Attached files

| file | filename |

|---|---|

| EX-24 - DIRECTORS POWER OF ATTORNEY - GREAT WEST LIFE & ANNUITY INSURANCE CO | poa.htm |

| EX-21 - GREAT WEST LIFE & ANNUITY INSURANCE CO | exhibit21.htm |

| EX-4.1 - GREAT WEST LIFE & ANNUITY INSURANCE CO | exhibit41.htm |

| EX-4.2 - GREAT WEST LIFE & ANNUITY INSURANCE CO | exhibit4-2.htm |

| EX-4.3 - ELECTION FORM - GREAT WEST LIFE & ANNUITY INSURANCE CO | electionform43.htm |

As filed with the Securities and Exchange Commission on November 20, 2009

Registration No. 333-_____

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

Registration Statement Under The Securities Act of 1933

Great-West Life & Annuity Insurance Company

(Exact Name of Registrant as Specified in its Charter)

|

Colorado |

6311 |

84-0467907 | ||

|

(State or other jurisdiction of

incorporation or organization) |

(Primary Standard Industrial Classification Code) |

(I.R.S. Employer

Identification Number) |

8515 East Orchard Road, Greenwood Village, Colorado 80111 (800) 537-2033

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

|

Mitchell T.G. Graye |

|

Copy to: |

|

President and Chief Executive Officer |

|

Stephen E. Roth, Esq. |

|

Great-West Life & Annuity Insurance Company |

|

Sutherland, Asbill & Brennan LLP |

|

8515 East Orchard Road |

|

1275 Pennsylvania Avenue, N.W. |

|

Greenwood Village, CO 80111 |

|

Washington, DC |

|

(800) 537-2033 |

|

20004-2415 |

|

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service) |

|

| Approximate date of commencement of proposed sale to the public: Continuously on and after the effective date of this Registration Statement. |

| If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x |

| If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of earlier effective registration statement for the same offering. ¨ |

|

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨ |

| If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨ |

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. |

|

Large Accelerated Filer ¨ |

|

Accelerated Filer ¨ |

|

Non-Accelerated Filer x |

|

Smaller Reporting Company ¨ |

|

(Do not check if a smaller reporting company) |

|

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of Securities to be Registered |

Amount to

be

Registered |

Proposed

Maximum Offering

Price Per Unit* |

Proposed

Maximum Aggregate

Offering Price |

|

Amount of

Registration

Fee |

|||||

|

Certificates issued pursuant to Guaranteed Income Annuity Contracts |

N/A |

N/A |

$ |

50,000,000 |

* |

|

$ |

2,790 |

||

|

* |

The proposed maximum aggregate offering price is estimated solely for the purposes of determining the registration fee. The amount to be registered and the proposed maximum offering price per unit are not applicable since these securities are not issued in predetermined amounts or units. |

| The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration

Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

|

SecureFoundationSM

Group Fixed Deferred Annuity Certificate

Issued by:

8515 East Orchard Road

Greenwood Village, CO 80111

Tel. (800) 537-2033

[May 1, 2010]

This prospectus describes the SecureFoundationSM Group Fixed Deferred Annuity Certificate (the “Certificate”) issued by Great-West Life & Annuity Insurance Company. The Certificate is offered to individual retirement account (“IRA”)

owners that purchase shares of one of the Maxim SecureFoundation mutual funds, which currently consist of the Maxim SecureFoundationSM Lifetime 2015 Portfolio, Maxim SecureFoundationSM Lifetime 2025 Portfolio, Maxim SecureFoundationSM Lifetime 2035 Portfolio, Maxim SecureFoundationSM Lifetime

2045 Portfolio, Maxim SecureFoundationSM Lifetime 2055 Portfolio (the “SecureFoundation Lifetime Portfolios”), and the Maxim SecureFoundationSM Balanced Portfolio (each, a “Covered Fund” and together, the “Covered Funds”). The Certificate provides for guaranteed income for the life of a designated person based on the Certificate

Owner’s investment in one or more of the Covered Funds, provided all conditions specified in the Certificate are met, regardless of how long the designated person lives or the actual performance or value of the Covered Funds. The Certificate has no cash value and no surrender value. The interests of the Certificate Owner in the Certificate may not be transferred, sold, assigned, pledged, charged, encumbered, or alienated in any way.

Prospective purchasers may apply to purchase a Certificate through GWFS Equities, Inc. (“GWFS Equities”), the principal underwriter for the Certificates or other broker-dealers that have entered into a selling agreement with GWFS Equities. GWFS Equities will use its best efforts to sell the Certificates, but is not required

to sell any specific number or dollar amount of Certificates.

This prospectus provides important information that a prospective purchaser of a Certificate should know before investing. Please retain this prospectus for future reference.

Neither the Securities and Exchange Commission (“SEC”) nor any state securities commission has approved or disapproved these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This prospectus does not constitute an offering in any jurisdiction in which such offering may not be lawfully made.

The Certificate:

|

Ÿ |

Is NOT a bank deposit | ||

|

Ÿ |

Is NOT FDIC insured | ||

|

Ÿ |

Is NOT insured or endorsed by a bank or any government agency | ||

|

Ÿ |

Is NOT available in every state |

The purchase of the Certificate is subject to certain risks. See “Risk Factors” on page 5. The Certificate is novel and

innovative. While we understand that the Internal Revenue Service may be considering tax issues associated with products similar to the Certificate, to date the tax consequences of the Certificate have not been addressed in published legal authorities. Under the circumstances, you should therefore consult a tax advisor before purchasing a Certificate.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the SEC is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale

is not permitted.

|

28 |

|

30 |

|

30 |

| ABOUT US | 32 |

| EXPERTS | 34 |

| DEFINITIONS | 36 |

SecureFoundationSM

Group Fixed Deferred Annuity Certificate

Issued by:

8515 East Orchard Road

Greenwood Village, CO 80111

Tel. (800) 537-2033

Certain terms used in this prospectus have specific and important meanings. Some important terms are explained below, and in most cases the meaning of other important terms is explained the first time they are used in the prospectus. You will also find in the back of this prospectus a listing of all of the terms, with

the meaning of each term explained.

|

Ÿ |

The “Certificate” is the SecureFoundation Group Fixed Deferred Certificate issued by Great-West Life & Annuity Insurance Company pursuant to the terms of a Group Fixed Deferred Annuity Contract (the “Group Contract”) issued to Orchard Trust Company, LLC (“Orchard Trust” or the “Group Contract Owner”). In

certain states this may be an individual contract, which will have the same features and benefits unless otherwise noted. |

|

Ÿ |

“We,” “us,” “our,” “Great-West,” or the “Company” means Great-West Life & Annuity Insurance Company. |

|

Ÿ |

“You” or “yours” means the owner of the Certificate described in this prospectus. The terms “you,” “yours,” “Owner,” and “Certificate Owner” may be used interchangeably in this prospectus. |

|

Ÿ |

“Covered Person” or “Covered Persons” means the person or persons, respectively, named in the Certificate whose age is used for certain important purposes under the Certificate, including determining the amount of the guaranteed income that may be provided by this Certificate. |

|

Ÿ |

“Covered Fund” or “Covered Funds” refer to the Maxim SecureFoundationSM Lifetime 2015 Portfolio, Maxim SecureFoundationSM Lifetime 2025 Portfolio, Maxim SecureFoundationSM Lifetime

2035 Portfolio, Maxim SecureFoundationSM Lifetime 2045 Portfolio, Maxim SecureFoundationSM Lifetime 2055 Portfolio, and the Maxim SecureFoundationSM Balanced Portfolio. |

The Certificate can be owned in the following ways:

|

Ÿ |

Sole Owner who is an individual and also the Covered Person. |

- 1 -

|

Ÿ |

Sole Owner who is an individual and the Covered Person, with his or her spouse as the joint Covered Person. |

We believe that in most cases the Certificate will have a sole Owner who is the only Covered Person. Therefore, for ease of reference, most of the discussion in this prospectus assumes you are the sole Owner and the only Covered Person under the Certificate. In some places in the prospectus, however, we explain how certain

features of the Certificate differ if there are joint Covered Persons.

The following is a summary of the Certificate. You should read the entire prospectus in addition to this summary.

Certificates are issued pursuant to the terms of the Group Contract, which is a group guaranteed income annuity contract issued by the Company and owned by Orchard Trust. Certificates are offered to IRA owners that purchase shares of a Covered Fund. Currently, there is no other way to purchase the Certificate. The

Certificate provides, under certain specified conditions, for guaranteed minimum lifetime income, regardless of how long you live or how the Covered Fund performs. The Certificate does not have a cash value.

Provided all conditions of the Certificate and Group Contract are met, if the value of the shares in your Covered Fund (“Covered Fund Value”) equals zero as a result of Covered Fund performance, the Guarantee Benefit Fee, certain other fees that are not directly associated with the Certificate or Group Contract (e.g., IRA

fees, custodian fees, advisory fees), and/or Guaranteed Annual Withdrawal(s) (“GAW”), we will make annual payments to you for the rest of your life.

The amount of the GAW that you may take may increase from time to time based on your Covered Fund Value. It may also decrease if you take Excess Withdrawals.

The guaranteed income provided by your Certificate is based on the age and life of the Covered Person (or if there are joint Covered Persons, on the age of the younger joint Covered Person and the lives of both Covered Persons). A joint Covered Person must be your spouse and your spouse must be your sole beneficiary under your IRA.

While your Certificate is in force, a Guarantee Benefit Fee will be calculated and deducted from your Covered Fund Value on a monthly basis. It will be paid by redeeming the number of fund shares of your Covered Fund equal to the Guarantee Benefit Fee. The Guarantee Benefit Fee is calculated as a specified percentage

of your Covered Fund Value at the time the Guarantee Benefit Fee is calculated.

The Guarantee Benefit Fee pays for the insurance protections provided by the Certificate.

The guaranteed maximum or minimum Guarantee Benefit Fee we can ever charge for your Certificate is shown below. We currently charge 0.90%, which is also shown below. We may change this fee at any time within the minimum and maximum range described below upon thirty (30)

days prior written notice to you.

|

· |

The maximum Guarantee Benefit Fee for the Certificate, as a percentage of your Covered Fund Value, on an annual basis, is 1.5%. |

|

· |

The minimum Guarantee Benefit Fee for the Certificate, as a percentage of your Covered Fund Value, on an annual basis, is 0.70%. |

- 2 -

|

· |

The current Guarantee Benefit Fee for the Certificate, as a percentage of your Covered Fund Value, on an annual basis, is 0.90%. |

The Guarantee Benefit Fee is in addition to any charges that are imposed in connection with advisory, custodial and other services, and charges imposed by the Covered Funds.

Premium taxes may be applicable in certain states. Premium tax applicability and rates vary by state and may change. We reserve the right to deduct any such tax from premium when received.

The Certificate provides two basic protections to Certificate Owners who purchase this Certificate as a source or potential source of lifetime retirement income or other long-term purposes. Provided that certain conditions are met, the Certificate protects the Certificate Owner from:

|

· |

longevity risk, which is the risk that a Certificate Owner will outlive the assets invested in the Covered Fund; and |

|

· |

income volatility risk, which is the risk of downward fluctuations in a Certificate Owner’s retirement income due to changes in market performance. |

Both of these risks increase as a result of poor market performance early in retirement. Point-in-time risk (which is the risk of retiring on the eve of a down market) significantly contributes to both longevity and income volatility risk.

The Certificate does not provide a guarantee that the Covered Fund or your IRA will retain a certain value or that the value of the Covered Fund or IRA will remain steady or grow over time. Instead, it provides for a guarantee, under certain specified conditions, that regardless of the performance of the Covered Funds in your Account

and regardless of how long you live, you will be able to receive a guaranteed level of annual income for life. Therefore, it is important for you to understand that while the preservation of capital may be one of your goals, the achievement of that goal is not guaranteed by the Certificate.

The Certificate has three phases: an “Accumulation Phase,” a “GAW Phase,” and a “Settlement Phase.”

|

· |

The Accumulation Phase: During the Accumulation Phase, you may make additional Certificate Contributions to your Covered Fund, which establishes your Benefit Base (this is the sum of all Certificate Contributions minus any withdrawals and

any adjustments made on the “Ratchet Date” as described later in this prospectus), and take withdrawals from your IRA just as you otherwise would be permitted to (although Excess Withdrawals will reduce the amount of the Benefit Base under the Certificate). You are responsible for managing your withdrawals during the Accumulation Phase. |

|

· |

The GAW Phase: After you (or if there are joint Covered Persons, the younger joint Covered Person) have turned age 55, then you can enter the GAW Phase and begin to take GAWs (which are annual withdrawals that do not exceed a specified amount) without reducing your Benefit Base. GAWs

before age 59 ½ may result in certain tax penalties. |

|

· |

Settlement Phase: If your Covered Fund Value falls to zero as a result of Covered Fund performance, the Guarantee Benefit Fee, certain other fees that are not directly associated with the Certificate or Group Contract (e.g., IRA fees,

custodian fees, advisory fees), and/or GAWs, the Settlement Phase will begin. During the Settlement Phase, we make Installments to you for as long as you live. However, the Settlement Phase may never occur, depending on how long you live and how well the Covered Fund performs. |

- 3 -

The Installments that you may receive when you are in the GAW Phase or Settlement Phase are determined by multiplying your Benefit Base by the GAW Percentage (GAW%), which is determined by the age of the Covered Person(s). As described in more detail below, the amount of the Installments

may increase on an annual basis during the GAW Phase due to positive Covered Fund performance, and will decrease as a result of any Excess Withdrawals.

You are required to purchase a Certificate when you first purchase shares of a Covered Fund. For the SecureFoundation Lifetime Portfolios, you do not actually purchase the Certificate until the first business day of the year that is ten years prior to the date in the name of the fund. There is no minimum initial investment. The

Certificates are issued in accordance with the terms of the Group Contract issued by us to Orchard Trust. The Group Contract is a group fixed deferred annuity contract. Your investment in any Covered Fund is limited to $5,000,000. Any amount over $5,000,000 will not increase your Benefit Base.

The Certificate may only be purchased under the Group Contract by owners of applicable IRAs. You may elect to purchase a Certificate by completing an application or other form authorized by us. If this form is accepted by us at our Administrative Office, we will issue a Certificate

to you describing your rights and obligations.

The following is a list of the currently available Covered Funds

Maxim SecureFoundationSM Lifetime 2015 Portfolio

Maxim SecureFoundationSM Lifetime 2025 Portfolio

Maxim SecureFoundationSM Lifetime 2035 Portfolio

Maxim SecureFoundationSM Lifetime 2045 Portfolio

Maxim SecureFoundationSM Lifetime 2055 Portfolio

Maxim SecureFoundationSM Balanced Portfolio

- 4 -

There are a number of risks associated with the Certificate as described below.

In certain circumstances you may not realize a benefit from the Certificate.

|

· |

You may need to make Excess Withdrawals, which have the potential to substantially reduce or even terminate the benefits available under the Certificate. Because personal financial needs can arise unpredictably (e.g., unexpected medical bills), you may need to make a withdrawal from your

Covered Fund before the start of the GAW Phase or following the start of the GAW Phase in an amount larger than the GAW. These types of withdrawals are Excess Withdrawals that will reduce or eliminate the guarantee provided by the Certificate. There is no provision under the Certificate to cure any decrease in the benefits due to Excess Withdrawals. To avoid making Excess Withdrawals, you will need to carefully manage your withdrawals. The Certificate does not require us to warn

you of Excess Withdrawals or other actions with adverse consequences.

|

|

· |

You may choose to cancel your Certificate prior to a severe market downturn. The Certificate is designed to protect you from outliving the assets in your Covered Fund. If you terminate the Certificate before reaching the GAW Phase or Settlement Phase, we will not make payments

to you, even if subsequent Covered Fund performance reduces your Covered Fund Value to zero. |

|

· |

If you change the provider of your IRA, you may never receive a benefit from the Certificate. The Certificate is currently available to participants in certain IRAs. If your IRA moves to a provider that does not offer the Certificate, you may never receive a benefit from the

Certificate. The Guarantee Benefit Fee will not be refunded. |

|

· |

- 5 -

|

· |

The deduction of the Guarantee Benefit Fee each month will negatively affect the growth of your Covered Fund Value. The growth of your Covered Fund Value is likely important to you because you may never receive Installments during Settlement Phase. Therefore, depending on how long you

live and how your investments perform, you may be financially better off without purchasing the Certificate. |

|

· |

The Certificate limits your investment choices. Only certain funds are available under the Certificate. These Covered Funds may be managed in a more conservative fashion than other mutual funds available to you. If you do not purchase the Certificate, it is possible

that you may invest in other mutual funds (or other types of investments) that experience higher growth or lower losses, depending on the market, than the Covered Funds experience. It is impossible to know how various investments will fare on a comparative basis. |

|

· |

The Group Contract Owner may terminate the Group Contract upon 75 days written notice to us. If the Group Contract Owner terminates the Group Contract, then all benefits, rights, and privileges provided by the Group Contract, including without limitation, the Certificate, shall terminate. In

this event, you may choose to utilize the Covered Fund Value in the ways described later in this prospectus under “Termination of the Group Contract—If the Group Contract Owner Terminates the Group Contract.” The Guarantee Benefit Fee will not be refunded if the Group Contract Owner terminates the Group Contract. |

|

· |

We may terminate the Group Contract upon 75 days written notice to the Group Contract Owner. If we terminate the Group Contract, such termination will not adversely affect your rights under the Group Contract, except that we will not permit additional Certificate Contributions to the Covered Fund. However,

we will accept reinvested dividends and capital gains. The Guarantee Benefit Fee will not be refunded if we terminate the Group Contract. |

|

· |

The IRA may terminate. In the event of a complete IRA termination, then all benefits, rights, and privileges provided by the Group Contract, including without limitation, the Certificate, shall terminate. In this event, you may choose to utilize the Covered Fund Value in the ways described

later in this prospectus under “Termination of the Group Contract—Other Termination.” The Guarantee Benefit Fee will not be refunded if the IRA terminates. |

|

· |

Covered Funds may become ineligible. If the Covered Fund that you invest in becomes ineligible for the Certificate, you will be forced to transfer the Covered Fund Value to another Covered Fund. We reserve the right to designate Covered Funds that were previously eligible for

use with the Certificate as ineligible for use with the Certificate, for any reason including due to changes to their investment objectives. In the event that all Covered Funds become ineligible or if the Covered Funds are liquidated, the Certificate will be terminated. This will be considered a termination of the Certificate by Great-West and your rights under the Certificate will not be adversely affected, except that no additional

Certificate Contributions may be made. The Guarantee Benefit Fee will not be refunded if the Covered Funds become ineligible or are liquidated. |

Your receipt of payments from us is subject to our claims paying ability.

|

· |

Any payments we are required to make to you under the Certificate will depend on our long-term ability to make such payments. We will make all payments under the Certificate in Settlement Phase from our general account, which is not insulated from the claims of our third party creditors. Therefore,

your receipt of payments from us is subject to our claims paying ability. |

Currently, our financial strength is rated by three nationally recognized statistical rating organizations (“NRSRO”), ranging from superior to excellent to very strong. Our ratings reflect the NRSROs' opinions that we have a superior, excellent, or a very strong ability to meet our ongoing obligations. An

excellent and very strong rating means that we may have somewhat larger long-term risks than higher rated companies that may impair its ability to pay benefits payable on outstanding insurance policies on time. The financial strength ratings are the NRSROs' current opinions of our financial strength with respect to our ability to pay under our outstanding insurance policies according to their terms and the timeliness of payments. The NRSRO ratings are not specific to the Certificate.

- 6 -

You may obtain information on our financial condition by reviewing Form 10-K, which is the Annual Report we file with the Securities and Exchange Commission pursuant to Sections 13 and 15(d) of the Securities Exchange Act of 1934. Our Form 10-K for the fiscal year ended December 31, 2008, is incorporated herein by reference. For

further information, see “Financial Condition of the Company” later in this prospectus.

There may be tax consequences associated with the Certificate.

|

· |

The Certificate is novel and innovative and to date, the tax consequences of the Certificate have not been addressed in published legal authorities. You should consult a tax advisor before purchasing a Certificate. See “Taxation

of the Certificate” later in this prospectus for further discussion of tax issues relating to the Certificate. |

Other Information

|

· |

You should be aware of various regulatory protections that do and do not apply to the Certificate. Your Certificate is registered in accordance with the Securities Act of 1933. The issuance and sale of your Certificate must be conducted in accordance with the requirements of

the Securities Act of 1933. We are also subject to applicable periodic reporting requirements and other requirements imposed by the Securities Exchange Act of 1934. |

|

· |

We are neither an investment company nor an investment adviser and do not provide investment advice to you in connection with the Certificate. Therefore, we are not governed by the Investment Advisers Act of 1940 (the “Advisers Act”) or the Investment Company Act of 1940 (the “1940

Act”). Accordingly, the protections provided by the Advisers Act and the 1940 Act are not applicable with respect to our sale of the Certificate to you. |

The Certificate is a group fixed deferred annuity certificate. Certificates are offered only to IRA owners whose assets are invested in one or more Covered Funds. The Certificates are designed for IRA owners who intend to use the investments in the Covered Fund in their IRA as the basis for periodic withdrawals (such

as systematic withdrawal programs involving regular annual withdrawals of a certain percentage of the Covered Fund Value) to provide income payments for retirement or for other purposes. For more information about the Covered Funds, you should talk to your advisor and review the accompanying prospectuses for the Covered Funds.

Provided that specified conditions are met, the Certificate provides for a guaranteed income over the remaining life of the Certificate Owner (or, if these are joint Covered Persons, the remaining lives of both joint Covered Persons), should the Covered Fund Value equal zero as a result of GAWs, the Guarantee Benefit Fee, certain other fees

that are not directly associated with the Certificate or Group Contract (e.g., IRA fees, custodian fees, advisory fees), and/or Covered Fund performance.

The Certificate provides protection relating to your Covered Funds by ensuring that, regardless of how your Covered Fund(s) actually performs or the actual Covered Fund Value when you begin your GAWs for retirement or other purposes, you will receive predictable income payments for as long as you live so long as specified conditions are met.

- 7 -

Currently, you may elect to purchase the Certificate by completing the election form and purchasing one or more of the Covered Funds described below. For the SecureFoundation Lifetime Portfolios, you do not actually purchase the Certificate until the first Business Day of the year that is ten years prior to the date in the name

of the fund, which is known as the “Guarantee Trigger Date.” For example, if you purchase the Maxim SecureFoundationSM Lifetime 2055 Portfolio, you will not purchase the Certificate until January 3, 2045, you will not have any rights or benefits under the Certificate until January 3, 2045, and you will not be charged the Guarantee Benefit Fee until the end of January 2045. The Guarantee Trigger Date

is also your Certificate Election Date. You should note that the Company issues the Certificates, but the Company is not your investment adviser and does not provide investment advice to you in connection with the Certificate.

As described in more detail in the Covered Fund prospectuses, in addition to the Guarantee Benefit Fee, there are certain fees and charges associated with the Covered Funds, which may reduce your Covered Fund Value. These fees may include management fees, distribution fees, acquired fund fees and expenses, redemption fees, exchange

fees, advisory fees, and/or administrative fees.

The following information about the Covered Funds is only a summary of important information you should know. More detailed information about the Covered Funds’ investment strategies and risks are included in each Covered Fund’s prospectus. Please read that separate prospectus carefully before investing in

a Covered Fund.

The portfolio is designed for investors seeking a professionally designed asset allocation program to simplify the accumulation of assets prior to retirement together with the potential benefit of the guarantee provided by the Certificate. The portfolio strives to provide shareholders with a high level of diversification primarily

through both a professionally designed asset allocation model and professionally selected investments in underlying portfolios (the “Underlying Portfolios”). The intended benefit of asset allocation is diversification, which is expected to reduce volatility over the long-term.

The portfolio is a “fund of funds” that pursues its investment objective by investing in other mutual funds, including Underlying Portfolios that may or may not be affiliated with the Maxim SecureFoundationsm Balanced Portfolio, cash and cash equivalents.

The portfolio has two classes of shares, Class G shares and Class G1 shares. Each class is identical except that Class G1 shares have a distribution or “Rule 12b-1” plan. The distribution plan provides for a distribution fee. Because the distribution fee is paid out of Class G1’s assets

on an ongoing basis, over time these fees will increase the cost of your investment and may cost you more than paying other types of sales charges.

The portfolio seeks long-term capital appreciation and income.

The portfolio’s investment objective is non-fundamental and can be changed without shareholder approval.

Under normal conditions, the portfolio will invest 50-70% of its net assets (plus the amount of any borrowings for investment purposes) in Underlying Portfolios that invest primarily in equity securities and 30-50% of its net assets (plus the amount of any borrowings for investment purposes) in Underlying Portfolios that invest primarily in

fixed income securities.

- 8 -

There are five separate SecureFoundation Lifetime Portfolios. These are the:

Maxim SecureFoundationSM Lifetime 2015 Portfolio

Maxim SecureFoundationSM Lifetime 2025 Portfolio

Maxim SecureFoundationSM Lifetime 2035 Portfolio

Maxim SecureFoundationSM Lifetime 2045 Portfolio

Maxim SecureFoundationSM Lifetime 2055 Portfolio

Each SecureFoundation Lifetime Portfolio provides an asset allocation strategy and is designed to meet certain investment goals based on an investor’s investment horizon (such as projected retirement date) and personal objectives.

Each SecureFoundation Lifetime Portfolio is a “fund of funds” that pursues its investment objective by investing in other mutual funds, including mutual funds that may or may not be affiliated with the SecureFoundation Lifetime Portfolios (collectively, “Underlying Portfolios”), cash and cash equivalents. The

SecureFoundation Lifetime Portfolios use asset allocation strategies to allocate assets among the Underlying Portfolios.

The SecureFoundation Lifetime Portfolios have two classes of shares, Class G shares and Class G1 shares. Each class is identical except that Class G1 shares have a distribution or “Rule 12b-1” plan. The distribution plan provides for a distribution fee. Because the distribution fee is paid

out of Class G1’s assets on an ongoing basis, over time these fees will increase the cost of your investment and may cost you more than paying other types of sales charges.

Each SecureFoundation Lifetime Portfolio seeks long-term capital appreciation and income consistent with its current asset allocation.

Each SecureFoundation Lifetime Portfolio’s investment objective is non-fundamental and can be changed without shareholder approval.

Each SecureFoundation Lifetime Portfolio seeks to achieve its objective by investing in a professionally selected mix of Underlying Portfolios that is tailored for investors planning to retire in, or close to, the year designated in the name of the SecureFoundation Lifetime Portfolio. Depending on its proximity to the year designated in the name of the SecureFoundation Lifetime

Portfolio, each SecureFoundation Lifetime Portfolio employs a different combination of investments among different Underlying Portfolios in order to emphasize, as appropriate, growth, income, and/or preservation of capital. Over time until the Guarantee Trigger Date, each SecureFoundation Lifetime Portfolio’s asset allocation strategy will generally become more conservative, with greater emphasis on investments that provide for income and preservation of capital, and less on those offering the

potential for growth. Once a SecureFoundation Lifetime Portfolio reaches its Guarantee Trigger Date, the asset allocation between equity and fixed-income investments is anticipated to become relatively static, subject to any revisions to the asset classes, asset allocations, and Underlying Portfolios made by Maxim Capital Management, LLC. After its Guarantee Trigger Date, it is anticipated that each SecureFoundation Lifetime Portfolio will invest 50-70% of its net assets in Underlying Portfolios

that invest primarily in equity securities and 30-50% of its net assets in Underlying Portfolios that invest primarily in fixed income securities.

We may, without the consent of you or the Group Contract Owner, offer new Covered Fund(s) or cease offering Covered Fund(s). We will notify the Group Contract Owner whenever the Covered Fund(s) are changed. If we cease offering Covered Funds, then the Certificate Contributions that you made before we ceased offering such

Covered Funds will continue to

- 9 -

be covered by the Certificate, but we will not accept new Certificate Contributions. In the event that no Covered Funds are available, the Group Contract and the Certificate will be terminated. See “Termination of the Group Contract.”

You may fund your IRA with proceeds rolled over or directly transferred from a tax-deferred retirement plan established under Section 401(a), 403(a), 403(b), or 457(b) of the Code (“tax-deferred retirement plan”). If your rollover is from a tax-deferred retirement plan and you have previously elected a Great-West guaranteed lifetime withdrawal product as part of your

investments in your tax-deferred retirement plan, your Benefit Base will be equal to your Benefit Base as it existed under your prior tax-deferred retirement plan immediately prior to your rollover. Your new Benefit Base after the IRA rollover will only equal the Benefit Base you had under your tax-deferred retirement plan if you: (a) invest the rollover or transfer proceeds covered by the Great-West guaranteed lifetime withdrawal benefit product immediately prior to distribution from the

tax-deferred retirement plan in the Covered Fund(s); (b) invest in the same Covered Fund, except if the Certificate Owner is in Settlement Phase; and (c) you Request the restoration of the Benefit Base as it existed under your tax-deferred retirement plan. You will deemed to have made the request if you become an IRA owner as a result of a de minimis rollover, which means that you will not need to take any further action to request the prior Benefit Base that you had under your tax-deferred

retirement plan. To maintain the same Benefit Base, you must be in the same Phase that you were in at the time of the rollover or transfer after the rollover or transfer is complete.

As stated previously in this prospectus, the Certificate has three phases: an “Accumulation Phase,” “GAW Phase,” and “Settlement Phase.” The Accumulation Phase is described in the following section of this prospectus.

The Accumulation Phase is the period of time between the Certificate Election Date, which is the date your Certificate is issued by Great-West, and the first day of the GAW Phase. During this Phase, you will establish your Benefit Base which will be used later to determine the amount of your GAWs.

On your Certificate Election Date, the initial Benefit Base is calculated based on your initial Covered Fund Value. However, if your initial Certificate Contribution is a rollover from a tax deferred retirement plan, your Benefit Base may equal the benefit base you had under your tax deferred retirement plan. See IRA

Rollovers above for more information.

The initial Benefit Base is the sum of all Certificate Contributions made to the Covered Fund(s) on the Certificate Election Date. Certificate Contributions immediately increase your Benefit Base on a dollar-for-dollar basis.

A few things to keep in mind regarding the Benefit Base:

|

· |

The Benefit Base is used only for purposes of calculating your Installment Payments during the GAW Phase and the Settlement Phase. It has no other purpose. The Benefit Base does not provide and is not available as a cash value or settlement value. |

|

· |

It is important that you do not confuse your Benefit Base with the Covered Fund Value. |

- 10 -

|

· |

During the Accumulation Phase and the GAW Phase, the Benefit Base will be re-calculated on an annual basis as described below, which is known as your Ratchet Date. |

During the Accumulation Phase, you may make additional Certificate Contributions to the Covered Funds in addition to your initial Certificate Contribution. Subsequent Certificate Contributions can be made by cash deposit (subject to limitations under federal tax law), Transfers, or may include rollovers from other retirement accounts. Additional

Certificate Contributions may not be made after the Accumulation Phase ends.

All additional Certificate Contributions made after the Certificate Election Date will increase the Benefit Base dollar-for-dollar. Reinvested dividends, capital gains, and settlements from the Covered Fund(s) will not be considered Certificate Contributions for the purpose of calculating the Benefit Base. However, they

will increase the Covered Fund Value.

During the Accumulation Phase, the Benefit Base will be evaluated and, if necessary, adjusted on an annual basis. This is known as the Ratchet Date and it occurs on the anniversary of the Certificate Election Date. It is important to be aware that even though your Covered Fund Value may increase due to dividends, capital

gains, or settlements from the underlying Covered Fund, the Benefit base will not increase due to dividends, capital gains or settlements from the underlying Covered Fund until the next Ratchet Date. Unlike Covered Fund Value, your Benefit Base will never decrease solely due to negative Covered Fund performance.

On each Ratchet Date during the Accumulation Phase, the Benefit Base is automatically adjusted (“ratcheted”) to the greater of:

(a) the current Benefit Base; or

(b) the current Covered Fund Value.

|

Example of Ratchet Date Adjustments during the Accumulation Period

Assume the following:

Benefit Base on Certificate Election Date (of January 2, 2009) = $100,000

Covered Fund Value on Certificate Election Date= $100,000

Dividends and Capital Gains paid June 30, 2009 = $5,000

Covered Fund Value on June 30, 2009 = $105, 000

Benefit Base on June 30, 2009 = $100,000

No other Certificate Contributions, Dividends, or Capital Gains are paid to the Account for the rest of the year.

Covered Fund Value on January 2, 2010 = $105,000

So, because the Covered Fund Value is greater than the Benefit Base on the Ratchet Date (January 2, 2010), the Benefit Base is adjusted to $105,000 effective January 2, 2010.

|

Great-West reserves the right to refuse additional Certificate Contributions at any time and for any reason. If Great-West refuses additional Certificate Contributions, you will retain all other rights under the Certificate.

- 11 -

Because the Certificate is held in your IRA, you may make withdrawals or change your Account investments at any time and in any amount that you wish, subject to any federal tax limitations. During the Accumulation Phase, however, any withdrawals or Transfers from your Covered Fund Value will be categorized as Excess Withdrawals.

You should carefully consider the effect of an Excess Withdrawal on both the Benefit Base and the Covered Fund Value during the Accumulation Phase, as this may affect your future benefits under the Certificate. In the event you decide to take an Excess Withdrawal, as discussed below, your Covered Fund Value will be reduced dollar-for-dollar

in the amount of the Excess Withdrawal. The Benefit Base will be reduced by the ratio of the Covered Fund Value after the Excess Withdrawal reduction is applied. Accordingly, your Benefit Base could be reduced by more than the amount of the withdrawal.

|

Example of Effects of an Excess Withdrawal taken during the Accumulation Period

Assume the following:

Covered Fund Value before the Excess Withdrawal adjustment = $50,000

Benefit Base = $100,000

Excess Withdrawal amount: $10,000

So,

Covered Fund Value after adjustment= $50,000 - $10,000 = $40,000

Covered Fund Value adjustment = $40,000/$50,000 = 0.80

Adjusted Benefit Base = $100,000 x 0.80 = $80,000

|

A Distribution or Transfer during the Accumulation Phase is considered an Excess Withdrawal. An Excess Withdrawal will reduce your Benefit Base and Covered Fund Value. A Distribution occurs when money is paid to you from the Covered Fund Value. A Transfer occurs when you transfer money from a Covered Fund to another IRA investment. A Transfer will

occur even if you transfer money from one Covered Fund to a different Covered Fund in your IRA. If you Transfer any amount out of out of the Maxim SecureFoundationSM Balanced Portfolio or the SecureFoundation Lifetime Portfolios after the Guarantee Trigger Date, then you will be prohibited from making any Transfers into the same Covered Fund for at least ninety (90) calendar days.

Note: The Certificate does not require us to warn you or provide you with notice regarding potentially adverse consequences that may be associated with any withdrawals or other types of transactions involving your Covered Fund. You should carefully monitor your Covered Fund, any withdrawals from your Covered

Fund, and any changes to your Benefit Base. You may contact us at 1-866-317-6586 for information about your Benefit Base.

At the time of any partial or periodic Distribution, if the Covered Person is 55 years of age or older, you may elect to begin the GAW Phase (as described below) and begin receiving GAWs at that time. If you choose not to begin the GAW Phase, the Distribution will be treated as an Excess Withdrawal and will reduce your Covered Fund Value and your Benefit Base (as described above).

- 12 -

If the Covered Person is not yet 55 years old, then any partial or periodic Distribution will be treated as an Excess Withdrawal as described above.

Any Distribution made to satisfy any contribution limitation imposed under federal law will be considered an Excess Withdrawal at all times. You should consult a qualified tax advisor regarding contribution limits and other tax implications.

If a GLWB Elector dies during the Accumulation Phase, then we will terminate the Certificate and pay the Covered Fund Value to the Beneficiary in accordance with the terms of the IRA (unless an election is made by a Beneficiary that is the spouse of the GLWB Elector). A Beneficiary that is the spouse of the GLWB Elector may choose

either to:

|

· |

become a new GLWB Elector and maintain the deceased GLWB Elector’s current Benefit Base (or proportionate share if multiple Beneficiaries) as of the date of death; or |

|

· |

to establish a new Account with a new Benefit Base based on the current Covered Fund Value on the date of the deceased GLWB Elector’s death. |

In either situation, the spouse Beneficiary shall become a GLWB Elector and the Ratchet Date will be the date when his or her Account is established.

A Beneficiary who is not the spouse of the GLWB Elector cannot elect to maintain the current Benefit Base, but may elect to establish a new Account. The Benefit Base and Certificate Election Date will be based on the current Covered Fund Value on the date his or her Account is established.

To the extent to that the Beneficiary becomes a GLWB Elector, he or she will be subject to all terms and conditions of the Certificate, the IRA Contract, and the Code. Any election made by Beneficiary pursuant to this section is irrevocable.

The GAW Phase begins when you elect to receive GAWs under the Certificate. The GAW Phase continues until the Covered Fund Value reaches zero and the Settlement Phase begins.

The GAW Phase cannot begin until all Covered Persons attain age 55 and have a distributable event under the IRA and the Code. Installments will not begin until Great-West receives appropriate and satisfactory information about the age of the Covered Person(s) in good order and in manner reasonably satisfactory to Great-West.

In order to initiate the GAW Phase, you must submit a written Request to Great-West. At that time, you must provide sufficient documentation for Great-West to determine the age of each Covered Person.

Because the GAW Phase cannot begin until all Covered Persons under the Certificate attain age 55, any Distributions taken before then will be considered Excess Withdrawals and will be deducted from the Covered Fund Value and Benefit Base. See Accumulation Phase for

more information. No Certificate Contributions may be made to the Covered Fund(s) on and after the Initial Installment Date, which is the date that GAWs begin.

It is important that you understand how the GAW is calculated because it will affect the benefits you receive under the Certificate. Once the GAW Phase has been initiated and the age of the Covered Person(s) is verified, we will determine the amount of the GAW.

- 13 -

To determine the amount of the GAW, we will compare the current Benefit Base to the current Covered Fund Value on the Initial Installment Date. If the Covered Fund Value exceeds the Benefit Base, the Covered Fund Value will become the Benefit Base and the GAW will be based on that amount.

During the GAW Phase, your Benefit Base will receive an annual adjustment or “ratchet” just as it did during the Accumulation Phase. Your Ratchet Date will become the anniversary of Initial Installment Date and will no longer be the anniversary of the Certificate Election Date.

Just like the Accumulation Phase, the Benefit Base will be automatically adjusted on an annual basis, on the Ratchet Date, to the greater of:

(a) the current Benefit Base; or

(b) the current Covered Fund Value.

Your Benefit Base is used to calculate the GAW you receive. However, even though the Benefit Base is adjusted annually, your GAW% will not change unless

you request a Reset of the GAW%. See “The GAW Phase--Optional Resets of the GAW% During the GAW Phase” below.

It is important to note that Installments during the GAW Phase will reduce your Covered Fund Value on a dollar-for-dollar basis, but they will not reduce your Benefit Base.

The GAW% is based on the age of the Covered Person(s) at the time of the first Installment. If there are two Covered Persons the percentage is based on the age of the younger Covered Person.

The GAW is based on a percentage of the Benefit Base pursuant to the following schedule:

|

Sole Covered Person |

Joint Covered Person | |

|

4.0% for life at ages 55-64 |

3.25% for youngest joint life at ages 55-64 | |

|

5.0% for life at ages 65-69 |

4.25% for youngest joint life at ages 65-69 | |

|

6.0% for life at ages 70-79 |

5.25% for youngest joint life at ages 70-79 | |

|

7.0% for life at ages 80+ |

6.25% for youngest joint life at ages 80+ | |

The GAW will then be calculated by multiplying the Benefit Base by the GAW%. The amount of the Installment equals the GAW divided by the number of payments per year under the elected Installment Frequency Option, as described below.

- 14 -

|

Numerical Example of GAW Calculation

Assume the following:

Sole Covered Person

Age of Covered Person at Initial Installment Date: 60

Covered Fund Value = $120,000

Current Benefit Base = $115,000

Adjusted Benefit Base at Initial Installment Date = $120,000

GAW% based on Age = 4.0%

GAW% x (Adjusted Benefit Base) = 4.0% x $120,000 = $4,800

Installment Frequency = Monthly (12 payments per year)

So GAW/Installment Frequency = $4,800/12 = $400

The monthly Installment will be $400

|

|

Numerical Example of GAW Calculation, Joint Covered Persons

Assume the following:

Joint Covered Persons

Age of primary Covered Person at Initial Installment Date: 65

Age of joint Covered Person at Initial Installment Date: 58

Youngest Age for Determination of GAW: 58

Covered Fund Value = $120,000

Current Benefit Base = $115,000

Adjusted Benefit Base at Initial Installment Date = $120,000

GAW% based on Age = 3.25%

GAW% x (Adjusted Benefit Base) = 3.25% x $120,000 = $3,900

Installment Frequency = Monthly (12 payments per year)

So GAW/Installment Frequency = $3,900/12 = $325

The monthly Installment will be $325 |

Any election which affects the calculation of the GAW is irrevocable. Please consider all relevant factors when making an election to begin the GAW Phase. For example, an election to begin the receiving Installments based on a sole Covered Person

cannot subsequently be changed to joint Covered Persons once the GAW Phase has begun. Similarly, an election to receive Installments based on joint Covered Persons cannot subsequently be changed to a sole Covered Person.

Your Installment Frequency Options are as follows:

(a) Annual – the GAW will be paid on the Initial Installment Date and each anniversary annually, or next business day, thereafter.

(b) Semi-Annual – half of the GAW will be paid on the Initial Installment Date and in Installments every 6 month anniversary, or next business day, thereafter.

- 15 -

(c) Quarterly – one quarter of the GAW will be paid on the Initial Installment Date and in Installments every 3 month anniversary, or next business day, thereafter.

(d) Monthly – one-twelfth of the GAW will be paid on the Initial Installment Date and in Installments every monthly anniversary, or next business day, thereafter.

You may Request to change the Installment Frequency Option starting on each Ratchet Date during the GAW Phase.

At any time during the GAW Phase, if you are receiving Installments more frequently than annually, you may elect to take a lump sum Distribution up to the remaining scheduled amount of the GAW for that year.

|

Numerical Example of Lump Sum Distribution

GAW = $4,800 with a monthly distribution of $400

Three monthly Installments have been made (3 x $400 = $1,200)

Remaining GAW = GAW – paid Installments to date = $4,800 - $1,200 = $3,600

So, a Lump Sum Distribution of $3,600 may be taken.

|

It is your responsibility to Request the suspension of the remaining Installments that are scheduled to be paid during the year until the next Ratchet Date and to re-establish Installments upon the next Ratchet Date, if applicable. If you choose not to suspend the remaining Installments for the year, an Excess Withdrawal may occur. (See

- Effect of Excess Withdrawals During the GAW Phase described below).

After receiving a Lump Sum Distribution and suspending Installments, you must notify Great-West that you wish to recommence Installment payments for the next year. Great-West must receive notice 30 calendar days before the next Ratchet Date that you wish to recommence payments; otherwise, Great-West will not make any Installments. The

Ratchet Date will not change if Installments are suspended.

You may Request, on an annual basis, a Reset of the GAW% during the GAW Phase within thirty (30) calendar days prior to the Ratchet Date.

If requested, Great-West shall multiply the Covered Fund Value as of the Ratchet Date by the GAW% (based on your, or the younger joint Covered Person’s, Attained Age on the Ratchet Date) and determine if it is higher than the current Benefit Base multiplied by the current applicable

GAW%. If so, the current GAW% will change to the Attained Age GAW% and the Benefit Base will change to the current Covered Fund Value as of the Ratchet Date. If it does not, the Reset shall be void but a Ratchet may still occur. If the Reset takes effect, it will be effective on the Ratchet Date as the Ratchet Date does not change due to Reset.

- 16 -

| If |

(Attained Age GAW%) x (Covered Fund Value as of Ratchet Date) is greater than |

| (Current GAW%) x (Current Benefit Base) |

| Then | (Attained Age GAW%) x (Covered Fund Value as of Ratchet Date) becomes new GAW and |

| (Covered Fund Value) = (New Benefit Base) |

|

Numerical Example When Reset is Beneficial

Assume the following:

Age at Initial Installment Date: 60

Attained Age: 70

Covered Fund Value = $120,000

Current Benefit Base = $125,000

Current GAW% before Ratchet Date: 4%

Attained Age GAW% after Ratchet Date: 6%

(Current GAW%) x (Current Benefit Base) = 4% x $125,000 = $5,000

(Attained Age GAW%) x (Covered Fund Value) = 6% x $120,000 = $7,200

So New GAW Amount is $7,200

New Benefit Base is $120,000

New GAW% is 6%

|

|

Numerical Example When Reset is NOT Beneficial

Assume the following:

Age at Initial Installment Date: 60

Attained Age: 70

Covered Fund Value = $75,000

Current Benefit Base = $125,000

Current GAW% before Ratchet: 4%

Attained Age GAW% after Ratchet Date: 6%

(Current GAW %) x (Current Benefit Base) = 4% x $125,000 = $5,000

(Attained age withdrawal %) x (Covered Fund Value) = 6% x $75,000 = $4,500

So, because $4,500 is less than current GAW of $5,000, no Reset occurs.

|

- 17 -

After the Initial Installment Date, a Distribution or Transfer that is greater than the GAW will be considered an Excess Withdrawal. The Benefit Base will be adjusted by the ratio of the new Covered Fund Value (after the Excess Withdrawal) to the previous Covered Fund Value (after the GAW).

If an Excess Withdrawal occurs, the GAW and current Benefit Base will be adjusted on the next Ratchet Date.

|

Numerical Example Effect of Excess Withdrawals During the GAW Phase

Assume the following:

Covered Fund Value before GAW = $55,000

Benefit Base = $100,000

GAW%: 5%

GAW Amount = $100,000 x 5% = $5,000

Total annual withdrawal: $10,000

So,

Excess Withdrawal = $10,000 – $5,000 = $5,000

Covered Fund Value after GAW = $55,000 – $5,000 = $50,000

Covered Fund Value after Excess Withdrawal = $50,000 – $5,000 = $45,000

Covered Fund Value Adjustment due to Excess Withdrawal = $45,000/$50,000 = 0.90

Adjusted Benefit Base = $100,000 x 0.90 = $90,000

Adjusted GAW Amount (assuming no Benefit Base increase on succeeding Ratchet Date) = $90,000 x 5% = $4,500

|

Note: The Certificate does not require us to warn you or provide you with notice regarding potentially adverse consequences that may be associated with any withdrawals or other types of transactions involving your Covered Fund. You should carefully monitor your Covered Fund, any withdrawals from your Covered

Fund, and any changes to your Benefit Base. You may contact us at 1-866-317-6586 for information about your Benefit Base.

If you die after the Initial Installment date without a joint Covered Person, the Certificate will terminate and no further Installments will be paid. The remaining Covered Fund Value shall be distributed to the Beneficiaries in accordance with the IRA. If permitted by the IRA and the Code, the GLWB Elector’s Beneficiary

may elect to become an Owner in which event an initial Benefit Base shall be established and he or she will be subject to all terms and conditions of the Certificate, the IRA Contract and the Code. This will be a new Certificate Election Date. Any election made by the Beneficiary is irrevocable.

Upon your death after the Initial Installment Date, and while the joint Covered Person is still living, the joint Covered Person/Beneficiary may elect to become an Owner (if permitted by the IRA and the Code) and he or she will acquire all rights under the Certificate and continue to receive GAW Installments based on your original election. Installments

may continue to be paid to the surviving Covered Person based on the GAW% for joint Covered Persons as described above.

- 18 -

Installments will continue to be paid to the surviving Covered Person until his or her death and the surviving Covered Person’s beneficiary will receive any remaining Covered Fund Value on the date of death. Alternatively, he or she may elect to receive his or her portion of the Covered Fund Value on the date of death as a

lump sum Distribution or can separately elect to become an Owner and will be subject to all terms and conditions of the Certificate, the IRA Contract and the Code. If the surviving Covered Person elects to separately become an Owner, the date of the election will be the new Ratchet Date.

|

Any election made by the Beneficiary is irrevocable. |

The Settlement Phase begins when the Covered Fund Value has reduced to zero as a result of negative Covered Fund performance, the Guarantee Benefit Fee, certain other fees that are not directly associated with the Certificate or Group Contract (e.g., IRA fees, custodian fees, advisory

fees), and/or GAWs, but the Benefit Base is still positive. It is also important to understand that the Settlement Phase is the first time that we use our own money to make Installments to you. During the GAW Phase, the GAWs are made first from your own investment.

Installments continue for your life under the terms of the Certificate, but all other rights and benefits under the Certificate will terminate. Installments will continue in the same frequency as previously elected, and cannot be changed during the Settlement Phase. Distributions and Transfers are not permitted during

the Settlement Phase.

During the Settlement Phase, the Guarantee Benefit Fee will not be deducted from the Certificate or from the Installments.

When the last Covered Person dies during the Settlement Phase, the Certificate will terminate and no Installments will be paid to the Beneficiary.

A note about the examples:

|

§ |

All Certificate Contributions are assumed to be at the end of the year and occur immediately before the next Ratchet Date. |

|

§ |

All withdrawals are assumed to be at the beginning of the year and occur on the Ratchet Date. |

|

§ |

All positive investment performance of the Covered Fund is assumed to be net of investment management fees. |

|

§ |

In all of the examples, we have assumed that you have access to your Covered Fund Value until it is depleted: |

|

o |

If you die before the Covered Fund Value is depleted, the remaining Covered Fund Value would be available to your Beneficiary. |

|

o |

If you need to take a withdrawal in excess of your GAW, you may take up to the Covered Fund Value, which will be considered an Excess Withdrawal. |

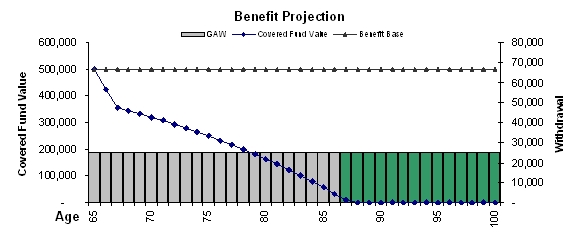

Example 1 – Basic: Assume you buy the Certificate at age 65 and start taking GAWs in annual Installments immediately. Also, assume that the Covered Fund Value (net of investment management fees) decreases by 10% in the first two years and increases by 5% every year thereafter.

Details:

|

§ |

Sole Covered Person |

|

§ |

Initial Covered Fund Value: $500,000 |

|

§ |

GAW Percent: 5% |

|

§ |

GAW Amount: $500,000 x 5% = $25,000 |

|

§ |

Guarantee Benefit Fee: 0.90% |

|

§ |

Changes in Covered Fund Value (net of investment management fees): |

|

o |

Year 1: -10%, Year 2: -10%, Years 3+: 5% |

- 19 -

Result:

|

§ |

You annually withdraw $25,000 from your Covered Fund until about age 87 when the Covered Fund is depleted: |

|

o |

At age 87 your Covered Fund Value is $9,474. |

|

o |

You withdraw the $9,474 which depletes the Covered Fund and you are now in Settlement Phase. |

|

o |

We provide the remaining $15,526 necessary to make the Installment of $25,000. |

|

§ |

We continue to pay Installments of $25,000 each year for your life. |

Illustration:

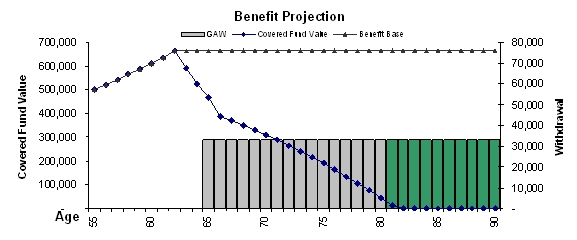

Example 2 – Ratchet: Assume you buy the Certificate at age 55 and start taking GAWs in annual Installments at age 65. Also, assume that the Covered Fund Value (net of investment management fees) increases by 5% in years 1 through 7, decreases by 10% in years 8 through

11, and increases by 5% thereafter.

Details:

| § | Sole Covered Person |

| § | Initial Covered Fund Value: $500,000 |

| § | GAW Percent: 5% |

| ▪ | Guarantee Benefit Fee: 0.90% |

| § | Changes in Covered Fund Value (net of investment management fees): |

|

o |

Years 1 through 7: 5%, Years 8 through 11: -10%, Years 12+: 5% |

Result:

|

§ |

Positive Covered Fund performance through year 7 results in a Covered Fund Value of $662,407 on your Ratchet Date. |

|

§ |

Your Benefit Base Ratchets to $662,407. |

|

§ |

Covered Fund Value at the beginning of year 10 is $468,552, but GAWs are based on the Benefit Base, which is $662,407. |

|

o |

GAWs are $662,407 x 5% = $33,120. |

|

§ |

You annually withdraw $33,120 from your Covered Fund until about age 81 when the Covered Fund is depleted: |

|

o |

At age 81, your Covered Fund Value is $13,326. |

|

o |

You withdraw the $13,326 which depletes the Covered Fund and you are now in Settlement Phase. We provide the remaining $19,794 necessary to make the Installment $33,120. |

|

§ |

We continue to pay Installments of $33,120 each year for your life. |

- 20 -

Illustration:

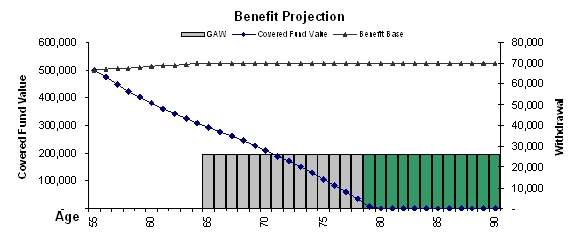

Example 3 – Additional Certificate Contributions: Assume you buy the Certificate at age 55 and you make annual Certificate Contributions of $2,500 until you start taking GAWs in annual Installments at age 65. Also, assume that the Covered Fund Value (net of investment management fees) decreases by 5% in years 1 through 10 and increases by 5% thereafter.

Details:

|

§ |

Sole Covered Person |

|

§ |

Initial Covered Fund Value: $500,000 |

|

§ |

Additional Annual Certificate Contributions until GAWs Begin: $2,500 |

|

§ |

GAW Percent: 5% |

|

§ |

Guarantee Benefit Fee: 0.90% |

|

§ |

Changes in Covered Fund Value (net of investment management fees): |

|

o |

Years 1 through 10: -5%, Years 11+: 5% |

Result:

|

§ |

Poor Covered Fund performance in years 1 through 10 results in a Covered Fund Value of $291,493 at the end of year 10. |

|

§ |

Your Benefit Base at the end of year 10 is $525,000 as a result of the additional Certificate Contributions in years 1 through 10. |

|

o |

GAWs are $525,000 x 5% = $26,250. |

|

§ |

You annually withdraw $26,250 from your Covered Fund until about age 79 when the Covered Fund is depleted: |

|

o |

At age 79, your Covered Fund Value is $8,316. |

|

o |

You withdraw the $8,316 which depletes the Covered Fund and you are now in Settlement Phase. We provide the remaining $17,934 necessary to make the Installment $26,250. |

|

§ |

We continue to pay Installments of $26,250 each year for your life. |

- 21 -

Illustration:

After you purchase your Certificate, you are required to pay the Guarantee Benefit Fee. The Guarantee Benefit Fee is set forth in your Certificate, and is based on the dollar amount of your Covered Fund Value. The Guarantee Benefit Fee will be deducted monthly as a separate charge from your Covered Fund and will be paid

by redeeming the number of fund shares of your Covered Fund(s) equal to the Guarantee Benefit Fee. We will collect the fee on a monthly basis in arrears. We reserve the right to change the frequency of the deduction, but will notify you in writing at least thirty (30) days prior to the change. Because your Benefit Base may not exceed $5,000,000, we will not charge the Guarantee Benefit on an amount of your Covered Fund Value that exceeds $5,000,000.

Currently the Guarantee Benefit Fee is 0.90% and is subject to a minimum of 0.70% and a maximum of 1.50%. This is the guaranteed maximum or minimum Guarantee Benefit Fee we can ever charge for your Certificate. We may change the current fee at any time within the minimum and maximum range described below upon thirty (30)

days written notice to you. Changing the Guarantee Benefit Fee is solely in our discretion. We do not need the happening of any event before we may change the Guarantee Benefit Fee.

The Guarantee Benefit Fee is in addition to any charges that are imposed in connection with advisory, custodial, and other services, and charges imposed by the mutual funds in which you invest.

|

Example of how the Guarantee Benefit Fee is Computed

Date: 1/31/2010

Covered Fund Value = $100,000

Benefit Base = $125,000

Guarantee Benefit Fee = 0.90% x Covered Fund Value / 12

Guarantee Benefit Fee = 0.90% x $100,000 / 12 = $75.00

|

The Guarantee Benefit Fee compensates us for the costs and risks we assume for providing the Certificate (including marketing, administration, and profit).

If we do not receive the Guarantee Benefit Fee (except during Settlement Phase), the Certificate will terminate as of the date that the fee is due.

- 22 -

Because the amount (in dollars) you pay us for the Guarantee Benefit Fee varies based in part on your Covered Fund Value, it will likely change from month-to-month. Only if your Covered Fund Value multiplied by the Guarantee Benefit Fee percentage is exactly the same amount (in dollars) every month will your actual fee remain constant.

|

Example 1: Declining Covered Fund Value results in declining Guarantee Benefit Fee

Date: 1/31/2010

Covered Fund Value = $100,000

Benefit Base = $125,000

Guarantee Benefit Fee = 0.90% x Covered Fund Value / 12

Guarantee Benefit Fee = 0.90% x $100,000 / 12 = $75.00

Date: 2/28/2010

Covered Fund Value = $90,000

Benefit Base = $125,000

Guarantee Benefit Fee = 0.90% x Covered Fund Value / 12

Guarantee Benefit Fee = 0.90% x $90,000 / 12 = $67.50

Note: in this example, the Guarantee Benefit Fee declined because the Covered Fund Value declined. This could be the result of negative Covered Fund performance.

|

|

Example 2: Increasing Covered Fund Value results in increasing Guarantee Benefit Fee

Date: 1/31/2010

Covered Fund Value = $100,000

Benefit Base = $125,000

Guarantee Benefit Fee = 0.90% x Covered Fund Value / 12

Guarantee Benefit Fee = 0.90% x $100,000 / 12 = $75.00

Date: 2/28/2010

Covered Fund Value = $120,000

Benefit Base = $125,000

Guarantee Benefit Fee = 0.90% x Covered Fund Value / 12

Guarantee Benefit Fee = 0.90% x $120,000 / 12 = $90.00

Note: in this example, the Guarantee Benefit Fee increased because the Covered Fund Value increased. This could be the result of several factors including positive Covered Fund performance, Transfers, or Certificate Contributions.

|

In the event of a divorce whose decree affects a Certificate, we will require written notice of the divorce in a manner acceptable to us and a copy of the applicable Qualified Domestic Relations Order (“QDRO”). A QDRO is a domestic relations order that creates or recognizes the existence of an Alternate Payee’s

right to receive all or a portion of the benefits payable with respect to a GLWB Elector. A QDRO may also assign an Alternate Payee the right to receive these benefits.

Depending on which phase the Certificate is in when we receive the QDRO, the benefits of the Certificate will be altered to comply with the QDRO. The Alternate Payee under the QDRO may make certain elections during the Accumulation or GAW Phases. Any elections made by the Alternate Payee are irrevocable To

the extent that an Alternate Payee becomes a GLWB Elector, he or she will be subject to all terms and conditions of the Certificate, the IRA Contract and the Code.

Great-West will make payment to the Alternate Payee and/or establish an Account on behalf of the Alternate Payee named in a QDRO approved during the Accumulation Phase. The Alternate Payee is responsible for submitting a Request to begin Distributions in accordance with the Code.

If the Alternate Payee is the GLWB Elector’s spouse during the Accumulation Phase, he or she may elect to become a GLWB Elector, either by:

|

(i) |

maintaining the current Benefit Base of the previous GLWB Elector; or |

|

(ii) |

establishing a new Benefit Base based on the current Covered Fund Value on the date his or her Account is established and he or she will continue as a GLWB Elector. |

If the Alternate Payee elects to maintain the current Benefit Base, the Benefit Base and the Covered Fund Value will be divided between the GLWB Elector and the Alternate Payee. The Covered Fund Value will be divided pursuant to the terms of the QDRO. The Benefit Base will be divided in the same proportion as the

Covered Fund Value.

In either situation, the Alternate Payee’s Certificate Election Date shall be the date the Account is established.

A non-spouse Alternate Payee cannot elect to maintain the current Benefit Base, or proportionate share, but may elect to establish a new GLWB. The Benefit Base and Certificate Election Date will be based on the current Covered Fund Value on the date his or her Account is established. Any election made by an Alternate Payee described

in this section is irrevocable.

Great-West will make payment to the Alternate Payee and/or establish an Account on behalf of the Alternate Payee named in a QDRO approved during the GAW Phase. The Alternate Payee is responsible for submitting a Request to begin Distributions in accordance with the Code.

Pursuant to the instructions in the QDRO, the Benefit Base and GAW will be divided in the same proportion as their respective Covered Fund Values as of the effective date of the QDRO. The GLWB Elector may continue to receive the proportional GAWs after the accounts are split. If the Alternate Payee is the GLWB Elector’s

spouse, he or she may elect to receive his or her portion of the Covered Fund Value as a lump sum Distribution or can separately elect to become a GLWB Elector.

- 24 -

Pursuant to the instructions in the QDRO, the Benefit Base and GAW will be divided in the same proportion as their respective Covered Fund Values as of the effective date of the QDRO. The GLWB Elector may continue to receive the proportional GAWs after the accounts are split, based on the amounts calculated pursuant to the joint

Covered Person GAW%.

If the Alternate Payee is the GLWB Elector’s spouse, he or she may elect to receive his or her portion of the Covered Fund Value as a lump sum Distribution or can separately elect to continue proportionate GAWs in the GAW Phase based on the amounts calculated pursuant to the joint Covered Persons GAW%, described in the GAW

Phase – Calculation of Installment, after the accounts are split. A new Ratchet Date will be established for the Alternate Payee on the date the Accounts are split. Within thirty (30) days of each person’s Ratchet Date, the GLWB Elector and Alternate Payee can each elect a Reset based on the person’s own Attained Age GAW% for joint Covered Persons.

In the alternative, the Alternate Payee may establish a new GLWB in the Accumulation Phase with the Benefit Base based on the current Covered Fund Value on the date his or her Account is established.

A non-spouse Alternate Payee cannot elect to maintain the current Benefit Base or GAW but may elect to establish a new GLWB. The Benefit Base and Certificate Election Date will be based on the current Covered Fund Value on the date his or her Account is established. Any election made by an Alternate Payee described in this section

is irrevocable.

If a Request in connection with a QDRO is approved during the Settlement Phase, Great-West will divide the Installment pursuant to the terms of the QDRO. Installments will continue pursuant to the lives of each payee.

If you elect to annuitize, if permitted by the IRA, prior to the Initial Installment Date, the Certificate will terminate for those Covered Fund assets and the Guarantee Benefit Fee will not be refunded. If, based upon information provided by the Certificate Owner, the GLWB Elector is entitled to a Distribution under the applicable terms and provisions of the IRA and the Code sections

governing the IRA, all or a portion of an Account may be applied to an annuity payment option selected by the GLWB Elector, so long as the requirements of the Code are met. Thereafter, the Certificate shall no longer be applicable with respect to amounts in the annuity payment option.

The amount to be applied to an annuity payment option is: (i) the portion of the Account value elected by GLWB Elector, less (ii) Applicable Tax, if any, less (iii) any fees and charges described in the Certificate. The minimum amount that may be applied under the elected annuity option is $5,000. If any payments to be

made under the elected annuity payment option will be less than $50, Great-West may make the payments in the most frequent interval that produces a payment of at least $50.

Great-West will issue a certificate or other statement setting forth in substance the benefits, rights, and privileges to which such person is entitled under the Group Contract, to each Annuitant describing the benefits payable under the elected annuity payment option.

An Annuitant is required to elect an annuity payment option. The Annuitant must Request an annuity payment option or change an annuity payment option no later than 30 days prior to the Annuity Commencement Date elected by the GLWB Elector.

- 25 -

To the extent available under the IRA, the annuity payment options are:

|

· |

Income for Single Life Only |

|

· |

Income for Single Life with Guaranteed Period |

|

· |

Income for Joint Life Only |

|

· |

Income for Joint Life with Guaranteed Period |

|

· |

Income for a Specific Period |

|

· |

Any other form of annuity payment permitted under the IRA, if acceptable to Great-West. |

The annuity option that will always be available is the Income for Single Life Only Annuity. If this annuity option is elected, Great-West will make payments to the Annuitant at a frequency specified in the annuity certificate or other statement for the duration of the Annuitant’s lifetime. Payments will cease pursuant

to the terms of the certificate or other statement.

Annuity purchase rates will be the same rates that are available for a Single Premium Immediate Annuity currently offered by Great-West at the time of annuitization.

The Certificate may be terminated if the Group Contract is terminated.