Attached files

| file | filename |

|---|---|

| 8-K - TEMPUR-PEDIC 8-K 10-22-2009 - TEMPUR SEALY INTERNATIONAL, INC. | form8k.htm |

2

Barry Hytinen

Vice President

3

Webcast

participants may email questions to:

investor.relations@tempurpedic.com

Agenda

Note

Regarding Trademarks, Trade Names and Service Marks:

Tempur,

Tempur-Pedic, The DeluxeBed by Tempur-Pedic, The ClassicBed by Tempur-Pedic, The

GrandBed by Tempur-Pedic, The TEMPUR-

Cloud Supreme, The TEMPUR-Cloud, The RhapsodyBed by Tempur-Pedic, The AdvantageBed by Tempur-Pedic, The Bella Fina Bed by Tempur-

Pedic, The BellaSonna Bed by Tempur-Pedic, The TEMPUR-Cloud Luxe by Tempur-Pedic, The CelebrityBed by Tempur-Pedic, The AlluraBed by

Tempur-Pedic, The Sensation, The Sensation Lite, The NeckPillow by Tempur-Pedic, The SymphonyPillow by Tempur-Pedic, The ComfortPillow

by Tempur-Pedic, The RhapsodyPillow by Tempur-Pedic are trademarks, trade names or service marks of Tempur-Pedic International Inc. and its

subsidiaries. All other trademarks, trade names and service marks in this presentation are the property of their respective owners.

Cloud Supreme, The TEMPUR-Cloud, The RhapsodyBed by Tempur-Pedic, The AdvantageBed by Tempur-Pedic, The Bella Fina Bed by Tempur-

Pedic, The BellaSonna Bed by Tempur-Pedic, The TEMPUR-Cloud Luxe by Tempur-Pedic, The CelebrityBed by Tempur-Pedic, The AlluraBed by

Tempur-Pedic, The Sensation, The Sensation Lite, The NeckPillow by Tempur-Pedic, The SymphonyPillow by Tempur-Pedic, The ComfortPillow

by Tempur-Pedic, The RhapsodyPillow by Tempur-Pedic are trademarks, trade names or service marks of Tempur-Pedic International Inc. and its

subsidiaries. All other trademarks, trade names and service marks in this presentation are the property of their respective owners.

Forward-Looking

Statements

This

presentation may contain “forward-looking statements,” within the meaning of

federal securities laws, which include information concerning the

Company’s plans, objectives, goals, strategies, future revenues or performance, financing needs and other information that is not historical information.

When used in this presentation, the words “estimates,” “expects,” “anticipates,” “projects,” “plans,” “intends,” “believes,” and variations of such words or

similar expressions are intended to identify forward-looking statements. All forward-looking statements, including without limitation, the Company’s

expectations regarding improving the quality and range of existing products; increasing brand awareness and brand consideration; the impact of the

introduction of new products, including the TEMPUR-Cloud™ Supreme; international and domestic growth opportunities; increasing market share;

improving gross margin; expanding and improving distribution channels; manufacturing capacity and utilization; consumer preferences and behavior; the

effectiveness of new cost structures; meeting financial obligations; cost and operating expense reductions and cash flow generation; and the Company’s

enhanced earnings power are based upon current expectations and beliefs and various assumptions. There can be no assurance that the Company will

realize these expectations or that these beliefs will prove correct.

Company’s plans, objectives, goals, strategies, future revenues or performance, financing needs and other information that is not historical information.

When used in this presentation, the words “estimates,” “expects,” “anticipates,” “projects,” “plans,” “intends,” “believes,” and variations of such words or

similar expressions are intended to identify forward-looking statements. All forward-looking statements, including without limitation, the Company’s

expectations regarding improving the quality and range of existing products; increasing brand awareness and brand consideration; the impact of the

introduction of new products, including the TEMPUR-Cloud™ Supreme; international and domestic growth opportunities; increasing market share;

improving gross margin; expanding and improving distribution channels; manufacturing capacity and utilization; consumer preferences and behavior; the

effectiveness of new cost structures; meeting financial obligations; cost and operating expense reductions and cash flow generation; and the Company’s

enhanced earnings power are based upon current expectations and beliefs and various assumptions. There can be no assurance that the Company will

realize these expectations or that these beliefs will prove correct.

There

are a number of risks and uncertainties that could cause actual results to

differ materially from the forward-looking statements contained in

this

presentation. Numerous factors, many of which are beyond the Company’s control, could cause actual results to differ materially from those expressed

as forward-looking statements. These risk factors include general economic and industry conditions, particularly in the retail sector, as well as consumer

confidence and the availability of consumer financing; the Company’s ability to reduce expenses to align with reduced sales levels; uncertainties arising

from global events; the effects of changes in foreign exchange rates on the Company’s reported earnings; consumer acceptance of the Company’s

products; industry competition; the efficiency and effectiveness of the Company’s advertising campaigns and other marketing programs; the Company’s

ability to increase sales productivity and expand distribution channels; the Company’s dependence on its significant customers; the Company’s ability to

address issues in certain underperforming international markets; the Company’s ability to continuously improve its product line, maintain efficient, timely

and cost-effective production and delivery of its products, and manage its growth; changes in foreign tax rates; rising commodity costs; the Company’s

ability to retain members of its senior management team; the effects of increased interest rates; the market price for the Company’s common stock

prevailing from time to time; and the nature of other investment opportunities presented to the Company from time to time.

presentation. Numerous factors, many of which are beyond the Company’s control, could cause actual results to differ materially from those expressed

as forward-looking statements. These risk factors include general economic and industry conditions, particularly in the retail sector, as well as consumer

confidence and the availability of consumer financing; the Company’s ability to reduce expenses to align with reduced sales levels; uncertainties arising

from global events; the effects of changes in foreign exchange rates on the Company’s reported earnings; consumer acceptance of the Company’s

products; industry competition; the efficiency and effectiveness of the Company’s advertising campaigns and other marketing programs; the Company’s

ability to increase sales productivity and expand distribution channels; the Company’s dependence on its significant customers; the Company’s ability to

address issues in certain underperforming international markets; the Company’s ability to continuously improve its product line, maintain efficient, timely

and cost-effective production and delivery of its products, and manage its growth; changes in foreign tax rates; rising commodity costs; the Company’s

ability to retain members of its senior management team; the effects of increased interest rates; the market price for the Company’s common stock

prevailing from time to time; and the nature of other investment opportunities presented to the Company from time to time.

Additional

information concerning these and other risks and uncertainties are discussed in

the Company's filings with the Securities and Exchange

Commission, including without limitation the Company's annual report on Form 10-K under the headings "Special Note Regarding Forward-Looking

Statements" and "Risk Factors". Any forward-looking statement speaks only as of the date on which it is made, and the Company undertakes no

obligation to update any forward-looking statements for any reason, including to reflect events or circumstances after the date on which such statements

are made or to reflect the occurrence of anticipated or unanticipated events or circumstances.

Commission, including without limitation the Company's annual report on Form 10-K under the headings "Special Note Regarding Forward-Looking

Statements" and "Risk Factors". Any forward-looking statement speaks only as of the date on which it is made, and the Company undertakes no

obligation to update any forward-looking statements for any reason, including to reflect events or circumstances after the date on which such statements

are made or to reflect the occurrence of anticipated or unanticipated events or circumstances.

5

Mark Sarvary

President & Chief Executive Officer

6

Tempur-Pedic Overview

7

Unique

Range Of Mattresses And Pillows Utilizing The

Proprietary Pressure Relieving Tempur Material

Proprietary Pressure Relieving Tempur Material

The

Grandbed

by

Tempur-Pedic®

The

RhapsodyBed

by

Tempur-Pedic®

The

DeluxeBed

by

Tempur-Pedic™

The

AdvantageBed

by

Tempur-Pedic™

The

TEMPUR-Cloud™ Supreme

The

SymphonyPillow

by

Tempur-Pedic®

The

ComfortPillow

by

Tempur-Pedic®

The

NeckPillow

by

Tempur-Pedic™

The

RhapsodyPillow

by

Tempur-Pedic®

8

Company

Thesis

® Established:

Worldwide leader in

specialty mattresses and premium mattresses

Ø Leader in the $5B

premium segment of the $13B global mattress market

® Differentiated:

Consumer preferred,

branded product line

Ø Most highly

recommended brand by owners, most desired brand for non-owners

Ø Over a decade of

industry-leading brand advertising, very high level of owner

referrals

® Profitable:

Industry-leading

margins and cash flows

Ø Gross margin ~47%,

potential 50%

Ø Operating margin

~17%, potential 25%

Ø Annual depreciation

& amortization is 2x annual capital expenditures

® Growing:

Significant top line

growth opportunity

Ø 2% U.S. mattress

market share

Source:

Management estimates

9

Independent

And Internal Research Confirms Tempur-Pedic Is A

Preferred Product

Preferred Product

Source:

The 2008 and 2009 Gallup Consumer Mattress Market Study and Update

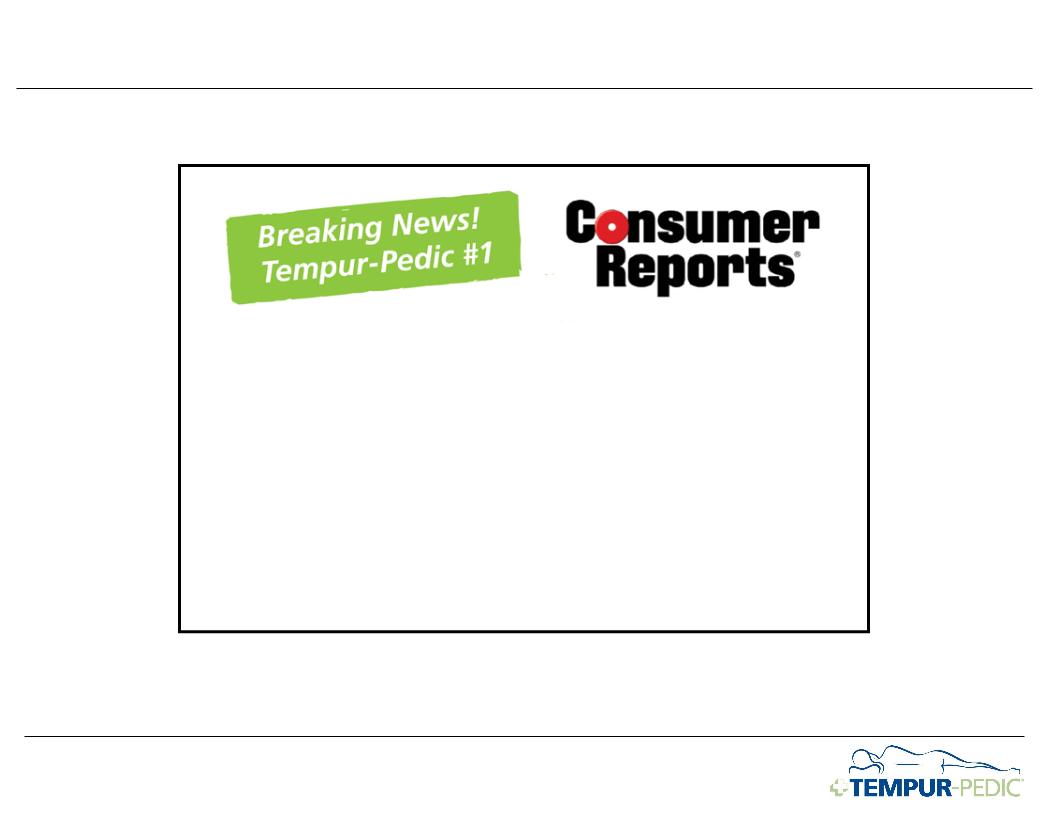

In its

October 2009 issue hot off the press,

Consumer Reports released the results of a survey

in which 17,000 people rated their mattresses. The

article, entitled “Would you buy that mattress

again?”, reports that Tempur-Pedic scored #1 on

“Would Definitely Buy Again” - beating ALL other

brands in the survey.

Consumer Reports released the results of a survey

in which 17,000 people rated their mattresses. The

article, entitled “Would you buy that mattress

again?”, reports that Tempur-Pedic scored #1 on

“Would Definitely Buy Again” - beating ALL other

brands in the survey.

10

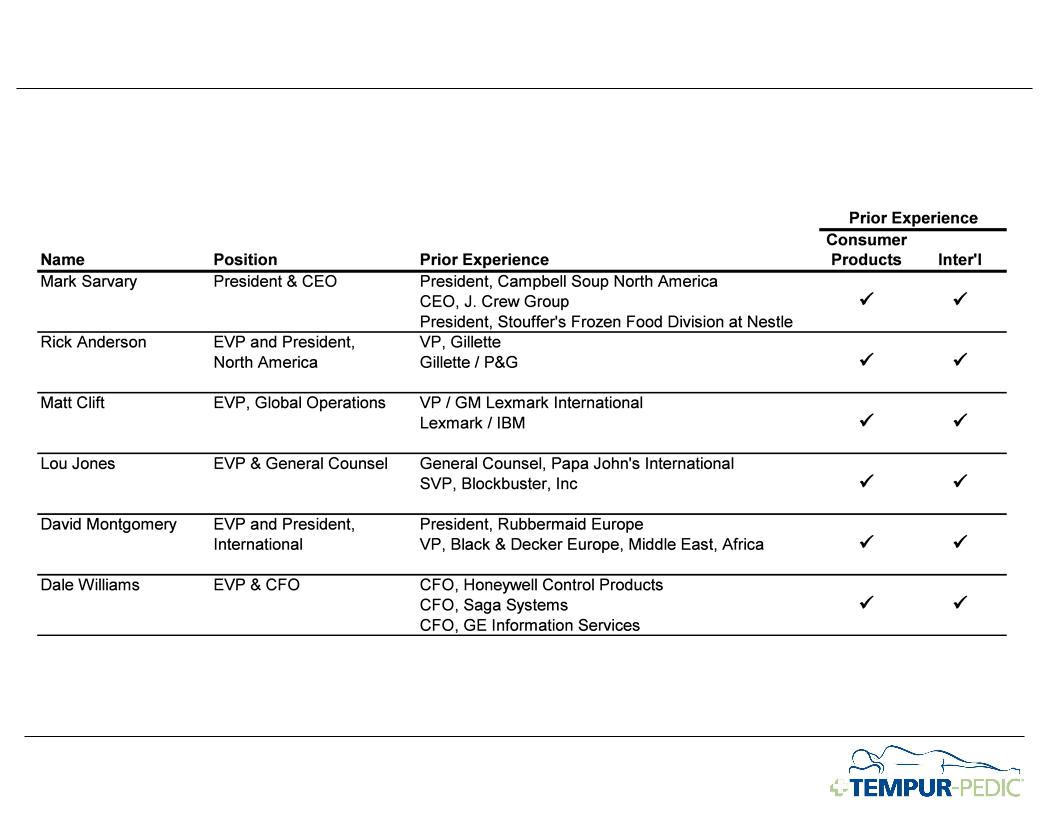

Strong

Management Team With > 150 Years Running Large,

International

Businesses

Businesses

11

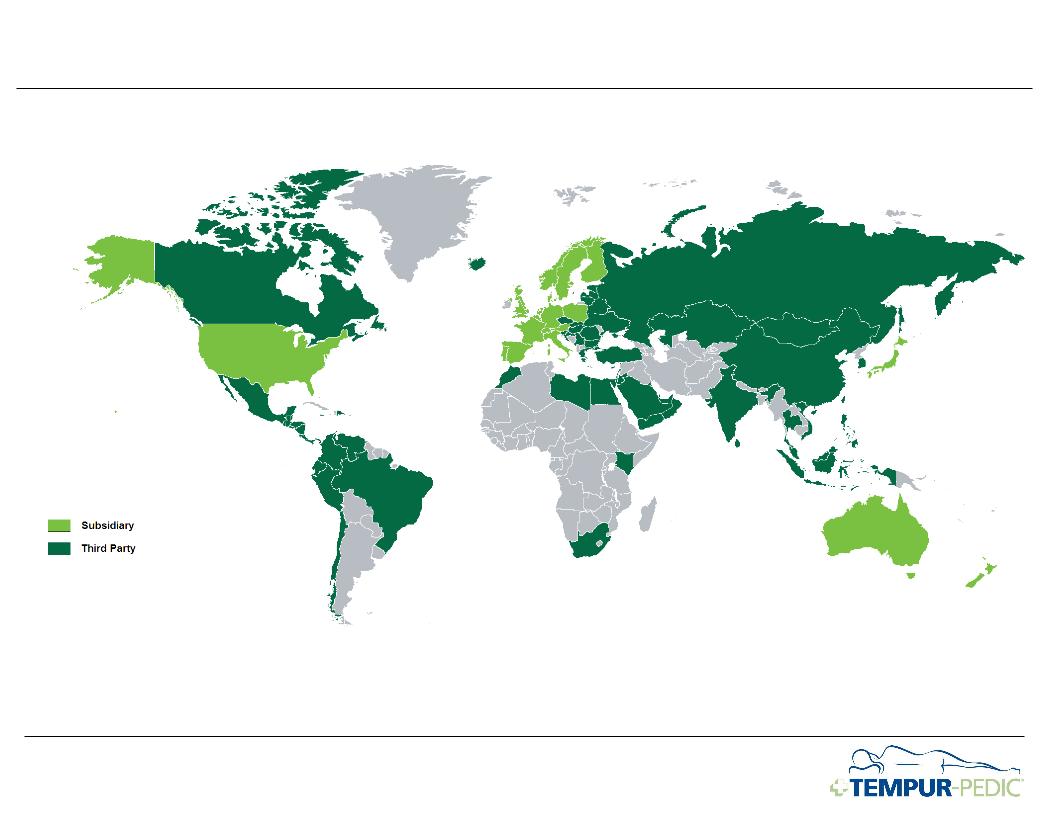

Global

Presence

12

Denmark

(500K

sq ft)

Duffield,

VA

(500K

sq ft)

Albuquerque,

NM

(800K

sq ft)

State-of-the-Art

Vertically Integrated Manufacturer

u Highly automated,

ISO-certified plants

u > $200 million

invested

13

2009 Performance

14

2009

Strategic Priorities

u Maintain a

reasonable cushion to financial covenants

u Improve cost

structure to maximize results in 2009 and to set stronger base for

2010

u Improve share versus

relevant competitive set, primarily premium and specialty

u Set stage for growth

in 2010 and beyond

Ø Improve retail

effectiveness

Ø Broaden product

range

Ø Grow direct

channel

Ø Improve household

penetration in International markets

u Maintain flexibility

to respond quickly should the economy recover

Progress

on 2009 Priorities

u Maintain a

reasonable cushion to financial covenants

ü Reduced debt by

>$100 million year to date (September 2009)

ü Lowered Debt to

EBITDA ratio to <2.0 times vs. our 3.0 times bank covenant

u Improve cost

structure to maximize results in 2009 and to set stronger base for

2010

ü Productivity program

on track - Gross margin in Q3 2009 586 bps higher than Q3 2008

ü Lowered SGA spend

16% through first three quarters of 2009 as compared to 2008

u Improve share versus

relevant competitive set, primarily premium and specialty

ü Increased mattress

market share sequentially every month of 2009

u Set stage for growth

in 2010 and beyond

ü Improve retail

effectiveness - Effective promotions, increased investment in

advertising

ü Broaden product

range - Successful launch of Cloud collection

ü Grow direct channel

- Year on year growth in 3rd quarter

2009

ü Improve household

penetration in International markets - Sensation and Sensation Lite

u Maintain flexibility

to respond quickly should the economy recover

ü Above budget

investment in advertising and R&D

ü Guidance raised on

10/15/09:

Ø Sales: $790 - $805MM

- down 15 to 13%

versus 2008

Ø Earnings: $1.00 -

$1.05 - up 6 to 12% versus

2008

Notes:

1. For a reconciliation of Funded Debt to EBITDA and 2008 Adjusted Net Income,

see Appendix to this presentation.

2.

Mattress share based on management estimates and ISPA monthly sample industry

reports for 2009

3.

For a discussion of the Company’s performance, please refer to the Company’s

press release for 3Q09 results and the Company’s prior 10K and 10Q

filings.

16

Industry Review

17

Industry

Situational Assessment

u Mattress industry

experiencing unprecedented downturn, though the market remains

large

large

u 2008 represents the

worst year on record for the bedding industry; 2009 still down

u Consumer credit,

while still available, has tightened

u Retailer

bankruptcies

u Many competitors in

financial distress

18

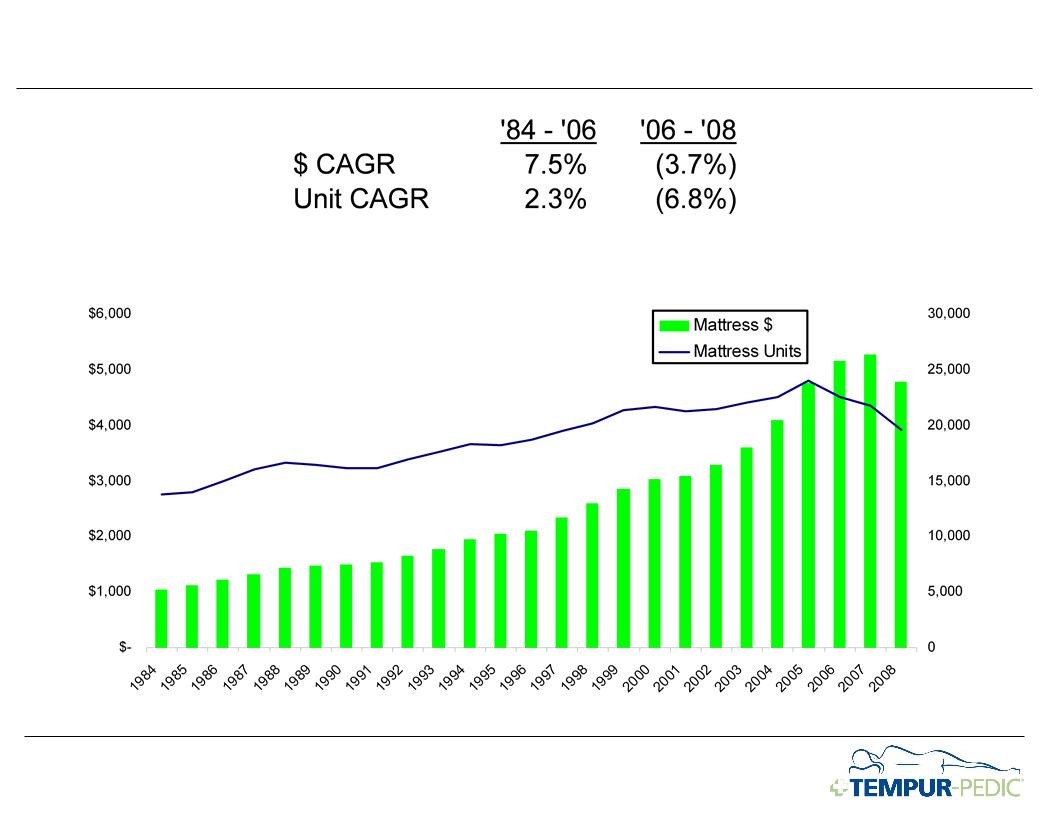

Historically,

A Steadily Growing Industry

Units

(In

Thousands)

Dollars

(In

Millions)

Source:

2008 and 2004 Annual ISPA Report of Sales and Trends

19

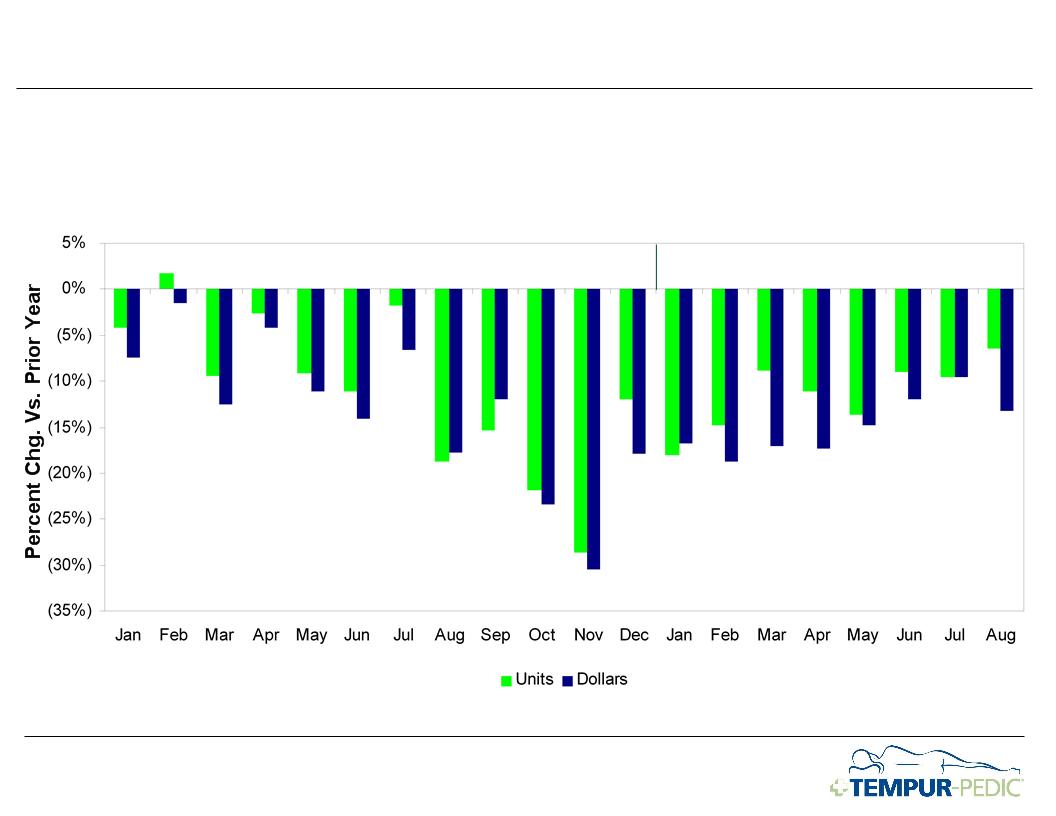

Recent

Trends Remain Weak And Unprecedented

2008

2009

Source:

2009 ISPA Sales Report

ISPA

Performance (vs. Prior Year)

20

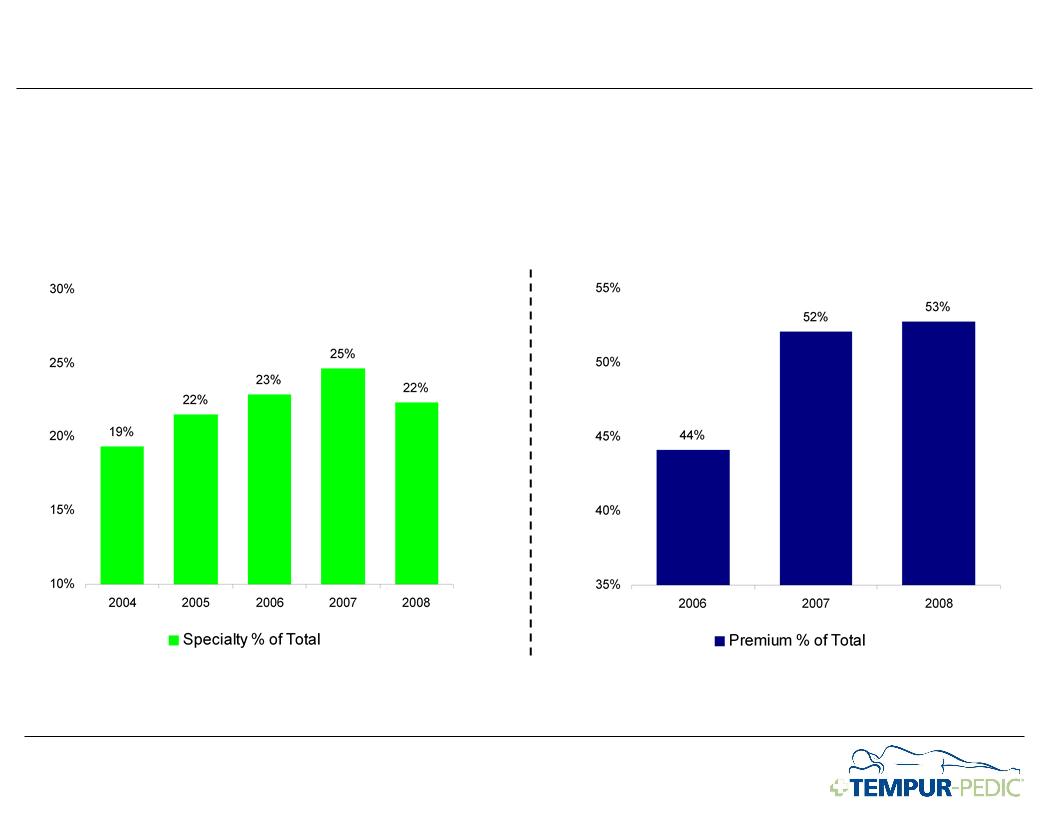

Long-term

Growth Of Specialty & Premium Mattress Segments

Source:

2008 ISPA Sales Report

Note:

Premium mattress category defined as $1,000+

Specialty

Share

Premium

Share

21

Tempur-Pedic Opportunity & Strategy

22

Very

Strong Brand Awareness, Particularly Among Premium

Buyers

Buyers

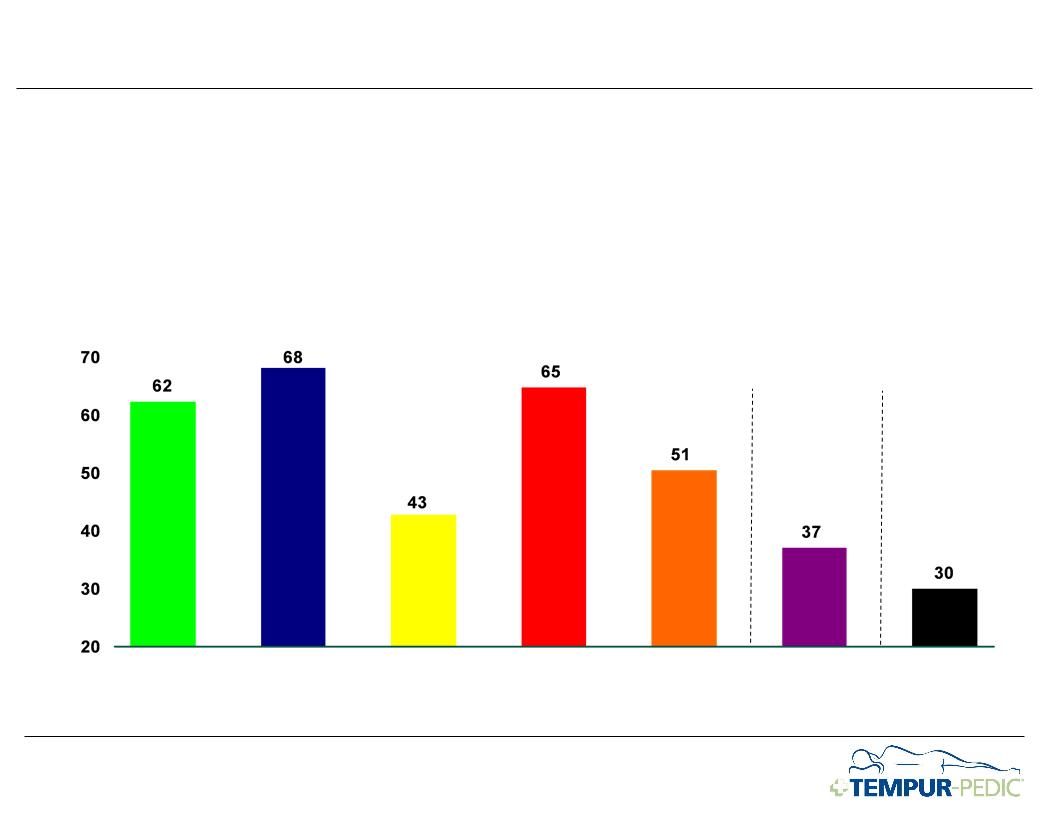

Source:

The 2008 and 2009 Gallup Consumer Mattress Market Study and Update

+28%

+3%

+0%

+4%

2004

2006

2008

All

U.S. Prospective Buyers

U.S.

Premium Prospective Buyers

2004

2006

2008

2004

2006

2008

2004

2006

2008

23

Strategic

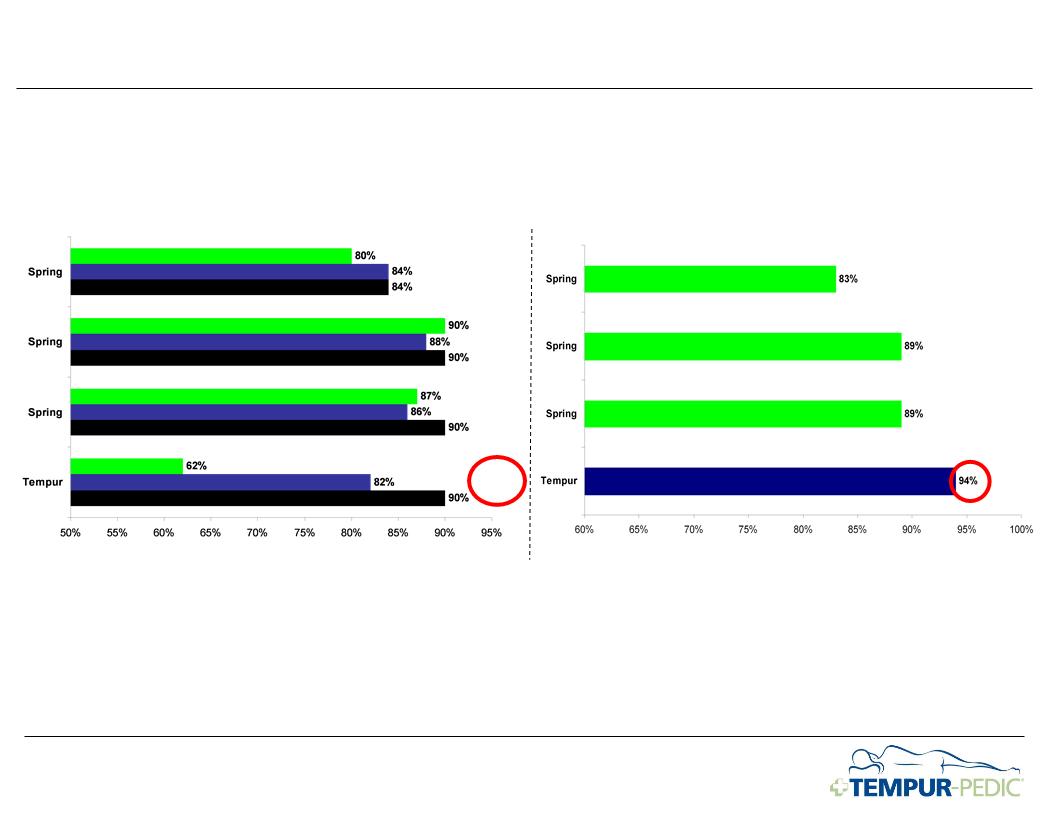

Research Summary

u Tempur-Pedic owners

like their beds much better than spring mattress owners

Ø Recommend to a

friend (top box): Tempur-Pedic: 65%, Spring 24-27%

Source:

Tempur-Pedic research

24

Strategic

Research Summary

u Tempur-Pedic owners

like their beds much better than spring mattress owners

Ø Recommend to a

friend (top box): Tempur-Pedic: 65%, Spring 24-27%

u Tempur-Pedic also

has very strong perception among the general population

Ø Most comfortable:

Tempur-Pedic 41% vs Spring 21-29%

Source:

Tempur-Pedic research

25

Strategic

Research Summary

u Tempur-Pedic owners

like their beds much better than spring mattress owners

Ø Recommend to a

friend (top box): Tempur-Pedic: 65%, Spring 24-27%

u Tempur-Pedic also

has very strong perception among the general population

Ø Most comfortable:

Tempur-Pedic 41% vs Spring 21-29%

u People say they are

going to consider a Tempur-Pedic for their next bed:

Ø Brands considered:

Tempur-Pedic: 45%, Spring 29-49%

Source:

Tempur-Pedic research

26

Strategic

Research Summary

u Tempur-Pedic owners

like their beds much better than spring mattress owners

Ø Recommend to a

friend (top box): Tempur-Pedic: 65%, Spring 24-27%

u Tempur-Pedic also

has very strong perception among the general population

Ø Most comfortable:

Tempur-Pedic 41% vs Spring 21-29%

u People say they are

going to consider a Tempur-Pedic for their next bed

Ø Brands considered:

Tempur-Pedic: 45%, Spring 29-49%

u Tempur-Pedic has

been voted best bed by Consumer Reports (October 2009)

Source:

Tempur-Pedic research

27

Strategic

Research Summary

…..and

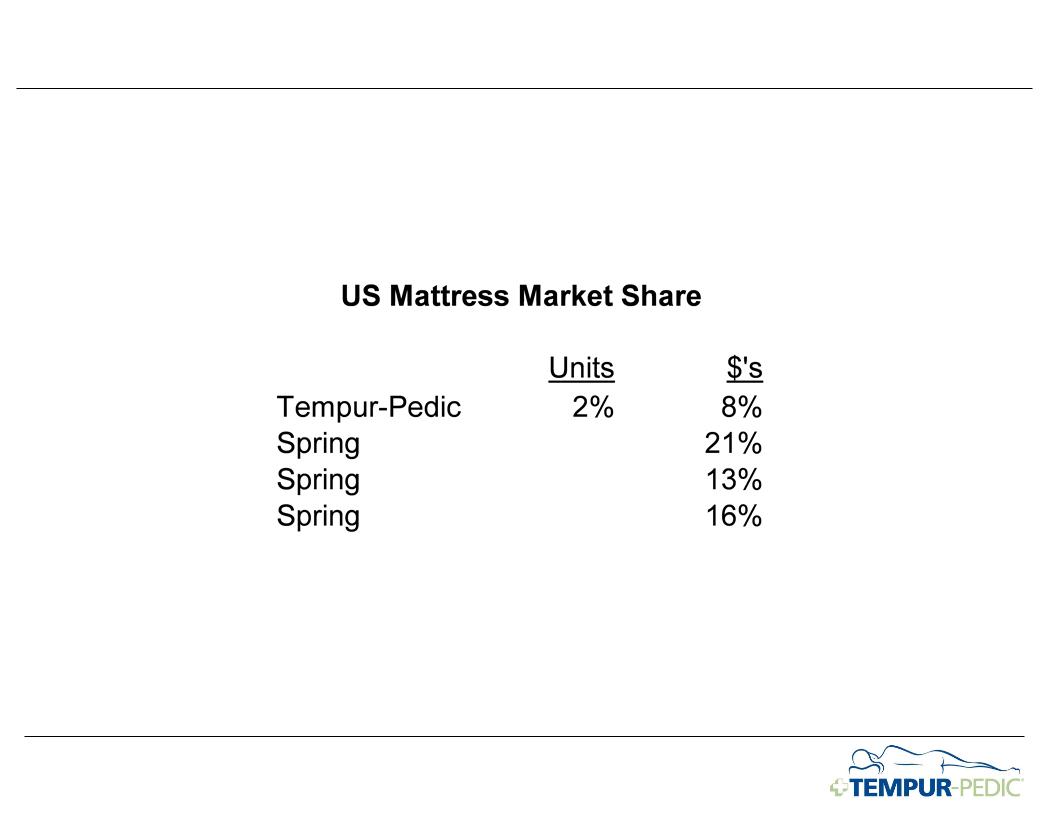

yet Tempur-Pedic has a very small market share

Source:

2007 Data - Furniture/Today market research (2008 Bedding Yearbook - Nov. 24,

2008)

28

Our

goal is to become the world’s

favorite

mattress and pillow brand.

29

How

Will We Achieve This Goal?

1. Make Sure Everyone

Knows They Would Sleep Better On Tempur

2. Make Sure There Is A

Tempur Bed And Pillow That Appeals To Everyone

3. Make Sure That

Tempur Is Available To Everyone

4. Make Sure Tempur

Continues To Deliver The Best Sleep

…and

make sure our cost structure is optimized to enable these marketing and

product development investments

product development investments

30

Tempur

Vision

People

who sleep on Tempur sleep better than those

who

don’t.

Our

goal is to become the world’s

favorite

mattress and pillow brand.

To

achieve our goal we will:

1. Make sure everyone

knows they would sleep better on Tempur

2. Make sure there is a

Tempur mattress and pillow that appeals to everyone

3. Make sure that

Tempur is available to everyone

4. Make sure Tempur

continues to deliver the best sleep

Make

sure our cost structure is optimized to enable marketing and product

investments

31

Implementing The Strategy

32

People

who sleep on Tempur sleep better than those

who

don’t.

Our

goal is to become the world’s

favorite

mattress and pillow brand.

To

achieve our goal we will:

1. Make sure everyone

knows they would sleep better on Tempur

2. Make

sure there is a Tempur mattress and pillow that

appeals to everyone

appeals to everyone

3. Make sure that

Tempur is available to everyone

4. Make sure Tempur

continues to deliver the best sleep

Make

sure our cost structure is optimized to enable marketing and product

investments

Tempur

Vision

33

1. “It’s too

expensive”

2. “It’s too

firm”

3. “It’s for ‘other

people’” (e.g. older, back pain, etc.)

Make

Sure There Is A Tempur Mattress And Pillow That Appeals

To Everyone

To Everyone

Why

isn’t Tempur-Pedic already the favorite mattress?

34

There

Is Enormous Potential For Growth Within The Price Ranges We

Currently Compete In

Currently Compete In

Source:

Tempur-Pedic estimates based on ISPA, Traqline, and management

estimates

The

AdvantageBed

by

Tempur-Pedic™

The

ClassicBed

by

Tempur-Pedic®

Queen

Mattress

$1,299

$1,299

Queen

Mattress

$1,699

$1,699

49%

Retail

Price

Point

Point

%

of Total Annual

U.S. Wholesale

Mattress Sales

U.S. Wholesale

Mattress Sales

35

1. “It’s too

expensive”

2. “It’s too

firm”

3. “It’s for ‘other

people’” (e.g. older, back pain, etc)

Make

Sure There Is A Tempur Mattress And Pillow That Appeals

To Everyone

To Everyone

Why

isn’t Tempur-Pedic already the favorite mattress?

36

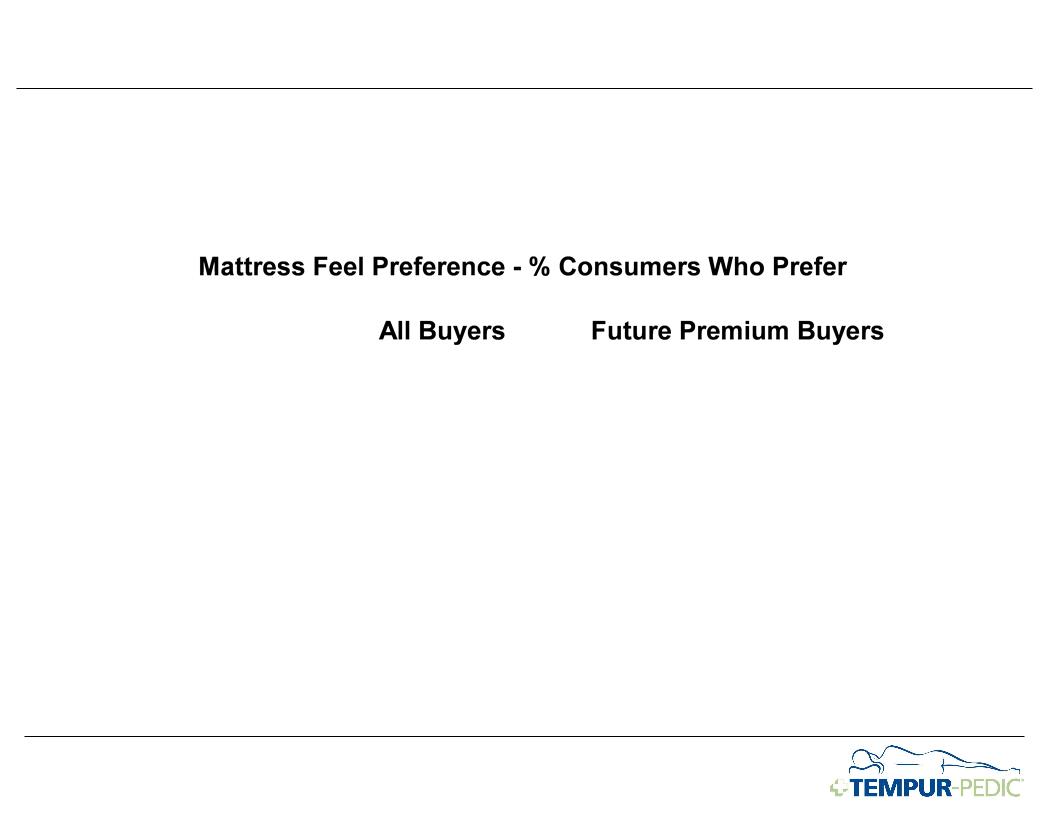

Most

Premium Mattress Buyers Prefer Soft / Medium

Source: 2009

SMI/Alcott Mattress Attitude & Usage Study

Premium

= Will spend $1,000+ for my next mattress set

Firm

Soft /

Medium

51%

49%

48%

52%

37

Initiated

A Major Research-Driven New Product Program In 9/08

Concept

Creation

Development

&

Testing

Manufacturing

Ramp-Up

Commercial-

ization

Design

Consumer

Research

38

Unprecedented

Product Research

u 15 months of

consumer research and development

u 6 separate rounds

of consumer testing

u Over 1,150 consumer

prototype evaluations

u Tested against

strong marketplace basket of competitors

u Tested via in-home

consumer sleep evaluations

u Tested among

premium buyers who prefer soft & pillow-tops

39

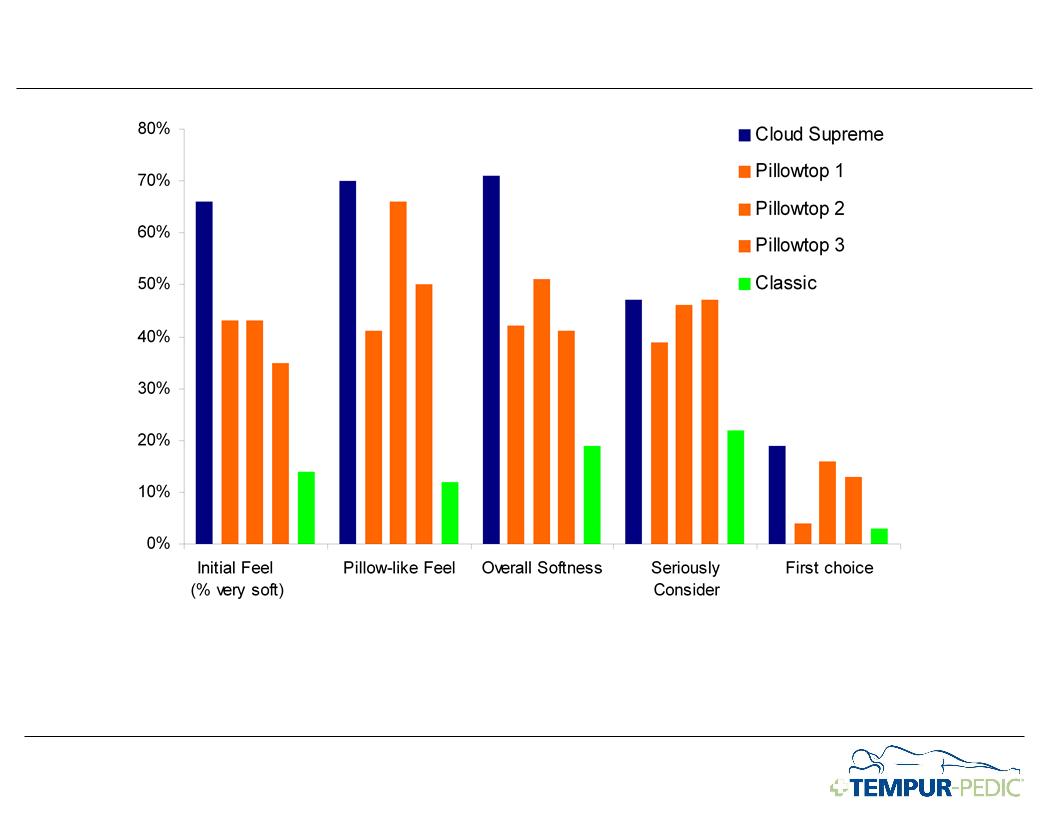

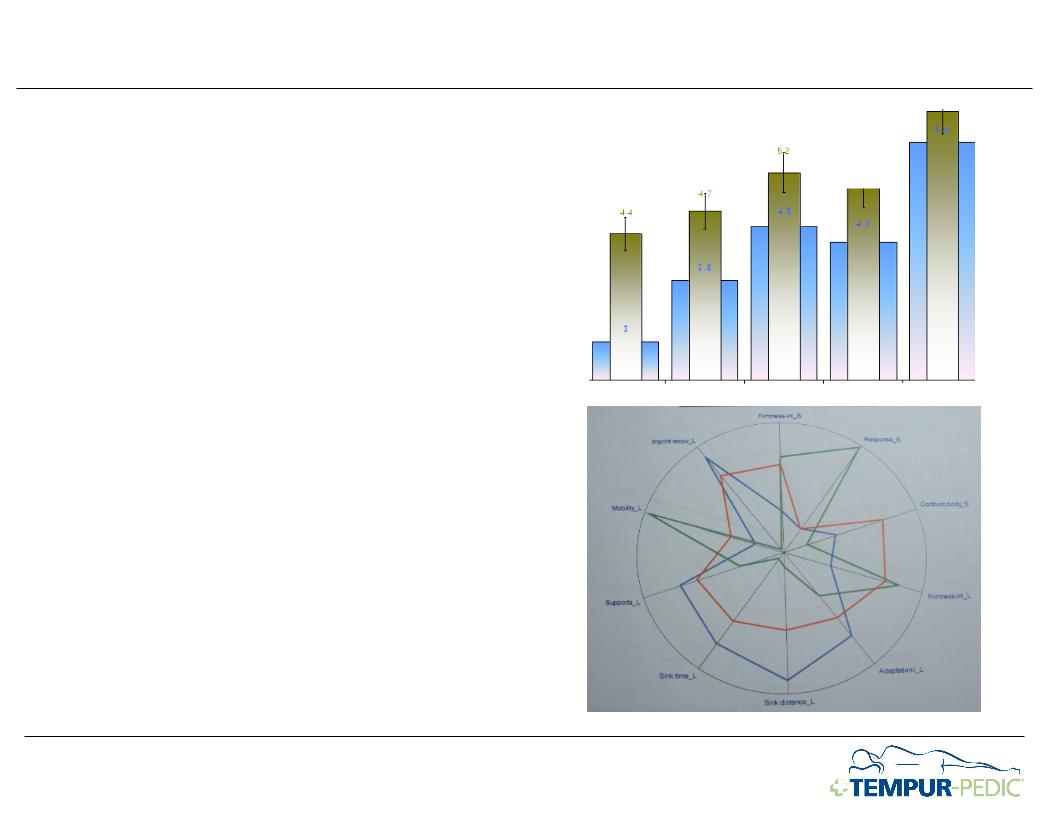

Innovation Research: Blind Sensory Room

40

Innovation

Research: Visual Design Room Layout

41

Research

Results Are Clear - Among Consumers Who Previously

Rejected

Tempur-Pedic

Tempur-Pedic

Source:

2009 Tempur-Pedic company research

Note: %

of people rating a 6 or 7 on a 7 point scale.

Better

Than

Competition

,

Different

From

Classic

42

TEMPUR-Cloud™

Supreme: 4th Quarter 2009

$1,999

Queen Mattress

Featuring

our latest formula, TEMPUR-ES™

43

TEMPUR-Cloud™:

1st Quarter 2010

$1,499

Queen Mattress

Featuring

our latest formula, TEMPUR-ES™

44

TEMPUR®

Collection

featuring

TEMPUR®

material

on

top

AdvantageBed

ClassicBed

DeluxeBed

BellaFina

Bed

CelebrityBed

Firm

Initial Feel

Excellent

Pressure Relief

Very

Supportive

Also

Introduced An Improved Brand Architecture

TEMPUR-HD®

Collection

featuring

TEMPUR-HD

® material

on

top

RhapsodyBed

BellaSonna

Bed

AlluraBed

GrandBed

Medium

Soft Initial Feel

Ultimate

in Pressure Relief

Very

Supportive

TEMPUR-Cloud™

Collection

featuring

TEMPUR-ES

™

material

on

top

TEMPUR-Cloud™

TEMPUR-Cloud™

Supreme

TEMPUR-Cloud™

Luxe

Pillowy

Soft Initial Feel

Uniquely

Responsive

Very

Good Pressure Relief

Very

Supportive

Tempur-Pedic’s

unsurpassed SUPPORT Technology is always underneath.

45

Our Sensation

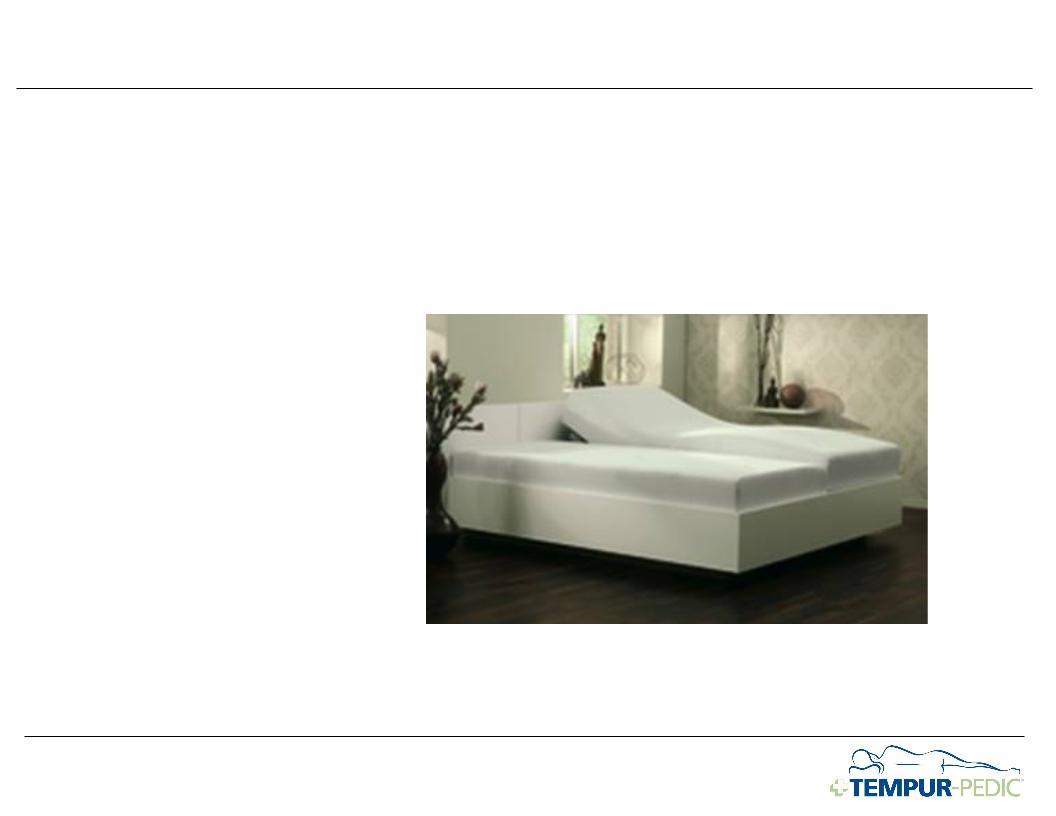

mattress line has a unique, dynamic support base

We

Are Currently Working On Our Next Generation Of Products

And Product Improvements

And Product Improvements

u Our R&D teams

are capable of designing products for nearly any consumer

requirement

requirement

u We continue to use

consumer research as a foundation

46

1. “It’s too

expensive”

2. “It’s too

firm”

3. “It’s for ‘other

people’” (e.g. older, back pain, etc.)

Make

Sure There Is A Tempur Mattress And Pillow That Appeals

To Everyone

To Everyone

Why

isn’t Tempur-Pedic already the favorite mattress?

47

u Tempur-Pedic is

rightly associated with the relief its unique

support provides people with back and neck pain…

support provides people with back and neck pain…

u But, Tempur-Pedic

owners are extraordinarily satisfied - and the

satisfaction doesn’t vary by age or medical condition

satisfaction doesn’t vary by age or medical condition

u Furthermore, desire

for Tempur-Pedic beds is greatest among the

younger, fitter generations…!

younger, fitter generations…!

Tempur-Pedic

Is For Everyone

48

Brand

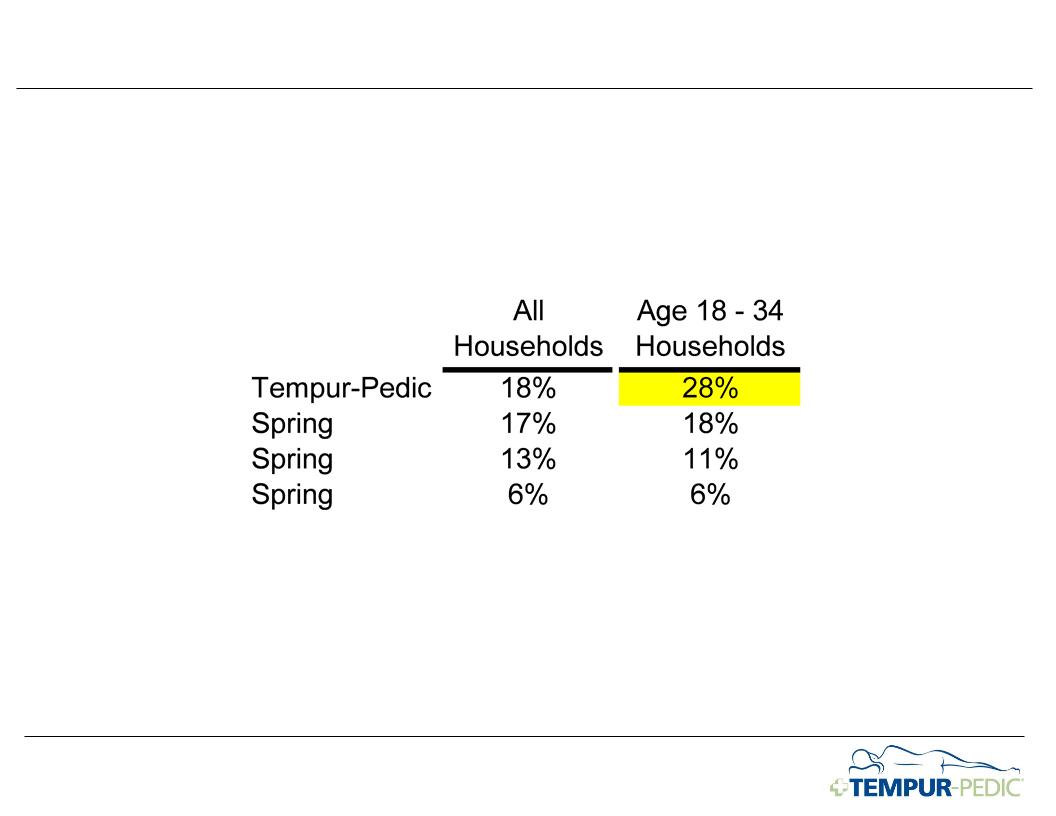

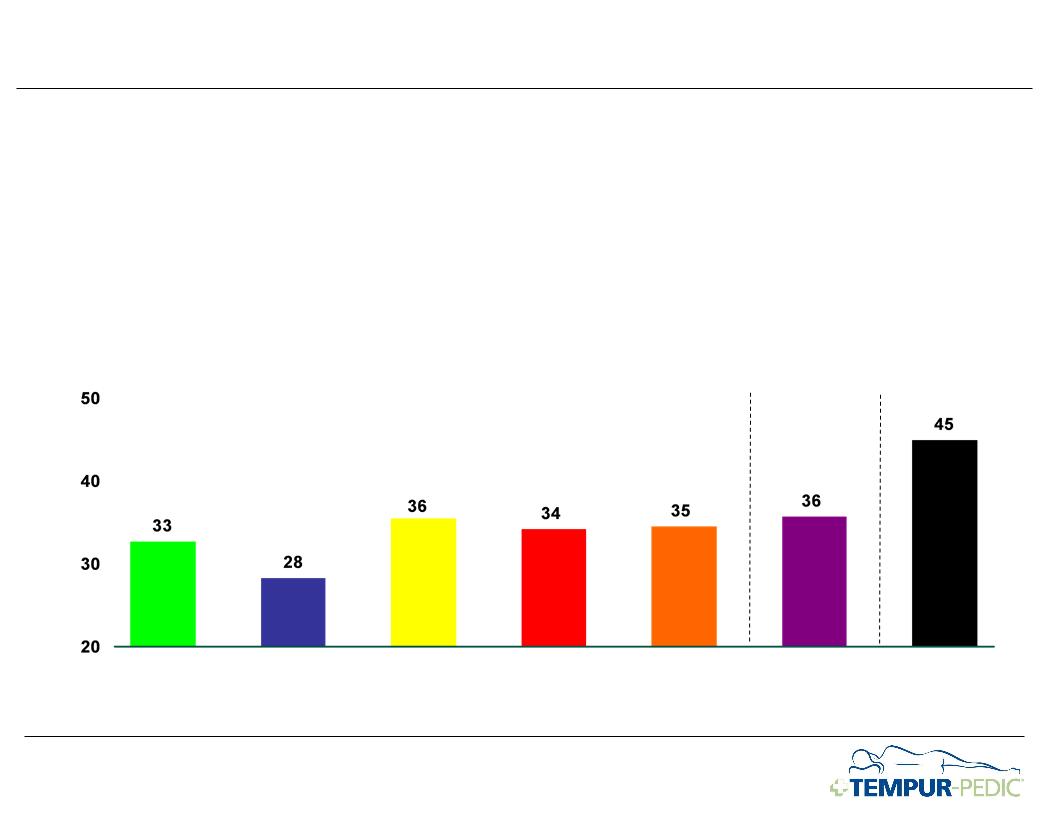

Consideration Is Strongest Among Younger Consumers

u Which

One

Brand

Are You Most Likely To Buy Next?

Source:

The 2008 and 2009 Gallup Consumer Mattress Market Study and

Update

49

People

who sleep on Tempur sleep better than those

who

don’t.

Our

goal is to become the world’s

favorite

mattress and pillow brand.

To

achieve our goal we will:

1. Make

sure everyone knows

they would sleep better on

Tempur

Tempur

2. Make sure there is a

Tempur mattress and pillow that appeals to everyone

3. Make sure that

Tempur is available to everyone

4. Make sure Tempur

continues to deliver the best sleep

Make

sure our cost structure is optimized to enable marketing and product

investments

Tempur

Vision

50

u On average,

Tempur-Pedic owners tell 14 people about their

mattress during their first year of ownership

mattress during their first year of ownership

u Consumers today

trust recommendations from friends, and even

strangers, more than advertising from businesses

strangers, more than advertising from businesses

u New advertising

campaign designed to communicate that

Tempur-Pedic is for everybody….

Tempur-Pedic is for everybody….

Leveraging

The Passion Of Our Owners

Source:

2008 Tempur-Pedic Owners Study

51

Unleashing

The Power Of Owner Satisfaction & Recommendations

52

People

who sleep on Tempur sleep better than those

who

don’t.

Our

goal is to become the world’s

favorite

mattress and pillow brand.

To

achieve our goal we will:

1. Make sure everyone

knows they would sleep better on Tempur

2. Make sure there is a

Tempur mattress and pillow that appeals to everyone

3. Make

sure that Tempur is available to everyone

4. Make sure Tempur

continues to deliver the best sleep

Make

sure our cost structure is optimized to enable marketing and product

investments

Tempur

Vision

53

Make

Sure Tempur Is Available To Everyone

u Expanding

points of distribution

Ø Opportunity for

distribution growth in the US:

Ø Potentially 500 -

1,500 incremental doors

Ø Significant

opportunity for growth in other developed markets

Ø Potentially 1,500 -

2,000 incremental doors

Ø Currently laying

groundwork for growth in China and Eastern Europe

u Improving

Effectiveness of Distribution

Ø Continuing to

strengthen the effectiveness of our promotions

Ø Improving focus and

effectiveness of our sales force

Ø Increasing the

integration of retailer and Tempur advertising

Source:

The 2008 and 2009 Gallup Consumer Mattress Market Study and

Update

54

Make

Sure Tempur Is Available To Everyone

55

People

who sleep on Tempur sleep better than those

who

don’t.

Our

goal is to become the world’s

favorite

mattress and pillow brand.

To

achieve our goal we will:

1. Make sure everyone

knows they would sleep better on Tempur

2. Make sure there is a

Tempur mattress and pillow that appeals to everyone

3. Make sure that

Tempur is available to everyone

4. Make

sure Tempur continues to deliver the best sleep

Make

sure our cost structure is optimized to enable marketing and product

investments

Tempur

Vision

56

56

Make

Sure That Tempur Continues To Deliver The Best Sleep

uTempur is developing

new

technologies to accurately

measure the physical

characteristics of mattresses

technologies to accurately

measure the physical

characteristics of mattresses

uThis is correlated

with consumer

sensory research to set design

parameters for new materials and

mattresses

sensory research to set design

parameters for new materials and

mattresses

57

58

Dale Williams

Executive Vice President & Chief Financial Officer

59

TPX

Financial Overview

60

u Difficult economy

negatively affected revenues

u Trends improving for

two consecutive quarters

($

in millions)

For

a discussion of the Company’s performance, please refer to the Company’s press

release for 3Q09 results and the Company’s prior 10K and 10Q

filings.

2004

2005

2006

2007

2008

TTM

Sept 09

Sept 09

YTD

Sept 09

Sept 09

TPX

Net Sales

61

For

a discussion of the Company’s performance, please refer to the Company’s press

release for 3Q09 results and the Company’s prior 10K and 10Q

filings.

$213M

$373M

3Q09

YTD Sales

Significant

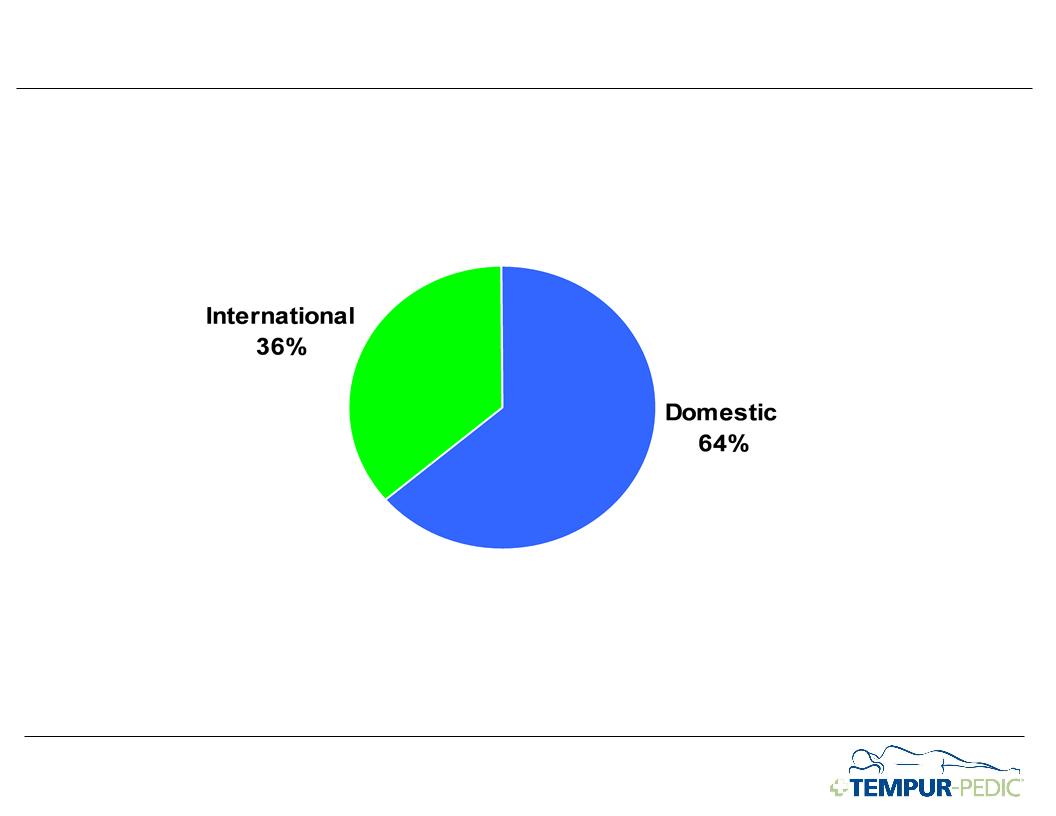

International Segment

62

International

Domestic

For

a discussion of the Company’s performance, please refer to the Company’s press

release for 3Q09 results and the Company’s prior 10K and 10Q

filings.

3Q09

YTD Sales

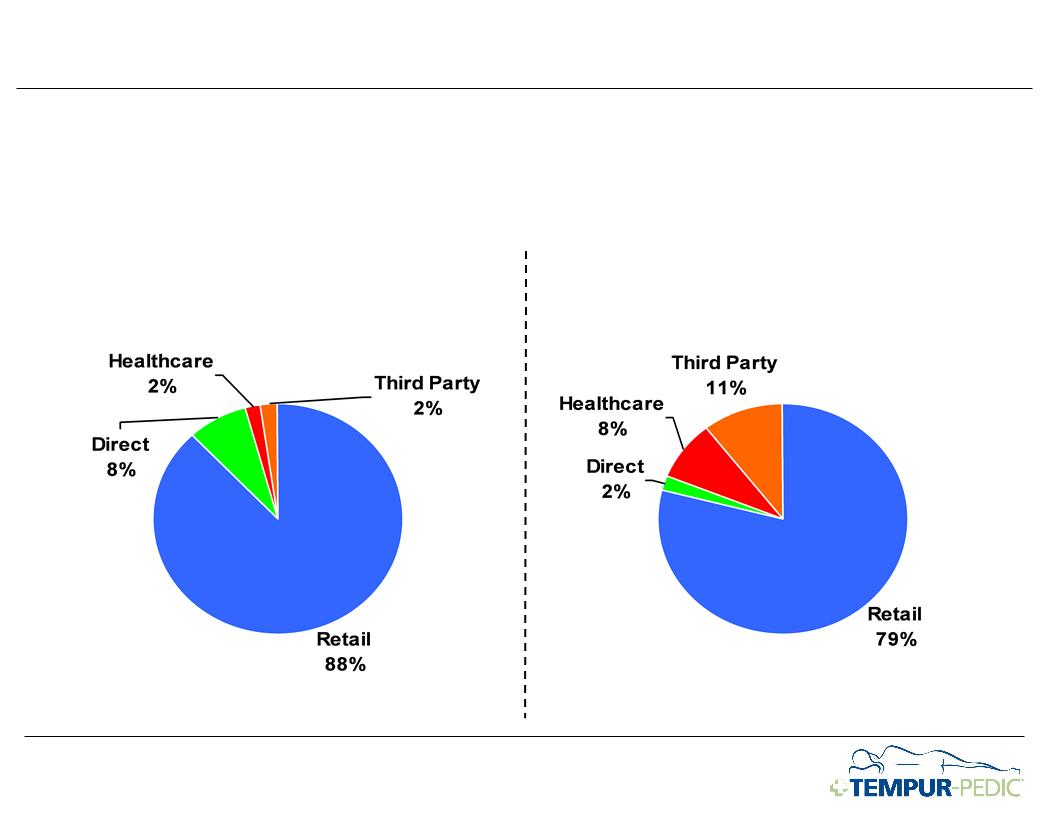

Sell

Globally Through Four Primary Channels

63

International

Domestic

For

a discussion of the Company’s performance, please refer to the Company’s press

release for 3Q09 results and the Company’s prior 10K and 10Q

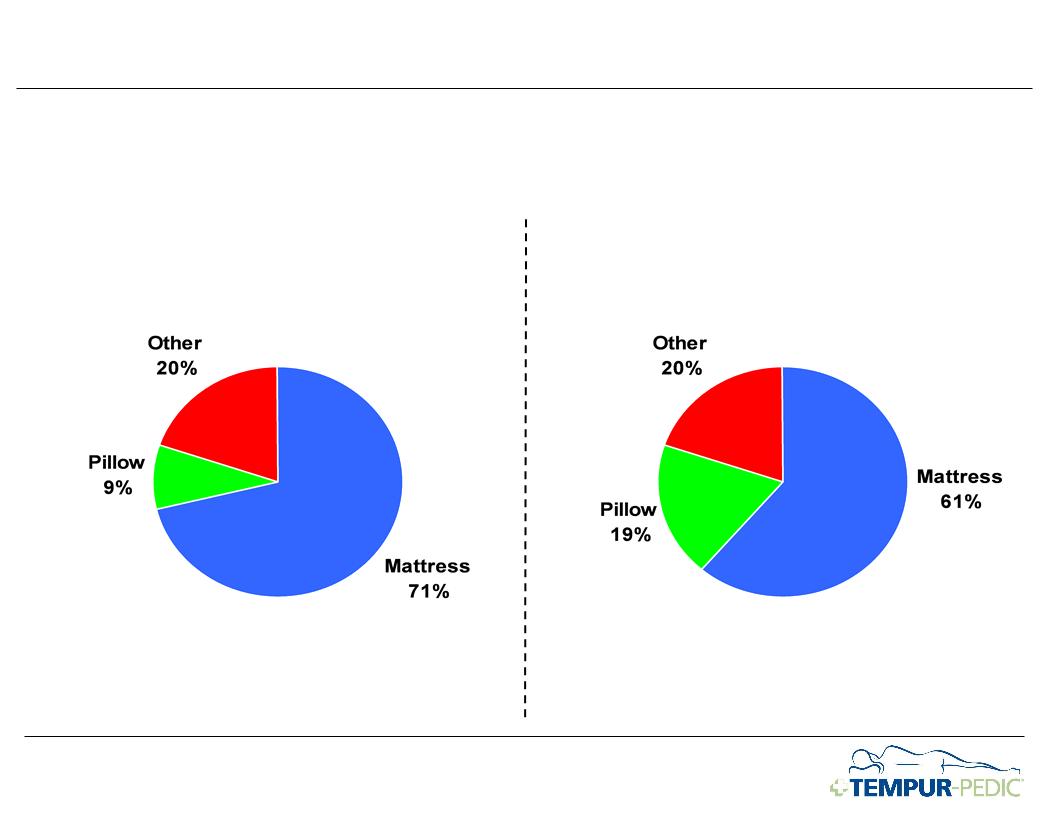

filings.

3Q09

YTD Sales

Mattresses

Drive Global Business, Yet Significant Revenue In Other

Product

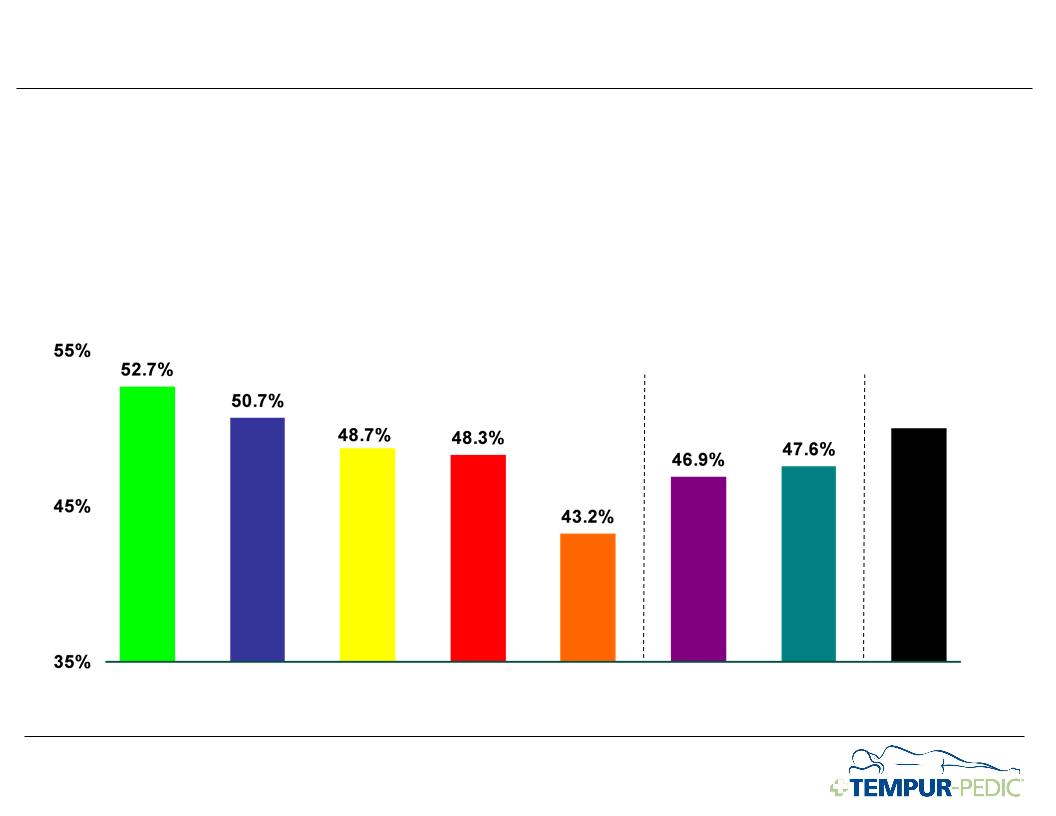

Lines

Lines

64

Cost

Imperative: Make Sure Our Cost Structure Is Optimized To

Enable Marketing And Product Development Investments

Enable Marketing And Product Development Investments

u Achieve Gross Profit

of ~50% with Operating Margin at ~25% of Net sales

u Invest ~9% of sales

in advertising and ~1% of sales in R&D

u Optimize effective

tax rate

u Optimize the use of

all capital and maintain debt at conservative levels

65

u Channel and product

mix has historically been a source of margin pressure

u In 1st year of 4 year

productivity program to drive +700 basis points of margin

u We plan to invest in

our product line to drive value and continue our technological

leadership

leadership

For

a discussion of the Company’s performance, please refer to the Company’s press

release for 3Q09 results and the Company’s prior 10K and 10Q

filings.

2004

2005

2006

2007

2008

Long

Range

Target

Range

Target

3Q09

YTD

Sept 09

Sept 09

~50%

TPX

Gross Margin

66

Significant

Effort Across The Business To Improve COGS

67

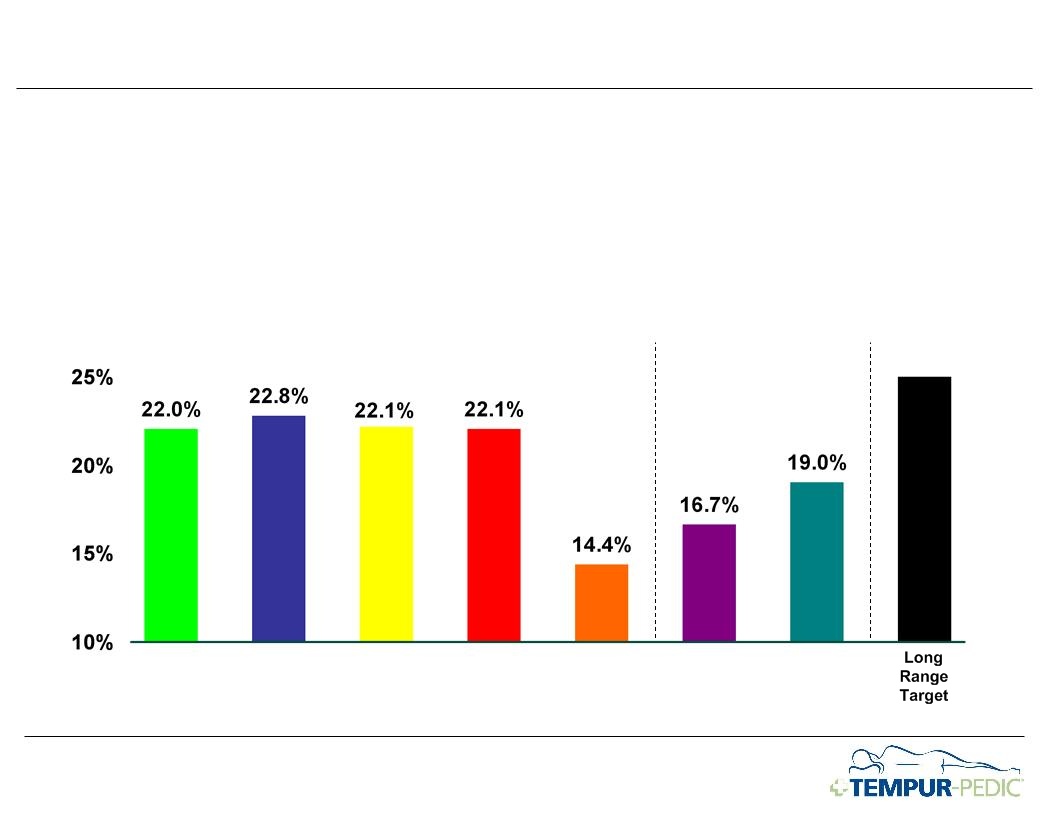

u Operating Margin has

been under pressure due to sales declines

u Over the long term,

our target for Operating Margin is ~25%

Ø Sales growth drives

leverage of fixed overheads in SG&A

Ø Maintain investment

in advertising and R&D

For

a discussion of the Company’s performance, please refer to the Company’s press

release for 3Q09 results and the Company’s prior 10K and 10Q

filings.

2004

2005

2006

2007

2008

Long

Range

Target

Range

Target

3Q09

YTD

Sept 09

Sept 09

~25%

TPX

Operating Margin

68

u We estimate our

manufacturing capacity is approximately $2.3 billion of net sales

u Based on current

plant utilization and net sales levels, believe we could triple

manufacturing output with existing plant capacity

manufacturing output with existing plant capacity

u In addition, see

opportunities to increase capacity ~5% annually above that without

significant additional capital expenditures

significant additional capital expenditures

u Implies strong

return on assets and invested capital

For

a discussion of the Company’s performance, please refer to the Company’s press

release for 3Q09 results and the Company’s prior 10K and 10Q

filings.

Manufacturing

Capacity In Place To Grow Sales ~3x

69

u Multi-year add back

to Net Income as Depreciation and Amortization should exceed

Capital Expenditures

Capital Expenditures

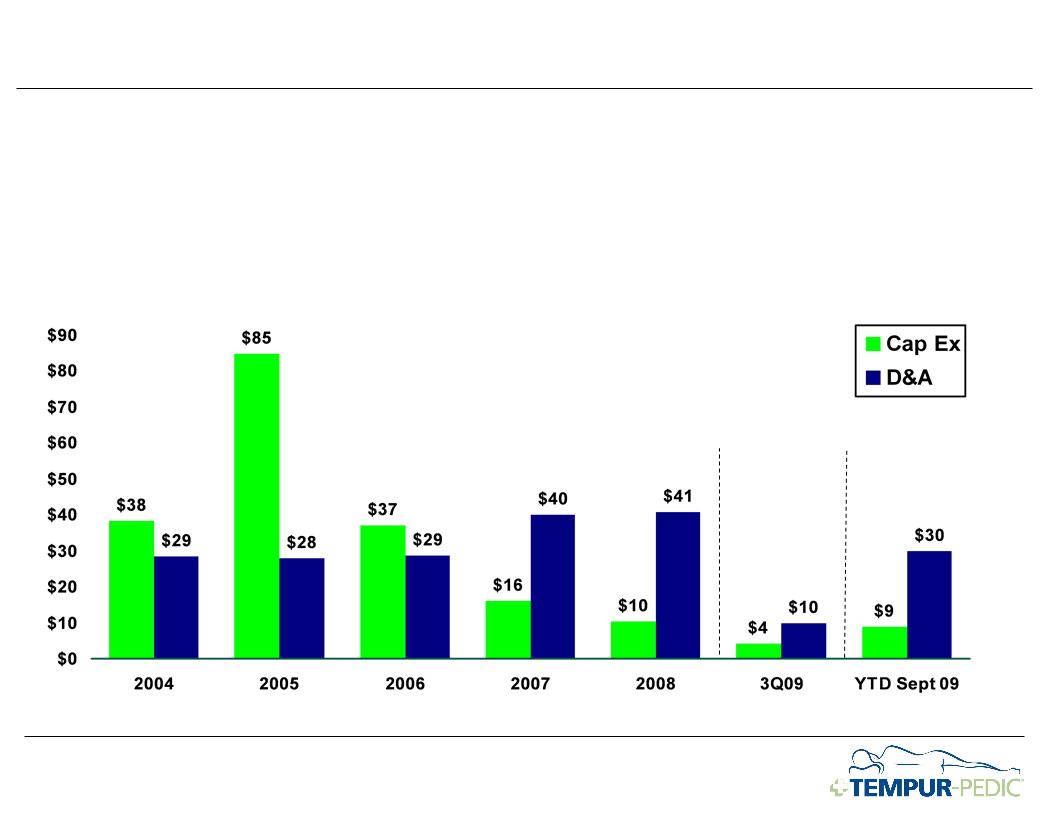

u Invested in

manufacturing footprint 2001-2006

u Anticipate annual

capital expenditures of $20 million or less for the foreseeable

future

($

in millions)

For

a discussion of the Company’s performance, please refer to the Company’s press

release for 3Q09 results and the Company’s prior 10K and 10Q

filings.

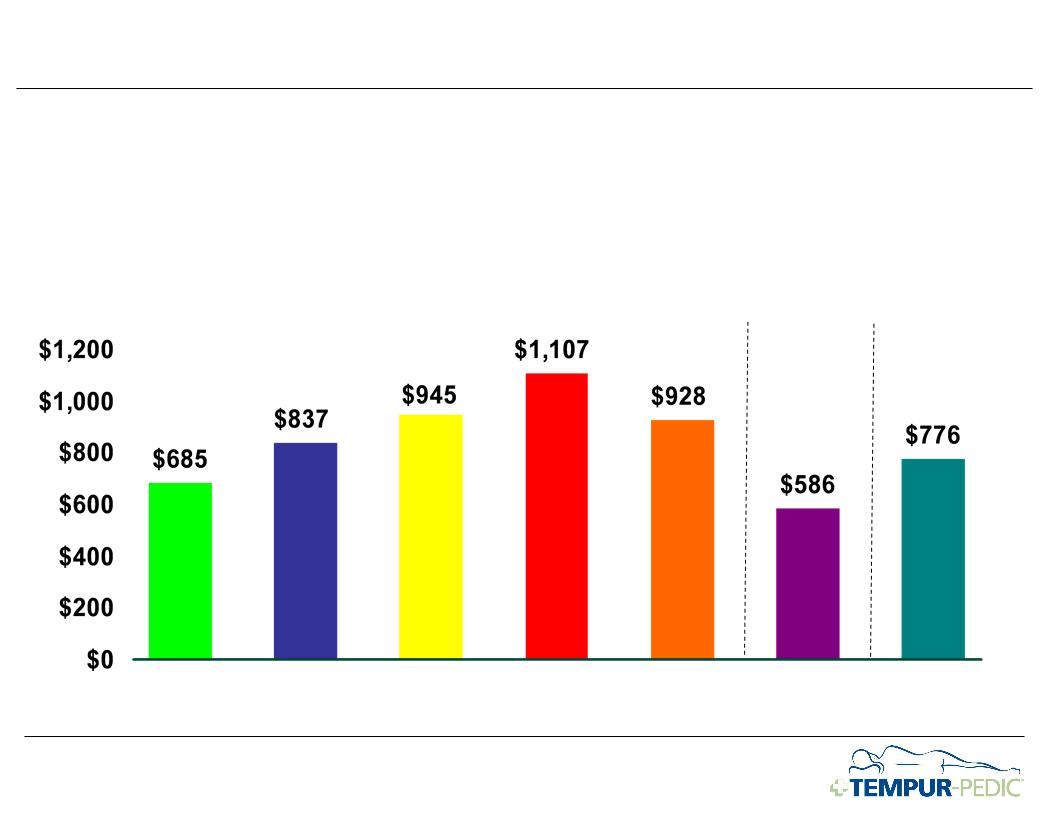

Depreciation

& Amortization vs. Capital Expenditures

For

a discussion of the Company’s performance, please refer to the Company’s press

release for 3Q09 results and the Company’s prior 10K and 10Q

filings.

Note:

For a reconciliation of 2008 Adjusted Net Income, Return on Assets, Return on

Invested Capital and a reconciliation of non-GAAP to GAAP financial

measures,

please see Appendix of this presentation.

please see Appendix of this presentation.

2004

*

*

2005

2006

2007

2008

TTM

Sept 09

Sept 09

2004

*

*

2005

2006

2007

2008

TTM

Sept 09

Sept 09

Return

on Assets

Return

on Invested Capital

Low

Levels Of Capital Should Drive High Returns Going

Forward

71

u We are focused on

driving working capital

u Significant

opportunities exist over the long term

u Long term goal of 25

day cash cycle

We

Are Focused On Driving Balance Sheet Metrics

72

u Strict credit

policies

u Will continue to

drive future improvements

For

a discussion of the Company’s performance, please refer to the Company’s press

release for 3Q09 results and the Company’s prior 10K and 10Q

filings.

2004

2005

2006

2007

2008

Long

Range

Target

Range

Target

3Q09

Days

Sales Outstanding

73

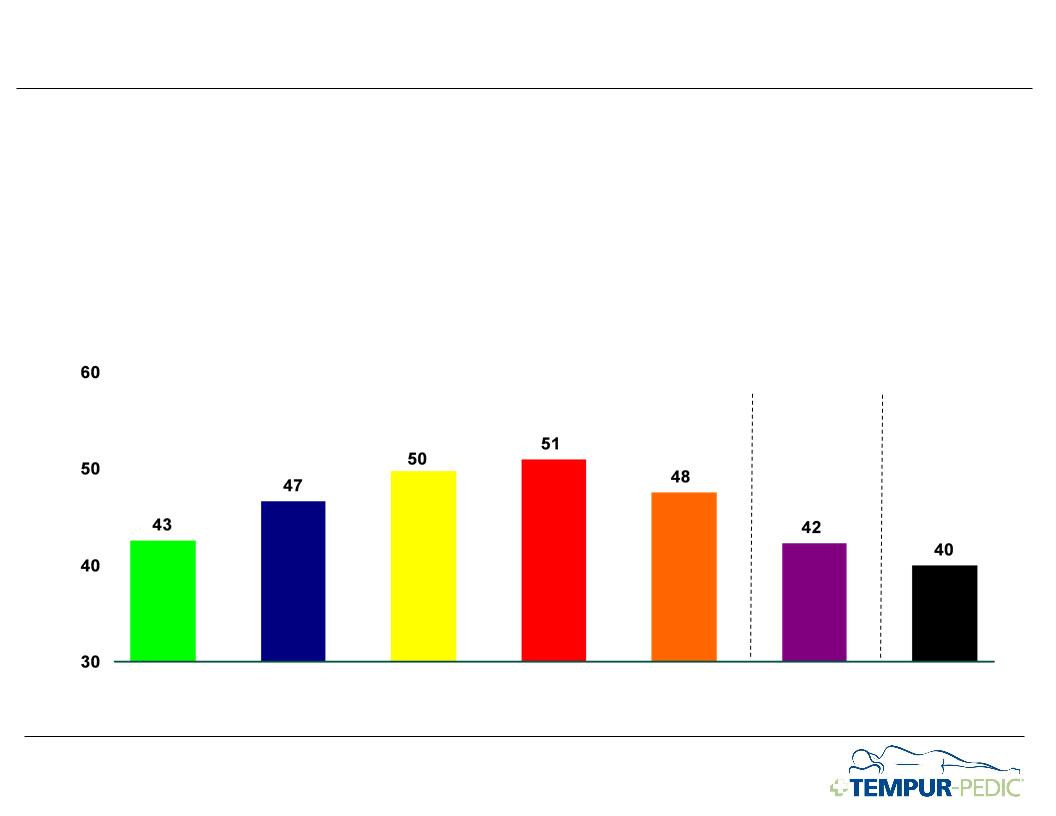

u Have been taking

early pay discounts, which shortens payables cycle è longer

term, see opportunities to extend

term, see opportunities to extend

For

a discussion of the Company’s performance, please refer to the Company’s press

release for 3Q09 results and the Company’s prior 10K and 10Q

filings.

2004

2005

2006

2007

2008

Long

Range

Target

Range

Target

3Q09

Days

Payable

74

u Significant

improvement in Inventory investment

u Optimizing

distribution network to drive further improvement

u Inventory too low as

of 3Q09 è Plan to modestly

increase inventory in 4Q09

For

a discussion of the Company’s performance, please refer to the Company’s press

release for 3Q09 results and the Company’s prior 10K and 10Q

filings.

2004

2005

2006

2007

2008

Long

Range

Target

Range

Target

3Q09

Days

Inventory

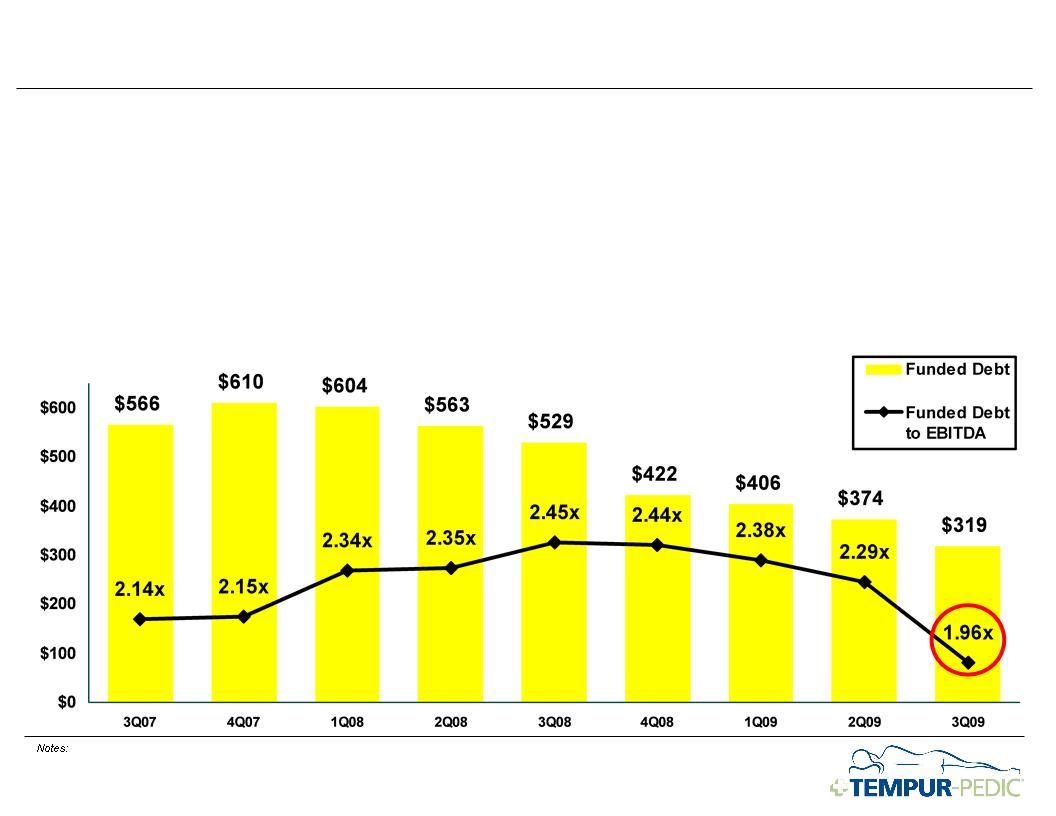

1. For

a discussion of the Company’s performance, please refer to the Company’s press

release for 3Q09 results and the Company’s prior 10K and 10Q

filings

2. Please

see Appendix A to this presentation for a

reconciliation of GAAP to Non-GAAP measures and calculation of Funded Debt to

EBITDA ratio.

u 3.0x covenant

through July 2012 (maturity)

u Substantial covenant

cushion

($

in millions)

Funded

Debt to EBITDA Covenant

76

Note

1: For a discussion of the Company’s performance, please refer to the Company’s

press release for 3Q09 results and the Company’s prior 10K and 10Q

filings

Note

2: Management estimates and assumptions.

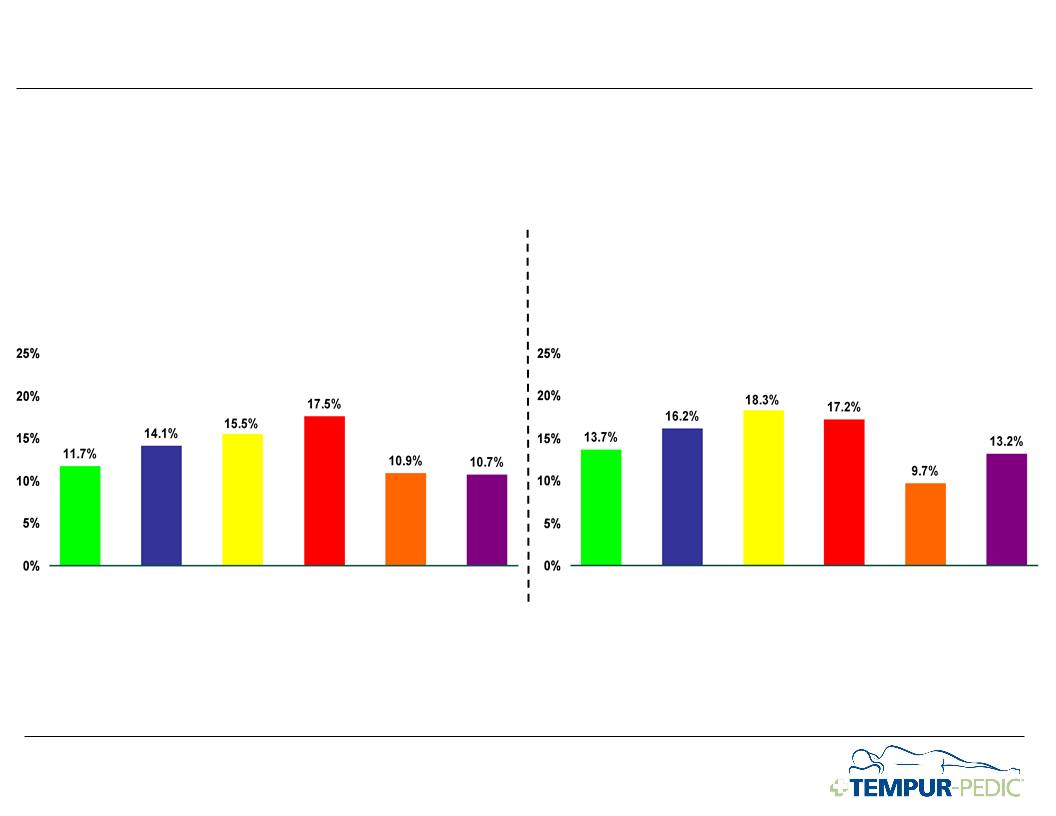

u We believe the

actions we have taken have substantially improved our

profitability

profitability

u Ongoing productivity

program will be supplemented with volume leverage

Ø Targeting Gross

Profit Margin to expand to 50% vs. 48.3% in ‘07

u At increasing rates

of sales, we expect margins to expand

Ø Targeting Operating

Profit Margin to expand to 25% vs. 22.1% in ‘07

Ø Driven by Gross

Profit Margin expansion and fixed cost leverage of

operating expenses

operating expenses

u Improved Capital

Structure results in lower interest expense

Ø Run rate ~1/2 of ’07

interest cost

Enhanced

Earnings Power In Our Business Model

78

Appendix

79

Reconciliation

of EBITDA to Net Income and Funded debt to Total debt

Non-GAAP

Measures

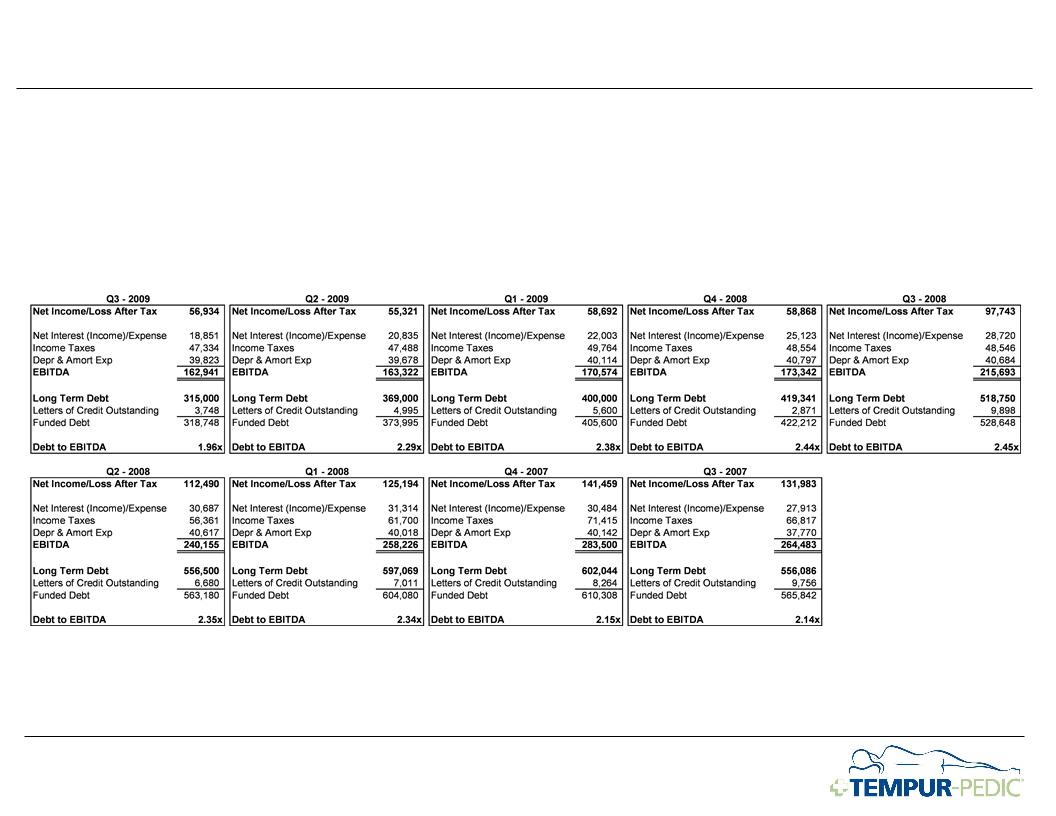

The

Company provides information regarding EBITDA and Funded debt which are not

recognized terms under GAAP (Generally Accepted Accounting

Principles) and do not purport to be alternatives to Net income as a measure of operating performance or Total debt. Because not all companies use

identical calculations, these presentations may not be comparable to other similarly titled measures of other companies. A reconciliation of EBITDA to the

Company’s Net income and a reconciliation of Funded debt to Total debt are provided below. Management believes that the use of these non-GAAP

financial measures provides investors with additional useful information with respect to the terms of the Company’s credit facility.

Principles) and do not purport to be alternatives to Net income as a measure of operating performance or Total debt. Because not all companies use

identical calculations, these presentations may not be comparable to other similarly titled measures of other companies. A reconciliation of EBITDA to the

Company’s Net income and a reconciliation of Funded debt to Total debt are provided below. Management believes that the use of these non-GAAP

financial measures provides investors with additional useful information with respect to the terms of the Company’s credit facility.

The

following tables set forth the reconciliation of the Company’s reported Net

income to the calculation of EBITDA and the reconciliation of the

Company’s reported Total debt to the calculation of Funded debt:

Company’s reported Total debt to the calculation of Funded debt:

GAAP

To Non-GAAP Reconciliations - Funded Debt / EBITDA

80

Reconciliation of

Adjusted Net Income to Net Income TTM 2009 and 2008 and Adjusted Earnings Per

Share for 2008

Non-GAAP

Measures

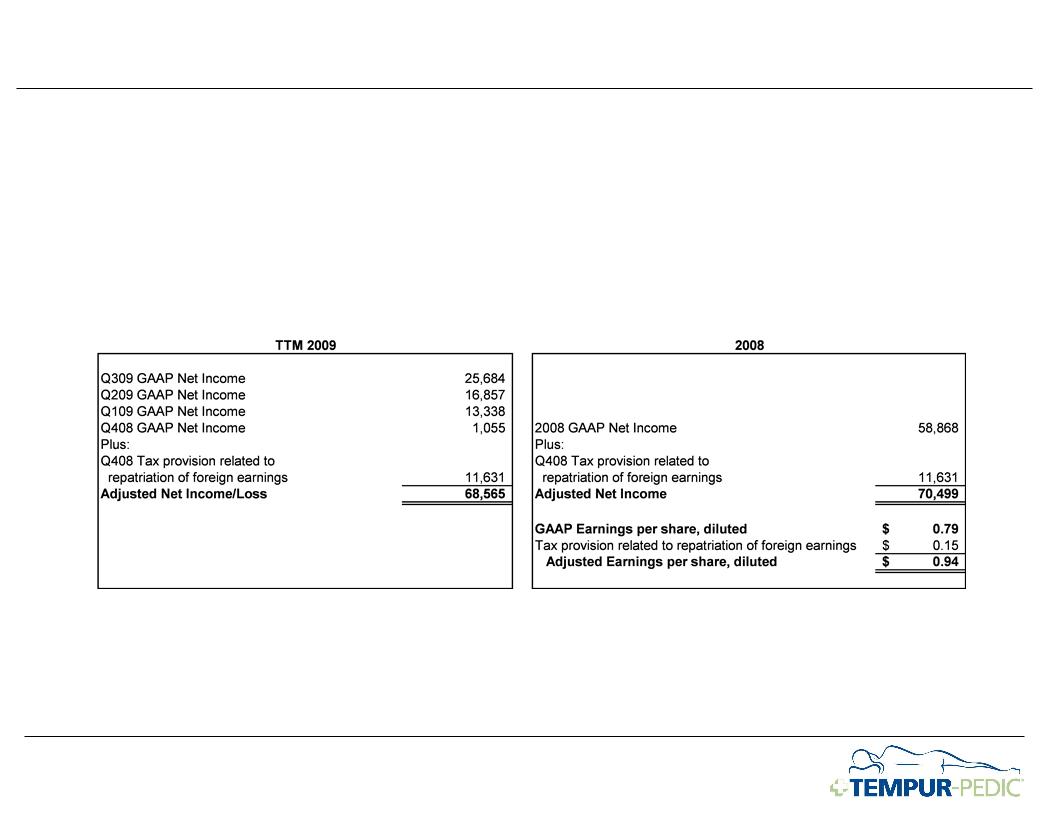

The

Company provides information regarding Adjusted Net income and Adjusted Earnings

per share which are not recognized terms under GAAP

(Generally Accepted Accounting Principles) and do not purport to be alternatives to Net income and Earnings per share as a measure of operating

performance. Because not all companies use identical calculations, these presentations may not be comparable to other similarly titled measures of other

companies. A reconciliation of Adjusted Net income and Adjusted Earnings per share to the Company’s Net income and Earnings per share is provided

below. Management believes that the use of these non-GAAP financial measures provides investors with additional useful information with respect to the

impact of the repatriation of foreign earnings.

(Generally Accepted Accounting Principles) and do not purport to be alternatives to Net income and Earnings per share as a measure of operating

performance. Because not all companies use identical calculations, these presentations may not be comparable to other similarly titled measures of other

companies. A reconciliation of Adjusted Net income and Adjusted Earnings per share to the Company’s Net income and Earnings per share is provided

below. Management believes that the use of these non-GAAP financial measures provides investors with additional useful information with respect to the

impact of the repatriation of foreign earnings.

The

following table sets forth the reconciliation of the Company’s reported Net

income to the calculation of Adjusted Net income for the trailing nine

months ending September 30, 2009 and twelve months ended December 31, 2008 and the reconciliation of the Company’s reported Earnings per share

to the calculation of Adjusted Earnings per share for the twelve months ended December 31, 2008.

months ending September 30, 2009 and twelve months ended December 31, 2008 and the reconciliation of the Company’s reported Earnings per share

to the calculation of Adjusted Earnings per share for the twelve months ended December 31, 2008.

GAAP

To Non-GAAP Reconciliations - Net Income and Earnings

Per Share

Per Share

81

The

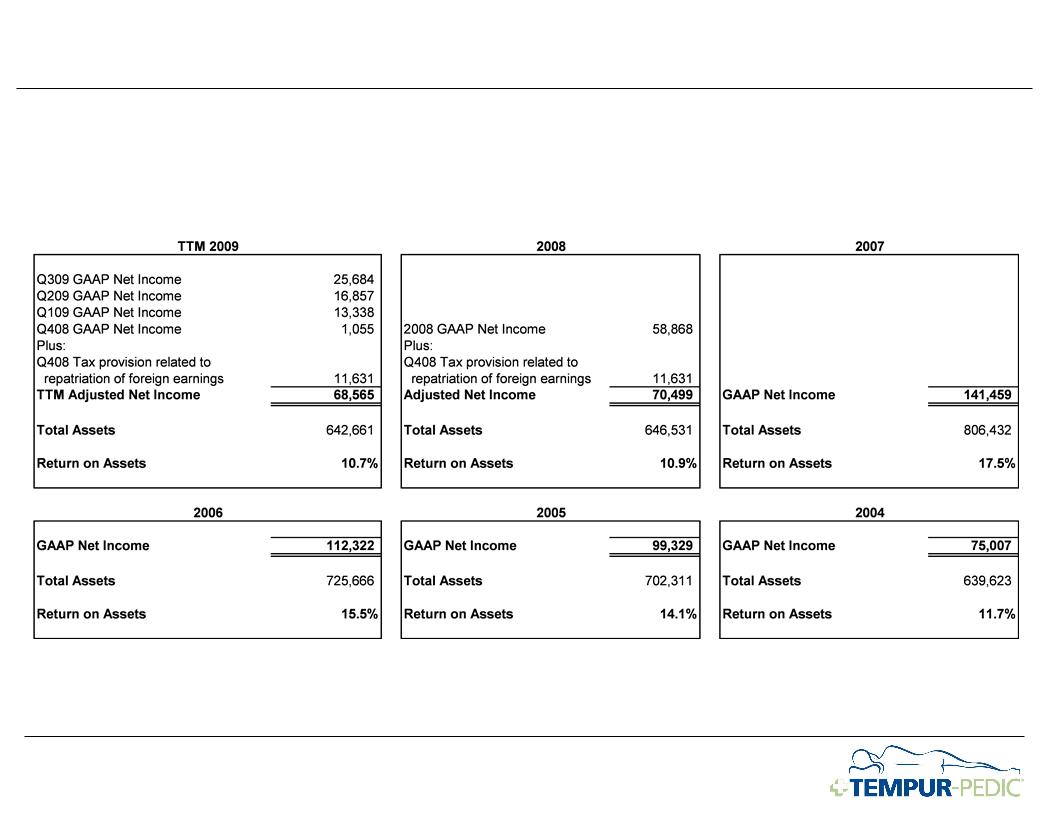

Company provides information regarding Return on Assets as the Company believes

it provides investors with

useful information. Return on Assets is calculated by dividing Net Income/Loss by Total Assets as reported in the

Company's 10K and 10Q filings. No adjustment for dividends was made in this calculation. See the GAAP to Non-GAAP

Reconciliation for a reconciliation of Adjusted Net Income in 2008.

useful information. Return on Assets is calculated by dividing Net Income/Loss by Total Assets as reported in the

Company's 10K and 10Q filings. No adjustment for dividends was made in this calculation. See the GAAP to Non-GAAP

Reconciliation for a reconciliation of Adjusted Net Income in 2008.

Calculation

Of Return On Assets

82

The

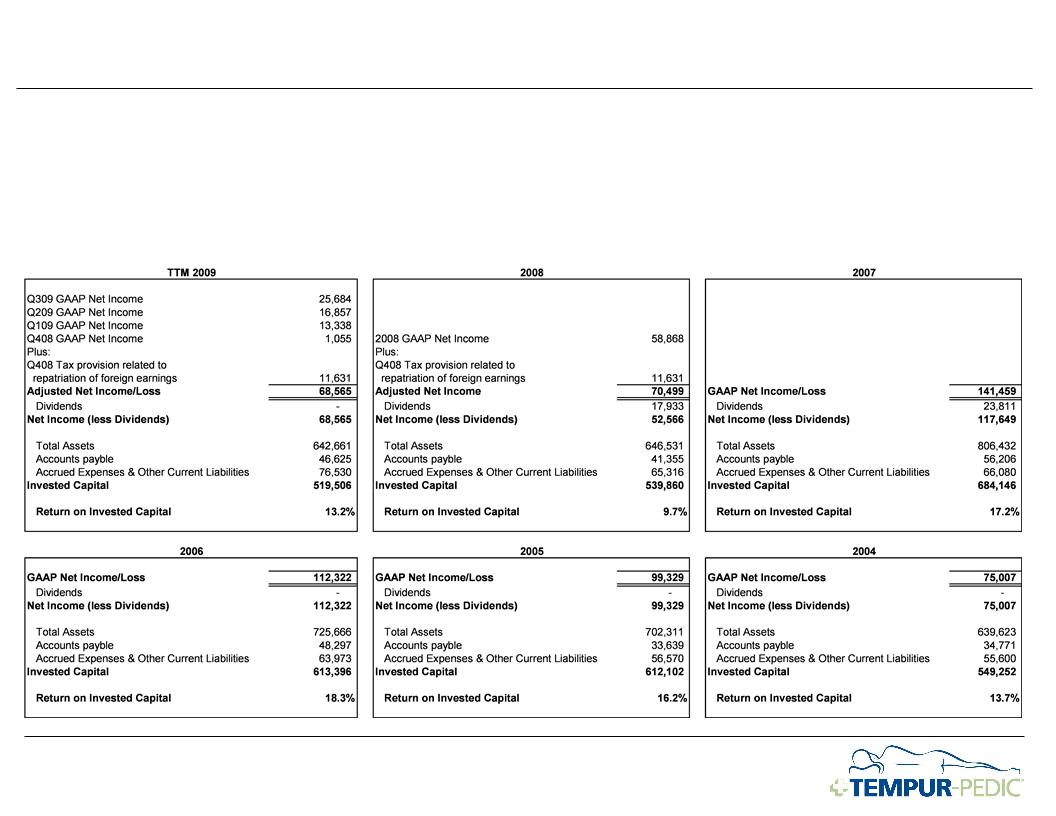

Company provides information regarding Return on Invested Capital as the Company

believes it provides investors

with useful information. We consider our Invested Capital to be Total Assets less Accounts Payable and Accrued

Expenses & Other Current Liabilities as reported in the company's 10K and 10Q filings. Return on Invested Capital is

calculated by dividing Net Income/Loss (less any dividends) by Invested Capital. See the GAAP to Non-GAAP

Reconciliation for a reconciliation of Adjusted Net Income in 2008.

with useful information. We consider our Invested Capital to be Total Assets less Accounts Payable and Accrued

Expenses & Other Current Liabilities as reported in the company's 10K and 10Q filings. Return on Invested Capital is

calculated by dividing Net Income/Loss (less any dividends) by Invested Capital. See the GAAP to Non-GAAP

Reconciliation for a reconciliation of Adjusted Net Income in 2008.

Calculation

Of Return On Invested Capital