Attached files

| file | filename |

|---|---|

| EX-23.2 - EX-23.2 - First Wind Holdings Inc. | a2195887zex-23_2.htm |

| EX-16.1 - EX-16.1 - First Wind Holdings Inc. | a2195887zex-16_1.htm |

| EX-24.1 - EX-24.1 - First Wind Holdings Inc. | a2195887zex-24_1.htm |

| EX-23.1 - EX-23.1 - First Wind Holdings Inc. | a2195887zex-23_1.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on December 22, 2009

Registration No. 333-152671

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

First Wind Holdings Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) |

4911 (Primary Standard Industrial Classification Code Number) |

26-2583290 (I.R.S. Employer Identification Number) |

179 Lincoln Street, Suite 500

Boston, MA 02111

617-960-2888

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant's Principal Executive Offices)

Paul Gaynor

Chief Executive Officer

First Wind Holdings Inc.

179 Lincoln Street, Suite 500

Boston, MA 02111

617-960-2888

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copies to:

| Paul H. Wilson, Jr. Executive Vice President, General Counsel and Secretary First Wind Holdings Inc. 179 Lincoln Street, Suite 500 Boston, MA 02111 617-960-2888 |

Richard J. Sandler Joseph A. Hall Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 212-450-4000 |

Dennis M. Myers, P.C. Elisabeth M. Martin Kirkland & Ellis LLP 300 North LaSalle Chicago, IL 60654 312-862-2000 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this Registration Statement is declared effective.

If any securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended (the "Securities Act"), check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b 2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement relating to this prospectus filed with the Securities and Exchange Commission is declared effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED DECEMBER 22, 2009

Shares

First Wind Holdings Inc.

Class A Common Stock

We are offering shares of our Class A common stock and we intend to use the net proceeds of this offering to fund capital expenditures and for general corporate purposes.

We will be a holding company and our sole asset will be approximately % of the Series A Units of First Wind Holdings, LLC. Concurrently with the completion of this offering, we will issue and shares of Class A and Class B common stock, respectively, to the continuing members of First Wind Holdings, LLC.

Before this offering there has been no public market for our Class A common stock. The initial public offering price of our Class A common stock is expected to be between $ and $ per share. We have applied to list our Class A common stock on the Nasdaq Global Market under the symbol "WIND."

The underwriters have an option to purchase up to additional shares from us to cover over-allotments, if any.

Investing in our Class A common stock involves risks. See "Risk Factors" beginning on page 16.

|

||||||

| |

Price to Public |

Underwriting Discounts and Commissions |

Proceeds to First Wind Holdings Inc. |

|||

|---|---|---|---|---|---|---|

Per share |

$ | $ | $ | |||

Total |

$ | $ | $ | |||

|

||||||

Delivery of the shares of Class A common stock will be made on or about .

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is .

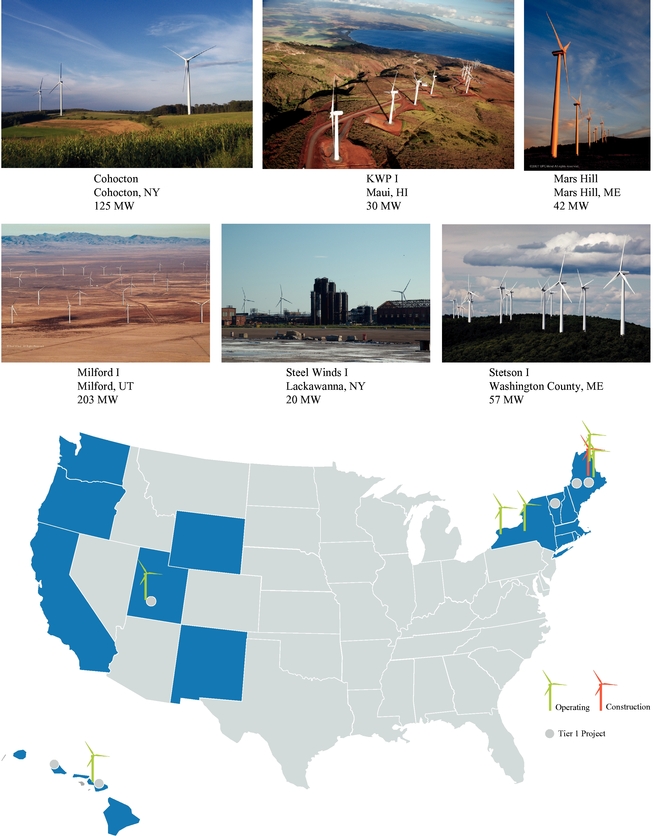

Highlighted areas represent states in which First Wind has projects in operation, under construction or in various stages of development. Green turbines represent operating projects, red turbines represent projects under construction, and the grey circles indicate the approximate locations of our Tier 1 development projects. See "Business—How We Classify Our Projects."

You should rely only on the information contained in this prospectus. We have not, and the underwriters have not, authorized anyone to provide you with different information. We are not making an offer to sell these securities in any state where an offer or sale is not permitted. You should not assume that the information appearing in this prospectus is accurate as of any date other than the respective dates as of which the information is given.

The service marks for our company name, "FIRST WIND", and our trademark "CLEAN ENERGY. MADE HERE." are the property of First Wind Holdings, LLC. All other trademarks and service marks appearing in this prospectus are the property of their respective holders. All rights reserved.

In this prospectus, unless the context otherwise requires, we refer to (i) First Wind Holdings Inc. and its subsidiaries, including First Wind Holdings, LLC, after giving effect to the reorganization described herein, as "First Wind," "we," "us," "our" or the "company"; (ii) entities in the D. E. Shaw group as "the D. E. Shaw group;" (iii) Madison Dearborn Capital Partners IV, L.P., as "Madison Dearborn;" and (iv) the D. E. Shaw group and Madison Dearborn collectively as "our Sponsors." We use the following electrical power abbreviations throughout this prospectus: "kW" means kilowatt, or 1,000 watts of electrical power; "MW" means megawatt, or 1,000 kW of electrical power; "GW" means

i

gigawatt, or 1,000 MW of electrical power; and "kWh," "MWh" and "GWh" mean an hour during which 1 kW, MW or GW, as applicable, of electrical power has been continuously produced. Capacity refers to rated capacity. References in this prospectus to "RECs" mean renewable energy certificates or other renewable energy attributes, as the context requires. Unless otherwise indicated, the financial information in this prospectus represents the historical financial information of First Wind Holdings, LLC.

ii

This summary highlights selected information from this prospectus but does not contain all information that you should consider before investing in our Class A common stock. You should read this entire prospectus carefully, including the information under "Risk Factors" beginning on page 16, and the consolidated financial statements included elsewhere in this prospectus.

We are an independent wind energy company focused solely on the development, financing, construction, ownership and operation of utility-scale wind energy projects in the United States. Our projects are located in the Northeastern and Western regions of the continental United States and in Hawaii. We have focused on these markets because we believe they provide the potential for future growth and investment returns at the higher end of the range available for wind projects. These markets are characterized by relatively high electricity prices, a shortage of renewable energy and sites with good wind resources that can be built in a cost effective manner. Moreover, we have focused our efforts on projects and regions with significant expansion opportunities, often enabled by transmission solutions that we have developed.

As of November 30, 2009, we operated six projects with combined rated capacity of 477 MW, and we owned two lines that connect projects to the electricity grid (generator leads) with transmission capacity of approximately 1,200 MW. In 2009, we doubled the number of projects in our operating fleet, adding three new projects with an aggregate capacity of 385 MW. Two of these projects, Milford I, which sells power into Southern California, and Stetson I, which sells power in New England, include wholly-owned generator leads we built in anticipation of expanding these projects.

We manage our business with a team of professionals with experience in all aspects of wind energy development, financing, construction and operations. We have a track record of selecting projects from our development pipeline and converting them into operating projects that we believe will meet our financial return requirements. By the end of 2010, we expect to have seven additional projects with 293 MW of capacity operating or under construction, one of which is already under construction. We target having approximately 1,000 MW of projects operating or under construction by the end of 2011. Thereafter, we target adding approximately 300 to 400 MW of operating/under-construction capacity each year to achieve our goal of having an operating/under-construction fleet in excess of 2,000 MW by the end of 2014. Expansions of current operating and under-construction projects make up approximately 51% (measured by capacity) of our targeted 2010-2011 projects. See "Business—Our Development Process" and "Business—Our Portfolio of Wind Energy Projects."

We believe our development pipeline of over 4,000 MW should enable us to meet our 2014 goal of having an operating/under-construction fleet of 2,000 MW. We have land rights for 85% of our development pipeline and meteorological data for nearly 90% of our development pipeline, in most cases covering at least three years. We have also conducted preliminary environmental screening for all of our projects. We are unlikely to complete all of the projects in our current development pipeline, while some of the projects we are likely to develop in the future are not in our current pipeline. Our ability to complete our projects and achieve anticipated generation capacities is subject to numerous risks and uncertainties as described under "Risk Factors."

Wind energy project returns depend mainly on the following factors: energy prices, transmission costs, wind resources, turbine costs, construction costs, financing cost and availability and government incentives. In applying our strategy, we take into account the combination of all of these factors and focus on margins, return on invested capital and value creation as opposed solely to project size. Some of our projects, while having high construction costs, still offer attractive returns because of favorable wind resources or energy prices. Additionally, in many cases, smaller, more profitable projects can create as much absolute value as do larger, lower-returning projects. We assess the profitability of each

1

project by evaluating its net present value. We also evaluate a project on the basis of its Project EBITDA, as described under "Management's Discussion and Analysis of Financial Condition and Results of Operations—How We Measure Our Performance" as compared with the project's development and construction costs.

We closely manage our commodity-price risk and generally construct wind energy projects only if we have put in place some form of a fixed-price, long-term power purchase agreement (PPA) and/or financial hedge. Approximately 85% of the estimated revenues through 2011 from our current operating projects are hedged. We plan to hedge approximately 90% of the estimated revenues for 2011 for the seven projects we plan to have under construction in 2010. See "Business—Revenues; Hedging Activities."

The United States is one of the largest and fastest growing wind energy markets. In 2008, the United States surpassed Germany as the world's largest market for wind energy, as cumulative installed capacity increased approximately 51% and accounted for 42% of all new energy supply in the United States, according to the American Wind Energy Association (AWEA). Moreover, our markets are among the highest growth U.S. markets due to demand driven by state-mandated renewable portfolio standards (RPS), premium electricity pricing, a shortage of renewable energy and strong wind resources. States in our markets in the Northeast, West and Hawaii have RPS legislation that calls for approximately 70 GW of installed renewable energy capacity to be built by 2020.

Achievements

We have achieved a number of milestones, including:

- •

- Northeast. We completed two of the largest utility-scale wind energy projects in New

England (Stetson I and Mars Hill in Maine) and obtained the first permit for a utility-scale wind energy project in Vermont since 1996. We have started construction of our Stetson II project, for

which we entered into a long-term PPA with Harvard University to provide 10% of its local electricity needs. This makes Harvard the largest academic institutional buyer of wind power in

the Northeast. See "Business—Our Regions—Northeast."

- •

- West. We entered into a long-term PPA with the Southern California Public

Power Authority (SCPPA) to supply 20 years of power to the cities of Los Angeles, Burbank and Pasadena from Milford I, our 203 MW wind energy project in Utah. This project includes a 1,000 MW

generator lead providing transmission to the electricity grid. Milford I commenced commercial operations in November 2009. Milford I is the first wind energy project to receive a grant of a right of

way permit under the Bureau of Land Management's new programmatic environmental impact statement for wind energy development. See "Business—Our Regions—West."

- •

- Hawaii. We successfully completed and are operating our Kaheawa Wind Power I

(KWP I) project in Maui, the largest wind energy project in Hawaii. See "Business—Our Regions—Hawaii."

- •

- Financing and U.S. Treasury Grants. Beginning in the fourth quarter of 2008, in the midst of very difficult financial and credit markets, we refinanced or raised approximately $1.9 billion for our company and projects in 16 refinancing and new capital-raising activities. These activities included project debt financings, tax equity financings, intermediate holding company financings, government grants and Sponsor equity contributions. In September 2009, we were among the first recipients of cash grants from the U.S. Treasury under Section 1603 of the American Recovery and Reinvestment Act of 2009 (ARRA), when we received approximately $115 million for our Cohocton and Stetson I projects. See "Industry—Drivers of U.S. Wind Energy Growth—State and Federal Government Incentives—American Recovery and Reinvestment Act of 2009 (ARRA)."

2

Revenues, Financing and Government Programs

We generate revenues from the sale of electricity and the sale of RECs from our operating projects:

- •

- Electricity

sales. We typically sell the power generated by our projects (sometimes bundled with RECs) either pursuant to PPAs with local utilities

or power companies or directly into the local power grid at market prices. Our PPAs have terms ranging from three to 20 years with fixed prices, market prices or a combination of fixed and

market prices. We also seek to hedge a significant portion of the market component of our power sales revenue with financial swaps. See "Management's Discussion and Analysis of Financial Condition and

Results of Operations—Factors Affecting Our Results of Operations, Financial Condition and Cash Flows—Power Purchase Agreements and Financial Hedging."

- •

- REC sales. The RECs associated with renewable electricity generation can be "unbundled" and sold as a separate attribute. In some states, we sell RECs to entities that must either purchase or generate specific quantities of RECs to comply with state or municipal RPS programs. Currently, 25 states and the District of Columbia have adopted RPS programs that operate in tandem with a credit trading system in which generators sell RECs for renewable power they generate in excess of state-mandated requirements.

We have generated substantial net losses and negative operating cash flows since our inception. See "Risk Factors—Risks Related to Our Business and the Wind Industry—We have generated substantial net losses and negative operating cash flows since our inception and expect to continue to do so as we develop and construct new wind energy projects."

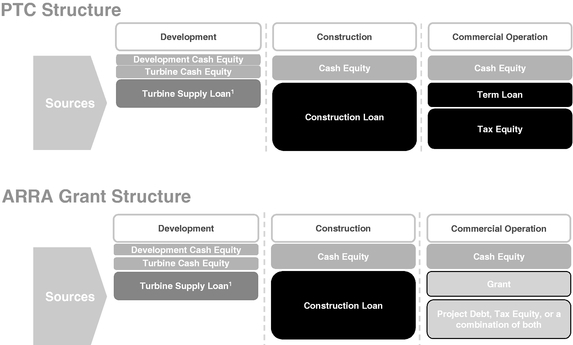

We finance our projects with various sources of funds, depending on a project's stage of development and other factors. We use equity, turbine supply loans, construction loans, non-recourse project financings, tax equity financings, term loans and, recently, grants from the U.S. Treasury under the ARRA.

We benefit from U.S. government programs established to stimulate the economy and increase domestic investment in the wind energy industry. In February 2009, the ARRA went into effect and extended the federal production tax credit (PTC) for renewable energy generators until the end of 2012. In the past, we have monetized PTCs through tax equity financings as part of our project financing strategy. In these transactions, we receive up-front payments, and our tax equity investors receive substantially all of the production tax credits and taxable income or loss generated by the project and a portion of the operating cash flows, until they achieve their targeted investment returns and return of capital, which we typically expect to occur in ten years.

The ARRA also made an investment tax credit (ITC) available to wind energy projects in lieu of PTCs. Project owners can for the first time receive the cash equivalent of the ITC in the form of a grant paid by the U.S. Treasury representing 30% of ITC-eligible costs of building a wind energy project, namely, the costs of constructing energy-producing assets. In September 2009, two of our projects were among the first recipients of such cash grants, receiving approximately $115 million. We intend to apply for, and expect to receive, cash grants for our Milford I project, our Stetson II project and the other projects we begin to construct in 2010. We have also applied for other federal government incentives, including loan guarantees from the Department of Energy. See "Industry—Drivers of U.S. Wind Energy Growth—State and Federal Government Incentives—American Recovery and Reinvestment Act of 2009 (ARRA)."

3

Strategy

Wind energy project returns depend mainly on the following factors:

- •

- Energy price. The realized price of energy, including

power, REC sales and capacity payments and the effect of cash settlements from related hedging activities.

- •

- Wind. The quality of the wind resources and the resulting

energy production, otherwise known as the net capacity factor (NCF). NCF is a measure of a turbine's production compared with the amount of power the turbine could have produced running at full

capacity for a particular period of time.

- •

- Construction costs. The fully loaded installed costs of

the project, including turbines, transmission, balance-of-plant, interest during construction, financing costs and fees and development expenses.

- •

- Financing. The financeability of and cost of capital to

construct the project.

- •

- Government incentives. PTC, ITC, government grants and other incentives.

Our business strategy is to build a diverse portfolio of operating projects and development opportunities. We seek opportunities where, if we are able to execute successfully, we will be able to generate attractive returns for our stockholders.

- •

- Develop our existing pipeline of projects and expand existing operating

projects. We have identified and are developing a broad pipeline of projects in our markets, including expanding our operating projects in existing locations. We believe

expansion projects have lower execution risks than other projects. We target having approximately 1,000 MW of projects operating or under construction by the end of 2011. Thereafter, we target adding

approximately 300 to 400 MW of operating/under-construction capacity each year to achieve our goal of having an operating/under-construction fleet in excess of 2,000 MW by the end of 2014. Expansions

of current operating and under-construction projects make up approximately 51% (measured by capacity) of our targeted 2010-2011 projects.

- •

- Continue to identify and create a new pipeline of diverse development project opportunities in

financially attractive markets. Our markets are undergoing significant growth, which we expect to continue, reaching 70 GW of RPS-driven demand by 2020. Our team of

developers focuses our prospecting and development efforts on identifying new opportunities and acquiring existing wind energy assets that we believe will meet our financial return requirements in

these markets.

- •

- Implement transmission solutions to support development

opportunities. We develop, build, own and operate generator leads connecting our projects to third-party electricity networks. We have

built two generator leads that provide us with significant opportunities for future development: the Stetson generator lead, which has approximately 140 MW of capacity available for our future

expansion projects, and the Milford generator lead, which has approximately 750 MW of capacity available for future expansion projects. In 2010, we plan to build expansion projects using both the

Stetson and Milford leads, leaving 700 MW of additional capacity on these lines. Our generator lead assets and capabilities enable us to develop projects in areas that would otherwise present

significant transmission challenges.

- •

- Focus on construction and operational control. We oversee the construction and operation of our projects. We believe having control of our projects enhances our credibility, allows us to make rapid decisions and strengthens our relationships with landowners, local communities, regulators and other stakeholders. For construction projects, we manage and mitigate budget and schedule risks through arrangements with contractors that have significant experience constructing wind

4

- •

- Obtain stable revenues from our operating

fleet. We manage exposure to market prices for electricity through long-term PPAs and hedging. We also seek to maximize the

value of the RECs we generate by selling our electricity into markets that have higher RPS requirements and strong markets for RECs. We believe that stabilizing our revenue stream benefits us, our

lenders and tax equity investors, and enhances our ability to obtain long-term, non-recourse financing for our projects on attractive terms.

- •

- Develop substantial local presence and community stakeholder involvement in our

markets. We establish a local presence from a project's early stage through the operating stage to work cooperatively with the communities where our projects are located to

more fully understand each community's unique issues and concerns. We believe this helps us to better assess the feasibility of projects and enhances our ability to complete and operate them

successfully.

- •

- Access financing to grow our portfolio. Our business is capital intensive and requires ongoing access to debt and equity capital markets to build our projects. We believe we demonstrated our capacity to do this during the difficult financial market conditions in 2008 and 2009.

energy projects. We also work closely with the manufacturers of our turbines with the goal of enhancing the operating performance of our fleet.

Competitive Strengths

We intend to use the following strengths to capitalize on what we believe to be significant opportunities for growth in the U.S. wind energy industry in general and in our markets in particular:

- •

- Track record in developing complex wind energy

projects. Our experienced management team has a track record of developing complex projects in each of our three markets. Our project

development strategy sometimes includes the construction of generator leads as in the case of Stetson I and Milford I, or the structuring and negotiation of creative financing and risk

management solutions as in our PPA with SCPPA for Milford I. In certain cases, as in KWP I, we took over projects from other developers who were unable to complete them.

- •

- Ability to finance multiple projects across our

portfolio. Wind energy project development and construction are capital intensive and require access to a relatively constant stream of

financing. As a result, our ability to access capital markets efficiently and effectively is crucial to our growth. The recent worldwide financial and credit crisis has reduced the availability of

liquidity and credit. However, during the difficult market conditions that began in the fall of 2008 and have persisted through 2009, we refinanced or raised approximately $1.9 billion for our

company and projects in 16 refinancing and new capital-raising activities. These activities included project debt financings, tax equity financings, intermediate holding company financings,

government grants and Sponsor equity contributions. We expect to fund the development of our projects with a combination of cash flows from operations, debt financings, tax equity financings,

government grants and capital markets transactions such as this offering. See "Business—Project Financing."

- •

- Established platform in attractive markets with significant growth

opportunities. We have a portfolio of projects in the Northeast, West and Hawaii where we believe we can generate attractive investment

returns. These markets are characterized by high electricity prices, a shortage of renewable energy and sites with good wind resources that can be built on cost-effectively. Many of our

projects have significant expansion opportunities, which in some cases will enable us to use our existing generator leads. Expansions of our current operating and under-construction projects make up

approximately 51% (measured by capacity) of our targeted 2010-2011 projects.

- •

- Well positioned for future turbine orders with few turbine commitments. We have secured sufficient turbines to execute our 2010 project plan. Because we believe the turbine market is currently

5

- •

- Experienced management team that owns significant equity in the company. Our management team is experienced in all aspects of the wind energy business. Over the past two years, we have added several key personnel to our team, primarily in the areas of construction, operations and finance. We believe we can achieve our operating/under-construction fleet goal of over 2,000 MW by the end of 2014 without significant additions to headcount and overhead costs related to non-operating activities. In addition, members of our senior management team have a meaningful equity stake in our company.

over-supplied, we have not entered into firm commitments to purchase turbines for projects in our development pipeline after 2010. Instead, we have agreements in place that give us the right, but not the obligation, to purchase additional turbines after 2010, allowing us to cancel our turbine orders with the forfeiture of deposits. We believe this gives us flexibility to acquire turbines at attractive prices and on favorable terms.

Market Opportunity

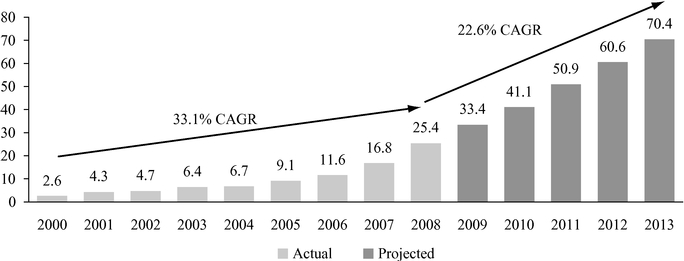

According to AWEA, wind energy capacity in the United States grew at a CAGR of 33% from 2000 through 2008. The Energy Information Administration (EIA) also indicates that wind energy was the fastest growing source of new electricity supply in the U.S. electrical generation market from 2000 through 2008. This growth reached a record high during 2008, when the cumulative installed wind capacity in the United States increased 51% from 16.8 GW to 25.4 GW and new wind energy capacity made up approximately 42% of total new electricity supply in the United States, according to AWEA.

Despite its significant growth in the United States, wind energy accounted for only 1.3% of total U.S. electricity production in 2008 according to the EIA. The EIA predicts that wind energy will account for only 2.5% of total U.S. electricity production in 2030. This represents a small portion compared with the percentage of electricity produced in 2008 by wind energy in Denmark, Spain and Germany—approximately 18%, 11% and 8%, respectively. EER forecasts that installed wind energy capacity in the United States will grow at a CAGR of 22.6% from 2008 through 2013. In certain U.S. markets, state-mandated RPS and similar voluntary programs, among other factors, have strengthened the demand for renewable energy.

We believe wind energy growth in the United States is being driven primarily by:

- •

- decreasing costs in the U.S. wind industry supply chain and continued improvements in wind technologies;

- •

- public concern about environmental issues, including climate change;

- •

- favorable federal and state policies regarding climate change and renewable energy, exemplified by state RPS programs and

the ARRA, that support the development of renewable energy;

- •

- increasing obstacles for the construction of conventional power plants; and

- •

- public concern over continued U.S. dependence on foreign energy imports.

Risk Factors

Our business is subject to numerous risks and uncertainties, including those relating to our ability to build our projects and convert our development pipeline into operating projects; our substantial net losses and negative operating cash flows; government policies supporting renewable energy development; our dependence on suitable wind conditions; the need for ongoing access to capital to support our growth; and the potential for mechanical breakdowns. You should carefully consider all of the information in this prospectus and, in particular, the information under "Risk Factors," prior to making an investment in our Class A common stock.

6

Class A Common Stock and Class B Common Stock

After completion of this offering, our outstanding capital stock will consist of Class A common stock and Class B common stock. Investors in this offering will hold shares of Class A common stock. See "Description of Capital Stock."

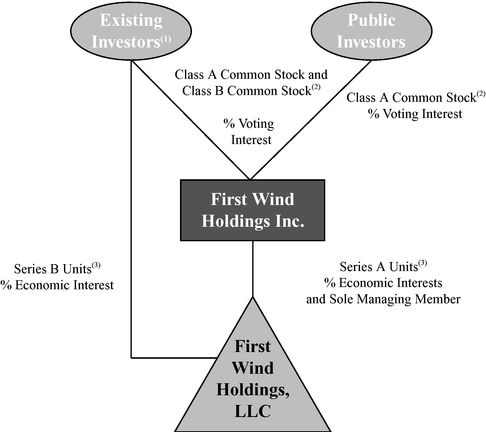

The Reorganization and Our Holding Company Structure

First Wind Holdings Inc. was formed in contemplation of this offering and, upon its completion, all of our business and operations will continue to be conducted through First Wind Holdings, LLC, which owns all of our interests in our operating subsidiaries. Prior to this offering, First Wind Holdings Inc. did not engage in any activities, except in preparation for this offering. After the completion of this offering and the reorganization described under "The Reorganization and Our Holding Company Structure," we will be a holding company and the sole managing member of First Wind Holdings, LLC. Our only business and material asset will be our managing member interest in First Wind Holdings, LLC. We will own approximately % of the economic interest in First Wind Holdings, LLC (assuming no exercise of the underwriters' over-allotment option) and entities in the D. E. Shaw group and Madison Dearborn Capital Partners IV, L.P., our Sponsors, will collectively own the balance. Our only source of cash flow from operations will be distributions from First Wind Holdings, LLC. See "The Reorganization and Our Holding Company Structure."

The diagram below illustrates our holding company structure and anticipated ownership immediately after completion of the reorganization and this offering (assuming no exercise of the underwriters' over-allotment option).

- (1)

- The members of First Wind Holdings, LLC, other than us, will consist of our Sponsors and certain of our employees and current investors in First Wind Holdings, LLC.

7

- (2)

- Each

share of Class A common stock and Class B common stock is entitled to one vote per share. The Class A common stockholders will

have the right to receive all distributions made on account of our capital stock, except for the right of the Class B common stockholders to receive their $0.0001 per share par value pari passu

upon liquidation, dissolution or winding up. Certain entities in the D. E. Shaw group have elected to receive Class A common stock in lieu of receiving Series B Units (and

the corresponding shares of Class B common stock). As a result, the D. E. Shaw group will hold Series B Units, Class A common stock and Class B common stock.

- (3)

- Series A Units and Series B Units will have the same economic rights.

Corporate Information

We began developing wind energy projects in North America in 2002. First Wind Holdings Inc. was incorporated in Delaware in May 2008. Our principal executive offices are located at 179 Lincoln Street, Suite 500, Boston, Massachusetts 02111, and our telephone number is (617) 960-2888. Our website is www.firstwind.com. The information contained on or accessible through our website is not part of this prospectus and you should not consider it in making an investment decision.

8

Class A common stock offered by us |

shares. | |

Class A common stock to be outstanding after this offering |

shares (assuming no exercise of the underwriters' over-allotment option). |

|

Class B common stock to be outstanding after this offering |

shares. Shares of our Class B common stock will be issued in connection with, and in equal proportion to, issuances of Series B Units of First Wind Holdings, LLC. When a Series B Unit is exchanged for a share of our Class A common stock or forfeited, the corresponding share of our Class B common stock will automatically be redeemed by us. See "The Reorganization and Our Holding Company Structure." |

|

Underwriters' over-allotment option |

shares. |

|

Use of proceeds |

We expect to receive net proceeds from the sale of Class A common stock offered hereby, after deducting estimated underwriting discounts and commissions and estimated offering expenses, of approximately $ million, based on an assumed offering price of $ per share (the midpoint of the range set forth on the cover of this prospectus). We intend to use such net proceeds to fund a portion of our capital expenditures for 2010–2013 and for general corporate purposes. |

|

Voting rights |

Each share of our Class A common stock and Class B common stock will entitle its holder to one vote on all matters to be voted on by stockholders. Holders of Class A common stock and Class B common stock will vote together as a single class on all matters presented to stockholders for their vote or approval, except as otherwise required by law. After completion of this offering, our Sponsors will own % of our outstanding Class A common stock and Class B common stock on a combined basis ( % if the underwriters exercise their over-allotment option in full) and will have effective control over the outcome of votes on all matters requiring approval by our stockholders. |

|

Exchange of Series B Units |

Each fully-vested Series B Unit of First Wind Holdings, LLC, together with a corresponding share of our Class B common stock, will be exchangeable for one share of Class A common stock as described under "The Reorganization and Our Holding Company Structure—Amended and Restated Limited Liability Company Agreement of First Wind Holdings, LLC." |

|

Dividend policy |

We do not anticipate paying dividends. See "Dividend Policy." |

|

Risk factors |

For a discussion of factors you should consider before making an investment, see "Risk Factors." |

|

Proposed Nasdaq Global Market symbol |

"WIND" |

9

The number of shares to be outstanding after completion of this offering is based on shares of Class A common stock outstanding as of after giving effect to the reorganization described under "The Reorganization and Our Holding Company Structure." The number of shares to be outstanding after this offering excludes additional shares of Class A common stock reserved for issuance under our long-term incentive plan.

Unless we specifically state otherwise, the information in this prospectus assumes:

- •

- the implementation of the reorganization described in "The Reorganization and Our Holding Company Structure;" and

- •

- no exercise of the underwriters' over-allotment option.

10

Summary Financial and Operating Data

The following tables present summary consolidated financial data as of and for the dates and periods indicated below. The summary consolidated statement of operations data for the years ended December 31, 2006, 2007 and 2008 and the summary consolidated balance sheet data as of December 31, 2007 and 2008 are derived from our audited consolidated financial statements included elsewhere in this prospectus. The summary consolidated statement of operations data for the nine months ended September 30, 2008 and 2009 and the summary consolidated balance sheet data as of September 30, 2009 are derived from our unaudited interim consolidated financial statements included elsewhere in this prospectus. The unaudited interim period financial information, in the opinion of management, includes all adjustments, which are normal and recurring in nature, necessary for the fair presentation of the periods shown.

The summary unaudited pro forma consolidated financial data for the year ended December 31, 2008 and for the nine months ended September 30, 2009 have been prepared to give pro forma effect to all of the reorganization transactions described in "The Reorganization and Our Holding Company Structure" and this offering as if they had been completed as of January 1, 2008 with respect to the unaudited consolidated pro forma statement of operations and as of September 30, 2009 with respect to the unaudited pro forma consolidated balance sheet data. These data are subject and give effect to the assumptions and adjustments described in the notes accompanying the unaudited pro forma financial statements included elsewhere in this prospectus. The summary unaudited pro forma financial data are presented for informational purposes only and should not be considered indicative of actual results of operations that would have been achieved had the reorganization transactions and this offering been consummated on the dates indicated, and do not purport to be indicative of statements of financial condition data or results of operations as of any future date or for any future period. Pro forma net loss per share is based on the weighted average common shares outstanding.

The summary consolidated financial data set forth below should be read in conjunction with the "Unaudited Pro Forma Financial Information," "Selected Historical Financial and Operating Data," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the

11

consolidated financial statements and related notes included elsewhere in this prospectus. Our historical results may not be indicative of the operating results to be expected in any future period.

| |

First Wind Holdings, LLC |

First Wind Holdings Inc. |

First Wind Holdings, LLC |

First Wind Holdings Inc. |

|||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2006 | 2007 | 2008 | Pro Forma | 2008 | 2009 | Pro Forma | ||||||||||||||||

| |

|

|

|

(unaudited) |

(unaudited) |

(unaudited) |

(unaudited) |

||||||||||||||||

| |

(in thousands, except unit/share data and other operating data) |

||||||||||||||||||||||

Statement of Operations Data: |

|||||||||||||||||||||||

Revenues: |

|||||||||||||||||||||||

Revenues |

$ | 7,063 | $ | 23,817 | $ | 28,790 | $ | $ | 21,712 | $ | 30,468 | $ | |||||||||||

Risk management activities related to operating projects |

8,848 | (11,471 | ) | 10,688 | (6,180 | ) | 27,580 | ||||||||||||||||

Total revenues |

15,911 | 12,346 | 39,478 | 15,532 | 58,048 | ||||||||||||||||||

Cost of revenues: |

|||||||||||||||||||||||

Wind energy project operating expenses |

1,339 | 9,175 | 10,613 | 6,592 | 13,269 | ||||||||||||||||||

Depreciation and amortization of operating assets |

1,945 | 8,800 | 10,611 | 6,978 | 23,445 | ||||||||||||||||||

Total cost of revenues |

3,284 | 17,975 | 21,224 | 13,570 | 36,714 | ||||||||||||||||||

Gross income (loss) |

12,627 | (5,629 | ) | 18,254 | 1,962 | 21,334 | |||||||||||||||||

Other operating expenses: |

|||||||||||||||||||||||

Project development |

16,028 | 25,861 | 35,855 | 19,348 | 32,694 | ||||||||||||||||||

General and administrative |

6,598 | 13,308 | 44,358 | 28,856 | 28,599 | ||||||||||||||||||

Depreciation and amortization |

294 | 1,215 | 2,325 | 1,712 | 2,443 | ||||||||||||||||||

Total other operating expenses |

22,920 | 40,384 | 82,538 | 49,916 | 63,736 | ||||||||||||||||||

Loss from operations |

(10,293 | ) | (46,013 | ) | (64,284 | ) | (47,954 | ) | (42,402 | ) | |||||||||||||

Risk management activities related to non-operating projects |

$ | (13,131 | ) | $ | (21,141 | ) | $ | 42,138 | $ | $ | 12,369 | $ | — | $ | |||||||||

Net loss attributable per common unit (basic and diluted) |

$ | (0.24 | ) | $ | (0.36 | ) | $ | (0.05 | ) | $ | $ | (0.15 | ) | $ | (0.06 | ) | $ | ||||||

Weighted average number of common units (basic and diluted) |

107,712,405 | 189,161,855 | 278,266,400 | 226,161,565 | 649,648,023 | ||||||||||||||||||

Pro forma net loss per share—basic and diluted(1) |

|||||||||||||||||||||||

Shares used in computing pro forma net loss per share—basic and diluted |

|||||||||||||||||||||||

Other Financial Data: |

|||||||||||||||||||||||

Net cash provided by (used in): |

|||||||||||||||||||||||

Operating activities |

$ | (31,799 | ) | $ | (26,370 | ) | $ | (41,589 | ) | $ | (15,894 | ) | $ | (39,742 | ) | ||||||||

Investing activities |

(311,281 | ) | (334,007 | ) | (477,268 | ) | (351,067 | ) | (326,440 | ) | |||||||||||||

Financing activities |

346,500 | 358,107 | 556,059 | 367,500 | 374,012 | ||||||||||||||||||

Selected Operating Data |

|||||||||||||||||||||||

Nameplate capacity (end of period) |

30 MW | 92 MW | 92 MW | 92 MW | 274 MW | ||||||||||||||||||

Megawatt hours generated |

56,629 | 239,940 | 275,024 | 194,718 | 437,143 | ||||||||||||||||||

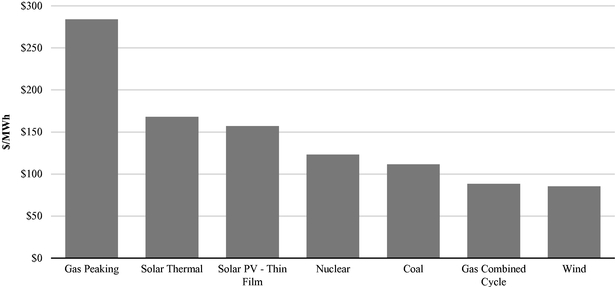

Average realized energy price ($/MWh)(2) |

$ | 108 | $ | 93 | $ | 85 | $ | 84 | $ | 77 | |||||||||||||

Project EBITDA(3) |

$ | 4,802 | $ | 15,433 | $ | 16,052 | $ | 11,392 | $ | 26,826 | |||||||||||||

- (1)

- The basic net loss attributable per common unit for each of the annual periods ended December 31, 2006, 2007 and 2008 and the nine-month periods ended September 30, 2008 and 2009 has been presented for informational and historical purposes only. After completion of this offering, as a result of the reorganization events that have taken place or that will take place immediately prior to completion of the offering as described in "The Reorganization and Our Holding Company Structure," the shares used in computing net earnings or loss per share will bear no relationship to these historical common units.

12

- (2)

- Average

realized energy price per MWh of energy generated is a metric that allows us to compare revenues from period to period, or on a project by project

basis, regardless of whether the revenues are generated under a fixed-price PPA, from sales at market prices with a financial swap, or a combination of the two. Although average realized energy price

is based, in part, on revenues recognized under accounting principles generally accepted in the United States (GAAP), this metric does not represent revenue per unit of production on a GAAP basis. We

adjust GAAP revenues used to compute this metric in two respects:

- •

- Under GAAP, recognition of revenues from the sale of New England RECs is delayed due

to regulations that limit their transfer to the buyer to quarterly trading windows that open two quarters subsequent to generation. To match New England REC revenue to the period in which the related

power was generated, in calculating this metric, we add New England REC revenues attributable to generation during a period but not yet recognized under GAAP, and subtract New England REC revenue

recognized under GAAP in the period but generated in a prior period.

- •

- In addition, in order to focus this metric on realized energy prices, we exclude the effects of mark-to-market adjustments on financial swaps and certain transmission costs incurred to secure RECs.

Average realized energy price changes over time due to several factors. Historically, the most significant factor has been the growth of our business and the corresponding change in pricing mix. Each project has a different pricing profile, including varying levels of hedging in relation to electricity generation, and in certain cases, short periods of unhedged exposure to market price fluctuations as hedging agreements are put in place.

The table below shows the calculation of our average realized energy price for the periods presented:

| |

Year Ended December 31, | Nine Months Ended September 30, |

||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2006 | 2007 | 2008 | 2008 | 2009 | |||||||||||||

Numerator (in thousands) |

||||||||||||||||||

Total revenue |

$ | 15,911 | $ | 12,346 | $ | 39,478 | $ | 15,532 | $ | 58,048 | ||||||||

Add (subtract): |

||||||||||||||||||

New England REC timing(a) |

— | 2,461 | 1,947 | 248 | 1,239 | |||||||||||||

Transmission costs |

— | (2,268 | ) | (3,316 | ) | (1,555 | ) | (2,387 | ) | |||||||||

Mark-to-market adjustment(b) |

(9,770 | ) | 9,801 | (14,760 | ) | 2,204 | (23,339 | ) | ||||||||||

|

$ | 6,141 | $ | 22,340 | $ | 23,349 | $ | 16,424 | $ | 33,561 | ||||||||

Denominator (MWh) |

||||||||||||||||||

Total energy production |

56,629 | 239,940 | 275,024 | 194,718 | 437,143 | |||||||||||||

Average realized energy price ($/MWh) |

||||||||||||||||||

(numerator/denominator) |

$108 | $93 | $85 | $84 | $77 | |||||||||||||

- (a)

- New England REC timing represents the difference between: (i) New England RECs generated in earlier periods that qualified for GAAP revenue recognition in the applicable period and (ii) New England RECs generated in the applicable period and sold to a creditworthy counterparty under a firm sales contract where revenue is deferred under GAAP until the applicable quarterly trading window occurs. The gross amounts of such New England RECs are as follows:

| |

Year Ended December 31, | Nine Months Ended September 30, |

||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2006 | 2007 | 2008 | 2008 | 2009 | |||||||||||||

| |

(in thousands) |

|||||||||||||||||

New England REC |

||||||||||||||||||

Included in revenues |

$ |

(17 |

) |

$ |

(2,364 |

) |

$ |

(5,274 |

) |

$ |

(3,936 |

) |

$ |

(7,937 |

) |

|||

Generated during the period |

17 | 4,825 | 7,221 | 4,184 | 9,176 | |||||||||||||

|

$ | — | $ | 2,461 | $ | 1,947 | $ | 248 | $ | 1,239 | ||||||||

- (b)

- The

mark-to-market adjustment for September 30, 2009, includes the effect of a cash settlement of a financial hedge for $4,147 in addition to market

adjustments of $19,192.

- (3)

- We evaluate the performance of our operating projects on the basis of their Project EBITDA, which is a non-GAAP financial measure. We use Project EBITDA to assess the performance of our operating projects because we believe it is a measure that allows us to: (i) more accurately evaluate the operating performance of our projects based on the energy generated during each period (through the treatment of mark-to-market adjustments and New England REC timing, for which the GAAP accounting treatment does not correspond to the energy generated during the period) and (ii) assess the

13

ability of our projects to support debt and/or tax equity financing (through the exclusion of depreciation and amortization that is not indicative of capital costs that would be expected over the term of the financing). Our ability to raise debt and/or tax equity financing for our projects is a key requirement of our development plan as described in "—Factors Affecting Our Results of Operations, Financial Condition and Cash Flows—Financing Requirements." We believe it is important for investors to understand the factors that we focus on in managing the business, and therefore we believe Project EBITDA is useful for investors to understand. In addition, as long as investors consider Project EBITDA in combination with the most directly comparable GAAP measure, gross income (loss), we believe it is useful for investors to have information about our operating performance on a period-by-period basis, without giving effect to GAAP requirements that require the recognition of income or expense that does not correspond to actual energy production in a given period, and we believe it is useful for investors to consider a measure that does not include project-related depreciation and amortization. Because lenders and providers of tax equity financing frequently disregard the non-cash charges and GAAP timing differences noted above when determining the financeability of a project, we believe that presenting information in this manner can help give investors an understanding of our ability to secure financing for our projects. Project EBITDA can be reconciled to gross income (loss), which we believe to be the most directly comparable financial measure calculated and presented in accordance with GAAP, as follows (in thousands):

| |

Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2006 | 2007 | 2008 | 2008 | 2009 | ||||||||||||||

Gross income (loss) |

$ | 12,627 | $ | (5,629 | ) | $ | 18,254 | $ | 1,962 | $ | 21,334 | ||||||||

Add (subtract): |

|||||||||||||||||||

Depreciation and amortization of operating assets |

1,945 | 8,800 | 10,611 | 6,978 | 23,445 | ||||||||||||||

New England REC timing |

— | 2,461 | 1,947 | 248 | 1,239 | ||||||||||||||

Mark-to-market adjustments |

(9,770 | ) | 9,801 | (14,760 | ) | 2,204 | (19,192 | ) | |||||||||||

Project EBITDA |

$ | 4,802 | $ | 15,433 | $ | 16,052 | $ | 11,392 | $ | 26,826 | |||||||||

Project EBITDA does not represent funds available for our discretionary use and is not intended to represent or to be used as a substitute for gross income (loss), net income or cash flow from operations data as measured under GAAP. The items excluded from Project EBITDA are significant components of our statement of income and must be considered in performing a comprehensive assessment of our overall financial performance. Project EBITDA and the associated period-to-period trends should not be considered in isolation.

14

The following table presents summary consolidated balance sheet data as of the dates indicated:

- •

- on an actual basis;

- •

- on a pro forma basis as of September 30, 2009 to give effect to all of the reorganization transactions described in

"The Reorganization and Our Holding Company Structure"; and

- •

- on a pro forma as adjusted basis as of September 30, 2009 to give further effect to our sale of shares of common stock in this offering at an assumed initial public offering price of $ per share, the midpoint of the range set forth on the cover of this prospectus, after deducting estimated underwriting discounts and commissions and estimated offering expenses.

| |

First Wind Holdings, LLC | |

|

|||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

As of December 31, | First Wind Holdings Inc. | ||||||||||||||||||

| |

2006 | 2007 | 2008 | As of September 30, 2009 |

Pro Forma As of September 30, 2009 |

Pro Forma As Adjusted September 30, 2009 |

||||||||||||||

| |

|

|

|

(unaudited) |

(unaudited) |

|

||||||||||||||

| |

(in thousands) |

|||||||||||||||||||

Balance Sheet Data: |

||||||||||||||||||||

Property, plant and equipment, net |

$ | 81,452 | $ | 192,076 | $ | 187,316 | $ | 478,166 | $ | $ | ||||||||||

Construction in progress |

85,153 | 346,320 | 571,586 | 910,563 | ||||||||||||||||

Total assets |

372,500 | 770,666 | 1,311,591 | 1,736,390 | ||||||||||||||||

Long-term debt, including debt with maturities less than one year |

257,884 | 465,449 | 532,441 | 854,378 | ||||||||||||||||

Members' capital/ stockholders' equity |

88,519 | 147,876 | 653,092 | 769,661 | ||||||||||||||||

- Note:

- Pro forma basic and diluted net loss per share was computed by dividing the pro forma net loss attributable to our Class A common stockholders by the shares of Class A common stock that we will issue and sell in this offering, plus shares issued in connection with our initial capitalization, assuming that these shares of Class A common stock were outstanding for the entirety of each of the historical periods presented on a pro forma basis. No pro forma effect was given to the future potential exchanges of the Series B Units (and the equal number of shares of our Class B common stock) of our subsidiary, First Wind Holdings, LLC, that will be outstanding immediately after the completion of this offering and the reorganization transactions for an equal number of shares of our Class A common stock because the issuance of shares of Class A common stock upon these exchanges would not be dilutive.

15

You should consider carefully each of the risks described below, together with all of the other information contained in this prospectus, before deciding to invest in our Class A common stock. If any of the following risks materializes, our business, financial condition and results of operations may be materially adversely affected. In that event, the trading price of our Class A common stock could decline, and you could lose some or all of your investment.

The risks described in this prospectus are those that we believe are material, but they are not the only risks and uncertainties that we face. Additional risk factors not currently known or which are currently believed to be immaterial may also have a material adverse effect on our business, financial condition and results of operations, or result in other events that could lead to a decline in the value of our Class A common stock. This prospectus also contains forward-looking statements that involve risks and uncertainties. Actual results could differ materially from those anticipated in these forward-looking statements as a result of various factors, including the risks described below and elsewhere in this prospectus. See "Cautionary Statement Regarding Forward-Looking Statements."

Risks Related to Our Business and the Wind Energy Industry

If we cannot continue to build our pipeline of projects under development and turn them into operating projects, our business will not grow and we may have significant write-offs.

We may be unable to meet our target of having in excess of 2,000 MW of operating/under-construction capacity by 2014, because we will need to add new projects to our pipeline on an ongoing basis. In addition, we may have difficulty in converting our development pipeline into operating projects or may be unable to find suitable projects to add to our pipeline. These circumstances could prevent those projects from commencing operations or from meeting our original expectations about how much energy they will generate or the returns they will achieve. Since completing the projects in our development pipeline as anticipated or at all involves numerous risks and uncertainties, some projects in our portfolio will not progress to construction or may be substantially delayed. From time to time we have abandoned projects on which we had started development work, or re-categorized projects to a less advanced stage than we had previously assigned them, representing in the aggregate approximately 103 MW of potential capacity. This resulted in $3.5 million and $3.1 million of write-offs in 2008 and 2009, respectively. Abandonment or re-categorization of our projects may make it difficult for us to achieve our operating capacity goals by our target dates. As we increase our development activities and the number of projects in our pipeline, such discontinuations and re-categorizations and the corresponding write-offs may increase. In addition, those projects that are constructed and begin operations may not meet our return expectations due to schedule delays, cost overruns or revenue shortfalls or they may not generate the capacity that we anticipate or result in receipt of revenue in the originally anticipated time period or at all. An inability to maintain our development pipeline or to convert those projects into financially successful operating projects would have a material adverse effect on our business, financial condition and results of operations.

We have generated substantial net losses and negative operating cash flows since our inception and expect to continue to do so as we develop and construct new wind energy projects.

We have generated substantial net losses and negative operating cash flows from operating activities since our operations commenced. We had accumulated losses of approximately $171.9 million from our inception through September 30, 2009. For the year ended December 31, 2008 and the nine months ended September 30, 2009, we generated net losses of $26.2 million and $47.3 million, respectively. In addition, our operating activities used cash of $41.6 million and $39.7 million for the year ended December 31, 2008 and the nine months ended September 30, 2009, respectively.

We expect that our net losses will continue and our cash used in operating activities will grow during the next several years, as compared with prior periods, as we increase our development activities

16

and construct additional wind energy projects. Wind energy projects in development typically incur operating losses prior to commercial operation at which point the projects begin to generate positive operating cash flow. We also expect to incur additional costs, contributing to our losses and operating uses of cash, as we incur the incremental costs of operating as a public company. Our costs may also increase due to such factors as higher than anticipated financing and other costs; non-performance by third-party suppliers or subcontractors; increases in the costs of labor or materials; and major incidents or catastrophic events. If any of those factors occurs, our losses could increase significantly and the value of our common stock could decline. As a result, our net losses and accumulated deficit could increase significantly.

We depend on federal, state and local government support for renewable energy, especially wind projects.

We depend on government policies that support renewable energy and enhance the economic feasibility of developing wind energy projects. The federal government and several of the states in which we operate or into which we sell power provide incentives that support the sale of energy from renewable sources, such as wind.

The Internal Revenue Code provides a production tax credit (PTC) for each kWh of energy generated by an eligible resource. Under current law, an eligible wind facility placed in service prior to the end of 2012 may claim the PTC. The PTC is a credit claimed against the income of the owner of the eligible project.

PTC eligible projects are also eligible for an investment tax credit (ITC) of 30% of the eligible cost-basis, which is in lieu of the PTC. The same placed-in-service deadline of December 31, 2012 applies for purposes of the ITC. The ITC is a credit claimed against the income of the owner of the eligible project.

The American Recovery and Reinvestment Act of 2009 (ARRA) created a grant administered by the U.S. Treasury that provides for a cash payment of the amount an eligible project otherwise would be able to claim under the ITC. In addition, there are various programs for loan guarantees. See "Industry—Drivers of U.S. Wind Energy Growth—State and Federal Government Incentives."

In addition to federal incentives, we rely on state incentives that support the sale of energy generated from renewable sources, including state adopted renewable portfolio standards (RPS) programs. Such programs generally require that electricity supply companies include a specified percentage of renewable energy in the electricity resources serving a state or purchase credits demonstrating the generation of such electricity by another source. However, the legislation creating such RPS requirements usually grants the relevant state public utility commission the ability to reduce electric supply companies' obligations to meet the RPS requirements in certain circumstances. If the RPS requirements are reduced or eliminated, this could result in our receiving lower prices for our power and in a reduction in the value of our RECs, which could have a material adverse effect on us. See "Industry—Drivers of U.S. Wind Energy Growth—State and Federal Government Incentives."

We depend on these programs to finance the projects in our development pipeline. If any of these incentives are adversely amended, eliminated, not extended beyond their current expiration dates, or if funding for these incentives is reduced, it would have a material adverse effect on our financing. The delay or failure by federal departments to administer these programs in a timely and efficient manner could have a material adverse effect on our financing.

While certain federal, state and local programs and policies promote renewable energy and additional legislation is regularly being considered that would enhance the demand for renewable energy, policies may be adversely modified, legislation may not pass or may be amended and governmental support of renewable energy development, particularly wind energy, may not continue or may be reduced. If governmental authorities do not continue supporting, or reduce their support for, the development of wind energy projects, our revenues may be adversely affected, our economic return

17

on certain projects may be reduced, our financing costs may increase, it may become more difficult to obtain financing, and our business and prospects may otherwise be adversely affected.

Most of our revenue comes from sales of electricity and RECs, which are subject to market price fluctuations, and there is a risk of a significant, sustained decline in their market prices. Such a decline may make it more difficult to develop our projects.

We may not be able to develop our projects economically if there is a significant, sustained decline in market prices for electricity or RECs without a commensurate decline in the cost of turbines and the other capital costs of constructing wind energy projects. Electricity prices are affected by various factors and may decline for many reasons that are not within our control. Those factors include changes in the cost or availability of fuel, regulatory and governmental actions, changes in the amount of available generating capacity from both traditional and renewable sources, changes in power transmission or fuel transportation capacity, seasonality, weather conditions and changes in demand for electricity. In addition, other power generators may develop new technologies or improvements to traditional technologies to produce power that could increase the supply of electricity and cause a sustained reduction in market prices for electricity and RECs. If governmental action or conditions in the markets for electricity or RECs cause a significant, sustained decline in the market prices of electricity or those attributes, without an offsetting decline in the cost of turbines or other capital costs of wind energy projects, we may not be able to develop and construct our pipeline of development projects or achieve expected revenues, which could have a material adverse effect on our business, financial condition and results of operations.

The production of wind energy depends heavily on suitable wind conditions. If wind conditions are unfavorable, our electricity production, and therefore our revenue, may be substantially below our expectations.

The electricity produced and revenues generated by a wind energy project depends heavily on wind conditions, which are variable and difficult to predict. We base our decisions about which sites to develop in part on the findings of long-term wind and other meteorological studies conducted in the proposed area, which measure the wind's speed, prevailing direction and seasonal variations. Actual wind conditions, however, may not conform to the measured data in these studies and may be affected by variations in weather patterns, including any potential impact of climate change. Therefore, the electricity generated by our projects may not meet our anticipated production levels or the rated or nameplate capacity of the turbines located there, which could adversely affect our business, financial condition and results of operations. Projections of wind resources also rely upon assumptions about turbine placement, interference between turbines and the effects of vegetation, land use and terrain, which involve uncertainty and require us to exercise considerable judgment. We or our consultants may make mistakes in conducting these wind and other meteorological studies. Any of these factors could cause us to develop sites that have less wind potential than we expected, or to develop sites in ways that do not optimize their potential, which could cause the return on our investment in these projects to be lower than expected.

If our wind energy assessments turn out to be wrong, our business could suffer a number of material adverse consequences, including:

- •

- our energy production and sales may be significantly lower than we predict;

- •

- our hedging arrangements may be ineffective or more costly;

- •

- we may not produce sufficient energy to meet our commitments to sell RECs and, as a result, we may have to buy RECs on the

open market to cover our obligations or pay damages; and

- •

- our projects may not generate sufficient cash flow to make payments of principal and interest as they become due on our project-related debt, and we may have difficulty obtaining financing for future projects.

18

Natural events may reduce energy production below our expectations.

A natural disaster, severe weather or an accident that damages or otherwise adversely affects any of our operations could have a material adverse effect on our business, financial condition and results of operations. Lightning strikes, blade icing, earthquakes, tornados, extreme wind, severe storms, wildfires and other unfavorable weather conditions or natural disasters could damage or require us to shut down our turbines or related equipment and facilities, impeding our ability to maintain and operate our facilities and decreasing electricity production levels and our revenues. Operational problems, such as degradation of turbine components due to wear or weather or capacity limitations on the electrical transmission network, can also affect the amount of energy we are able to deliver. Any of these events, to the extent not fully covered by insurance, could have a material adverse effect on our business, financial condition and results of operations.

Operational problems may reduce energy production below our expectations.

Spare parts for wind turbines and key pieces of electrical equipment may be hard to acquire or unavailable to us. Sources for some significant spare parts and other equipment are located outside of North America. If we were to experience a shortage of or inability to acquire critical spare parts, we could incur significant delays in returning facilities to full operation. In addition, we generally do not hold spare substation main transformers. These transformers are designed specifically for each wind energy project, and the current lead time to receive an order for this type of equipment is over eight months. If we have to replace any of our substation main transformers, we could be unable to sell electricity from the affected wind energy project until a replacement is installed. That interruption to our business might not be fully covered by insurance.

One of our key turbine suppliers, Clipper Windpower Plc, has experienced certain technical issues with its wind turbine technology and may continue to experience similar issues.

Clipper, one of our two turbine suppliers in our existing operating fleet, is a new entrant into the wind turbine market. Clipper's first prototype wind turbine, the 2.5 MW Liberty, was placed in service in April 2005. We now operate 116 Liberty turbines (290 MW) and plan to install 34 Liberty turbines in 2010 (85 MW). We have entered into agreements which provide us the right but not the obligation to acquire up to 253 Liberty turbines (632 MW) for installation during 2011-2015. We deployed the first eight commercially produced Liberty turbines at our Steel Winds I project, which commenced commercial operations on June 1, 2007. Since our initial deployment, Clipper has announced and remediated three defects affecting the Liberty turbines deployed by us and other customers that resulted in prolonged downtime for turbines at various projects, including our Steel Winds I and Cohocton projects. Among issues adversely affecting Liberty turbine performance were drive trains that incorporated a supplier-related deficiency, a design deficiency resulting in separation of bonding materials in the blades of several turbines and minor defects in the blade skin resulting from a defective manufacturing process. At present, all such items affecting our installed Clipper fleet have been remediated and availability of the Liberty turbines in our fleet is within warranted levels.

The Liberty turbines, however, may not perform in accordance with Clipper's specifications for their anticipated useful life or may require additional warranty or non-warranty repairs. In addition, the initial failure of performance has adversely affected our ability to arrange and close turbine supply loans, tax equity financing transactions and construction loans involving Liberty turbines. Moreover, Clipper may not be able to fund its obligations to us and its other customers under its outstanding warranty agreements.

A failure of Clipper to produce Liberty turbines that perform within design specifications would preclude us from completing projects that could otherwise incorporate Clipper technology and likely result in our determination to elect not to purchase any or all Liberty turbines that we have the right but not the obligation to acquire from 2011 through 2015.

19

We have paid Clipper approximately $60 million of deposits and progress payments towards turbine purchases from 2011–2015 and intend to pay approximately $30 million more in deposits and progress payments through January 15, 2011. If we elect for any reason not to acquire any additional turbines from Clipper, we will forfeit the pro rata portion of these deposits and progress payments corresponding to the schedule of future turbine purchases: $38.6 million for turbines scheduled to be purchased in 2011, $17.9 million for 2012, $10.7 million for 2013, $13.4 million for 2014 and $8.9 million for 2015.

We have no commitments from turbine manufacturers other than Clipper for projects we plan to have in construction after 2010.

A portion of our revenues from the sale of RECs are not hedged, and we are exposed to volatility of commodity prices with respect to those sales.

REC prices are driven by various market forces, including electricity prices and the availability of electricity from other renewable energy sources and conventional energy sources. We are unable to hedge a portion of our revenues from RECs in certain markets where conditions limit our ability to sell forward all of our RECs. Our ability to hedge RECs generated by our Northeast projects is limited by the unbundled nature of the RECs and the relative illiquidity of this market, and revenues associated with these RECs account for a majority of the unhedged revenue stream from our existing operating fleet. We are exposed to volatility of commodity prices with respect to the portion of RECs that are unhedged, including risks resulting from volatility in commodities, changes in regulations, including state RPS targets, general economic conditions and changes in the level of renewable energy generation. We will have quarterly variations in our revenues from the sale of unhedged RECs.

We have a limited operating history and our rapid growth may make it difficult for us to manage our business efficiently.

Since we began our business in 2002 and began commercial operation of our first wind energy project in 2006, there is limited history to use to evaluate our business. You should consider our prospects in light of the risks and uncertainties growing companies encounter in rapidly evolving industries such as ours. Also, our rapid growth may make it difficult for us to manage our business efficiently, effectively manage our capital expenditures and control our costs, including general and administrative costs. These challenges could have a material adverse effect on our business, financial condition and results of operation.

We rely on a limited number of key customers.

There are a limited number of possible customers for electricity and RECs produced in a given geographic location. As a result, we do not have many choices about the buyers of our electricity, which limits our ability to negotiate the terms under which we sell electricity. Also, since we depend on sales of electricity and RECs to certain key customers, our operations are highly dependent upon these customers' fulfilling their contractual obligations under our power purchase agreements (PPAs) and other material sales contracts. For example, 48% of our revenues were generated from sales of electricity under PPAs with three customers in the nine months ended September 30, 2009. Our customers may not comply with their contractual payment obligations or may become subject to insolvency or liquidation proceedings during the term of the relevant contracts. In addition, the credit support we received from such customers to secure their payments under the PPAs may not be sufficient to cover our losses if they fail to perform. To the extent that any of our customers are, or are controlled by, governmental entities, they may also be subject to legislative or other political action that impairs their contractual performance. Failure by any key customer to meet its contractual commitments or insolvency or liquidation of our customers could have a material adverse effect on our business, financial condition and results of operations.

20

We face competition primarily from other renewable energy sources and, in particular, other wind energy companies.