Attached files

| file | filename |

|---|---|

| 8-K - Colfax CORP | v166530_8k.htm |

Investor Presentation

November 16, 2009

The following information contains forward-looking statements, including forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking

statements include, but are not limited to, statements concerning Colfax's plans, objectives, expectations and intentions and other statements that are not historical or current facts. Forward- looking statements are based on Colfax's

current expectations and involve risks and uncertainties that could cause actual results to differ materially from those expressed or implied in such forward-looking statements. Factors that could cause Colfax's results to differ materially

from current expectations include, but are not limited to factors detailed in Colfax's reports filed with the U.S. Securities and Exchange Commission as well as its Annual Report on Form 10-K under the caption “Risk Factors”. In

addition, these statements are based on a number of assumptions that are subject to change. This presentation speaks only as of this date. Colfax disclaims any duty to update the information herein.

Forward-Looking Statements

1

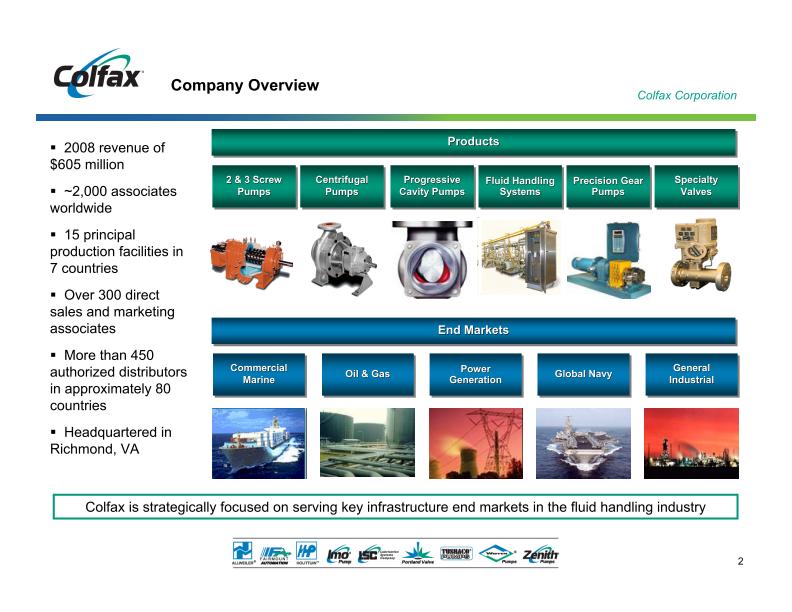

2008 revenue of $605 million

~2,000 associates worldwide

15 principal production facilities in 7 countries

Over 300 direct sales and marketing associates

More than 450 authorized distributors in approximately 80 countries

Headquartered in Richmond, VA

Colfax is strategically focused on serving key infrastructure end markets in the fluid handling industry

2 & 3 Screw

Pumps

Centrifugal

Pumps

Progressive

Cavity Pumps

Precision Gear Pumps

Specialty

Valves

Fluid Handling Systems

End Markets

Products

Global Navy

General

Industrial

Commercial

Marine

Oil & Gas

Power Generation

Company Overview

2

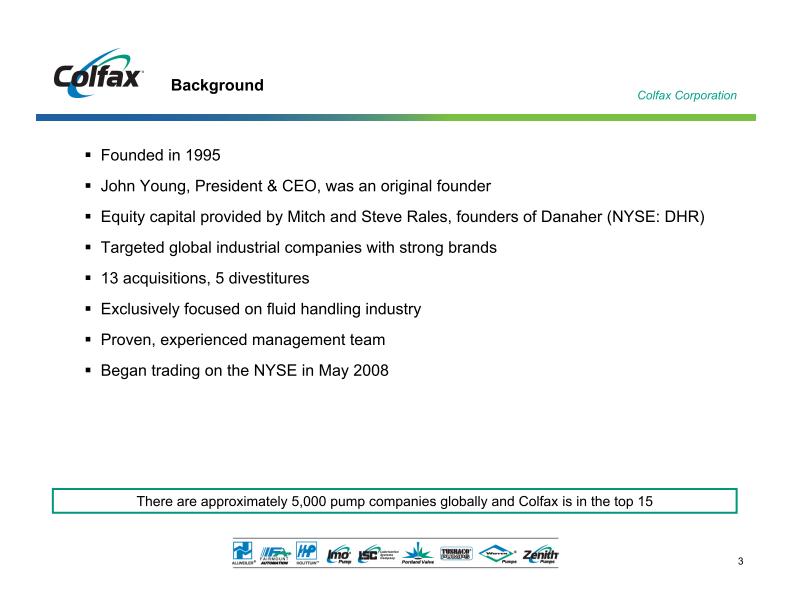

Founded in 1995

John Young, President & CEO, was an original founder

Equity capital provided by Mitch and Steve Rales, founders of Danaher (NYSE: DHR)

Targeted global industrial companies with strong brands

13 acquisitions, 5 divestitures

Exclusively focused on fluid handling industry

Proven, experienced management team

Began trading on the NYSE in May 2008

There are approximately 5,000 pump companies globally and Colfax is in the top 15

Background

3

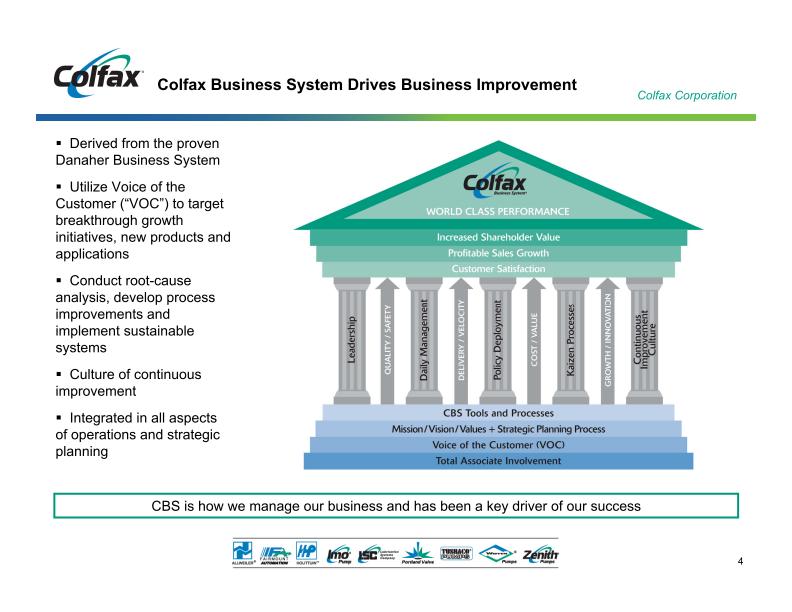

Derived from the proven Danaher Business System

Utilize Voice of the Customer (“VOC”) to target breakthrough growth initiatives, new products and applications

Conduct root-cause analysis, develop process improvements and implement sustainable systems

Culture of continuous improvement

Integrated in all aspects of operations and strategic planning

CBS is how we manage our business and has been a key driver of our success

Colfax Business System Drives Business Improvement

4

Global leader in specialty fluid handling products

Proven application expertise in solving critical customer needs

Serving growing global infrastructure driven end markets

Leading brand names generating aftermarket sales and services

Experienced management team in place to grow organically and through strategic acquisition

Strong financial position

Significant insider ownership

Consistent track record of driving profitable organic sales growth

Investment Highlights

5

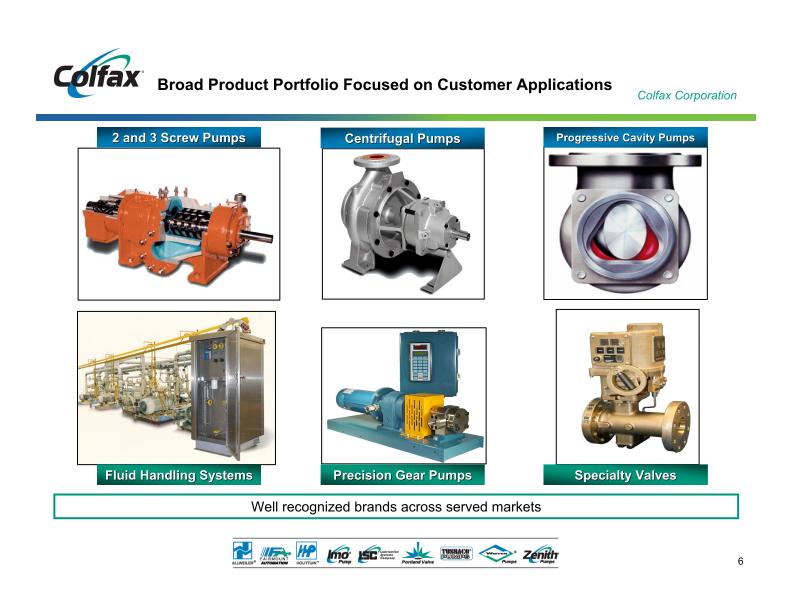

2 and 3 Screw Pumps

Well recognized brands across served markets

Fluid Handling Systems

Precision Gear Pumps

Progressive Cavity Pumps

Specialty Valves

Centrifugal Pumps

Broad Product Portfolio Focused on Customer Applications

6

7

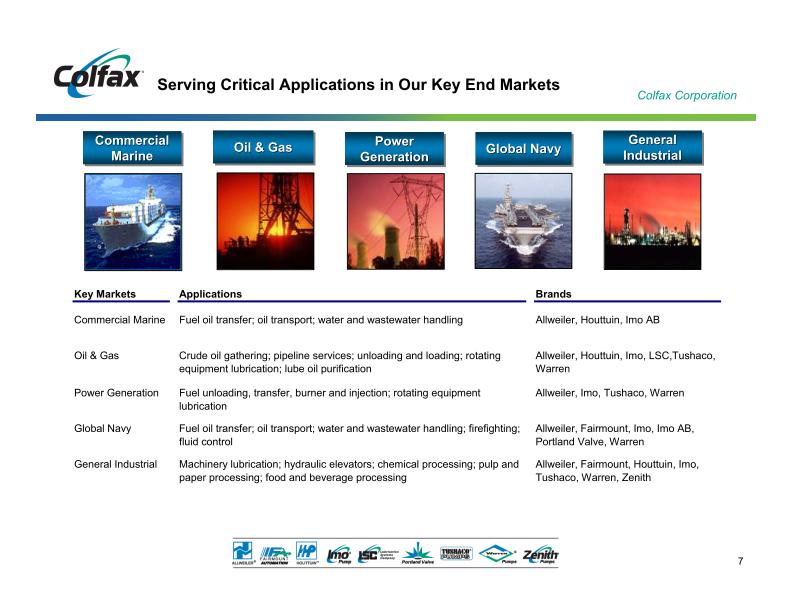

Commercial Marine

Serving Critical Applications in Our Key End Markets

General Industrial

Power Generation

Oil & Gas

Global Navy

Key Markets

Applications

Brands

Commercial

Marine

Fuel oil transfer; oil transport; water and wastewater handling

Allweiler,

Houttuin

,

I

mo

AB

Oil & Gas

Crude oil gathering; pipeline services; unloading and loading; rotating

equipment lubrication; lube oi

l purification

Allweiler, Houttuin,

Imo,

LSC,

Tushaco

,

Warren

Power Generation

Fuel unloading, transfer, burner and injection; rotating equipment

lubrication

Allweiler, Imo,

Tushaco

, Warren

Global

Navy

Fuel oil transfer; oil transport; water and wastewate

r handling; firefighting;

fluid control

Allweiler,

Fairmount,

I

mo

,

I

m

o

AB,

Portland

Valve,

Warren

General Industrial

Machinery lubrication; hydraulic elevators; chemical processing; pulp and

paper processing; food and beverage processing

Allweiler,

Fairm

ount,

Houttuin,

I

mo

,

Tushaco

, Warren,

Zenith

Key Markets

Applications

Brands

Commercial

Marine

Fuel oil transfer; oil transport; water and wastewater handling

Allweiler,

Houttuin

,

I

mo

AB

Oil & Gas

Crude oil gathering; pipeline services; unloading and loading; rotating

equipment lubrication; lube oi

l purification

Allweiler, Houttuin,

Imo,

LSC,

Tushaco

,

Warren

Power Generation

Fuel unloading, transfer, burner and injection; rotating equipment

lubrication

Allweiler, Imo,

Tushaco

, Warren

Global

Navy

Fuel oil transfer; oil transport; water and wastewate

r handling; firefighting;

fluid control

Allweiler,

Fairmount,

I

mo

,

I

m

o

AB,

Portland

Valve,

Warren

General Industrial

Machinery lubrication; hydraulic elevators; chemical processing; pulp and

paper processing; food and beverage processing

Allweiler,

Fairm

ount,

Houttuin,

I

mo

,

Tushaco

, Warren,

Zenith

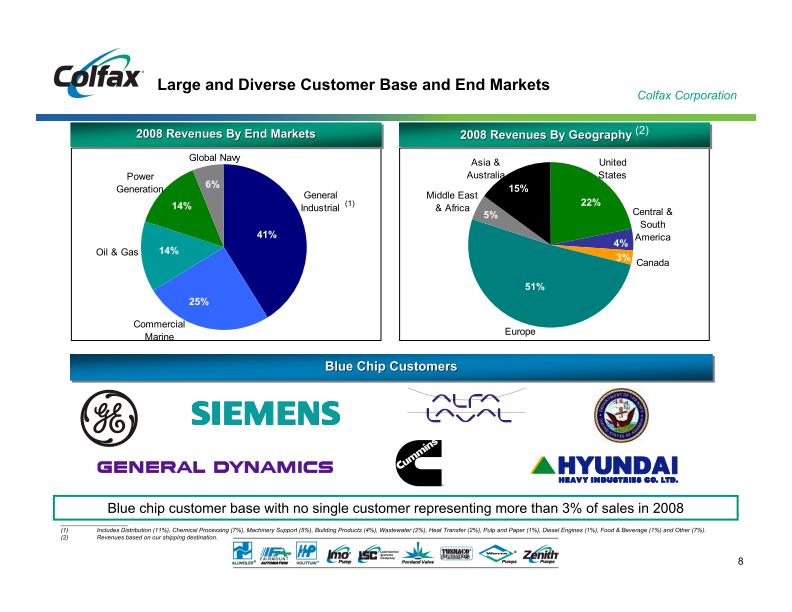

Large and Diverse Customer Base and End Markets

Blue Chip Customers

(2)

2008 Revenues By End Markets

3%

4%

15%

5%

51%

22%

(1)

6%

14%

14%

25%

41%

____________________

(1) Includes Distribution (11%), Chemical Processing (7%), Machinery Support (5%), Building Products (4%), Wastewater (2%), Heat Transfer (2%), Pulp and Paper (1%), Diesel Engines (1%), Food & Beverage (1%) and Other (7%).

(2) Revenues based on our shipping destination. Blue chip customer base with no single customer representing more than 3% of sales in 2008 Global Navy Marine Commercial Oil & Gas Industrial General Generation Power Asia & Australia Europe United States Canada Central & South America Middle East & Africa 8

EMEA

= $338mm

____________________

(1) Sales figures reflect sales destination.

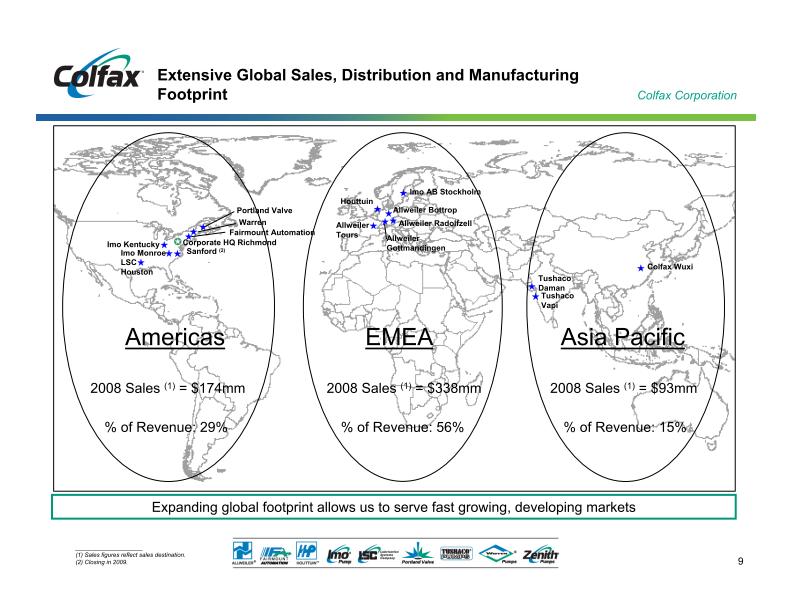

(2) Closing in 2009. Americas = $174mm % of Revenue: 29% % of Revenue: 56% % of Revenue: 15% LSC Houston Warren Corporate HQ Richmond Imo Kentucky Imo Monroe (2) Houttuin Tushaco Vapi Tushaco Daman Colfax Wuxi Imo AB Stockholm Allweiler Gottmandingen Portland Valve Allweiler Tours Allweiler Radolfzell Allweiler Bottrop Fairmount Automation Expanding global footprint allows us to serve fast growing, developing markets Extensive Global Sales, Distribution and Manufacturing Footprint Asia Pacific = $93mm 9

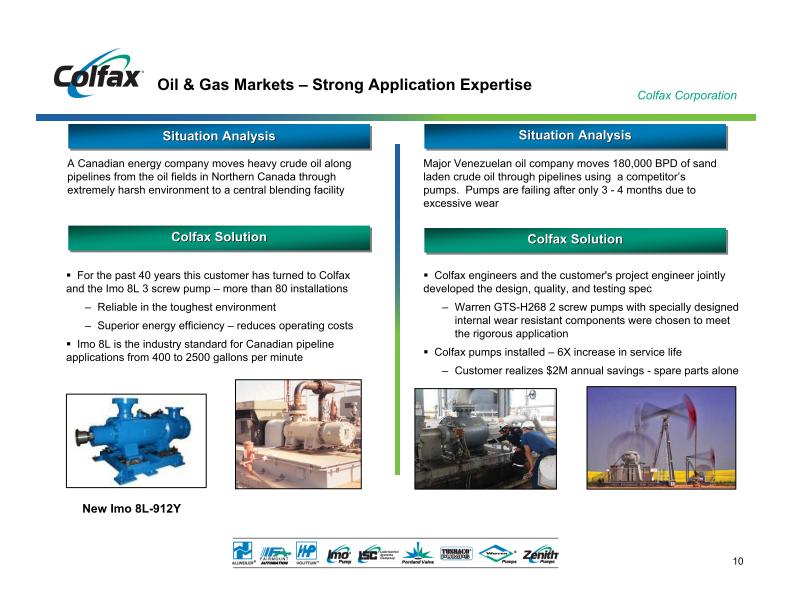

Situation Analysis

A Canadian energy company moves heavy crude oil along pipelines from the oil fields in Northern Canada through extremely harsh environment to a central blending facility

Colfax engineers and the customer's project engineer jointly developed the design, quality, and testing spec

Warren GTS-H268 2 screw pumps with specially designed internal wear resistant components were chosen to meet the rigorous application

Colfax pumps installed – 6X increase in service life

Colfax Solution

Situation Analysis

Major Venezuelan oil company moves 180,000 BPD of sand laden crude oil through pipelines using a competitor’s pumps. Pumps are failing after only 3 - 4 months due to excessive

wear

Colfax Solution

For the past 40 years this customer has turned to Colfax and the Imo 8L 3 screw pump – more than 80 installations

Reliable in the toughest environment

Superior energy efficiency – reduces operating costs

Imo 8L is the industry standard for Canadian pipeline applications from 400 to 2500 gallons per minute

Oil & Gas Markets – Strong Application Expertise

New Imo 8L-912Y

10

Expansion of Systems Business

Situation Analysis

A major Japanese OEM turbine manufacturer wanted to reduce installation time required at power plant construction sites. Initial focus - integrate components associated with the fuel filter,

pump and motor system.

Colfax Solution

Enhanced design, reduced costs

Initial system delivered in 2009, others on order

Global installations

Integrated system is now the standard fuel injection system design for this major turbine OEM customer

Situation Analysis

Colfax Solution

Americas region OEM and end-user customers need turn-key solutions – not just pumps.

Colfax Americas Engineered Systems business started in 2007 to address need for highly engineered systems

Services offered include: custom engineered skid packages or module subassemblies, fabrication, testing, and start up/commissioning

2009 forecast - $10M incremental sales

Environmentally-friendly module with internal, submersible lubricant pump and motor

11

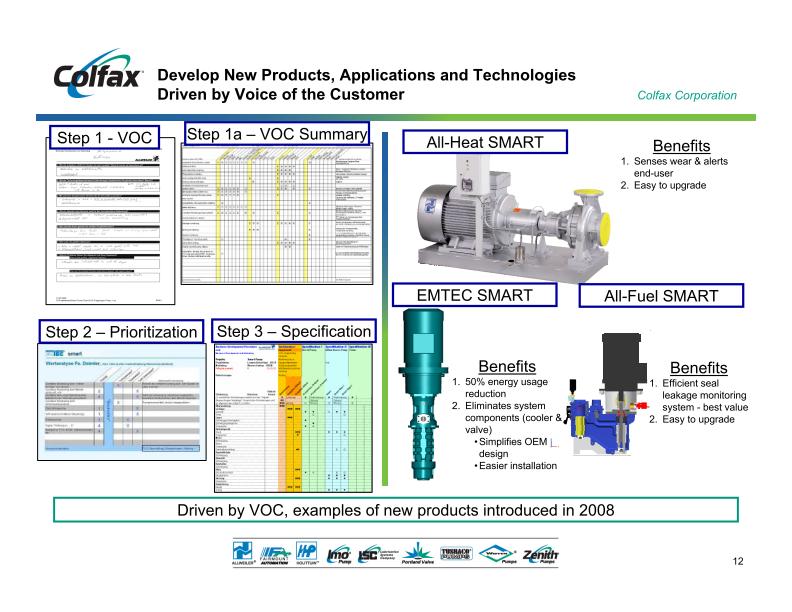

Driven by VOC, examples of new products introduced in 2008

Develop New Products, Applications and Technologies Driven by Voice of the Customer

Step 1 - VOC

Step 1a – VOC Summary

Step 2 – Prioritization

Step 3 – Specification

All-Heat SMART

EMTEC SMART

Benefits

1. Senses wear & alerts end-user

2. Easy to upgrade Benefits

1. 50% energy usage reduction

2. Eliminates system components (cooler & valve) Simplifies OEM design Easier installation All-Fuel SMART

1. Efficient seal leakage monitoring system - best value

2. Easy to upgrade 12

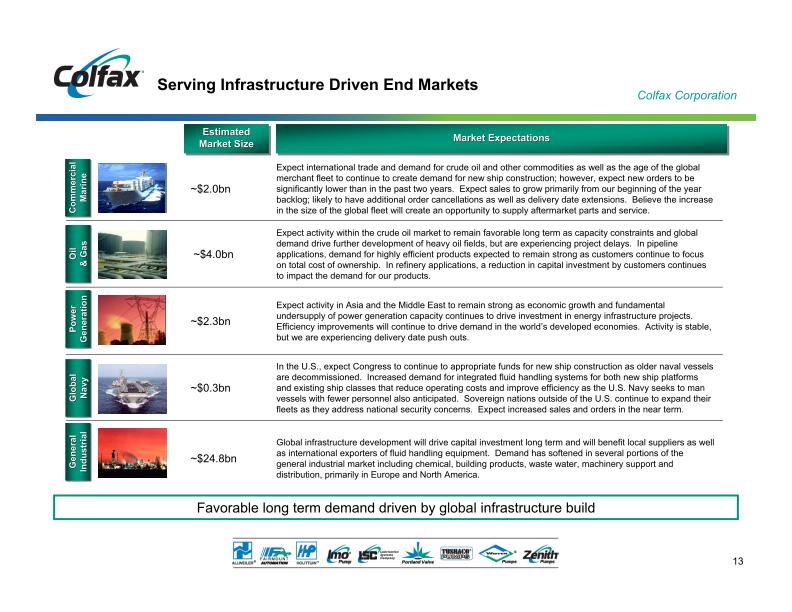

~$24.8bn

~$0.3bn

~$2.3bn

~$4.0bn

~$2.0bn

Global infrastructure development will drive capital investment long term and will benefit local suppliers as well as international exporters of fluid handling equipment. Demand has softened in several

portions of the general industrial market including chemical, building products, waste water, machinery support and distribution, primarily in Europe and North America.

In the U.S., expect Congress to continue to appropriate funds for new ship construction as older naval vessels are decommissioned. Increased demand for integrated fluid handling systems for both

new ship platforms and existing ship classes that reduce operating costs and improve efficiency as the U.S. Navy seeks to man vessels with fewer personnel also anticipated. Sovereign

nations outside of the U.S. continue to expand their fleets as they address national security concerns. Expect increased sales and orders in the near term.

Expect activity in Asia and the Middle East to remain strong as economic growth and fundamental undersupply of power generation capacity continues to drive investment in energy infrastructure projects. Efficiency

improvements will continue to drive demand in the world’s developed economies. Activity is stable, but we are experiencing delivery date push outs.

Expect activity within the crude oil market to remain favorable long term as capacity constraints and global demand drive further development of heavy oil fields, but are experiencing project delays. In

pipeline applications, demand for highly efficient products expected to remain strong as customers continue to focus on total cost of ownership. In refinery applications, a reduction in capital investment by customers continues to impact

the demand for our products.

Expect international trade and demand for crude oil and other commodities as well as the age of the global merchant fleet to continue to create demand for new ship construction; however, expect new orders to

be significantly lower than in the past two years. Expect sales to grow primarily from our beginning of the year backlog; likely to have additional order cancellations as well as delivery date extensions. Believe the increase in

the size of the global fleet will create an opportunity to supply aftermarket parts and service.

Estimated

Market Size

Favorable long term demand driven by global infrastructure build

Market Expectations

Serving Infrastructure Driven End Markets

13

Capitalize on growth opportunities by offering regionally developed products and solutions

Standard packages of Imo and Allweiler products produced at our Greenfield, Wuxi China facility for Commercial Marine

Continue to invest in sales and marketing capabilities to more effectively serve local Asia Pacific markets

Opened Defense Centre of Excellence in Mumbai to serve defense industry in the region

Leverage application expertise to design fluid handling solutions that cater to heavy crude oil exploration in Latin America, Middle East and Russia

Opened sales and engineering office in Bahrain in March

Utilize Indian / Chinese low cost manufacturing to supply components to other Colfax business units

Execute acquisitions

Assam, India

Shanghai, China

Target Fast Growing Regions

14

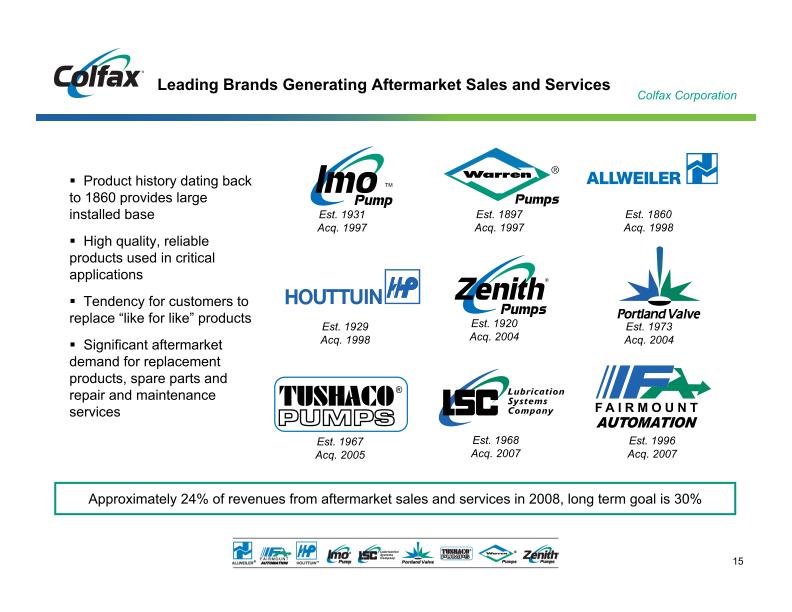

Est. 1860

Acq. 1998

Est. 1897

Acq. 1997

Est. 1929

Acq. 1998

Est. 1931

Acq. 1997

Est. 1973

Acq. 2004

Est. 1920

Acq. 2004

Est. 1967

Acq. 2005

Est. 1968

Acq. 2007

Est. 1996

Acq. 2007

Product history dating back to 1860 provides large installed base

High quality, reliable products used in critical applications

Tendency for customers to replace “like for like” products

Significant aftermarket demand for replacement products, spare parts and repair and maintenance services

Approximately 24% of revenues from aftermarket sales and services in 2008, long term goal is 30%

Leading Brands Generating Aftermarket Sales and Services

15

Continue to proactively engage with highly strategic targets

Product, market and geographically focused searches

Evaluate opportunistic bolt-on companies

Pursue adjacent fluid handling acquisitions

Effective selection and integration of 13 acquisitions since 1995

Acquisition Criteria

Acquisition Initiatives

Acquire companies in the fluid handling industry

Strong brand name recognition

Leading market position

Differentiated product technology / highly engineered product

Complementary end market / geographic focus

year

Continue to Pursue Strategic Acquisitions that Complement Our Platform

16

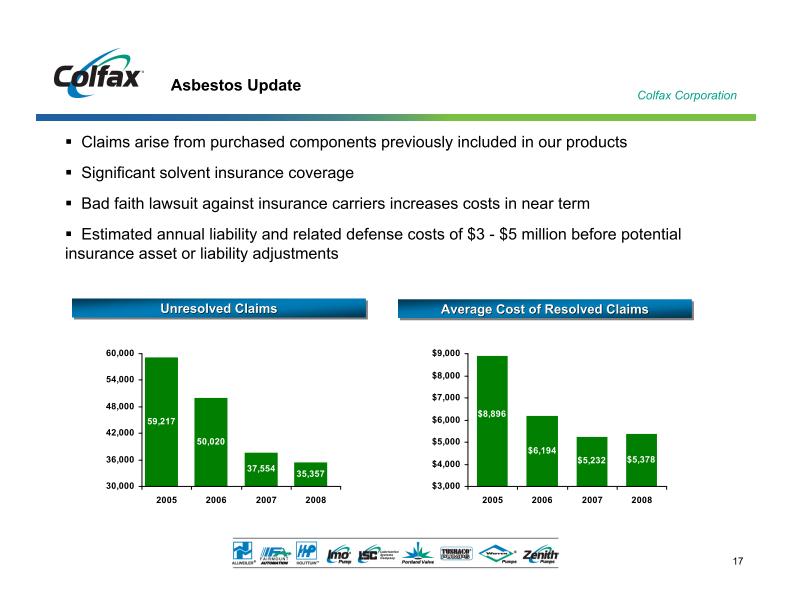

Claims arise from purchased components previously included in our products

Significant solvent insurance coverage

Bad faith lawsuit against insurance carriers increases costs in near term

Estimated annual liability and related defense costs of $3 - $5 million before potential insurance asset or liability adjustments

Asbestos Update

2008

2007

2006

2005

60,000

54,000

48,000

42,000

36,000

30,000

35,357

37,554

50,020

59,217

Average Cost of Resolved Claims

Unresolved Claims

$6,194

$5,378

$5,232

$8,896

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

2005

2006

2007

2008

17

Financial Overview

18

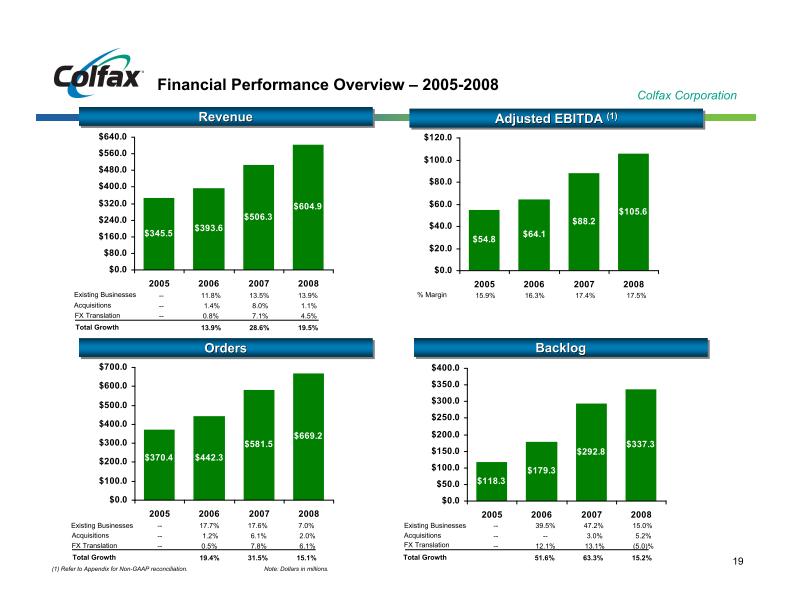

Financial Performance Overview – 2005-2008

2008

2007

2006

2005

$400.0

$350.0

$300.0

$250.0

$200.0

$150.0

$100.0

$50.0

$0.0

$337.3

$292.8

$179.3

$118.3

$54.8

$64.1

$88.2

$105.6

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

2005

2006

2007

2008

Backlog

$345.5

$393.6

$506.3

$604.9

$0.0

$80.0

$160.0

$240.0

$320.0

$400.0

$480.0

$560.0

$640.0

2005

2006

2007

2008

% Margin

15.9%

16.3%

17.4%

17.5%

(1)

Total Growth

31.5%

15.1%

Existing Businesses

19.4%

17.6%

7.0%

Acquisitions

6.1%

2.0%

FX Translation

7.8%

6.1%

--

--

--

17.7%

1.2%

0.5%

Total Growth

63.3%

15.2%

Existing Businesses

51.6%

47.2%

15.0%

Acquisitions

3.0%

5.2%

FX Translation

13.1%

(5.0)%

--

--

--

39.5%

--

12.1%

Total Growth

28.6%

19.5%

Existing Businesses

13.9%

13.5%

13.9%

Acquisitions

8.0%

1.1%

FX Translation

7.1%

4.5%

--

--

--

11.8%

1.4%

0.8%

Orders

(1) Refer to Appendix for Non-GAAP reconciliation. Note: Dollars in millions.

Revenue

$442.3

$581.5

$669.2

$370.4

$0.0

$100.0

$200.0

$300.0

$400.0

$500.0

$600.0

$700.0

2005

2006

2007

2008

19

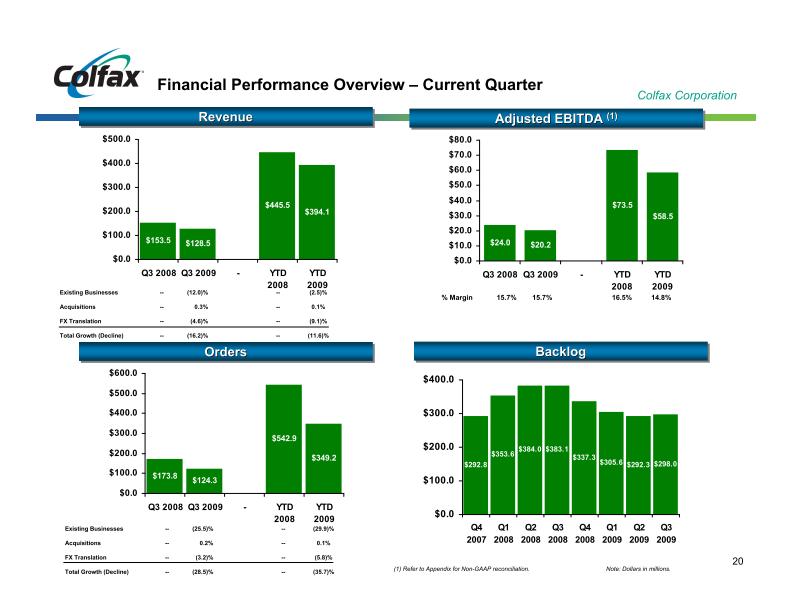

Financial Performance Overview – Current Quarter

0.1%

--

0.2%

--

Acquisitions

(28.5)%

(3.2)%

(25.5)%

(35.7)%

--

--

Total Growth (Decline)

(5.8)%

--

--

FX Translation

(29.9)%

--

--

Existing Businesses

2009

YTD

2008

YTD

-

Q3 2009

Q3 2008

$600.0

$500.0

$400.0

$300.0

$200.0

$100.0

$0.0

$349.2

$542.9

$124.3

$173.8

14.8%

16.5%

15.7%

15.7%

% Margin

(1)

Backlog

Orders

(1) Refer to Appendix for Non-GAAP reconciliation. Note: Dollars in millions.

Revenue

0.1%

--

0.3%

--

Acquisitions

(16.2)%

(4.6)%

(12.0)%

(11.6)%

--

--

Total Growth (Decline)

(9.1)%

--

--

FX Translation

(2.5)%

--

--

Existing Businesses

2009

Q3

2009

Q2

2009

Q1

2008

Q4

2008

Q3

2008

Q2

2008

Q1

2007

Q4

$400.0

$300.0

$200.0

$100.0

$0.0

$298.0

$292.3

$305.6

$337.3

$383.1

$384.0

$353.6

$292.8

2009

YTD

2008

YTD

-

Q3 2009

Q3 2008

$500.0

$400.0

$300.0

$200.0

$100.0

$0.0

$394.1

$445.5

$128.5

$153.5

$24.0

$20.2

$73.5

$58.5

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

$80.0

Q3 2008

Q3 2009

-

YTD

2008

YTD

2009

20

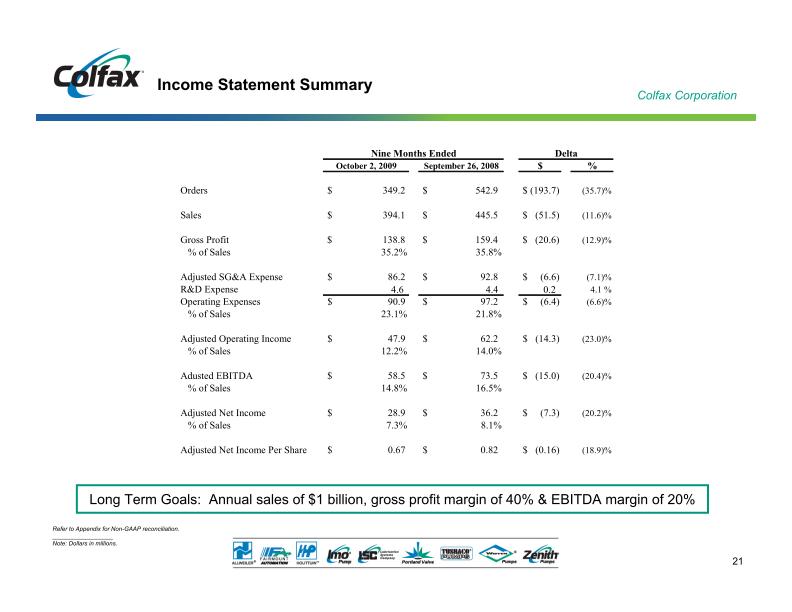

Income Statement Summary

Refer to Appendix for Non-GAAP reconciliation.

__________________

Note: Dollars in millions.

Long Term Goals: Annual sales of $1 billion, gross profit margin of 40% & EBITDA margin of 20%

Delta

October 2, 2009

September 26, 2008

$

%

Orders

$ 349.2

$ 542.9

$ (193.7)

(35.7)%

Sales

$ 394.1

$ 445.5

$ (51.5)

(11.6)%

Gross Profit

$ 138.8

$ 159.4

$ (20.6)

(12.9)%

% of Sales

35.2%

35.8%

Adjusted SG&A Expense

$ 86.2

$ 92.8

$ (6.6)

(7.1)%

R&D Expense

4.6

4.4

0.2

4.1 %

Operating Expenses

$ 90.9

$ 97.2

$ (6.4)

(6.6)%

% of Sales

23.1%

21.8%

Adjusted Operating Income

$ 47.9

$ 62.2

$ (14.3)

(23.0)%

% of Sales

12.2%

14.0%

Adusted EBITDA

$ 58.5

$ 73.5

$ (15.0)

(20.4)%

% of Sales

14.8%

16.5%

Adjusted Net Income

$ 28.9

$ 36.2

$ (7.3)

(20.2)%

% of Sales

7.3%

8.1%

Adjusted Net Income Per Share

$ 0.67

$ 0.82

$ (0.16)

(18.9)%

Nine Months Ended

21

____________________

Note: Dollars in millions.

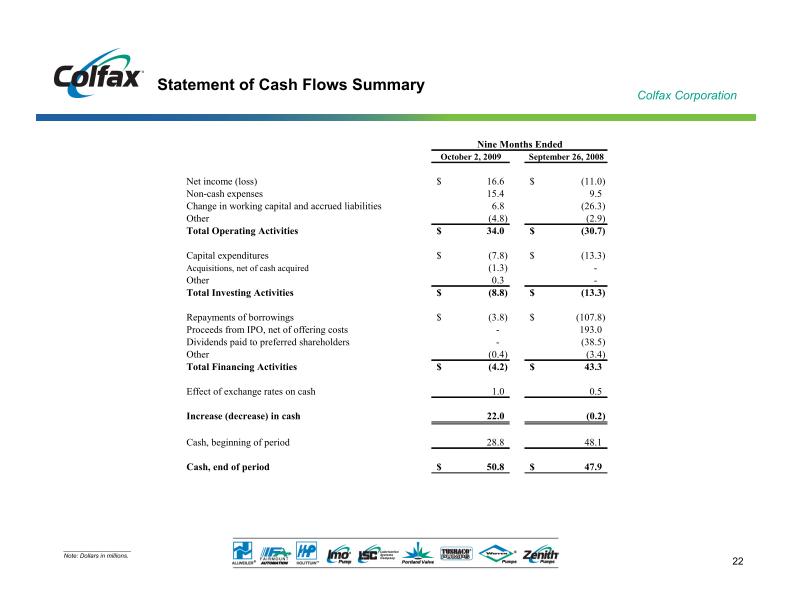

Statement of Cash Flows Summary

October 2, 2009

September 26, 2008

Net income (loss)

16.6

$

(11.0)

$

Non-cash expenses

15.4

9.5

Change in working capital and accrued liabilities

6.8

(26.3)

Other

(4.8)

(2.9)

Total Operating Activities

34.0

$

(30.7)

$

Capital expenditures

(7.8)

$

(13.3)

$

Acquisitions, net of cash acquired

(1.3)

-

Other

0.3

-

Total Investing Activities

(8.8)

$

(13.3)

$

Repayments of borrowings

(3.8)

$

(107.8)

$

Proceeds from IPO, net of offering costs

-

193.0

Dividends paid to preferred shareholders

-

(38.5)

Other

(0.4)

(3.4)

Total Financing Activities

(4.2)

$

43.3

$

Effect of exchange rates on cash

1.0

0.5

Increase (decrease) in cash

22.0

(0.2)

Cash, beginning of period

28.8

48.1

Cash, end of period

50.8

$

47.9

$

Nine Months Ended

22

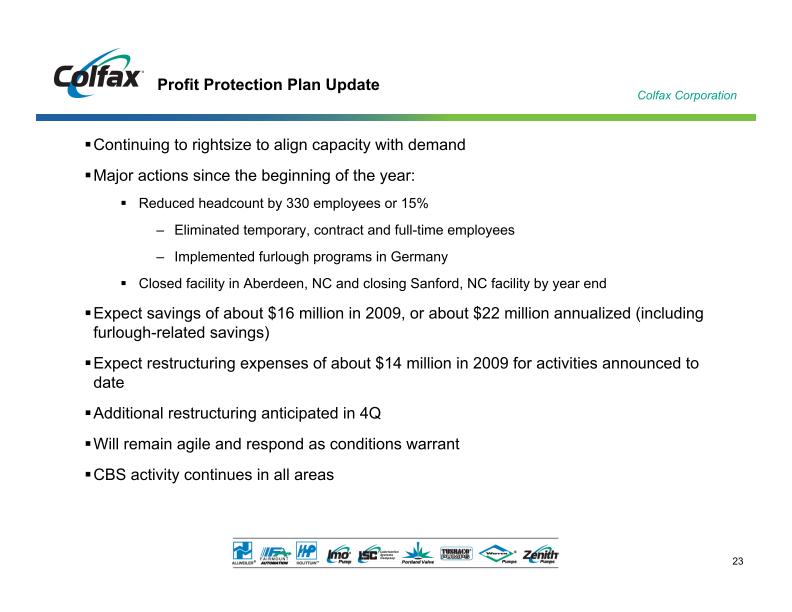

Continuing to rightsize to align capacity with demand

Major actions since the beginning of the year:

Reduced headcount by 330 employees or 15%

Eliminated temporary, contract and full-time employees

Implemented furlough programs in Germany

Closed facility in Aberdeen, NC and closing Sanford, NC facility by year end

Expect savings of about $16 million in 2009, or about $22 million annualized (including furlough-related savings)

Expect restructuring expenses of about $14 million in 2009 for activities announced to date

Additional restructuring anticipated in 4Q

Will remain agile and respond as conditions warrant

CBS activity continues in all areas

Profit Protection Plan Update

23

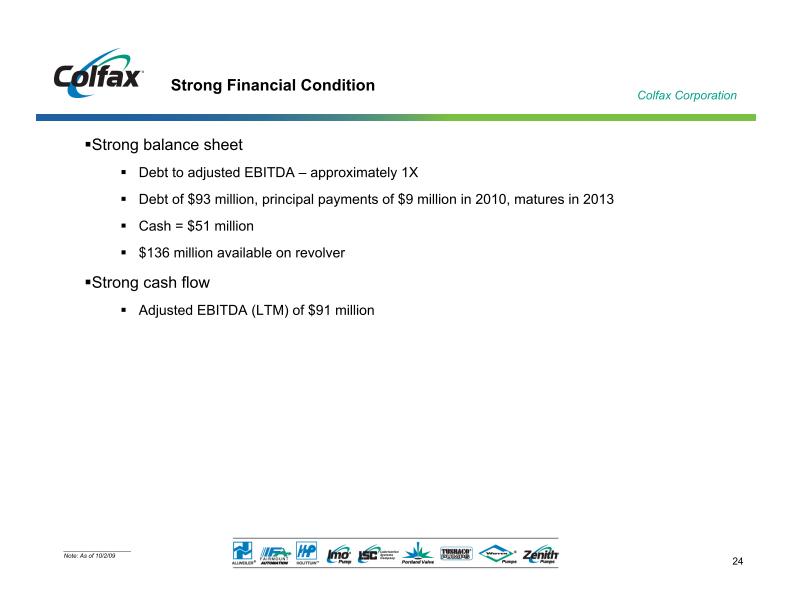

Strong balance sheet

Debt to adjusted EBITDA – approximately 1X

Debt of $93 million, principal payments of $9 million in 2010, matures in 2013

Cash = $51 million

$136 million available on revolver

Strong cash flow

Adjusted EBITDA (LTM) of $91 million

Strong Financial Condition

____________________

Note: As of 10/2/09

24

Well Positioned for the Future

Leading Brand Names Generating Aftermarket

Sales and Services

Experienced Management Team in Place to Grow Organically and Through Strategic Acquisitions

Global Leader in Specialty Fluid Handling Products

Proven Application

Expertise in Solving

Critical Customer Needs

Serving

Growing Infrastructure

Driven End Markets

CBS-Driven Culture Focused on Profitable Sales Growth

25

Appendix

26

Adjusted net income, adjusted net income per share, adjusted operating income and adjusted EBITDA exclude asbestos liability and defense costs (income) and asbestos coverage litigation expenses, certain

legacy legal charges, restructuring and other related charges, certain due diligence costs, certain other post-employment benefit settlement, cross currency swap, environmental indemnification and discontinued operations expense (income), as well as

one time initial public offering-related costs to the extent they impact the periods presented. Adjusted selling, general and administrative expenses exclude legacy legal adjustments and certain due diligence costs. Adjusted net income also

reflects interest expense as if the initial public offering (IPO) had occurred at the beginning of 2007 and presents income taxes at an effective tax rate of 32% in 2009 and 34% in 2008. Adjusted net income per share in 2008 assumes the 44,006,026 shares

outstanding at the closing of the IPO to be outstanding since January 1, 2007. Organic sales growth (decline) and organic order growth (decline) exclude the impact of foreign exchange rate fluctuations and acquisitions. These non-GAAP

financial measures assist Colfax in comparing its operating performance on a consistent basis because, among other things, they remove the impact of changes in our capital structure and asset base, non-recurring items such as IPO-related costs, legacy

asbestos issues (except in the case of EBITDA) and items outside the control of its operating management team.

Sales and order information by end market are estimates. We periodically update our customer groupings in order to refine these estimates. During 2009, reclassifications of previously

reported amounts were made to conform to current period presentation. No changes have been made to total sales or orders.

Disclaimer

27

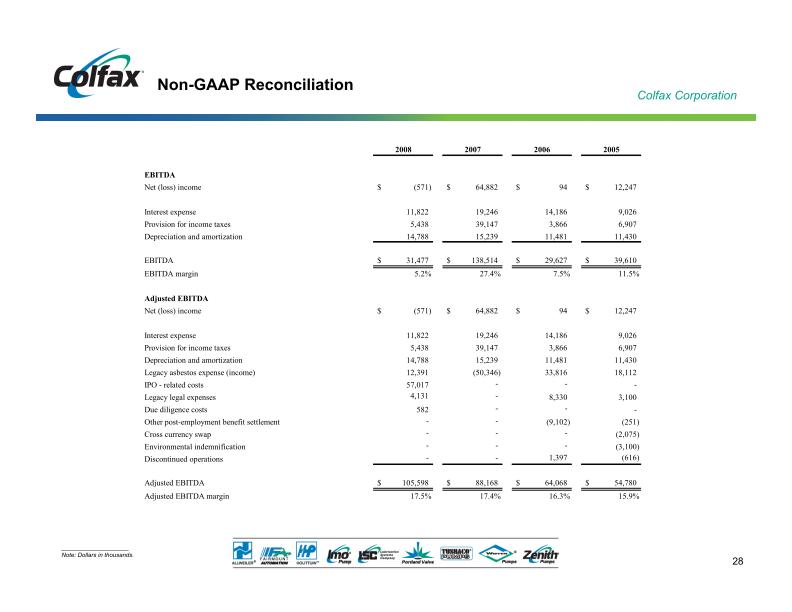

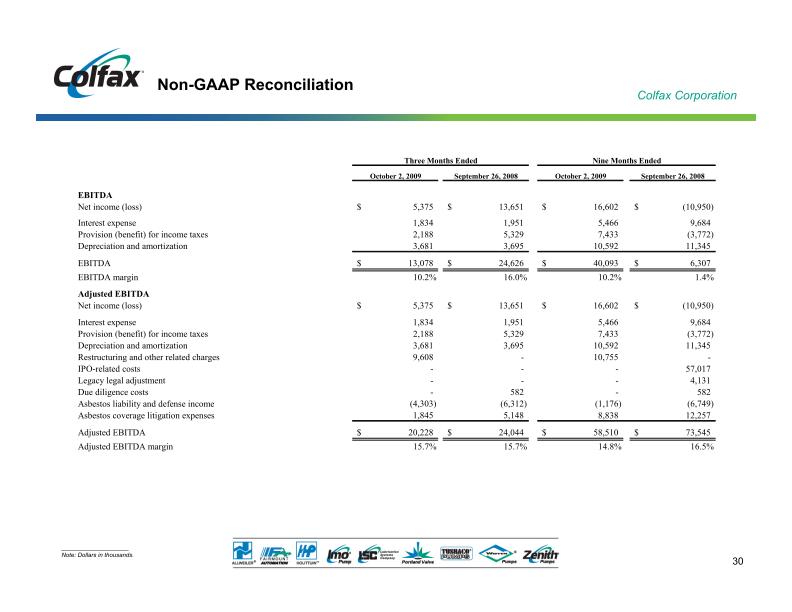

Non-GAAP Reconciliation

____________________

Note: Dollars in thousands.

2008

2007

2006

2005

EBITDA

Net (loss) income

(571)

$

64,882

$

94

$

12,247

$

Interest expense

11,822

19,246

14,186

9,026

Provision for income taxes

5,438

39,147

3,866

6,907

Depreciation and amortization

14,788

15,239

11,481

11,430

EBITDA

31,477

$

138,514

$

29,627

$

39,610

$

EBITDA margin

5.2%

27.4%

7.5%

11.5%

Adjusted EBITDA

Net (loss) income

(571)

$

64,882

$

94

$

12,247

$

Interest expense

11,822

19,246

14,186

9,026

Provision for income taxes

5,438

39,147

3,866

6,907

Depreciation and amortization

14,788

15,239

11,481

11,430

Legacy asbestos expense (income)

12,391

(50,346)

33,816

18,112

IPO - related costs

57,017

-

-

-

Legacy legal expenses

4,131

-

8,330

3,100

Due diligence costs

582

-

-

-

Other post-employment benefit settlement

-

-

(9,102)

(251)

Cross currency swap

-

-

-

(2,075)

Environmental indemnification

-

-

-

(3,100)

Discontinued operations

-

-

1,397

(616)

Adjusted EBITDA

105,598

$

88,168

$

64,068

$

54,780

$

Adjusted EBITDA margin

17.5%

17.4%

16.3%

15.9%

28

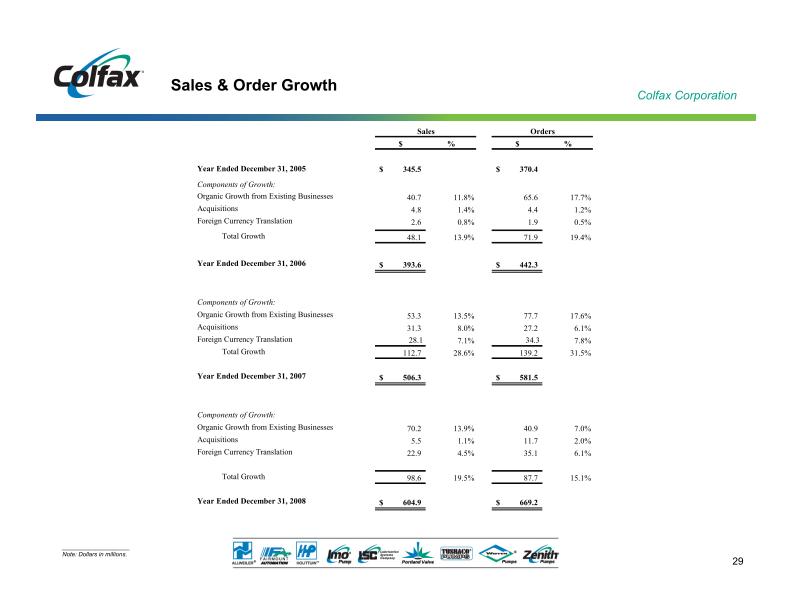

Sales & Order Growth

____________________

Note: Dollars in millions.

$

%

$

%

Year Ended December 31, 2005

345.5

$

370.4

$

Components of Growth:

Organic Growth from Existing Businesses

40.7

11.8%

65.6

17.7%

Acquisitions

4.8

1.4%

4.4

1.2%

Foreign Currency Translation

2.6

0.8%

1.9

0.5%

Total Growth

48.1

13.9%

71.9

19.4%

Year Ended December 31, 2006

393.6

$

442.3

$

Components of Growth:

Organic Growth from Existing Businesses

53.3

13.5%

77.7

17.6%

Acquisitions

31.3

8.0%

27.2

6.1%

Foreign Currency Translation

28.1

7.1%

34.3

7.8%

Total Growth

112.7

28.6%

139.2

31.5%

Year Ended December 31, 2007

506.3

$

581.5

$

Components of Growth:

Organic Growth from Existing Businesses

70.2

13.9%

40.9

7.0%

Acquisitions

5.5

1.1%

11.7

2.0%

Foreign Currency Translation

22.9

4.5%

35.1

6.1%

Total Growth

98.6

19.5%

87.7

15.1%

Year Ended December 31, 2008

604.9

$

669.2

$

Sales

Orders

29

____________________

Note: Dollars in thousands.

Non-GAAP Reconciliation

October 2, 2009

September 26, 2008

October 2, 2009

September 26, 2008

EBITDA

Net income (loss)

5,375

$

13,651

$

16,602

$

(10,950)

$

Interest expense

1,834

1,951

5,466

9,684

Provision (benefit) for income taxes

2,188

5,329

7,433

(3,772)

Depreciation and amortization

3,681

3,695

10,592

11,345

EBITDA

13,078

$

24,626

$

40,093

$

6,307

$

EBITDA margin

10.2%

16.0%

10.2%

1.4%

Adjusted EBITDA

Net income (loss)

5,375

$

13,651

$

16,602

$

(10,950)

$

Interest expense

1,834

1,951

5,466

9,684

Provision (benefit) for income taxes

2,188

5,329

7,433

(3,772)

Depreciation and amortization

3,681

3,695

10,592

11,345

Restructuring and other related charges

9,608

-

10,755

-

IPO-related costs

-

-

-

57,017

Legacy legal adjustment

-

-

-

4,131

Due diligence costs

-

582

-

582

Asbestos liability and defense income

(4,303)

(6,312)

(1,176)

(6,749)

Asbestos coverage litigation expenses

1,845

5,148

8,838

12,257

Adjusted EBITDA

20,228

$

24,044

$

58,510

$

73,545

$

Adjusted EBITDA margin

15.7%

15.7%

14.8%

16.5%

Three Months Ended

Nine Months Ended

30

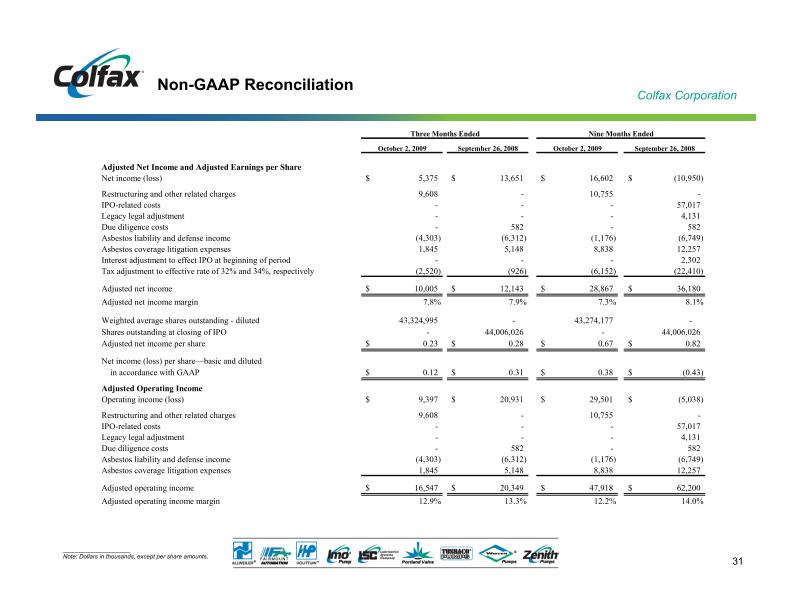

____________________

Note: Dollars in thousands, except per share amounts.

Non-GAAP Reconciliation

October 2, 2009

September 26, 2008

October 2, 2009

September 26, 2008

Adjusted Net Income and Adjusted Earnings per Share

Net income (loss)

5,375

$

13,651

$

16,602

$

(10,950)

$

Restructuring and other related charges

9,608

-

10,755

-

IPO-related costs

-

-

-

57,017

Legacy legal adjustment

-

-

-

4,131

Due diligence costs

-

582

-

582

Asbestos liability and defense income

(4,303)

(6,312)

(1,176)

(6,749)

Asbestos coverage litigation expenses

1,845

5,148

8,838

12,257

Interest adjustment to effect IPO at beginning of period

-

-

-

2,302

Tax adjustment to effective rate of 32% and 34%, respectively

(2,520)

(926)

(6,152)

(22,410)

Adjusted net income

10,005

$

12,143

$

28,867

$

36,180

$

Adjusted net income margin

7.8%

7.9%

7.3%

8.1%

Weighted average shares outstanding - diluted

43,324,995

-

43,274,177

-

Shares outstanding at closing of IPO

-

44,006,026

-

44,006,026

Adjusted net income per share

0.23

$

0.28

$

0.67

$

0.82

$

Net income

(

loss

)

per share—basic and diluted

in accordance with GAAP

0.12

$

0.31

$

0.38

$

(0.43)

$

Adjusted Operating Income

Operating income (loss)

9,397

$

20,931

$

29,501

$

(5,038)

$

Restructuring and other related charges

9,608

-

10,755

-

IPO-related costs

-

-

-

57,017

Legacy legal adjustment

-

-

-

4,131

Due diligence costs

-

582

-

582

Asbestos liability and defense income

(4,303)

(6,312)

(1,176)

(6,749)

Asbestos coverage litigation expenses

1,845

5,148

8,838

12,257

Adjusted operating income

16,547

$

20,349

$

47,918

$

62,200

$

Adjusted operating income margin

12.9%

13.3%

12.2%

14.0%

Three Months Ended

Nine Months Ended

31

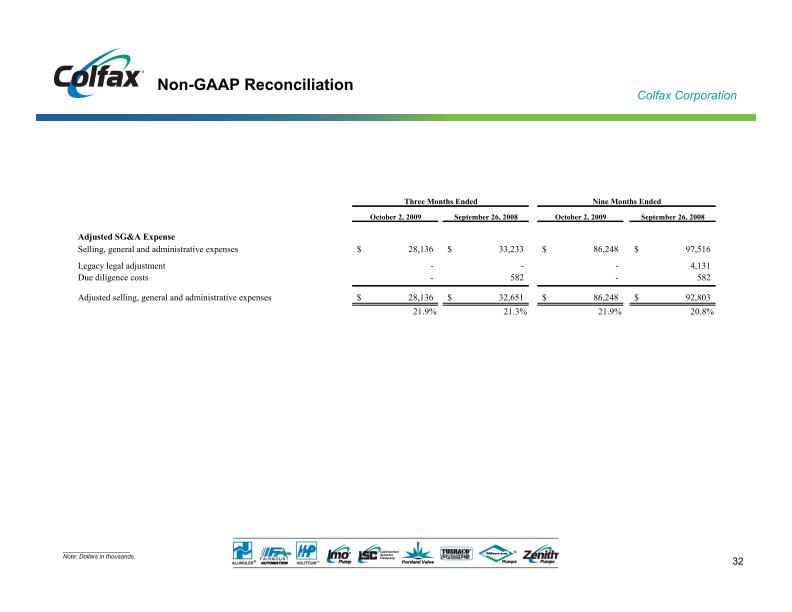

____________________

Note: Dollars in thousands.

Non-GAAP Reconciliation

October 2, 2009

September 26, 2008

October 2, 2009

September 26, 2008

Adjusted SG&A Expense

Selling, general and administrative expenses

28,136

$

33,233

$

86,248

$

97,516

$

Legacy legal adjustment

-

-

-

4,131

Due diligence costs

-

582

-

582

Adjusted selling, general and administrative expenses

28,136

$

32,651

$

86,248

$

92,803

$

21.9%

21.3%

21.9%

20.8%

Three Months Ended

Nine Months Ended

32

____________________

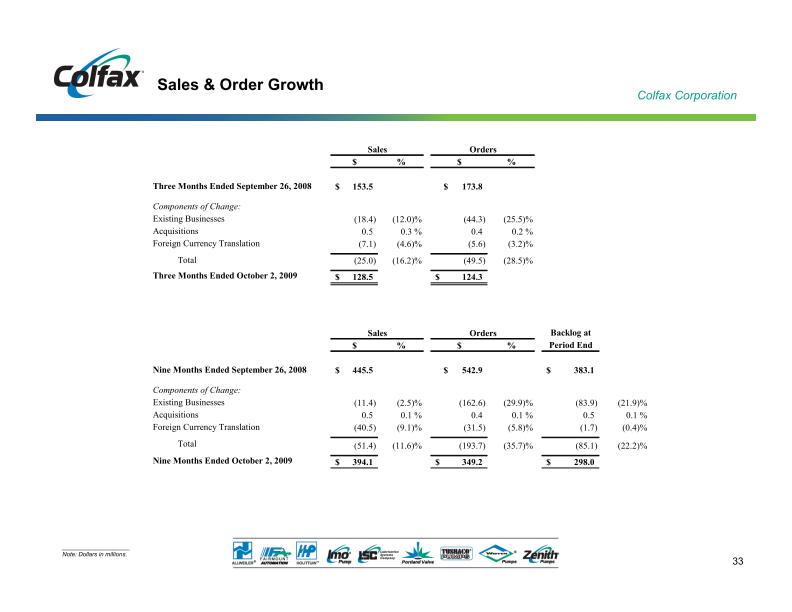

Note: Dollars in millions.

Sales & Order Growth

$

%

$

%

Three Months Ended September 26, 2008

153.5

$

173.8

$

Components of Change:

Existing Businesses

(18.4)

(12.0)%

(44.3)

(25.5)%

Acquisitions

0.5

0.3 %

0.4

0.2 %

Foreign Currency Translation

(7.1)

(4.6)%

(5.6)

(3.2)%

Total

(25.0)

(16.2)%

(49.5)

(28.5)%

Three Months Ended October 2, 2009

128.5

$

124.3

$

Backlog

at

$

%

$

%

Period

End

Nine Months Ended September 26, 2008

445.5

$

542.9

$

383.1

$

Components of Change:

Existing Businesses

(11.4)

(2.5)%

(162.6)

(29.9)%

(83.9)

(21.9)%

Acquisitions

0.5

0.1 %

0.4

0.1 %

0.5

0.1 %

Foreign Currency Translation

(40.5)

(9.1)%

(31.5)

(5.8)%

(1.7)

(0.4)%

Total

(51.4)

(11.6)%

(193.7)

(35.7)%

(85.1)

(22.2)%

Nine Months Ended October 2, 2009

394.1

$

349.2

$

298.0

$

Sales

Orders

Sales

Orders

33