Attached files

| file | filename |

|---|---|

| EX-4.1 - Southfield Energy CORP | v169328_ex4-1.htm |

| EX-5.1 - Southfield Energy CORP | v169328_ex5-1.htm |

| EX-23.1 - Southfield Energy CORP | v169328_ex23-1.htm |

| EX-10.6 - Southfield Energy CORP | v169328_ex10-6.htm |

| EX-23.2 - Southfield Energy CORP | v169328_ex23-2.htm |

As

filed with the Securities and Exchange Commission on December 17,

2009

(Registration

No. 333-162029)

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington, D.C.

20549

Amendment

No. 2 to

FORM

S-1

REGISTRATION

STATEMENT

UNDER

THE

SECURITIES ACT OF 1933

Southfield

Energy Corporation

(Exact

name of registrant as specified in its charter)

|

Nevada

|

1311

|

20-5361270

|

||

|

(State

or other jurisdiction of

incorporation

or organization)

|

(Primary

Standard Industrial

Classification

Code Number)

|

(I.R.S.

Employer

Identification

Number)

|

1240

Blalock Road, Suite 150

Houston,

Texas 77055

( 713) 266-3700

(Address,

including zip code, and telephone number, including area code, of registrant’s

principal executive offices)

Ben

Roberts

Chief

Executive Officer

Southfield

Energy Corporation

1240

Blalock Road, Suite 150

Houston,

Texas 77055

Telephone:

(713) 266-3700

Facsimile:

(713) 266-3701

(Name,

address, including zip code, and telephone number, including area code, of agent

for service)

Copies

to:

Locke

Lord Bissell & Liddell LLP

600

Travis Street, Suite 3400

Houston,

Texas 77002

(713)

226-1249

Attn:

J. Eric Johnson

Approximate date of commencement of

proposed sale to the public: As soon as practicable after this

Registration Statement becomes effective.

If any of

the securities being registered on this Form are to be offered on a delayed or

continuous basis pursuant to Rule 415 under the Securities Act of 1933,

check the following box. x

If this

Form is filed to register additional securities for an offering pursuant to

Rule 462(b) under the Securities Act, please check the following box and

list the Securities Act registration statement number of the earlier effective

registration statement for the same offering. ¨

If this

Form is a post-effective amendment filed pursuant to Rule 462(c) under the

Securities Act, check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same

offering. ¨

If this

Form is a post-effective amendment filed pursuant to Rule 462(d) under the

Securities Act, check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same

offering. ¨

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting company. See

the definitions of “large accelerated filer,” “accelerated filer,” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act. (Check

one):

|

Large

accelerated filer ¨

|

Accelerated

filer ¨

|

Non-accelerated

filer ¨

|

Smaller

reporting company x

|

|

(Do

not check if a smaller reporting company)

|

|||

CALCULATION

OF REGISTRATION FEE

|

Title of Each Class of

Securities To Be

Registered

|

Amount to be

Registered

|

Proposed

Maximum Offering

Price Per Unit

|

Proposed Maximum

Aggregate

Offering Price

|

Amount of

Registration Fee

|

||||||||||||

|

Three

Year 10% Notes

|

$ | 10,000,000 | 100 | % | $ | 10,000,000 | $ | 558 | ||||||||

The registrant hereby amends this

registration statement on such date or dates as may be necessary to delay its

effective date until the registrant shall file a further amendment which

specifically states that

this registration statement shall thereafter become effective in accordance with

Section 8(a) of the Securities Act of 1933 or until the registration

statement shall become effective on such date as the Securities and Exchange

Commission, acting pursuant to said Section 8(a), may

determine.

|

The information in

this prospectus is not complete and may be changed. We may not sell these

securities until the registration statement filed with the Securities and

Exchange Commission is effective. This prospectus is

not an offer to sell these securities and it is not soliciting an offer to

buy these securities in any state where the offer or sale is not

permitted.

|

PROSPECTUS

Southfield

Energy Corporation

$10,000,000

Three Year 10% Notes

We are

offering up to $10,000,000 in aggregate principal amount of our Three Year Notes

(“3 Year Notes”) in a direct public offering on a continuous basis (the

“Offering”). A minimum initial investment of $1,000 is required. The

Offering will end upon the earlier of the receipt of the maximum aggregate

principal amount of $10,000,000 or one year from the effective date of this

prospectus (the “Closing”).

We will

issue the 3 Year Notes in denominations of at least $1,000, subject to the

initial investment requirement of $1,000. The 3 Year Notes shall mature

three years from the date of issuance. The 3 Year Notes shall bear

interest at a fixed rate (calculated based on a 365-day year) of ten percent

(10%) per annum. We will pay interest on a 3 year Note on a quarterly

basis in arrears; simple interest will accrue from the date of

purchase.

We are

offering the 3 Year Notes on a “self-underwritten” basis, with no minimum.

The officers and directors of the Company intend to sell the 3 Year Notes

directly, who will not be separately compensated therefor. The intended

methods of communication include, without limitation, telephone and personal

contact. For more information, see the section titled “Plan of

Distribution” herein. However, we reserve the right to utilize

broker-dealers, placement agents and/or finders (“Placement Agent”), where

permitted by law, to assist us in locating potential investors, in which case we

will pay commissions and non-accountable expenses of up to 11% of the gross

offering price of the 3 Year Notes. The Placement Agent will not be

required to sell any specific number or dollar amount of securities but will use

their best efforts to sell the 3 Year Notes.

We do not

have to sell any minimum amount of 3 Year Notes to accept and use the proceeds

from this Offering. We cannot assure you that all or any portion of the 3

Year Notes we are offering will be sold. If we fail to raise the maximum

aggregate principal amount of $10,000,000, we may not be able to

execute our business plan. You will not be entitled to the return

of your investment. The 3 Year Notes are not listed on any securities

exchange and there is no public trading market for the 3 Year Notes. We

have the right to reject any subscription, in whole or in part, for any or no

reason. We may redeem the 3 Year Notes in whole or in part and from time

to time after one year from the closing, but upon at least 15 days prior written

notice to you.

You

should read this prospectus and any applicable prospectus supplement carefully

before you invest in the 3 Year Notes. These 3 Year Notes are our general

unsecured obligations and will rank junior and be subordinate in right of

payment to all future senior debt. The 3 Year Notes will not be secured by

liens on any of our assets. Payment of the 3 Year Notes is not insured or

guaranteed by the Federal Deposit Insurance Corporation (“FDIC”), any

governmental or private insurance fund, or any other entity. We will

establish an initial interest reserve equal to five percent of the gross

proceeds from the Offering and will deposit such reserve with a third party as

subscriptions are accepted. With the exception of the interest reserve account,

we have not made any arrangements to place any of the proceeds from this

Offering in an escrow, trust or similar account.

We are

issuing the 3 Year Notes pursuant to an Indenture that contains provisions

related to events of default, the collective rights of the 3 Year Note holders,

and the servicing and administration of the 3 Year Notes.

2

See “Risk Factors” beginning

on page 12 for certain factors you should consider before buying the 3 Year

Notes .

Neither

the Securities and Exchange Commission nor any state securities commission has

approved or disapproved of these securities or determined if this prospectus is

truthful or complete. Any representation to the contrary is a criminal

offense.

|

Per 3 Year Note

|

Total

|

|||||||

|

Public

offering price

|

$ | 1,000 | $ | 10,000,000 | ||||

|

Underwriting

Commission and Non-Accountable Expense Allowance (1)

|

$ | 110 | $ | 1,100,000 | ||||

|

Other

Expenses (2)

|

$ | 100 | $ | 100,000 | ||||

|

Proceeds,

before expenses, to Southfield Energy Corporation

|

$ | 880 | $ | 8,800,000 | ||||

(1)

Assuming a Placement Agent is retained, represents the maximum amount of

commissions and non-accountable expenses to be paid assuming the maximum

aggregate principal amount of $10,000,000 is raised.

(2)

Includes professional services fees, printing and distribution costs and

Offering related travel and communication costs.

The

date of this prospectus is [●], 2009.

3

TABLE

OF CONTENTS

|

About

this Prospectus

|

5

|

||

|

Where

You Can Find More Information

|

5

|

||

|

Cautionary

Statement Concerning Forward-Looking Statements

|

6

|

||

|

Prospectus

Summary

|

8

|

||

|

Risk

Factors

|

12

|

||

|

Use

of Proceeds

|

22

|

||

|

Description

of 3 Year Notes

|

23

|

||

|

Summary

of Indenture

|

23

|

||

|

Material

Tax Consequences

|

26

|

||

|

Capitalization

|

31

|

||

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

32

|

||

|

Quantitative

and Qualitative Disclosures About Market Risk

|

39

|

||

|

Business

|

40

|

||

|

Management

|

52

|

||

|

Director

and Executive Officer Compensation

|

55

|

||

|

Certain

Relationships and Related Party Transactions

|

57

|

||

|

Security

Ownership of Certain Beneficial Owners and Management

|

58

|

||

|

Plan

of Distribution

|

59

|

||

|

Legal

Matters

|

60

|

||

|

Experts

|

60

|

||

|

Changes

In and Disagreements With Accountants On Accounting and Financial

Disclosure

|

60

|

||

|

Index

to Financial Statements

|

F-1

|

4

ABOUT

THIS PROSPECTUS

This

prospectus highlights selected information about us and our 3 Year Notes but

does not contain all the information that you should consider before investing

in the 3 Year Notes. You should read this entire prospectus carefully,

including the information included under the heading “Risk

Factors.”

You

should rely only on the information contained in this prospectus or to which we

have referred you. We a have not authorized anyone to provide you with

different information. If anyone provides you with different or inconsistent

information, you should not rely on it. We are not making an offer to sell

these securities in any jurisdiction where such offer or sale is not permitted.

You should assume that the information appearing in this prospectus is accurate

as of the date on the front cover of this prospectus only. Our business,

financial condition, results of operations and prospects may have changed since

that date.

WHERE

YOU CAN FIND MORE INFORMATION

We have

filed with the SEC, under the Securities Act of 1933, as amended (the

“Securities Act”), a registration statement on Form S-1 with respect to the

3 Year Notes offered in this prospectus. This prospectus, which constitutes part

of the registration statement, does not contain all the information set forth in

the registration statement or the exhibits and schedules which are part of the

registration statement, portions of which are omitted as permitted by the rules

and regulations of the U.S. Securities and Exchange Commission (“SEC”).

Statements made in this prospectus regarding the contents of any contract or

other document are summaries of the material terms of the contract or document.

With respect to each contract or document filed as an exhibit to the

registration statement, reference is made to the corresponding exhibit.

For further information pertaining to us and to the 3 Year Notes offered by this

prospectus, reference is made to the registration statement, including the

exhibits and schedules thereto, copies of which may be inspected, without

charge, at the public reference facilities of the SEC at 100 F Street, N.E.,

Room 1580, Washington, D.C. 20549. Copies of all or any portion of the

registration statement may be obtained from the SEC at prescribed rates.

Information on the public reference facilities may be obtained by calling the

SEC at 1-800-SEC-0330. In addition, the SEC maintains a web site that contains

reports, proxy and information statements, and other information that is filed

electronically with the SEC. The web site can be accessed at www.sec.gov

.

After

effectiveness of the registration statement, which includes this prospectus, we

will be required to comply with the informational requirements of the Securities

Exchange Act of 1934, as amended (the “Exchange Act”), and, accordingly, will

file current reports on Form 8-K, quarterly reports on Form 10-Q,

annual reports on Form 10-K, proxy statements and other information with

the SEC. Those reports, proxy statements and other information will be

available for inspection and copying at the public reference facilities, the SEC

web site referred to above and our own website at www.southfieldenergy.com

.

5

CAUTIONARY

STATEMENT CONCERNING FORWARD-LOOKING STATEMENTS

This

prospectus and the documents incorporated by reference in this prospectus

contain or incorporate by reference certain statements that are, or may be

deemed to be, “forward-looking statements” within the meaning of

Section 27A of the Securities Act and Section 21E of the Exchange

Act. Forward-looking statements include statements regarding our plans,

beliefs or current expectations and may be signified by the words “could,”

“should,” “expect,” “project,” “estimate,” “believe,” “anticipate,” “intend,”

“budget,” “plan,” “forecast,” “predict” and other similar expressions.

Forward-looking statements appear in a number of places throughout this

prospectus and the documents incorporated by reference into this prospectus with

respect to, among other things: profitability; planned capital

expenditures; estimates of oil and gas production; estimates of future oil and

gas prices; estimates of oil and gas reserves; our future financial condition or

results of operations; and our business strategy and other plans and objectives

for future operations.

By their

nature, forward-looking statements involve risks and uncertainties because they

relate to events and depend on circumstances that may or may not occur in the

future. We caution you that forward-looking statements are not guarantees

of future performance and that our actual results of operations, financial

condition and liquidity, and the development of the industry in which we

operate, may differ materially from those made in or suggested by the

forward-looking statements made in this prospectus. In addition, even if

our results of operations, financial condition and liquidity and the development

of the industry in which we operate are consistent with the forward-looking

statements contained in this prospectus, those results or developments may not

be indicative of results or developments in subsequent periods.

The

following listing represents some, but not necessarily all, of the risk factors

that may cause actual results to differ from those anticipated or

predicted:

|

|

•

|

the volatility of oil, natural

gas and natural gas liquid

prices;

|

|

|

•

|

estimation, development and

acquisition of oil and gas

reserves;

|

|

|

•

|

cash flow, liquidity and

financial condition;

|

|

|

•

|

business and financial

strategy;

|

|

|

•

|

amount, nature and timing of

capital expenditures;

|

|

|

•

|

availability and terms of

capital;

|

|

|

•

|

timing and amount of future

production of oil and gas;

|

|

|

•

|

availability of drilling,

production and well service equipment for our

operators;

|

|

|

•

|

operating costs and other

expenses;

|

|

|

•

|

prospect development and property

acquisitions;

|

|

|

•

|

marketing of oil, natural gas and

natural gas liquids;

|

|

|

•

|

competition in the oil and gas

industry;

|

|

|

•

|

the impact of weather and the

occurrence of natural disasters such as fires, earthquakes and other

catastrophic events;

|

|

|

•

|

governmental regulation of the

oil and gas industry;

|

|

|

•

|

developments in oil-producing and

gas-producing countries;

|

6

|

|

•

|

strategic plans, expectations and

objectives for future

operations;

|

|

|

•

|

the costs and legal liabilities

associated with being a “public”

company;

|

|

|

•

|

the amount of time required by

management to comply with being a public

company;

|

|

|

•

|

the depletion of our oil and gas

assets at a rate faster than

anticipated;

|

|

|

•

|

our ability to generate

sufficient revenues and cash flow to meet our short and long term

obligations;

|

|

|

•

|

our ability to hire and retain

qualified personnel to execute our operations;

and

|

|

|

•

|

global demand for and supply of

oil & natural gas.

|

You should also read carefully the

factors described in the “Risk factors” section beginning on page 12 to better understand the risks and

uncertainties inherent in our business and underlying any forward-looking

statements .

7

PROSPECTUS

SUMMARY

This

summary highlights information about us and the Offering contained elsewhere in

this prospectus. Because it is a summary, it does not contain all the

information that you should consider before investing in our 3 Year Notes.

You should read the entire prospectus carefully before making an investment

decision, including the information presented under the heading “Risk Factors”

and the historical financial statements and the accompanying notes thereto

included elsewhere in this prospectus.

All

references in this prospectus to “we,” “us,” “our,” “Company” and “Southfield”

refer to Southfield Energy Corporation.

Overview

We are an

independent energy company based in Houston, Texas that invests in the

exploration, development, and production of moderate risk, oil and gas wells in

the United States. We focus on partnering alongside proven operators

with strong track records of success. The Company’s core strategy is to

earn revenue from existing non-operated working interests while investing in new

opportunities to increase our oil and gas production and reserves; primarily

through acquisitions of existing production and working interest investments in

drilling programs of experienced and successful oil and gas operators active in

Texas, Louisiana and Oklahoma.

We

currently focus our efforts on our oil and natural gas properties on the Mary

King Estell lease in the Richard King Field of Nueces County, Texas. We

intend on building our business by acquiring additional non-operated working

interests in productive oil and natural gas wells and other oil and gas

interests. A non-operated working interest grants us a proportionate share

of the property’s oil and gas production, and requires us to pay a proportionate

share of the costs associated with drilling and production without acting as the

operator of the property’s wells.

We have a

non-operated working interest in five gas wells in the Richard King Field of

Nueces County, Texas. Durango Resources Corporation is the operator of the

wells.

Our

Properties

We

currently have the following oil and gas property interests:

|

Property

|

Non-Operated Working

Interest

|

Net Revenue

Interest

|

Area (acres)

|

|||||||||

|

Richard

King Field

|

15 | % | 11.25 | % (1) | 160 | |||||||

(1) Based

on a 75% net revenue interest for all working interest owners.

We are

mainly focused on the following activities:

|

|

·

|

Identifying attractive investment

opportunities in the oil and gas industry with moderate risk and favorable

upside potential;

|

|

|

·

|

Negotiating the acquisition of

working interests on terms that we feel are favorable to

us;

|

|

|

·

|

Acquiring non-operated working

interests in oil and gas wells and mineral interests that we can exploit

for the benefit of our

stockholders;

|

|

|

·

|

Earning secure and reliable

revenue from non-operated working interests while engaging in the

exploration and development of oil and gas properties to generate

additional revenue; and

|

|

|

·

|

Managing the return on our

investments to replace reserves and increase revenue through re-investment

activities.

|

8

The

following table sets forth summary information about our net oil and gas assets

as of December 31, 2008:

|

Estimated Proved Reserves at

December 31, 2008(1)

|

Production

for

the

Year

Ended

December 31,

|

Reserve-to-

Production

|

Estimated 2008

Production

|

|||||||||||||||||||||

|

Oil

(Bbl)

|

NGL

(Bbl)

|

Gas

(MMcf)

|

Total

(BOE)(2)

|

2008

(BOE)(2)

|

Ratio

(Years)(3) |

Decline

Rate(4)

|

||||||||||||||||||

|

5,690

|

1,780 | 217 | 43,637 | 7,127 | 6.12 | 14 | % | |||||||||||||||||

|

(1)

|

Proved Reserves are those

quantities of petroleum which, by analysis of geological and engineering

data, can be estimated with reasonable certainty to be commercially

recoverable, from a given date forward, from known reservoirs and under

current economic conditions, operating methods, and government

regulations.

|

|

(2)

|

Barrels of oil Equivalent (BOE)

is a unit of energy that approximates the energy released by burning one

barrel of oil. A BOE is typically 6,000 cubic feet of natural gas. BOE

calculations are estimates due to the variance of btu content amongst

barrels of oil and cubic feet of natural gas. BOE’s in the above table are

used as an approximation for measuring the total energy contained in oil

and natural gas either produced or remaining as

reserves.

|

|

(3)

|

This ratio estimates the number

of years that it would require to produce our remaining reserves assuming

that production rates are held

constant.

|

|

(4)

|

Estimated production decline

measures the petroleum produced as a percentage of the total reserves

remaining at the end of the period plus production in that

period.

|

|

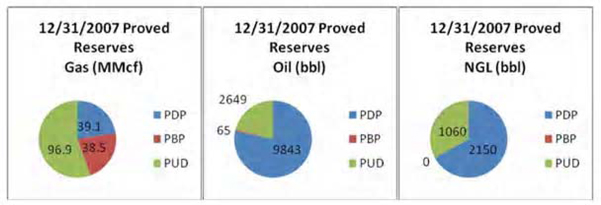

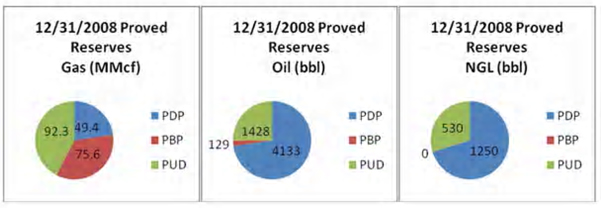

Aldwell Unit

|

Mary King Estell

|

|||||||||||||||

|

Oil (bbl)

|

Gas (MMcf)

|

Oil (bbl)

|

Gas (MMcf)

|

|||||||||||||

|

PDP

|

4,094 | 10.8 | 40 | 38.6 | ||||||||||||

|

PBP

|

0 | 0 | 129 | 75.6 | ||||||||||||

|

PUD

|

1,279 | 4.6 | 149 | 87.8 | ||||||||||||

|

Total

|

5,372 | 15.4 | 318 | 202 | ||||||||||||

Engineering

abbreviations are as follows: Proved Developed Reserves (PDP), Proved Behind

Pipe Reserves (PBP), and Proved Undeveloped Reserves (PUD)

We also

make equity investments in other oil and gas companies. In September and

October 2008, we purchased an aggregate of 350,000 shares of common stock of

Meridian Resources Corporation, an exploration and production company whose

shares trade on the New York Stock Exchange under the ticker symbol “TMR.”

As of December 31, 2008, we incurred an unrealized holding loss of $325,465 on

our investment. As of December 31, 2008 the net market value of our

investment was $199,500, comprising approximately 22.2% of total assets.

In June 2009, we sold an aggregate of 100,000 shares of common stock of Meridian

Resources and realized a loss of $134,096. Although we do not own equity

investments in any other company, we may buy such equities in the future.

We do not have any current plans, proposals or arrangements, written or

otherwise, to increase our equity investment in Meridian Resources Corporation

or any other company. As of September 30, 2009 we determined the decline in

value of the Meridian shares to be other than temporary. Based on this

determination the shares were adjusted to their market value as of September 30,

2009 of $102,500. The difference between the cost and market value of the shares

was recorded as impairment expense for $243,095.

In the

future, we may expand the scope of our investments depending on whether we find

any unique investment opportunities and if we have sufficient capital to execute

such plans. Our future business plans may include the acquisition of

mineral lease interests, purchase of existing production and infrastructure and

equipment.

Our

principal office is located at 1240 Blalock Road, Suite 150, Houston, Texas

77055. We currently lease approximately 3,000 square feet and incurred

approximately $25,000 in rent expense for 2008. We believe the size of our

office space is sufficient for our business purposes.

The

Offering

|

Securities

Offered

|

We

are offering up to $10,000,000 in aggregate principal amount of our 3 Year

Notes. The Company will establish an initial interest reserve equal to

five percent of gross proceeds from the Offering and deposit with a third

party as subscriptions are received. See “Description of 3 Year

Notes.”

|

||

|

Denominations

|

Increments

of at least $1,000.

|

||

|

Minimum

Investment

|

A

minimum initial investment of $1,000 is required.

|

||

|

Form of

Investment

|

Investments

in 3 Year Notes may be made by check or wire.

|

||

|

Interest

Rate

|

Fixed

interest rate, calculated using 365-day year, of 10% per

annum.

|

9

|

Payment

of Interest

|

Interest

is payable on a quarterly basis in arrears.

|

||

|

3

Year Maturity

|

3

Year Notes shall mature 3 years from the date of your

purchase.

|

||

|

Redemption

by Us

|

We

may redeem the 3 Year Notes at any time after one year from the date of

purchase and upon 15 days prior written notice to you for a price equal to

principal plus interest accrued to the date of

redemption.

|

||

|

Subordinated

|

3

Year Notes are general unsecured obligations and will rank junior and be

subordinate in right of payment to all future senior debt. The 3

Year Notes will not be secured by liens on any of our assets. This means

that if we are unable to pay our debts when due, the 3 Year Notes would

all be paid, if at all, after any payment would be made on any senior

debt.

|

||

|

Event

of Default

|

An

event of default on the 3 Year Notes is generally defined as a default in

the payment of principal, or a default in the payment of interest, our

becoming subject to certain events of bankruptcy or insolvency, or our

failure to comply with any covenant contained in the

Indenture.

|

||

|

Indenture

and Trustee

|

The

3 Year Notes will be governed by an Indenture and a trustee will represent

the interest of holders of 3 Year Notes.

|

||

|

Use

of Proceeds

|

If

all the 3 Year Notes offered by this prospectus are sold, we expect to

receive approximately $8,800,000 in net proceeds after deducting all costs

and expenses associated with this Offering, assuming a Placement Agent is

retained. We intend to use the net proceeds from this Offering to first

pay for operating expenses, including management compensation related to

the operation of the Company. We then plan on using the proceeds to

purchase working interests in existing oil and gas production and new

drilling opportunities. Further, we will reserve an amount of money

equal to 5% of the gross proceeds from the Offering for payment of

interest. See “Use of Proceeds” for more

information.

|

||

|

Material

Tax Consequences

|

For

a discussion of material federal income tax consequences that may be

relevant to prospective 3 Year Note holders who are individual citizens or

residents of the United States, please read “Material Tax

Consequences.”

|

||

|

Listing

and Trading Symbol

|

Our

3 Year Notes have not been approved for trading on any exchange and we

have no current plans to request such a listing.

|

||

|

Risk

Factors

|

See

“Risk Factors” on page 12 and other information included in this

prospectus and any prospectus supplement for a discussion of factors you

should carefully consider before investing in the 3 Year

Notes.

|

||

10

Our

Company

We were

incorporated in the State of Nevada on July 5, 2005 with the objective to own

and acquire producing oil and gas properties and to participate in the drilling

of new oil & gas wells. Our principal office is located at 1240

Blalock Road, Suite 150, Houston, Texas 77055. Our telephone number is

(713) 266-3700. Information about us can be found at www.southfieldenergy.com.

Information contained in our website does not constitute part of this

prospectus.

Other

Information

We expect

to make our periodic reports and other information filed or furnished to the SEC

available, free of charge, through our website, as soon as reasonably

practicable after those reports and other information are electronically filed

with or furnished to the SEC. Information on our website or any other

website is not incorporated by reference into this prospectus and does not

constitute a part of this prospectus.

11

RISK

FACTORS

The nature of our business

activities subjects us to certain hazards and risks. You should consider

carefully the following risk factors together with all of the other information

included in this prospectus in evaluating an investment in our 3 Year Notes.

The risk factors set forth below are

not the only risks that may affect our business. Our business could also be

impacted by additional risks not currently known to us or that we currently deem

to be immaterial. If any of the following risks were

actually to occur, our business, financial condition or results of operations

could be materially adversely affected. In that case, we might not be able to

pay the principal and

interest on our

3 Year Notes, and you could

lose part or all of your investment .

Risks

Related to Our Business

We may not have

sufficient cash flow from operations to pay interest on the 3

Year Notes when due or to repay principal upon maturity.

Revenue

and profit from oil and gas is uncertain. Prices may drop lower than they

are today. We expect to invest in working interests in new oil and gas

wells. These investments may not be profitable and we may lose our entire

investment. Oil and gas properties are depleting assets and we will have

to successfully continue to find additional oil and gas to offset the natural

decline of producing wells in which we own an interest. These

uncertainties are a material risk of investing in oil and gas and may materially

affect our ability to make interest payments when due and to repay principal

upon maturity.

The

amount of cash we actually generate will depend upon numerous factors related to

our business including, among other things:

|

|

•

|

the amount of oil and gas our

operators produce;

|

|

|

•

|

the prices at which our operators

sell our oil and gas

production;

|

|

|

•

|

the level of our operating costs,

including fees and reimbursement of expenses expended to operate the

company and to compensate its management team, board of directors and

employees;

|

|

|

•

|

our ability to replace declining

reserves;

|

|

|

•

|

prevailing economic

conditions;

|

|

|

•

|

the level of competition we

face;

|

|

|

•

|

fuel conservation measures and

alternate fuel

requirements; and

|

|

|

•

|

government regulation and

taxation.

|

In

addition, the actual amount of cash that we will have available to make payments

on the principal and interest of the 3 Year Notes will depend on other factors,

including:

|

|

•

|

the level of our expenditures for

acquisitions of additional oil and gas

investments;

|

|

|

•

|

our ability to make borrowings or

to raise additional capital in the

future;

|

|

|

•

|

sources of cash used to fund

acquisitions;

|

|

|

•

|

debt service requirements

of our 3 Year Notes or future financing

agreements;

|

|

|

•

|

fluctuations in our working

capital needs;

|

12

|

|

•

|

general and administrative

expenses;

|

|

|

•

|

timing and collectability of any

receivables; and

|

|

|

•

|

the amount of cash reserves

established by our management team for the proper conduct of our

business.

|

All of

our current revenues are generated by our interest in the Richard King

Field. Delays or interruptions in our interests in the Richard King Field

natural gas and production operations including, but not limited to, the failure

of third parties on which we rely to provide key services, could negatively

impact our revenues.

Approximately

80% of our oil and natural gas revenue for the year ended December 31, 2008 and

the nine months ended September 30, 2009 was derived from the Richard King

Field. As of September 30, 2009, 100% of our oil and natural gas

properties were derived from the Richard King Field. Should the production in

this field decrease at a rate faster than anticipated, our revenues and cash

flow to make payments on the 3 Year Notes could be adversely affected. In

connection with the Richard King Field, we have partnered with Durango Resources

Corporation as operator. The failure of Durango Resources to perform its

duties as operator in the Richard King Field could prevent us from generating

revenues. In addition, events referred to as force majeure, such as an act

of God, act of a public enemy, fire, flood, lightning, etc. could prevent us

from generating revenues.

Effective

September 2009, we sold our assets located in the Aldwell Unit to Mariner

Energy, Inc., the operator, for approximately $300,000, excluding a six percent

sales commission. The Aldwell Unit accounted for the remaining balance of

our oil and natural gas revenue for the year ended December 31, 2008 and the

nine months ended September 30, 2009. As such, for the remainder of the

fiscal year, our future revenues will be derived primarily from our Richard King

Field properties.

Our

business may be harmed by failures of third party operators on which we

rely.

Our

ability to manage and mitigate the various risks associated with our operations

in Nueces County, Texas, is limited since we rely on third parties to operate

our projects. We are a non-operating interest owner in our properties. With

respect to our non-operated working interests, we have entered into agreements

with third party operators for the conduct and supervision of drilling,

completion and production operations. In the event that commercial

quantities of oil and natural gas are discovered on one of our properties, the

success of the oil and natural gas operations on that property depends in large

measure on whether the operator of the property properly performs its

obligations. The failure of such operators and their contractors to

perform their services in a proper manner could result in materially adverse

consequences to the owners of interests in that particular property, including

us.

We

cannot control activities on properties we do not operate. Our inability to fund

required capital expenditures with respect to non-operated properties may result

in a reduction or forfeiture of our interests in those properties.

Other

companies operated all of our production as of September 30, 2009. We have

limited ability to exercise influence over operations for these properties or

their associated costs. Our dependence on the operator and other working

interest owners for these projects and our limited ability to influence

operations and associated costs could prevent the realization of our targeted

returns on capital with respect to exploration, exploitation, development or

acquisition activities. The success and timing of exploration, exploitation and

development activities on properties operated by others depend upon a number of

factors determined by the operator, including:

|

|

•

|

the timing and amount of capital

expenditures;

|

|

|

•

|

the operator's expertise and

financial resources;

|

|

|

•

|

approval of other participants in

drilling wells; and

|

|

|

•

|

selection of drilling, completion

and production equipment.

|

Where we

are not the majority owner or operator of a particular oil and natural gas

project, we may have no control over the timing or amount of capital

expenditures associated with the project. If we are not willing and able

to fund required capital expenditures relating to a project when required by the

majority owner or operator, our interests in the project may be reduced or

forfeited.

13

Because oil and

gas properties are depleting

assets we must

drill new

wells or make acquisitions

in order to maintain our production and reserves and sustain our payments of

principal and interest to the 3 Year Note holders over

time.

Producing

oil and gas reservoirs are characterized by declining production rates.

Because our reserves and production decline continually over time, we will

need to drill additional wells or make acquisitions to sustain revenue over

time. We may be unable to accomplish this if:

|

|

•

|

Sellers do not agree to sell any

assets to us;

|

|

|

•

|

we are unable to identify

attractive drilling or acquisition opportunities in our area of

operations;

|

|

|

•

|

we are unable to agree on

investment terms or a purchase price for assets that are attractive to us;

or

|

|

|

•

|

we are unable to obtain financing

for acquisitions on economically acceptable

terms.

|

We will require

substantial capital expenditures to replace our production and reserves, which

will reduce our available cash

for interest and principal payments. We may be unable

to obtain needed capital or financing due to our financial

condition, which could

adversely affect our ability to replace our production and proved

reserves.

To fund

our projects, we will be required to use cash generated from our operations in

addition to the proceeds of this Offering. We may also engage in

additional borrowings or obtain financing from the issuance of additional equity

interests in the Company, or some combination thereof. To the extent our

production declines faster than we anticipate or the cost to acquire additional

reserves is greater than we anticipate, we will require a greater amount of

capital to maintain our production and proved reserves. The use of cash

generated from operations to fund oil and gas investments will reduce cash

available to pay interest and principal on our 3 Year Notes. Our ability

to obtain bank financing or to access the capital markets for future equity or

debt offerings may be limited by our financial condition at the time of any such

financing or offering, the covenants in our 3 Year Notes or future financing

agreements, adverse market conditions or other contingencies and uncertainties

that are beyond our control. Our failure to obtain the funds necessary for

future oil and gas investments could materially affect our business, results of

operations, financial condition and ability to pay interest and principal on the

3 Year Notes.

Any new wells in

which we participate are subject to

substantial risks that could reduce our ability to make profits from

operations.

Investments

that we believe will increase revenue, may nevertheless result in losses.

Any oil and gas investment involves potential risks, including, among

other things:

|

|

•

|

the validity of our assumptions

about reserves, future production, revenues and costs, including

synergies;

|

|

|

•

|

a decrease in our liquidity by

using a significant portion of our available cash to finance

investments;

|

14

|

•

|

a significant increase in our

interest expense or financial leverage if we incur additional debt to

finance investments;

|

|

•

|

the diversion of management’s

attention from other business concerns;

and

|

|

•

|

an inability to hire, train or

retain qualified personnel to manage and operate our growing business and

assets.

|

We

could lose our ownership interests in our properties due to a title defect of

which we are not presently aware.

As is

customary in the oil and gas industry, only a perfunctory title examination, if

any, is conducted at the time properties believed to be suitable for drilling

operations are first acquired. Before starting drilling operations, a more

thorough title examination is usually conducted and curative work is performed

on known significant title defects. We typically depend upon title opinions

prepared at the request of the operator of the property to be drilled. The

existence of a title defect on one or more of the properties in which we have an

interest could render it worthless and could result in a large expense to our

business. Industry standard forms of operating agreements usually provide that

the operator of an oil and natural gas property is not to be monetarily liable

for loss or impairment of title. The operating agreements to which we are a

party provide that, in the event of a monetary loss arising from title failure,

the loss shall be borne by all parties in proportion to their interest

owned.

The prices

of oil and

gas have

reached historic highs in

recent years and are highly

volatile. A sustained decline in these commodity prices would

cause a

decline in our cash flow from operations, which may force us to reduce

principal

and interest payments on the 3 Year Notes or cease

paying them altogether.

The oil

and gas markets are highly volatile, and future oil and gas prices are

uncertain. Oil and gas prices reached historically high levels in mid 2008, when

oil sold for over $140 per barrel and natural gas sold for over $12 per thousand

cubic feet (mcf). However, as of the date of this Offering, prices for oil and

natural gas are currently fluctuating between $60-80 per barrel and $3-5 per

mcf, less than 50% of their previous highs. Prices for oil and gas may fluctuate

widely in response to relatively minor changes in the supply of and demand for

oil and gas, market uncertainty and a variety of additional factors, such

as:

|

•

|

domestic and foreign supply of

and demand for oil and gas;

|

|

•

|

weather

conditions;

|

|

•

|

overall domestic and global

political and economic conditions, including those in the Middle East,

Africa and South America;

|

|

•

|

actions of the Organization of

Petroleum Exporting Countries and other state-controlled oil companies

relating to oil price and production

controls;

|

|

•

|

the impact of increasing

liquefied natural gas, or LNG, deliveries to the United

States;

|

|

•

|

technological advances affecting

energy consumption and energy

supply;

|

|

•

|

domestic and foreign governmental

regulations and taxation;

|

|

•

|

the impact of energy conservation

efforts;

|

|

•

|

the capacity, cost and

availability of oil and gas pipelines and other transportation facilities,

and the proximity of these facilities to our wells;

and

|

|

•

|

the price and availability of

alternative fuels.

|

15

Our

revenue, profitability and cash flow depend upon the prices and demand for oil

and gas, and a drop in prices can significantly affect our financial results and

impede our growth. We may not be able to sustain payments of principal and

interest to the 3 Year Note holders during periods of lower commodity

prices.

Future price

declines may result in another write-down of our asset carrying values, which

could adversely affect our results of operations and limit our ability to borrow

and make payments on the

principal and interest to the 3 Year Note holders.

Due to

low commodity prices for oil and gas at December 31, 2008, we were required to

impair our assets located in the Aldwell Unit. An impairment test was conducted

using data in a reserve report prepared by a reserve engineering firm. While

conducting the impairment test, management determined that the estimated

undiscounted future net cash flow provided in the reserve report was less that

the carrying value of the Aldwell Unit on the Company’s Balance Sheet on

December 31, 2008 and that the assets were subject to impairment. The assets

were subsequently impaired.

Further

declines in oil and gas prices may result in our having to make substantial

downward adjustments to our estimated proved reserves. If this occurs, or if our

estimates of production or economic factors change, accounting rules may require

us to write down, as a noncash expense, the carrying value of our oil and gas

properties for impairments. We are required to perform impairment tests on our

assets whenever events or changes in circumstances warrant a review of our

assets. To the extent such tests indicate a reduction of the estimated useful

life or estimated future cash flows of our assets, the carrying values may not

be recoverable and therefore require write-downs. We may incur further

impairment charges in the future, which could materially affect our results of

operations in the period incurred and our ability to borrow funds, which in turn

may adversely affect our ability to generate revenues.

Our future

hedging

activities could result in financial losses or could reduce our income, which

may adversely affect our ability to repay

interest

and principal on the 3 Year Notes when due.

To

achieve more predictable cash flow and to reduce our exposure to adverse

fluctuations in the prices of oil and gas, we may enter into derivative

arrangements covering a significant portion of our oil and gas production that

could result in both realized and unrealized hedging losses.

Our

estimated proved reserves are based on many assumptions that may prove to be

inaccurate. Any material inaccuracies in these reserve estimates or underlying

assumptions will materially affect the quantities and present value of our

proved reserves.

It is not

possible to measure underground accumulations of oil or gas in an exact way. Oil

and gas reserve engineering requires subjective estimates of underground

accumulations of oil and gas and assumptions concerning future oil, natural gas

and natural gas liquid (“NGL”) prices, production levels, and operating and

development costs. In estimating our level of proved oil and gas reserves, we

and our independent reservoir engineers make certain assumptions that may prove

to be incorrect, including assumptions relating to:

|

•

|

a constant level of future oil,

NGL and gas prices;

|

|

•

|

future production

levels;

|

|

•

|

capital

expenditures;

|

|

•

|

operating and development

costs;

|

|

•

|

the effects of regulation;

and

|

|

•

|

availability of

funds.

|

16

If these

assumptions prove to be incorrect, our estimates of proved reserves, the

economically recoverable quantities of oil, NGL and gas attributable to any

particular group of properties, the classifications of reserves based on risk of

recovery and our estimates of the future net cash flows from our proved reserves

could change significantly. Over time, we may make material changes to reserve

estimates to take into account changes in our assumptions and the results of

actual drilling and production.

The

present value of future net cash flows from our estimated proved reserves is not

necessarily the same as the current market value of our estimated proved oil and

gas reserves. We base the estimated discounted future net cash flows from our

estimated proved reserves on prices and costs in effect on the day of estimate.

However, actual future net cash flows from our oil and gas properties also will

be affected by factors such as:

|

•

|

the actual prices we receive for

oil, NGL and gas;

|

|

•

|

our actual operating costs in

producing oil, NGL and gas;

|

|

•

|

the amount and timing of actual

production;

|

|

•

|

the amount and timing of our

capital expenditures;

|

|

•

|

supply of and demand for oil, NGL

and gas; and

|

|

•

|

changes in governmental

regulations or taxation.

|

The

timing of both our production and our incurrence of expenses in connection with

the production and development of oil and gas properties will affect the timing

of actual future net cash flows from proved reserves, and thus their actual

present value. In addition, the 10% discount factor we use when calculating

discounted future net cash flows in compliance with the Financial Accounting

Standards Board’s Statement of Financial Accounting Standards No. 69 may not be

the most appropriate discount factor based on interest rates in effect from time

to time and risks associated with us or the oil and gas industry in

general.

Producing oil and

gas involves numerous risks and uncertainties that could adversely affect our

financial condition or results of operations and, as a result, limit

our ability

to pay principal and

interest payments to our

3 Year Note

holders.

As

non-operated working interest owners we do not operate wells; however, we share

in the costs of production for these wells. The operating cost of a well

includes variable costs, and increases in these costs can adversely affect the

economics of a well. Furthermore, our producing operations may be curtailed or

delayed or become uneconomical as a result of other factors,

including:

|

•

|

high costs, shortages or delivery

delays of equipment, labor or other

services;

|

|

•

|

unexpected operational events

and/or conditions;

|

|

•

|

reductions in oil, NGL and gas

prices;

|

|

•

|

limitations in the market for

oil, NGL and gas;

|

|

•

|

adverse weather

conditions;

|

|

•

|

facility or equipment

malfunctions;

|

|

•

|

equipment failures or

accidents;

|

|

•

|

title

problems;

|

17

|

•

|

pipe or cement failures or casing

collapses;

|

|

•

|

compliance with environmental and

other governmental

requirements;

|

|

•

|

environmental hazards, such as

gas leaks, oil spills, pipeline ruptures and discharges of toxic

gases;

|

|

•

|

lost or damaged oilfield work

over and service tools;

|

|

•

|

unusual or unexpected geological

formations or pressure or irregularities in

formations;

|

|

•

|

fires;

|

|

•

|

natural disasters;

and

|

|

•

|

uncontrollable flows of oil, gas

or well fluids.

|

If any of

these factors were to occur with respect to a particular field, we could lose

all or a part of our investment in the field, or we could fail to realize the

expected benefits from the field, either of which could materially and adversely

affect our revenue and profitability.

We may incur debt

to enable us to pay our interest and

principal payments, which may negatively affect our ability to execute our

business plan.

If we use

borrowings under a credit facility to meet 3 Year Note obligations for an

extended period of time rather than toward funding future investments and other

matters relating to our operations, we may be unable to support or grow our

business. Such a curtailment of our business activities, combined with our

payment of principal and interest on our future indebtedness to pay these

distributions, will reduce our cash available to make payments of principal and

interest on our 3 Year Notes and will materially affect our business, financial

condition and results of operations.

Our

operations are subject to operational hazards and unforeseen interruptions for

which we may not be adequately insured.

Operators

of our wells are subject to a variety of operating risks in our wells, gathering

systems and associated facilities, such as leaks, explosions, mechanical

problems and natural disasters, all of which could cause substantial financial

losses. Any of these or other similar occurrences could result in the disruption

of our operations, substantial repair costs, personal injury or loss of human

life, significant damage to property, environmental pollution, impairment of our

operations and substantial revenue losses.

We

currently possess a Business Owners insurance policy which includes property,

business interruption and general liability insurance at levels we believe are

appropriate for an early stage company; however, insurance against all

operational risk is not available to us. We are not fully insured against all

risks. In addition, pollution and environmental risks generally are not fully

insurable.

Shortages of

drilling rigs, supplies, oilfield services, equipment and crews could delay our

operations and reduce our available

cash.

To the

extent that in the future we acquire and develop undeveloped properties, higher

commodity prices generally increase the demand for drilling rigs, supplies,

services, equipment and crews, and can lead to shortages of, and increasing

costs for, drilling equipment, services and personnel. Shortages of, or

increasing costs for, experienced drilling crews and equipment and services

could restrict our future ability to drill wells and conduct operations. Any

delay in the drilling of new wells or significant increase in drilling costs

could reduce our future revenues and cash available for

distribution.

18

The

third parties on whom we rely for gathering and transportation services are

subject to complex federal, state and other laws that could adversely affect the

cost, manner or feasibility of conducting our business.

The

operations of the third parties on whom we rely for gathering and transportation

services are subject to complex and stringent laws and regulations that require

obtaining and maintaining numerous permits, approvals and certifications from

various federal, state and local government authorities. These third parties may

incur substantial costs in order to comply with existing laws and regulation. If

existing laws and regulations governing such third party services are revised or

reinterpreted, or if new laws and regulations become applicable to their

operations, these changes may affect the costs that we pay for such services.

Similarly, a failure to comply with such laws and regulations by the third

parties on whom we rely could have a material adverse effect on our business,

financial condition, and results of operations.

If third-party

pipelines and other facilities interconnected to our gas pipelines and

processing facilities become partially or fully unavailable to transport gas,

our revenues from

operations could be

adversely affected.

We depend

upon third party pipelines and other facilities that provide delivery options to

and from pipelines and processing facilities that our operators utilize. If any

of these third-party pipelines and other facilities become partially or fully

unavailable to transport gas, or if the gas quality specifications for these

pipelines or facilities change so as to restrict our operators’ ability to

transport gas on these pipelines or facilities, our revenues and cash available

to make principal and interest payments to the 3 Year Note holders could be

adversely affected.

Our

operations are subject to various litigation risks that could increase our

expenses, impact our profitability and lower the value of your investment in

us.

We are

not currently involved in any litigation; however, the nature of our operations

exposes us to possible future litigation claims. There is a risk that any claim

could be adversely decided against us, which could harm our financial condition

and results of operations. Similarly, the costs associated with defending

against any claim could dramatically increase our expenses, as litigation is

often very expensive. Possible litigation matters may include, but are not

limited to, environmental damage and remediation, insurance coverage, property

rights and easements and the maintenance of oil and gas leases. Should we become

involved in any litigation we will be forced to direct our limited resources to

defending against or prosecuting the claim(s), which could impact our

profitability and lower the value of your investment in us.

Our

business is subject to environmental legislation and any changes in such

legislation could prevent us from earning revenues.

The oil

and gas industry is subject to many laws and regulations that govern the

protection of the environment, health and safety and the management,

transportation and disposal of hazardous substances. These laws and regulations

may require the removal or remediation of pollutants and may impose civil and

criminal penalties for any violations thereof. Some of the laws and regulations

authorize the recovery of natural resource damages by the government, injunctive

relief and the imposition of stop, control, remediation and abandonment

orders.

Complying

with environmental and natural resource laws and regulations may increase our

operating costs as well as restrict the scope of our operations. Any regulatory

changes that impose additional environmental restrictions or requirements on us

could affect us in a similar manner. If the costs of such compliance or changes

exceed our budgeted costs, we may not be able to earn revenues.

19

We

may become an “investment company” as defined in the Investment Company Act of

1940.

Under the

Investment Company Act of 1940 (the “Act”), as amended, we may be deemed to be

an inadvertent investment company if it is determined that the value of the

Company’s equity investment in Meridian Resources Corporation account for more

than 40% of the total value of the Company’s assets, and no other exemption is

available. As of September 30, 2009 our investment in Meridian Resources

Corporation comprised only approximately 12.4% of total assets but this

percentage can increase in the future if the price per share of Meridian

Resources common stock increases. As well, if we make other equity investments

in other oil and gas companies, these investments will be aggregated with our

Meridian Resources investment to determine if we surpass the 40% threshold. If

so, and if we were to be deemed an inadvertent investment company, we believe

that we may be eligible for temporary relief from the application of the Act if

we have a bona fide intent to be engaged primarily, as soon as reasonably

possible (in any event within one year), in a business other than that of

investing, reinvesting, owning, holding or trading in securities. We may also

sell a number of shares of common stock of Meridian Resources or any other

future equity investments in other companies to lower the percentage below 40%.

However, we may sell such stock at times that may not be ideal for us which

adversely affect the price we receive. We do not have any current plans,

proposals or arrangements, written or otherwise, to increase our equity

investment in Meridian Resources Corporation or any other company.

Investment

companies are subject to substantial regulation concerning management,

operations, transactions with affiliated persons, portfolio composition,

including restrictions with respect to diversification and industry

concentration and other restrictions, and, unless we complied with the Act, we

would be prohibited from engaging in transactions involving interstate commerce.

To comply, we would be required to significantly modify our operating structure

and file reports with the SEC regarding various aspects of our business. The

cost of such compliance would result in the Company incurring substantial

additional annual expenses. In addition, compliance with the Act may not be

consistent with the Company’s current business strategies.

Risks

Related to this Offering

We may issue

additional debt, including notes

that are

senior to the current 3 Year Notes , without your

approval.

The

amount of additional debt that can be raised by us is not limited. We may issue

an unlimited number of notes that are senior to the 3 Year Notes without your

approval.

3

Year Note Holders will not have the same rights to vote on matters submitted to

the shareholders for consideration and approval as the holders of common

shares.

Certain

matters, such as the appointment of directors, amendment of corporate documents,

etc. must be submitted to a vote of the shareholders for approval. The 3 Year

Note Holders will not have voting rights on such matters as do the common

shareholders.

3

Year Note Holders will have very limited liquidity for their 3 Year Notes. We do

not intend nor expect to request that Southfield be listed for trading on any

exchange.

The

Company does not intend nor expect to list the 3 Year Notes registered in this

Offering for trading on any exchange or over-the-counter listing service. As a

result, the Holders of the 3 Year Notes are not expected to have any market

liquidity in their investment and should be prepared to hold the 3 Year Notes to

Maturity.

As a result of

investing in our 3 Year Notes, you

may become subject to state and local taxes.

Interest

earned on the 3 Year Notes will be taxed by the Federal and state governments in

accordance with current and future tax laws. You should expect to pay taxes at

your marginal rate for investments of this type.

Some

of our officers and directors have relationships with other companies in the oil

and natural gas industry that could result in conflicts of

interest.

Some of

our officers and directors serve as officers and directors of other companies

engaged in the oil and natural gas industry and may have other relationships

with such companies. For example, Chet Gutowsky and Tyson Rohde both serve as

officers and directors of Biotricity Corporation, an alternative energy company

located in Houston, Texas. To the extent those companies are involved in

ventures in which we may participate, or compete for acquisitions or financial

resources with us, the relevant director will face a conflict of interest. In

the event such a conflict arises, the relevant director will be required to

disclose the nature and extent of the conflict and abstain from voting for or

against any action of the board of directors that is or could be affected by the

conflict.

20

We

are dependent upon our key officers and employees and our inability to retain

and attract key personnel could significantly hinder our growth strategy and

cause our business to fail.

A loss of

one or more of our current directors, officers or key employees could severely

and negatively impact our operations and delay or preclude us from achieving our

business objectives. Our executive officers have a combined experience of

approximately 50 years in the oil and gas industry. We have not entered into

employment agreements with our officers, and we could suffer the loss of key

individuals for one reason or another at any time in the future. There is no

guarantee that we could attract or locate other individuals with similar skills

or experience to carry out our business objectives.

Our

directors and officers hold significant positions in our shares of common stock

and their interests may not always be aligned with those of our other

shareholders.

As of

September 30, 2009 our directors and officers beneficially own 18.9% of our

outstanding common stock. See “Security Ownership of Certain Beneficial Owners

and Management.” This shareholding level will allow the directors, officers and

certain beneficial owners to have a significant degree of influence on matters

that are required to be approved by shareholders, including the election of

directors and the approval of significant transactions. The short-term interests

of our directors, officers and certain beneficial owners may not always be

aligned with the long-term interests of our shareholders, and vice versa.

Because our directors, officers and certain beneficial owners have a significant

degree of influence on matters that are required to be approved by our

shareholders, they could influence the approval of transactions.

The 3 Year Notes

will not be issued under the protections of the Trust Indenture Act of

1939.

You should be aware that the Indenture is not a trust indenture qualified under

the Trust Indenture Act of 1939, as amended

(the “Indenture Act”). A qualified

trust indenture is often required for public offerings of debt securities in

principal amounts of more than $10 million. A non-qualified trust indenture may

also be required in public offerings of debt securities in principal amounts

less than $10 million. The term “qualified” relates

to mandatory provisions of a trust indenture and the requirements of

independence of the indenture trustee in relation to the entity offering the

debt securities. The presence of a qualified trust indenture and independent

indenture trustee is generally intended to provide for the collective

representation of debt investors through the monitoring activities of the

indenture trustee as to:

|

|

·

|

The authentication and issuance of debt

securities;

|

|

|

·

|

The monitoring of events of default and the taking

of remedial action by the trustee for the collective benefit of the

investors;

|

|

|

·

|

The maintenance of collateral which may secure the

debt security obligations;

and

|

|

|

·

|

Other matters relating to the terms of the debt

security issuance intended to protect investor initially and on a

continuous basis.

|

While we believe the Indenture contains some of the

terms and provisions of a qualified trust

indenture, you do not have all the protective aspects of a trust indenture and

an independent trustee and may be required to act individually on your own

behalf if we fail to make a required principal or interest payment on your 3 Year

Note.

We

have not deposited any collateral with the Trustee to secure payment of any

interest of principal on the 3 Year Notes.

We are

offering unsecured, general obligation 3 Year Notes. As such, we are not

required and have not deposited any collateral with the Trustee to secure

payment of interest and principal on 3 Year Notes. We will only reserve an

amount equal to 5% of gross proceeds from the Offering for payment of

interest.

There

may not be any money available to pay your respective 3 Year Note.

We will

issue 3 Year Notes as subscriptions are accepted by us. Each 3 Year Note will be

issued as of the acceptance date, and will mature 3 years from the date of

issuance. Your 3 Year Note may have a later maturity date than investors who

subscribed before you. It is possible that some investors who subscribed before

you will receive principal and interest payments before you, by virtue of them

subscribing to the Offering before you. We may run out of money to fulfill our

principal and interest obligations to you and other investors who subscribed at

the same time or later than you.

21

USE

OF PROCEEDS

We expect

to receive net proceeds from this Offering of approximately $8.8 million,

assuming the maximum offering of $10.0 million is raised and further assuming

that we will engage the services of a Placement Agent to assist in selling the 3

Year Notes. In such event, we estimate that we would pay Placement Agent

commissions of up to $800,000 and a non-accountable expense allowance of up to