Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - AMERICAN ITALIAN PASTA CO | a2195602zex-23_1.htm |

| EX-32 - EX-32 - AMERICAN ITALIAN PASTA CO | a2195602zex-32.htm |

| EX-21 - EX-21 - AMERICAN ITALIAN PASTA CO | a2195602zex-21.htm |

| EX-23.2 - EX-23.2 - AMERICAN ITALIAN PASTA CO | a2195602zex-23_2.htm |

| EX-10.1 - EX-10.1 - AMERICAN ITALIAN PASTA CO | a2195602zex-10_1.htm |

| EX-31.2 - EX-31.2 - AMERICAN ITALIAN PASTA CO | a2195602zex-31_2.htm |

| EX-31.1 - EX-31.1 - AMERICAN ITALIAN PASTA CO | a2195602zex-31_1.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| (Mark one) | ||

| ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the fiscal year ended October 2, 2009 | ||

| OR | ||

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the transition period from to | ||

Commission file number 001-13403

AMERICAN ITALIAN PASTA COMPANY

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

84-1032638 (I.R.S. Employer Identification No.) |

|

4100 N. Mulberry Drive, Suite 200 Kansas City, Missouri (Address of principal executive offices) |

64116 (Zip Code) |

Registrant's telephone number, including area code: (816) 584-5000

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Name of Each Exchange on Which Registered | |

|---|---|---|

| Class A Convertible Common Stock: $.001 par value per share |

The NASDAQ Stock Market, LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "large accelerated filer", "accelerated finer", and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller Reporting Company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

As of April 3, 2009, the aggregate market value of the Registrant's Class A Convertible Common Stock held by non-affiliates (using the closing price) was approximately $676,000,000.

The number of shares outstanding as of November 12, 2009 of the Registrant's Class A Convertible Common Stock was 21,055,000 and there were no shares outstanding of the Registrant's Class B Convertible Common Stock.

DOCUMENTS INCORPORATED BY REFERENCE: Portions of the definitive Proxy Statement to be delivered to Stockholders in connection with the 2010 Annual Meeting of Stockholders are incorporated by reference in Part III.

AMERICAN ITALIAN PASTA COMPANY

FORM 10-K

FISCAL YEAR ENDED OCTOBER 2, 2009

INDEX

i

Cautionary Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K contains statements concerning potential future events. These forward-looking statements are based upon assumptions by our management, as of the date of this Annual Report on Form 10-K, including assumptions about risks and uncertainties faced by us. Readers can identify these forward-looking statements by the use of verbs such as expects, anticipates, believes, estimates, intends, projects, may, will, predicts, or similar verbs or conjugations of such verbs. If any of our assumptions prove incorrect or should unanticipated circumstances arise, our actual results could materially differ from those anticipated by such forward-looking statements. The differences could be caused by a number of factors or combination of factors including, but not limited to, those factors described below in Item 1A—Risk Factors. Readers are strongly encouraged to consider those factors when evaluating any such forward-looking statements. Except as otherwise required by the federal securities laws, we will not update any forward-looking statements in this Annual Report on Form 10-K to reflect future events or developments.

ii

General

American Italian Pasta Company is a Delaware corporation and was incorporated and commenced operations in 1988. Unless the context otherwise indicates, all references in this Annual Report on Form 10-K to "the Company", "we", "us", "our", and similar words are to American Italian Pasta Company and its subsidiaries. We believe we are the largest producer and marketer of dry pasta in North America, by volume, based on data available from The Nielsen Company ("Nielsen"), published competitor financial information, industry sources such as the National Pasta Association, suppliers, trade magazines and our own market research.

We report on a 52/53 week fiscal year end that generally consists of four thirteen week quarters that end on the Friday nearest the end of the quarter. Approximately every sixth year we report on a 53-week fiscal year that results in a fourteen week first quarter of that fiscal year. Fiscal year 2009, which ended on October 2, 2009, was a 53-week fiscal year. Fiscal years 2008 and 2007 were 52 weeks and ended on September 26, 2008 and September 28, 2007, respectively. There is no material seasonal impact on our operations. During the 53-week fiscal year ended October 2, 2009, we had revenues of $628.2 million.

We have production, milling, and distribution facilities located in Excelsior Springs, Missouri, Columbia, South Carolina, Tolleson, Arizona, and Verolanuova, Italy. We outsource distribution at all of our facilities and we outsource milling at the Arizona and Italy plants. Our U.S. plants serve both retail and institutional customers. We believe the construction of the Missouri plant in 1988 represented the first use in North America of a vertically integrated, high-capacity pasta plant using Italian milling and pasta production technology. Our South Carolina plant, which is also vertically integrated, commenced operations in 1995, and our Arizona plant commenced operations in 2003. Our Italian plant, which was constructed in 2001, serves primarily retail and institutional customers internationally and also serves retail and institutional customers in the United States.

Our executive offices are located at 4100 N. Mulberry Drive, Suite 200, Kansas City, Missouri 64116, and our telephone number is (816) 584-5000. Our website is located at http://www.aipc.com. Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and all amendments to those reports are made available on our website as soon as reasonably practical after these materials are electronically filed with or furnished to the Securities and Exchange Commission. Information contained in our website is not a part of this Annual Report on Form 10-K.

AIPC Way

We have developed the AIPC Way, which embodies our vision, mission, operational model, business approach, core capabilities and values. The components of the AIPC Way are as follows:

- •

- Vision—What we will achieve—To be, and to be seen as, the best developer of category solutions for

our customers in dry grocery.

- •

- Mission—What we will do—Focus on dry grocery categories where we can leverage our relationships

and capabilities, to develop private label, branded and ingredient solutions for our retail, foodservice and industrial customers and, by exceeding expectations, provide our customers and shareholders

with enhanced value.

- •

- Operating Model—How we plan and execute—Always operate with high ethical standards. Strategic planning. Business planning and performance management. Sales and operations planning. People evaluation and development.

1

- •

- Core Capabilities—What do we need to be great—Great people. Category leadership. Service

leadership. Speed to market. Operational excellence. Cross function collaboration. Strong customer relationships.

- •

- Values—What we believe—Integrity. Quality. Environmental sustainability. Empowerment and accountability. Passion to exceed.

Pasta Markets

North American sales represented approximately 93%, 92% and 93% of our total revenues during fiscal years 2009, 2008 and 2007, respectively. The remainder of our sales were primarily in Europe.

The North American retail pasta category in all its forms ("Mega Pasta") includes such categories as refrigerated pasta, frozen meals with pasta, canned non-soup pasta, and stove top meals. As measured by Nielsen, pasta sales for the Mega Pasta category were estimated to be approximately $6.9 billion in fiscal year 2009. Nielsen data does not include Wal-Mart Stores, Inc. ("Wal-Mart") or other mass merchants.

Our products are marketed in the dry pasta category, which is a component of Mega Pasta. We estimate category trends as reported by Nielsen based upon total U.S. grocery and mass merchants. According to these estimates, during the 52 week period ended September 26, 2009 (the date nearest our fiscal year end for which this information is available), the dry pasta market volume grew at a rate of approximately 4.5% as compared to the comparable prior 52 week period. With the economic downturn, more people are choosing to cook at home and are taking advantage of the many alternatives available with a versatile food such as dry pasta. Dry pasta offerings include traditional semolina pasta as well as alternative formulations such as whole-wheat, multi-grain, and omega-added. Consumption of traditional semolina pasta, which comprises approximately 90% of the pasta market when expressed as a percent of pounds consumed, increased 3.9% during the 52 weeks ending September 26, 2009. During the same period, consumption of alternative formulation pasta grew at a growth rate of 9.9%. In addition, across nearly every store product category, consumers have been taking advantage of lower priced private label alternatives to traditional branded label products. For the pasta category, during the 52 week period ending September 26, 2009, total volume brand growth was 2.2% and private label growth was 9.4%.

The pasta industry consists of two primary customer markets: (i) Retail, which includes grocery retailers, club stores, mass merchants, drug and discount stores that sell branded and private label pasta to consumers; and (ii) Institutional, which includes both food service distributors that supply restaurants, hotels, schools and hospitals, as well as food processors that use pasta as a food ingredient.

Customer Markets—Retail: Retail market revenues include the sales of our pasta products to customers who resell the pasta in retail channels, including traditional grocery retailers, club stores, mass merchants, drug and discount stores. Based on Nielsen, Wal-Mart, and other mass merchant data, we believe we are the leading producer of retail dry pasta in the U.S. Our retail revenues include the sale of both our proprietary brands and the sale of private label brands (or, as we refer to them, "customer brands"). Our strategy is to provide our retail partners with a full portfolio of pasta products, including proprietary brands, private label customer brands, authentic Italian imported products, and alternative formula products, all delivered within the highest quality standards and with exceptional customer service.

During fiscal year 2009, we implemented a strategy (developed in fourth quarter of 2008) of focusing on growing customer brands in the overall market and our proprietary brands in core markets where they are strongest. As a part of that strategy, we began to extract our proprietary branded products from those markets in which they were underperforming in anticipation of realigning our proprietary brand portfolio. Further, we expanded our customer brand offerings to include more

2

premium and healthy products and invested more resources in category management and in helping retailers increase customer brand sales and profit. As a result, during fiscal 2009 we experienced volume and revenue growth in our customer brands and focus proprietary brands, partly offset by the anticipated decrease in proprietary branded products' volume and revenue in those markets in which we extracted branded products.

Customer Markets—Institutional: The Institutional market includes both food service distributors that supply restaurants, hotels, schools and hospitals, as well as food processors that use pasta as a food ingredient.

Food service customers include businesses that sell products to restaurants, healthcare facilities, schools, hotels, industrial caterers, and multi-unit restaurant chains that procure directly. The food service market is highly fragmented and is served by numerous regional and local food distributors. During fiscal year 2009, the food service channel, including restaurants, has been challenged as a result of current macro-economic conditions.

The Institutional market also includes sales to food processors who use pasta as an ingredient in their food products such as frozen dinner entrees, side dishes, dry side dish mixes, canned soups, and single-serve meals. The consistency and quality of the color, starch release, texture, cooking consistency, and gluten and protein content of pasta produced for food processors is crucial to the success of their products. As a result, food processors have stringent specifications for these attributes. The size of the Institutional market is affected by the number of food processors that elect to produce pasta internally rather than outsourcing their production. Ingredient customers often specify the use of non-durum wheat classes for production, and our revenues for these products are typically based upon a pass-through of charges in raw material costs and certain other cost changes as price adjustments. Although our per unit margin remained stable during 2009, the average selling prices decreased due primarily to declines in the cost of non-durum wheat and these pass-through arrangements.

Products

Our product line is comprised of approximately 3,700 items or stock-keeping units ("SKUs"). In many instances, we produce pasta to our customers' unique specifications. We produce approximately 300 different shapes and sizes of pasta products in multiple package configurations, including bulk packages for institutional customers and individually-wrapped packages for retail consumers. The varied shapes and sizes include long goods such as spaghetti, linguine, fettuccine, angel hair and lasagna, and short goods such as elbow macaroni, mostaccioli, rigatoni, rotini, ziti and egg noodles. These products are manufactured for a variety of customers including those who purchase our products as branded offerings from retailers and for retailers who sell products we manufacture as customer brands.

Our products are produced to satisfy the specifications of our customers as well as our own product specifications. We conduct internal laboratory evaluations against competitive products on physical characteristics and cooking performance. Physical characteristics considered include color, speck count, shape and consistency. Cooking performance considerations include starch release, protein content, and texture. Our customers also perform competitive product comparisons on a regular basis.

Marketing and Distribution

We actively sell and market our domestic products through our sales employees and with the use of food brokers and distributors throughout the United States and Canada. Our senior management is directly involved in the selling process in all customer markets. Our sales and marketing strategy is to provide category leadership, quality product, a complete product offering, competitive pricing and superior customer service to attract new customers and to maintain and grow pasta sales to existing customers. We work with our customers to develop marketing and promotional programs specifically

3

tailored to stimulate pasta consumption in their trading area based upon the specific strategy and role for pasta.

We have established a significant market presence in North America by developing strategic customer relationships with food industry leaders that have substantial pasta requirements. We supply customer branded and proprietary branded pasta to many of the largest grocery retailers in the United States, including serving as the exclusive supplier of customer brand pasta to Wal-Mart. We are the largest pasta supplier to Sysco Corporation ("Sysco"), the nation's largest marketer and distributor of food service products. We also have developed supply relationships with leading food processors, which use our pasta as an ingredient in their food products.

Our Italian plant enables us to offer authentic Italian pasta products. This facility serves European, North American, and other international markets with proprietary branded, customer branded, ingredient and food service products.

We have demonstrated our commitment to customer service through the development of enhanced customer service programs. Examples of these programs include our implementation of an Efficient Customer Response ("ECR") model, which uses Electronic Data Interchange ("EDI") and vendor replenishment programs to assist key customers, and category management services for our customer branded and proprietary branded customers.

As part of our overall customer development strategy, we use our category management expertise to assist customers in optimizing category growth and profitability. Our category management expertise allows us to recommend SKU assortment and shelf space allocation to both customer branded and proprietary branded customers. Our representatives also assist food processors in incorporating our pasta as an ingredient in their customers' food products. We provide technical support to our institutional customers by making recommendations regarding the processing of pasta in their facilities. We believe that these value-added activities provide customers with a better appreciation and acceptance of our products.

Our primary distribution centers in North America are strategically located at our production facilities in Missouri, South Carolina and Arizona to serve the national market. Finished products are automatically conveyed via enclosed case conveying systems from the production facilities to the distribution centers for palletizing and storage until shipping. The combination of integrated facilities and multiple distribution centers enables us to realize distribution cost savings and provides lead-time, fill rate and inventory management advantages to our customers. The operation of the Missouri, South Carolina and Arizona distribution centers is outsourced under a long term agreement with Ozburn-Hessey Logistics, LLC ("OHL"), a firm specializing in warehouse and logistics management services.

Pasta Production

Pasta's primary ingredient is semolina, which is extracted from durum wheat through a milling process. Durum wheat is used primarily for pasta. Each variety of durum wheat has its own unique set of protein, gluten content, moisture, density, color and other attributes which affect the quality and other characteristics of the semolina. We select and blend different durum wheat varieties in order to meet customer semolina specifications. Other types of wheat, as specified by our customers, may be used for production of our ingredient business pasta.

Our ability to produce high-quality pasta generally begins with purchasing durum wheat directly from elevators, U.S. grower-owned cooperatives, and the Canadian Wheat Board among other sources. This purchasing method ensures that the extracted semolina meets our specifications. We have several sources for durum wheat and are not dependent on any one supplier or sourcing area. As a result, we believe that we have adequate sources of supply for durum wheat. We occasionally buy and sell semolina to balance our milling and production requirements.

4

Durum wheat is a closely traded cash crop whose market price fluctuates and for which there is not a futures market. Therefore, we are not able to hedge purchases. To a certain extent, we manage our durum wheat cost risk through advance purchase contracts for the physical delivery of durum wheat that are generally less than six months in duration. We seek to manage the balance of such risk through continued improvement in our efficiencies and pricing of our products. Competitive pressures may limit our ability to fully recover additional raw material costs.

Durum wheat is shipped by rail to our production facilities in Missouri and South Carolina under annually negotiated contracts or market tariff rates. We source durum wheat and have it converted to semolina and semolina/flour blends for our Tolleson, Arizona facility from an adjacent milling facility owned by Bay State Milling Company ("Bay State") under the terms of a long-term supply agreement. The agreement is for an initial 10-year term with renewal provisions thereafter. In the event of ownership changes or sustained under-performance, we have contractual rights to purchase the mill at a book value established at the start of the supply agreement less accumulated depreciation. We are obligated to purchase 80% of our annual Tolleson requirements for semolina from Bay State with an annual minimum of 50 million pounds. We have satisfied our minimum requirements and paid Bay State approximately $27.8 million in fiscal year 2009, $21.2 million in fiscal year 2008, and $13.8 million in fiscal year 2007.

In Italy, we purchase our semolina requirements from Italian mills to meet our specific quality and customer needs.

We generate and sell by-products from our milling operations in the form of flour and mill feed. Proceeds from the sale of by-products is recognized as a reduction of our cost of goods sold. These products compete in the marketplace with alternative products for feed usage and, therefore, fluctuate in price accordingly.

We purchase our packaging supplies, including poly-cellophane, paperboard cartons, boxes and totes from third parties. We believe we have adequate sources of packaging supplies. In addition, we rely on supply chain logistics and operations planning to optimize finished goods inventory, minimize the risk of obsolescence for finished goods and raw materials, maximize customer service, and achieve efficient factory utilization.

Our U.S. and Italian production facilities are inspected for sanitation and food safety each year by the American Institute of Baking ("AIB"), a United States baking, food processing and allied industries evaluation agency. Our plants consistently achieve the AIB Excellent/Superior ratings. Our U.S. and Italian plants are also inspected by the British Retail Consortium ("BRC"), one of the recognized European Food Safety Bodies, for compliance to the new Global Food Safety Initiative ("GFSI") requirements, as approved by the Grocery Manufacturers Association ("GMA"). Our plants have received "Grade A/B" Certification from the BRC. In addition, we maintain a comprehensive Hazard Analysis Critical Control Point ("HACCP") program in all of our plants that ensures adequate protection and controls of our food safety systems on a daily basis.

Our Italian plant is an ISO 9002 certified production facility and is certified organic by Consorzio Per Il Controllo Dei Prodotti Biologici (Consortium for the Control of Biological Production). In addition, our Tolleson, Arizona plant is certified organic by the Organic Crop Improvement Association International.

Trademarks

We hold a number of federally registered and common law trademarks, primarily related to our brands, which we consider to be of value and importance to our business. We have also registered other trademarks.

5

Dependence on Major Customers

Historically, a limited number of customers have accounted for a substantial portion of our revenues. During the fiscal years ended October 2, 2009, September 26, 2008 and September 28, 2007, sales to Wal-Mart accounted for approximately 25%, 22% and 23%, respectively, of our total revenue. We expect to continue to rely on a limited number of major customers for a substantial portion of our revenue.

We generally do not have long-term supply contracts with our customers, including Wal-Mart. Additionally, we are dependent upon our customers to sell our products and to assist us in promoting market acceptance of, and creating demand for, our products.

Competition

We operate in a highly competitive environment against numerous well-established national, regional and foreign companies, and many smaller companies. We compete in the procurement of raw materials, the development of new products and product lines, the improvement and expansion of previously introduced products and product lines, and the production, marketing and distribution of these products. Some of these companies with which we compete have longer operating histories, significantly greater brand recognition, or more financial or other resources. Our products compete with a broad range of food products, both in the retail and institutional customer markets. Competition in these markets generally is based on achieving advantages relating to distribution, product quality, pricing, packaging, advertising, promotion, customer service, and logistics capabilities.

Our direct competitors include Barilla (a large privately owned Italian diversified food company), New World Pasta Company owned by Ebro Puleva (a Spanish company), Dakota Growers Pasta Company, Philadelphia Macaroni Co. Inc., A. Zerega's Sons, Inc., and other foreign companies. For sales in Europe and other international markets, our Italian plant competes with Barilla and numerous European pasta producers.

Government Regulation; Environmental Matters

We are subject to various laws and regulations related to the operation of our production facilities, the production, packaging, labeling and marketing of our products and pollution control, including air emissions, which are administered by federal, state, and other governmental agencies. Our production facilities are subject to inspection by the U.S. Food and Drug Administration ("FDA") and the Occupational Safety and Health Administration, as well as various state agencies.

Our facilities are subject to air permitting regulations administered by the U.S. Environmental Protection Agency and/or authorized States under federal and/or state regulations implementing the federal Clean Air Act. Each of our facilities is currently operating under valid permits. Costs to renew these permits are immaterial.

Our facilities are subject to certain safety regulations including regulations issued pursuant to the U.S. Occupational Safety and Health Act. These regulations require us to comply with certain manufacturing safety standards to protect our employees from accidents. We believe that we are in compliance with all employee safety regulations.

Our facilities are also subject to annual reporting requirements under the Emergency Planning and Community Right-to-Know Act and its implementing regulations. No permit is required, but we do submit reports to federal and/or state regulators, local emergency planning organizations, and the local fire department with jurisdiction over the facilities quantifying all hazardous materials stored on our property that meet or exceed threshold quantities. Costs associated with this annual reporting are minimal.

6

The Comprehensive Environmental Response Compensation and Liability Act of 1980 ("CERCLA"), as amended, and other similar state laws require the cleanup of hazardous waste disposal sites. Parties that may be liable under CERCLA for the cleanup of a hazardous waste disposal site include the current property owner, the operator, owners and operators of the property at the time of a release of hazardous substances, the arranger of the disposal, and the transporter of hazardous substances. To date, we have not been notified by the U.S. Environmental Protection Agency, any state agency, or any other private party that we are considered responsible or potentially responsible for some aspect of the cleanup of any hazardous waste disposal site under CERCLA or any other similar state laws.

We received the Customs Trade Partnership Against Terrorism ("C-TPAT") certification from the United States Customs and Border Protection ("CBP") division of the Department of Homeland Security. C-TPAT was developed by the CBP after the September 11, 2001 terrorist attacks as a way to identify low risk importers and facilitate the efficient release of goods, even under heightened security conditions. To become a participant of C-TPAT, our security measures were reviewed and certified by CBP. As part of the C-TPAT certification and review process, CBP has reviewed the implementation of our security measures and, effective August 2009, we became Tier 2 C-TPAT Certified. C-TPAT certification includes certain benefits to participants and may help reduce the risk of significant delays in the importation of our product.

All imported pasta is subject to U.S. import regulations. Duties are assessed in accordance with the Harmonized Tariff Schedule of the United States.

Employees

As of October 2, 2009, we employed 675 full-time persons worldwide of whom 190 were selling and administrative employees and 485 were manufacturing employees. Our 620 U.S. employees were not represented by any labor unions. We have 55 Italian employees, 45 of whom were represented by a labor union. We consider our employee relations to be excellent.

7

You should carefully consider the risks described below, as well as the other information included or incorporated by reference in this Annual Report on Form 10-K, before investing in our common stock. If any of the following risks occur, our business, financial condition or operating results could be materially adversely affected. The risks described below are not the only risks we face. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also materially adversely effect our business, financial condition or operating results.

A change in our relationship with our major customers could adversely affect our revenues.

Historically, a limited number of customers have accounted for a substantial portion of our revenues. If our relationship with one or more of our major customers changes or ends, our sales could suffer, which could have a material adverse effect on our business, financial condition or results of operations. We expect that we will continue to rely on a limited number of major customers for a substantial portion of our revenues in the future. During the 2009, 2008, and 2007 fiscal years, sales to Wal-Mart accounted for approximately 25%, 22% and 23%, respectively. During the 2009, 2008, and 2007 fiscal years, sales to Sysco accounted for approximately 8%, 9% and 9%, respectively. Currently, we do not have long-term supply agreements with a substantial number of our customers, including Wal-Mart and Sysco.

Fluctuations in the cost of raw materials, energy, packaging materials or other items could adversely affect us.

The principal raw material for the bulk of our products is durum wheat. We generally procure durum from North Dakota, Montana, Canada, and the southwest section of the U.S. for our Missouri and South Carolina plants, and we generally procure durum from the southwest section of the U.S. for our Arizona plant. The cost of durum wheat represents a substantial portion of our total cost of goods sold and changes in the supply of durum wheat could have a material adverse effect on our operating profit and margins. As durum wheat is used almost exclusively in pasta production and is a narrowly traded, cash-only commodity crop, we have limited means to protect ourselves from price fluctuations. Durum prices have been volatile and may continue to be volatile in the future.

The supply and price of durum wheat in North America and on a global scale is subject to market conditions and is influenced by several factors beyond our control, including:

- •

- general economic conditions;

- •

- global supply and demand (including acres planted and harvest quality and quantity);

- •

- natural disasters, insects, plant diseases, and weather conditions;

- •

- competition for raw materials from other users of durum wheat;

- •

- trade relations;

- •

- governmental programs and regulations;

- •

- natural gas costs, as natural gas is the primary component of anhydrous ammonia fertilizer used in the production of durum

wheat; and

- •

- transportation and fuel costs.

We rely on the supply of flexible film, folding cartons and other packaging materials, which represent a significant portion of our cost of goods sold, that fluctuate in price due to market conditions beyond our control.

We rely on rail carriers for transportation of durum wheat to our milling facilities, and ocean and truck freight for movement of our finished goods. Fuel costs have been and may continue to be

8

volatile. Increases in fuel costs would likely result in increased transportation costs and could have a material adverse effect on our business, financial condition or results of operations.

Historically, changes in sale prices of our pasta products have lagged changes in our materials costs. Furthermore, if the cost of raw materials, energy, packaging materials or other items increase, competitive pressures may limit our ability to raise prices or affect the timing or magnitude of such price increases. Conversely, if the cost of raw materials, energy, packaging materials or other items decrease, competitive pressures may cause us to lower prices before we have fully utilized higher priced inventory or the magnitude of price decreases may exceed the magnitude of the corresponding decrease in raw materials, energy, packaging materials or other costs. Accordingly, fluctuations in the cost or supply of raw materials (including durum wheat ingredients), energy (including utility and transportation costs), packaging materials or other items may have a material adverse impact on our results of operations and cash flows.

If our customers curtail their operations, our financial performance may be adversely affected.

Due to the highly competitive environment, combined with macro-economic challenges existing in the food retailing and foodservice industries, some of our retail and foodservice customers have experienced economic difficulty. In addition, the food retailing industry has experienced consolidation. Certain of our customers have been forced to close stores and certain others have sought bankruptcy protection. If a material number of our customers, or any one large customer, closed a significant number of stores, filed for bankruptcy protection, or consolidated operations with another company, these actions could have a material adverse impact on our business, financial condition, or results of operations.

A decline in demand for dry pasta could adversely affect our financial performance.

We focus primarily on producing and selling dry pasta. We expect to continue this primary focus. Because of our product concentration, any decline in consumer demand or preference, including diet driven changes, for dry pasta or any other factor that adversely affects the pasta market could have a material adverse effect on our business, financial condition or results of operations.

If aggregate production capacity in the U.S. pasta industry increases or is under-utilized, we may have to adopt a more aggressive pricing strategy, which could adversely affect our results of operations.

Our competitive environment is affected by the relationship between aggregate industry production capacity and aggregate market demand for pasta products. Production capacity above market demand can have a material adverse effect on our business, financial condition or results of operations.

If we are not able to compete effectively with established domestic and foreign producers of pasta products, our financial performance may be adversely affected.

The markets in which we operate are highly competitive. We compete against numerous well-established national, regional, local and foreign companies in every aspect of our business. Some of our competitors may have longer operating histories, greater brand recognition, or more financial or other resources than we do. Our customers may not continue to buy our products and we may not be able to compete effectively with these competitors.

Our advantage relative to customer brands may be diminished if competitors obtain the technology necessary to efficiently manufacture and distribute large numbers of stock-keeping units (SKU).

We believe our success in the customer brand market is attributable, in part, to our ability to efficiently manage the manufacture and distribution of large numbers of SKUs. Currently, we handle approximately 3,700 SKUs, most of which are related to customer brands. The technology and

9

know-how to manage large numbers of SKUs is not proprietary. If a competitor were to invest the technology and know-how to develop efficient SKU management, this portion of our business may be adversely affected, which could have a material adverse impact on our business, financial condition, or results of operations.

If we are unable to manage our production and inventory levels, our ability to operate cost-effectively and to maintain high customer service standards may be adversely affected.

Unanticipated fluctuations in demand make it difficult to manage production schedules, plant operations and inventories. Also, customer inventory management systems that are intended to reduce a retailer's inventory investment increase pressure on suppliers like us to fill orders promptly and thereby shift a portion of the retailer's inventory management cost to the supplier. If we overestimate the demand, the result will be the production of excess inventory which could result in markdowns and increased inventory carrying costs. If we underestimate the demand for our products, our customer service standards may suffer as we may be unable to provide adequate supplies of pasta products to retailers in a timely fashion, which may result in loss of sales and/or customers.

Our need for substantial capital and our level of indebtedness may restrict our operating and financial flexibility and could adversely affect our business, financial condition or operating results.

Our business has required and will continue to require substantial capital investment. A portion of this investment has been financed through third-party lenders. The amount of debt we carry and the terms of our indebtedness could adversely affect us in several ways, including:

- •

- our ability to obtain additional financing in the future for working capital, capital expenditures, and general corporate

purposes, including strategic acquisitions, may be impaired;

- •

- our ability to use operating cash flow in other areas of our business may be limited because a substantial portion of our

cash flow from operations may have to be dedicated to the payment of the principal and interest on our indebtedness;

- •

- the terms of such indebtedness restrict our ability to pay dividends; and

- •

- the level of debt we carry could restrict our corporate activities, including our ability to respond to competitive market conditions, to provide for capital expenditures beyond those permitted by our loan agreements, or to take advantage of acquisition opportunities and grow our business.

In the event that we fail to comply with the covenants in our current credit facility, or any future loan agreements, there could be an event of default under the applicable instrument. As a result, all amounts outstanding under our current or any future debt instruments may become immediately due and payable. We have used, and may in the future use, interest rate protection agreements covering our variable rate debt to limit our exposure to variable rates. However, we may not be able to enter into such agreements or such agreements may adversely affect our financial performance. If interest rates were to increase significantly or if we are unable to generate sufficient cash flow from operations in the future, we may not be able to service our debt and may have to refinance all or a portion of our debt, structure our debt differently, obtain additional financing or sell assets to repay such debt.

We may not be able to find alternative financing at the maturity of our credit facility.

Our U.S. credit facility matures in March 2011 and we may not be able to secure refinancing or alternative financing at commercially reasonable terms. Any financing obtained may contain restrictive covenants limiting our flexibility related to operations, capital expenditures, capital structure or other matters.

10

Changes in our capital structure could adversely affect our business, financial condition, or operating results.

Our current credit facility expires in March 2011. Prior to that time, we may decide, for strategic or other reasons, to terminate our credit facility and implement a new capital structure. Our new capital structure may result in a new credit facility, issuance of public debt, issuance of convertible debt, issuance of new shares, the repurchase of existing shares, other alternatives, or a combination of alternatives. Implementation of a new capital structure bears various risks, including risks related to new covenants, restrictions on specified business activities, potential mis-alignment with strategic initiatives, and a potential decrease in future financial flexibility.

If existing anti-dumping measures imposed against certain foreign imports terminate, we will face increased competition from foreign companies and our profit margins or market share could be adversely affected.

Anti-dumping and countervailing duties on certain Italian and Turkish imports imposed by the United States Department of Commerce ("DOC") in 1996 enable us and our domestic competitors to compete more favorably against Italian and Turkish producers in the U.S. pasta market. In September 2007, the U.S. International Trade Commission ("ITC") extended the anti-dumping and countervailing duty orders for an additional five years, through 2012. If the anti-dumping and countervailing duty orders are repealed or foreign producers sell competing products in the United States at prices lower than ours or enter the U.S. market by establishing production facilities in the United States, the result would further increase competition in the U.S. pasta market and could have a material adverse effect on our business, financial condition or results of operations.

A write-off or write down of our intangible and other long-lived assets could adversely affect our results of operations.

Our total assets include substantial intangible assets representing the acquisition date fair value of acquired brand names. We review these intangible assets for impairment annually or whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. A determination that all or a portion of our intangible assets are not recoverable, although a non-cash charge to operations, could have a material adverse effect on our results of operations or total capitalization. At October 2, 2009, the balance of our intangible brand assets was $79.1 million.

Our total assets also reflect substantial long-lived fixed assets for property, plant and equipment. We review long-lived assets for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. We evaluate recoverability of assets to be held and used by comparing the carrying amount of an asset to future net cash flows expected to be generated by the asset. If such assets are considered to be impaired, the impairment to be recognized is measured by the amount by which the carrying amount of the assets exceeds the fair value of the assets. Assets to be disposed of are reported at the lower of the carrying amount or fair value less costs to sell. A determination requiring write off of a significant portion of fixed assets, although a non-cash charge to operations, could have a material adverse effect on our results of operations or total capitalization. At October 2, 2009, net long-lived fixed assets totaled $291.2 million.

Because we produce food products, we may be subject to product liability claims and have costs related to product recalls.

We may need to recall some of our products if they are misbranded or mislabeled or become adulterated or infested. We may also be subject to claims or lawsuits if the consumption of any of our products causes injury. A widespread product recall or a significant product liability judgment against us could cause products to be unavailable for a period of time and result in a loss of consumer and customer confidence in our food products and could have a material adverse effect on our business. We carry insurance against most of these matters; however, our insurance coverage may not be adequate.

11

The cost of commercially available insurance has increased significantly and such insurance may not be available in the future at prices that we can afford. In addition, because we often indemnify our customers for costs related to product recalls, we could be subject to additional expenses that may not be covered by insurance and could have a material adverse impact on our business, results of operations, or financial condition.

The loss of the services of one or more members of our senior management team or other key subject matter expert could have a material adverse effect on our business, financial condition and results of operations.

Our operations and prospects depend in large part on the performance of our senior management team. We may not be able to find qualified replacements for any of these individuals if their services were no longer available. We do not currently maintain key person life insurance on any member of our senior management team. Except for Mr. John P. Kelly, our President and Chief Executive Officer, we do not provide employment agreements to our executive officers.

In addition to the executive team there are a limited number of subject matter experts in key functions that could impair the effective operations of the business or reporting requirements if appropriate replacements could not be found in a timely fashion.

If our competitors develop or acquire advanced technology, our financial performance may be adversely affected.

If other pasta producers acquire equipment similar to our equipment or more advanced equipment that provides greater efficiencies, what we believe to be our current competitive advantage might be diminished or eliminated, potentially causing pressure on profit margins or reducing our market share. Erosion of this advantage could have a material adverse effect on our business, financial condition or results of operations.

Disruptions in transportation of raw materials or finished products could adversely affect our financial results.

Durum wheat is shipped by rail to our production facilities in Missouri and South Carolina under annually negotiated contracts or market tariff rates. From time to time we also ship semolina, milled and processed at the Missouri facility, to our South Carolina facility. There is no assurance that the transportation costs will remain the same as fuel costs are volatile and, under these contracts, rail carriers have the ability to pass through certain increases in fuel cost. An extended interruption in our ability to ship durum wheat by railroad to the Missouri or South Carolina plants, or semolina to our South Carolina facility, could cause us to incur significantly higher costs and longer lead times associated with the distribution of our pasta to our customers. If we are unable to provide adequate supplies of pasta products to our customers in a timely fashion due to such delays, we may subsequently lose sales. This could have a material adverse effect on our business, financial condition or results of operations.

Disruptions in utilities at our facilities would impair our ability to produce products and could adversely affect our financial results.

Each of our production facilities relies heavily on the local electric, gas and water utilities for supply. If there are significant and lengthy interruptions in any of these utilities, our ability to meet customer shipments could be impaired. The disruptions could come from natural disasters, terrorist attacks or other causes. This could have a material adverse effect on our business, financial condition or results of operations.

12

Disruptions or failures in the software we use in our operations, or in the supporting hardware, could adversely affect our financial results.

We rely on a number of key systems to produce, ship, invoice and account for our products. In the event of a material failure of or disruption to one or more of these systems, including disruptions caused by the failure of the supporting hardware, our ability to accomplish one or more of these functions could be impaired. If the cause of the failure or disruption cannot be remedied in a short period of time, we would not be able to produce or ship products. This could have a material adverse effect on our business, financial condition or results of operations.

Our international business may not be successful.

We operate a pasta-producing facility in Italy. We do not have the same competitive scale of operations or historic relationships with the European trade or European supply base in overseas markets that we do in the U.S.

There are several risks inherent in doing business on an international level. These risks include:

- •

- export and import restrictions;

- •

- tariffs, trade duties, and other trade barriers;

- •

- difficulties in staffing and managing foreign operations;

- •

- managing regulatory requirements across multiple foreign jurisdictions;

- •

- fluctuations in currency exchange rates and inflation risks;

- •

- seasonal fluctuations in business activity in other parts of the world;

- •

- changes in a specific country's or region's political or economic conditions, particularly in emerging markets;

- •

- potentially adverse tax consequences; and

- •

- difficulty in securing or transporting raw materials or transporting finished product.

Any of these risks could adversely impact the success of our international operations. If our international revenues are inadequate to offset the expense of maintaining foreign operations, our business or results of operations could be harmed.

Our competitive position and financial results and condition could be adversely impacted if we are unable to protect our intellectual property.

Our brands are important to our success and our competitive position. Our actions to establish and protect our brands and other proprietary rights may be inadequate to prevent imitation of our products by others. Moreover, we may face claims by third parties that we violate their intellectual property rights. Any litigation or claims against us, whether or not successful, could result in substantial cost, divert management's time and attention from our core business, or significantly harm our reputation, our business or our results of operations.

A failure to comply with applicable laws and regulations could adversely affect our business.

We are subject to laws and regulations administered by federal, state, and other governmental agencies related to the operation of our production facilities, the production, packaging, labeling and marketing of our products and pollution control, including air emissions. Any determination by the FDA or other agencies that our facilities are not in compliance with applicable regulations could interfere with the continued manufacture and distribution of the affected products and, in some cases,

13

might also require the recall of previously distributed products. In addition, we could become subject to increased regulatory oversight related to ensuring a secure national food chain and, as a result, could incur material costs to comply with additional testing protocols, precertification of shipments, or other procedures required by such regulations. Any such determination or change in regulation could have a material adverse effect on our business, financial condition or results of operations.

Under environmental laws, we are exposed to liability primarily as an owner and operator of real property and, as such, we may be responsible for the clean-up or other remediation of contaminated property. Environmental laws and regulations can change rapidly and we may become subject to more stringent environmental laws and regulations in the future that may be retroactively applied to earlier events. In addition, compliance with more stringent environmental laws and regulations could involve significant capital investments. Additional information is provided in this Annual Report on Form 10-K under the heading "Business—Governmental Regulation; Environmental Matters."

We are subject to a consent injunction and agreement which, if we violate, could require us to pay substantial fines or other penalties or otherwise have a material adverse effect on us.

We are subject to a consent injunction with the Securities and Exchange Commission ("SEC") and a settlement agreement with the United States Attorney's Office for the Western District of Missouri on behalf of the Department of Justice ("DOJ"), violation of either of which could have a material adverse effect on us. In the fourth quarter of fiscal year 2008, the SEC and the DOJ announced the completion of their investigation of us and resolution of outstanding investigative matters. Under the terms of a settlement with the SEC, we agreed to a consent injunction requiring future compliance with federal securities laws. Under an agreement with the DOJ, we agreed to continue to cooperate with the DOJ. To the extent we fail to comply with either agreement, we could be subject to additional sanctions or fines, which could have a material adverse effect on our business, results of operations or financial condition.

Our ability to pay dividends to shareholders is restricted by factors including contractual provisions and our financial performance.

We have not paid dividends since June 2005. We anticipate that future free cash flow will be used principally to fund interest expense and repayment of debt. Payment of dividends is restricted by provisions in our current credit facility.

A significant percent of our outstanding voting stock is held by a limited number of institutional investors.

A significant percent of our outstanding voting stock is held by a limited number of institutional investors. As a result, the decision of relatively small number of shareholders could have a substantial impact on the trading price of our stock. Continued concentrated ownership could result in fewer shares being available to be traded in the market, resulting in reduced liquidity. In addition, a decision by one or more large investor to liquidate its holdings could adversely affect the trading price of our stock. So long as a significant percentage of our shares are held by a small number of investors, it is easier for any one shareholder to join with other shareholders to attempt to effect control of our company.

The integration of acquired businesses may require significant resources and may not be successful.

In the future, we may consider opportunities to expand our business through the acquisition of other companies, assets, or product lines. If we are unsuccessful in executing the integration of acquired companies, assets, or product lines, or if the integration is more difficult than anticipated, we may experience disruptions to our operations. A difficult or unsuccessful integration could have an adverse effect on our business, results of operations, or financial condition.

14

Risks that may affect our ability to successfully integrate and to fully realize the anticipated benefits of the acquisition include:

- •

- diversion of management's attention from other business concerns;

- •

- adverse effects on existing business relationships with customers;

- •

- increasing the scope and complexity of our operations; and

- •

- conforming standards, processes, information technology systems, procedures, and controls of the acquired business with our operations

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

Production Facilities: As of October 2, 2009, we owned pasta production plants located in Excelsior Springs, Missouri, Columbia, South Carolina, Tolleson, Arizona, and Verolanuova, Italy. Our U.S. facilities are strategically located to support North American distribution of our products and benefit from the rail and interstate highway infrastructure near each facility. As of October 2, 2009, our facilities had combined annual production capacity of approximately 940 million pounds of pasta. In addition, we occasionally purchase pasta products from other manufacturers for resale.

Distribution Centers: We own the distribution centers adjoining our Missouri, South Carolina, and Arizona plants. In addition, as of October 2, 2009, we leased space in public warehouses in Missouri and Arizona.

The warehousing operations at each of our distribution centers in Missouri, South Carolina and Arizona, including our leased facility in Missouri, are outsourced under a long-term agreement with OHL. OHL specializes in warehouse and logistics management services. In addition, OHL provides traffic and freight management services to us under a long term contract, thereby effectively providing for the shipment of our finished products from our domestic facilities.

Our credit facility, executed on March 13, 2006 and last amended December 27, 2007, grants a collateral interest to our lenders in substantially all of our tangible and intangible domestic assets.

SEC Investigation

In September 2008, the Company agreed to a consent injunction and settled all outstanding matters pertaining to the SEC investigation of the Company's historical accounting practices. Certain former officers of the Company also resolved claims asserted against them by the SEC in 2008 and 2009, with the exception of one former officer. As a result, the Company may continue to have indemnity obligations to this former officer under Delaware law and our articles of incorporation. We believe the effect of any indemnification obligation on our cash flows and results of operations will be immaterial.

Other Matters

From time to time and in the ordinary course of our business, we are the subject of government investigations or audits and named as a defendant in legal proceedings related to various other issues, including worker's compensation claims, tort claims and contractual disputes.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

We did not submit any matters to the vote of our stockholders during the fourth quarter of fiscal year 2009.

15

ITEM 5. MARKET FOR REGISTRANT'S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

Our Class A Convertible Common Stock, par value $0.001 per share (the "common stock") was quoted on the NASDAQ Global Market under the symbol "AIPC".

Our articles of incorporation allowed two classes of common stock, Class A Convertible voting, and Class B Convertible nonvoting, with certain initial investors permitted to convert back and forth between the classes. The conversion features were not exercised and the conditions under which the Class B shares may be issued no longer exist.

The range of the high and low prices per share of the common stock for fiscal year 2009 and 2008 was as follows:

| |

Year Ended October 2, 2009 |

Year Ended September 26, 2008 |

|||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

High | Low | High | Low | |||||||||

First Quarter |

$ | 23.80 | $ | 11.90 | $ | 9.10 | $ | 6.55 | |||||

Second Quarter |

$ | 35.15 | $ | 21.68 | $ | 7.00 | $ | 4.39 | |||||

Third Quarter |

$ | 34.24 | $ | 23.59 | $ | 12.35 | $ | 5.45 | |||||

Fourth Quarter |

$ | 32.08 | $ | 27.17 | $ | 15.90 | $ | 11.00 | |||||

Holders

As of November 12, 2009, there were approximately 1,100 shareholders of record of our common stock.

Dividends

Payment of dividends is restricted by provisions in our current credit facility.

Securities Authorized for Issuance Under Equity Compensation Plans

See Item 12, "Security Ownership of Certain Beneficial Owners and Management and Related Stock Holder Matters," contained in this Annual Report on Form 10-K for additional information regarding our equity compensation plans.

Recent Sales of Unregistered Securities

None.

Issuer Purchases of Equity Securities

During the fourth quarter of fiscal 2009, we purchased 1,803 shares of our common stock, at an average price paid per share of $31.74 (all purchases were made during the four week period ending August 28, 2009), in connection with the withholding of taxes upon vesting of nonvested shares.

On October 4, 2002, our Board of Directors authorized up to $20.0 million to implement a common stock repurchase plan. There is $7.9 million available under the common stock repurchase plan. Purchases under the plan are restricted by provisions in our current credit facility and, accordingly, there were no purchases during fiscal year 2009.

16

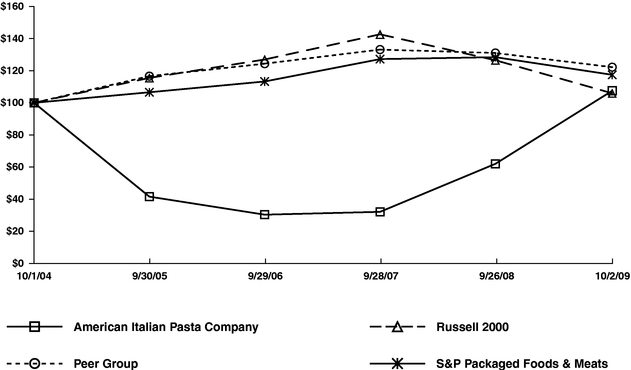

Stockholder Return Performance Graph

The following graph compares the cumulative total stockholders' return on the common stock for the five fiscal years ended October 2, 2009 (October 1, 2004 to October 2, 2009) against the cumulative total return of the Russell 2000® Index, the S&P Packaged Foods & Meats Index, and the peer group we used in fiscal 2008. The graph and table assume that $100 was invested on October 1, 2004 (the last day of fiscal year 2004) in our common stock, the Russell 2000® Index, the S&P Packaged Foods & Meats Index, and the peer group and that all dividends were reinvested.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among American Italian Pasta Company, The Russell 2000 Index,

The S&P Packaged Foods & Meats Index And A Peer Group

- *

- $100 invested on 10/1/04 in stock or 9/30/04 in index, including reinvestment of dividends.

| |

Russell 2000® Index(1) |

Peer Group(2) | S&P Packaged Foods & Meats(3) |

American Italian Pasta |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

October 1, 2004 |

100.00 | 100.00 | 100.00 | 100.00 | |||||||||

September 30, 2005 |

115.51 | 116.59 | 106.56 | 41.57 | |||||||||

September 29, 2006 |

126.97 | 124.37 | 113.27 | 30.34 | |||||||||

September 28, 2007 |

142.64 | 133.14 | 127.21 | 32.11 | |||||||||

September 26, 2008 |

126.50 | 131.02 | 128.41 | 62.00 | |||||||||

October 2, 2009 |

105.94 | 122.18 | 117.43 | 107.50 | |||||||||

- (1)

- The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000 is constructed to provide a comprehensive and unbiased small-cap barometer and is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap

17

opportunity set. Information concerning the Russell 2000 Index is available on the Internet at www.russell.com.

- (2)

- In

fiscal 2008, we compared our performance against a peer group, selected on the basis of similarity of their business to ours, comprised of the following

companies: Flowers Foods Inc. (FLO); Hormel Foods Corp. (HRL); J & J Snack Foods Corp. (JJSF); McCormick & Company Inc. (MKC); Ralcorp Holdings Inc. (RAH);

Smithfield Foods Inc. (SFD); and Treehouse Foods Inc. (THS). During 2009, we determined we would compare against the S&P Packaged Foods & Meats Index, a published industry or

line-of-business index, which we believe provides more meaningful information. For fiscal 2009, our transition year, we have included our performance against the peer group

used during fiscal 2008. We will not use this peer group in the future.

- (3)

- The S&P Packaged Foods & Meats Index includes producers of packaged foods including dairy products, fruit juices, meats, poultry, fish and pet foods.

18

ITEM 6. SELECTED FINANCIAL DATA

The following table presents selected historical financial data for the fiscal years ended October 2, 2009, September 26, 2008, September 28, 2007, September 29, 2006, and September 30, 2005 (in thousands, except per share data).

| |

YEAR ENDED | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||

| |

(53 weeks) |

(52 weeks) |

(52 weeks) |

(52 weeks) |

(52 weeks) |

|||||||||||

STATEMENT OF OPERATIONS DATA: |

||||||||||||||||

Revenues(1) |

$ | 628,162 | $ | 569,196 | $ | 398,122 | $ | 367,023 | $ | 364,159 | ||||||

Cost of goods sold |

451,513 | 446,891 | 308,819 | 284,777 | 300,151 | |||||||||||

Gross profit |

176,649 |

122,305 |

89,303 |

82,246 |

64,008 |

|||||||||||

Selling and marketing expense |

27,989 | 27,727 | 21,503 | 22,871 | 20,342 | |||||||||||

General and administrative expense(2) |

34,363 | 46,663 | 33,548 | 35,459 | 23,198 | |||||||||||

Litigation settlement(3) |

— | — | — | — | 14,000 | |||||||||||

Impairment charges to brands |

— | 3,654 | — | 998 | 88,550 | |||||||||||

(Gain) loss on disposition of brands(4) |

(500 | ) | — | — | 4,708 | — | ||||||||||

(Gains) losses related to long-lived assets(5) |

1,385 | 1,139 | (109 | ) | 22,268 | 9,759 | ||||||||||

Recovery from restructuring program(6) |

— | — | — | — | (554 | ) | ||||||||||

Operating profit (loss) |

113,412 | 43,122 | 34,361 | (4,058 | ) | (91,287 | ) | |||||||||

Interest expense, net |

16,499 | 26,240 | 29,421 | 29,509 | 16,234 | |||||||||||

Other (income) expense, net |

(8 | ) | 92 | (245 | ) | (913 | ) | (3,544 | ) | |||||||

Income (loss) before income taxes |

96,921 | 16,790 | 5,185 | (32,654 | ) | (103,977 | ) | |||||||||

Income tax provision (benefit) |

8,633 | (2,321 | ) | (163 | ) | (2,241 | ) | (3,730 | ) | |||||||

Net income (loss) |

$ | 88,288 | $ | 19,111 | $ | 5,348 | $ | (30,413 | ) | $ | (100,247 | ) | ||||

Net income (loss) per common share (basic) |

$ |

4.27 |

$ |

1.00 |

$ |

0.29 |

$ |

(1.65 |

) |

$ |

(5.49 |

) |

||||

Net income (loss) per common share (assuming dilution) |

$ |

4.10 |

$ |

0.99 |

$ |

0.28 |

$ |

(1.65 |

) |

$ |

(5.49 |

) |

||||

Cash dividend declared per common share |

$ |

— |

$ |

— |

$ |

— |

$ |

— |

$ |

0.5625 |

||||||

Weighted-average common shares outstanding |

20,692 |

19,118 |

18,673 |

18,386 |

18,247 |

|||||||||||

Weighted-average common shares outstanding (including dilutive securities) |

21,555 |

19,384 |

18,951 |

18,386 |

18,247 |

|||||||||||

OTHER FINANCIAL DATA (AT END OF PERIOD): |

||||||||||||||||

Cash and cash equivalents |

$ | 30,959 | $ | 38,623 | $ | 16,635 | $ | 22,805 | $ | 11,911 | ||||||

Working capital |

$ | 96,458 | $ | 72,350 | $ | 55,505 | $ | 54,285 | $ | 58,971 | ||||||

Plant, property and equipment—net |

$ | 291,212 | $ | 303,503 | $ | 316,109 | $ | 324,464 | $ | 360,740 | ||||||

Brands |

$ | 79,074 | $ | 79,769 | $ | 83,282 | $ | 82,772 | $ | 88,750 | ||||||

Total assets |

$ | 530,063 | $ | 553,024 | $ | 527,963 | $ | 531,969 | $ | 571,926 | ||||||

Long term debt, less current maturities |

$ | 104,100 | $ | 217,000 | $ | 240,000 | $ | 260,500 | $ | 276,006 | ||||||

Stockholders' equity |

$ | 307,416 | $ | 205,971 | $ | 171,918 | $ | 160,336 | $ | 186,026 | ||||||

Total debt/total capitalization |

26 | % | 54 | % | 58 | % | 62 | % | 60 | % | ||||||

Depreciation and amortization expense(7) |

$ | 24,986 | $ | 24,092 | $ | 23,409 | $ | 24,895 | $ | 25,132 | ||||||

We report on a 52/53 week fiscal year end, with a 53-week fiscal year occurring approximately every six years. Fiscal year 2009 was a 53-week fiscal year and fiscal years 2008, 2007, 2006 and 2005 were 52-week years. Accordingly, fiscal year 2009 includes revenues and expenses for one extra week.

19

- (1)

- The

U.S. Government enacted the Continued Dumping and Subsidy Offset Act of 2000 (the "CDSOA") which provides that assessed anti-dumping and

subsidy duties liquidated by the Department of Commerce after October 1, 2000 will be distributed to affected domestic producers. Accordingly, revenues in fiscal years 2009, 2008, 2007, 2006

and 2005 include payments received from the Department of Commerce of $0.8 million, $4.7 million, $3.0 million, $2.6 million and $1.0 million, respectively, as our

calculated share based on tariffs liquidated by the government during these periods on Italian and Turkish imported pasta. Effective October 1, 2007, the CDSOA was repealed, resulting in the

discontinuation of future distributions to affected domestic producers for duties assessed after such date. It is not possible to reasonably estimate amounts, if any, to be received in fiscal years

subsequent to 2009 on duties assessed prior to October 1, 2007.

- (2)

- Included

in general and administrative expenses are professional fees related to the restatement of historical financial statements and pending legal

matters that amounted to $0.8 million, $17.5 million, $13.3 million, $16.1 million, and $2.5 million in fiscal years 2009, 2008, 2007, 2006, and 2005, respectively.

- (3)

- Litigation

settlement relates to our settlement of the federal securities class action lawsuit. The settlement was for $25.0 million, comprised of

$11.0 million in cash, provided by our insurers, and $14.0 million satisfied through the issuance of 1.4 million shares of our common shares.

- (4)

- During

fiscal year 2009 we sold an unused brand for $0.5 million. The fiscal year 2006 loss on disposition of brands resulted from the sale of our

Mrs. Leeper's and Eddie's Spaghetti brands.

- (5)

- Losses

related to long-lived assets include the loss on sale of our Kenosha plant in fiscal year 2006 and losses related to certain pasta

manufacturing and packaging equipment that were disposed and excess equipment written down to fair market value, primarily in fiscal years 2005 and 2006. During fiscal year 2007 we recognized

$0.1 million on the gain on the sale of certain excess equipment. The losses during fiscal year 2009 and 2008 are due primarily to the write-off of fixed assets due to routine plant

changes and asset upgrades.

- (6)

- In

fiscal year 2005, we recognized $0.6 million benefit related to the reversal of a previously established restructuring reserve due to the early

reactivation of the Kenosha plant which was not contemplated at the time the restructuring reserve was established.

- (7)

- Reflects aggregate depreciation and amortization expense of property, plant and equipment and other amortizable assets excluding deferred debt issuance costs. Depreciation and amortization is included in our statement of operations under the captions cost of goods sold and general and administrative expense.

20

ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis of financial condition and results of operations should be read in conjunction with "Selected Financial Data," our consolidated historical financial statements and the notes to those statements that appear elsewhere in this report. Our discussion contains forward-looking statements based upon current expectations that involve risks and uncertainties, such as our plans, objectives, expectations and intentions. Actual results and the timing of events could differ materially from those anticipated in these forward-looking statements as a result of a number of factors, including those set forth under "Cautionary Note Concerning Forward-Looking Information" and "Risk Factors" elsewhere in this report.

Overview

We report on a 52/53 week fiscal year ending on the Friday nearest the end of the quarter. Fiscal year 2009 was a 53-week year and fiscal years 2008 and 2007 were 52-week years.

We believe we are the largest producer and marketer of dry pasta in North America, by volume, based on data available from Nielsen, published competitor financial information, industry sources such as the National Pasta Association, suppliers, trade magazines, other market date, and our own market research. Management believes that the combination of our low cost structure, our product strategy of offering proprietary branded, customer branded, imported and specialty products, our scalable production facilities and our key customer relationships create competitive advantages.

We generate revenues in two customer markets: retail and institutional. Retail market revenues include the sales of our pasta products to customers who resell the pasta in retail channels, including traditional grocery retailers, club stores, mass merchants, drug and discount stores, and encompasses sales of our proprietary branded products, customer branded (also referred to as "private label") products, and imported products. These revenues represented 78.9%, 74.8%, and 76.5% of our total revenue for the years ended October 2, 2009, September 26, 2008 and September 28, 2007, respectively. Institutional market revenues include the sales of our pasta products to customers to foodservice distributors (comprised of businesses and organizations that sell products to restaurants, healthcare facilities, schools, hotels, industrial caterers, and multi-unit restaurant chains that procure directly), food processors that use pasta as a food ingredient, government agencies, and other customers that we periodically supply. The institutional market represented 21.1%, 25.2% and 23.5% of our total revenue for the years ended October 2, 2009, September 26, 2008 and September 28, 2007, respectively.

Average selling prices for both our branded and non-branded products are based on the competitive market environment. In addition, average selling prices for our non-branded products may be affected by customer-specific packaging and raw material requirements, product manufacturing complexity and other service requirements. Average retail and institutional prices will also vary due to changes in the relative share of customer revenues and item specific sales volumes (i.e., product sales mix). Generally, average retail selling prices are higher than institutional selling prices. Selling prices of our proprietary branded products are higher than selling prices for our other product categories, including customer brands. Revenues are reported net of cash discounts, product returns, and promotional and slotting allowances.