presentations, including telephone conferences and/or web casts open to the public, in press releases or reports, on our web sites or otherwise. Statements that are not historical are forward-looking and reflect expectations and assumptions. We try to identify forward-looking statements in this report and elsewhere by using words such as "expect," "strive," "looking ahead," "outlook," "forecast," "optimistic," "anticipate," "continue," "plan," "estimate," "believe," "should," "could," "will," "would," "possible," "may," "likely," "intend," and similar expressions or future dates. Our forward-looking statements generally relate to our future performance, including our anticipated operating results, liquidity requirements, and financial condition; our business strategies and goals; and the effect of laws, rules, regulations, new accounting pronouncements, and outstanding litigation on our business and future performance.

Forward-looking statements involve risks and uncertainties. These risks and uncertainties include factors that affect all businesses operating in a global market as well as matters specific to Toro. The most significant factors known to us that could materially adversely affect our business, operations, industry, financial position, or future financial performance are described below in Part I, Item 1A,"Risk Factors." We wish to caution readers not to place undue reliance on any forward-looking statement which speaks only as of the date made and to recognize that forward-looking statements are predictions of future results, which may not occur as anticipated. Actual results could differ materially from those anticipated in the forward-looking statements and from historical results, due to the risks and uncertainties described elsewhere in this report, including in Part I, Item 1A, "Risk Factors," as well as others that we may consider immaterial or do not anticipate at this time. The risks and uncertainties described in this report, including in Part I, Item 1A, "Risk Factors," are not exclusive and further information concerning our company and our businesses, including factors that potentially could materially affect our operating results or financial condition, may emerge from time to time.

We assume no obligation to update forward-looking statements to reflect actual results or changes in factors or assumptions affecting such forward-looking statements. We advise you, however, to consult any further disclosures we make on related subjects in our future quarterly reports on Form 10-Q and current reports on Form 8-K that we file with or furnish to the SEC.

10

The following are significant factors known to us that could materially adversely affect our business, operating results, financial condition, or future financial performance.

Economic conditions and outlook in the United States and around the world could continue to adversely affect our net sales and earnings.

Demand for our products depends upon economic conditions and outlook, which include but are not limited to recessionary conditions in the U.S. and other regions around the world and worldwide slow or negative economic growth rates; slow down or reductions in levels of golf course development, renovation, and improvement; slow down or reductions in levels of home ownership, construction, and home sales; consumer spending levels; credit availability and credit terms for our distributors, dealers, and end-user customers; short-term, mortgage, and other interest rates; unemployment rates; interest rates; inflation; consumer confidence; and general economic and political conditions and expectations in the U.S. and the foreign economies in which we conduct business. Slow or negative economic growth rates; inflationary pressures; higher commodity costs and fuel prices; slow downs or reductions in golf course development, renovation, and improvement; slow downs or reductions in home construction and sales; home foreclosures; reduced credit availability or unfavorable credit terms for our distributors, dealers, and end-user customers; higher short-term, mortgage, and other interest rates; unemployment rates; and recessionary economic conditions and outlook could cause our distributors, dealers, and end-user customers to reduce spending, which may cause them to delay or forego purchases of our products and could have an adverse effect on our net sales and earnings.

Increases in the cost, or disruption in the availability, of raw materials and components that we purchase and increases in our other costs of doing business, such as transportation costs, may adversely affect our profit margins and business.

We purchase raw materials such as steel, aluminum, fuel, petroleum-based resins, linerboard, and other commodities, and components, such as engines, transmissions, transaxles, hydraulics, and electric motors, for use in our products. Increases in the cost of such raw materials and components may adversely affect our profit margins if we are unable to pass along to our customers these cost increases in the form of price increases or otherwise reduce our cost of goods sold. Historically, we have used internal cost reduction efforts, proactive vendor negotiations, alternate sourcing options, substitute materials, and moderate price increases on some of our products to offset a portion of increased raw material, component, and other costs. However, we may not be able to fully offset any such increased costs in the future. Further, if our price increases are not accepted by our customers and the market, our net sales, earnings, and market share could be adversely affected. Although most of the raw materials and components used in our products are commercially available from a number of sources and in adequate supply, any disruption in the availability of such raw materials and components, our inability to timely or otherwise obtain substitutes for such items, or any deterioration in our relationships with or the financial viability of our suppliers could adversely affect our business. Increases in our other costs of doing business may also adversely affect our profit margins and business. For example, an increase in fuel costs may result in an increase in our transportation costs, which also could adversely affect our operating results and business.

Weather conditions may reduce demand for some of our products and adversely affect our net sales.

From time to time, weather conditions in a particular geographic region may adversely affect sales of some of our products and field inventory levels. For example, in the past, drought conditions have had an adverse effect on sales of certain mowing equipment products, unusually rainy weather or severe drought conditions that result in watering bans have had an adverse effect on sales of our irrigation products, and lower snow fall accumulations in key markets have had an adverse effect on sales of our snow thrower products. To the extent that such unfavorable weather conditions are exacerbated by global climate change or otherwise, our sales may be affected to a greater degree than we have previously experienced.

Our professional segment net sales are dependent upon the level of residential and commercial construction, the level of homeowners' outsourcing lawn care, the amount of investment in golf course renovations and improvements, new golf course development, golf course closures, the amount of government spending, and other factors.

Our professional segment products are sold by distributors or dealers, or directly to government customers, rental companies, and professional users engaged in maintaining and creating landscapes, such as golf courses, sports fields, municipal properties, and residential and commercial landscapes. Accordingly, our professional segment net sales are impacted by the level of residential and commercial construction, the level of homeowners' outsourcing lawn care, the amount of investment in golf course renovations and improvements, new golf course construction, availability of credit to finance product purchases, and the amount of

11

government spending. Among other things, any one or a combination of the following factors could have an adverse effect on our professional segment net sales:

- •

- reduced tax revenue, increased governmental expenses in other areas, tighter government budgets and government deficits, generally resulting in reduced government spending for grounds maintenance equipment;

- •

- reduced consumer and business spending, causing homeowners not to outsource lawn care and causing landscape contractor professionals to forego or postpone purchases of our products;

- •

- reduced levels of commercial and residential construction, resulting in a decrease in demand for our products; and

- •

- reduced levels of new golf course construction and investment in golf course renovations and improvements, reduced number of golf rounds played at public and private golf courses resulting in reduced revenue for such golf courses, decreased membership at private golf courses resulting in reduced revenue and, in certain cases, financial difficulties for such golf courses, and golf course closures, any of which could result in a decrease in spending and demand for our products.

Our residential segment net sales are dependant upon consumer spending levels, the amount of product placement at retailers, changing buying patterns of customers, and The Home Depot, Inc. as a major customer.

The elimination or reduction of shelf space assigned to our residential products by retailers could adversely affect our residential segment net sales. Our residential segment net sales are also dependent upon changing buying patterns of customers. For example, there has been a trend away from purchases at dealer outlets and hardware retailers to home centers and mass retailers, as well as a trend for broader and lower price points at home centers and mass retailers. This trend has resulted in a demand for residential products purchased at retailers, such as The Home Depot, which accounted for approximately 10 to 14 percent of our total consolidated net sales in each of fiscal 2009, 2008, and 2007. We believe that our diverse distribution channels and customer base should reduce the long-term impact on us if we were to lose The Home Depot or any other substantial customer. However, the loss of any substantial customer, a significant reduction in sales to The Home Depot or other customers, or our inability to respond to future changes in buying patterns of customers and new distribution channels could have a material impact on our business and operating results. Changing buying patterns of customers also could result in reduced sales of one or more of our residential segment products, resulting in increased inventory levels. Although our residential lawn and garden products are generally manufactured throughout the year, our residential snow removal equipment products are generally manufactured in the summer and fall months but may be extended into the winter months depending upon demand. Our production levels and inventory management goals are based on estimates of retail demand for our products, taking into account production capacity, timing of shipments, and field inventory levels. If we overestimate or underestimate demand during a given season, we may not maintain the appropriate inventory levels, which could negatively impact our net sales, working capital, or hinder our ability to meet customer demand.

If we are unable to continue to enhance existing products and develop and market new products that respond to customer needs and preferences and achieve market acceptance, we may experience a decrease in demand for our products, and our business could suffer.

One of our growth strategies is to develop innovative, customer-valued products to generate revenue growth. Our sales from new products in the past have represented a significant component of our net sales and are expected to continue to represent a significant component of our future net sales. We may not be able to compete as effectively with our competitors, and ultimately satisfy the needs and preferences of our customers, unless we can continue to enhance existing products and develop new innovative products in the markets in which we compete. Product development requires significant financial, technological, and other resources. Although in the past we have implemented Lean manufacturing and other productivity improvement initiatives to provide investment funding for product enhancements and new products, we cannot be certain that we will be able to continue to do so in the future. Product improvements and new product introductions also require significant planning, design, development, and testing at the technological, product, and manufacturing process levels and we may not be able to timely develop product improvements or new products. Our competitors' new products may beat our products to market, be more effective with more features and/or less expensive than our products, obtain better market acceptance, or render our products obsolete. Any new products that we develop may not receive market acceptance or otherwise generate any meaningful net sales or profits for us relative to our expectations based on, among other things, existing and anticipated investments in manufacturing capacity and commitments to fund advertising, marketing, promotional programs, and research and development.

12

We face intense competition in all of our product lines with numerous manufacturers, including from some that have greater operations and financial resources than us. We may not be able to compete effectively against competitors' actions, which could harm our business and operating results.

Our products are sold in highly competitive markets throughout the world. Principal competitive factors in our markets include product innovation, quality and reliability, product support and customer service, pricing, warranty, brand awareness, reputation, distribution, shelf space, and financing options. We compete in all of our product lines with numerous manufacturers, some which have substantially greater operations and financial resources than us. As a result, they may be able to adapt more quickly to new or emerging technologies and changes in customer preferences, or to devote greater resources to the development, promotion, and sale of their products than we can. In addition, competition could increase if new companies enter the market or if existing competitors expand their product lines or intensify efforts within existing product lines. Our current products, products under development, and our ability to develop new and improved products may be insufficient to enable us to compete effectively with our competitors. Internationally, our residential segment products typically face more competition where foreign competitors manufacture and market products in their respective countries. We experience this competition primarily in Europe. In addition, fluctuations in the value of the U.S. dollar may affect the price of our products in foreign markets, thereby impacting their competitiveness. Pricing volatility has also become an increasingly important competitive factor for many of our products. We may not be able to compete effectively against competitors' actions, which may include the movement by competitors of significant manufacturing to low cost countries for significant cost and price reductions, and could harm our business and operating results.

A significant percentage of our consolidated net sales are generated outside of the United States, and we intend to continue to expand our international operations. Our international operations require significant management attention and financial resources, expose us to difficulties presented by international economic, political, legal, accounting, and business factors, and may not be successful or produce desired levels of net sales.

We manufacture our products in the United States, Mexico, Australia, the United Kingdom, and Italy for sale throughout the world and maintain sales offices in the United States, Belgium, the United Kingdom, France, Australia, Singapore, Japan, China, Italy, and Korea. Our net sales outside the United States were 32.0 percent, 32.4 percent, and 29.0 percent of our total consolidated net sales for fiscal 2009, 2008, and 2007, respectively. International markets have, and will continue to be, a focus for revenue growth. We believe many opportunities exist in the international markets, and over time we intend for international net sales to comprise a larger percentage of our total consolidated net sales. Several factors, including weakened international economic conditions, could adversely affect such growth. Additionally, the expansion of our existing international operations and entry into additional international markets require significant management attention and financial resources. Many of the countries in which we sell our products, or otherwise have an international presence are, to some degree, subject to political, economic, and/or social instability, including cartel-related violence. Our international operations expose us and our representatives, agents, and distributors to risks inherent in operating in foreign jurisdictions. These risks include:

- •

- increased costs of customizing products for foreign countries;

- •

- difficulties in managing and staffing international operations and increases in infrastructure costs including legal, tax, accounting, and information technology;

- •

- the imposition of additional U.S. and foreign governmental controls or regulations; new or enhanced trade restrictions and restrictions on the activities of foreign agents, representatives, and distributors; and the imposition of increases in costly and lengthy import and export licensing and other compliance requirements, customs duties and tariffs, license obligations, and other non-tariff barriers to trade;

- •

- the imposition of U.S. and/or international sanctions against a country, company, person, or entity with whom we do business that would restrict or prohibit our continued business with the sanctioned country, company, person, or entity;

- •

- international pricing pressures;

- •

- laws and business practices favoring local companies;

- •

- adverse currency exchange rate fluctuations;

- •

- longer payment cycles and difficulties in enforcing agreements and collecting receivables through certain foreign legal systems;

- •

- difficulties in enforcing or defending intellectual property rights; and

- •

- multiple, changing, and often inconsistent enforcement of laws, rules, and regulations, including rules relating to environmental, health, and safety matters.

Our international operations may not produce desired levels of net sales or one or more of the factors listed above may harm our business and operating results. Any material decrease in our international sales or profitability could also adversely impact our operating results.

13

Fluctuations in foreign currency exchange rates could result in declines in our reported net sales and net earnings.

Because the functional currency of our foreign operations is the applicable local currency, we are exposed to foreign currency exchange rate risk arising from transactions in the normal course of business, such as sales and loans to wholly owned subsidiaries as well as sales to third party customers, purchases from suppliers, and bank lines of credit with creditors denominated in foreign currencies. Our reported net sales and net earnings are subject to fluctuations in foreign currency exchange rates. Because our products are manufactured or sourced primarily from the United States and Mexico, a stronger U.S. dollar and Mexican peso generally has a negative impact on results from operations, while a weaker dollar and peso generally has a positive effect. Our primary foreign currency exchange rate exposure is with the EU Euro, the Australian dollar, the Canadian dollar, the British pound, the Mexican peso, and the Japanese yen against the U.S. dollar. While we actively manage the exposure of our foreign currency market risk in the normal course of business by entering into various foreign exchange contracts, these instruments may not effectively limit our underlying exposure from currency exchange rate fluctuations or minimize our net earnings and cash volatility associated with foreign currency exchange rate changes. Further, a number of financial institutions similar to those that serve as counterparties to our foreign exchange contracts have been adversely affected by the unprecedented distress in the worldwide credit markets. The failure of one or more counterparties to our foreign currency exchange rate contracts to fulfill their obligations to us could adversely affect our operating results.

We manufacture our products at and distribute our products from several locations in the United States and internationally. Any disruption at any of these facilities or our inability to cost-effectively expand existing and/or move production between manufacturing facilities could adversely affect our business and operating results.

We manufacture most of our products at seven locations in the United States, two locations in Mexico, and one location in each of Australia, Italy, and the United Kingdom. We also have several locations that serve as distribution centers, warehouses, test facilities, and corporate offices. In addition, we have agreements to manufacture products at several third-party manufacturers. These facilities may be affected by natural or man-made disasters. In the event that one of our manufacturing facilities was affected by a disaster, we could be forced to shift production to one of our other manufacturing facilities. Although we purchase insurance for damage to our property and disruption of our business from casualties, such insurance may not be sufficient to cover all of our potential losses. Any disruption in our manufacturing capacity could have an adverse impact on our ability to produce sufficient inventory of our products or may require us to incur additional expenses in order to produce sufficient inventory, and therefore, may adversely affect our net sales and operating results. Any disruption or delay at our manufacturing facilities, including a work slowdown, strike, or similar action at any one of our three facilities operating under a collective bargaining agreement or the failure to renew or enter into new collective bargaining agreements, including two such agreements that expire in fiscal 2010, could impair our ability to meet the demands of our customers, and our customers may cancel orders or purchase products from our competitors, which could adversely affect our business and operating results. Our operating results may also be adversely affected if we are unable to cost-effectively expand existing and move production between manufacturing facilities as needed from time to time.

We intend to grow our business through additional acquisitions and alliances, stronger customer relations, and new joint ventures and partnerships, which are risky and could harm our business.

One of our growth strategies is to drive growth in our businesses and accelerate opportunities to expand our global presence through targeted acquisitions, alliances, stronger customer relations, and new joint ventures and partnerships that add value while considering our existing brands and product portfolio. The benefits of an acquisition or new joint venture or partnership may take more time than expected to develop or integrate into our operations, and we cannot guarantee that previous or future acquisitions, alliances, joint ventures, or partnerships will in fact produce any benefits. In addition, acquisitions, alliances, joint ventures, and partnerships involve a number of risks, including:

- •

- diversion of management's attention;

- •

- difficulties in integrating and assimilating the operations and products of an acquired business or in realizing projected efficiencies, cost savings, and synergies;

- •

- potential loss of key employees or customers of the acquired businesses or adverse effects on existing business relationships with suppliers and customers;

- •

- adverse impact on overall profitability if acquired businesses do not achieve the financial results projected in our valuation models;

- •

- reallocation of amounts of capital from other operating initiatives and/or an increase in our leverage and debt service requirements to pay the acquisition purchase prices, which could in turn restrict our ability to access additional capital when needed or to pursue other important elements of our business strategy;

- •

- inaccurate assessment of undisclosed, contingent or other liabilities or problems, unanticipated costs associated with an acquisition, and an inability to recover or manage such liabilities and costs; and

14

- •

- incorrect estimates made in the accounting for acquisitions, incurrence of non-recurring charges, and write-off of significant amounts of goodwill or other assets that could adversely affect our operating results.

Our ability to grow through acquisitions will depend, in part, on the availability of suitable acquisition candidates at acceptable prices, terms, and conditions, our ability to compete effectively for these acquisition candidates, and the availability of capital and personnel to complete such acquisitions and run the acquired business effectively. These risks could be heightened if we complete a large acquisition or multiple acquisitions within a relatively short period of time. In addition, some acquisitions may require the consent of the lenders under our credit agreements. We cannot predict whether such approvals would be forthcoming or the terms on which the lenders would approve such acquisitions. Any potential acquisition could impair our operating results, and any large acquisition could impair our financial condition, among other things.

As a result of our recently established financing joint venture, we are dependent upon the joint venture to provide competitive inventory financing programs, including floor plan and open account receivable financing, to certain distributors and dealers of our products. Any difficulty in transitioning our inventory financing programs to the joint venture, any material change in the availability or terms of credit offered to our customers by the joint venture, any termination or disruption of our joint venture relationship or any delay in securing replacement credit sources could adversely affect our net sales and operating results.

Historically, most of our dealers and distributors generally financed their inventories with either TCC, our wholly owned finance subsidiary, or third party financing companies. As a result of our recent joint venture with TCFIF, we are dependent upon the joint venture for our inventory financing programs, including floor plan and open account receivable financing, for distributors and dealers of our products in the U.S. and to select distributors of our products in Canada. The purpose of the joint venture is to provide access to reliable, competitive financing to our distributors and dealers in the U.S. and to select distributors of our products in Canada to support their businesses and increase our net sales, as well as to free up our working capital for other strategic purposes. Additionally, in connection with the joint venture, we are dependent upon TCFCFC to provide inventory financing to dealers of our products in Canada.