Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2009

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No.: 1-16335

Magellan Midstream Partners, L.P.

(Exact name of registrant as specified in its charter)

| Delaware | 73-1599053 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) |

One Williams Center, P.O. Box 22186, Tulsa, Oklahoma 74121-2186

(Address of principal executive offices and zip code)

(918) 574-7000

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company.

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12-b-2 of the Exchange Act). Yes ¨ No x

As of October 30, 2009, there were 106,587,822 outstanding common units of Magellan Midstream Partners, L.P. that trade on the New York Stock Exchange under the ticker symbol “MMP.”

Table of Contents

PART I

FINANCIAL INFORMATION

1

Table of Contents

PART I

FINANCIAL INFORMATION

| ITEM 1. | FINANCIAL STATEMENTS |

MAGELLAN MIDSTREAM PARTNERS, L.P.

CONSOLIDATED STATEMENTS OF INCOME

(In thousands, except per unit amounts)

(Unaudited)

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| (As Adjusted) | (As Adjusted) | |||||||||||||||

| 2008 | 2009 | 2008 | 2009 | |||||||||||||

| Transportation and terminals revenues |

$ | 164,470 | $ | 173,504 | $ | 471,855 | $ | 495,227 | ||||||||

| Product sales revenues |

127,540 | 66,076 | 439,622 | 165,119 | ||||||||||||

| Affiliate management fee revenue |

183 | 190 | 549 | 570 | ||||||||||||

| Total revenues |

292,193 | 239,770 | 912,026 | 660,916 | ||||||||||||

| Costs and expenses: |

||||||||||||||||

| Operating |

81,626 | 73,863 | 193,845 | 195,178 | ||||||||||||

| Product purchases |

89,523 | 47,902 | 342,383 | 141,522 | ||||||||||||

| Depreciation and amortization |

21,563 | 24,613 | 63,847 | 70,928 | ||||||||||||

| General and administrative |

17,754 | 20,002 | 55,104 | 61,386 | ||||||||||||

| Total costs and expenses |

210,466 | 166,380 | 655,179 | 469,014 | ||||||||||||

| Gain on assignment of supply agreement |

— | — | 26,492 | — | ||||||||||||

| Equity earnings |

1,722 | 1,368 | 3,504 | 2,826 | ||||||||||||

| Operating profit |

83,449 | 74,758 | 286,843 | 194,728 | ||||||||||||

| Interest expense |

15,033 | 20,837 | 40,726 | 52,198 | ||||||||||||

| Interest income |

(351 | ) | (225 | ) | (950 | ) | (652 | ) | ||||||||

| Interest capitalized |

(1,322 | ) | (874 | ) | (3,734 | ) | (2,752 | ) | ||||||||

| Debt placement fee amortization expense |

211 | 331 | 548 | 775 | ||||||||||||

| Other (income) expense |

— | 11 | (254 | ) | (636 | ) | ||||||||||

| Income before provision for income taxes |

69,878 | 54,678 | 250,507 | 145,795 | ||||||||||||

| Provision for income taxes |

524 | 463 | 1,469 | 1,272 | ||||||||||||

| Net income |

$ | 69,354 | $ | 54,215 | $ | 249,038 | $ | 144,523 | ||||||||

| Allocation of net income: |

||||||||||||||||

| Non-controlling owners’ interest in income of consolidated subsidiaries (pre-simplification) |

$ | 51,707 | $ | 36,054 | $ | 182,868 | $ | 99,729 | ||||||||

| Limited partners’ interest |

18,052 | 18,161 | 67,384 | 44,794 | ||||||||||||

| General partner’s interest |

(405 | ) | — | (1,214 | ) | — | ||||||||||

| Net income |

$ | 69,354 | $ | 54,215 | $ | 249,038 | $ | 144,523 | ||||||||

| Basic and diluted net income per limited partner unit |

$ | 0.46 | $ | 0.43 | $ | 1.70 | $ | 1.11 | ||||||||

| Weighted average number of limited partner units outstanding used for basic and diluted net income per unit calculation |

39,631 | 41,831 | 39,629 | 40,377 | ||||||||||||

See notes to consolidated financial statements.

2

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

CONSOLIDATED BALANCE SHEETS

(Unaudited, in thousands)

| December 31, 2008 |

September 30, 2009 |

|||||||

| (As Adjusted) | ||||||||

| ASSETS | ||||||||

| Current assets: |

||||||||

| Cash and cash equivalents |

$ | 37,912 | $ | 3,674 | ||||

| Accounts receivable (less allowance for doubtful accounts of $462 and $157 at December 31, 2008 and September 30, 2009, respectively) |

37,517 | 48,959 | ||||||

| Other accounts receivable |

11,805 | 17,597 | ||||||

| Inventory |

47,734 | 190,202 | ||||||

| Energy commodity derivative contracts |

20,200 | — | ||||||

| Energy commodity derivatives deposit |

— | 8,776 | ||||||

| Reimbursable costs |

8,176 | 14,817 | ||||||

| Other current assets |

7,297 | 11,616 | ||||||

| Total current assets |

170,641 | 295,641 | ||||||

| Property, plant and equipment |

2,890,672 | 3,309,666 | ||||||

| Less: accumulated depreciation |

529,356 | 593,292 | ||||||

| Net property, plant and equipment |

2,361,316 | 2,716,374 | ||||||

| Equity investments |

23,190 | 22,838 | ||||||

| Long-term receivables |

7,390 | 658 | ||||||

| Goodwill |

14,766 | 14,766 | ||||||

| Other intangibles (less accumulated amortization of $8,290 and $9,504 at December 31, 2008 and September 30, 2009, respectively) |

5,539 | 4,325 | ||||||

| Debt placement costs (less accumulated amortization of $2,937 and $3,712 at December 31, 2008 and September 30, 2009, respectively) |

7,649 | 11,285 | ||||||

| Other noncurrent assets |

10,217 | 20,425 | ||||||

| Total assets |

$ | 2,600,708 | $ | 3,086,312 | ||||

| LIABILITIES AND OWNERS’ EQUITY | ||||||||

| Current liabilities: |

||||||||

| Accounts payable |

$ | 40,051 | $ | 43,743 | ||||

| Accrued payroll and benefits |

21,884 | 23,020 | ||||||

| Accrued interest payable |

15,077 | 31,411 | ||||||

| Accrued taxes other than income |

20,151 | 23,560 | ||||||

| Environmental liabilities |

19,634 | 18,137 | ||||||

| Deferred revenue |

21,492 | 26,182 | ||||||

| Accrued product purchases |

23,874 | 21,061 | ||||||

| Energy commodity derivative contracts |

— | 8,860 | ||||||

| Energy commodity derivatives deposit |

18,994 | — | ||||||

| Other current liabilities |

19,128 | 20,555 | ||||||

| Total current liabilities |

200,285 | 216,529 | ||||||

| Long-term debt |

1,083,485 | 1,624,564 | ||||||

| Long-term pension and benefits |

31,787 | 33,836 | ||||||

| Other noncurrent liabilities |

8,853 | 7,449 | ||||||

| Environmental liabilities |

22,166 | 22,815 | ||||||

| Commitments and contingencies |

||||||||

| Owners’ equity: |

||||||||

| Partners’ capital: |

||||||||

| Common unitholders |

68,063 | 1,196,512 | ||||||

| Accumulated other comprehensive loss |

(340 | ) | (15,393 | ) | ||||

| Total partners’ capital |

67,723 | 1,181,119 | ||||||

| Non-controlling owners’ interests in consolidated subsidiaries (pre-simplification) |

1,186,409 | — | ||||||

| Total owners’ equity |

1,254,132 | 1,181,119 | ||||||

| Total liabilities and owners’ equity |

$ | 2,600,708 | $ | 3,086,312 | ||||

See notes to consolidated financial statements.

3

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited, in thousands)

| Nine Months Ended September 30, |

||||||||

| 2008 | 2009 | |||||||

| (As Adjusted) | ||||||||

| Operating Activities: |

||||||||

| Net income |

$ | 249,038 | $ | 144,523 | ||||

| Adjustments to reconcile net income to net cash provided by operating activities: |

||||||||

| Depreciation and amortization |

63,847 | 70,928 | ||||||

| Debt placement fee amortization |

548 | 775 | ||||||

| Loss on sale and retirement of assets |

3,824 | 3,981 | ||||||

| Equity earnings |

(3,504 | ) | (2,826 | ) | ||||

| Distributions from equity investment |

3,200 | 3,168 | ||||||

| Equity-based incentive compensation expense |

4,384 | 7,361 | ||||||

| Amortization of prior service cost (credit) and net actuarial loss |

(65 | ) | 942 | |||||

| Gain on assignment of supply agreement |

(26,492 | ) | — | |||||

| Changes in operating assets and liabilities: |

||||||||

| Accounts receivable and other accounts receivable |

(5,261 | ) | (17,234 | ) | ||||

| Inventory |

39,328 | (56,336 | ) | |||||

| Reimbursable costs |

300 | (6,641 | ) | |||||

| Accounts payable |

16,284 | 4,343 | ||||||

| Accrued payroll and benefits |

(4,641 | ) | 1,136 | |||||

| Accrued interest payable |

14,716 | 16,334 | ||||||

| Accrued taxes other than income |

1,268 | 3,409 | ||||||

| Accrued product purchases |

3,940 | (2,813 | ) | |||||

| Accrued product shortages |

12,673 | — | ||||||

| Supply agreement deposit |

(18,500 | ) | — | |||||

| Energy commodity derivative contracts, net of margin deposits |

(3,966 | ) | 589 | |||||

| Current and noncurrent environmental liabilities |

(17,396 | ) | (868 | ) | ||||

| Other current and noncurrent assets and liabilities |

(2,041 | ) | 8,717 | |||||

| Net cash provided by operating activities |

331,484 | 179,488 | ||||||

| Investing Activities: |

||||||||

| Property, plant and equipment: |

||||||||

| Additions to property, plant and equipment |

(208,859 | ) | (157,321 | ) | ||||

| Proceeds from sale of assets |

3,846 | 333 | ||||||

| Changes in accounts payable |

6,326 | (651 | ) | |||||

| Acquisition of business |

(20,567 | ) | (358,442 | ) | ||||

| Net cash used by investing activities |

(219,254 | ) | (516,081 | ) | ||||

| Financing Activities: |

||||||||

| Distributions paid |

(195,243 | ) | (210,081 | ) | ||||

| Net repayments under revolver |

(148,500 | ) | (37,000 | ) | ||||

| Borrowings under long-term notes, net |

249,980 | 568,699 | ||||||

| Debt placement costs |

(2,048 | ) | (4,411 | ) | ||||

| Net receipt from financial derivatives |

4,030 | — | ||||||

| Capital contributions by affiliate |

2,453 | — | ||||||

| Change in outstanding checks |

(3,026 | ) | 2,151 | |||||

| Settlement of tax withholdings on long-term incentive compensation |

— | (3,450 | ) | |||||

| Simplification of capital structure |

— | (13,553 | ) | |||||

| Net cash provided (used) by financing activities |

(92,354 | ) | 302,355 | |||||

| Change in cash and cash equivalents |

19,876 | (34,238 | ) | |||||

| Cash and cash equivalents at beginning of period |

938 | 37,912 | ||||||

| Cash and cash equivalents at end of period |

$ | 20,814 | $ | 3,674 | ||||

| Supplemental non-cash financing activity: |

||||||||

| Issuance of Magellan Midstream Partners, L.P., common units in settlement of long-term incentive plan awards |

$ | 8,536 | $ | 1,943 | ||||

See notes to consolidated financial statements.

4

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited, in thousands)

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2008 | 2009 | 2008 | 2009 | |||||||||||||

| (As Adjusted) | (As Adjusted) | |||||||||||||||

| Net income |

$ | 69,354 | $ | 54,215 | $ | 249,038 | $ | 144,523 | ||||||||

| Other comprehensive income: |

||||||||||||||||

| Net gain on commodity hedges |

— | 639 | — | 639 | ||||||||||||

| Reclassification of net gain on cash flow hedges to interest expense |

(41 | ) | (41 | ) | (123 | ) | (123 | ) | ||||||||

| Reclassification of net gain on commodity hedges to product sales revenues |

— | (255 | ) | — | (255 | ) | ||||||||||

| Amortization of prior service cost (credit) and actuarial loss |

(21 | ) | 270 | (65 | ) | 942 | ||||||||||

| Adjustment to recognize the funded status of postretirement plans |

746 | 522 | 746 | 522 | ||||||||||||

| Total other comprehensive income |

684 | 1,135 | 558 | 1,725 | ||||||||||||

| Comprehensive income |

70,038 | 55,350 | 249,596 | 146,248 | ||||||||||||

| Comprehensive income attributable to non-controlling owners’ interest in consolidated subsidiaries (pre-simplification) |

52,377 | 34,063 | 183,414 | 98,316 | ||||||||||||

| Comprehensive income attributable to partners’ capital |

$ | 17,661 | $ | 21,287 | $ | 66,182 | $ | 47,932 | ||||||||

See notes to consolidated financial statements.

5

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

| 1. | Basis of Presentation |

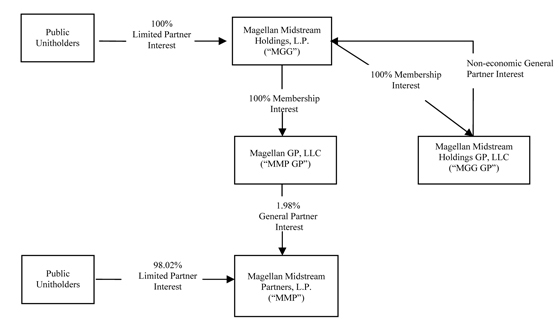

These financial statements were originally the financial statements of Magellan Midstream Holdings, L.P. (“MGG”) prior to the effective date of the simplification of our capital structure (see Note 2—Simplification Agreement below). The Simplification was accounted for in accordance with Accounting Standards Codification (“ASC”) 810-10-45; Paragraphs 22 and 23, Consolidation—Overall—Changes in Parent’s Ownership Interest in a Subsidiary. Under ASC 810, the exchange of MGG units for Magellan Midstream Partners, L.P. (“MMP”) units was accounted for as an MGG equity issuance and MGG was the surviving entity for accounting purposes. Although MGG was the surviving entity for accounting purposes, MMP was the surviving entity for legal purposes; consequently, the name on these financial statements was changed from “Magellan Midstream Holdings, L.P.” to “Magellan Midstream Partners, L.P.”

Historically, MGG’s sole ownership of MMP’s general partner, Magellan GP, LLC (“MMP GP”), provided MGG with an indirect approximate 2% general partner interest in MMP. MGG’s ownership of MMP’s general partner interest gave it control of MMP as the limited partner interests of MMP (i) did not have the substantive ability to dissolve MMP, (ii) could remove MMP GP as MMP’s general partner only with a supermajority vote of MMP’s common units representing limited partner interest in it (“MMP limited partner units”) and the MMP limited partner units that could be voted in such an election were restricted, and (iii) did not possess substantive participating rights in MMP’s operations. As a result, MGG’s consolidated financial statements included the assets, liabilities and cash flows of MMP and MMP GP.

During the periods that MGG controlled MMP, MGG had no substantial assets and liabilities other than those of MMP. MGG’s consolidated balance sheet included non-controlling owners’ interests of consolidated subsidiaries, which reflected the proportion of MMP owned by MMP’s partners other than MGG. In addition, MGG’s consolidated balance sheet reflected adjustments to the historical amounts reported on MMP’s balance sheet for the fair value of MGG’s proportionate share of MMP’s assets and liabilities at the time of MGG’s acquisition of interest in MMP and MMP GP.

Because of the changes the Simplification Agreement has had on these financial statements and MMP’s organizational structure, and because the nature of the pre-simplification and post-simplification Magellan entities are significantly different, management believed the use of the terms “we,” “our,” “us” and similar language would be confusing. Therefore, these notes to consolidated financial statements refer to specific Magellan entities, with Magellan Midstream Partners, L.P. prior to the simplification referred to as “MMP” and after the simplification as “Magellan Partners.”

| 2. | Simplification Agreement |

In March 2009, MMP and its general partner and MGG and its general partner entered into an Agreement Relating to Simplification of Capital Structure (the “Simplification Agreement” or “the simplification”). Pursuant to the Simplification Agreement, which was approved by both MMP’s and MGG’s unitholders on September 25, 2009, MMP amended and restated its existing partnership agreement to provide for the transformation of the incentive distribution rights and approximate 2% general partner interest owned by MMP GP into common units in MMP and a non-economic general partner interest (the “transformation”). Once the transformation was completed, MMP GP distributed the common units of MMP that it received in the transformation to MGG (the “unit distribution”). Once the transformation and unit distribution were completed, pursuant to a Contribution and Assumption Agreement: (i) MGG contributed 100% of its member interests in Magellan Midstream Holdings GP, LLC (“MGG GP”), its general partner, to MMP GP; (ii) MGG contributed 100% of its member interests in MMP GP to MMP; (iii) MGG contributed to MMP all of its cash and assets, other than the common units of MMP it received in the unit distribution; and (iv) MMP assumed all of MGG’s liabilities (collectively, the “contributions”). Once the transformation, unit distribution and contributions were completed, MGG distributed the common units in MMP it received in the unit distribution to its unitholders (the “redistribution”) and was dissolved. The transformation of the general partner interest and incentive distribution rights into common units in MMP occurred on September 28, 2009.

Pursuant to the Simplification Agreement, MGG received approximately 39.6 million of MMP’s common units in the transformation and unit distribution and each of MGG’s unitholders received 0.6325 of MMP common units in the redistribution for each MGG common unit they owned. As a result, the number of MMP limited partner units outstanding increased from 67.0 million units to 106.6 million units. However, for historical reporting purposes, the impact of this

6

Table of Contents

change resulted in a reverse unit split of 0.6325 to 1.0. Therefore, the weighted average units outstanding used for basic and diluted earnings per unit calculations are MGG’s historical weighted average units outstanding adjusted for the retrospective application of the reverse unit split. Amounts reflecting historical MGG limited partner unit and per unit amounts included in this report have been restated for the reverse unit split.

The reconciliation of MMP’s net income, as historically reported, to the net income reported in these financial statements is as follows (in thousands):

| Three Months Ended September 30, 2008 |

Nine Months Ended September 30, 2008 |

|||||||

| Net income, as previously reported |

$ | 73,336 | $ | 261,032 | ||||

| Adjustments: |

||||||||

| Additional depreciation expense |

(3,837 | ) | (11,511 | ) | ||||

| Other |

(145 | ) | (483 | ) | ||||

| Net income |

$ | 69,354 | $ | 249,038 | ||||

At the time of MGG’s acquisition of general and limited partner interests in MMP on June 17, 2003, MGG recorded MMP’s property, plant and equipment at 54.6% of their fair values and at 46.4% of their historical carrying values reflecting MGG’s ownership percentages in MMP at that time. This step-up in basis is the reason MGG recorded higher depreciation expense than MMP. Other adjustments include the amortization of the step-up to fair value made by MGG on June 17, 2003 of other items, including the fair value of MMP’s debt and certain commercial contracts. Additionally, other adjustments include the stand-alone G&A expenses that MGG incurred.

MMP GP continues to manage Magellan Partners following the simplification and Magellan Partners’ management team remains unchanged. Additionally, three of the four independent members of MGG’s general partner’s board of directors have joined the board of directors of MMP GP. The other independent member of MGG’s general partner’s board of directors, Patrick C. Eilers, was already serving as an independent member of MMP GP’s board of directors.

During the three and nine months ended September 30, 2009, Magellan Partners incurred $6.9 million and $13.6 million, respectively, of costs associated with the simplification of its capital structure. In accordance with ASC 810-10-45, Consolidation – Overall – Changes in Parent’s Ownership Interest in a Subsidiary, Magellan Partners charged these costs to equity. The amount for the nine months ended September 30, 2009 was reported under the caption “Simplification of capital structure” in the financing activities section of Magellan Partners’ consolidated statements of cash flows.

| 3. | Organization |

Magellan Partners is a Delaware limited partnership, and its units are traded on the New York Stock Exchange under the ticker symbol “MMP.” MMP GP, a Delaware limited liability company, serves as its general partner. Magellan Partners and MMP GP have contracted with MGG GP to provide all general and administrative (“G&A”) services and operating functions required for Magellan Partners’ operations. Prior to the simplification of MMP’s capital structure, MMP’s organizational structure and that of its affiliate entities, as well as how MMP refers to these affiliates in its notes to consolidated financial statements, was as follows:

7

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

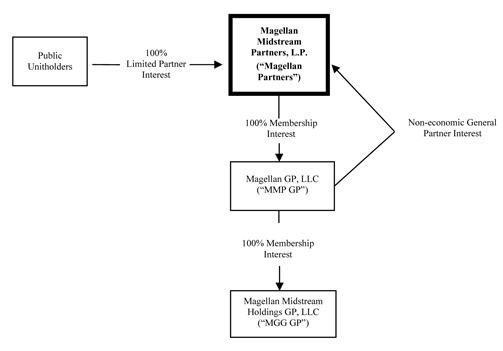

The Simplification Agreement (see Note 2—Simplification Agreement) was approved by MMP’s and MGG’s unitholders; therefore, effective September 28, 2009, MMP’s organizational structure became as follows:

Magellan Partners operates and reports in three business segments: the petroleum products pipeline system, the petroleum products terminals and the ammonia pipeline system. Magellan Partners’ reportable segments offer different products and services and are managed separately because each requires different marketing strategies and business knowledge.

In the opinion of management, Magellan Partners’ accompanying consolidated financial statements, which are unaudited except for the consolidated balance sheet as of December 31, 2008, which is derived from audited financial statements, include all normal

8

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

and recurring adjustments necessary to present fairly its financial position as of September 30, 2009, and the results of operations for the three and nine months ended September 30, 2008 and 2009 and cash flows for the nine months ended September 30, 2008 and 2009. The results of operations for the nine months ended September 30, 2009 are not necessarily indicative of the results to be expected for the full year ending December 31, 2009.

Pursuant to the rules and regulations of the Securities and Exchange Commission (“SEC”), the financial statements in this report do not include all of the information and notes normally included with financial statements prepared in accordance with accounting principles generally accepted in the United States. These financial statements should be read in conjunction with Magellan Partners’ audited consolidated balance sheets as of December 31, 2008 and 2007, and the related statements of income, partners’ capital and cash flows for each of the three years in the period ended December 31, 2008 and notes thereto included in Magellan Partners’ 8-K report filed with the SEC, concurrent with this 10-Q report, on November 3, 2009.

| 4. | Allocation of Net Income |

For purposes of both calculating earnings per unit and determining the capital balances of the general partner and the limited partners, the allocation of net income was as follows (in thousands):

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2008 | 2009 | 2008 | 2009 | |||||||||||||

| Net income |

$ | 69,354 | $ | 54,215 | $ | 249,038 | $ | 144,523 | ||||||||

| Net income applicable to non-controlling owner’s interests (a) (b) |

51,707 | 36,054 | 182,868 | 99,729 | ||||||||||||

| Net income applicable to limited partners and general partner |

17,647 | 18,161 | 66,170 | 44,794 | ||||||||||||

| Allocation of net income applicable to limited partners and general partner: |

||||||||||||||||

| Direct charges to general partner: |

||||||||||||||||

| Reimbursable general and administrative costs |

408 | — | 1,224 | — | ||||||||||||

| Income applicable to limited partners and general partner before direct charges to general partner |

18,055 | 18,161 | 67,394 | 44,794 | ||||||||||||

| General partner’s share of income (c) |

0.0141 | % | 0 | % | 0.0141 | % | 0 | % | ||||||||

| General partner’s allocated share of net income before direct charges |

3 | — | 10 | — | ||||||||||||

| Direct charges to general partner |

408 | — | 1,224 | — | ||||||||||||

| Net loss allocated to general partner |

$ | (405 | ) | $ | — | $ | (1,214 | ) | $ | — | ||||||

| Net income applicable to limited partners and general partner |

$ | 17,647 | $ | 18,161 | $ | 66,170 | $ | 44,794 | ||||||||

| Less: net loss allocated to general partner |

(405 | ) | — | (1,214 | ) | — | ||||||||||

| Net income allocated to limited partners |

$ | 18,052 | $ | 18,161 | $ | 67,384 | $ | 44,794 | ||||||||

| (a) | On January 1, 2009, MMP adopted ASC 810-10-45, Consolidations – General – Other Presentation Matters. Under this ASC, non-controlling owners’ interest in income is no longer reported as a deduction in arriving at net income. Instead, net income is allocated between the non-controlling owners’ interest and the limited partner owners’ interest. As prescribed in ASC 810-10-65, Consolidations – General - Transition and Open Effective Date Information, MMP retroactively applied this guidance to the three and nine months ended September 30, 2008. Also, effective September 30, 2009, the Simplification Agreement was completed (see Note 2—Simplification Agreement) under which MMP acquired the non-controlling owner’s interests. Therefore, effective September 28, 2009, the non-controlling owner’s interests will no longer be allocated a portion of MMP’s net income, i.e. 100% of MMP’s net income will be attributable to the limited partners. |

| (b) | These amounts represent MMP’s allocation of pre-simplification net income. MMP completed the Simplification during the current quarter (see Note 2—Simplification Agreement). For periods prior to the Simplification, the net income allocated to non-controlling owner’s interests was determined by deducting MMP GP’s allocated share of MMP’s net income for the period from MMP’s net income. MMP GP’s allocated share of MMP’s net income was determined by multiplying MMP’s net income by MMP GP’s proportionate share of distributions (including incentive distribution rights) for the period, adjusted for direct charges by MMP to MMP GP, plus MMP GP’s approximate 2% ownership interest in undistributed MMP net income, if any. Because MGG has been dissolved and the incentive distribution rights formerly paid by MMP have been eliminated, the income allocated to MMP GP’s interest for the current quarter is net income attributable to the pre-simplification period, adjusted for indemnified environmental and MGG stand-alone G&A expenses, times the proportion of the distributions that will be paid for the current quarter on the MMP units received in exchange for the approximate 2% general partner ownership interest and incentive distribution rights. Therefore, for the current quarter, the net income allocated to the non-controlling owner’s interest was determined as follows: |

9

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

| Net income |

$ | 54,215 | |||||||||||

| Previously indemnified environmental expense |

4,078 | ||||||||||||

| MGG stand-alone G&A expense |

1,029 | ||||||||||||

| Net income before indemnified environmental and MGG stand-alone G&A expense |

$ | 59,322 | |||||||||||

| Allocation of net income to pre-simplification and post-simplification periods: |

| ||||||||||||

| Number of Days in Quarter |

Amount | ||||||||||||

| (in thousands) | |||||||||||||

| Pre-simplification period net income before indemnified environmental and MGG stand-alone G&A expense (July 1, 2009 through September 27, 2009) (1) |

89 | $ | 57,388 | ||||||||||

| Post-simplification period net income before indemnified environmental and MGG stand-alone G&A expense (September 28, 2009 through September 30, 2009) (1) |

3 | 1,934 | |||||||||||

| Net income before indemnified environmental and MGG stand-alone G&A expense |

92 | $ | 59,322 | ||||||||||

| Allocation of net income: |

| ||||||||||||

| MMP Units Outstanding After Simplification |

Per Unit Distribution Amount |

Distribution Amount |

Percentage | ||||||||||

| MGG units converted to MMP units |

39,623,944 | (2) | $ | 0.71 | $ | 28,133,000 | 37.175 | ||||||

| Pre-simplification MMP units outstanding |

66,963,878 | $ | 0.71 | 47,544,353 | 62.825 | ||||||||

| Total MMP units outstanding post-simplification |

106,587,822 | $ | 75,677,353 | 100.000 | |||||||||

| Amount | |||||||||||||

| (in thousands) | |||||||||||||

| Pre-simplification period net income before indemnified environmental and MGG stand-alone G&A expense |

$ | 57,388 | |||||||||||

| Percentage of current quarter distributions paid to MGG units that converted to MMP units |

37.175 | % | |||||||||||

| Pre-simplification period net income allocated to limited partners |

21,334 | ||||||||||||

| Less: Indemnified environmental and MGG stand-alone G&A expenses |

(5,107 | ) | |||||||||||

| Plus: Post-simplification period net income before indemnified environmental and MGG stand-alone G&A expenses |

1,934 | ||||||||||||

| Net income allocated to limited partners’ interest |

$ | 18,161 | |||||||||||

| Pre-simplification period net income before indemnified environmental and MGG stand-alone G&A expenses |

$ | 57,388 | |||||||||||

| Percentage of current quarter distributions paid to pre-simplification MMP units outstanding |

62.825 | % | |||||||||||

| Net income allocated to limited non-controlling owners’ interest |

$ | 36,054 | |||||||||||

| (1) | As part of the simplification process, 62.6 million MGG limited partner units converted to 39.6 million MMP limited partner units on September 28, 2009. |

| (2) | There were 62,646,551 MGG units outstanding prior to the simplification. These units converted to MMP units at the exchange ratio of 0.6325 (62,646,551 units x 0.6325 = 39,623,944). |

| (c) | In December 2008, MGG acquired its general partner from MGG Midstream Holdings, L.P. (“MGG MH”); subsequently, its general partner owned a non-economic general partner interest in MGG and was not allocated a portion of MGG’s net income. |

| 5. | Acquisitions |

Longhorn Partners Pipeline, L.P.

On July 29, 2009, MMP acquired substantially all of the assets of Longhorn Partners Pipeline, L.P. (which we refer to as the “Longhorn acquisition”) for $252.3 million plus the fair market value of the linefill of $86.1 million. The operating results from this acquisition have been included in Magellan Partners’ petroleum products pipeline system segment’s results since the acquisition date.

The Longhorn acquisition primarily include an approximate 700-mile common carrier pipeline system that transports refined petroleum products from Houston to El Paso, Texas and a terminal in El Paso, Texas. The El Paso, Texas terminal serves local petroleum products demand and distributes product to connecting third-party pipelines for ultimate delivery to markets in Arizona and New Mexico. Magellan Partners intends to connect this pipeline system to its existing terminal at East Houston to provide additional supply options for current and potential customers to transport petroleum products to Southwestern markets. Further, Magellan Partners will complete construction of an additional 400,000 barrels of storage that is currently underway at the El Paso terminal.

The Longhorn acquisition was accounted for as an acquisition of a business under the purchase method of accounting in accordance with ASC 805, Business Combinations. The assets acquired and liabilities assumed were recorded at their estimated fair market values as of the acquisition date. The purchase price and preliminary assessment of the fair value of the assets acquired (liabilities assumed) is as follows (in thousands):

10

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

| Purchase price |

$ | 338,439 | ||

| Fair value of assets acquired (liabilities assumed) (1): |

||||

| Property, plant and equipment |

$ | 252,327 | ||

| Inventory |

86,132 | |||

| Environmental liabilities assumed |

(20 | ) | ||

| Total |

$ | 338,439 | ||

| (1) | The initial accounting for property, plant and equipment is incomplete pending finalization of valuation reports on pipeline assets used as the basis for fair value of such assets. |

Magellan Partners’ reported net revenues and net income for 2009 include operating results from the Longhorn acquisition from July 29, 2009 through September 30, 2009. Net revenues and net loss resulting from the Longhorn acquisition that were included in Magellan Partners’ operating results were $0.9 million and $(4.1) million, respectively, for both the three and nine months ended September 30, 2009.

Wynnewood Terminal

During September 2009, MMP acquired a terminal in Wynnewood, Oklahoma for $20.0 million in a sale/lease-back arrangement. The Wynnewood terminal is connected to a refinery that is an origin point on Magellan Partners’ petroleum products pipeline system. The Wynnewood terminal acquisition was accounted for as an acquisition of a business under the purchase method of accounting in accordance with ASC 805, Business Combinations. The assets acquired were recorded at their estimated fair market values as of the acquisition date as property, plant and equipment in Magellan Partners’ petroleum products pipeline segment.

Pro Forma Information (unaudited)

The following summarized pro forma consolidated income statement information assumes that the Longhorn acquisition and the Wynnewood terminal acquisition discussed above occurred as of January 1, 2008. These pro forma results are for comparative purposes only and may not be indicative of the results that would have occurred if MMP had completed these acquisitions as of the periods shown below or the results that will be attained in the future. The amounts presented below are in thousands:

| Three Months Ended September 30, 2008 | Nine Months Ended September 30, 2008 | |||||||||||||||||||

| As Reported |

Pro Forma Adjustments |

Pro Forma | As Reported | Pro Forma Adjustments |

Pro Forma | |||||||||||||||

| Revenues |

$ | 292,193 | $ | 26,029 | $ | 318,222 | $ | 912,026 | $ | 86,625 | $ | 998,651 | ||||||||

| Net income |

$ | 69,354 | $ | 3,961 | $ | 73,315 | $ | 249,038 | $ | 20,227 | $ | 269,265 | ||||||||

| Three Months Ended September 30, 2009 | Nine Months Ended September 30, 2009 | |||||||||||||||||||

| As Reported |

Pro Forma Adjustments |

Pro Forma | As Reported | Pro Forma Adjustments |

Pro Forma | |||||||||||||||

| Revenues |

$ | 239,770 | $ | (83 | ) | $ | 239,687 | $ | 660,916 | $ | 8,502 | $ | 669,418 | |||||||

| Net income |

$ | 54,215 | $ | (12,043 | ) | $ | 42,172 | $ | 144,523 | $ | (35,632 | ) | $ | 108,891 | ||||||

Significant pro forma adjustments for the Longhorn acquisition include its revenues and net income for the period prior to MMP’s acquisition. Because the assets included in the Longhorn acquisition had minimal commercial activity following the former owner’s bankruptcy filing in July 2008, revenues and net income generated by the assets were substantially lower in 2009.

11

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Pro forma adjustments for the Wynnewood terminal include lease revenue based on a $2.0 million annual lease payment amount and depreciation expense based on $0.5 million annually.

Pro forma adjustments for both acquisitions include interest expense on borrowings necessary to complete the acquisitions.

| 6. | Product Sales Revenues |

The amounts Magellan Partners reports as product sales revenues on its consolidated statements of income include revenues from the sale of petroleum products and from mark-to-market adjustments from New York Mercantile Exchange (“NYMEX”) contracts. MMP began using NYMEX contracts during the third quarter of 2008 as economic hedges against changes in the price of petroleum products it expects to sell from its petroleum products blending activities. From the third quarter of 2008 through the second quarter of 2009 none of the NYMEX contracts MMP entered into qualified for hedge accounting treatment under ASC 815-30, Derivatives and Hedging. However, effective July 2, 2009, most of the NYMEX contracts associated with MMP’s petroleum products blending activities qualified for hedge accounting treatment and were recorded as cash flow hedges. Additionally, Magellan Partners currently uses NYMEX contracts as economic hedges against changes in the price of petroleum products associated with the linefill purchased in connection with the Longhorn acquisition and these NYMEX contracts do not qualify for hedge accounting treatment. As a result of the different accounting treatment applied to the various types of NYMEX contracts entered into, the amounts Magellan Partners reports as product sales revenues can include amounts from the following sources:

| • | The physical sale of petroleum products; |

| • | Mark-to-market adjustments of NYMEX contracts that did not qualify for hedge accounting treatment associated with economic hedges of Magellan Partners petroleum products blending and fractionation activities; |

| • | The closing value of NYMEX contracts which qualified for hedge accounting treatment and were accounted for as cash flow hedges that matured during the period; and |

| • | Mark-to-market adjustments of NYMEX contracts which did not qualify for hedge accounting treatment associated with economic hedges of Magellan Partners linefill related to the Longhorn acquisition. |

For the three and nine months ended September 30, 2008 and 2009, reported product sales revenues included the following (in thousands):

| Three Months Ended September 30, |

Nine Months Ended September 30, |

||||||||||||

| 2008 | 2009 | 2008 | 2009 | ||||||||||

| Physical sale of petroleum products |

$ | 115,169 | $ | 60,211 | $ | 427,251 | $ | 182,650 | |||||

| NYMEX contract adjustments: |

|||||||||||||

| Change in unrealized value of NYMEX contracts that did not qualify for hedge accounting treatment associated with Magellan Partners petroleum products blending and fractionation activities |

12,371 | 2,803 | 12,371 | (20,593 | ) | ||||||||

| Reclassification from accumulated other comprehensive loss of matured NYMEX contracts that qualified for hedge accounting treatment associated with Magellan Partners petroleum products blending activities |

— | 255 | — | 255 | |||||||||

| Change in unrealized value of NYMEX contracts that did not qualify for hedge accounting treatment associated with the linefill related to the Longhorn acquisition |

— | 2,807 | — | 2,807 | |||||||||

| Total NYMEX contract adjustments |

12,371 | 5,865 | 12,371 | (17,531 | ) | ||||||||

| Total petroleum product sales revenues |

$ | 127,540 | $ | 66,076 | $ | 439,622 | $ | 165,119 | |||||

12

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

| 7. | Owners’ Equity |

The changes in owners’ equity for the nine months ended September 30, 2008 and 2009 are provided in the tables below (in thousands):

| Partners’ Capital |

Partners’ Accumulated Other Comprehensive Loss |

Non-controlling Owners’ Interest |

Total Owners’ Equity |

|||||||||||||

| Balance, January 1, 2008 |

$ | 57,421 | $ | (91 | ) | $ | 1,127,236 | $ | 1,184,566 | |||||||

| Comprehensive income: |

||||||||||||||||

| Net income |

66,170 | — | 182,868 | 249,038 | ||||||||||||

| Reclassification of net gain on interest rate cash flow hedges to interest expense |

— | (3 | ) | (120 | ) | (123 | ) | |||||||||

| Amortization of prior service credit and net actuarial loss |

— | — | (65 | ) | (65 | ) | ||||||||||

| Adjustment to recognize the funded status of postretirement plans |

— | 15 | 731 | 746 | ||||||||||||

| Total comprehensive income |

66,170 | 12 | 183,414 | 249,596 | ||||||||||||

| Capital contributions by affiliate |

2,453 | — | — | 2,453 | ||||||||||||

| Distributions |

(60,588 | ) | — | (134,655 | ) | (195,243 | ) | |||||||||

| Equity method incentive compensation expense |

3,804 | — | — | 3,804 | ||||||||||||

| Issuance of MMP common units in settlement of long-term incentive plan awards |

— | — | 8,536 | 8,536 | ||||||||||||

| Other |

(28 | ) | — | 25 | (3 | ) | ||||||||||

| Balance, September 30, 2008 |

$ | 69,232 | $ | (79 | ) | $ | 1,184,556 | $ | 1,253,709 | |||||||

| Partners’ Capital |

Partners’ Accumulated Other Comprehensive Loss |

Non-controlling Owners’ Interest |

Total Owners’ Equity |

|||||||||||||

| Balance, January 1, 2009 |

$ | 68,063 | $ | (340 | ) | $ | 1,186,409 | $ | 1,254,132 | |||||||

| Comprehensive income: |

||||||||||||||||

| Net income |

47,898 | — | 96,625 | 144,523 | ||||||||||||

| Net gain on commodity hedges |

— | 13 | 626 | 639 | ||||||||||||

| Reclassification of net gain on interest rate cash flow hedges to interest expense |

— | (3 | ) | (120 | ) | (123 | ) | |||||||||

| Reclassification of net gain on commodity hedges to product sales revenues |

— | (5 | ) | (250 | ) | (255 | ) | |||||||||

| Amortization of prior service cost and net actuarial loss |

— | 19 | 923 | 942 | ||||||||||||

| Adjustment to recognize the funded status of postretirement plans |

— | 10 | 512 | 522 | ||||||||||||

| Total comprehensive income |

47,898 | 34 | 98,316 | 146,248 | ||||||||||||

| Distributions |

(67,470 | ) | — | (142,611 | ) | (210,081 | ) | |||||||||

| Equity method incentive compensation expense |

5,526 | — | — | 5,526 | ||||||||||||

| Simplification of capital structure |

(13,553 | ) | — | — | (13,553 | ) | ||||||||||

| Issuance of MMP common units in settlement of long-term incentive plan awards |

(4,406 | ) | — | 6,349 | 1,943 | |||||||||||

| Issuance of MMP limited partner units in settlement of special unit awards |

377 | — | — | 377 | ||||||||||||

| Settlement of tax withholdings on long-term incentive compensation |

(3,450 | ) | — | — | (3,450 | ) | ||||||||||

| Issuance of MMP units pursuant to the Simplification Agreement |

1,163,549 | (15,087 | ) | (1,148,462 | ) | — | ||||||||||

| Other |

(22 | ) | — | (1 | ) | (23 | ) | |||||||||

| Balance, September 30, 2009 |

$ | 1,196,512 | $ | (15,393 | ) | $ | — | $ | 1,181,119 | |||||||

13

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

| 8. | Segment Disclosures |

Magellan Partners’ reportable segments are strategic business units that offer different products and services. Magellan Partners’ segments are managed separately because each segment requires different marketing strategies and business knowledge. Management evaluates performance based on segment operating margin, which includes revenues from affiliates and external customers, operating expenses, product purchases and equity earnings. Transactions between Magellan Partners’ business segments are conducted and recorded on the same basis as transactions with third-party entities.

Magellan Partners believes that investors benefit from having access to the same financial measures being used by management. Operating margin, which is presented in the tables below, is an important measure used by management to evaluate the economic performance of Magellan Partners’ core operations. This measure forms the basis of Magellan Partners’ internal financial reporting and is used by management in deciding how to allocate capital resources between segments. Operating margin is not a generally accepted accounting principles (“GAAP”) measure, but the components of operating margin are computed by using amounts that are determined in accordance with GAAP. A reconciliation of operating margin to operating profit, which is its nearest comparable GAAP financial measure, is included in the tables below. Operating profit includes expense items, such as depreciation and amortization and G&A expenses, that management does not consider when evaluating the core profitability of Magellan Partners’ operations.

| Three Months Ended September 30, 2008 | |||||||||||||||||||

| (in thousands) | |||||||||||||||||||

| Petroleum Products Pipeline System |

Petroleum Products Terminals |

Ammonia Pipeline System |

Intersegment Eliminations |

Total | |||||||||||||||

| Transportation and terminals revenues |

$ | 125,746 | $ | 34,472 | $ | 5,128 | $ | (876 | ) | $ | 164,470 | ||||||||

| Product sales revenues |

118,979 | 8,561 | — | — | 127,540 | ||||||||||||||

| Affiliate management fee revenue |

183 | — | — | — | 183 | ||||||||||||||

| Total revenues |

244,908 | 43,033 | 5,128 | (876 | ) | 292,193 | |||||||||||||

| Operating expenses |

63,977 | 14,320 | 4,766 | (1,437 | ) | 81,626 | |||||||||||||

| Product purchases |

88,169 | 1,606 | — | (252 | ) | 89,523 | |||||||||||||

| Equity earnings |

(1,722 | ) | — | — | — | (1,722 | ) | ||||||||||||

| Operating margin |

94,484 | 27,107 | 362 | 813 | 122,766 | ||||||||||||||

| Depreciation and amortization |

13,781 | 6,685 | 284 | 813 | 21,563 | ||||||||||||||

| G&A expenses |

13,068 | 4,123 | 563 | — | 17,754 | ||||||||||||||

| Operating profit (loss) |

$ | 67,635 | $ | 16,299 | $ | (485 | ) | $ | — | $ | 83,449 | ||||||||

| Three Months Ended September 30, 2009 | |||||||||||||||||||

| (in thousands) | |||||||||||||||||||

| Petroleum Products Pipeline System |

Petroleum Products Terminals |

Ammonia Pipeline System |

Intersegment Eliminations |

Total | |||||||||||||||

| Transportation and terminals revenues |

$ | 128,979 | $ | 41,755 | $ | 4,017 | $ | (1,247 | ) | $ | 173,504 | ||||||||

| Product sales revenues |

62,447 | 3,629 | — | — | 66,076 | ||||||||||||||

| Affiliate management fee revenue |

190 | — | — | — | 190 | ||||||||||||||

| Total revenues |

191,616 | 45,384 | 4,017 | (1,247 | ) | 239,770 | |||||||||||||

| Operating expenses |

51,814 | 16,341 | 7,392 | (1,684 | ) | 73,863 | |||||||||||||

| Product purchases |

47,050 | 1,349 | — | (497 | ) | 47,902 | |||||||||||||

| Equity earnings |

(1,368 | ) | — | — | — | (1,368 | ) | ||||||||||||

| Operating margin (loss) |

94,120 | 27,694 | (3,375 | ) | 934 | 119,373 | |||||||||||||

| Depreciation and amortization |

15,180 | 8,165 | 334 | 934 | 24,613 | ||||||||||||||

| G&A expenses |

14,441 | 4,998 | 563 | — | 20,002 | ||||||||||||||

| Operating profit (loss) |

$ | 64,499 | $ | 14,531 | $ | (4,272 | ) | $ | — | $ | 74,758 | ||||||||

14

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

| Nine Months Ended September 30, 2008 | |||||||||||||||||||

| (in thousands) | |||||||||||||||||||

| Petroleum Products Pipeline System |

Petroleum Products Terminals |

Ammonia Pipeline System |

Intersegment Eliminations |

Total | |||||||||||||||

| Transportation and terminals revenues |

$ | 353,664 | $ | 104,043 | $ | 16,534 | $ | (2,386 | ) | $ | 471,855 | ||||||||

| Product sales revenues |

414,461 | 25,161 | — | — | 439,622 | ||||||||||||||

| Affiliate management fee revenue |

549 | — | — | — | 549 | ||||||||||||||

| Total revenues |

768,674 | 129,204 | 16,534 | (2,386 | ) | 912,026 | |||||||||||||

| Operating expenses |

145,944 | 42,473 | 9,825 | (4,397 | ) | 193,845 | |||||||||||||

| Product purchases |

336,367 | 6,528 | — | (512 | ) | 342,383 | |||||||||||||

| Equity earnings |

(3,504 | ) | — | — | — | (3,504 | ) | ||||||||||||

| Gain on assignment of supply agreement |

(26,492 | ) | — | — | — | (26,492 | ) | ||||||||||||

| Operating margin |

316,359 | 80,203 | 6,709 | 2,523 | 405,794 | ||||||||||||||

| Depreciation and amortization |

40,854 | 19,629 | 841 | 2,523 | 63,847 | ||||||||||||||

| G&A expenses |

39,678 | 12,898 | 2,528 | — | 55,104 | ||||||||||||||

| Operating profit |

$ | 235,827 | $ | 47,676 | $ | 3,340 | $ | — | $ | 286,843 | |||||||||

| Nine Months Ended September 30, 2009 | |||||||||||||||||||

| (in thousands) | |||||||||||||||||||

| Petroleum Products Pipeline System |

Petroleum Products Terminals |

Ammonia Pipeline System |

Intersegment Eliminations |

Total | |||||||||||||||

| Transportation and terminals revenues |

$ | 365,886 | $ | 120,623 | $ | 12,494 | $ | (3,776 | ) | $ | 495,227 | ||||||||

| Product sales revenues |

154,571 | 10,548 | — | — | 165,119 | ||||||||||||||

| Affiliate management fee revenue |

570 | — | — | — | 570 | ||||||||||||||

| Total revenues |

521,027 | 131,171 | 12,494 | (3,776 | ) | 660,916 | |||||||||||||

| Operating expenses |

139,864 | 46,703 | 13,732 | (5,121 | ) | 195,178 | |||||||||||||

| Product purchases |

138,552 | 4,455 | — | (1,485 | ) | 141,522 | |||||||||||||

| Equity earnings |

(2,826 | ) | — | — | — | (2,826 | ) | ||||||||||||

| Operating margin (loss) |

245,437 | 80,013 | (1,238 | ) | 2,830 | 327,042 | |||||||||||||

| Depreciation and amortization |

43,645 | 23,346 | 1,107 | 2,830 | 70,928 | ||||||||||||||

| G&A expenses |

44,232 | 15,393 | 1,761 | — | 61,386 | ||||||||||||||

| Operating profit (loss) |

$ | 157,560 | $ | 41,274 | $ | (4,106 | ) | $ | — | $ | 194,728 | ||||||||

| Segment assets |

$ | 2,170,365 | $ | 828,728 | $ | 38,116 | $ | — | $ | 3,037,209 | |||||||||

| Corporate assets |

49,103 | ||||||||||||||||||

| Total assets |

$ | 3,086,312 | |||||||||||||||||

The increase in segment assets from previously reported periods resulted primarily from the Longhorn acquisition during third quarter 2009 (see Note 5—Acquisitions).

15

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

| 9. | Related Party Disclosures |

Affiliate Entity Transactions

Magellan Partners has a 50% ownership interest in a crude oil pipeline company and is paid a management fee for its operation. During both the three month periods ended September 30, 2008 and 2009, MMP received operating fees from this pipeline company of $0.2 million, which was reported as affiliate management fee revenue. Affiliate management fee revenue for the nine months ended September 30, 2008 and 2009 was $0.5 million and $0.6 million, respectively.

The following table summarizes affiliate costs and expenses that are reflected in the accompanying consolidated statements of income (in thousands):

| Three Months Ended September 30, |

Nine Months Ended September 30, | |||||||

| 2008 | 2009 | 2008 | 2009 | |||||

| MGG GP—allocated operating expenses |

21,335 | 23,969 | 63,887 | 69,523 | ||||

| MGG GP—allocated G&A expenses |

12,140 | 14,813 | 36,648 | 41,890 | ||||

Under MMP’s services agreement with MGG GP, MMP reimburses MGG GP for the costs of employees necessary to conduct its operations and administrative functions. The accrued payroll and benefits accruals associated with this agreement at December 31, 2008 and September 30, 2009 were $21.9 million and $23.0 million, respectively. The long-term pension and benefits accruals associated with this agreement at December 31, 2008 and September 30, 2009 were $31.8 million and $33.8 million, respectively. MMP settles its payroll, payroll-related expenses and non-pension postretirement benefit costs with MGG GP on a monthly basis and funds its long-term affiliate pension liabilities through payments to MGG GP when it makes contributions to its pension funds. Effective with the closing of the Simplification Agreement (see Note 2—Simplification Agreement), MGG GP became a subsidiary of MMP; therefore, these transactions will not be reported as related transactions subsequent to that date.

Historically, MGG reimbursed MMP for G&A expenses, excluding equity-based compensation, in excess of a G&A cap. The amount of G&A costs MGG reimbursed to MMP for the three and nine months ended September 30, 2008 was $0.4 million and $1.2 million, respectively. MGG MH, the former owner of MGG’s general partner, reimbursed MGG for the same amounts MGG reimbursed to MMP for these excess G&A expenses. MGG recorded these reimbursements as a capital contribution from its general partner. No reimbursements were made to MMP for excess G&A costs in 2009.

Other Related Party Transactions

One of MMP GP’s independent board members, John P. DesBarres, served as a board member for American Electric Power Company, Inc. (“AEP”) of Columbus, Ohio until his death in December 2008. During the three and nine months ended September 30, 2008, MMP’s operating expenses included $0.7 million and $1.8 million, respectively, of power costs incurred with Public Service Company of Oklahoma (“PSO”), which is a subsidiary of AEP. MMP had no amounts payable to or receivable from PSO or AEP at December 31, 2008.

Because MMP’s historical distributions exceeded target levels as specified in its partnership agreement, until the completion of the simplification of MMP’s capital structure, MMP GP received approximately 50%, including its approximate 2% general partner interest, of any incremental cash distributed per MMP limited partner unit. Since MGG owned MMP GP during that period, it benefitted from these distributions. For the nine months ended September 30, 2008 and 2009, distributions paid to MMP GP by MMP based on MMP GP’s general partner interest and incentive distribution rights totaled $62.7 million and $70.4 million, respectively. Until December 3, 2008, the executive officers of MGG’s general partner collectively owned a direct interest in MGG MH of approximately 4% (MGG MH owned MGG’s general partner until December 3, 2008). The executive officers of MGG’s general partner, through their ownership in MGG MH, indirectly benefited from MMP’s distributions and directly benefited from MGG’s distributions. As of September 30, 2009, Magellan Partners’ executive officers own less than 1% of Magellan Partners’ common units.

16

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

| 10. | Inventory |

Inventory at December 31, 2008 and September 30, 2009 was as follows (in thousands):

| December 31, 2008 |

September 30, 2009 | |||||

| Refined petroleum products |

$ | 20,917 | $ | 127,094 | ||

| Transmix |

13,099 | 17,849 | ||||

| Natural gas liquids |

7,534 | 38,054 | ||||

| Additives |

6,184 | 7,205 | ||||

| Total inventory |

$ | 47,734 | $ | 190,202 | ||

The increase in refined petroleum products from December 31, 2008 to September 30, 2009 was primarily attributable to the linefill inventory related to the Longhorn acquisition, which totaled $100.9 million as of September 30, 2009. The increase in natural gas liquids was due to the purchase of butane during second and third quarter 2009 in anticipation of the upcoming petroleum products blending season.

| 11. | Employee Benefit Plans |

Magellan Partners sponsors two pension plans for certain union employees, a pension plan for certain non-union employees, a postretirement benefit plan for selected retired employees and a defined contribution plan. The following tables present Magellan Partners’ consolidated net periodic benefit costs related to the pension plans and other postretirement benefit plan during the three and nine months ended September 30, 2008 and 2009 (in thousands):

| Three Months Ended September 30, 2008 |

Nine Months Ended September 30, 2008 |

|||||||||||||||

| Pension Benefits |

Other Post- Retirement Benefits |

Pension Benefits |

Other Post- Retirement Benefits |

|||||||||||||

| Components of Net Periodic Benefit Costs: |

||||||||||||||||

| Service cost |

$ | 1,368 | $ | 109 | $ | 4,104 | $ | 327 | ||||||||

| Interest cost |

675 | 256 | 2,024 | 772 | ||||||||||||

| Expected return on plan assets |

(676 | ) | — | (2,027 | ) | — | ||||||||||

| Amortization of prior service cost (credit) |

77 | (212 | ) | 231 | (639 | ) | ||||||||||

| Amortization of actuarial loss |

37 | 77 | 112 | 231 | ||||||||||||

| Net periodic benefit cost |

$ | 1,481 | $ | 230 | $ | 4,444 | $ | 691 | ||||||||

| Three Months Ended September 30, 2009 |

Nine Months Ended September 30, 2009 |

|||||||||||||||

| Pension Benefits |

Other Post- Retirement Benefits |

Pension Benefits |

Other Post- Retirement Benefits |

|||||||||||||

| Components of Net Periodic Benefit Costs: |

||||||||||||||||

| Service cost |

$ | 1,646 | $ | 73 | $ | 4,937 | $ | 305 | ||||||||

| Interest cost |

802 | 118 | 2,407 | 675 | ||||||||||||

| Expected return on plan assets |

(680 | ) | — | (2,042 | ) | — | ||||||||||

| Amortization of prior service cost (credit) |

76 | (213 | ) | 230 | (638 | ) | ||||||||||

| Amortization of actuarial loss |

408 | (1 | ) | 1,223 | 127 | |||||||||||

| Net periodic benefit cost |

$ | 2,252 | $ | (23 | ) | $ | 6,755 | $ | 469 | |||||||

17

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

| 12. | Debt |

Debt at December 31, 2008 and September 30, 2009 was as follows (in thousands):

| December 31, 2008 |

September 30, 2009 |

Weighted-Average Interest Rate at September 30, 2009 (1) |

|||||||

| Revolving credit facility |

$ | 70,000 | $ | 33,000 | 0.7 | % | |||

| 6.45% Notes due 2014 |

249,681 | 249,719 | 6.3 | % | |||||

| 5.65% Notes due 2016 |

253,328 | 253,005 | 5.7 | % | |||||

| 6.40% Notes due 2018 |

261,555 | 260,643 | 5.9 | % | |||||

| 6.55% Notes due 2019 |

— | 579,266 | 5.0 | % | |||||

| 6.40% Notes due 2037 |

248,921 | 248,931 | 6.3 | % | |||||

| Total debt |

$ | 1,083,485 | $ | 1,624,564 | |||||

| (1) | Weighted-average interest rate includes the impact of the amortization of discounts and gains and losses realized on various hedges (see Note 13—Derivative Financial Instruments for detailed information regarding the amortization of these gains and losses). |

Note discounts and premiums are being amortized or accreted to the applicable notes over their respective lives.

Revolving Credit Facility. The total borrowing capacity under the revolving credit facility, which matures in September 2012, is $550.0 million. Borrowings under the facility are unsecured and bear interest at LIBOR plus a spread ranging from 0.3% to 0.8% based on Magellan Partners’ credit ratings and amounts outstanding under the facility. Additionally, a commitment fee is assessed at a rate from 0.05% to 0.125%, depending on Magellan Partners’ credit ratings. Borrowings under this facility are used for general purposes, including capital expenditures. As of September 30, 2009, $33.0 million was outstanding under this facility and $3.9 million was obligated for letters of credit. Amounts obligated for letters of credit are not reflected as debt on Magellan Partners’ consolidated balance sheets.

6.45% Notes due 2014. In May 2004, MMP sold $250.0 million aggregate principal of 6.45% notes due 2014 in an underwritten public offering. The notes were issued for the discounted price of 99.8%, or $249.5 million.

5.65% Notes due 2016. In October 2004, MMP issued $250.0 million of 5.65% notes due 2016 in an underwritten public offering. The notes were issued for the discounted price of 99.9%, or $249.7 million. The outstanding principal amount of the notes was increased by $3.5 million and $3.2 million at December 31, 2008 and September 30, 2009, respectively, for the unamortized portion of a gain realized upon termination of a related interest rate swap (see Note 13—Derivative Financial Instruments).

6.40% Notes due 2018. In July 2008, MMP issued $250.0 million of 6.40% notes due 2018 in an underwritten public offering. The outstanding principal amount of the notes was increased by $11.6 million and $10.7 million at December 31, 2008 and September 30, 2009, respectively, for the unamortized portion of gains realized upon termination or discontinuation of hedge accounting treatment of associated interest rate swaps (see Note 13—Derivative Financial Instruments).

6.55% Notes due 2019. In June and August 2009, MMP issued $550.0 million of 6.55% notes due 2019 in underwritten public offerings. The notes were issued at a net premium of 103.4%, or $568.7 million. Net proceeds from these offerings, after underwriter discounts of $3.6 million and offering costs of $0.8 million, were $564.3 million. The net proceeds were used to repay, in total, $454.3 million of borrowings outstanding under MMP’s revolving credit facility ($338.4 million of which was related to the Longhorn acquisition), with the balance used for general purposes including capital expenditures. In connection with these offerings, MMP entered into interest rate swap agreements to effectively convert $250.0 million of these notes to floating-rate debt (see Note 13—Derivative Financial Instruments). The outstanding principal amount of the notes was increased by $10.8 million at September 30, 2009 for the fair value of the associated interest rate swap agreements.

6.40% Notes due 2037. In April 2007, MMP issued $250.0 million of 6.40% notes due 2037 in an underwritten public offering. The notes were issued for the discounted price of 99.6%, or $248.9 million.

18

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

| 13. | Derivative Financial Instruments |

Commodity Derivatives

Magellan Partners’ petroleum products blending activities generate gasoline products and Magellan Partners can estimate the timing and quantities of sales of these products. Magellan Partners uses a combination of forward sales contracts and NYMEX agreements to lock in most of the gross margins realized from its blending activities. Magellan Partners accounts for the forward sales contracts as normal sales.

As discussed in Note 6—Product Sales Revenues, MMP began using NYMEX contracts during the third quarter of 2008 as economic hedges against changes in the price of petroleum products it expected to sell from its petroleum products blending activities. From the third quarter of 2008 through the second quarter of 2009, none of the NYMEX contracts MMP entered into qualified for hedge accounting treatment under ASC 815-30, Derivatives and Hedging. However, effective July 2, 2009, because of other agreements that MMP entered into, most of the NYMEX contracts associated with MMP’s petroleum products blending activities qualified for hedge accounting treatment and have been recorded as cash flow hedges. All of these contracts mature within the next twelve months.

During the three and nine months ended September 30, 2009, MMP closed its positions on NYMEX contracts associated with the sale of 0.3 million barrels and 1.4 million barrels, respectively, of gasoline and realized gains (losses) of $(2.9) million and $11.2 million, respectively. At September 30, 2009, the fair value of open NYMEX contracts, representing 2.6 million barrels of petroleum products, was a net liability of $8.2 million, of which $8.9 million was recorded as energy commodity derivative contracts and $0.7 million was recorded as noncurrent assets on its consolidated balance sheet. These open NYMEX contracts mature between October 2009 and August 2011. At September 30, 2009, Magellan Partners had made margin deposits of $8.8 million for these contracts, which it recorded as energy commodity derivatives deposit on its consolidated balance sheet. Magellan Partners has the right to offset the fair value of its open NYMEX contracts against its margin deposits under a master netting arrangement with its counterpart; however, it has elected to separately disclose these amounts on its consolidated balance sheet.

Interest Rate Derivatives

Magellan Partners uses interest rate derivatives to help manage interest rate risk. As of September 30, 2009, Magellan Partners had two offsetting interest rate swap agreements outstanding:

| • | In July 2008, MMP entered into a $50.0 million interest rate swap agreement (“Derivative A”) to hedge against changes in the fair value of a portion of the $250.0 million of 6.40% notes due 2018. Derivative A effectively converted $50.0 million of those notes from a 6.40% fixed rate to a floating rate of six-month LIBOR plus 1.83%. Derivative A terminates in July 2018. MMP originally accounted for Derivative A as a fair value hedge. In December 2008, in order to capture the economic value of Derivative A at that time, MMP entered into an offsetting derivative, as described below, and discontinued hedge accounting for Derivative A. The $5.4 million fair value of Derivative A at that time was recorded as an adjustment to long-term debt which is being amortized over the remaining life of the 6.40% fixed-rate notes due 2018. For the three and nine months ended September 30, 2009, a gain (loss) of $1.6 million and $(1.7) million, respectively, was recorded to other income on Magellan Partners’ consolidated statement of income resulting from the change in fair value of Derivative A, net of semi-annual interest settlement payments. |

| • | In December 2008, concurrent with the discontinuance of hedge accounting for Derivative A, MMP entered into an offsetting $50.0 million interest rate swap agreement with a different financial institution pursuant to which it pays a fixed rate of 6.40% and receives a floating rate of six-month LIBOR plus 3.23%. This agreement terminates in July 2018. MMP entered into this agreement to offset changes in the fair value of Derivative A, excluding adjustments due to changes in counterparty credit risks. This agreement was not designated as a hedge for accounting purposes. For the three and nine months ended September 30, 2009, a gain (loss) of $(1.6) million and $2.3 million, respectively, was recorded to other income on Magellan Partners’ consolidated statement of income resulting from the change in fair value of this agreement, net of semi-annual interest settlement payments. |

Additionally, Magellan Partners had the following interest rate swap agreements outstanding as of September 30, 2009:

| • | In June 2009, MMP entered into a total of $150.0 million of interest rate swap agreements to hedge against changes in the fair value of a portion of the $550.0 million of 6.55% notes due 2019. Magellan Partners accounts for these agreements as |

19

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

| fair value hedges. These agreements effectively convert $150.0 million of Magellan Partners’ 6.55% fixed-rate notes to floating-rate debt. Under the terms of the agreements, Magellan Partners will receive the 6.55% fixed rate of the notes and pay six-month LIBOR in arrears plus 2.18%. The agreements terminate in June 2019, which is the maturity date of the related notes. Payments will settle in January and July each year. During each period, Magellan Partners will record the impact of these swaps based on the forward LIBOR curve. Any differences between actual LIBOR determined on the settlement date and Magellan Partners’ estimate of LIBOR will result in an adjustment to its interest expense. |

| • | In August 2009, MMP entered into a total of $100.0 million of interest rate swap agreements to hedge against changes in the fair value of a portion of the $550.0 million of 6.55% notes due 2019. Magellan Partners accounts for these agreements as fair value hedges. These agreements effectively convert $100.0 million of Magellan Partners’ 6.55% fixed rate notes to floating-rate debt. Under the terms of the agreements, Magellan Partners will receive the 6.55% fixed rate of the notes and pay six-month LIBOR in arrears plus 2.34%. The agreements terminate in June 2019, which is the maturity date of the related notes. Payments will settle in January and July each year. During each period, Magellan Partners will record the impact of these swaps based on the forward LIBOR curve. Any differences between actual LIBOR determined on the settlement date and Magellan Partners’ estimate of LIBOR will result in an adjustment to its interest expense. |

All of the interest rate derivatives discussed above contain credit-risk-related contingent features. These features provide that in the event of Magellan Partners’ default on any obligation of $25.0 million or more or, in certain circumstances a change in control of Magellan Partners’ general partner or a merger in which its credit rating becomes “materially weaker”, which would generally be interpreted as falling below investment grade, the counterparties to Magellan Partners’ interest rate derivatives agreements could terminate those agreements and require immediate settlement. None of Magellan Partners’ interest rate derivatives were in a liability position as of September 30, 2009.

The changes in derivative gains (losses) included in accumulated other comprehensive loss (“AOCL”) for the three and nine months ended September 30, 2008 and 2009 are as follows (in thousands):

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| Derivative Gains (Losses) Included in AOCL |

2008 | 2009 | 2008 | 2009 | ||||||||||||

| Beginning balance |

$ | 3,735 | $ | 3,571 | $ | 3,817 | $ | 3,653 | ||||||||

| Net gain on commodity hedges |

— | 639 | — | 639 | ||||||||||||

| Reclassification of net gain on cash flow hedges to interest expense |

(41 | ) | (41 | ) | (123 | ) | (123 | ) | ||||||||

| Reclassification of net gain on commodity hedges to product sales revenues |

— | (255 | ) | — | (255 | ) | ||||||||||

| Ending balance |

$ | 3,694 | $ | 3,914 | $ | 3,694 | $ | 3,914 | ||||||||

As of September 30, 2009, the net gain estimated to be classified to interest expense and product sales revenues over the next twelve months from AOCL is approximately $0.2 million and $0.4 million, respectively.

20

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

The following is a summary of the current impact of MMP’s historical derivative activity on long-term debt resulting from the termination of or the discontinuance of hedge accounting treatment of Magellan Partners’ fair value hedges as of and for the three and nine months ended September 30, 2009 (in thousands):

| As of September 30, 2009 |

Three Months Ended September 30, 2009 |

Nine Months Ended September 30, 2009 |

||||||||||||

| Hedge |

Total Gain Realized |

Unamortized Amount Recorded in Long-term Debt |

Amount Reclassified to Interest Expense from Long-term Debt |

Amount Reclassified to Interest Expense from Long-term Debt |

||||||||||

| Fair value hedges (date executed): |

||||||||||||||

| Interest rate swaps 6.40% Notes (July 2008) |

$ | 11,652 | $ | 10,662 | $ | (304 | ) | $ | (912 | ) | ||||

| Interest rate swaps 5.65% Notes (October 2004) |

3,830 | 3,207 | (114 | ) | (341 | ) | ||||||||

| Total fair value hedges |

$ | 13,869 | $ | (418 | ) | $ | (1,253 | ) | ||||||

The following is a summary of the effect of derivatives accounted for under ASC 815-25, Derivatives and Hedging—Fair Value Hedges, that were designated as hedging instruments on Magellan Partners’ consolidated statement of income for the three and nine months ended September 30, 2009 (in thousands):

| Amount of Gain Recognized on Derivative |

Amount of Interest Expense Recognized on Fixed-Rate Debt (Related Hedged Item) |

|||||||||||||||

| Derivative Instrument |

Location of Gain |

Three Months Ended September 30, 2009 |

Nine Months Ended September 30, 2009 |

Three Months Ended September 30, 2009 |

Nine Months Ended September 30, 2009 |

|||||||||||

| Interest rate swap agreements |

Interest expense |

$ | 1,516 | $ | 1,564 | $ | (6,997 | ) | $ | (7,271 | ) | |||||

The following is a summary of the effect of derivatives accounted for under ASC 815-30, Derivatives and Hedging—Cash Flow Hedges, that were designated as hedging instruments on Magellan Partners’ consolidated statement of income for the three and nine months ended September 30, 2009 (in thousands):

| Effective Portion | ||||||||||||||

| Amount of Gain Recognized in AOCL on Derivative |

Location of Gain Reclassified from AOCL into Income |

Amount of Gain Reclassified from AOCL into Income | ||||||||||||

| Derivative Instrument |

3Q09 | 2009 | 3Q09 | 2009 | ||||||||||

| Interest rate swap agreements |

$ | — | $ | — | Interest expense | $ | 41 | $ | 123 | |||||

| NYMEX commodity contracts |

639 | 639 | Product sales revenues | 255 | 255 | |||||||||

| Total cash flow hedges |

$ | 639 | $ | 639 | $ | 296 | $ | 378 | ||||||

There was no ineffectiveness recognized on the financial instruments disclosed in the above table during the three and nine months ended September 30, 2009.

21

Table of Contents

MAGELLAN MIDSTREAM PARTNERS, L.P.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

The following is a summary of the effect of derivatives accounted for under ASC 815-10-35; Paragraph 2, Derivatives and Hedging—Overall—Subsequent Measurement, that were not designated as hedging instruments on Magellan Partners’ consolidated statement of income for the three and nine months ended September 30, 2009 (in thousands):

| Amount of Gain (Loss) Recognized on Derivative |

||||||||||

| Derivative Instrument |

Location of Gain (Loss) Recognized on Derivative |

Three Months Ended September 30, 2009 |

Nine Months Ended September 30, 2009 |

|||||||

| Interest rate swap agreements |

Other income |

$ | (11 | ) | $ | 636 | ||||

| NYMEX commodity contracts |

Product sales revenues |

5,607 | (17,778 | ) | ||||||

| Total |

$ | 5,596 | $ | (17,142 | ) | |||||

The following is a summary of the amounts included in Magellan Partners’ consolidated balance sheet of the fair value of derivatives accounted for under ASC 815-25, Derivatives and Hedging—Fair Value Hedges, that were designated as hedging instruments as of September 30, 2009 (in thousands):

| Asset Derivatives |