Attached files

Table of Contents

As filed with the Securities and Exchange Commission on November 3, 2009

No. 333-161381

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 3

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

HealthPort, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 7389 | 27-0717051 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

925 North Point Parkway

Suite 350

Alpharetta, Georgia 30005

(770) 670-2150

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Michael J. Labedz

President and Chief Executive Officer

HealthPort, Inc.

925 North Point Parkway

Suite 350

Alpharetta, Georgia 30005

(770) 670-2150

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

| Joshua N. Korff, Esq. Jason K. Zachary, Esq. Kirkland & Ellis LLP 601 Lexington Avenue New York, New York 10022 (212) 446-4800 |

Wayne D. Boberg, Esq. Matthew F. Bergmann, Esq. Winston & Strawn LLP 35 West Wacker Drive Chicago, Illinois 60601 (312) 558-5600 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

| Large accelerated filer ¨ |

Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) | ||||||

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered |

Amount to be |

Proposed Maximum |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(2)(3) | ||||

| Common Stock, $0.001 par value per share |

6,900,000 shares | $16.00 | $110,400,000 | $6,161 | ||||

| (1) | Includes shares of common stock that the underwriters have the option to purchase from us to cover over-allotments, if any. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(a) under the Securities Act of 1933, as amended. |

| (3) | Previously paid. |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

EXPLANATORY NOTE

HealthPort, Inc., the registrant whose name appears on the cover page of this registration statement, is a newly formed Delaware corporation. Shares of common stock of HealthPort, Inc. are being offered by this prospectus. We were formed solely for the purpose of reorganizing the organizational structure of CT Technologies Holdings, LLC in order for the registrant to be a corporation rather than a limited liability company. Prior to the effectiveness of this registration statement, each member of CT Technologies Holdings, LLC will contribute all of their equity interests in CT Technologies Holdings, LLC to us in return for our common stock and senior preferred stock. As a result, CT Technologies Holdings, LLC will become our wholly-owned subsidiary. We intend to use a portion of the net proceeds from this offering to redeem in whole our senior preferred stock. The consolidated financial statements and consolidated financial data included in this prospectus are those of CT Technologies Holdings, LLC and its consolidated subsidiaries and do not give effect to the corporate reorganization.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, Dated November 3, 2009

PROSPECTUS

HealthPort, Inc.

6,000,000 Shares

Common Stock

This is the initial public offering of HealthPort, Inc. We are offering 6,000,000 shares of our common stock. We anticipate that the initial public offering price will be between $14.00 and $16.00 per share. We have applied to have our common stock approved for listing on The NASDAQ Global Market under the symbol “HPRT.”

After this offering, ABRY Partners, LLC, through its affiliated funds, will own approximately 56% of our common stock. We intend to use a portion of the net proceeds from this offering for the redemption in whole of our senior preferred stock and the remaining net proceeds for the repayment of a portion of our outstanding indebtedness.

Investing in our common stock involves risk. See “Risk Factors” beginning on page 15.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||

| Public offering price |

$ | $ | ||||

| Underwriting discounts and commissions |

$ | $ | ||||

| Proceeds, before expenses, to HealthPort, Inc. |

$ | $ | ||||

We have granted the underwriters the right to purchase up to 900,000 additional shares of common stock to cover over-allotments.

Delivery of the shares of common stock in book-entry form only will be made on or about , 2009.

| Deutsche Bank Securities | William Blair & Company |

| Raymond James | Needham & Company, LLC | |

The date of this prospectus is , 2009.

Table of Contents

ABOUT THIS PROSPECTUS

We have a number of registered trademarks, including our corporate blue and grey logo and design. Solely for convenience, we refer to our trademarks in this prospectus without the™ and® symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights to our trademarks. This prospectus may contain trademarks and trade names of other companies. All trademarks and trade names appearing in this prospectus are the property of their respective holders.

INDUSTRY AND MARKET DATA

This prospectus includes market share and industry data and forecasts that we have obtained or developed from independent consultant reports, publicly-available information, various industry publications, other published industry sources and our internal data and estimates. This includes information relating to the healthcare industry from several independent outside sources, including International Data Corp., Frost & Sullivan, the U.S. Centers for Medicare and Medicaid Services, the American Health Information Management Association and various other governmental agencies. See “Business.”

Our internal data, estimates and forecasts are based upon information obtained from our customers, partners, trade and business organizations and other contacts in the markets in which we operate and our management’s understanding of industry conditions.

i

Table of Contents

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our common stock, you should carefully read this entire prospectus, including our consolidated financial statements and the related notes and the information set forth under the headings “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in each case included elsewhere in this prospectus. Some of the statements in this prospectus constitute forward-looking statements. See “Forward-Looking Statements.”

We are a newly formed Delaware corporation that has not, to date, conducted any activities other than those incident to our formation and the preparation of this registration statement. We were formed solely for the purpose of reorganizing the organizational structure of CT Technologies Holdings, LLC in order for the registrant to be a corporation rather than a limited liability company. Prior to the effectiveness of this registration statement, each member of CT Technologies Holdings, LLC will contribute all of their equity interests in CT Technologies Holdings, LLC to us in return for our common stock and senior preferred stock. As a result, CT Technologies Holdings, LLC will become our wholly-owned subsidiary. We refer to the foregoing as our corporate reorganization. Except where the context otherwise requires or where otherwise indicated, (i) the terms “we,” “us,” “our,” “our company,” “our business” and “Successor” refer to HealthPort, Inc. and its consolidated subsidiaries as a combined entity, giving effect to our corporate reorganization and (ii) the term “Predecessor” or “Companion” refers to Companion Technologies Corporation. See “— Our Corporate Structure.” Certain differences in the numbers in the tables and text throughout this prospectus may exist due to rounding.

Our Business

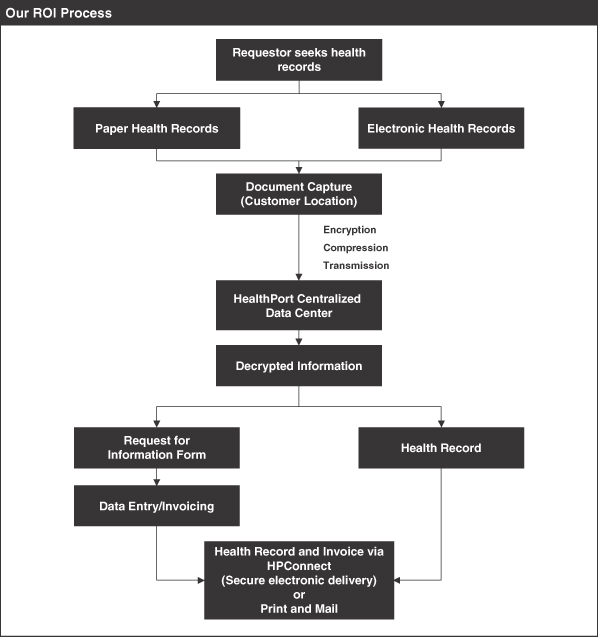

We are a leading provider of healthcare information services and technology solutions to approximately 1,900 hospitals and health systems and 8,000 independent and hospital-affiliated physician clinics. Our primary business is providing outsourced technology-enabled release-of-information services to our customers, which we refer to as ROI. ROI is the process by which information contained in patient health records is requested by and provided to authorized requestors such as attorneys, insurance companies, government agencies and others. We believe we are the largest provider of ROI services with a market share of approximately 20%, and utilize our expertise and technology to fulfill requests for health records in an accurate, regulatory-compliant and timely manner. Our ROI services enable our customers to reduce staffing levels associated with these time-consuming and labor-intensive healthcare information functions, allowing them to increase their focus on patient care, and to more effectively comply with increasingly complex and cumbersome regulatory requirements. We also provide other software and services which complement our ROI services, including recovery audit compliance solutions, revenue cycle management software, healthcare coding and consulting services and physician practice management software.

Our centralized operating model, combined with our proprietary technology platform, is unique to the ROI industry and enables greater economies of scale as well as expedited response times and high service levels. Unlike our competitors’ ROI service offerings, which typically involve simply photocopying and mailing health records, we employ on-site digital

1

Table of Contents

imaging and electronically transfer the requested health record via an encrypted Internet-based channel to our centralized data center, from which we are able to deliver the information in either electronic or paper-based form based on the requestor’s preferred medium.

Healthcare providers are required by law to provide ROI services. We estimate, based upon publicly available market information, the total market for ROI services to be approximately $1.2 billion, of which we estimate approximately $500 million relates to hospitals and health systems and $700 million relates to independent and hospital-affiliated physician clinics. We estimate that approximately two-thirds of these services are performed using internal resources, while one-third is outsourced to third-party vendors. We believe we are the largest outsourced ROI provider with approximately 70% of the outsourced market. Requestors pay the healthcare provider or outsourced service provider for retrieval and delivery of the health record directly, in accordance with a fee schedule typically established by state regulation. As a result, unlike healthcare providers, we are not affected by changes in regulated reimbursement rates by commercial payers, Medicare or Medicaid. We believe that the complexity of healthcare regulation, as well as recent federal initiatives to control the rising cost of healthcare through the elimination of administrative and clinical inefficiencies, will significantly increase the adoption of healthcare information systems and promote the use of electronic transactions and further utilization of our outsourced services and solutions.

For the twelve months ended December 31, 2008, we generated net revenue of $188.2 million and incurred a net loss of $49.8 million. For the twelve months ended December 31, 2008, we generated pro forma net revenue of $242.1 million and incurred a pro forma loss from continuing operations of $59.2 million, inclusive of the September 2008 acquisition of ChartOne, Inc., or ChartOne, as if acquired on January 1, 2008. For the nine months ended September 30, 2009, we generated net revenue of $193.2 million and incurred a net loss of $8.9 million. Our board of directors and management also use Adjusted EBITDA, a non-GAAP financial measure, as one of the primary measures for planning and forecasting overall expectations and for evaluating, on at least a quarterly and annual basis, our financial performance. See page 12 for a discussion of Adjusted EBITDA, an accompanying presentation of the most directly comparable GAAP financial measure and a reconciliation of the differences between Adjusted EBITDA and the most directly comparable GAAP financial measure.

Our Services and Solutions

We conduct our operations through two business segments: Release-of-Information Services and Software and Other Services. All of our services and solutions are supported by our proprietary technology platform. This infrastructure provides for connectivity between us, our hospital, health system and physician clinic customers, health record requestors and other constituents. In addition, it allows for functionality developed in our software and other services segment to be leveraged in our ROI services to enhance the value proposition to our customers.

Release-of-Information Services

We offer ROI services on an outsourced basis to hospitals, health systems and physician clinics. Our centralized operating model coupled with our proprietary technology platform enable us to offer important benefits to our ROI customers, including expedited response times

2

Table of Contents

and high service levels. We provide user-friendly, secure on-line tracking functionality for both requestors and customers with extensive reporting capabilities. We also offer the ability for qualified requestors to access their health record requests on-line, and our flexible platform allows most electronic health record, or EHR, systems to integrate into our proprietary technology. To accommodate paper-based requests, our centralized data center uses an automated document processing system. This system performs address verification and electronic pre-sort functions, produces postage statements and prints, packages and seals the requested materials, resulting in high efficiency levels.

Software and Other Services

Our software and other services segment provides solutions that complement our ROI services, including recovery audit contractor, or RAC, compliance solutions, revenue cycle management, or RCM, software, healthcare coding and consulting services and physician practice management software. Our RAC solution allows our customers to prepare for and comply with a new Medicare payment recovery system that is being phased in and is scheduled for nationwide implementation in 2010, helping them track and organize health record requests, coding, billing, reviews and all associated paperwork. Our RCM software enables healthcare providers to ensure that payment is properly received for the medical services provided to patients. Our healthcare coding and consulting services include compliance expertise with the Health Insurance Portability and Accountability Act, or HIPAA, data management, compliance auditing, education, master patient index classification and medical coding. Our practice management software assists physician practices with administrative tasks such as patient information tracking, appointment scheduling and billing.

Our Strengths

Leading Market Position. We believe we are the largest ROI service provider to the healthcare industry with approximately 20% of the ROI services market. We believe that approximately two-thirds of ROI services are performed using internal resources and the remaining one-third is outsourced to third-party vendors. We believe we are the largest outsourced ROI provider with approximately 70% of the outsourced market. The remaining portion of the market is highly fragmented, consisting primarily of regional and local providers. As a result of increased legislative complexity and cost containment initiatives, we believe healthcare providers are increasingly adopting an outsourced strategy.

Advanced ROI Services. Our centralized operating model, combined with our proprietary technology platform, is unique to the outsourced ROI industry and allows for greater efficiencies and accuracy in processing health information requests. We employ on-site digital imaging, which enables requested health records to be transmitted electronically to our centralized data center, driving significant economies of scale.

Compelling Value Proposition. We offer a compelling value proposition for hospitals, health systems and physician clinics by allowing these healthcare providers to reduce staffing levels associated with time-consuming and labor-intensive healthcare information management functions. A reduced administrative burden allows our customers to focus on patient care and more effectively comply with complex regulatory requirements.

Highly Predictable Revenue Model. We operate a highly predictable and non-cyclical business model, and our ROI customer retention rates have historically exceeded 95%. In

3

Table of Contents

addition, the majority of our ROI customers have entered into multi-year contracts with us, which typically generate recurring volumes of health record requests. In excess of 95% of our revenue are repeat or recurring in nature because of the contractual nature of our business.

Strong Cash Flow with Low Capital Requirements. Our business generates strong, stable cash flows as a result of our significant operating leverage, our relatively low working capital requirements and the modest capital expenditures needed to support our infrastructure. In addition, to the extent that we can generate pre-tax income in the future, we expect to be able to use our approximately $126 million of federal net operating loss carryforwards, as of December 31, 2008, to offset our potential future taxable income, subject to federal tax limitations.

Diversified Customer Base. We serve approximately 1,900 hospitals and health systems and 8,000 independent and hospital-affiliated physician clinics, with no single customer accounting for more than 1% of our revenue. In addition, our customers are also highly diversified by geography, type and size, with customers ranging from national hospital systems and academic institutions to small rural clinics.

Experienced Management Team. We have assembled a highly experienced management team. Our senior management team averages more than 20 years of healthcare industry experience.

Our Growth Strategy

Increase Penetration of ROI Services Market. We believe that the overall trend towards outsourcing non-core functions across the healthcare industry will continue to apply to the outsourcing of the ROI process. The increasing complexity of healthcare legislation in combination with recent federal initiatives to control the rising cost of healthcare through the elimination of administrative and clinical inefficiencies will further accelerate the outsourcing trend and, we believe, increase the use of our outsourcing services by hospitals, health systems and physician clinics. We also believe that our proprietary technology and our ability to help our customers maintain regulatory compliance while reducing costs will continue to allow us to successfully differentiate our ROI services from those of our competitors and increase our market share.

Enhance Our Value Proposition through New Services and Solutions. We leverage our ROI services platform to develop and drive the adoption of new services and solutions within the healthcare information management function of our customers. Our long-standing customer relationships provide us with ongoing opportunities to examine our customers’ needs and to design and offer additional value-added services and solutions to address those needs.

Capitalize on Industry Trends. We believe that increasing regulatory complexity, advancements in information technology and the continued growth in the volume of health records will continue to drive ROI industry growth and will cause more healthcare providers to outsource ROI services.

Further Realize Efficiencies of Scale and Rationalize Costs to Improve Profitability. We evaluate and implement initiatives on an ongoing basis to improve our operating and financial performance through cost savings, productivity improvements and streamlining our operations by using new technologies.

4

Table of Contents

Continue to Successfully Acquire and Integrate Businesses. We have grown our business both organically and through acquisitions and have successfully acquired and integrated multiple businesses across the ROI and healthcare information technology sectors. We intend to continue to selectively acquire businesses that will expand our services and solutions while enhancing value for our company.

Risk Factors

Investing in our company entails a high degree of risk, including those summarized below and those more fully described in the “Risk Factors” section beginning on page 15 of this prospectus. You should consider carefully such risks before deciding to invest in our common stock. These risks include, among others:

| • | our ability to retain existing customers; |

| • | our limited operating history in light of recent acquisitions and growth, including our lack of public company operating experience; |

| • | the integration of acquired businesses, the performance of acquired businesses and the prospects for future acquisitions; |

| • | our history of operating losses and ability to use net loss carryforwards; |

| • | competition in the markets in which we serve; |

| • | changes in prices set by various state legislatures and regulatory bodies; |

| • | our ability to increase market penetration in the in-sourced ROI services market; |

| • | departure of key executives; |

| • | changes in healthcare laws and regulations; and |

| • | the other factors set forth under “Risk Factors.” |

Our Principal Stockholder

Following the completion of this offering, ABRY Partners, LLC, which we refer to as ABRY Partners, through its affiliated funds, will own approximately 56% of our outstanding common stock, or 54% if the underwriters’ over-allotment option is fully exercised. This ownership of our shares by ABRY Partners will result in their ability to have a majority vote over fundamental and significant corporate matters and transactions. See “Risk Factors — Risks Related to Our Organization and Structure.”

Founded in 1989, ABRY Partners is a leading media, communications and information services-focused private equity investment firm. ABRY Partners invests in high quality companies and partners with management to help build their businesses. Since its founding, ABRY Partners has completed over $21.0 billion of transactions, including private equity, mezzanine and preferred equity placements, representing investments in approximately 450 businesses. ABRY Partners is headquartered in Boston, Massachusetts.

5

Table of Contents

Corporate Reorganization

We are a newly formed Delaware corporation that has not, to date, conducted any activities other than those incident to our formation and the preparation of this registration statement. We were formed solely for the purpose of reorganizing the organizational structure of CT Technologies Holdings, LLC in order for the registrant to be a corporation rather than a limited liability company. Prior to the effectiveness of this registration statement, each member of CT Technologies Holdings, LLC will contribute all of their equity interests, including all Series A, B and C shares and all senior preferred shares, in CT Technologies Holdings, LLC to us in return for shares of our common stock and senior preferred stock. After each member contributes all of their equity interests in CT Technologies Holdings, LLC to us, CT Technologies Holdings, LLC will become our wholly-owned subsidiary. If any equity interests are not contributed to us prior to effectiveness of this registration statement, CT Technologies Holdings, LLC will be merged with and into us and we will issue shares of our common stock or senior preferred stock, as applicable, in accordance with the terms of the CT Technologies Holdings, LLC Agreement to such non-contributing members, if any, and their equity interests will be cancelled. We refer to these events as our corporate reorganization.

As a result of the corporate reorganization, CT Technologies Holdings, LLC’s Series A and C shares will be exchanged for 15,163,138 shares of our common stock based upon a price of $15.00 per share, the midpoint of the range set forth on the cover page of this prospectus. In addition, any outstanding Series B-1 and B-2 shares that have vested on or prior to our corporate reorganization will be exchanged for 1,433,371 shares of our common stock based upon a price of $15.00 per share, the midpoint of the range set forth on the cover page of this prospectus. The number of shares of common stock issued in connection with our corporate reorganization will not be adjusted based on the actual initial public offering price of our common stock. Holders of unvested Series B-1 and B-2 shares will not receive any consideration in connection with the corporate reorganization. Upon completion of this offering, we intend to issue 146,398 shares of restricted stock and stock options to exercise 2,036,200 shares of common stock to our directors and director nominees and certain other officers and key personnel. In addition, shares of CT Technologies Holdings, LLC’s senior preferred shares will be exchanged for shares of our senior preferred stock prior to the effectiveness of this registration statement. The senior preferred stock will have substantially similar preferences, powers, rights, limitations and restrictions as the senior preferred shares. We intend to use a portion of the net proceeds from this offering for the redemption in whole of our senior preferred stock. See “Corporate Reorganization” and “Description of Capital Stock — Senior Preferred Stock.”

For further information regarding the ownership of our common stock by our executive officers and members of our board of directors, see “Certain Relationships and Related Party Transactions” and “Security Ownership of Certain Beneficial Owners.”

6

Table of Contents

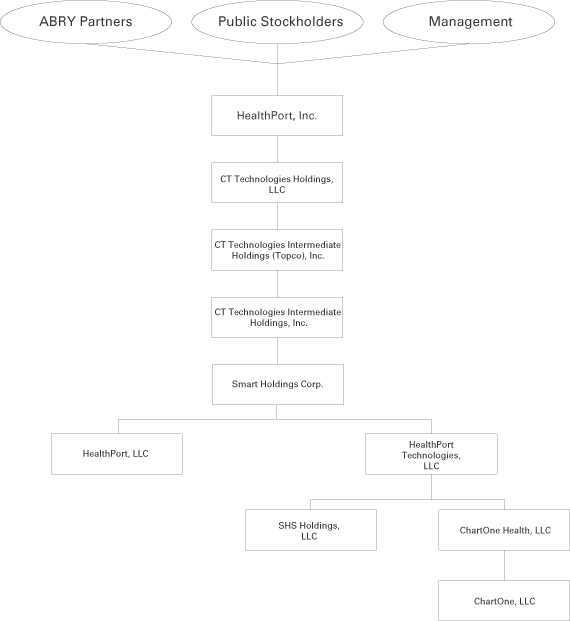

Our Corporate Structure

The following chart indicates our corporate structure following our corporate reorganization and the offering contemplated by this prospectus.

| (1) | Each HealthPort entity in the chart above is a wholly-owned subsidiary of its respective parent. |

7

Table of Contents

Corporate and Other Information

We are a newly formed Delaware corporation that has not, to date, conducted any activities other than those incident to our formation and the preparation of this registration statement. Our principal executive offices are located at 925 North Point Parkway, Suite 350, Alpharetta, Georgia 30005 and our telephone number is (770) 670-2150. Our corporate website address is www.healthport.com. We do not incorporate the information contained on, or accessible through, our corporate website into this prospectus, and you should not consider it part of this prospectus.

8

Table of Contents

The Offering

| Common stock offered by us |

6,000,000 shares. |

| 6,900,000 shares if the underwriters exercise their over- allotment option in full. |

| Total common stock to be outstanding immediately after this offering |

22,596,509 shares. |

| 23,496,509 shares if the underwriters exercise their over-allotment option in full. |

| Preferred stock outstanding |

We intend to use a portion of the net proceeds from this offering for the redemption in whole of our senior preferred stock. See “Description of Capital Stock — Senior Preferred Stock.” |

| Principal stockholders |

Upon completion of this offering, funds affiliated with ABRY Partners, LLC will own a controlling interest in us. We intend to avail ourselves of the controlled company exception under the corporate governance rules of The NASDAQ Stock Market. |

| Use of proceeds |

We estimate that the net proceeds to us from this offering, after deducting underwriting discounts and commissions and estimated offering expenses, will be approximately $79.8 million, assuming the shares are offered at $15.00 per share, the midpoint of the price range set forth on the cover page of this prospectus. We intend to use the net proceeds we receive from this offering to (i) redeem in whole our senior preferred stock, which amounts to approximately $43.8 million, including payment of the early redemption fee and (ii) repay approximately $36.0 million outstanding principal and accrued cash interest under our senior subordinated notes, including payment of an early prepayment fee. If the underwriters exercise their over-allotment option, we intend to use any additional net proceeds to repay a portion of our borrowings under our senior secured credit facility and senior subordinated notes and for general corporate purposes, which we intend to use for the further repayment of borrowings under our senior secured credit facility. See “Use of Proceeds” and “Description of Certain Indebtedness.” |

| Dividend policy |

We have not declared or paid any dividends on our common stock. We cannot pay any dividends on our common stock until we have redeemed and paid in full our senior preferred stock, which we intend to redeem in whole in connection with this offering. Our ability to pay dividends on our common stock is also limited by the covenants of our senior secured credit facility and may be further restricted by the terms of any of our future debt or preferred securities. See “Dividend Policy.” |

9

Table of Contents

| Risk Factors |

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 15 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

| Proposed symbol for trading on The NASDAQ Global Market |

“HPRT” |

Unless otherwise indicated, all information in this prospectus:

| • | gives effect to the corporate reorganization; |

| • | excludes 2,182,598 shares of restricted stock and stock options to be granted to our directors and director nominees and certain officers and key employees upon completion of this offering; |

| • | excludes 4,000,000 shares of common stock reserved for future grants under our omnibus incentive plan, which we plan to adopt in connection with this offering; and |

| • | assumes the underwriters will not exercise their over-allotment option. |

10

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA

The following table sets forth our summary consolidated financial and other data for the periods and at the dates indicated. We derived the statements of operations data presented below for the period from January 1, 2006 through December 30, 2006 (Predecessor) and years ended December 31, 2007 and 2008 (Successor) from our audited consolidated financial statements included elsewhere in this prospectus. The unaudited pro forma statement of operations for the year ended December 31, 2008 gives effect to the acquisition of ChartOne as if it occurred at the beginning of such period. The unaudited pro forma statement of operations data was prepared in accordance with Article 11 of Regulation S-X and is more fully presented in our pro forma consolidated financial information section beginning on page F-114 of this prospectus. We derived the statements of operations data and selected balance sheet data for the nine months ended September 30, 2008 and 2009 and the historical balance sheet data as of September 30, 2009 from our unaudited consolidated financial statements included elsewhere in this prospectus. We have prepared the unaudited consolidated financial information set forth below on the same basis as our audited consolidated financial statements and have included all adjustments that we consider necessary for a fair presentation of our financial position and operating results for such periods. The interim results set forth below are not necessarily indicative of our future performance and do not reflect results for the year ending December 31, 2009 or for any other period.

On December 30, 2006, ABRY Partners and its co-investors, together with certain members of our board of directors, our executive officers and other members of management, through CT Technologies Holdings, LLC, acquired Companion Technologies Corporation. All periods prior to December 30, 2006 are referred to as Predecessor, and all periods including and after such date are referred to as Successor. There were no material operating results on December 31, 2006 as it fell on a Sunday. The consolidated financial statements for all Successor periods are not comparable to those of the Predecessor periods.

The as adjusted balance sheet data gives effect to the receipt and application of $79.8 million of net proceeds to us from this offering as described in “Use of Proceeds,” as if it had occurred as of September 30, 2009. The as adjusted balance sheet data is not necessarily indicative of what our financial position would have been if this offering had been completed as of the date indicated, nor is such data necessarily indicative of our financial position for any future date or period.

Our historical results are not necessarily indicative of future operating results. You should read the information set forth below in conjunction with “Risk Factors,” “Selected Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes included elsewhere in this prospectus.

11

Table of Contents

| (in thousands) | ||||||||||||||||||||||||||

| Predecessor | Successor | |||||||||||||||||||||||||

| Period from January 1, 2006 Through December 30, 2006 |

Year Ended December 31, |

Pro Forma Year Ended December 31, 2008 |

Nine Months Ended September 30, |

|||||||||||||||||||||||

| 2007 | 2008 | 2008 | 2009 | |||||||||||||||||||||||

| (unaudited) | ||||||||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||||||||

| Net revenue |

$ | 38,267 | $ | 102,369 | $ | 188,169 | $ | 242,077 | $ | 127,722 | $ | 193,190 | ||||||||||||||

| Expenses: |

||||||||||||||||||||||||||

| Cost of services and products (exclusive of items shown separately below) |

12,663 | 54,318 | 109,973 | 144,570 | 72,647 | 111,251 | ||||||||||||||||||||

| Bad debt expense (recovery) |

(185 | ) | 3,216 | 9,088 | 10,293 | 6,536 | 8,301 | |||||||||||||||||||

| Selling, general and administrative |

31,744 | 40,287 | 56,575 | 73,575 | 38,988 | 45,889 | ||||||||||||||||||||

| Depreciation and amortization |

676 | 6,099 | 12,183 | 16,569 | 8,689 | 10,887 | ||||||||||||||||||||

| Impairment of goodwill and intangible assets |

— | — | 25,966 | 25,966 | — | — | ||||||||||||||||||||

| Total operating costs and expenses |

44,898 | 103,920 | 213,785 | 270,973 | 126,860 | 176,328 | ||||||||||||||||||||

| Income (loss) from operations |

(6,631 | ) | (1,551 | ) | (25,616 | ) | (28,896 | ) | 862 | 16,862 | ||||||||||||||||

| Interest income (expense), net |

60 | (10,333 | ) | (20,906 | ) | (29,746 | ) | (13,214 | ) | (22,863 | ) | |||||||||||||||

| Change in fair value of interest rate swaps |

— | 7 | (1,945 | ) | (1,945 | ) | — | (741 | ) | |||||||||||||||||

| Equity in net gains of affiliates |

1,426 | — | — | — | — | — | ||||||||||||||||||||

| Loss on transfer of investment in affiliate |

(223 | ) | — | — | — | — | — | |||||||||||||||||||

| Loss from continuing operations before income tax benefit (expense) |

(5,368 | ) | (11,877 | ) | (48,467 | ) | (60,587 | ) | (12,352 | ) | (6,742 | ) | ||||||||||||||

| Income tax benefit (expense) |

853 | 5,258 | 1,409 | 1,387 | (554 | ) | (1,574 | ) | ||||||||||||||||||

| Loss from continuing operations |

(4,515 | ) | (6,619 | ) | (47,058 | ) | (59,200 | ) | (12,906 | ) | (8,316 | ) | ||||||||||||||

| Other Financial Data: |

||||||||||||||||||||||||||

| Adjusted EBITDA(1) |

$ | 1,312 | $ | 6,968 | $ | 18,765 | $ | 28,337 | $ | 12,941 | $ | 30,780 | ||||||||||||||

12

Table of Contents

| Successor | ||||||

| At September 30, 2009 | As Adjusted At September 30, 2009 | |||||

| (unaudited) (in thousands) | ||||||

| Balance Sheet Data: |

||||||

| Cash and cash equivalents |

$ | 2,191 | $ | 2,191 | ||

| Total assets |

332,308 | 332,308 | ||||

| Total debt(2) |

247,446 | 174,773 | ||||

| Total equity |

32,277 | 113,566 | ||||

| (1) | We define Adjusted EBITDA as income (loss) from continuing operations before interest expense (income), income tax (expense) benefit, depreciation and amortization, impairment of intangible assets, non-cash equity-based compensation expense, severance expense, integration costs, amortization of capitalized software development (included in our cost of services and products) and other non-recurring and non-cash items. We use Adjusted EBITDA to facilitate a comparison of our operating performance on a consistent basis from period to period that, when viewed in combination with our results under U.S. generally accepted accounting principles, or GAAP, and the following reconciliation, we believe provides a more complete understanding of factors and trends affecting our business than GAAP measures alone. We believe Adjusted EBITDA assists our board of directors, management and investors in comparing our operating performance on a consistent basis because it removes the impact of our capital structure (such as interest expense and acquisition costs), asset base (such as depreciation and amortization) and items outside the control of our management team (such as income taxes), as well as other non-cash (such as purchase accounting adjustments, equity-based compensation expense and impairment of intangible assets) and non-recurring items (such as litigation expenses and acquisition costs), from our operations. Despite the importance of this measure in analyzing our business and evaluating our operating performance, Adjusted EBITDA has limitations as an analytical tool, and you should not consider it in isolation, or as a substitute for analysis of our results as reported under GAAP; nor is Adjusted EBITDA intended to be a measure of liquidity or free cash flow for our discretionary use. Some of the limitations of Adjusted EBITDA are: |

| • | Adjusted EBITDA does not reflect our cash expenditures or future requirements for capital expenditures or contractual commitments; |

| • | Adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs; |

| • | Adjusted EBITDA does not reflect the interest expense or the cash requirements to service interest or principal payments under our credit agreement; |

| • | Adjusted EBITDA does not reflect income tax payments we are required to make; and |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized often will have to be replaced in the future, and Adjusted EBITDA does not reflect any cash requirements for such replacements. |

| To properly and prudently evaluate our business, we encourage you to review the financial statements included elsewhere in this prospectus and not rely on any single financial measure to evaluate our business. We also strongly urge you to review the reconciliation of loss from continuing operations to Adjusted EBITDA. Adjusted EBITDA, as presented in this prospectus, may differ from and may not be comparable to similarly titled measures used by other companies because Adjusted EBITDA is not a measure of financial performance under GAAP and is susceptible to varying calculations. The following table sets forth a reconciliation of loss from continuing operations, a comparable GAAP-based measure, to Adjusted EBITDA. All of the items included in the reconciliation from loss from continuing operations to Adjusted EBITDA are either (i) non-cash items (such as depreciation and amortization, equity-based compensation expense, purchase accounting adjustments and impairment of intangible assets), (ii) items that management does not consider in assessing our on going operating performance (such as income taxes and interest expense) or (iii) non-recurring items. In the case of the non-cash items, management believes that investors can better assess our comparative operating performance because the measures without such items are less susceptible to variances in actual performance resulting from depreciation, amortization and other non-cash charges and more reflective of other factors that affect operating performance. In the case of the other items, management believes that investors can better assess our operating performance if the measures are presented without these items because their financial impact does not reflect ongoing operating performance. |

13

Table of Contents

The following is a reconciliation of loss from continuing operations to Adjusted EBITDA for the periods presented (in thousands):

| Predecessor | Successor | |||||||||||||||||||||||||

| Period From January 1, 2006 Through December 30, 2006 |

December 31, 2007 |

December 31, 2008 |

December 31, 2008 Non-GAAP With Acquisition(a) |

Nine Months Ended September 30, |

||||||||||||||||||||||

| 2008 | 2009 | |||||||||||||||||||||||||

| (unaudited) | ||||||||||||||||||||||||||

| Loss from continuing operations |

$ | (4,515 | ) | $ | (6,619 | ) | $ | (47,058 | ) | $ | (59,200 | ) | $ | (12,906 | ) | $ | (8,316 | ) | ||||||||

| Depreciation and amortization |

676 | 6,099 | 12,183 | 16,569 | 8,689 | 10,887 | ||||||||||||||||||||

| Amortization of capitalized software development |

— | 2,000 | 2,375 | 2,375 | 1,715 | 702 | ||||||||||||||||||||

| Impairment of goodwill and intangible assets |

— | — | 25,966 | 25,966 | — | — | ||||||||||||||||||||

| Interest expense, net |

(60 | ) | 10,333 | 20,906 | 29,746 | 13,214 | 22,863 | |||||||||||||||||||

| Change in fair value of interest rate swaps |

— | (7 | ) | 1,945 | 1,945 | — | 741 | |||||||||||||||||||

| Equity in net gains of affiliates |

(1,426 | ) | — | — | — | — | — | |||||||||||||||||||

| Loss on transfer of investment in affiliate |

223 | — | — | — | — | — | ||||||||||||||||||||

| Income tax (benefit) expense |

(853 | ) | (5,258 | ) | (1,409 | ) | (1,387 | ) | 554 | 1,574 | ||||||||||||||||

| Severance and integration costs(b) |

7,267 | — | 3,314 | 11,780 | 1,542 | 1,768 | ||||||||||||||||||||

| Equity-based compensation expense |

— | 420 | 543 | 543 | 133 | 561 | ||||||||||||||||||||

| Adjusted EBITDA |

$ | 1,312 | $ | 6,968 | $ | 18,765 | $ | 28,337 | $ | 12,941 | $ | 30,780 | ||||||||||||||

| (a) | The December 31, 2008 Non-GAAP With Acquisition reconciliation begins with loss from continuing operations. Our loss from continuing operations is presented in compliance with Article 11 of Regulation S-X. The Article 11 pro forma detailed calculation is presented on page F-114 of this prospectus. We reconcile loss from continuing operations to Adjusted EBITDA, a non-GAAP financial measure. We believe this non-GAAP financial measure is important to investors because it reflects the operations of a significant acquisition (ChartOne) as if it occurred on January 1, 2008. This non-GAAP financial measure has limitations and should not be considered in isolation, or as a substitute for analysis of our results as reported under GAAP. |

| (b) | In the period from January 1, 2006 through December 30, 2006, there was $7.3 million of integration-related costs associated with the acquisition of Companion from Blue Cross Blue Shield of South Carolina. Included in the $7.3 million is a Blue Cross Blue Shield allocation of $2.8 million as well as $4.5 million of expenses eliminated in conjunction with the acquisition on December 30, 2006. |

| In the twelve months ended December 31, 2008 and December 31, 2008 Non-GAAP With Acquisition, and the nine months ended September 30, 2008 and 2009, there were severance and integration costs relating to the integration of ChartOne of $3.3 million, $1.5 million and $1.8 million, respectively. Also included in the December 31, 2008 Non-GAAP With Acquisition period is an adjustment of $8.5 million relating to success bonuses to certain employees for the sale of ChartOne. |

| (2) | Total debt at September 30, 2009 includes long-term obligations, net of current portion, of $196.7 million, current portion of long-term obligations of $12.2 million and senior preferred shares of $38.6 million. Total debt as adjusted at September 30, 2009 includes long-term obligations, net of current portion, of $196.7 million, current portion of long-term obligations of $12.2 million and assumes the repayment in whole of the senior preferred shares and the repayment of $34.1 million of the principal amount of the senior subordinated notes. |

14

Table of Contents

Investing in our common stock involves significant risks. You should carefully consider the risks set forth below, as well as other information contained in this prospectus, before making a decision to invest in our common stock. If any of the following risks actually materialize, then our business, financial condition and results of operations may suffer. In addition, there may be risks of which we are currently unaware or that we currently regard as immaterial based on the information available to us that later prove to be material. These risks may adversely affect our business, financial condition and operating results. As a result, the price of our common stock could decline, and you could lose some or all of your investment. In assessing the risks described below, you should also refer to the other information contained in this prospectus, including our consolidated financial statements and the related notes, before deciding to purchase any shares of our common stock. Certain statements in “Risk Factors” are forward-looking statements. See “Forward-Looking Statements.”

Risks Related to Our Business

If we are unable to retain our existing customers, our business, financial condition and results of operations could suffer.

Our success depends substantially upon the retention of our customers. Although no single customer accounted for more than 1% of our revenue for fiscal year 2008, we may not be able to retain some of our existing customers if we are unable to achieve improved efficiencies and cost-effectiveness in providing our ROI services, effectively comply with a complex array of regulatory requirements, manage expenses associated with our customers’ health information management functions or successfully track and audit health record requests. We also may not be able to retain our customers if we do not fulfill health record requests promptly, fail to code properly or otherwise fail to meet the service standards of our customers or if our software solutions contain errors or otherwise fail to perform properly. Historically, we have benefited from high customer retention rates; however, we may not be able to maintain high customer retention rates in the future. The failure to maintain our existing customers may cause our revenue to decrease and our results from operations could suffer.

Our business may suffer as a result of our limited operating history in light of our recent acquisitions and growth and lack of public company operating experience.

We have grown rapidly in recent years, including through acquisitions, and have a limited operating history at our current scale of operations. We have developed our business over the past several years through acquisitions, including the acquisition of Smart Document Solutions, LLC, which we refer to as SDS, and ChartOne. Our SDS operations have only operated under our management since their acquisition in June 2007. Our ChartOne operations have only operated under our management since their acquisition in September 2008. In addition, we lack public company operating experience. Our limited operating history and lack of public company operating experience make it difficult to evaluate our future prospects. If we are unable to execute our business strategy and grow our business, either as a result of our inability to manage our current size, effectively manage the business in a public company environment or to manage our future growth through our acquisitions or for any other reason, our business, prospects, financial condition and results of operations may be harmed.

Our business will suffer if we fail to successfully integrate acquired businesses and technologies or to appropriately assess the risks in particular transactions.

We have in the past acquired, and may in the future acquire, businesses, technologies, services, product lines and other assets. For example, in September 2008 we acquired our

15

Table of Contents

largest competitor, ChartOne, and integrated its operations with our business. The successful integration of any businesses and assets we acquire into our operations, on a cost-effective basis, may be critical to our future performance. The amount and timing of the expected benefits of any acquisition, including potential synergies between our current business and the acquired business, are subject to significant risks and uncertainties. These risks and uncertainties include, but are not limited to, those relating to:

| • | our ability to maintain relationships with the customers of an acquired business; |

| • | the diversion of our management’s attention, as integrating the operations and assets of the acquired businesses will require a substantial amount of our management’s time; |

| • | our ability to sell services and software to customers with which we have established relationships and those with which the acquired businesses have established relationships; |

| • | the ability to achieve operating and financial synergies anticipated to result from the acquisitions; |

| • | our ability to retain or replace key personnel; |

| • | potential conflicts in customer, vendor or marketing relationships; |

| • | our ability to coordinate organizations that are geographically diverse and may have different business cultures; and |

| • | compliance with regulatory requirements. |

Although our management attempts to evaluate the risks inherent in each transaction and to evaluate acquisition candidates appropriately, we may not properly ascertain all such risks and the acquired businesses and assets may not perform as we expect or enhance the value of our company as a whole. In addition, acquired companies or businesses may have larger-than-expected liabilities that are not covered by the indemnification, if any, that we are able to obtain from the sellers.

We have a history of operating losses and may suffer losses in the future.

We have incurred losses since our operations began on December 31, 2006. In each of the fiscal years ended December 31, 2007 and 2008, we recorded net losses of approximately $7.4 million and $49.8 million, respectively. Our net loss for the nine months ended September 30, 2009 was $8.9 million, and we may incur losses in the future.

Our ability to use net operating loss carryforwards could be substantially limited in excess of existing limitations if we experience an ownership change as defined in the Internal Revenue Code.

As of December 31, 2008, our federal net operating loss carryforward was approximately $126 million subject to annual utilization limitations pursuant to Internal Revenue Code Section 382. If not utilized, net operating loss carryforwards will expire between 2012 and 2028. Of the $126.0 million net operating loss carryforwards, approximately $100.0 million are subject to existing Internal Revenue Code Section 382 limitations. If we are unable to fully utilize our net operating losses to offset taxable income generated in the future, our results of operations could be materially and negatively impacted.

Section 382 of the Internal Revenue Code contains rules that limit the ability of a company that undergoes an ownership change, which is generally any change in ownership of more than 50% of its stock over a three-year period, to use its net operating loss carryforwards and certain built-in losses recognized in years after the ownership change. These rules generally operate by focusing on ownership changes among stockholders owning directly or indirectly 5% or more of the stock of a company and any change in ownership arising from a new issuance of stock by the company.

16

Table of Contents

If we undergo an ownership change for purposes of Section 382 as a result of future transactions involving our common stock, including purchases or sales of stock between 5% stockholders, our ability to use our net operating loss carryforwards and to recognize certain built-in losses would be subject to additional limitations of Section 382. Generally, if an ownership change occurs, the yearly taxable income limitation on the use of net operating loss carryforwards and certain built-in losses is equal to the product of the applicable long-term tax exempt rate and the value of the company’s stock immediately before the ownership change. Depending on the resulting limitation, a significant portion of our net operating loss carryforwards could expire before we would be able to use them. Our inability to use our net operating loss carryforwards could have a negative impact on our financial position and results of operations.

We face significant competition for our services and solutions, and the majority of our addressable market, instead of using a third-party provider, performs internally some of the same services that we offer.

The markets for our various services and solutions are intensely competitive, continually evolving and subject to technological change. We face competition from many regional ROI service providers, healthcare information technology and service providers and other technology companies within our ROI services and our software and other services market segments. Many of our potential customers perform ROI services through their own staff and do not use outsourced service providers, which requires us to compete with our potential customers’ in-house staff for business. In February 2009, Congress passed the American Recovery and Reinvestment Act of 2009, or ARRA, which provides $20 billion to encourage the adoption and meaningful use of electronic health records systems. As hospitals, physician clinics and other providers adopt and utilize electronic health records systems, they may be able to perform the ROI functions internally and the need for our services may decrease. If we do not compete successfully for new customers, we will have limited growth and the price of our stock may suffer.

Our prices for the delivery of health records to requestors is typically set by state regulation or statute and is not determined by us.

Our prices for the delivery of health records to requestors are typically established by statute or regulation by the state where the customer is located and are only subject to change by the various state legislatures or regulatory bodies. In addition, the Social Security Administration establishes prices for the delivery of health records that it requests, which are typically below the prices set by the various state legislatures or regulatory bodies. Requestors may seek reimbursement from us if we inadvertently charge a price that exceeds the price established by statute, state regulation or the Social Security Administration. In addition, if these regulated prices are decreased or if any increases in our future costs exceed future increases in the regulated prices, our business would be less profitable and our results of operation would be adversely affected.

If we are not able to increase market penetration of hospitals, health systems and physician clinics who currently conduct the ROI function internally, or offer new and valuable services and solutions, we may not be able to increase sales and our revenue and results of operations may suffer.

We must increase the use of outsourced ROI services by hospitals, health systems and physician clinics who currently use their own personnel to perform the ROI function and we must continue to improve the functionality of our existing services and solutions in a timely manner and introduce new solutions in order to attract new customers and retain existing

17

Table of Contents

customers. We may not be successful in convincing hospitals, health systems and physician clinics to use our outsourced ROI services rather than continuing with their in-house operations. Further, the pace of change in the markets we serve is rapid, and our competitors regularly introduce new products and services. Our failure to increase market utilization of outsourced ROI services or our failure to improve the functionality of our existing services and solutions or introduce new solutions, could result in little or no growth for our business, which could cause our financial results to suffer and result in depressing the price of our common stock after we have completed this offering.

We are dependent on the continued service of key executives, the loss of any of whom could adversely affect our business.

Our performance is substantially dependent on the performance of our senior management team, including Michael Labedz, our President and Chief Executive Officer, and Brian Grazzini, our Chief Financial Officer. We have entered into agreements with each member of our senior management team that restrict their ability to compete with us should they decide to leave our company. Even though we have entered into these agreements, we cannot be sure that any member of our senior management team will remain with us or that they will not compete with us in the future. The loss of any member of our senior management team could impair our ability to execute our business plan and growth strategy, cause us to lose customers and reduce revenue, or lead to employee morale problems and/or the loss of key employees.

Our success depends in part on our ability to identify, recruit and retain skilled management and technical personnel. If we fail to recruit and retain suitable candidates or if our relationship with our employees changes or deteriorates, there could be an adverse affect on our business.

Our future success depends upon our continuing ability to identify, attract, hire and retain highly qualified personnel, including skilled technical, management, service, technology and sales and marketing personnel, all of whom are in high demand and are often subject to competing offers. Competition for qualified personnel in the healthcare information technology and services industry is intense, and we cannot assure you that we will be able to hire or retain a sufficient number of qualified personnel to meet our requirements, or that we will be able to do so at salary, benefit and other compensation costs that are acceptable to us. A loss of a substantial number of qualified employees, or an inability to attract, retain and motivate additional highly skilled employees required for expansion of our business, could have an adverse effect on our business. In addition, while approximately 30 of our employees are currently unionized, additional unionization of our employees is possible in the future. Such unionizing activities could be costly to address and, if successful, would likely adversely impact our operations.

Disruptions in service or damages to our centralized data center, or other software or systems failures, could adversely affect our business.

Our centralized data center is essential to our business. Our operations depend upon our ability to maintain and protect our computer systems, most of which are located in our centralized data center that we operate in Alpharetta, Georgia. We maintain insurance against fires, floods, other natural disasters and general business interruptions to mitigate the adverse effects of a disruption, relocation or change in operating environment at our data center; however, the situations and the amount of insurance coverage may not be adequate in any particular case. The occurrence of any of these events could result in interruptions, delays or cessations in service to our customers, which could impair or prohibit our ability to provide our services and solutions, reduce the attractiveness of our services and solutions to our customers and adversely impact our financial condition and results of operations.

18

Table of Contents

Disruption of our computer systems by break-ins, hackers, improper access, computer viruses or other attacks could result in service interruptions for our customers, which could increase our costs to comply with federal regulations and adversely effect our business.

Despite the implementation of security measures, our technology or systems that we interface with, including the Internet and related systems, may be vulnerable to physical break-ins, hackers, improper employee or contractor access, computer viruses, programming errors, denial-of-service attacks, terrorist attacks or other attacks by third parties or similar disruptive problems. Any of these can cause system failure, including network, software or hardware failure, which can result in service disruptions or increased response time for our services and solutions. In addition, as part of ARRA, Congress amended the healthcare privacy and security provisions of HIPAA. HIPAA imposes limitations on the use and disclosure of an individual’s healthcare information on healthcare providers, healthcare clearinghouses, and health insurance plans, collectively referred to as covered entities. The HIPAA amendments also impose these limitations and the corresponding penalties for non-compliance on individuals and entities that provide services to healthcare providers and other covered entities, collectively referred to as business associates. ARRA also made significant increases in the penalties for improper use or disclosure of an individual’s health information under HIPAA. The amendments also create notification requirements for individuals whose health information has been accessed, which in some cases may include public notice requirements. Notification is not required under HIPAA if the health information accessed is deemed secured in accordance with encryption and other standards to be developed by the U.S. Department of Health and Human Services, or HHS. We are subject to HIPAA as a healthcare clearinghouse and as a business associate. As a result, we may be required to expend significant capital and other resources to protect against security breaches and hackers or to alleviate problems caused by such breaches.

Unsuccessful implementation of our services and solutions with our customers may harm our future financial success.

In connection with the implementation of our services and solutions with new customers, we may encounter unanticipated difficulties and delays as a result of failure by us or by the customer to meet respective implementation responsibilities. If the customer implementation process is not executed successfully or if execution is delayed, our relationships with some of our customers may be adversely impacted and our results of operations will be impacted negatively. In addition, cancellation of any implementation of our services and solutions after it has begun may involve loss to us of time, effort and resources invested in the cancelled implementation as well as lost opportunity for acquiring other customers over that same period of time. The costs and lost future revenue associated with an implementation failure could adversely effect our financial results.

Our business involves the use, transmission and storage of personal health information and the failure to properly safeguard such information could result in significant liability and possible damages.

Our business activities involve the use, transmission and storage of personal health information. ARRA substantially increases penalties for improper use or disclosure of an individual’s health information and makes healthcare clearinghouses and business associates, such as us, as well as our customers, liable for such penalties under HIPAA. ARRA authorizes states’ attorneys general to enforce HIPAA requirements and recover penalties. In addition, ARRA requires a covered entity to notify individuals whose health information has been accessed. If the disclosure or breach involves individuals that cannot be located and the breach involves 10 or more individuals, or if the breach involves the information of more than 500

19

Table of Contents

individuals, public notice is required. If improper disclosure is caused by one of our employees or results from a breach of our computer systems or data center, we could be subject to substantial liability to the government or to the individual whose information has been disclosed. We may also be subject to substantial liability to our customers for penalties they owe to the government and possibly for damages to them for their loss of reputation as a result of negative publicity. Accordingly, security breaches of our computer systems or data center could expose us to a risk of loss or litigation, government enforcement actions and contractual liabilities. Although we have contractual provisions attempting to limit our liability in these areas, we cannot assure you that they will be successful or enforceable, or that other parties will accept such contractual provisions as part of our agreements. Moreover, these contractual provisions would not protect us against enforcement by federal or state governments. Any security breaches also could impact our ability to provide our services and solutions, as well as impact the confidence of our customers in our services and solutions, either of which could have an adverse effect on our business, financial condition and results of operations.

We attempt to limit, by contract, our liability for damages arising from our negligence, errors, mistakes or security breaches. However, contractual limitations on liability may not be enforceable or may otherwise not provide sufficient protection to us from liability for damages, especially in light of new HIPAA provisions. We maintain liability insurance coverage, including coverage for errors and omissions. It is possible, however, that claims could exceed the amount of our applicable insurance coverage, if any, or that this coverage may not continue to be available on acceptable terms or in sufficient amounts. Even if these claims do not result in liability to us, investigating and defending against them could be expensive and time-consuming and could divert management’s attention away from our operations. In addition, negative publicity caused by these events may harm our reputation and our business.

If the protection of our intellectual property is inadequate, our competitors may gain access to our technology or confidential information and we may lose our competitive advantage.

Our success as a company depends in part upon our ability to protect our core technology and intellectual property. To accomplish this, we rely on a combination of intellectual property rights, including trade secrets, copyrights and trademarks, as well as customary contractual protections. We use internal and external measures to protect our proprietary software and confidential information. Such measures include contractual protections with employees, contractors and customers, as well as U.S. copyright laws.

We protect the intellectual property in our software with customary contractual protections in our agreements that impose restrictions on our customers’ ability to use such software, such as prohibiting reverse engineering and limiting the use of copies. We also seek to avoid disclosure of our intellectual property by relying on non-disclosure and intellectual property assignment agreements with our employees and consultants that acknowledge our ownership of all intellectual property developed by the individual during the course of his or her work with us. The agreements also require each person to maintain the confidentiality of all proprietary information disclosed to them. Other parties may not comply with the terms of their agreements with us, and we may not be able to enforce our rights adequately against these parties. The disclosure to, or independent development by, a competitor of any trade secret, know-how or other technology that is competitive with our business could materially adversely affect any competitive advantage we may have over any such competitor.

We cannot assure you that the steps we have taken to protect our intellectual property rights will be adequate to deter misappropriation of our rights or that we will be able to detect unauthorized uses and take timely and effective steps to enforce our rights. If unauthorized uses

20

Table of Contents

of our intellectual property were to occur, we might be required to engage in costly and time-consuming litigation to enforce these rights. We cannot assure you that we would prevail in any such litigation. If others were able to use our intellectual property, our business and financial results could be adversely affected.

Our indebtedness could adversely affect our financial health, harm our ability to react to changes to our business and prevent us from fulfilling our obligations under our indebtedness.

As of September 30, 2009, after giving effect to the completion of this offering and application of our net proceeds therefrom, we would have had total indebtedness of approximately $174.8 million. Based on that level of indebtedness and interest rates applicable at September 30, 2009 our annual interest expense would have been $17.7 million. Although we believe that our current cash flows will be sufficient to cover our annual interest expense, any increase in the amount of our indebtedness or any decline in the amount of cash available to make interest payments could require us to divert funds identified for other purposes for debt service and impair our liquidity position. If we cannot generate sufficient cash flow from operations to service our debt, we may need to refinance our debt, dispose of assets or issue equity to obtain necessary funds. We do not know whether we will be able to take any of such actions on a timely basis or on terms satisfactory to us or at all.

Our indebtedness could limit our ability to:

| • | obtain necessary additional financing for working capital, capital expenditures or other purposes in the future; |

| • | plan for, or react to, changes in our business and the industries in which we operate; |

| • | make future acquisitions or pursue other business opportunities; and |

| • | react in an extended economic downturn. |

Despite our current indebtedness, we may still be able to incur significantly more debt. The incurrence of additional debt could increase the risks associated with our substantial leverage, including our ability to service our indebtedness. In addition, because borrowings under our credit agreement bear interest at a variable rate, our interest expense could increase, exacerbating these risks. For instance, assuming an aggregate principal balance of $132.3 million outstanding under our variable rate borrowings, which was the amount outstanding as of September 30, 2009, giving effect to the application of net proceeds from this offering, a 1% increase in the interest rate we are charged on our debt would increase our annual interest expense by $1.3 million.

Recent events in the credit markets may affect our ability to refinance our existing debt or obtain additional debt financing on acceptable terms.

We may need or seek additional financing in the future to either refinance our existing indebtedness, fund our operations, fund acquisitions or strategic relationships, develop or enhance our technological infrastructure and our existing services and solutions or implement other projects. Our senior secured credit facility matures on September 22, 2013; therefore, we do not have near-term impending maturity on our senior secured credit facility. However, given the state of the current credit environment resulting from, among other things, the general weakening of the global economy, it may be difficult to refinance our existing indebtedness or obtain any such additional financing on acceptable terms, which could have an adverse effect on our financial condition, including our results of operations and/or business plans. In addition, if as a result of the current conditions in the credit markets any of the lenders participating in our revolving credit facility are unable to fund borrowings under such facility, our liquidity could be adversely affected.

21

Table of Contents

The terms of our credit agreement and our note purchase agreement may restrict our current and future operations, which would adversely affect our ability to respond to changes in our business and to manage our operations.

Our credit agreement and our note purchase agreement contain, and any future indebtedness of ours would likely contain, a number of restrictive covenants that impose significant operating and financial restrictions on us, including restrictions on our ability to, among other things:

| • | incur additional debt; |

| • | issue preferred stock; |

| • | create liens; |

| • | create or incur contingent obligations; |

| • | engage in sales of assets and subsidiary stock; |

| • | enter into sale-leaseback transactions; |

| • | make investments and acquisitions; |

| • | enter into hedging arrangements; |

| • | make capital expenditures; |

| • | pay dividends and make other restricted payments; |

| • | enter into transactions with affiliates; and |

| • | transfer all or substantially all of our assets or enter into merger or consolidation transactions. |