Attached files

| file | filename |

|---|---|

| EX-23.1 - EX-23.1 - Birds Eye Foods, Inc. | a2194823zex-23_1.htm |

Use these links to rapidly review the document

Table of contents

Index to consolidated financial statements

As filed with the Securities and Exchange Commission on October 8, 2009

No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER

THE SECURITIES ACT OF 1933

Birds Eye Foods, Inc.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

2030 (Primary Standard Industrial Classification Code Number) |

26-0398310 (I.R.S. Employer Identification No.) |

90 Linden Oaks

PO Box 20670

Rochester, New York 14625

(585) 383-1850

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

Neil Harrison

Chairman and Chief Executive Officer

Birds Eye Foods, Inc.

90 Linden Oaks

PO Box 20670

Rochester, New York 14625

(585) 383-1850

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies of all communications, including communications sent to agent for service, should be sent to: | ||

Joshua N. Korff, Esq. Kirkland & Ellis LLP 601 Lexington Avenue New York, New York 10022 (212) 446-4800 |

Arthur D. Robinson, Esq. Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, New York 10017 (212) 455-2000 |

|

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

|

||||

| Title of each class of securities to be registered |

Proposed maximum aggregate offering price(1)(2) |

Amount of registration fee(2) |

||

|---|---|---|---|---|

Common Stock, $0.01 par value per share |

$350,000,000 | $19,530 | ||

|

||||

(1) Includes shares of common stock that the underwriters may purchase (including pursuant to the option to purchase additional shares, if any) from the selling stockholder.

(2) Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated October 8, 2009

Prospectus

shares

BIRDS EYE FOODS, INC.

Common stock

This is the initial public offering of our common stock. Of the shares of common stock to be sold in the offering, we are selling shares and Birds Eye Holdings LLC, which we refer to as Holdings or the selling stockholder, is selling shares. We will not receive any of the proceeds from the shares of common stock being sold by the selling stockholder. We expect the initial public offering price to be between $ and $ per share.

Prior to the offering, there has been no public market for our common stock. We expect to apply for listing of our common stock on The under the symbol " ."

| |

Per share |

Total |

|||||

|---|---|---|---|---|---|---|---|

Initial public offering price |

$ | $ | |||||

Underwriting discount |

$ |

$ |

|||||

Proceeds to Birds Eye Foods, Inc., before expenses |

$ |

$ |

|||||

Proceeds to the selling stockholder, before expenses |

$ |

$ |

|||||

Investing in our common stock involves a high degree of risk. See "Risk factors" beginning on page 14 of this prospectus.

The selling stockholder has granted the underwriters an option for a period of 30 days from the date of this prospectus to purchase up to additional shares of our common stock at the public offering price less the underwriting discount to cover over-allotments.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares on or about , 2009.

J.P.Morgan

, 2009

You should rely only on the information contained in this prospectus or in any free-writing prospectus we may specifically authorize to be delivered or made available to you. We have not and the underwriters have not authorized anyone to provide you with additional or different information. We are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where such offers and sales are permitted. The information in this prospectus or in any free-writing prospectus is accurate only as of its date, regardless of its time of delivery or of any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

Until , 2009 (25 days after the commencement of the offering), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the dealer's obligation to deliver a prospectus when acting as an underwriter and with respect to unsold allotments or subscriptions.

i

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider in making your investment decision. You should read the following summary together with the entire prospectus, including the more detailed information regarding us, the common stock being sold in this offering and our financial statements and the related notes appearing elsewhere in this prospectus. You should carefully consider, among other things, the matters discussed in the sections entitled "Risk factors" and "Management's discussion and analysis of financial condition and results of operations" in this prospectus before deciding to invest in our common stock. Some of the statements in this prospectus constitute forward-looking statements. See "Forward-looking statements."

Except where the context otherwise requires or where otherwise indicated, the terms "Birds Eye," "we," "us," "our," "our company" and "our business" refer to Birds Eye Foods, Inc. and its consolidated subsidiaries as a combined entity. Certain differences in the numbers in the tables and text throughout this prospectus may exist due to rounding.

The fiscal year of Birds Eye ends on the last Saturday in June. Fiscal year 2007 consisted of 53 weeks, while fiscal years 2008 and 2009 consisted of 52 weeks each. For example, references to "fiscal year 2009" refer to our fiscal year ended June 27, 2009.

Except for volume data relating to Birds Eye, or as otherwise noted herein, the industry, market and competitive position data contained in this prospectus have been compiled by us based on data and other information obtained from International Resources, Inc., which we refer to as IRI. We note that IRI data relating to the size of markets exclude non-traditional grocery channels such as Walmart and other club, dollar and mass merchandisers. The IRI data is for the 52 week period ended on September 6, 2009, unless otherwise noted. All market share data are based on U.S. dollar sales at retail, unless otherwise noted. While we believe that industry publications, studies and surveys, such as those released by IRI, are reliable, we have not independently verified industry, market and competitive position data from third-party sources. Accordingly, investors should not place undue weight on the industry, market and competitive position data presented in this prospectus.

Our company

We are a leading marketer, manufacturer, and distributor of branded, packaged food products, including an expanding platform of healthy, high-quality frozen vegetables and frozen meals and a portfolio of branded specialty foods. Our frozen food products are marketed under the iconic Birds Eye brand name which holds the #1 market share position in frozen vegetables and the #2 market share position in complete bagged meals. Our branded specialty food products, which include fruit fillings and toppings, snack foods and chili products, hold many leading market share positions in their core geographic markets. We believe the Birds Eye brand generated approximately $1 billion in retail sales in 2009 (including Walmart), and is one of the fastest growing major brands in the U.S. frozen food industry. Over the past several years, we have made considerable investments to strengthen our Birds Eye brand and expand our portfolio of product offerings, which has resulted in meaningful net sales growth. From fiscal year 2005 to fiscal year 2009, our consolidated net sales grew from $636 million to $936 million, representing a compound annual growth rate, which we refer to as CAGR of

1

10.1%, and our consolidated Adjusted EBITDA (as defined in footnote 9 in "—Summary consolidated financial and other data") grew from $88 million to $150 million, representing a CAGR of 14.2%. See "—Summary consolidated financial and other data" for more information. We operate two primary business segments: our frozen food group and our specialty food group.

Our frozen food group, which includes our Birds Eye frozen vegetables and our Voila! and Steamfresh complete bagged meals, accounted for 69.2% of our fiscal year 2009 net sales. We have grown our frozen food business by successfully developing innovative new products in both the frozen vegetables and frozen complete bagged meal categories supported by consistent and significant marketing investment. Birds Eye is the largest U.S. frozen vegetables brand with our steamed and non-steamed product offering and holds a 26.5% market share. Our Steamfresh product line offers consumers an innovative method to steam Birds Eye vegetables and meals in a specially designed microwaveable bag. Our complete bagged meal product portfolio holds a combined 21.8% market share and includes our value-oriented Voila! products and our premium Steamfresh products. Voila! and Steamfresh complete bagged meals offer consumers value-added meal solutions that include a protein, starch and vegetables in one convenient package. Our strong historical net sales growth benefited from actions taken in both frozen vegetables and complete bagged meals. Also, we experienced growth from the introduction of Steamfresh vegetables in fiscal year 2006 and within the complete bagged meal category we have driven net sales growth through both our Voila! product line and our introduction of Steamfresh meals in fiscal year 2009. From fiscal year 2005 to fiscal year 2009, our frozen food segment net sales grew from $363 million to $647 million representing a CAGR of 15.5%, and Segment EBITDA (as defined in footnote 10 under "—Summary consolidated financial and other data") grew from $55 million to $94 million representing a CAGR of 14.1%.

Our specialty food group accounted for 29.9% of our fiscal year 2009 net sales. From fiscal year 2005 to fiscal year 2009 the specialty food group improved Segment EBITDA margins from 12.7% to 21.3% thereby generating strong cash flow. In fiscal year 2009, the specialty food group segment had net sales of $279 million and Segment EBITDA of $60 million.

Our industrial-other segment comprises the remaining 1% of our net sales, which are frozen vegetables sold to a limited number of industrial customers.

Industry overview

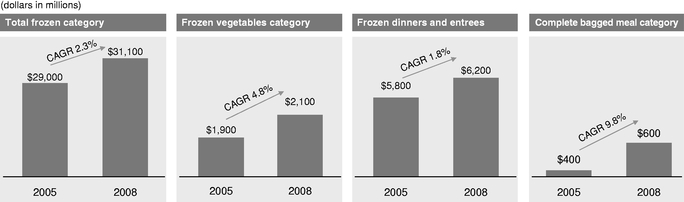

The U.S. frozen food industry is a large, attractive market supported by favorable consumer and retailer fundamentals. The frozen dinners and entrees (excluding pizza) and frozen vegetables categories represented the first and fifth largest categories within the U.S. frozen food industry and generated approximately $6 billion and approximately $2 billion in grocery channel retail sales, respectively. In addition to grocery channel retail sales, we estimate that Walmart represents an additional 27% and 22% of the overall retail sales of the frozen dinners and entrees and frozen vegetables markets, respectively. The complete bagged meal segment of the frozen dinners and entrees category generates annual grocery channel retail sales of approximately $580 million. From calendar year 2005 to 2008, frozen food industry grocery channel retail sales grew at a CAGR of approximately 2.3%, while our key category segments, including frozen dinners and entrees and frozen vegetables grew at a CAGR of approximately 1.8% and 4.8%, respectively, while the complete bagged meal segment grew at a CAGR of approximately 9.8%. We believe that the steam-based vegetables category will experience less

2

growth in the future than during its initial development years. In addition, we anticipate that our primary categories will experience heightened levels of competition resulting in an increase in the number of new product introductions, pricing pressures and increased couponing. See "Management's discussion and analysis of financial condition and results of operations." We believe that recent growth in categories like frozen dinners and entrees and frozen vegetables has been driven by increased consumer demand for good tasting, convenient and nutritious meals and snacks.

Our competitive strengths

Iconic Birds Eye brand with leading U.S. market share positions

Birds Eye is one of the most recognized frozen vegetables brands in the United States as evidenced by our 54% unaided brand awareness as of May 2009. Birds Eye currently holds the #1 market share position with a 26.5% share of the U.S. frozen vegetables category. On a combined basis, Steamfresh and Voila! hold the #2 market share position with a combined 21.8% share of the U.S. complete bagged meal category. We believe that our leading market share positions provide us with a competitive advantage in key areas such as premium pricing, shelf space allocation, and our ability to grow through brand extensions and new product development in both existing and new categories.

Successful history of innovation and new product development

Over our last five fiscal years, we have focused our research and development efforts on the frozen vegetables and complete bagged meal categories. With the launch of Steamfresh in January 2006, we were the first company to capture a nationwide market share with a microwaveable product that enables consumers to conveniently steam vegetables in their packaging. Since that time, the steamed vegetables category has grown to become an approximately $580 million category for the retail grocery channel. Since the introduction of the complete bagged meal category in the late 1990's, which we entered in 1998 with the introduction of Voila!, the category has grown to become an approximately $580 million category for the retail grocery channel. As a result of our continued focus on new product development, approximately 15.4% and 17.9% of our net sales of the frozen food group in fiscal years 2009 and 2008, respectively, were generated by products that we did not sell two years prior. Our product innovation has contributed to Birds Eye becoming the fastest growing major brand in the frozen food category over the past three calendar years with a retail grocery channel sales CAGR of 14.9%.

Excellent, longstanding relationships with leading U.S. retailers

We have longstanding relationships with leading U.S. retailers, many of which we have been doing business with for over two decades. For the 52-week period ended June 14, 2009, weighted average annual retail sales of Birds Eye frozen vegetables represented approximately 40% of the sales of branded frozen vegetables and 21% of complete bagged meals sold by our eight largest customers—C&S Wholesale, Food Lion, Kroger, Publix, Safeway, SuperValu, Wakefern (Shop Rite) and Walmart. We have been recognized throughout the industry with many awards and acknowledgements, including awards for packaging excellence, new product initiatives and category insight. We have a strong relationship with Walmart, which generated approximately 25% of our fiscal year 2009 net sales.

3

Proven strategy that has delivered strong organic growth

We have implemented a successful strategic plan to invest in and grow our Birds Eye brand through increased consumer marketing (which we define to include coupon redemption expense, advertising, research, package design and other marketing expenses) and trade promotions (which we define as promotional spending, slotting expenses and discounts and allowances), targeted product innovation, brand extensions and a continued focus on competing in higher margin, growing categories. As a result, we have become a market leading, branded food company with a track record of attractive organic growth and significantly improved operating results. From fiscal year 2005 to fiscal year 2009, we increased our spending on consumer marketing for our frozen food group at a CAGR of approximately 19%. During this same time period, our consolidated net sales grew from $636 million in fiscal year 2005 to $936 million in fiscal year 2009, representing a CAGR of 10.1%. Despite the recent U.S. economic recession, our consolidated net sales grew from $868 million in fiscal year 2008 to $936 million in fiscal year 2009, representing an increase of 7.8%, and our consolidated Adjusted EBITDA grew from $140 million to $150 million, representing an increase of 7.2%.

Experienced and focused management team

We have an experienced senior management team, with our eight most senior executives averaging 12 years with our company and over 25 years of experience in the highly competitive branded consumer goods industry. Following a comprehensive strategic review in 2005, management has successfully executed a strategy that has enabled us to become a market-leading, branded frozen food business. As such, we believe that continued strategic investments in our Birds Eye brand and focus on product innovation will help drive strong net sales and Adjusted EBITDA growth while enhancing our leading market share positions.

Our strategy

We intend to expand our position as a leading innovator and marketer of frozen foods by pursuing the following strategies:

Continue to deliver excellent consumer value by leveraging our iconic Birds Eye brand and leading U.S. market share positions

We continuously strive to provide consumers with high quality, great tasting and convenient products sold at competitive prices. We believe that our continued efforts to deliver innovative products will support the leading market share positions of our Birds Eye products and will offer opportunities for future brand extensions, as well as support our pricing strategies.

Continue to innovate and support the Birds Eye brand, with significant consumer marketing and trade promotions

We have invested significant funds in developing a growing pipeline of new products that we believe will strengthen our leading U.S. market share positions. We utilize rigorous and consistently applied processes and criteria to launch successful new products, and then support these new products with strategic consumer marketing and trade promotions. We target consumer marketing and trade promotions expense as a percentage of frozen food net sales in the high single digits. Our new product initiatives focus on emerging consumer trends, broadening consumer demographics and increasing meal and snack time opportunities for consumers to enjoy our products throughout the day.

4

Enhance margins through optimization of product mix and cost reduction initiatives

In 2006, we divested our lower margin, non-branded business as part of our successful re-emphasis on branded frozen products, and have since focused on the attractive, higher growth and higher margin branded frozen food segment. Through this effort, we have decreased our base SKU count from approximately 4,500 to 480 since fiscal year 2005. By actively managing both our product mix towards higher gross margin SKUs and our operating efficiencies, we believe we can continue to drive gross margin enhancement.

Maintain the strong free cash flow of the specialty food group

We are dedicated to continuing the strong free cash flow of the specialty food group through cost-effective trade promotions and competitive pricing while reducing production and overhead costs. The segment has historically generated high margins and strong free cash flow with fiscal year 2009 Segment EBITDA margin of 21.3% and Segment EBITDA of $60 million. We expect to leverage the strong free cash flow from the specialty food group to supplement investment in our faster growing frozen food group and assist with paying down our debt.

Risk factors

An investment in our common stock involves a high degree of risk, and our ability to successfully operate our business is subject to numerous risks, including those that are generally associated with operating in the retail industry. You should carefully consider the following, as well as the more detailed discussion of risk factors set forth under "Risk factors" and the other information included in this prospectus:

- •

- we may experience liabilities or adverse effects on our reputation as a result of product recalls;

- •

- the effects of strong competition in the food industry, including competitive pricing and marketing actions, could

adversely affect our profitability and market share;

- •

- if we fail to protect our key brand names, infringe intellectual property rights of third parties or inadequately protect

our intellectual property rights, our business could be harmed;

- •

- the loss of one or more of our significant customers may adversely affect our results of operations;

- •

- the consolidation of retail customers may adversely impact our operating margins and profitability;

- •

- we may be unable to anticipate changes in consumer preferences and buyer behavior as well as risks associated with new

product introductions, which could adversely impact our profitability;

- •

- changes in consumer preferences, including shifts to lower-priced alternatives as a result of the global economic crisis

or otherwise, could adversely affect our business; and

- •

- fluctuations in the cost and availability of supply chain elements could increase operating costs and lower profitability.

5

Our corporate structure

On August 19, 2002, pursuant to the terms of the Unit Purchase Agreement dated June 20, 2002, by and among Pro-Fac Cooperative, Inc., a New York agricultural cooperative, which we refer to as Pro-Fac, Birds Eye Group, Inc. (f/k/a Birds Eye Foods, Inc.), at the time a wholly-owned subsidiary of Pro-Fac, and Birds Eye Holdings LLC (f/k/a Vestar/Agrilink Holdings LLC), a Delaware limited liability company, which we refer to as Holdings, Holdings and its affiliates acquired control of us.

Birds Eye Foods, Inc. was incorporated as a Delaware corporation in 2007. We are a wholly-owned subsidiary of Holdings, and are the sole stockholder of Birds Eye Holdings, Inc., which in turn is the sole stockholder of Birds Eye Group, Inc., our principal operating subsidiary. At September 30, 2009, funds affiliated with Vestar Capital Partners, which we refer to as Vestar, Pro-Fac, and our management and directors had ownership interests in Holdings of approximately 55%, 40%, and 5%, respectively. Vestar has a voting majority of all outstanding Holdings common units. Following this offering, Holdings will own approximately % of our common stock (approximately % if the underwriters' option to purchase additional shares is exercised in full).

The following is a summary chart of our corporate structure as of the date hereof:

6

Corporate and other information

Our executive offices are located at 90 Linden Oaks, Rochester, New York 14625, and our telephone number is (585) 383-1850. Our principal website address is www.birdseyefoods.com. Information contained on any of our websites is not incorporated into, and does not constitute part of this prospectus.

Birds Eye, Steamfresh and Voila! are some of our registered trademarks. Other brand names or trademarks appearing in this prospectus are the property of their respective owners. Solely for convenience, our trademarks and tradenames referred to in this prospectus are without the ® symbol, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensors to these trademarks and tradenames.

7

| Issuer | Birds Eye Foods, Inc., a Delaware corporation. | |

Selling stockholder |

Birds Eye Holdings LLC |

|

Common stock offered by us |

shares of common stock, par value $0.01 per share. |

|

Common stock offered by the selling stockholder |

shares of common stock, par value $0.01 per share. |

|

Over-allotment option |

The selling stockholder has granted the underwriters an option to purchase up to an additional shares of common stock within 30 days of the date of this prospectus in order to cover over-allotments, if any. |

|

Common stock outstanding after this offering |

shares of common stock outstanding. |

|

Offering price |

We expect the offering price to be between $ and $ per share. |

|

Use of proceeds |

We estimate that the net proceeds to us from this offering, after deducting underwriting discount and estimated offering expenses, will be approximately $ million, assuming shares offered at $ per share, the midpoint of the price range set forth on the cover of this prospectus. We will not receive any of the proceeds from the shares of common stock being sold by the selling stockholder. |

|

We intend to use approximately $ million of our net proceeds from this offering to repay outstanding term loans pursuant to a credit agreement among Birds Eye Foods, Inc., UBS Loan Finance, LLC, as the lender and UBS AG, Stamford Branch, as administrative agent, which we refer to as the Birds Eye Credit Facility. See "Use of proceeds," "Capitalization" and "Description of certain indebtedness." |

||

Dividend policy |

We have no current plans to pay any cash dividends in the foreseeable future. |

|

Proposed symbol |

" " |

8

| Directed share program | At our request, the underwriters have reserved up to % of the shares of common stock offered hereby for sale at the initial public offering price to persons who are directors, officers or employees, or who are otherwise associated with us, through a directed share program. The sales will be made by through a directed share program. We do not know if these persons will choose to purchase all or any portion of these reserved shares, but any purchases they do make will reduce the number of shares available to the general public. See "Underwriting." | |

Risk factors |

You should carefully read and consider the information set forth under "Risk factors" and all other information set forth in this prospectus before investing in our common stock. |

Unless otherwise indicated, all information contained in this prospectus assumes:

- •

- no exercise of the underwriters' option to purchase up to additional shares of common stock

from the

selling stockholder to cover over-allotments, if any; and

- •

- that the common stock to be sold in this offering is sold at $ , which is the midpoint of the range set forth on the cover page of this prospectus.

Except as otherwise noted, the number of shares of our common stock stated in this prospectus to be outstanding after this offering:

- •

- gives effect to a -for-one stock split to take place immediately prior to completion

of this offering; and

- •

- excludes shares of common stock reserved for issuance under the equity compensation plan that we plan to adopt in connection with this offering.

9

Summary consolidated financial and other data

The following table sets forth our summary consolidated financial and other data for the periods and as of the dates indicated. The selected income statement data for the fiscal years ended June 30, 2007, June 28, 2008 and June 27, 2009 and selected consolidated balance sheet data as of June 27, 2009 are derived from our audited consolidated financial statements included elsewhere in this prospectus. Our subsidiary, Birds Eye Holdings, Inc., was previously directly, wholly owned by Holdings. Holdings transferred its ownership interest in Birds Eye Holdings, Inc. (and, indirectly, Birds Eye Group, Inc.) to us on July 1, 2007, making each of Birds Eye Holdings, Inc. and its subsidiary Birds Eye Group, Inc., a wholly-owned subsidiary of ours. This transaction was accounted for as a reorganization of entities under common control, and accordingly, there was no change in the basis of the underlying assets and liabilities. The accompanying consolidated financial statements for fiscal years 2008 and 2009 are reflective of the change in reporting entity that occurred as a result of the ownership transfer on July 1, 2007. Our consolidated financial statements reflect the financial statements of Birds Eye Holdings, Inc. for the periods prior to July 1, 2007. Fiscal year 2007 consisted of 53 weeks and fiscal years 2008 and 2009 consisted of 52 weeks.

The historical results presented below are not necessarily indicative of the results to be expected for any future period. This information should be read in conjunction with "Risk factors," "Use of proceeds," "Capitalization," "Selected consolidated financial data," "Management's discussion and analysis of financial condition and results of operations," and our financial statements and the related notes thereto are included elsewhere in this prospectus.

10

| |

Fiscal year ended | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| (in thousands, except share data) |

June 30, 2007 |

June 28, 2008 |

June 27, 2009 |

||||||||

Consolidated statement of income data: |

|||||||||||

Net sales |

$ | 782,714 | $ | 868,318 | $ | 935,644 | |||||

Cost of sales |

548,190 | 596,983 | 669,427 | ||||||||

Gross profit |

234,524 | 271,335 | 266,217 | ||||||||

Selling, administrative and general expense |

149,200 | 148,833 | 135,722 | ||||||||

Restructuring(1) |

399 | 690 | 1,169 | ||||||||

Other expense(2) |

1,379 | — | — | ||||||||

Operating income |

83,546 | 121,812 | 129,326 | ||||||||

Loss on early extinguishment of debt(3) |

2,272 | — | — | ||||||||

Interest expense |

25,680 | 63,100 | 50,001 | ||||||||

Pretax income from continuing operations |

55,594 | 58,712 | 79,325 | ||||||||

Tax provision |

22,410 | 21,491 | 26,220 | ||||||||

Income from continuing operations |

33,184 | 37,221 | 53,105 | ||||||||

Discontinued operations (loss)/gain, net of taxes(4) |

(42,080 | ) | 830 | 540 | |||||||

Net (loss)/income |

$ | (8,896 | ) | $ | 38,051 | $ | 53,645 | ||||

Income from continuing operations allocated to common stockholder(5) |

$ | 1,727 | $ | 37,221 | $ | 53,105 | |||||

Net (loss)/income allocated to common stockholder(5) |

$ | (40,353 | ) | $ | 38,051 | $ | 53,645 | ||||

Basic and diluted net (loss)/income per share(6) |

|||||||||||

Income from continuing operations |

|||||||||||

Discontinued operations, net of taxes |

|||||||||||

Net (loss)/income |

|||||||||||

Basic and diluted weighted average number of shares of common stock outstanding(6) |

|||||||||||

| |

|

June 27, 2009 | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| (in thousands) |

|

Actual |

As adjusted(7)(8) |

|||||||

Consolidated balance sheet data: |

||||||||||

Cash and cash equivalents |

$ | 65,005 | $ | |||||||

Working capital |

$ | 170,616 | $ | |||||||

Total assets |

$ | 673,597 | $ | |||||||

Total long-term debt |

$ | 703,216 | $ | |||||||

Stockholder's deficit |

$ | (243,805 | ) | $ | ||||||

11

| |

Fiscal year ended | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| (in thousands) |

June 30, 2007 |

June 28, 2008 |

June 27, 2009 |

||||||||

Other consolidated financial data: |

|||||||||||

Capital expenditures |

$ | 16,875 | $ | 21,610 | $ | 25,803 | |||||

Cash flow from operations |

60,144 | 91,214 | 48,024 | ||||||||

Cash flow from investing |

82,470 | (17,269 | ) | (24,928 | ) | ||||||

Cash flow from financing |

(210,582 | ) | (4,074 | ) | (33,890 | ) | |||||

Adjusted EBITDA(9) |

$ | 107,149 | $ | 140,126 | $ | 150,204 | |||||

Segment EBITDA(10) |

|||||||||||

Frozen food group |

$ | 57,680 | $ | 87,980 | $ | 93,639 | |||||

Specialty food group |

$ | 51,428 | $ | 54,155 | $ | 59,599 | |||||

Industrial-other |

$ | (1,959 | ) | $ | (2,009 | ) | $ | (3,034 | ) | ||

(1) In both fiscal years 2009 and 2007, we eliminated positions from various departments as part of our cost reduction efforts. In fiscal year 2008, a member of our senior management team departed and we recognized a charge related to this departure.

(2) We recognized a loss on the sale of an idle manufacturing facility and administrative office.

(3) On March 22, 2007, we amended and restated our credit agreement among Birds Eye Group, Inc., Birds Eye Holdings, Inc. and a syndicate of banks and other lenders arranged and managed by JPMorgan Chase Bank, N.A., which we refer to as the Opco Credit Facility, and used part of the proceeds to pay off existing outstanding term loans, in conjunction with this repayment, we recorded a charge to write off deferred financing fees. In addition, on November 20, 2006, we repurchased the remaining balance of our previously issued senior subordinated notes, and in conjunction with this we recognized a gain to write off the remaining unamortized premium.

(4) During fiscal year 2007, we completed the sale of our non-branded frozen vegetable business. See Note 3 to the "Notes to consolidated financial statements" for a complete discussion on the components of discontinued operations.

(5) The income from continuing operations allocated to our common stockholder and net loss allocated to our common stockholder for fiscal year 2007 is net of preferred dividends and accretion costs on preferred stock that was outstanding at that time. In fiscal year 2007, we refinanced our Opco Credit Facility. Proceeds from this refinancing were used to redeem all preferred stock that Birds Eye Holdings, Inc. had outstanding at that time.

(6) All shares and per share data amounts give effect to a for-one stock split to take place immediately prior to the completion of the offering.

(7) The as adjusted column in the balance sheet data table above reflects the balance sheet data as further adjusted for (a) our receipt of the estimated net proceeds from the sale of shares of common stock offered by us at an assumed initial public offering price of $ per share, the midpoint of the price range set forth on the cover of this prospectus, after deducting the estimated underwriting discount and estimated offering expenses payable by us and (b) the repayment of outstanding indebtedness as described in "Use of proceeds." See "Capitalization" and "Use of proceeds."

(8) A $1.00 increase (decrease) in the assumed initial public offering price of $ per share, the mid-point of the price range set forth on the cover of this prospectus, would increase (decrease) each of cash and cash equivalents, total assets and total stockholder's equity (deficit) by approximately $ million, assuming that the number of shares offered by us, as set forth on the cover of this prospectus, remains the same and after deducting the estimated underwriting discount and estimated offering expenses payable by us. Similarly, if we change the number of shares offered by us, the net proceeds we receive will increase or decrease by the increase or decrease in the number of shares sold, multiplied by the offering price per share, less the estimated underwriting discount and estimated offering expenses payable by us.

(9) EBITDA means net (loss)/income before interest expense, tax provision and depreciation and amortization. Segment EBITDA for the periods presented in footnote 10 below means EBITDA for one of our three reporting segments. Adjusted EBITDA for the periods presented above means EBITDA adjusted for the items described in the table below. These measures are not considered to be Generally Accepted Accounting Principles, which we refer to as GAAP, financial measures. Generally, a non-GAAP financial measure is a numerical measure of a company's performance, financial position or cash flows that either excludes or includes amounts that are not

12

normally included or excluded in the most directly comparable measure calculated and presented in accordance with GAAP. We believe that EBITDA, Segment EBITDA and Adjusted EBITDA provide investors with helpful information with respect to our operations and cash flows. EBITDA, Segment EBITDA and Adjusted EBITDA are measures used by our management, including our chief operating decision-maker, in evaluating the performance of our business, and are factors in measuring compliance with debt covenants relating to certain of our borrowing arrangements. We include them to provide additional information with respect to our ability to meet our future debt service, capital expenditures and working capital requirements. EBITDA, Segment EBITDA and Adjusted EBITDA as presented may not be comparable to similarly titled measures reported by other companies since not all companies necessarily calculate EBITDA, Segment EBITDA and Adusted EBITDA in an identical manner and, therefore, they are not necessarily an accurate measure of comparison between companies. The following table presents a reconciliation of net (loss)/income, the most directly comparable financial measure under GAAP to EBITDA and Adjusted EBITDA for the periods presented. See "Management's discussion and analysis of financial condition and results of operations—Results of operation—Non-GAAP financial measures."

| |

Fiscal year ended | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| (in thousands) |

June 30, 2007 |

June 28, 2008 |

June 27, 2009 |

||||||||

Net (loss)/income (GAAP measure) |

$ | (8,896 | ) | $ | 38,051 | $ | 53,645 | ||||

Interest expense |

25,680 | 63,100 | 50,001 | ||||||||

Tax provision |

22,410 | 21,491 | 26,220 | ||||||||

Depreciation and amortization |

18,978 | 17,624 | 18,409 | ||||||||

EBITDA (Non-GAAP measure) |

58,172 | 140,266 | 148,275 | ||||||||

Discontinued operations, net of taxes |

42,080 | (830 | ) | (540 | ) | ||||||

Restructuring(a) |

399 | 690 | 1,169 | ||||||||

Other expense(b) |

1,379 | — | 1,300 | ||||||||

Loss on early extinguishment of debt(c) |

2,272 | — | — | ||||||||

Transition costs(d) |

2,847 | — | — | ||||||||

Adjusted EBITDA (Non-GAAP measure) |

$ | 107,149 | $ | 140,126 | $ | 150,204 | |||||

(a) Restructuring is primarily comprised of employee termination costs.

(b) Other expense in fiscal year 2007 comprised a loss on disposal of our idle manufacturing and administrative office in Green Bay, Wisconsin. Other expense in fiscal year 2009 consisted of consulting fees incurred to assist with strategic evaluations.

(c) Loss on early extinguishment of debt in fiscal year 2007 represents the write-off of deferred financing costs related to the repayment of term loans net of gain related to the redemption of senior subordinated notes.

(d) Transition costs in fiscal year 2007 represents incremental expenses incurred in connection with the divestiture of our non-branded frozen vegetable business.

(10) The following table presents a reconciliation of Segment EBITDA to segment operating income, the most directly comparable financial measure under GAAP for each operating segment for the periods presented. We do not allocate interest expense, our tax provision or miscellaneous income or expense items, such as restructuring expense, other expense or loss on early extinguishment of debt, to Segment EBITDA.

| |

Frozen food group | Specialty food group | Industrial-other | ||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Fiscal year ended | ||||||||||||||||||||||||||||

| (in thousands) |

June 30, 2007 |

June 28, 2008 |

June 27, 2009 |

June 30, 2007 |

June 28, 2008 |

June 27, 2009 |

June 30, 2007 |

June 28, 2008 |

June 27, 2009 |

||||||||||||||||||||

Operating (loss)/income (GAAP measure) |

$ | 45,091 | $ | 76,689 | $ | 81,617 | $ | 45,471 | $ | 48,006 | $ | 53,411 | $ | (2,391 | ) | $ | (2,193 | ) | $ | (3,233 | ) | ||||||||

Depreciation and amortization |

12,589 | 11,291 | 12,022 | 5,957 | 6,149 | 6,188 | 432 | 184 | 199 | ||||||||||||||||||||

Segment EBITDA (Non-GAAP measure) |

$ | 57,680 | $ | 87,980 | $ | 93,639 | $ | 51,428 | $ | 54,155 | $ | 59,599 | $ | (1,959 | ) | $ | (2,009 | ) | $ | (3,034 | ) | ||||||||

13

An investment in our common stock involves a high degree of risk. You should consider carefully the risks described below, together with the financial and other information contained in this prospectus, before you decide to purchase shares of our common stock. If any of the following risks actually occurs, our business, financial condition, results of operations, cash flows and prospects could be materially and adversely affected. However, the selected risks described below are not the only risks facing us. Additional risks and uncertainties not currently known to us or those we currently view to be immaterial may also materially and adversely affect our business, financial condition, results of operations, cash flows and prospects. As a result, the trading price of our common stock could decline and you could lose all or part of your investment in our common stock.

Risks related to our business

We may experience liabilities or adverse effects on our reputation as a result of product recalls.

The sale of food products for human consumption entails an inherent risk of product liability and product recall and the resultant adverse publicity. Such liabilities and recalls may result from product contamination, spoilage or mishandling. This risk will be amplified in future periods as we extend our offerings to include more varieties of seafood. Pathogens, such as listeria, are generally found in the environment and consequently, there is a risk that they, as a result of food processing, could be present in our products. These risks may not be eliminated by adherence to good manufacturing practices and finished product testing. We may be subject to significant liability if the consumption of any of our products causes injury, illness or death. We could be required to recall certain of our products in the event of contamination, adverse test results or damage to the products, which could result in significant costs incurred as a result of any recall, including potential destruction of inventory and lost sales. In addition to the risks of product liability or product recall due to deficiencies caused by our operations, we may encounter the same risks if any third party tampers with our products. We may be required to undertake product recalls, and product liability claims may be asserted against us in the future. We have little, if any, control over proper handling procedures once our products have been shipped for distribution. Even if a product liability claim is unsuccessful or is not fully pursued, the negative publicity surrounding a significant product liability case or product recall could adversely affect the value of our brands and our reputation with existing and potential customers.

In addition, while we do not own the Birds Eye or Steamfresh trademarks in a number of foreign jurisdictions, the negative publicity surrounding product recalls and product liability claims with respect to the Birds Eye or Steamfresh names in these jurisdictions could nonetheless adversely affect our reputation and the value of our brand. See "—If we fail to protect our key brand names, infringe intellectual property rights of third parties or inadequately protect our intellectual property rights, our business could be harmed."

Our product liability insurance coverage may not adequately protect us from all of the liabilities and expenses that we may incur in connection with such events and we do not carry insurance coverage for product recalls. If we were to suffer a loss that is not adequately

14

covered by insurance, our results of operations and financial condition would be adversely affected.

The effects of strong competition in the food industry, including competitive pricing and marketing actions, could adversely affect our profitability and market share.

Our product categories are highly competitive with respect to price, product innovation, product quality, brand recognition and loyalty and the ability to identify and satisfy consumer preferences. Our competitors continue to introduce new products and brand extensions, particularly in the complete bagged meal segment. Our product lines are sensitive to competition from national and regional brands, and many of our product lines compete directly or indirectly with private label products and fresh alternatives. We cannot predict the pricing, product innovation or promotional actions of our competitors or whether those actions will have a negative effect on us.

This competitive environment subjects us to the risk of adverse impact to our financial performance if we are required to respond to pricing actions or increased brand investment by our competitors. Such competitive pressures may also limit our ability to increase prices, including in response to increased costs. Our financial performance will be adversely affected if our profit margins decrease, either as a result of a reduction in prices or increased costs, and we are unable to increase sales volume to offset margin decreases. These limitations may cause us to lose market share, which may require us to lower prices, increase our consumer marketing and/or increase trade promotions, each of which would adversely affect our financial performance.

In order to maintain or increase our current market share in this highly competitive environment, we expect to increase our consumer marketing, trade promotions and new product innovation. The success of our consumer marketing, trade promotions and new product innovation is subject to risks, including uncertainties about consumer and trade acceptance. As a result, we cannot guarantee that these higher levels of expenditures will maintain or enhance our market share and such increases in spending could result in lower levels of net sales and operating profitability.

If we fail to protect our key brand names, infringe intellectual property rights of third parties or inadequately protect our intellectual property rights, our business could be harmed.

We consider our key trademarks to be of significant importance to our business. We have obtained U.S. registrations for these marks, including Birds Eye and Steamfresh, and have the exclusive rights to use Voila! for our products pursuant to a perpetual, royalty free license. Our failure to successfully protect our trademarks could diminish the value and efficacy of our brand recognition, and could cause customer confusion, which could, in turn, adversely affect our net sales and profitability.

Although we have rights to the Birds Eye and Steamfresh trademarks in the United States and certain other jurisdictions, unaffiliated third parties own rights to the Birds Eye and Steamfresh trademarks in many other countries.

We cannot be certain that the conduct of our business does not and will not infringe the intellectual property rights of others, or that the intellectual property of third parties does not and will not infringe ours. Parties have filed, and in the future may file, claims against us alleging that we have infringed third party intellectual property rights. If we are held liable for

15

infringement, we could be required to pay damages or obtain licenses or to cease making or selling certain products. There can be no assurance that licenses will be available at all, or will be available on commercially reasonable terms, and the cost to defend these claims, whether or not meritorious, could be significant and could divert the attention of management.

We rely on the trademark, copyright and trade secret laws of the U.S. and other countries to protect our proprietary rights, but there can be no guarantee that these will adequately protect all of our rights, or that any of our intellectual property rights will not be challenged or held invalid or unenforceable in a dispute with third parties. If we are unable to enforce our intellectual property rights against third parties, our business, financial condition and results of operations may be adversely affected.

The loss of one or more of our significant customers may adversely affect our results of operations.

We have several large customers that account for a significant portion of our net sales. Our top ten customers accounted for approximately 64% of our net sales during fiscal year 2009, with our largest customer, Walmart, representing 25% of our fiscal year 2009 net sales and our second largest customer, C&S Wholesale Grocers, representing 8% of our fiscal year 2009 net sales. We do not have long-term contracts with our customers, and as a result, our customers could significantly decrease or cease their business with us with limited or no notice. Many retailers are aggressively managing their inventory levels downward and these initiatives will have negative impacts to net sales in the periods these actions are taken. Our results of operations could be adversely affected by the loss of one or more of our large customers or if net sales from one or more of these customers is significantly reduced.

The consolidation of retail customers may adversely impact our operating margins and profitability.

Our customers, such as supermarkets, warehouse clubs and food distributors, have consolidated in recent years and consolidation may continue. As a result of these consolidations, our large retail customers may seek lower pricing or increased trade promotions from their suppliers, including us. If we fail to respond to these trends in our industry, our volume growth could slow or we may need to lower prices or increase trade promotions and consumer marketing for our products, both of which would adversely affect our financial results. These retailers may use shelf space currently used for our products for their own private label products. In addition, retailers are increasingly carrying fewer brands in any one category and our results of operations will suffer if we are not selected by our significant customers to remain a vendor. In the event of consolidation involving our current retailers, we may lose key business if the surviving entities do not continue to purchase products from us.

We may be unable to anticipate changes in consumer preferences and buyer behavior as well as risks associated with new product introductions, which could adversely impact our profitability.

Our success is dependent in part on our ability to anticipate and react to changes in the tastes and eating habits of consumers and to offer new products or improve existing products to appeal to their preferences. Additionally, we must anticipate and react to changes in consumer buying behavior, including preferred shopping destinations, coupon usage, pack size and many other factors. There are inherent risks in the marketplace associated with new product or packaging introductions, including uncertainties about trade and consumer acceptance. We

16

may be required to increase consumer marketing to support new product development and increase trade promotions and other brand investments associated with the introduction of new products or line extensions into the marketplace. We may not be successful in developing new products or improving existing products, and our new products may not achieve consumer acceptance. Our failure to anticipate, identify or react quickly to these changes and trends, and to introduce new and improved products on a timely basis, could result in reduced demand for our products, which could adversely affect our operating results and profitability.

Changes in consumer preferences, including shifts to lower-priced alternatives as a result of the global economic crisis or otherwise, could adversely affect our business.

Retailers are increasingly offering their own private label products that compete as a cheaper alternative to our branded products. The willingness of consumers to purchase our branded products depends in part on the perception that our branded products are of higher quality than less expensive alternatives. If the difference in quality between our branded products and store brands narrows, or if there is a perception of such a narrowing, consumers may choose not to buy our branded products. Furthermore, in periods of economic uncertainty like we are currently experiencing, consumer spending shifts towards cheaper alternatives, such as private label products or other economy brands. As consumers have recently become more value conscious, we have seen a shift in consumer purchases from our premium frozen vegetables offerings to our more value-oriented offerings. Both of these trends may result in a reduction in the volume of sales of our higher margin products or a shift in our product mix to lower margin offerings.

Trends within the food industry change often and failure to identify and react to changes in the trends could lead to, among other things, reduced demand and price reductions for our products. Competitive pressures and changes in consumer preferences could cause us to lose market share or decrease our margins, both of which would adversely affect our operating results.

Fluctuations in the cost and availability of supply chain elements could increase operating costs and lower profitability.

We source raw materials, including fruits, vegetables, proteins and seafood, as well as packaging material and other materials to manufacture products. We may experience shortages in these items or increases in the costs of such items as a result of market fluctuations, weather conditions or other unforeseen circumstances. We do not have long-term contracts with fixed pricing for many of our purchased materials, but instead primarily rely on negotiating contracts on an annual basis. Due to fluctuations in commodity prices, such contracts may not be favorably priced compared to prior periods. Also, since we contract for certain raw vegetables on specified acreage, we have in the past and may in the future be required to purchase raw materials on the spot market if the vegetable production on the acreage contracted for is not adequate. We do not engage in hedging activities with respect to our purchased fruits and vegetables commodities. Rising fuel and energy costs may also have a significant impact on our cost of operations, including the manufacture, transport, and distribution of products. We have engaged in a swap agreement relating to diesel fuel. See "Management discussion and analysis of financial condition and results of operations—Quantitative and qualitative disclosures about market risk—Commodity price risk." Fuel costs may fluctuate due to a number of factors outside of our control, including market fluctuations, governmental policy and regulation and weather conditions. For example, commodity and input cost inflation in fiscal year 2009

17

contributed to a decrease in our gross margin percentage of 280 basis points as compared to fiscal year 2008. U.S. governmental policies relating to farm and ethanol policies may directly or indirectly influence the competing demand for corn for use in the manufacture of ethanol, which may affect the number of corn acres planted, corn prices or the level of corn inventories. Our results of operations would be adversely affected by a decrease in the supply of corn or an increase in the price of corn.

Changes in the prices of our products may lag behind changes in the costs of our materials. Competitive pressures also may limit our ability to raise prices in response to increased raw materials, packaging and fuel costs. Accordingly, if we are unable to increase our prices to offset increased costs, our financial performance would be adversely affected.

We are subject to transportation risks.

An extended interruption in our ability to ship our products would have a material adverse effect on our business, financial condition and results of operations. Similarly, any extended disruption in the distribution of our products would have a material adverse effect on our business, financial condition and results of operations. While we believe we are adequately insured and would attempt to transport our products by alternative means if we were to experience an interruption due to strikes, natural disasters or otherwise, we cannot be sure that we would be able to do so or be successful in doing so in a timely and cost-effective manner.

Labor strikes or work stoppages by our employees could harm our business.

As of September 2009 we had a total of approximately 1,700 full-time, or non-seasonal employees. Most of our full-time distribution, production and maintenance employees are covered by collective bargaining agreements. Labor organizing activities could result in additional employees becoming unionized. We have several collective bargaining or other labor agreements covering a total of approximately 1,025 employees. We have 3 agreements expiring in fiscal year 2010 covering approximately 505 employees, including one agreement covering approximately 305 employees that expires on December 31, 2009. We are planning on renewing this agreement. We cannot assure you that we will be able to negotiate these or other collective bargaining agreements on the same or more favorable terms as the current agreements, or at all, and without production interruptions, including labor stoppages. Failure to renew existing agreements or a prolonged labor dispute, including but not limited to a work stoppage, could adversely affect our business operations and financial performance.

Any significant deterioration of employee relations, increase in labor costs, slowdowns or work stoppages, or shortages of labor at any of our locations, whether due to union activities, employee turnover or otherwise, could have a material adverse effect on our business, financial condition and results of operations. See "Business—Employees."

Our operations are subject to numerous laws and regulations. Non-compliance with these laws and regulations, or the enactment of more stringent laws or regulations, could adversely affect our business.

Food production and marketing are highly regulated by a variety of federal, state, local and foreign agencies, and new regulations and changes to existing regulations are issued regularly. New laws and regulations or changes in the existing laws and regulations could increase our costs of doing business and adversely affect our profitability. As we enter new lines of business,

18

we may be subject to additional laws or regulations that could increase the cost of doing business. In addition, because we advertise many of our products, we could be the target of claims relating to false or deceptive advertising under federal, state and foreign laws and regulations.

Our operations are also subject to various federal, state and local environmental, health, safety and other laws and regulations. Environmental, health and safety laws and regulations are subject to amendment, to the imposition of new or additional requirements and to changing interpretations by governmental agencies and courts. We cannot assure you that we will always operate in compliance with environmental requirements, and if we fail to comply with such requirements, we could incur material penalties, fines and damages and negative publicity. As an owner and operator of real property, we can be found jointly and severally liable under such laws for costs associated with investigating, removing and remediating hazardous or toxic substances that may exist on, in or about such real property. Such liability can be imposed without regard to whether the owner or operator had knowledge of, or was actually responsible for causing, the conditions being addressed. Further, it is possible that we could be found liable regarding properties we formerly owned or operated or regarding properties at which wastes we generated were disposed of. In addition, it is possible that we may face claims alleging harmful exposure to, or property damage resulting from, the release of hazardous or toxic substances at or from our locations or otherwise related to our business. We do not carry insurance coverage for environmental liabilities. Environmental conditions relating to any former, current or future locations could adversely impact our business and results of operations.

Our inability to achieve efficiency in production could adversely impact operating costs.

Many of our costs, such as those for raw materials, energy and freight, are outside of our control. Therefore, our future success and profitability depends in part on our ability to be efficient in the production and manufacturing of our products. A failure to lower costs through productivity gains could weaken our competitive position. Further, if the productivity or cost saving initiatives that we have implemented or any future productivity or cost savings initiatives do not generate the expected cost savings and synergies, our results of operations may be adversely affected.

Our substantial debt could adversely affect our ability to raise additional capital to fund our operations, limit our ability to pursue our growth strategy and to react to changes in the economy or our industry.

Our debt includes the Opco Credit Facility, which is comprised of a $450 million senior secured B term loan, which we refer to as the Term Loan Facility, and a $125 million senior secured revolving credit facility, which we refer to as the Revolving Credit Facility, of which $16 million in letters of credit were outstanding as of June 27, 2009. The outstanding principal amount of the Term Loan Facility at June 27, 2009 was $381 million. Our debt also includes the Birds Eye Credit Facility, which is comprised of a $310 million term loan with an outstanding principal balance at June 27, 2009 of $323 million. Our significant level of consolidated debt could:

- •

- limit our ability to obtain additional financing to operate our business;

- •

- require us to dedicate a substantial portion of our cash flow to payments on our debt, thereby reducing our ability to use our cash flow to fund working capital, capital expenditures and other general capital requirements;

19

- •

- limit our flexibility to plan for and react to changes in our business and the industry in which we operate;

- •

- place us at a competitive disadvantage relative to some of our competitors that have less debt than us;

and

- •

- increase our vulnerability to general adverse economic and industry conditions, including changes in interest rates, or a downturn in our business or the economy.

Our senior credit facilities contain various covenants that may restrict our financial and operating flexibility.

The Birds Eye Credit Facility and Opco Credit Facility contain various covenants that limit our ability to engage in specified types of transactions. These covenants limit our and our subsidiaries' ability to, among other things:

- •

- incur additional indebtedness or issue certain preferred stock;

- •

- create certain liens or encumbrances;

- •

- enter into transactions with affiliates;

- •

- merge or consolidate with other entities;

- •

- sell assets;

- •

- enter into sale-leaseback transactions; or

- •

- make certain distributions, investments and other restricted payments.

A default under the Birds Eye Credit Facility or the Opco Credit Facility may result in a cross-default to the other credit facility even if the underlying event or condition would not or did not result in a default under such other credit facility, or such default was waived. A breach of a covenant or restriction contained in these agreements could result in a default that could in turn permit the affected lender to accelerate the repayment of principal and accrued interest on our outstanding loans and terminate their commitments to lend additional funds. If the lenders under such indebtedness accelerate the repayment of our borrowings, we cannot assure you that we will have sufficient assets to repay those borrowings as well as other indebtedness.

After this offering, under the Birds Eye Credit Facility and the Opco Credit Facility, if a party other than Vestar beneficially owns (1) capital stock with voting power greater than that of Vestar or (2) 35% or more of the total voting power of our capital stock, the lenders under each agreement may require us to repay all outstanding amounts under such agreement and, in the case of the Birds Eye Credit Facility, a prepayment premium. In addition, under the Birds Eye Credit Facility, the lenders have the right to require us to apply the net proceeds we receive from any public offering to repay the outstanding principal indebtedness under the facility plus any accrued but unpaid interest. The lenders under the Birds Eye Credit Facility may require us to apply the net proceeds we receive from any future equity offerings to repay any indebtedness outstanding at that time.

For the Opco Credit Facility, we have pledged a significant portion of our assets as collateral. If we are unable to repay those amounts, the lenders under the Opco Credit Facility could proceed against the collateral granted to them to secure the indebtedness. Our ability to comply with the covenants in these credit facilities can be affected by events beyond our control, including the other risks described herein, and we cannot assure you that we will meet these covenants or, in the event of default, we cannot be assured that waivers, amendments or

20

alternative or additional financings could be obtained, or if obtained, would be on terms acceptable to us.

Some of our debt has variable rates of interest, which could result in higher interest expense in the event of an increase in interest rates.

As of June 27, 2009, approximately $475 million of our loans under the Birds Eye Credit Facility and Opco Credit Facility were subject to variable interest rates. In addition, if we borrow additional amounts under the revolving portion of the Opco Credit Facility, the interest rates on those borrowings may vary depending on the base rate or Eurodollar Rate (LIBOR), and other debt we incur also could be variable-rate debt. If market interest rates rise, any debt subject to variable interest rates will create higher debt service requirements, which could adversely affect our cash flow. While we have and may in the future enter into agreements limiting our exposure to higher interest rates, any such agreements may not offer complete protection from this risk. We and our subsidiaries may be able to incur substantial indebtedness in the future, subject to the restrictions contained in the Birds Eye Credit Facility and the Opco Credit Facility. If new indebtedness is added to our current debt levels, the related risks that we now face could intensify.

We may not be able to successfully integrate growth opportunities or consummate divestitures.

Periodically, we evaluate growth opportunities that would strategically fit within our business portfolio. Future acquisitions by us could result in:

- •

- dilutive issuances of equity securities;

- •

- reductions in our operating results;

- •

- incurrence of debt and contingent liabilities;

- •

- future impairment of goodwill and other intangibles; and

- •

- other acquisition-related expenses.

Our failure to successfully integrate or grow these acquired entities into our business could adversely affect our reputation and have an adverse effect on our financial performance.

In addition, we may, periodically, divest businesses that no longer strategically fit within our business portfolio, and our profitability may be impacted by gains or losses on such sales, or lost operating income from those businesses. Furthermore, we may be unable to divest businesses that are not core businesses or may not be able to do so on terms that are favorable to us. In addition, we may be required to incur asset impairment charges related to acquired or divested businesses which may lower our profitability. Acquisition and divestiture activities present financial, managerial and operational challenges, including diversion of management attention from existing businesses, difficulty with integrating or separating personnel and financial and other systems, increased expenses, indemnities and potential disputes with the buyers and sellers.

Impairment in the carrying value of goodwill or other intangibles could negatively impact our net worth.

As of June 27, 2009, we carried approximately $53.3 million of goodwill and $211.2 million of trademark and other intangible assets on our balance sheet. The carrying value of goodwill represents the fair value of acquired businesses in excess of identifiable assets and liabilities as of the acquisition date. The carrying value of other intangibles represents the fair value of

21

trademarks, trade names, and other acquired intangibles. Goodwill and other acquired intangibles that are expected to contribute indefinitely to our cash flows are not amortized, but must be evaluated by management at least annually for impairment. Impairments to goodwill may be caused by factors outside our control, such as increasing competitive pricing pressures or the bankruptcy of a significant customer and could negatively impact our net worth.

If we lose key personnel or are unable to recruit qualified personnel, our ability to implement our business strategies could be delayed or hindered.

Our success depends, in part, upon the efforts of certain of our executive officers and other key personnel. We rely substantially upon the services of our senior management team. The loss of the services of these key personnel could prevent us from fully implementing our business strategies and materially adversely affect our business, financial condition and results of operations. Other than our Chairman and Chief Executive Officer, we do not have employment contracts with any other member of senior management and each member of our senior management team could end their employment at any time. See "Executive compensation—Employment agreements and termination and change in control benefits."

As we grow, we will need to recruit and retain qualified management personnel, but we may not be able to do so. Our ability to recruit and retain such personnel will depend upon a number of factors, such as our results of operations, prospects and the level of competition then prevailing in the market for qualified personnel. Failure to recruit and retain such personnel could materially adversely affect our business, financial condition and results of operations.

We may experience losses or be subject to increased funding and expenses to our qualified pension plan, which could negatively impact profits.

We maintain a qualified defined benefit plan. Although we have frozen benefits under the plan for all employees, we remain obligated to ensure that the plan is funded in accordance with applicable regulations. Our pension plan is currently underfunded by approximately $40 million below the total benefit obligation of the plan as of June 27, 2009. In the event the stock market deteriorates, the funds in which we have invested do not perform according to expectations, or the valuation of the projected benefit obligation increases due to changes in interest rates or other factors, we may be required to make significant cash contributions to the pension plan and recognize increased expense within our financial statements. If our cash flow from operations is insufficient to fund our pension liability, we may be forced to reduce or delay capital expenditures or seek additional capital to service our pension liabilities.

Natural disasters, unusually adverse weather conditions, pandemic outbreaks, boycotts and geo-political events could adversely affect our financial performance.

The occurrence of one or more natural disasters, such as hurricanes and earthquakes, unusually adverse weather conditions, such as floods or droughts, pandemic outbreaks, boycotts and geo-political events, such as civil unrest in countries in which our raw materials are located and acts of terrorism, or similar disruptions could adversely affect the supply and cost of raw materials and our operations. These events could result in increases in fuel (or other energy) prices or a fuel shortage, the temporary or permanent closure of one or more of our customers' stores or one or more of our manufacturing facilities, the temporary lack of an adequate work force in a market, the temporary or long-term disruption in the supply of raw

22

materials, the temporary disruption in the transport of our products to customers and disruption to our information systems. To the extent these events result in physical damage or disruption to our manufacturing or distribution capabilities or our information processing capabilities, our operations could be materially adversely affected. These events and factors can otherwise disrupt and adversely affect our operations and financial performance.

Risks related to this offering and ownership of our common stock

Concentration of ownership among our principal stockholders may prevent new investors from influencing significant corporate decisions.

We are controlled, and after this offering is completed will continue to be controlled by Vestar. Vestar will own, in the aggregate, approximately % of the voting interest in Holdings, and Holdings will own % of our outstanding common stock after the consummation of this offering (or % if the underwriters exercise their option to purchase additional shares in full). Vestar will have the ability through its interest in Holdings to elect our entire board of directors. As a result, Vestar, which has a voting majority of all outstanding Holdings common units, will be able to exercise control over all matters requiring stockholder approval, including the election of directors, amendment of our amended and restated certificate of incorporation and approval of significant corporate transactions, and will have significant control over our management and policies. The interests of this stockholder may not be consistent with your interests as a stockholder.