Attached files

Table of Contents

As filed with the Securities and Exchange Commission on December 7, 2009

No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

LL Services Inc.

to be renamed

LANGUAGE LINE SERVICES HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 4899 | 27-1316758 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

One Lower Ragsdale Drive

Monterey, California 93940

(877) 886-3885

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Dennis G. Dracup

Chairman and Chief Executive Officer

Language Line Services Holdings, Inc.

One Lower Ragsdale Drive

Monterey, California 93940

(831) 648-5811

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

| Joshua N. Korff, Esq. Kirkland & Ellis LLP 601 Lexington Avenue New York, New York 10022 (212) 446-4800 |

Richard D. Truesdell, Jr., Esq. Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 (212) 450-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ | |||||

| (Do not check if a smaller reporting company) |

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(2) | ||

| Common Stock, $0.01 par value per share |

$400,000,000 | $22,320 | ||

| (1) | Includes shares of common stock that may be sold if the over-allotment option granted to the underwriters is exercised in full. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We and the selling stockholder may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS (Subject to Completion)

Issued December 7, 2009

Shares

LANGUAGE LINE SERVICES HOLDINGS, INC.

Common Stock

Language Line Services Holdings, Inc. is offering shares of its common stock and the selling stockholder is selling shares. We will not receive any of the proceeds from the shares of common stock being sold by the selling stockholder. This is our initial public offering and no public market exists for our shares. We anticipate that the initial public offering price will be between $ and $ per share.

Investing in our common stock involves risk. See “Risk Factors” beginning on page 15 to read about factors you should consider before buying shares of our common stock.

We intend to apply to list our common stock on The NASDAQ Global Market under the symbol “ .”

| Per Share | Total | |||||

| Price to Public |

$ | $ | ||||

| Underwriting Discounts and Commissions |

$ | $ | ||||

| Proceeds, Before Expenses, to Language Line Services Holdings, Inc. |

$ | $ | ||||

| Proceeds, Before Expenses, to the Selling Stockholder |

$ | $ | ||||

The underwriters may also purchase up to an additional shares of common stock from the selling stockholder at the public offering price, less the underwriting discount, within 30 days from the date of this prospectus to cover over-allotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares to purchasers on , 2010.

| Morgan Stanley | Credit Suisse | BofA Merrill Lynch |

, 2010.

Table of Contents

[ARTWORK]

Table of Contents

You should rely only on the information contained in this prospectus or in any free-writing prospectus we may specifically authorize to be delivered or made available to you. We have not, the selling stockholder has not and the underwriters have not authorized anyone to provide you with additional or different information. We and the selling stockholder are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where such offers and sales are permitted. The information in this prospectus or a free-writing prospectus is accurate only as of its date, regardless of its time of delivery or of any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

Until , 2010 (25 days after the commencement of the offering), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to unsold allotments or subscriptions.

i

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider in making your investment decision. You should read the following summary together with the entire prospectus, including the more detailed information regarding us, the common stock being sold in this offering and our financial statements and the related notes appearing elsewhere in this prospectus. You should carefully consider, among other things, the matters discussed in the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus before deciding to invest in our common stock. Some of the statements in this prospectus constitute forward-looking statements. See “Forward-Looking Statements.”

We are a newly formed Delaware corporation that has not, to date, conducted any activities other than those incident to our formation and the preparation of this registration statement. We were formed solely for the purpose of reorganizing the organizational structure of Language Line Holdings LLC, our parent, in order for the registrant to be a corporation rather than a limited liability company. Our predecessor is Language Line Holdings LLC. Except where the context otherwise requires or where otherwise indicated, prior to the Reorganization, as defined below, the terms “Language Line,” “we,” “us,” “our,” “our company,” “the Company” and “our business” refer to our predecessor and after the Reorganization, these terms refer to Language Line Services Holdings, Inc. and its consolidated subsidiaries as a combined entity. Certain differences in the numbers in the tables and text throughout this prospectus may exist due to rounding.

Our Company

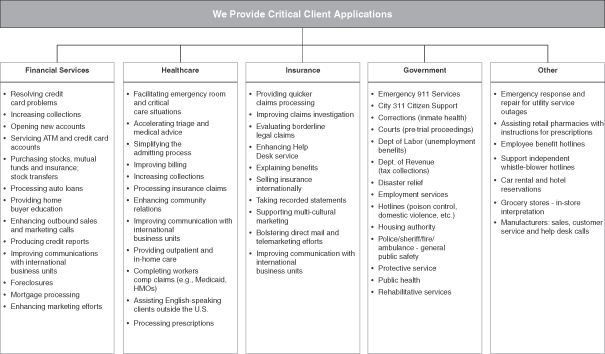

We believe we are a global leader in providing on-demand language interpretation services. Supporting over 170 languages, we provide our interpretation services to businesses, government and other public sector clients primarily via telephone interpretation. We also provide video and in-person interpretation services. Within seconds of receiving an inbound call, 24 hours a day and seven days a week, we provide our clients with an over-the-phone interpreter with the appropriate language and topic-specific skill set who can help facilitate a conversation between our client and our client’s limited English proficiency, which we refer to as LEP, customers. In 2008, we helped more than 35 million people communicate across linguistic barriers by providing over-the-phone interpretation, which we refer to as OPI, services to our clients. We focus on high-value interactions that require immediate availability of our multi-lingual resources, including emergency rooms or 911 calls, or flexible, customized interpretation services to businesses, such as mortgage or insurance claims processing. Our interpretation services enable our clients to increase their revenue and deliver mission-critical services to their customers, thereby improving their customer loyalty. We also help clients comply with applicable laws and regulations by providing in-language support to our clients’ growing population of current and prospective LEP customers in the growing and largely underserved LEP marketplace.

We offer a wide range of language interpretation services across a diverse group of industry verticals, including healthcare, government, financial services, insurance, telecommunications and utilities. We have over 10,000 clients, including approximately 60% of the Fortune 500 companies and all of the top 20 emergency 911 response centers in the U.S. For the nine months ended September 30, 2009, our largest client represented less than 5% of revenue and our largest vertical market, healthcare, represented less than 30% of revenue. Our diverse industry focus and delivery of revenue-enhancing and mission-critical services have driven increased demand and interpreter minutes growth even in challenging economic times. For example, throughout the current recessionary environment, we have provided interpretation services for calls related to mortgage foreclosure, helping our clients’ customers understand terms or negotiate payments. These applications complement our financial services clients’ traditional use of our services, which include resolving credit card problems, increasing collections, opening new accounts, providing home buyer education and producing credit reports. Our insurance

1

Table of Contents

industry clients use our services to process claims, improve claim investigations, evaluate questionable claims, enhance help desk service and explain benefits. We assist healthcare clients by facilitating emergency room and critical care situations, accelerating triage and medical advice, simplifying patient admission processes, improving billing and increasing collections. We also support emergency 911 services, disaster relief, citizen support 311 services and other services for governments and municipalities.

We leverage our industry-leading operating scale, interpreter workforce and proprietary technology to deliver to our clients a high quality, cost-effective, on-demand alternative to staffing in-house multilingual employees or utilizing face-to-face interpretation services, which we refer to as FFI. Our clients rely on the quality, accuracy and professionalism of our highly skilled interpreters who facilitated over 21 million calls in 2008, helping people communicate across linguistic barriers. Our low-cost delivery model and focus on operating efficiency has enabled us to be competitive in the pricing of our services, while maintaining strong profitability levels. Given the strong secular trends for our services and the uniquely low capital requirements of our business model, we have consistently grown our business and delivered strong free cash flow. We have grown our revenue to $278.2 million in 2008 from $185.3 million in 2006, representing a compounded annual growth rate, which we refer to as CAGR, of 22.5%. Our income from operations for 2008 was $70.3 million, and from 2006 to 2008 our ratio of annual capital expenditure to revenue has averaged 1.7%.

Our compelling value proposition in providing high quality language services of a mission-critical nature has contributed to our client retention and recurring revenue. Many of our clients are required or mandated by law and regulation to service their customers in the customers’ native language. Our client churn in the United States (as measured by lost minutes) was less than 5% in 2008, and 90% of our 250 largest U.S. clients in 2008 have been procuring our services for over five years. The majority of our revenue is generated from long-term subscriptions from corporate clients who are charged on a “pay for use” basis that optimizes a client’s outsourcing costs relative to less efficient and capital intensive in-house solutions. Our clients incur minimal start-up costs and can transition to our on-demand interpretation services solution within days of selecting us as a vendor.

Over our 27-year history, we have established the world’s largest language interpretation workforce consisting of over 4,000 well-trained, dedicated interpreters who deliver quality, accurate and professional interpretation services on a 24/7 basis. Our delivery model is scalable and requires low capital investment to maintain and grow, as the majority of our interpreters work from home in the United States, supplemented by interpreters located in six domestic and international interpretation centers. This model enables our cost structure to be variable, optimizing interpreter availability with fluctuations in demand across multiple languages and skill sets without the fixed cost burden of facilities-based agent models.

We continually invest in our proprietary technology platforms to provide operating leverage in our outsourcing model and to sustain high barriers to competitive entry. Our scalable call-routing and interpreter scheduling technologies augment our ability to offer superior service at a lower cost than our competitors. Our call routing technology, Telephone Interpretation Technology and Networking, which we refer to as TITAN, handles thousands of calls simultaneously and, within seconds, sources our highest quality, lowest cost available interpreters with an optimized interpretive skill set, whether they are working at home or in one of our global interpretation centers. Additionally, we developed a fully integrated interpreter scheduling system to forecast and optimize interpreter utilization across multiple languages and skill sets based on a proprietary 10-year call history database.

Our Market Opportunity

The language services market represents a large and rapidly growing market opportunity. According to Common Sense Advisory, Inc., Norbridge, Inc. and management estimates, the language services market in the United States was estimated at approximately $12.1 billion in 2007 and is expected to grow 14.6% annually,

2

Table of Contents

reaching $24.0 billion by 2012. We primarily participate in the $3.4 billion “spoken word” language services sector, which is comprised of the $1.6 billion OPI market and the $1.8 billion FFI market, both of which have grown at an annual rate of approximately 10% since 2007.

We believe that growth in the language services market will be driven primarily by a number of macro trends including growth in the immigrant population, regulatory and public policy initiatives, an increasing focus on ethnic marketing and continued outsourcing of language services. Immigration in the U.S. has reached record high levels in recent years, and population growth is occurring fastest in geographies including California, Arizona and Florida, where a significant percentage of families do not speak English as a primary language. In addition, legislation is being enacted on a federal and statewide basis that encourages, and in some cases mandates, serving LEP populations in their native language, including Title VI of the Civil Rights Act of 1964. Additionally, ethnic marketing needs have increased as LEP households’ buying power has grown significantly, and corporations look to gain customers within these populations. Finally, we expect continued outsourcing of language-based services and believe it will be a significant growth driver; today we estimate that less than 25% of the OPI market opportunity is currently outsourced to third-party providers such as Language Line.

Immigrant Population

Immigrants comprise a significant portion of the U.S. population and are expected to continue to grow as a percentage of the overall population. According to the Pew Research Center, the population of the United States will rise from 296 million people in 2005 to 438 million people in 2050. Of this expected growth, approximately 82% or 117 million people will be from immigrants arriving from 2005 to 2050 and their U.S.-born descendants. As a result, nearly one in five Americans will be an immigrant in 2050, compared with one in eight in 2005. Additionally, the Hispanic population, which is already the largest minority group in the United States, will triple in size and make up 29% of the U.S. population by 2050, compared with 14% in 2005. We expect the growth in the immigrant population to drive an increase in LEP speakers, the primary users of language services, as evidenced by the U.S. Census Bureau’s 2000 Census that concluded that 83% of immigrants in 2000 spoke a language other than English at home.

Public Policy

Legislation at the national and local levels frequently mandates public services for LEP populations in their native language. For example, an executive order pursuant to Title VI of the Civil Rights Act of 1964 requires that healthcare, government agencies and social services have language interpretation services available for non-English speakers in order to receive government funding. On August 11, 2000, President Clinton signed Executive Order 13166, “Improving Access to Services for Persons with Limited English Proficiency,” which required Federal agencies to examine the services they provide, identify any need for services to those with limited English proficiency and develop and implement a system to provide those services so LEP persons can have meaningful access to them. This Executive Order also requires that Federal agencies work to ensure that recipients of Federal financial assistance provide meaningful access to their LEP applicants and beneficiaries. These public policy initiatives are also occurring at the state and local level. For example, in January 2009, legislation went into effect in California that requires health insurers to provide LEP customers with access to translated documents and language assistance when seeking any form of medical care. Similar public policy initiatives supporting the need for interpretation related services are in effect in other English-speaking countries, including the Human Rights Charter in the United Kingdom and the Canadian Charter of Rights and Freedoms.

Ethnic Marketing in the United States

Ethnic segments, especially Asians and Hispanics, continue to have a growing impact on the U.S. economy. For instance, according to the Selig Center for Economic Growth, Asian buying power has increased almost

3

Table of Contents

five-fold from $116 billion in 1990 to $509 billion in 2008, and Hispanic buying power has grown 349% from $212 billion in 1990 to $951 billion in 2008. According to a study published by K&L Advertising, LEP customers are nearly four times more likely to purchase products and services from companies that communicate with them in their native language. While the combined buying power for the Hispanic and Asian population is greater than $1.0 trillion today, a significant number of Hispanic and Asian households are “linguistically isolated,” making native language based interaction vital for client acquisition and retention. For example, according to First Data Corporation, in 2007 53% of the Mexican immigrant population in the United States does not have a checking account or is “un-banked,” compared with 17% of the U.S. born population. Additionally, according to Pew Hispanic Center and LIMRA International in 2006, among the Hispanic population, home ownership was approximately 49% compared with approximately 68% for the population as a whole, and only 36% of households have life insurance compared with 54% for the population as a whole. We believe that demand for OPI and other language services will continue to grow as companies focus on ethnic marketing opportunities as a way to grow revenue, increase market share and build profitable client relationships in populations that are largely under-served today.

Our Business Model

A majority of our revenue is generated from subscribed interpretation, which is designed for clients with frequent interpretation needs. Usage for the majority of clients is billed in one-minute increments. Price per billed minute is typically based on the language requested and time of day, subject to discounts related to billed minute volume pricing arrangements with certain clients.

Our top 10 languages accounted for over 91% of our billed minutes in 2008; Spanish language accounted for approximately 70% of our billed minutes in 2008, which is consistent with historical percentages. We provide a number of complementary services that allow us to offer a full service language solution to our clients. Included among those services are FFI, document translation, video interpretation services, which we refer to as VIS, and American Sign Language.

Our Competitive Strengths

We believe we have established ourselves as the market leader for OPI services as a result of significant investments in technology and network infrastructure, the breadth of languages we offer, the quality of our interpreters, our significant cost advantage and our consistent and reliable performance. In-house interpretation, performed either by bilingual call center agents or face-to-face agents, presents our largest form of competition; however, in-house interpretation services generally offer fewer languages, reduced on-demand interpreter availability, slower call handling times and higher cost of service. Additionally, while there are some technology solutions offered at lower price points with high availability, such as web self-service, Interactive Voice Recognition, which we refer to as IVR, and machine translation, these options offer fewer language capabilities, have limited flexibility and cannot provide interpretation for critical situations.

Additionally, we have targeted the FFI market both as a growth opportunity and a vehicle to enhance client retention and new client acquisition. A key strategy of our service offering is to migrate a portion of client FFI sessions to a more efficient and cost-effective OPI service. We intend to leverage our global interpreter network, technology platform and strong market position to expand our presence in the FFI market over time.

Our global presence, scalable operating platform, proprietary technology, highly skilled interpreter workforce and low-cost services delivery model create a unique client value proposition, and we believe these factors have established our company as a leading provider of on-demand interpretation services.

4

Table of Contents

Industry-leading operating scale and global interpreter workforce

We believe we are the largest independent provider of OPI services globally. We offer high quality and accurate interpretation services to over 10,000 clients in the U.S., Canada and the U.K. through our over 4,000 skilled and professionally trained interpreters. We successfully connect our clients with interpreters on a 24/7 basis offering over 170 different languages in less than twenty seconds over 99.5% of the time. We believe our scale affords us the ability to deliver a greater breadth of services at a significantly lower cost than our competitors.

Attractive value proposition leading to long-term, recurring client relationships

We have a differentiated service offering that includes on-demand interpreter availability on a 24/7 basis, customized interpretation solutions and a pay-for-use client pricing model. Demand for our services continues to grow through economic cycles due to the mission-critical nature of our services, our diverse client base and the multitude of the language service applications we provide. The majority of our client revenue is generated from subscribed interpretation, which is designed for clients with frequent interpretation needs. The stability and predictability of our revenue is attributable to the diversified client base and to our proven ability to retain a large percentage of our clients. Our client churn in the United States (as measured by lost minutes) was less than 5% in 2008, and 90% of our 250 largest U.S. clients in 2008 have been procuring our services for over five years.

Innovative interpreter workforce recruiting, training and monitoring

We believe the quality of our interpreter services is among the best in the industry, driven by our rigorous and industry-recognized interpreter recruiting, training, certification and retention programs. By using predominantly dedicated employee interpreters, unlike our competitors who largely utilize independent contractor interpreters, we are able to achieve a higher degree of control over the training and management of our interpreters and can better ensure the quality of the interpretation service. In our front-end recruiting process, only one out of every 12 applicants is selected. Our screening and recruiting process ensures high quality interpreters since skills in language, inter-cultural communication and customer service are monitored by our dedicated Quality Assurance department. Once hired, all employee interpreters undergo training on ethical standards, client requirements, interpretation and customer service. Additionally, the interpreters participate in industry-specific training programs developed in collaboration with industry experts, such as Medical Interpreting Training, Insurance Interpreter Training, Finance Interpreter Training, 911 Interpreter Training and Legal and Court Interpreting Training. Our specialized interpreter certification program is a significant competitive differentiator and value-added service. As of September 30, 2009, approximately 50% of our interpreters have been awarded or are pending certification under the Federal Government Security Requirements issued by the U.S. Department of Homeland Security and approximately 8% have certifications in medical interpretation. We meet and exceed the rigorous American Society for Testing and Materials standards for interpreter quality and training.

Proprietary call handling and skills-based routing technology platforms

We continually invest in our proprietary and patented technology platforms to maintain the best service metrics in the OPI industry, to provide operating leverage in our on-demand outsourcing model and to sustain high barriers to entry. Our patented and scalable call-routing technology, TITAN, helps drive continued client loyalty through skills-based call routing and fast connect times. TITAN enables us to efficiently handle thousands of simultaneous calls, allowing us to quickly connect our interpreters to our clients and ensure a high-quality client experience. For the nine months ended September 30, 2009, our average answer time was 0.4 seconds, and our interpreter connect time was less than 20 seconds, with Spanish, our most popular

5

Table of Contents

language, connecting at an average of less than 15 seconds. Some of our clients, for example, include 911 emergency response centers and hospitals, for which high-quality language services with fast connect times are often critical. Depending on the type of service required, calls are routed on a skills-basis to interpreters who are able to interpret general and customer service calls as well as more specialized interpreters trained by industry experts in the fields of healthcare, insurance and financial terminology, as well as emergency and 911 procedures. Our TITAN system is further supported by a state-of-the-art telecom infrastructure that provides increased reliability and business continuity.

Operational excellence and focus on low-cost delivery of services

Our focus on operational excellence and globally deployed best operating practices assures that we can deliver a consistent, scalable and high-quality interpretation experience to our clients and our clients’ customers from any of our interpreters working from home and from our six interpretation centers located in domestic and international locations. Our scale, coupled with our call delivery technology, helps drive down our unit costs, which is important to delivering our value proposition. Our delivery system includes an efficient interpreter sourcing strategy balancing interpreter location and skills mix, continuous improvement in interpreter productivity and scalability as our business grows. Our proprietary database of call arrival patterns, combined with our fully integrated scheduling program maximizes the efficiency and utilization of our global interpreter workforce and optimizes our fixed cost base. This system continually synthesizes over ten years of historical call volume data in rolling 15-minute increments and analyzes patterns of total call volume, language usage, industry distribution and client distribution to optimize the time our interpreters are occupied. Our interpreter productivity (defined as the number of revenue-generating interpreted minutes compared with the number of minutes paid to interpreters), for example, improved by 55% between 1999 and 2008. Our ability to maximize the productivity of an interpreter during each working hour as well as the competitive salaries we can afford to pay to attract talented interpreters are significant competitive differentiators in terms of profitability and operating leverage.

Proven, experienced management team

We have a proven, experienced management team that has been instrumental in establishing and expanding our industry leadership position. Combined, management has over 50 years of experience with us. Management has instituted a number of initiatives to position us for growth; management has (i) aggressively managed and invested in our sales and marketing function in order to drive same-client revenue growth and revenues from new client acquisitions; (ii) developed and invested in patented technologies in order to introduce new language service offerings and improve operating efficiency; (iii) implemented process improvements to increase our operating efficiency and profitability; and (iv) successfully integrated multiple acquisitions, one of which expanded our presence into the U.K. Management has grown our revenue to $278.2 million in 2008 from $185.3 million in 2006, representing a CAGR of 22.5%.

Our Growth Strategies

We expect our future growth to be driven by the continued secular growth of the overall language services market; however, we have also undertaken several key strategic initiatives intended to outpace market growth, including:

Further penetration of our existing client base

We believe less than 25% of the OPI market opportunity today has been outsourced to third-party OPI providers such as Language Line. We offer a wide range of OPI applications for over 10,000 clients across a number of diverse industry verticals, including healthcare, government, financial services, insurance, telecommunications and utilities. We have a strong track record of extending the scope of these client

6

Table of Contents

relationships over time by selling other proven industry applications. As an example, one national property and casualty insurance company grew the number of LEP calls serviced from 628 since becoming a client in 1990, to 140,000 calls in 2008. This client began using us for auto and homeowner claims and has extended its use of our services over time to include customer service centers and its sales agent network. We leverage our industry specific expertise and partner with our clients to identify additional areas of need for interpretation to expand our services. As a result, we have compiled a detailed database of our existing clients’ in-house OPI operations, which enables us to be highly-targeted, effective and efficient in our sales efforts. From 2006 to 2008, revenue from current U.S. clients as of December 31, 2008 (excluding clients gained through acquisitions) grew approximately 14% annually on a compounded basis.

Acquisition of new clients

We aim to develop new client relationships and further diversify our client base by targeting clients and industry verticals that exhibit a demonstrated need for language interpretation services. For example, we estimate penetration in the insurance, healthcare, utilities and telecommunications industries was approximately 33%, 20%, 19% and 12%, respectively, of the available interpretation minute opportunity in 2007. We believe that our unique service offerings, breadth of language capabilities, interpreter quality, technology and call-routing infrastructure and industry-specific knowledge position us to attract new clients. We have been successful acquiring new clients in the past. New U.S. clients acquired since 2006 represented approximately 12% of our revenue in 2008.

Expand addressable market opportunities with new products and services, including face-to-face interpretation

By providing a comprehensive language services offering, we intend to further enhance client retention, pursue new clients and create incremental profit margin contribution. For example, we have only recently begun to penetrate the large and fragmented FFI market, which represents an opportunity for us to accelerate our growth and achieve profitable incremental scale. We plan to launch these services in selected geographic markets, supplementing our traditional OPI services with FFI. Other targeted complementary services include document translation and Language Line University, our service to test, train and certify interpreters that may work for us or directly for our customers.

Pursue international expansion opportunities

We have expanded our service offering into the U.K. and Canada by deploying our sales force in those countries and also by acquiring what we believe was the leading OPI provider in the U.K. We believe there is further opportunity to grow our business in these countries. According to Norbridge, Inc., in 2006 there were approximately 7.6 million LEP speakers in the U.K. and approximately 3.5 million in Canada, and both countries encourage, and in a growing number of cases mandate, companies to serve its customers in their native language. Given our limited penetration of these markets and the potential market opportunity, we believe further growth opportunities exist to expand our client base outside of the United States.

Pursue accretive bolt-on acquisitions

Although we have significant market share of the outsourced OPI market in the United States, the remaining domestic and international markets are highly fragmented. Given the scale in our operating platform, we have historically made successful accretive bolt-on acquisitions. We have a demonstrated track record of successful execution and integration of our past acquisitions, including OnLine Interpreters, Language Line Limited in the U.K. and TeleInterpreters, over the last seven years.

7

Table of Contents

Our Principal Stockholder

Following the completion of this offering, ABRY Partners, LLC, which we refer to as ABRY Partners, through its affiliated funds, will beneficially own approximately % of our outstanding common stock, or % if the underwriters’ over-allotment option is fully exercised. This ownership of our shares by ABRY Partners and its affiliated funds will result in its ability to have a majority vote over fundamental and significant corporate matters and transactions. See “Risk Factors—Risks Related to this Offering and Ownership of Our Common Stock.”

Founded in 1989, ABRY Partners is a leading media, communications and information services-focused private equity investment firm. ABRY Partners invests in high quality companies and partners with management to help build their businesses. Since its founding, ABRY Partners has completed over $21.0 billion of transactions, including private equity, mezzanine and preferred equity placements, representing investments in approximately 450 businesses. ABRY Partners is headquartered in Boston, Massachusetts.

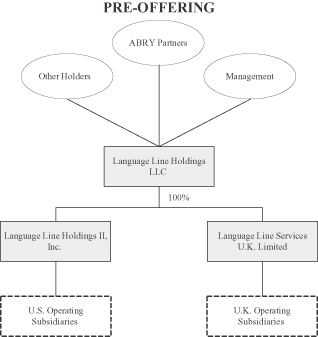

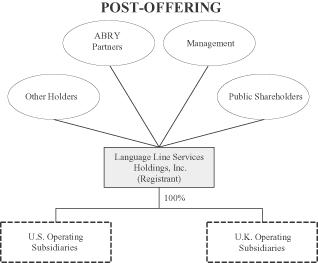

Our Corporate Structure

LL Services Inc. was incorporated in Delaware in November 2009. We are a newly formed Delaware corporation that has not, to date, conducted any activities other than those incident to our formation and the preparation of this registration statement. Prior to completion of this offering, we will be renamed Language Line Services Holdings, Inc. We are a wholly-owned subsidiary of Language Line Holdings LLC. Prior to completion of this offering, Language Line Holdings LLC, our parent, will contribute all of its ownership interest in Language Line Holdings II, Inc., our principal U.S. operating subsidiary, and Language Line Services U.K. Limited, our principal foreign operating subsidiary, to us, which will make each of Language Line Holdings II, Inc. and Language Line Services U.K. Limited wholly-owned subsidiaries of ours. In exchange for that contribution, we will issue shares of our common stock to Language Line Holdings LLC. We refer to these transactions as the Reorganization. At September 30, 2009, funds affiliated with ABRY Partners and our management and directors had ownership interests in Language Line Holdings LLC of approximately % and %, respectively.

After the completion of this offering, Class A common units, which we refer to as Class A units, mandatorily redeemable Class D common units, which we refer to as Class D units, and any vested and unvested Class C restricted common units, which we refer to as Class C-1, C-2, C-3, C-4, C-5 and C-6 units or, collectively, Class C units, of Language Line Holdings LLC will be exchanged for cash and shares of our common stock valued at $ based upon the price to public set forth on the cover page of this prospectus. The number of shares of our common stock issued in connection with the Reorganization will not be adjusted based on the actual initial offering price of our common stock, although the allocation of shares among the current unitholders of Language Line Holdings LLC may change. We refer to these transactions as the Exchange. Language Line Holdings LLC will dissolve after the Exchange. Upon completion of this offering, we intend to issue shares of restricted stock and stock options to exercise shares of common stock to our directors and director nominees and certain other officers and key employees.

In November 2009, Language Line Holdings LLC, our parent, refinanced a large portion of our existing balance sheet debt with a $575.0 million senior secured credit agreement. Proceeds were used to refinance our existing senior secured credit facilities, mezzanine facility, mandatorily redeemable convertible Coto preferred units, which we refer to as Coto preferred units, 11 1/8% senior subordinated notes, which we refer to as the Senior Subordinated Notes and 14 1/8% senior discount notes, which we refer to as the Discount Notes. We refer to these transactions as the Refinancing.

8

Table of Contents

Corporate and Other Information

Our principal executive offices are located at One Lower Ragsdale Drive, Monterey, California 93940 and our telephone number is (877) 886-3885. Our corporate website address is www.languageline.com. We do not incorporate the information contained on, or accessible through, our corporate website into this prospectus, and you should not consider it part of this prospectus.

9

Table of Contents

THE OFFERING

| Common stock offered by us |

shares. |

Common stock offered by the selling

| stockholder |

shares. |

Common stock to be outstanding immediately

| after this offering |

shares. |

| Over-allotment option |

The selling stockholder has granted the underwriters an option to purchase up to an additional shares of common stock within 30 days of the date of this prospectus in order to cover over-allotments, if any. |

| Use of proceeds |

We estimate that the net proceeds to us from this offering, after deducting underwriting discounts and commissions and estimated offering expenses, will be approximately $ million, assuming the shares are offered at $ per share, the midpoint of the price range set forth on the cover page of this prospectus. If the underwriters’ over-allotment option to purchase additional shares is exercised, we do not expect to receive any additional proceeds. We will not receive any of the proceeds from the shares of common stock being sold by the selling stockholder. |

We intend to use the net proceeds we receive from this offering to (i) pay a dividend to Language Line Holdings LLC, our parent, which it will use to redeem in whole its mandatorily redeemable series A preferred units, which we refer to as series A preferred units, which amounts to approximately $ million, approximately $ million of which is owned by affiliates of ABRY Partners and approximately $ of which is owned by an affiliate of Merrill Lynch, Pierce, Fenner & Smith Incorporated, an underwriter of this offering, and (ii) approximately $ million to repay outstanding term loans pursuant to a credit agreement among Language Line Holdings II, Inc., one of our direct subsidiaries, and Citicorp USA, Inc., which we refer to as the Citi Loan, $ of which is to pay ABRY Partners a fee for guaranteeing the Citi Loan. See “Use of Proceeds,” “Certain Relationships and Related Party Transactions,” and “Description of Certain Indebtedness.”

| Dividend policy |

We have not historically declared or paid any dividends on our common stock. We cannot pay any dividends on our common stock until Language Line Holdings LLC, our parent, has redeemed and paid in full its series A preferred units. We intend to use a portion of the net proceeds we |

10

Table of Contents

| receive from this offering to pay a dividend to Language Line Holdings LLC, which it will use to redeem in whole its series A preferred units. Our ability to pay dividends on our common stock is also limited by the covenants of our senior secured credit agreement and may be further restricted by the terms of any of our future debt or preferred securities. See “Dividend Policy.” |

| Proposed symbol for trading on The NASDAQ Global Market |

“ ” |

| Directed share program |

At our request, the underwriters have reserved up to % of the shares of common stock offered hereby for sale at the initial public offering price to persons who are directors, officers or employees, or who are otherwise associated with us, through a directed share program. The sales will be made by Credit Suisse Securities (USA) LLC through a directed share program. We do not know if these persons will choose to purchase all or any portion of these reserved shares, but any purchases they do make will reduce the number of shares available to the general public. See “Underwriting.” |

| Conflicts of interest |

An affiliate of one of the underwriters is a holder of series A preferred units of Language Line Holdings LLC and will receive a portion of the net proceeds of this offering. See “Conflicts of Interest.” |

| Risk factors |

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 15 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

Unless otherwise indicated or context otherwise requires, all information contained in this prospectus:

| • | assumes no exercise of the underwriters’ option to purchase up to additional shares of common stock from the selling stockholder to cover over-allotments, if any; |

| • | assumes that the common stock to be sold in this offering is sold at $ , which is the midpoint of the range set forth on the cover page of this prospectus; and |

| • | gives effect to the Reorganization. |

Except as otherwise noted, the number of shares of our common stock stated in this prospectus to be outstanding after this offering excludes Class C units of Language Line Holdings LLC issued under its existing incentive unit agreements, which will be exchanged into shares of our common stock after this offering in connection with the Exchange, and shares of restricted stock and stock options to purchase shares of common stock reserved for issuance under our 2010 Omnibus Incentive Plan that we plan to adopt in connection with this offering.

11

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA

The following table sets forth our predecessor’s summary consolidated financial and other data for the periods and at the dates indicated. Our predecessor is Language Line Holdings LLC. The summary consolidated financial data for each of the years in the three-year period ended December 31, 2008 and as of December 31, 2008 have been derived from the audited consolidated financial statements included elsewhere in this prospectus. The historical financial data for the nine months ended September 30, 2008 and the nine months ended September 30, 2009 and as of September 30, 2009 have been derived from the unaudited condensed consolidated financial statements included elsewhere in this prospectus. The unaudited condensed consolidated financial statements have been prepared on the same basis as the audited consolidated financial statements and, in the opinion of our management, reflect all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of this data. The results for any interim period are not necessarily indicative of the results that may be expected for a full year.

The historical results presented below are not necessarily indicative of the results to be expected for any future period. This information should be read in conjunction with “Risk Factors,” “Selected Consolidated Financial and Other Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and the consolidated financial statements and the related notes included elsewhere in this prospectus.

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2006 | 2007 | 2008 | 2008 | 2009 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||

| Revenues |

$ | 185,340 | $ | 202,924 | $ | 278,174 | $ | 204,580 | $ | 227,474 | ||||||||||

| Cost of revenues (exclusive of items shown separately below) |

64,911 | 71,029 | 101,469 | 75,352 | 79,118 | |||||||||||||||

| Selling, general and administrative |

35,417 | 40,316 | 65,714 | 40,208 | 91,885 | |||||||||||||||

| Depreciation and amortization expense |

38,016 | 34,398 | 40,700 | 29,120 | 27,527 | |||||||||||||||

| Impairment of goodwill |

5,293 | 1,342 | — | — | — | |||||||||||||||

| Total operating costs and expenses |

143,637 | 147,085 | 207,883 | 144,680 | 198,530 | |||||||||||||||

| Income from operations |

41,703 | 55,839 | 70,291 | 59,900 | 28,944 | |||||||||||||||

| Interest expense |

79,377 | 76,612 | 76,783 | 58,781 | 60,433 | |||||||||||||||

| Interest and other income, net |

1,591 | 1,514 | 537 | 780 | 300 | |||||||||||||||

| Net income (loss) before income taxes |

(36,083 | ) | (19,259 | ) | (5,955 | ) | 1,899 | (31,189 | ) | |||||||||||

| Income tax (benefit) expense |

(2,517 | ) | 404 | 8,615 | 6,461 | 11,525 | ||||||||||||||

| Net loss before noncontrolling interest |

(33,566 | ) | (19,663 | ) | (14,570 | ) | (4,562 | ) | (42,714 | ) | ||||||||||

| Noncontrolling interest (preferred stock dividends of a subsidiary) |

— | — | 1,829 | 1,336 | 1,518 | |||||||||||||||

| Net loss |

$ | (33,566 | ) | $ | (19,663 | ) | $ | (16,399 | ) | $ | (5,898 | ) | $ | (44,232 | ) | |||||

12

Table of Contents

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||||

| 2006 | 2007 | 2008 | 2008 | 2009 | ||||||||||||||||||

| (in thousands, except per unit and per share data) | ||||||||||||||||||||||

| Net loss per Class A unit, basic and diluted |

$ | (0.25 | ) | $ | (0.14 | ) | $ | (0.11 | ) | $ | (0.04) | $ | (0.31 | ) | ||||||||

| Weighted average number of Class A units, basic and diluted |

132,364 | 139,707 | 139,707 | 139,707 | 139,707 | |||||||||||||||||

| Net loss per Class D unit, basic and diluted |

$ | (0.21 | ) | $ | (0.12 | ) | $ | (0.10 | ) | $ | (0.04 | ) | $ | (0.26 | ) | |||||||

| Weighted average number of Class D units, basic and diluted |

5,091 | 5,091 | 5,091 | 5,091 | 5,091 | |||||||||||||||||

| Pro forma net income (loss) per share of common stock, basic and diluted (1) |

$ | $ | ||||||||||||||||||||

| Pro forma weighted average shares outstanding, basic and diluted (1) |

||||||||||||||||||||||

| Other Financial Data: |

||||||||||||||||||||||

| Adjusted EBITDA (2) |

$ | 85,807 | $ | 91,908 | $ | 121,755 | $ | 89,092 | $ | 106,139 | ||||||||||||

| Other Non-Financial Data: |

||||||||||||||||||||||

| Billed minute growth |

24.8 | % | 17.5 | % | 42.8 | % | 39.8 | % | 17.4 | % | ||||||||||||

| ARPM decline |

(1.3 | %) | (7.1 | %) | (7.3 | %) | (7.0 | %) | (4.7 | %) | ||||||||||||

| As of September 30, 2009 | |||||||||

| As of December 31, 2008 |

Actual | As Adjusted(3)(4)(5) | |||||||

| (in thousands) | |||||||||

| Balance Sheet Data: |

|||||||||

| Cash and cash equivalents |

$ | 24,577 | $ | 68,495 | |||||

| Working capital |

39,027 | 101,353 | |||||||

| Total assets |

949,146 | 977,212 | |||||||

| Series A preferred units |

|

160,274 |

|

178,954 |

|

||||

| Total debt (6) |

557,796 | 548,144 | |||||||

| Total temporary equity |

|

25,529 |

|

39,567 |

|

||||

| Total members’/stockholders’ equity (deficit) |

26,853 | (30,377 | ) | ||||||

| (1) | For a description of the pro forma adjustments used to calculate pro forma net loss per share of common stock for the year ended December 31, 2008 and for the nine months ended September 30, 2009, refer to Note 1 “Pro forma earnings per share” to the notes to the consolidated financial statements included elsewhere in this prospectus. |

| (2) | We define Adjusted EBITDA as net loss before noncontrolling interest, interest expense and other income, net, income tax (benefit) expense, depreciation and amortization, impairment of goodwill, equity-based compensation expense and merger related expenses. We use Adjusted EBITDA to facilitate a comparison of our operating performance on a consistent basis from period to period that, when viewed in combination with our results under U.S. generally accepted accounting principles, which we refer to as GAAP, and the following reconciliation, we believe provides a more complete understanding of factors and trends affecting our business than GAAP measures alone. We believe Adjusted EBITDA assists our board of directors, management and investors in comparing our operating performance on a consistent basis because it removes the impact of our capital structure (such as interest expense and other income, net, and noncontrolling interest), asset base (such as depreciation and amortization) and items outside the control of our management team (such as income taxes), as well as other items which are non-cash (such as equity-based compensation expense and impairment of goodwill) and non-recurring items (such as merger related expenses), from our operations. Despite the importance of this measure in analyzing our business and evaluating our operating performance, Adjusted EBITDA has limitations as an analytical tool, and you should not consider it in isolation, or as a substitute for analysis of our results as reported under GAAP; nor is Adjusted EBITDA intended to be a measure of liquidity or free cash flow for our discretionary use. Some of the limitations of Adjusted EBITDA are: |

| • | Adjusted EBITDA does not reflect all of our cash expenditures or future requirements for capital expenditures or contractual commitments; |

13

Table of Contents

| • | Adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs; |

| • | Adjusted EBITDA does not reflect the interest expense or the cash requirements to service interest or principal payments under our senior secured credit agreement; |

| • | Adjusted EBITDA does not reflect income tax payments we are required to make; |

| • | Although equity-based compensation expense is a non-cash charge, Adjusted EBITDA does not reflect the cash requirements for vested units we elected to repurchase upon the cessation of employment during the years ended December 31, 2006, December 31, 2007, December 31, 2008 and nine months ended September 30, 2008 and September 30, 2009 totaling $42,000, $15,000, $26,000, $1,000 and $0, respectively; and |

| • | Although depreciation and amortization are non-cash charges, the assets being depreciated and amortized often will have to be replaced in the future, and Adjusted EBITDA does not reflect any cash requirements for such replacements. |

To properly and prudently evaluate our business, we encourage you to review the financial statements included elsewhere in this prospectus and not rely on any single financial measure to evaluate our business. We also strongly urge you to review the reconciliation of net loss before noncontrolling interest from continuing operations to Adjusted EBITDA. Adjusted EBITDA, as presented in this prospectus, may differ from and may not be comparable to similarly titled measures used by other companies because Adjusted EBITDA is not a measure of financial performance under GAAP and is susceptible to varying calculations. The following table sets forth a reconciliation of net loss before noncontrolling interest a comparable GAAP-based measure, to Adjusted EBITDA. All of the items included in the reconciliation from net loss before noncontrolling interest to Adjusted EBITDA are either (i) non-cash items (such as depreciation and amortization, equity-based compensation expense and impairment of goodwill), (ii) items that management does not consider in assessing our on going operating performance (such as income taxes and interest expense and other income, net) or (iii) non-recurring items (such as merger related expenses). In the case of the non-cash items, management believes that investors can better assess our comparative operating performance because the measures without such items are less susceptible to variances in actual performance resulting from depreciation, amortization and other non-cash charges and more reflective of other factors that affect operating performance. In the case of the other items, management believes that investors can better assess our operating performance if the measures are presented without these items because their financial impact does not reflect ongoing operating performance.

The following is a reconciliation of net loss before noncontrolling interest to Adjusted EBITDA for the periods presented.

| Year Ended December 31, | Nine Months Ended September 30, |

|||||||||||||||||||

| 2006 | 2007 | 2008 | 2008 | 2009 | ||||||||||||||||

| (in thousands) | ||||||||||||||||||||

| Net loss before noncontrolling interest |

$ | (33,566 | ) | $ | (19,663 | ) | $ | (14,570 | ) | $ | (4,562 | ) | $ | (42,714 | ) | |||||

| Interest expense and other income, net |

77,786 | 75,098 | 76,246 | 58,001 | 60,133 | |||||||||||||||

| Income tax (benefit) expense |

(2,517 | ) | 404 | 8,615 | 6,461 | 11,525 | ||||||||||||||

| Depreciation and amortization |

38,016 | 34,398 | 40,700 | 29,120 | 27,527 | |||||||||||||||

| Impairment of goodwill |

5,293 | 1,342 | — | — | — | |||||||||||||||

| Equity-based compensation |

— | 329 | 10,398 | 72 | 49,668 | |||||||||||||||

| Merger related expenses |

795 | — | 366 | — | — | |||||||||||||||

| Adjusted EBITDA |

$ | 85,807 | $ | 91,908 | $ | 121,755 | $ | 89,092 | $ | 106,139 | ||||||||||

| (3) | Reflects shares of common stock outstanding as of , 2009. |

| (4) | A $1.00 increase (decrease) in the assumed initial public offering price of $ per share, the midpoint of the price range set forth on the cover of this prospectus, would increase (decrease) each of cash and cash equivalents, total assets and total stockholders’ equity by approximately $ million, assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. Similarly, if we change the number of shares offered by us, the net proceeds we receive will increase or decrease by the increase or decrease in the number of shares sold, multiplied by the offering price per share, less the incremental estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

| (5) | The as adjusted column in the balance sheet data table above reflects the balance sheet data as further adjusted for (i) our receipt of the estimated net proceeds from the sale of shares of common stock offered by us at an assumed initial public offering price of $ per share, the midpoint of the price range set forth on the cover page of this prospectus, after deducting the estimated underwriting discount and estimated offering expenses payable by us; (ii) the payment of a dividend and repayment of outstanding indebtedness as described in “Use of Proceeds”; (iii) the Refinancing; and (iv) the Reorganization. See “Capitalization” and “Use of Proceeds.” |

| (6) | Total debt at December 31, 2008 includes long-term obligations, net of current portion of $533.4 million and current portion of long-term obligations of $18.6 million, and the related party loan of $5.8 million. Total debt at September 30, 2009 includes long-term obligations, net of current portion of $537.9 million and current portion of long-term obligations of $3.9 million, and the related party loan of $6.3 million. |

14

Table of Contents

This offering and an investment in our common stock involve a high degree of risk. You should consider carefully the risks described below, together with the financial and other information contained in this prospectus, before you decide to purchase shares of our common stock. If any of the following risks actually occurs, our business, financial condition, results of operations, cash flow and prospects could be materially and adversely affected. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business, financial condition, results of operations, cash flow and prospects. As a result, the trading price of our common stock could decline and you could lose all or part of your investment in our common stock.

Risks Related to Our Business

If we are unable to retain our existing clients, our business, financial condition and results of operations could suffer.

Our success depends substantially upon the retention of our clients. Historically, we have benefited from high client retention rates; however, we may not be able to maintain high client retention rates in the future. Although no single client accounted for more than 5% of our revenue in 2008, the loss of a large client may have an adverse effect on our business. Continued client retention depends on us improving efficiencies and cost-effectiveness in providing our language interpretation services and effectively complying with a complex array of regulatory requirements. We also may not be able to retain our clients if we do not fulfill their language interpretation services in a cost-effective manner, fail to provide accurate language interpretation services or otherwise fail to meet the service standards of our clients or if our proprietary call-routing software fails to perform properly. Many of our clients may look to perform their language interpretation services through the use of internal personnel rather than outsourcing the language interpretation services to us. The failure to maintain our existing clients may cause our revenue to decrease and our results from operations could suffer.

If we are unable to successfully implement and execute our business strategy, our business, financial condition and results of operations could be adversely affected.

The implementation and execution of our business strategy will place significant demands on our senior management and operational, financial and marketing resources. The successful implementation of our business strategy involves the following principal risks, which could adversely affect our business, financial condition and results of operations:

| • | the operation of our business may place significant or unachievable demands on our management team; |

| • | we may be unable to increase our penetration of the OPI market at an average revenue per billed minute of service which is acceptable to us; |

| • | we may be unable to continue to achieve cost reductions on a per billed minute basis consistent with our low-cost provider strategy; and |

| • | we may be unable to recruit a sufficient number of qualified interpreters. |

Our continued success depends on our clients’ trend toward outsourcing OPI services.

Our business depends on the continued need for outsourced OPI services as driven by general economic and public policy factors. These trends may not continue, as businesses and organizations may either elect to perform OPI services in-house or discontinue OPI services, both of which would have a negative effect on our revenues.

15

Table of Contents

Additionally, Spanish-English interpretation services accounted for the majority of our total OPI billed minutes in 2008 and the first nine months of 2009. A decision by our clients to conduct an increasing amount of OPI services in-house, especially for the rapidly growing Spanish-speaking community, could have an adverse effect on our business, financial condition and results of operations.

Our profitability may suffer as a result of competition in our markets.

Our interpretation services are subject to significant price competition. Our existing contracts with our clients generally are non-exclusive, terminable after a period of notice and have no requirement for a minimum amount of billed minutes. Our competitors offer services that are largely similar to ours, and we generally obtain our clients through a competitive bidding process, usually by responding to a request for proposal, in which a potential client may negotiate among multiple interpretation service providers. In addition, the cost incurred by our clients to switch or use multiple interpretation service providers is minimal. From time to time, we may need to reduce our prices or offer other concessions for some of our services to respond to competitive and client pressures and to maintain market share. These concessions include volume discounts, waiving fees and reduction in the prices we charge for our services. Such pressures also may restrict our ability to offset our costs to provide interpretation services. Any reduction in prices as a result of competitive pressures, or any failure to increase prices when our costs increase, would harm profit margins and, if our volume of billed minutes fails to grow sufficiently to offset any reduction in margins, our business, financial condition and results of operations may be adversely affected.

The OPI services market in which we compete is highly competitive and our failure to compete effectively could erode our market share.

Our failure to compete effectively in the outsourced OPI services market that we serve could erode our market share and negatively impact our ability to service our debt. We expect that our existing competitors will strive to improve their outsourced OPI services and introduce new services with competitive price and customer service characteristics. From time to time we may lose clients as a result of competition. Certain of our potential competitors may attempt to leverage their existing infrastructure to compete with us. For example, a large call center company may have the requisite scale to enter into the OPI services market. If this were to occur, the outsourced OPI industry may become more competitive and may force us to decrease our profit margins in order to maintain our market position.

We compete on a number of factors including, but not limited to, quality of interpreters, breadth of languages, connection speeds, reliability and price. We believe these service attributes are key considerations in the purchase decisions of our clients. If we are unsuccessful in competing on these factors, our business, financial condition and results of operations may be adversely affected.

Our average revenue per billed minute, which we refer to as ARPM, has been declining.

One of our responses to competition in our markets has been, from time to time, to lower the amount we charge to clients, and as such, our average rate per billed minute has declined over the past 5 years, and the first nine months of 2009 and is anticipated to decline in the future. This response encourages our clients to purchase more billed minutes but results in lower profitability. If we are unable to attract sufficient volume to offset lower per minute charges or if average revenue per billed minute decrease beyond our expectations, we may be unable to generate revenue growth or maintain current revenue levels in the future.

Client consolidations could result in a loss of clients or contract concessions that would adversely affect our operating results.

We serve clients in targeted industries that have historically experienced a significant level of consolidation. If one of our clients is acquired by another company, including one of our existing clients, provisions in certain

16

Table of Contents

contracts allow these clients to cancel or renegotiate their contracts, or to seek contract concessions. Such consolidations may result in the termination or phasing out of an existing client contract, volume discounts and other contract concessions that may adversely affect our business, financial condition and results of operations.

Our contracts generally provide for early termination, have no minimum level of billing requirement and often do not designate us as the exclusive provider of services, all of which may have an adverse effect on our operating results.

Most of our contracts do not ensure that we will generate a minimum level of revenue, and the profitability of each client program may fluctuate, sometimes significantly, throughout the various stages of a program. Our objective is to sign multi-year contracts with our clients. However, our contracts generally enable the clients to terminate the contract or reduce the volume of billed minutes. If our clients terminate or reduce demand for our services, our business, financial condition and results of operations may be adversely affected.

Our financial results depend on our interpreter productivity, in particular our ability to route calls and forecast our clients’ customer demand to make corresponding decisions regarding staffing levels, investments and operating expenses.

Our interpreter productivity has a substantial and direct effect on our profitability, and we may not achieve desired productivity levels or maintain our historically increasing level of productivity. Our productivity is affected by a number of factors, including:

| • | our ability to predict our clients’ customer demand for our services and thereby to make corresponding decisions regarding staffing levels, investments and other operating expenditures; |

| • | our effective utilization of technology and information, including our call-routing technology and our database of historical call volume data; |

| • | our ability to hire and assimilate new employees and manage employee turnover; and |

| • | our need to devote time and resources to training, professional development and other non-chargeable activities. |

Some of our contracts with our clients provide that we must meet certain performance criteria, including average connect times and interpreter availability thresholds. To meet these criteria, we use our proprietary call routing technology to connect our clients and our clients’ customers from any of our interpreters working from home and from our six interpretation centers located in domestic and international locations. Our continued success depends on our ability to meet these performance criteria by effectively routing calls and accurately forecasting our clients’ demand for interpretation services, and if our existing technology fails or becomes obsolete, our business, financial condition and results of operations may be adversely affected.

We may not be able to use intellectual property rights to protect our proprietary technologies, trademarks and other intellectual property.

We use proprietary technologies to competitively offer interpretation services. Our policy is to enter into confidentiality agreements with our employees, outside consultants, agency employees and independent contractors. We also use patent and trademarks, in addition to contractual restrictions, to protect our technology or other intellectual property. In spite of these legal protections, it may be possible for a third party to obtain and use our proprietary technology without authorization. Although we hold registered or pending United States

17

Table of Contents

patents and foreign patents covering certain aspects of our technology, we cannot assure you of the level of protection that these patents will provide. We may have to resort to litigation to enforce our intellectual property rights, to protect trade secrets or know-how, or to determine their scope, validity or enforceability. The laws of other countries may afford us little or no effective protection of our intellectual property rights. Enforcing or defending rights in our proprietary technology may be expensive, cause diversion of our resources and ultimately be unsuccessful. Our inability to prevent others from using our proprietary technologies or trademarks may reduce our competitiveness in offering interpretation services, which may adversely affect our business, financial condition and results of operations.

Unfavorable conditions in the U.S. and global economies may adversely affect demand for our services.

As demand for our services is sensitive to changes in the level of economic activity, our business may suffer during an economic downturn or recession. Our clients’ customers are sensitive to changes in economic conditions, and a reduction in demand for our clients’ products or services may result in a decrease in demand for our services. Slowing economic activity may also result in our clients canceling or delaying projects, or a reduction of the scope or breadth of services, including a reduction in the number of languages in which our clients provide products or services to their clients. If demand for our clients’ products or services decreases, then demand for our services may decrease, which may adversely affect our business, financial condition and results of operations.

More generally, the current unfavorable changes in global economic conditions, including recession, inflation, fluctuating energy costs, geopolitical issues, the availability and cost of credit, the U.S. mortgage market and a declining real estate market in the U.S., have contributed to increased volatility and diminished expectations for the global economy and expectations of slower global economic growth going forward. These factors, combined with volatile oil prices, declining business and consumer confidence and increased unemployment, have precipitated an economic slowdown. If the economic climate in the U.S. or abroad does not improve from its current condition or further deteriorates, our business and profitability may be negatively impacted. More specifically, our clients or potential clients may reduce their demand for our services, which may adversely impact our business, financial condition and results of operations.

Further reduction in the availability of credit on terms favorable to our clients may adversely affect the ability of our clients to obtain financing for their operations and could result in a decrease in demand for or cancellation of our services. There is no assurance that government responses to the disruptions in the financial markets will restore business and consumer confidence, stabilize the markets or increase liquidity and the availability of credit. In addition, during economic downturns, companies may slow the rate at which they pay their vendors or become unable to pay their debts as they become due. If our clients do not pay amounts owed to us in a timely manner or become unable to pay such amounts to us at a time when we have substantial amounts receivable from such client, reserves for doubtful accounts and write-offs of accounts receivable may increase, and in turn our cash flow and profitability may suffer.

Further, recent events, including the fallout from problems in the U.S. credit markets, indicate a moderate to severe recession in the U.S. and world economies, which could have an impact on our clients and the volume of business they are able to conduct with us and their ability to pay for services rendered. Additionally, the securities and credit markets have recently been experiencing volatility and disruption, which could impact our ability to access capital.

We cannot predict when global economic conditions will begin to recover or when and to what extent conditions affecting our clients will improve. Also, we cannot assure you that the actions we have taken or may take in the future in response to these global economic conditions will be successful or that our business, financial condition and results of operations will not be adversely impacted by these conditions.

18

Table of Contents

Our business could be adversely affected by a variety of factors related to doing business internationally.

We currently conduct operations internationally. Although our OPI services constitute generally accepted business practices in the United States, such practices may not be accepted in certain international markets. To the extent there is consumer, business or government resistance to the use of OPI services in international markets we target, our international growth prospects could be affected. In addition, our international operations are subject to numerous inherent challenges and risks, including the difficulties associated with operating in multilingual and multicultural environments, varying and potentially burdensome regulatory requirements, fluctuations in currency exchange rates, political and economic conditions in various jurisdictions, tariffs and other trade barriers, longer accounts receivable collection cycles, barriers to the repatriation of earnings and potentially adverse tax consequences. Moreover, expansion into new geographic regions will require considerable management and financial resources and, as a result, may negatively impact our business, financial condition and results of operations.

Pursuing and completing potential acquisitions could divert management attention and financial resources and may not produce the desired business results.