Attached files

| file | filename |

|---|---|

| EX-99.1 - PRESS RELEASE - Energy Transfer Operating, L.P. | dex991.htm |

| 8-K - SUNOCO LOGISTICS PARTNERS LP--FORM 8-K - Energy Transfer Operating, L.P. | d8k.htm |

Third Quarter 2009 Earnings Conference Call October 26, 2009 Sunoco Logistics Partners L.P. Exhibit 99.2 |

Forward-Looking Statement You should review this slide presentation in conjunction with the third quarter

2009 earnings conference call for Sunoco Logistics Partners L.P.,

held on October 26 at 2:00 p.m. EDT. You may listen to the

audio portion of the conference call on our website at www.sunocologistics.com or by dialing (USA toll- free) 1-877-297-3442. International callers should dial

1-706-643-1335. Please enter Conference ID #34719298. Audio replays of the conference call will be available for two weeks after the

conference call beginning approximately two hours following the

completion of the call. To access the replay, dial 1-800-642-1687. International callers should dial 1-706-645-9291. Please

enter Conference ID # 34719298. During the call, those statements

we make that are not historical facts are forward-looking statements. Although we believe the assumptions underlying these

statements are reasonable, investors are cautioned that such

forward-looking statements involve risks that may affect our business prospects and performance, causing actual results to differ from those discussed during the

conference call. Such risks and uncertainties include, among

other things: our ability to successfully consummate announced acquisitions and organic growth projects and integrate them into existing business operations; the ability of announced acquisitions to be cash-flow accretive; increased competition;

changes in the demand both for crude oil that we buy and sell, as

well as for crude oil and refined products that we store and distribute; the loss of a major customer; changes in our tariff rates; changes in throughput

of third-party pipelines that connect to our pipelines and

terminals; changes in operating conditions and costs; changes in the level of environmental remediation spending; potential equipment malfunction; potential

labor relations problems; the legislative or regulatory

environment; plant construction/repair delays; and political and economic conditions, including the impact of potential terrorist acts and international hostilities. These and other applicable risks and uncertainties are described more fully in our Form 10-Q, filed with the Securities and Exchange Commission on August 5, 2009. We

undertake no obligation to update publicly any forward-looking

statements whether as a result of new information or future events. 2 |

Q3 2009 Assessment Net income for the third quarter 2009 was $48.5 million compared to $50.3 million in the prior year’s quarter Distributable cash flow increased to $54.4 million, a 3.7% increase from

third quarter 2008 Completed construction of the Nederland to Motiva’s Port Arthur

pipeline and storage project Increased total distribution to $1.065 ($4.26 annualized) per unit, an 10.4

percent increase over the prior year’s distribution

– Represents the twenty-fifth distribution increase in the past

twenty-six quarters Debt to EBITDA ratio of 2.5x for the last twelve months 3 |

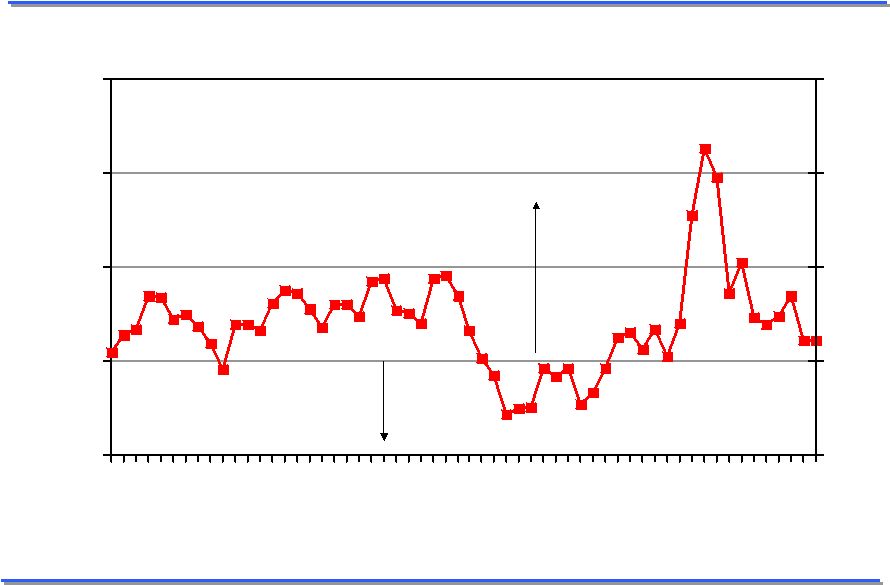

WTI NYMEX Month 2 vs Month 1 -2 0 2 4 6 2005 2006 2007 2008 2009 -2 0 2 4 6 MB contango backwardation 4 |

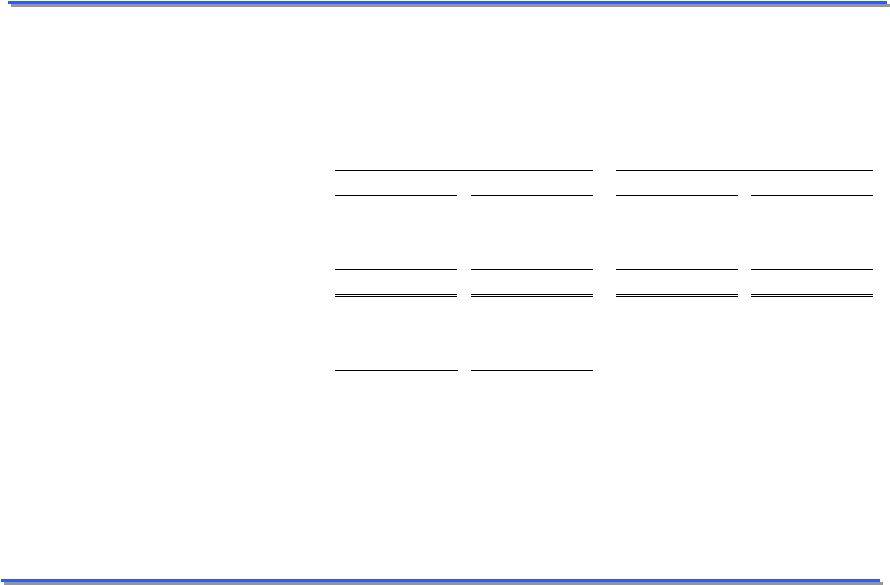

Q3 2009 Financial Highlights ($ in millions, unaudited) Three Months Ended Nine Months Ended September 30, September 30, 2009 2008 2009 2008 Sales and operating revenue 1,420.0 $ 2,829.5 $ 3,740.8 $ 8,539.3 $ Other income 8.8 6.3 21.3 19.9 Total revenues 1,428.8 2,835.8 3,762.1 8,559.2 Cost of products sold and other operating expenses 1,342.0 2,752.6 3,450.5 8,316.7 Depreciation and amortization 12.2 10.0 35.3 29.5 Selling, general and administrative expenses 14.7 15.3 47.6 44.8 Impairment Charges - - - 5.7 Total costs and expenses 1,368.9 2,777.9 3,533.4 8,396.7 Operating income 59.9 57.9 228.7 162.5 Interest cost and debt expense, net 12.6 8.5 36.3 25.9 Capitalized interest (1.2) (0.9) (3.6) (2.6) Net Income 48.5 $ 50.3 $ 196.0 $ 139.2 $ 5 |

Q3 2009 Financial Highlights 6 (amounts in millions, except unit and per share unit amounts, unaudited)

Three Months Ended Nine Months Ended September 30, September 30, 2009 2008 2009 2008 Calculation of Limited Partners' interest: Net Income 48.5 $ 50.3 $ 196.0 $ 139.2 $ Less: General Partners' interest (13.4) (9.7) (38.9) (26.2) Limited Partners' interest in Net Income 35.1 $ 40.6 $ 157.1 $ 113.0 $ Net Income per Limited Partner unit: Basic (1) 1.13 $ 1.42 $ 5.22 $ 3.94 $ Diluted (1) 1.13 $ 1.41 $ 5.19 $ 3.92 $ Weighted Average Limited Partners' units outstanding (in thousands): Basic 30,981 28,657 30,085 28,648 Diluted 31,190 28,846 30,288 28,831 (1) Effective January 1, 2009, the Partnership changed its calculation of

earnings per unit to conform to updated accounting guidance that requires undistributed earnings to be allocated to the limited partner and general

partner interests in accordance with the Partnership agreement. Prior period amounts have been restated for comparative purposes. This change resulted in an

increase in net income per diluted LP unit of $0.22 and $0.56 for the three and nine months ended September 30, 2008 respectively.

|

Q3 2009 Financial Highlights ( $ in millions, unaudited) Three Months Ended Nine Months Ended September 30, September 30, 2009 2008 2009 2008 Capital Expenditure Data: Maintenance capital expenditures 6.3 $

7.8 $

15.3 $

15.7 $

Expansion capital expenditures 82.1 28.7 143.5 73.4 Total 88.4 $

36.5 $

158.8 $ 89.1 $

September 30, December 31, 2009 2008 Balance Sheet Data (at period end): Cash and cash equivalents 2.0 $

2.0 $

Total Debt 889.4 747.6 Total Partners' Capital 853.0 669.9 7 |

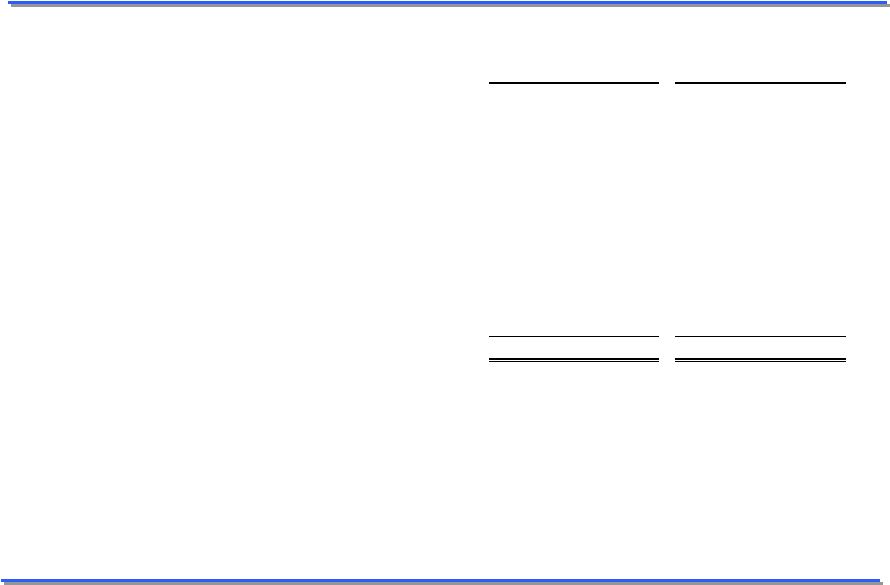

Q3 2009 Financing Update ($ in millions, unaudited) 8 Balance as of: September 30, 2009 December 31, 2008 Revolving Credit Facilities (1) : $400 million - due November 2012 258,723 $

323,385 $

$100

million - due May 2009 - - $62.5 million - due September 2011 31,250 - Senior Notes: 7.25% Senior Notes - due 2012 250,000 250,000 6.125% Senior Notes - due 2016 175,000 175,000 8.75% Senior Notes - due 2014 175,000 - Less: unamortized bond discount (599) (754) Total Debt 889,374 $

747,631

$

(1) As of

September 30, 2009, the Partnership has unutilized borrowing capacity of $167.5 million under its revolving credit facilities. |

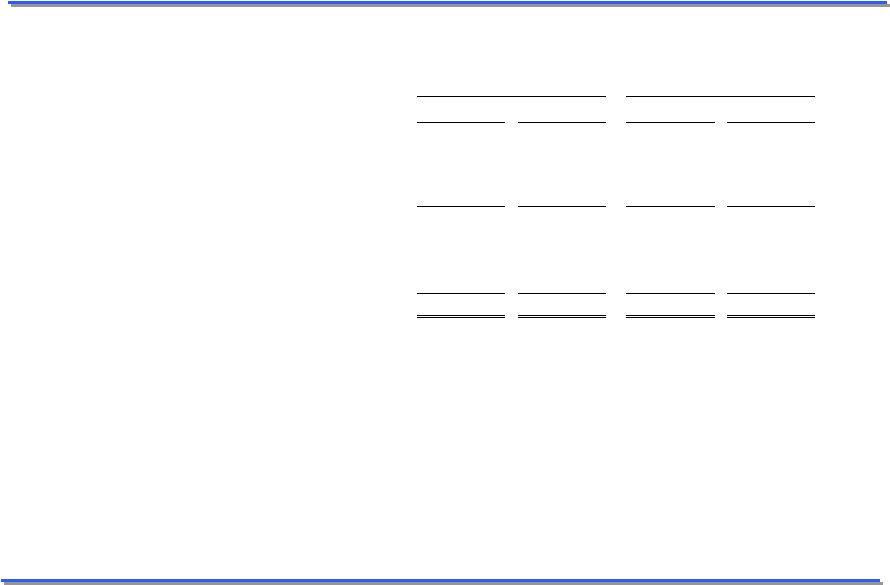

Refined Products Pipeline System 9 (amounts in millions, unless otherwise noted, unaudited) Three Months Ended Nine Months Ended September 30, September 30, 2009 (4) 2008 (3) 2009 (4) 2008 (3) Financial Highlights Sales and operating revenue 32.0 $ 25.7 $ 94.6 $ 73.6 $ Other income 3.9 2.3 9.2 6.5 Total revenues 35.9 28.0 103.8 80.1 Operating expenses 14.4 11.1 43.7 33.6 Depreciation and amortization 3.2 2.2 9.6 6.6 Selling, general and administrative expenses 5.0 5.2 16.1 15.1 Operating income 13.3 $ 9.5 $ 34.4 $ 24.8 $ Operating Highlights Total shipments (mm barrel miles per day) 56.8 43.8 58.1 44.1 Revenue per barrel mile (cents) 0.612 0.638 0.595 0.609 (1) Excludes amounts attributable to equity ownership interests in the

corporate joint ventures. (2) Represents total average daily

pipeline throughput multiplied by the number of miles of pipeline through which each barrel has been shipped. (3) On January 1, 2009 the reporting segments were realigned. All prior

period reporting segment results were recast for comparative purposes. (4) Includes results from the Partnership's purchase of the MagTex refined products terminals from the date of acquisition. (1) (2) |

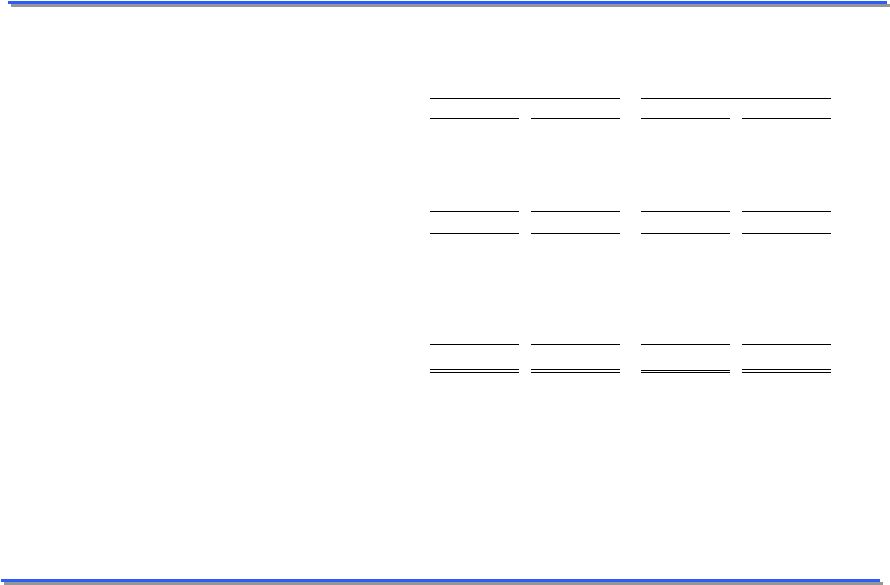

Terminal Facilities 10 (amounts in millions, unless otherwise noted, unaudited) Three Months Ended Nine Months Ended September 30, September 30, 2009 2008 2009 2008 Financial Highlights Sales and operating revenue 46.2 $ 40.6 $ 139.4 $ 119.3 $ Other income - - 1.4 0.8 Total revenues 46.2 40.6 140.8 120.1 Operating expenses 15.7 17.9 48.4 45.5 Depreciation and amortization 5.2 4.2 14.5 12.1 Selling, general and administrative expenses 4.6 4.8 14.8 13.9 Impairment charge - - - 5.7 Operating income 20.7 $ 13.7 $ 63.1 $ 42.9 $ Operating Highlights Terminal throughput (000's bpd) Refined product terminals (2) 465.2 437.0 463.0 428.1 Nederland terminal 559.9 545.1 619.3 541.5 Refinery terminals (1) 609.0 646.5 597.2 648.0 (1) Consists of the Partnership Fort Mifflin Terminal Complex, the Marcus

Hook Tank Farm and the Eagle Point Dock. (2) Includes results

from the Partnership's purchase of the MagTex and the Romulus,

MI refined products terminals from the date of acquisition. |

Crude Oil Pipeline System 11 (amounts in millions, unless otherwise noted, unaudited) Three Months Ended Nine Months Ended September 30, September 30, 2009 2008 (3) 2009 2008 (3) Financial Highlights Sales and operating revenue 1,341.9 $ 2,763.2 $ 3,506.8 $ 8,346.5 $ Other income 4.9 4.0 10.7 12.5 Total revenues 1,346.8 2,767.2 3,517.5 8,359.0 Cost of products sold and other operating expenses 1,311.9 2,723.6 3,358.3 8,237.6 Depreciation and amortization 3.9 3.6 11.2 10.7 Selling, general and administrative expenses 5.1 5.4 16.8 15.9 Operating income 25.9 $ 34.6 $ 131.2 $ 94.8 $ Operating Highlights (1)(4) Terminal throughput (000's bpd) Crude oil pipeline throughput (000's bpd) 611.0 649.3 648.2 672.9 Crude oil purchases at wellhead (000's bpd) 176.6 176.7 183.0 175.2 Gross margin per barrel of pipeline throughput (cents) (2) 46.5 57.2 77.6 52.2 (1) Excludes amounts attributable to equity ownership interests in the

corporate joint ventures. (2) Represents total segment sales and

other operating revenue minus cost of products sold and operating expenses and depreciation and amortization divided by crude oil pipeline throughput. (3) On January 1, 2009 the reporting segments were realigned. All prior

period reporting segment results were recast for comparative purposes. (4) Includes results from the Partnership's purchase of the Excel pipeline

from the acquisition date. |

Appendix Sunoco Logistics Partners L.P. 12 |

Non-GAAP Financial Measures ($ in thousands, unaudited) Three Months Ended Nine Months Ended September 30, September 30, 2009 2008 2009 2008 Net Income 48,460 $ 50,334 $ 196,009 $ 139,160 $ Add: Interest cost and debt expense, net 12,592 8,506 36,278 25,904 Less: Capitalized Interest (1,171) (977) (3,629) (2,613) Add: Depreciation and amortization 12,240 10,010 35,328 29,499 Add: Impairment charge - - - 5,674 EBITDA 72,121 $ 67,873 $ 263,986 $ 197,624 $ Less: Interest expense (11,421) (7,529) (32,649) (23,291) Less: Maintenance capital (6,304) (7,884) (15,326) (15,655) Add: Sunoco reimbursements - - - 1,851 Distributable Cash Flow ("DCF") 54,396 $ 52,460 $ 311,961 $ 160,529 $ Non-GAAP Financial Measures (1) In this release, the Partnership’s EBITDA and DCF references are not presented in accordance with generally accepted accounting principles (“GAAP”) and are not intended to be used in lieu of GAAP presentations of net income. Management of the Partnership believes EBITDA and DCF information enhance an investor's understanding of a business’ ability to generate cash for payment of distributions and other purposes. In addition, EBITDA is also used as a measure in the Partnership's revolving credit facilities in determining its compliance with certain covenants. However, there may be contractual, legal, economic or other reasons which may prevent the Partnership from satisfying principal and interest obligations with respect to indebtedness and may require the Partnership to allocate funds for other purposes. EBITDA and DCF do not represent and should not be considered an alternative to net income or

operating income as determined under United States GAAP and may not be comparable to other similarly titled measures of other businesses. 13 |

Non-GAAP Financial Measures ($ in thousands, unaudited) Non-GAAP Financial Measures (1) In this release, the Partnership’s EBITDA and DCF references are not presented in accordance with generally accepted accounting principles (“GAAP”) and are not intended to be used in lieu of GAAP presentations of net income. Management of the Partnership believes EBITDA and DCF information enhance an investor's understanding of a business’ ability to generate cash for payment of distributions and other purposes. In addition, EBITDA is also used as a measure in the Partnership's revolving credit facilities in determining its compliance with certain covenants. However, there may be contractual, legal, economic or other reasons which may prevent the Partnership from satisfying principal and interest obligations with respect to indebtedness and may require the Partnership to allocate funds for other purposes. EBITDA and DCF do not represent and should not be considered an alternative to net income or

operating income as determined under United States GAAP and may not be comparable to other similarly titled measures of other businesses. Earnings before interest, taxes, depreciation Twelve months ended and amortization ("EBITDA") September 30, 2009 Net Income 271,329 $

Add: Interest

cost and debt expense 45,341 Less: Capitalized interest (4,871) Add: Depreciation and amortization 45,883 EBITDA 357,682 $

Total Debt as of

September 30, 2009 889,374 $

Total Debt to

EBITDA Ratio 2.5 14 |

Refined Products Pipeline System Recast (amounts in millions, unless otherwise noted, unaudited) 43.1 0.601 45.5 0.587 Total shipments (mm barrel miles per day) (3) Revenue per barrel mile (cents) Operating Highlights (1)(2) 10.9 2.2 4.9 $ 8.6 11.6 2.2 5.1 $ 6.7 Operating expenses Depreciation and amortization Selling, general and administrative expenses Operating income $ 23.6 3.0 26.6 $ 24.3 1.3 25.6 Sales and other operating revenue Other income Total revenues Financial Highlights (1) Q2 2008 Q1 2008 (1) On January 1, 2009 the reporting segments were realigned. All

prior period reporting segment results were recast for comparative purposes. (2) Excludes amounts attributable to equity ownership interests in the

corporate joint ventures. (3) Represents total average daily

pipeline throughput multiplied by the number of miles of pipeline through which each barrel has been shipped. Q3 2008 $ 25.7 2.3 27.9 11.1 2.2 5.1 $ 9.5 Q4 2008 14.8 2.7 4.7 $ 9.7 $ 29.9 2.0 31.9 43.8 0.638 55.0 0.590 15 |

Crude Oil Pipeline System Recast (amounts in millions, unless otherwise noted, unaudited) 694.1 177.4 51.2 675.5 171.5 48.5 Crude oil pipeline throughput (000’s bpd) Crude oil purchases at wellhead (000’s bpd) Gross margin per barrel of pipeline throughput (cents) (3) Operating Highlights (1)(2) 3,216.1 3.6 5.0 $ 32.8 2,298.0 3.5 5.5 $ 27.3 Operating expenses Depreciation and amortization Selling, general and administrative expenses Operating income $ 3,252.5 5.0 3,257.5 $2,330.7 3.6 2,334.3 Sales and other operating revenue Other income Total revenues Financial Highlights (1) Q2 2008 Q1 2008 (1) On January 1, 2009 the reporting segments were realigned. All

prior period reporting segment results were recast for comparative purposes. (2) Excludes amounts attributable to equity ownership interests in the

corporate joint ventures. (3) Represents total segment sales and

other operating revenue minus cost of products sold and operating expenses and depreciation and amortization divided by crude oil pipeline throughput. Q3 2008 $ 2,763.2 4.0 2,767.2 2,723.6 3.6 5.4 $ 34.6 Q4 2008 1,435.7 3.6 5.3 $ 57.8 $ 1,500.0 2.4 1,502.4 649.3 176.7 57.2 711.6 185.0 93.4 16 |